Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

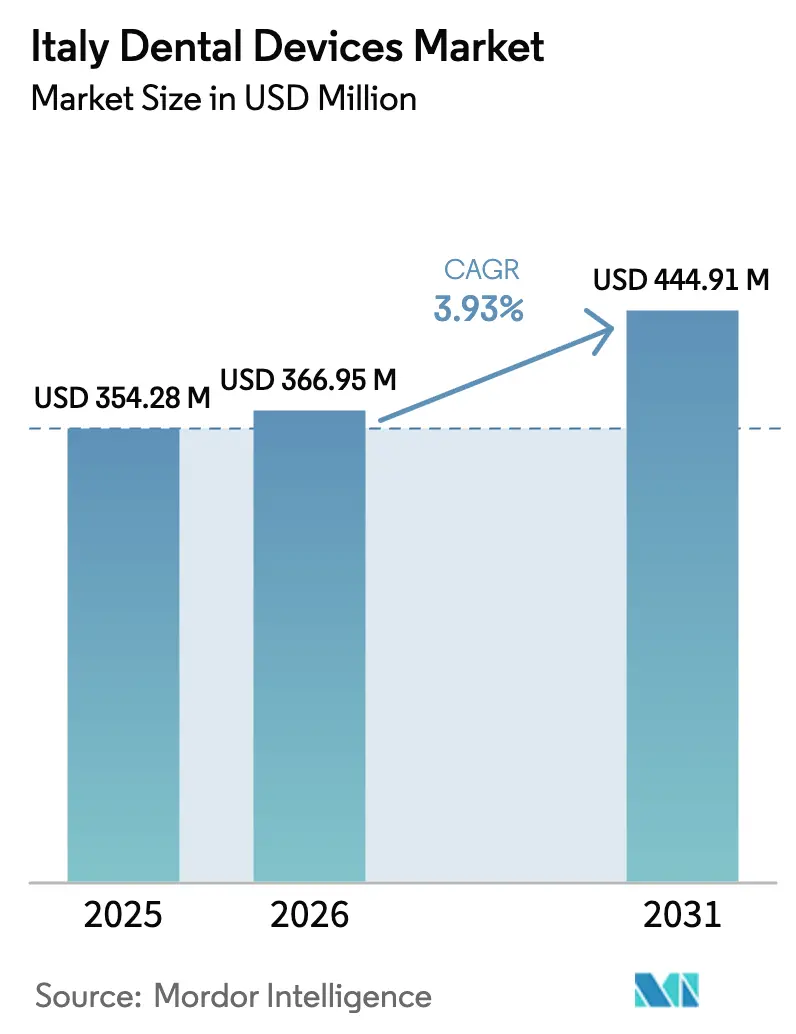

| Base Year Market Size (2025) | USD 354.28 Million |

| Market Size (2026) | USD 366.95 Million |

| Market Size (2031) | USD 444.91 Million |

| Growth Rate (2026 - 2031) | 3.93% CAGR |

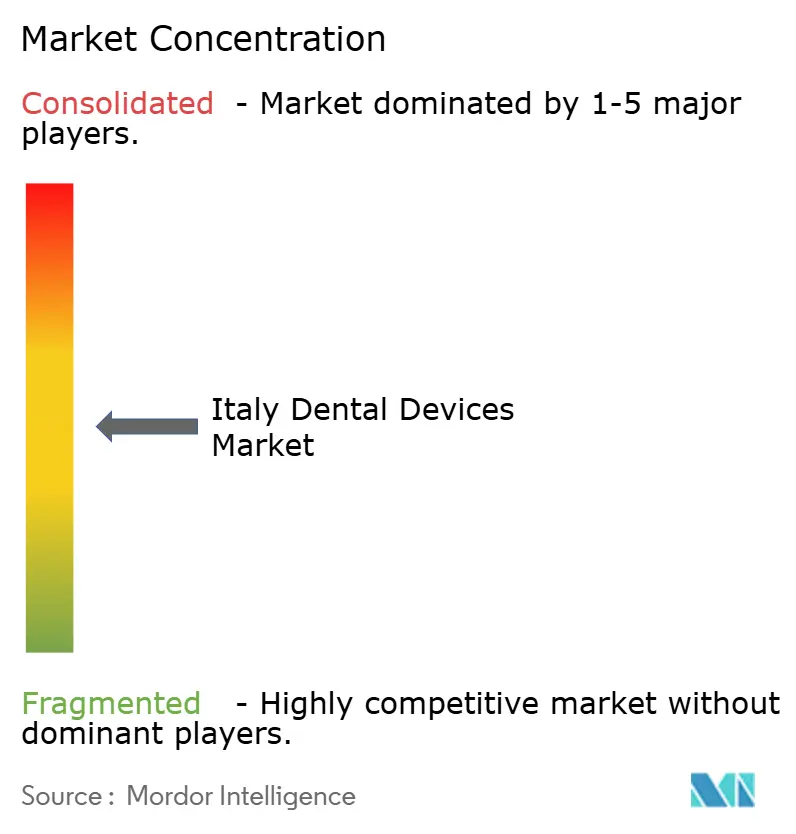

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Dental Devices Market Analysis by Mordor Intelligence

The Italy Dental Devices Market size is expected to increase from USD 354.28 million in 2025 to USD 366.95 million in 2026 and reach USD 444.91 million by 2031, growing at a CAGR of 3.93% over 2026-2031.

Steady topline growth masks an ongoing shift from volume-based consumables to digital capital equipment as practices modernize their workflows. Demand is underpinned by rapid population aging, with the 65-plus cohort projected to approach 34.5% by 2050, intensifying the need for implants, crowns, and full-arch restorations. Constrained National Health Service coverage leaves most oral care spending out of pocket, pushing private clinics to invest in productivity-enhancing imaging and CAD/CAM systems. Government Industry 4.0 tax credits, which reimburse up to 40% of qualifying digital purchases, further accelerate equipment adoption. Moderate vendor concentration and rising software subscription models are reshaping competitive dynamics, while supply-chain fragility around zirconia and a tightening labor pool are applying cost pressure.

Key Report Takeaways

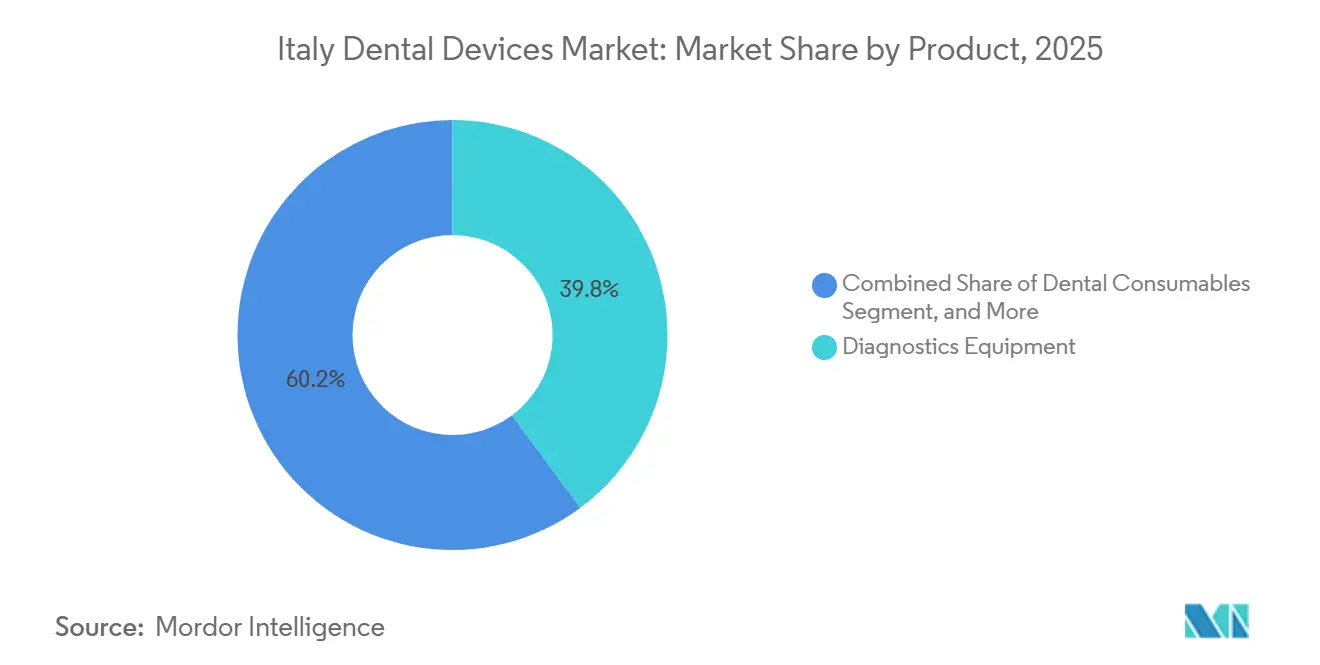

- By product, diagnostics equipment held 39.84% of 2025 revenue, whereas Dental consumables are projected to grow fastest at a 4.53% CAGR through 2031.

- By treatment, orthodontics led with a 31.56% share in 2025, while Prosthodontics is forecast to grow at a 5.76% CAGR through 2031.

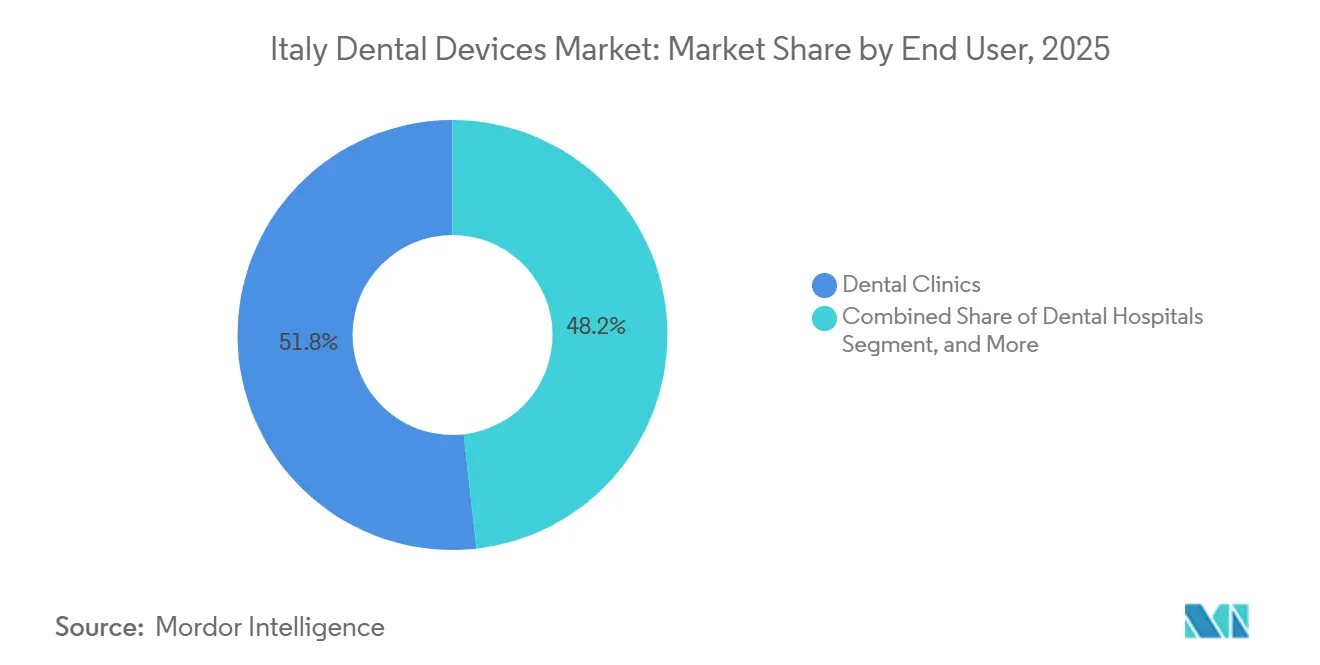

- By end user, dental clinics accounted for 51.78% of spending in 2025 and represent the fastest-growing channel, expanding 6.75% per year through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Dental Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Dental Caries and Periodontal Diseases | +0.8% | National, higher burden in Southern Italy | Medium term (2-4 years) |

| Aging Population Driving Demand for Restorative Dentistry | +1.2% | National, concentrated in Northern & Central regions | Long term (≥4 years) |

| Growing Adoption of Digital Dentistry & CAD/CAM Systems | +0.9% | National, led by urban private clinics | Medium term (2-4 years) |

| Inbound Dental Tourism to Specialised Clinics | +0.3% | Milan, Bologna, Rome | Short term (≤2 years) |

| Government Industry 4.0 Tax Credits for Dental 3-D Printing | +0.4% | Lombardy, Veneto | Short term (≤2 years) |

| Subscription-Based Aligner Therapy via Tele-dentistry | +0.3% | Urban centers with digital infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Caries and Periodontal Diseases

Caries-free prevalence among 12-year-olds stands at only 30.45%, and 13.1% of adults suffer severe periodontitis, both rates climbing in Southern regions. Each diagnosis triggers demand for intraoral radiography, laser detection, and ultrasonic scalers, helping Diagnostics Equipment dominate 2025 revenue. ISO 13485 compliance keeps procurement focused on established multinationals.

Aging Population Driving Demand for Restorative Dentistry

The elderly share of Italy’s population will rise to 34.5% by 2050, lifting demand for implants supported by CBCT imaging and zirconia prosthetics.[1]Istituto Nazionale di Statistica, “Demographic Projections for Italy,” ISTAT, istat.it Photogrammetry-based digitization delivers sub-50 µm accuracy, reducing fit errors and peri-implant complications. As a result, prosthodontic procedures post the fastest CAGR at 5.76%.

Growing Adoption of Digital Dentistry & CAD/CAM Systems

Italian practices have installed more than 6,500 intraoral scanners since COVID-19, achieving a penetration rate of greater than 40%. Dentsply Sirona’s Primescan 2 integrates AI margin detection, cutting chairside design time by 20%. Industry 4.0 incentives can trim the effective cost of a EUR 50,000 mill to EUR 30,000, accelerating uptake.[2]Ministry of Economic Development, “Industry 4.0 Tax Credit Program,” mise.gov.it

Inbound Dental Tourism to Specialised Italian Clinics

Although outbound flows are higher, inbound tourists seek high-end implantology priced at EUR 15,000–30,000 per case. These clinics fuel demand for CBCT, navigation systems, and 3-D-printed meshes, adding 0.3 percentage points to the CAGR of the Italian dental devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Advanced Dental Equipment | -0.6% | National, acute in Southern & rural areas | Short term (≤2 years) |

| Shortage of Skilled Dental Technicians | -0.4% | National, higher in South | Medium term (2-4 years) |

| Regional Reimbursement Fragmentation for Implants | -0.3% | North-South divide | Long term (≥4 years) |

| Volatile Zirconia Supply under EU Critical-Raw-Material Rules | -0.2% | National, impacts labs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Dental Equipment

Digital systems range from EUR 20,000 scanners to EUR 100,000 integrated suites, equivalent to 20% of single-chair annual revenue.[3]European Commission, “Critical Raw Materials Act,” ec.europa.eu Recurring software fees and training reduce margins, especially in the South, where scanner penetration is only 28%.

Shortage of Skilled Dental Technicians

Italy graduates fewer than 6 dentists per 100,000 residents, and technician programs enroll even fewer, resulting in lab turnaround times of 10-14 days. Vertical integration by vendors such as Straumann compresses independent-lab opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Gain Share as Digital Workflows Mature

Diagnostic equipment accounted for 39.84% of 2025 revenue, reflecting a sizable installed base of CBCT and panoramic units required for implant planning. Dental Consumables are projected to grow 4.53% annually as analog impression materials give way to scan bodies, zirconia blanks, and biocompatible resins. Guided-surgery templates fabricated via stereolithography consistently hold entry-point deviations below 1 mm, boosting implant predictability.

The Italian dental devices market, attributed to diagnostic equipment, is forecast to retain leadership through 2031, while consumables narrow the gap thanks to higher unit turnover. Compliance with EU Medical Device Regulation increases post-market obligations, consolidating share among ISO-certified suppliers.

By Treatment: Prosthodontics Accelerates on Aging Demographics

Orthodontics commanded a 31.56% share in 2025, buoyed by clear-aligner uptake that now covers more than 60% of new orthodontic cases. Nonetheless, prosthodontic interventions will register the highest CAGR at 5.76%, driven by demographic aging and diffusion of guided-surgery protocols. Photogrammetry delivers trueness under 50 µm, enabling passive-fit full-arch restorations with greater than 95% ten-year survival.

Consequently, prosthodontics’ share of the Italy dental devices market size is projected to climb steadily, reinforcing downstream demand for CBCT scanners and zirconia consumables. Orthodontic growth will gradually temper as aligner penetration approaches saturation in urban centers.

By End User: Private Clinics Dominate Amid Public-Coverage Gaps

Dental clinics accounted for 51.78% of 2025 expenditure and will expand by 6.75% annually, outpacing hospitals and academia. Limited NHS coverage means 77% of dental spending is private, motivating clinicians to differentiate via technology.

Private facilities thus represent the core customer base for premium imaging and CAD/CAM solutions in the Italian dental devices market, whereas hospitals remain focused on complex maxillofacial care, and academic institutes rely on grant-funded purchases.

Geography Analysis

Northern regions such as Lombardy, Veneto, and Emilia-Romagna spend more than EUR 200 per capita on oral care, boast >50% scanner penetration, and house dense private-clinic networks. Southern regions average spend of less than EUR 120 and less than 30% scanner adoption, perpetuating a two-tier Italy dental devices market. Industry 4.0 incentives are more heavily drawn in the North, where clinics possess the liquidity to pre-finance eligible hardware.

Tele(oral)medicine, supported by EUR 1 billion in NRRP funding, aims to narrow gaps, yet broadband and digital literacy bottlenecks slow Southern uptake. Uniform MDR rules apply nationwide, but inspection intensity varies; Northern authorities conduct more frequent audits, resulting in higher device-quality compliance.

Italy’s domestic manufacturing base, represented by over 100 UNIDI-member companies generating EUR 1.3 billion in turnover in 2021, reduces logistics costs and provides rapid service support, giving it a competitive edge against Asian imports. The Italian dental devices market, therefore, benefits from being a significant end market and from serving as a European production hub.

Regulatory Landscape

Italy regulates dental devices under the EU Medical Device Regulation (EU) 2017/745, with the Ministry of Health acting as the national Competent Authority through the national implementing framework, including Legislative Decree No. 137/2022. During the transition to full EUDAMED functionality, manufacturers and other economic operators must register devices in Italy's national medical device database (BD/RDM, Repertorio dei Dispositivi Medici), which remains a practical anchor for market access and traceability workflows.

Regulatory controls are tightening around classification and post-market oversight. From January 1, 2026, the Italian Classification of Medical Devices (CID) replaces the legacy CND classification, requiring updates to coding, registration, and internal master data used for submissions and supply-chain documentation. In November 2025, the Council of Ministers approved a bill to establish a National Single Registry for Implantable Medical Devices, which raises expectations for implant traceability and monitoring and has implications for implant and prosthodontic device suppliers, as well as their Italian distribution networks.

Competitive Landscape

Multinationals Dentsply Sirona, Straumann Group, Solventum, Envista, and Henry Schein account for a significant share of diagnostics and therapeutic equipment sales, reflecting moderate concentration in the Italian dental devices market. Their strategies hinge on technology differentiation: Primescan 2’s AI margin detection shortens same-day crown workflows by 20%, while Straumann’s Abutment Direct acquisition slashes custom-abutment turnaround to 48 hours.

Value-oriented Italian manufacturers compete on price and local service, particularly in the South, where capital budgets are tight. Equipment-as-a-service leasing, still nascent, could lower adoption barriers by 40–50% and disrupt upfront-sale models.

Regulatory complexity also shapes competition: ISO 13485 certification and MDR post-market surveillance favor incumbents with established compliance systems. Meanwhile, direct-to-consumer aligner firms and AI diagnostic software begin to siphon procedure volume from traditional channels, pressuring mid-tier vendors.

Italy Dental Devices Industry Leaders

Carestream Health Inc.

GC Corporation

Dentsply Sirona

Envista Holdings (Nobel Biocare Services AG)

3M

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is opening at the intersection of digital dentistry and software-driven compliance. With more than 6,500 intraoral scanners installed in Italy and scanner penetration above 40% (but materially lower in parts of Southern Italy), clinics and labs can monetize the installed base through connected CAD/CAM, workflow automation, and interoperability upgrades, rather than relying only on new hardware purchases. Industry 4.0 tax credits, which reimburse up to 40% of qualifying digital purchases, support investment cases for chairside and lab digitization, especially where clinics can pre-finance eligible equipment, while the shift toward subscription software models creates room for vendors that can bundle imaging, design, and practice-management integrations.

A second opportunity set is clinical software under regulatory scrutiny, including AI-enabled diagnostics and decision support. Under EU MDR, leading dental AI diagnostic tools have been positioned as Class IIa medical devices, and AI modules are being incorporated into major dental management software used in Italy (including OrisLine from Henry Schein, as well as Dentaloffice and Tueor Cube), expanding demand beyond imaging hardware into recurring software adoption by private clinics. Meanwhile, devices that incorporate medicinal substances with ancillary action (Class III under MDR) require a scientific opinion from AIFA within the conformity assessment pathway, supporting suppliers that can manage combination-product documentation and provide end-to-end compliance support for Italian implantology and restorative workflows.

Recent Industry Developments

- July 2026: Dentsply Sirona rolled out a major update to its SureSmile software platform focused on improving clinical workflow and the practitioner user experience. The release reinforces the role of software ecosystems in orthodontic case management and increases switching costs for clinics standardized on a single digital platform.

- June 2026: Dentsply Sirona shifted MIS implant and prosthetic solutions in Italy to a direct distribution model, effective June 1, 2026. This change increases control over local go-to-market execution for implant portfolios and can reshape channel economics for distributors and competing implant vendors.

- May 2026: Dentsply Sirona launched Smart View Detect, an AI-enabled diagnostic tool for CBCT scans in Europe, available from May 12, 2026. Adding AI-assisted interpretation to the imaging workflow supports premium positioning for diagnostics equipment and expands opportunities to attach software subscriptions to installed CBCT bases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of dental devices used in Italy for examining, diagnosing, treating, restoring, and removing teeth, along with related oral structures, as purchased by dental care settings and other end users.

Scope exclusions: services and purely cosmetic, non-medical retail products sold outside professional dental care settings are excluded from this sizing.

Segmentation Overview

- By Product

- Diagnostics Equipment

- Dental Laser

- Radiology Equipment

- Dental Chair & Equipment

- Therapeutic Equipment

- Dental Consumables

- Other Dental Equipments

- Diagnostics Equipment

- By Treatment

- Orthodontic

- Endodontic

- Periodontic

- Prosthodontic

- By End User

- Dental Hospitals

- Dental Clinics

- Academic & Research Institutes

- Other End Users

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to anchor the model to real Italy signals and keep assumptions consistent across product groups. We leaned on public sources such as the Italian National Institute of Statistics for demographic and health-spend context, Eurostat for macro indicators, and OECD health datasets for dentist density and care access indicators that influence procedure volumes.

To keep device demand tied to the supply chain, we also reviewed Italian and EU trade statistics (imports and exports) and association publications from Italian dental industry bodies. We then checked peer-reviewed clinical journals to understand treatment mix shifts (for example, aligner adoption and implant utilization). Company annual reports, investor presentations, and reputable press were used to sanity-check pricing and product availability, and a paid subscription for company financials and news helped us cross-check revenue exposure and local footprint. These examples are not exhaustive, and other sources were also used to collect data, validate assumptions, and clarify open points during research.

Primary Interviews and Surveys

Primary discussions were used to confirm what the desk signals could not fully explain, especially around the split between consumables and equipment, typical replacement cycles, and the practical price bands paid by clinics. We spoke with a mix of manufacturers, distributors, dental clinic owners, procurement heads, and lab-linked stakeholders across Italy so adoption patterns and channel markups could be checked, then applied consistently in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | |

| Mid tier: 53% | Functional/Unit leaders: 41% | |

| Smaller Players: 16% | Managers: 45% |

Market-Sizing & Forecasting

Sizing was built using both top-down and bottom-up logic so the total stays traceable to real-world activity. On the top-down side, we reconstructed a demand pool using Italy dental care utilization signals and treatment mix, then translated it into device consumption using typical device-per-procedure and replacement relationships that were validated in interviews.

For Italy, a few market fingerprints drive most of the variation, and we used them as model inputs: dentist and clinic density, procedure mix across orthodontics, endodontics, periodontics, and prosthodontics, the cadence of chairside and imaging equipment replacement, and the installed-base effect that supports steady consumables demand. Pricing was handled through observed Italy price ranges and expected ASP progression, then checked against channel behavior so margins do not inflate totals unrealistically. We also ran selective bottom-up approximations, including sampled supplier and distributor revenue mapping and volume-times-ASP checks by key product buckets. Where a segment had limited public visibility, we filled gaps with conservative penetration assumptions.

For forecasting, we relied on scenario analysis tied to the drivers above, so growth is not based on a single CAGR assumption. The scenarios were stress-tested with expert feedback on factors such as consumer dental spend sensitivity, public and private care mix, and technology uptake. The final forecast path was selected as the most repeatable with the available evidence.

Data Validation & Update Cycle

Validation was done in steps so a single data point could not sway the estimate. We triangulated totals against independent signals, including trade flows, procedure and provider indicators, and implied equipment replacement demand, then ran variance checks to flag outliers in pricing, growth rates, and segment splits.

Before sign-off, the model is reviewed by another analyst, and anomalies trigger a re-check of assumptions and, when needed, re-contact with primary sources to confirm what changed and why. Reports are refreshed annually, with interim updates when there is a material shift in policy, reimbursement, supply constraints, or technology adoption. Right before delivery, a fresh review pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Italy Dental Devices Market Size Versus Other Published Estimates

Published numbers for Italy dental devices do not always match because the boundaries of what gets counted can change from one study to another. In this space, the biggest swings usually come from whether the estimate is limited to dental devices used in clinical care, or whether it also folds in adjacent dental supply spending and broader retail-style categories.

Evidence such as Italy domestic dental industry sell-out signals, trade flow direction, and the implied replacement cycle for capital equipment are the checks that keep Mordor Intelligence's estimate tied to a clinical dental device demand pool, rather than a wider dental consumption total. Differences also come from pricing methods, where some estimates apply a single uplift to all categories, and from update timing, where older FX assumptions or aggressive post-COVID rebound curves can raise the base year level.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 354.28 M (2025) | |

| Global Consultancy A | USD 1.18 B (2024) | Uses an expanded scope labeled equipment and consumables, which can pull in a wider spend set than clinical dental devices alone, and it applies a higher growth curve over 2025-2030 that changes the base level expectations. |

| Industry Association B | USD 2.00 B (2025) | Reports a domestic sell-out market for the broader dental industry, where distribution markups and a wider basket can be embedded, which makes the total structurally larger than a devices-only count. |

Across the three figures, the spread is mainly explained by scope and pricing boundaries, not arithmetic differences. When the model is anchored to clinical usage signals and replacement behavior, the total is easier to reconcile with observable Italy activity and to update consistently year to year.

Key Questions Answered in the Report

How big is the Italy dental devices market in 2026?

The Italy dental devices market size is estimated at USD 0.37 billion for 2026.

Which segment grows fastest through 2031?

Prosthodontic treatments lead with a 5.76% CAGR, driven by implant demand from an aging population.

Why do private clinics dominate procurement?

Limited public reimbursement leaves 77% of spending out-of-pocket, giving private clinics both the incentive and autonomy to invest in advanced equipment.

What role do Industry 4.0 tax credits play?

They reimburse up to 40% of eligible digital hardware costs, effectively lowering scanner and milling-unit prices and hastening adoption.

Which regions invest most in digital dentistry?

Northern regions such as Lombardy and Veneto show >50% scanner penetration and per-capita dental spending above EUR 200.

Page last updated on: