Dental Laboratory Handpieces Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

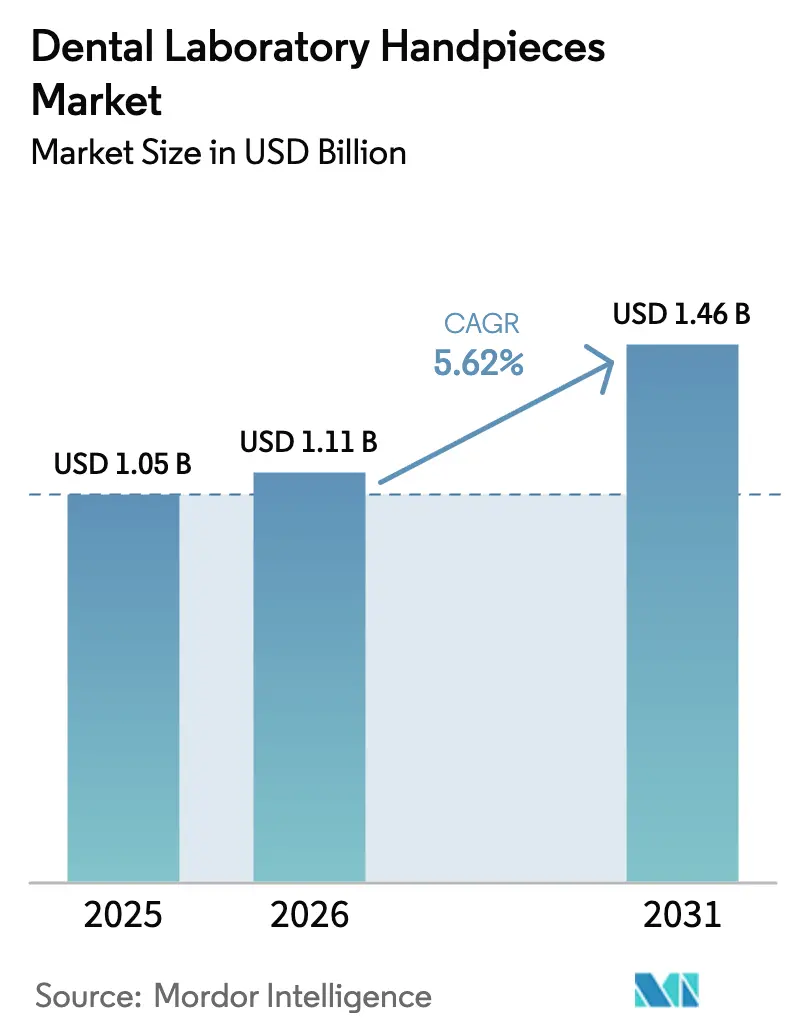

| Market Size (2026) | USD 1.11 Billion |

| Market Size (2031) | USD 1.46 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

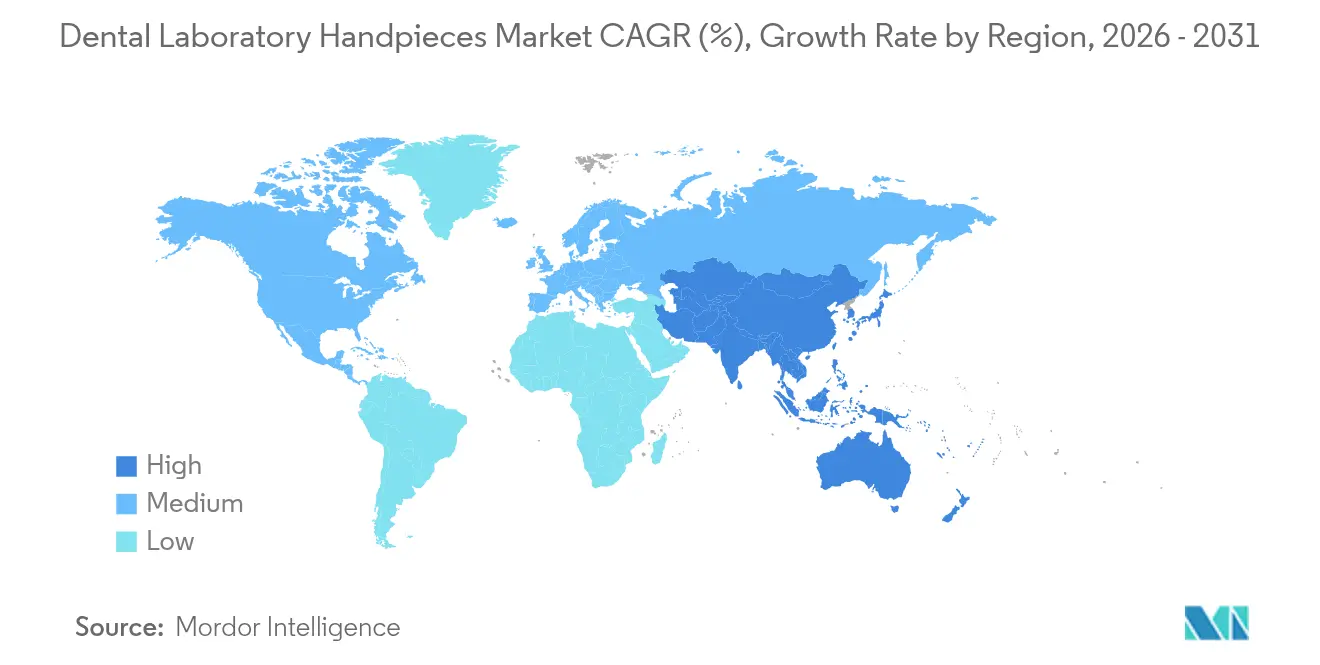

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Laboratory Handpieces Market Analysis by Mordor Intelligence

The dental laboratory handpieces market size was valued at USD 1.05 billion in 2025 and estimated to grow from USD 1.11 billion in 2026 to reach USD 1.46 billion by 2031, at a CAGR of 5.62% during the forecast period (2026-2031). Sustained demand stems from laboratories replacing legacy air-driven tools with precision electric alternatives that provide stable torque, quieter operation and compliance with stricter ergonomic rules. Widespread adoption of CAD/CAM workflows is accelerating upgrades because high-density zirconia, titanium and hybrid ceramics require repeatable high-torque cutting. Ageing but dentate populations, especially in North America and Europe, are keeping restorative case volumes high, while WHO-led oral-health programmes are broadening access to laboratory services in emerging economies. Supply-chain pressure on micromotor components raises near-term cost headwinds, yet manufacturers are countering through design modularity and localised assembly that shorten lead times.

Key Report Takeaways

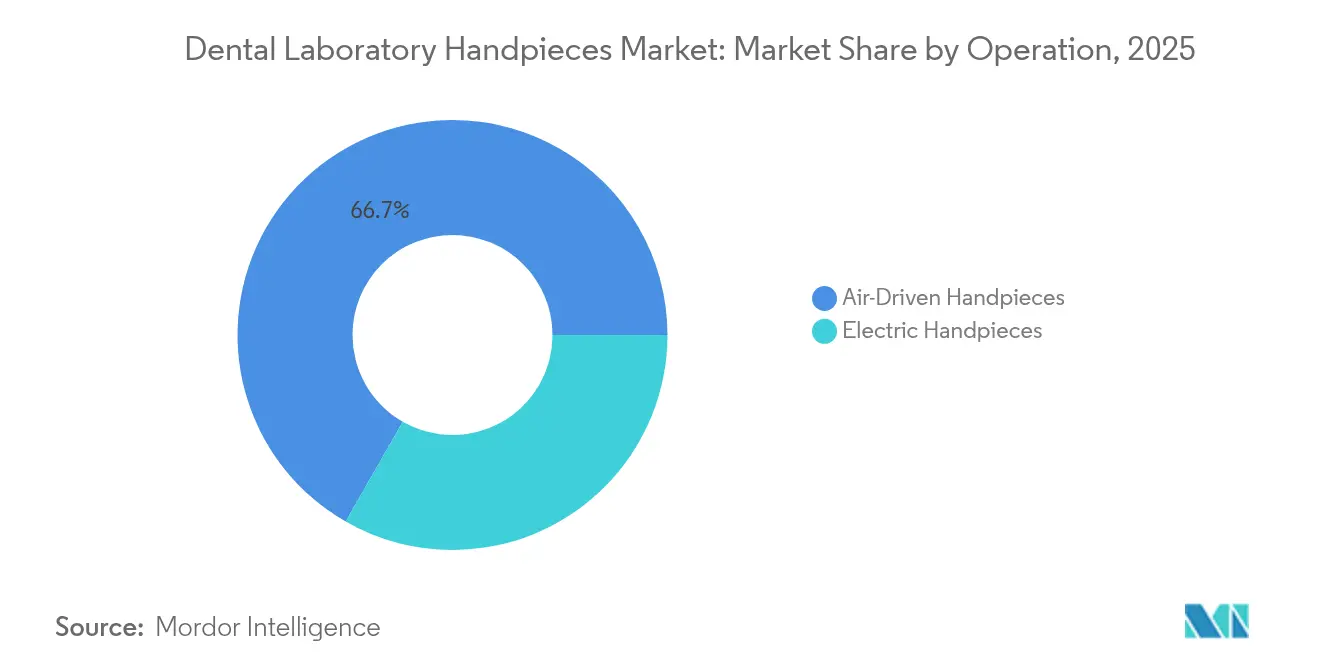

- By operation, air-driven units retained 66.72% of dental laboratory handpieces market share in 2025, whereas electric systems are on track for the quickest ascent at 7.50% CAGR to 2031.

- By speed type, high-speed devices captured 62.85% of dental laboratory handpieces market size in 2025; low-speed units are projected to expand at 6.74% CAGR between 2026-2031.

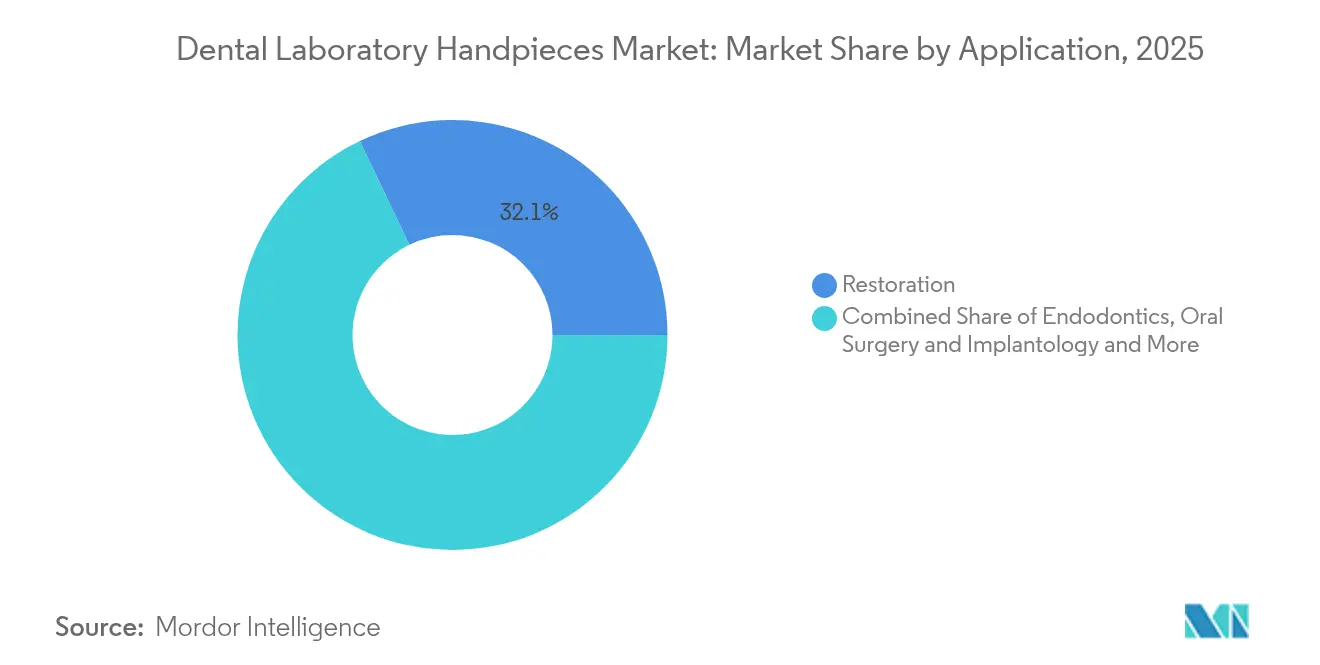

- By application, restoration work accounted for 32.10% share of the dental laboratory handpieces market size in 2025 and oral surgery & implantology is advancing at a 7.72% CAGR through 2031.

- By end user, dental clinics held 48.36% revenue share in 2025, while dental laboratories register the fastest 7.44% CAGR due to consolidation-driven equipment standardisation.

- By geography, North America commanded 38.71% of the dental laboratory handpieces market share in 2025; Asia-Pacific is expected to post the highest 8.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Laboratory Handpieces Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of dental caries and periodontal diseases | +1.2% | Global; highest in Asia-Pacific & Africa | Long term (≥ 4 years) |

| Growing geriatric population demanding restorative care | +1.0% | North America & Europe, extending to Asia-Pacific | Medium term (2-4 years) |

| Rapid shift from air-driven to electric lab handpieces | +0.8% | Global; led by North America & Europe | Short term (≤ 2 years) |

| Digital dentistry (CAD/CAM) boosting high-torque lab tools | +0.7% | North America & Europe; emerging Asia-Pacific | Medium term (2-4 years) |

| Dental-tourism hubs upgrading laboratory infrastructure | +0.5% | Asia-Pacific, Middle East, South America | Short term (≤ 2 years) |

| Stricter infection-control standards favouring autoclavable designs | +0.4% | Global; strongest in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Caries & Periodontal Diseases

Roughly 3.5 billion people live with untreated oral conditions that now cost health systems more than USD 700 billion annually. Severe periodontitis alone affects 951.3 million working-age adults, pushing laboratories to process higher restorative workloads that necessitate advanced, high-torque handpieces. The disease burden is shifting toward low-income settings where infrastructure investments are ramping, thereby multiplying equipment orders. Laboratories in mature markets also feel the strain because clinicians prioritise minimally invasive dentistry that relies on precision finishing rather than extraction-driven workflows. Rising complexity, coupled with stricter cross-infection rules, means handpieces must integrate sealed bearings and be fully autoclavable without degrading performance.

Growing Geriatric Population Demanding Restorative Care

One in four Americans will be older than 65 by 2034, yet tooth retention rates have climbed, creating restorative workloads that were unheard of a decade ago. Older patients commonly present with comorbidities, so equipment must meet heightened infection-control thresholds and minimise vibration to protect fragile dentition. Longer chairtime associated with complex prosthetics fuels demand for ergonomic, low-noise handpieces that cut fatigue for both patient and technician. Laboratories in Asia-Pacific are preparing for a similar demographic wave, prompting early adoption of electric micromotor systems in urban centres.

Rapid Shift from Air-Driven to Electric Lab Handpieces

Electric models sustain constant torque from 20,000-200,000 rpm, whereas air-driven tools lose power under load, especially when milling zirconia or cobalt-chrome frameworks[1]Aegis Dental Network Staff, “Power to the Handpiece,” aegisdentalnetwork.com. The performance delta shortens turnaround times, which is crucial for same-day prosthetics and chairside milling. Noise and vibration reductions improve occupational health, aligning with OSHA standards and the EU Physical Agents Directive that caps hand-arm vibration exposure. Manufacturers now offer fully sealed brushless systems with predictive maintenance software to alert technicians before gear wear compromises accuracy.

Digital Dentistry (CAD/CAM) Boosting High-Torque Lab Tools

CAD/CAM adoption demands repeatable micron-level cuts through hybrid ceramics and multilayer zirconia. Conventional air turbines struggle to keep pace, nudging laboratories toward electric handpieces that integrate with milling units and 3D-printing post-processing lines[2]FDI World Dental Federation, “CAD/CAM Dentistry,” fdiworlddental.org. Multifunctional designs now embed LED lighting, irrigation ports and sensor feedback to support closed-loop machining. Recent patents highlight convergence: a 2021 filing allows the same handpiece to deliver photodynamic therapy alongside high-speed cutting, pointing to multifunction lab stations in the near future.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance cost of advanced systems | -0.9% | Global; highest in low- & middle-income economies | Medium term (2-4 years) |

| Limited oral-care spending in low-income economies | -0.7% | Africa, parts of Asia-Pacific, South America | Long term (≥ 4 years) |

| Supply-chain bottlenecks for precision micro-motors | -0.5% | Global; manufacturing concentrated in Asia | Short term (≤ 2 years) |

| Emerging ergonomic & noise regulations increasing redesign cost | -0.3% | Europe, North America; expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Cost of Advanced Systems

Electric handpiece packages routinely exceed USD 4,000, nearly quadruple a mid-range air turbine, and scheduled motor rebuilds can equal 50% of purchase price over five years. Budget-constrained labs delay upgrades, stretching instrument life beyond optimal safety windows. Specialised training and calibration tools add indirect expenses that weigh heavily on single-chair clinics in developing regions. Accelerated innovation also shortens depreciation cycles, causing owners to hesitate before committing capital.

Limited Oral-Care Spending in Low-Income Economies

Many governments allocate less than 1% of healthcare budgets to dentistry, meaning households pay directly for treatment. Studies from Tanzania and similar markets reveal root-canal fees equal up to 10 days’ disposable income, effectively sidelining elective prosthetic work. Without patient demand, laboratories defer equipment investment, perpetuating a cycle of outdated technology and lower care quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operation: Electric Systems Challenge Air-Driven Dominance

Air-driven units retained 66.72% of dental laboratory handpieces market share in 2025 because legacy compressors remain plentiful and technicians are familiar with their maintenance routines. Yet electric variants are rising swiftly at 7.50% CAGR as laboratories pursue constant torque for precision zirconia milling. Brushless motors extend service life, while sealed gearboxes reduce aerosolised lubricant contamination. The dental laboratory handpieces market now sees bundled electric packages that integrate RPM feedback into CAD/CAM platforms, allowing automatic parameter adjustment when material density shifts. Laboratories focused on high-end implant frameworks cite a 15% reduction in remakes after switching to electric systems, validating the technology premium. Price parity is narrowing as large-scale procurement and local assembly bring costs down, reinforcing the adoption curve.

Electric adoption is also supported by government subsidies for energy-efficient equipment because electric systems consume less compressed air. Manufacturers highlight Total Cost of Ownership calculators showing breakeven within three years when factoring lower service downtime. Consequently, the dental laboratory handpieces market records higher resale values for electric units, improving asset liquidity for clinics planning future upgrades.

By Speed Type: High-Speed Dominance Amid Low-Speed Innovation

High-speed turbines commanded 62.85% of dental laboratory handpieces market size in 2025 owing to unmatched bulk-cutting efficiency required for initial crown reduction. They spin at up to 420,000 rpm, shaving minutes off each case and maximising laboratory throughput. Meanwhile, low-speed devices are advancing at 6.74% CAGR because finishing, polishing and endodontic shaping need more tactile control. Recent low-speed models feature quick-release heads and 4:1 gear ratios that preserve torque while trimming RPM to 20,000 for delicate work.

An increasing share of CAD/CAM post-processing relies on low-speed polishing to refine marginal integrity without micro-cracking ceramic edges. Infection-control updates mandate heat sterilisation for both speed categories, pushing demand for corrosion-resistant internal water lines. Manufacturers answered with titanium-sleeved rotors and autoclavable LED couplers, lengthening lifespan across speed types.

By Application: Restoration Leadership Faces Surgical Growth

Restorative cases generated 32.10% revenue in 2025, underpinning daily laboratory workflows such as crown and bridge manufacture. Volume remains high because population-level sugar consumption keeps caries incidence steady, while durable composite materials raise patient expectations for aesthetic outcomes. Oral surgery and implantology, however, are outpacing all categories with 7.72% CAGR as implants displace removable dentures among ageing yet active adults. The dental laboratory handpieces market benefits because implant drilling and abutment adjustment require vibration-free, high-torque tools.

Endodontics demands slender, torque-sensing handpieces that navigate complex canal systems, and manufacturers now provide apex-locator integration for real-time feedback. Orthodontic appliance fabrication adds specialist needs such as narrow-body polishers for aligner edge trimming, creating micro-niche opportunities for differentiated product lines.

By End User: Clinics Lead While Laboratories Accelerate

Dental clinics delivered 48.36% of 2025 revenue because they handle chairside adjustments that require versatile, multi-purpose handpieces. However, laboratory-centric buyers are registering the highest 7.44% CAGR as consolidation moves production into centralised hubs seeking industrial-grade equipment standards. Bulk purchasing allows lab chains to negotiate extended warranties and auto-calibration add-ons, accelerating electric penetration.

Hospitals continue procuring specialty tools for maxillofacial units, while academic centres adopt smart handpieces with data-logging for student feedback. These educational purchases influence long-term preferences because graduates often bring those brand loyalties into private practice, indirectly shaping future demand within the dental laboratory handpieces market.

Geography Analysis

North America contributed 38.71% of dental laboratory handpieces market size in 2025 due to reimbursement frameworks and stringent CDC sterilisation standards that shorten replacement cycles. A 10% tariff on imported equipment imposed in 2025 elevated landed prices, nudging clinics toward US-assembled devices and encouraging OEMs to expand domestic output capacity. Ageing populations retaining natural dentition sustain complex restorative workloads, keeping utilisation rates high.

Asia-Pacific is the fastest-growing region at 8.22% CAGR, fuelled by urban middle-class expansion and government programmes that integrate oral health into universal coverage. China reports dental disease prevalence above 90%, yet dentist density lags OECD peers, spurring investment in high-throughput laboratories. Manufacturers like Dentis established a Vietnam subsidiary in 2025 to shorten delivery times and adapt products to local price points.

Europe posts steady growth as the EU vibration directive elevates demand for ergonomic handpieces. Laboratories upgrade to compliant models with on-board damping sleeves that cut vibration exposure by 40%, aligning with occupational health mandates. Meanwhile, South America, the Middle East and Africa represent long-tail opportunities. Infrastructure upgrades tied to WHO 2023-2030 Oral Health Action Plan unlock multilateral funding, though limited insurance coverage slows high-end equipment uptake.

Competitive Landscape

The dental laboratory handpieces market is moderately fragmented, with Dentsply Sirona, KaVo Dental, NSK and Bien-Air Dental leading on innovation. Each brand invests in torque-sensing algorithms and sealed ceramic bearings to outpace rivals on lifespan metrics.

Strategic alliances shape distribution. KaVo and A-dec linked delivery units with electric motors in 2025, giving clinics turnkey packages that streamline installation. Dentsply Sirona partnered with Alexandria University to seed next-generation training labs, cultivating brand adoption among future clinicians. Component bottlenecks prompted moves toward dual-sourcing rare-earth magnets, and some firms consider vertical integration into micromotor production to safeguard supply.

Emerging Asian manufacturers supply cost-optimised electric systems that target developing markets at 30% below Western pricing. Established players respond with mid-tier lines featuring modular couplings and refurbishable gearboxes, extending product lifespan while protecting market share. Competitive intensity now hinges on total ecosystem integration, including software that logs sterilisation cycles and predicts bearing wear, crucial for compliance audits.

Dental Laboratory Handpieces Industry Leaders

Dentsply Sirona

KaVo Dental

Bien-Air Dental SA

W&H Dentalwerk GmbH

NSK / Nakanishi Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Dentis Co., Ltd. opened a subsidiary in Ho Chi Minh City to build a Southeast Asian distribution network and plans further expansion into Thailand, Japan and Poland.

- February 2025: Planmeca and KaVo Dental North America inaugurated a shared headquarters that consolidates training, service and logistics for their combined product portfolios.

Global Dental Laboratory Handpieces Market Report Scope

Dental laboratory handpieces are one of the most critical and essential parts of dental practice for performing various procedures, including surgeries, implantology, aesthetics, endodontics, and restoration. Endodontic handpieces are specialist dental implements used to clean and shape canals during root canal treatments. In most circumstances, these tools can accurately drive endodontic files. The implant handpieces were formulated with oral and maxillofacial surgery in mind. They are incredibly durable as they are manufactured with high-quality stainless steel with a unique coating.

The dental laboratory handpiece market is segmented into operation, speed type, application, end-user, and geography. The market is segmented by operation into air-driven handpieces and electric handpieces. The market is bifurcated by speed type into high speed dental handpieces and low speed dental handpieces. By application, the market is divided into endodontics, oral surgery & implantology, restoration, and others. By end user, the market is segmented into hospitals, dental clinics, dental laboratories, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report also offers the market size and forecasts for 17 countries across the region. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| Air-Driven Handpieces |

| Electric Handpieces |

| High-Speed Handpieces |

| Low-Speed Handpieces |

| Endodontics |

| Oral Surgery & Implantology |

| Restoration |

| Orthodontics & Research |

| Hospitals |

| Dental Clinics |

| Dental Laboratories |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Operation | Air-Driven Handpieces | |

| Electric Handpieces | ||

| By Speed Type | High-Speed Handpieces | |

| Low-Speed Handpieces | ||

| By Application | Endodontics | |

| Oral Surgery & Implantology | ||

| Restoration | ||

| Orthodontics & Research | ||

| By End User | Hospitals | |

| Dental Clinics | ||

| Dental Laboratories | ||

| Academic & Research Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the dental laboratory handpieces market in 2026?

The dental laboratory handpieces market size reached USD 1.11 billion in 2026 and is projected to rise steadily through 2031.

Which region grows fastest for dental laboratory handpieces?

Asia-Pacific leads growth with an expected 8.22% CAGR to 2031, spurred by healthcare modernisation and dental-tourism investment.

What segment holds the largest share by speed type?

High-speed handpieces claimed 62.85% of dental laboratory handpieces market share in 2025 due to their efficiency in bulk material removal.

Why are electric handpieces gaining popularity?

Electric units deliver constant torque, reduced vibration and noise, and full sterilisation compatibility, aligning with modern CAD/CAM and ergonomic needs.

Which driver most strongly influences future demand?

Rising global prevalence of dental caries and periodontal diseases adds an estimated +1.2% to forecast CAGR, ensuring continuous demand for restorative equipment.

Page last updated on: