Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

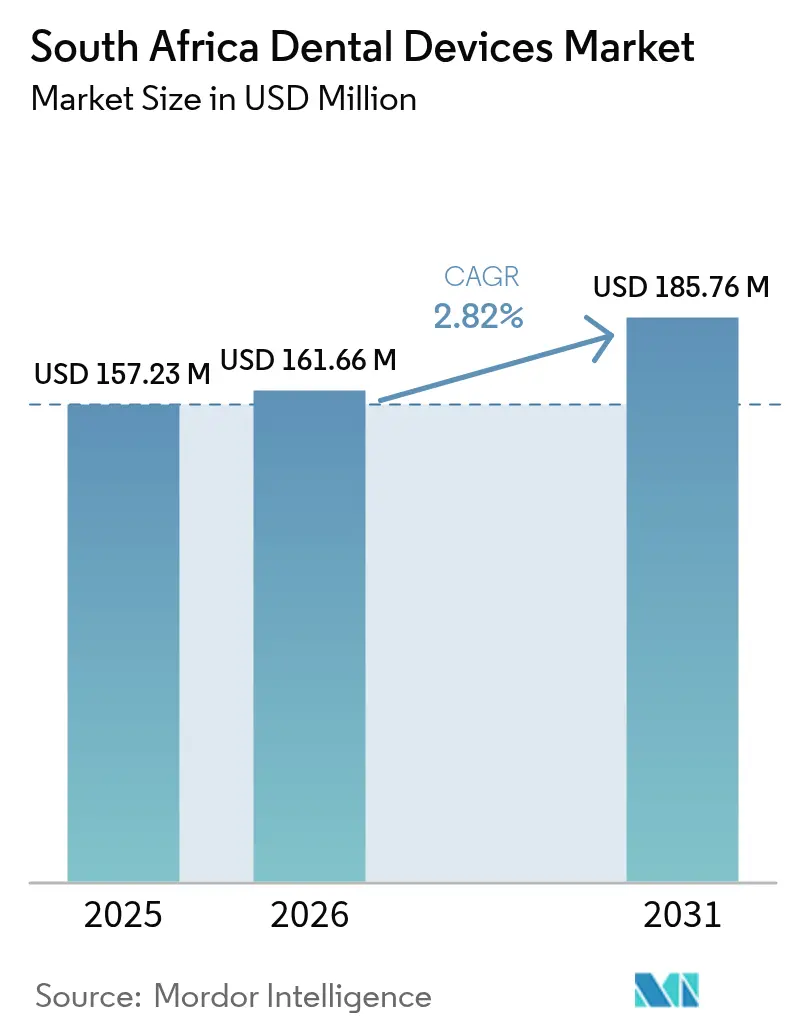

| Base Year Market Size (2025) | USD 157.23 Million |

| Market Size (2026) | USD 161.66 Million |

| Market Size (2031) | USD 185.76 Million |

| Growth Rate (2026 - 2031) | 2.82% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Dental Devices Market Analysis by Mordor Intelligence

The South Africa dental devices market size is expected to grow from USD 157.23 million in 2025 to USD 161.66 million in 2026 and is forecast to reach USD 185.76 million by 2031 at 2.82% CAGR over 2026-2031. Modest headline growth masks pronounced shifts in product mix, end-user preferences, and technology adoption. Dental consumables continue to underpin revenues because they support every treatment protocol and generate dependable cash flow for practices. At the same time, chair-side CAD/CAM systems and other digital workflow tools are expanding quickly in urban clinics as a hedge against laboratory delays and load-shedding interruptions. Corporate dental-chain consolidation is adding purchasing power and standardized protocols, while medical-tourism demand from neighboring SADC countries is boosting high-value implant volumes. Finally, persistent power outages and a chronic shortage of technicians and hygienists temper overall growth, forcing practices to favor equipment with built-in power-backup options and streamlined staffing requirements.

Key Report Takeaways

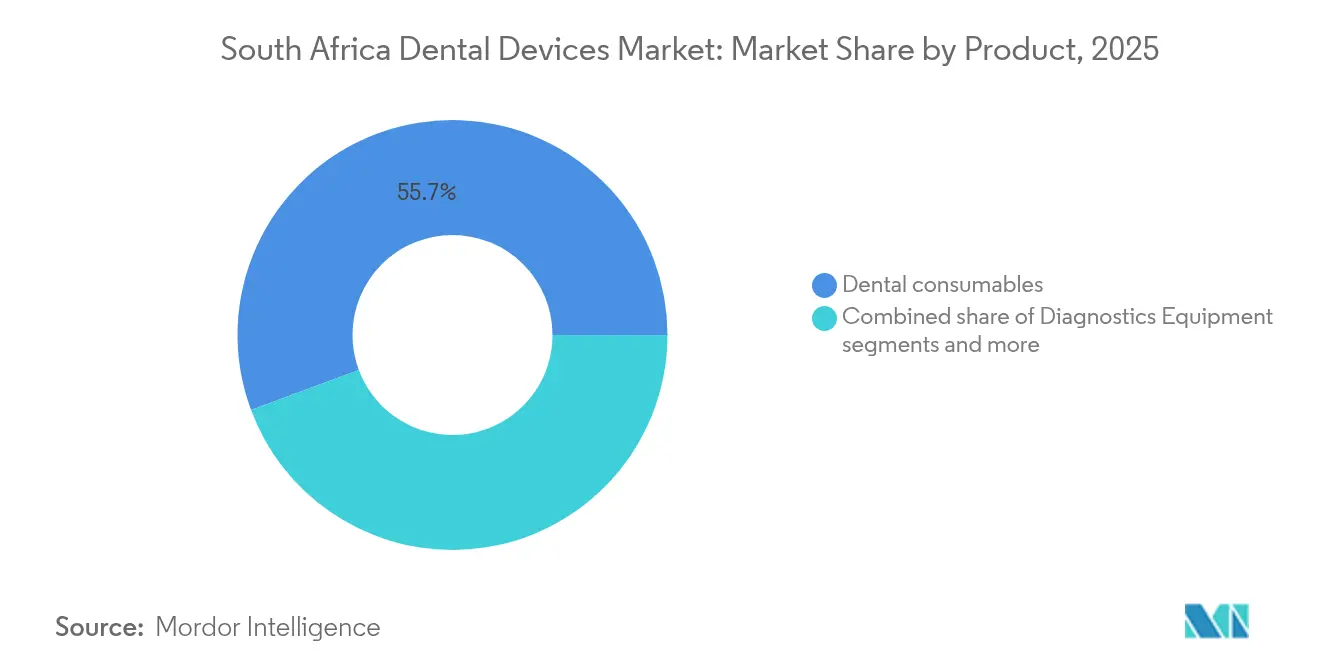

- By product type, dental consumables led with 55.68% of South Africa dental devices market share in 2025; dental equipment is projected to expand at a 3.12% CAGR through 2031.

- By treatment, prosthodontic procedures accounted for 33.12% of the South Africa dental devices market size in 2025, while orthodontics records the highest projected CAGR at 3.86% between 2026 and 2031.

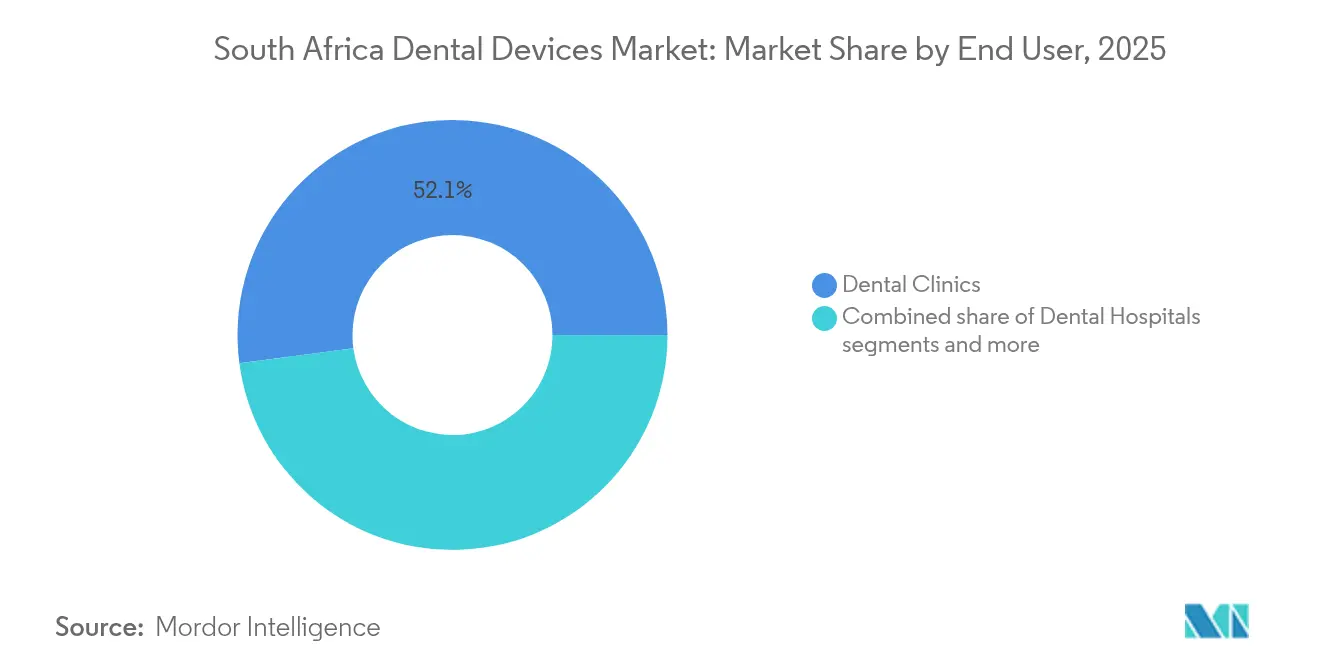

- By end user, dental clinics captured 52.10% revenue share in 2025 and are advancing at a 3.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Dental Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Cosmetic & Aesthetic Dentistry in Gauteng & Western Cape | +0.7% | Gauteng and Western Cape provinces | Medium term (2-4 years) |

| Government-Backed Oral-Health Screening Programs Targeting Low-Income Communities | +0.5% | National, with focus on rural and underserved areas | Long term (≥ 4 years) |

| Emergence of Chair-side CAD/CAM Systems in Urban Clinics | +0.6% | Urban centers (Johannesburg, Cape Town, Durban) | Short term (≤ 2 years) |

| Growing Medical-Tourism Flow from SADC Neighbours for Implant Procedures | +0.4% | Border regions and major cities | Medium term (2-4 years) |

| Rapid Expansion of Corporate Dental-Chain Networks (e.g., Intercare, Medicross) | +0.5% | National, with concentration in urban centers | Medium term (2-4 years) |

| Uptake of Digital Impressions to Shorten Lab Turn-Around Time | +0.4% | Urban centers with established dental laboratories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Cosmetic & Aesthetic Dentistry

The premium segment for elective smile makeovers is maturing quickly in Johannesburg, Cape Town, and Durban as middle-income households channel discretionary spending toward appearance-enhancing care. Digital smile-design software and minimally invasive veneer systems have become status symbols among urban professionals, producing higher margins than basic restorative work and lifting unit values for whitening kits, composite resins, and ceramic blocks. Approximately 70% of specialists in these cities now rely on digital-dentistry tools for case planning, a figure that has quadrupled since 2020. Social-media visibility and a rising culture of personal branding reinforce demand, while tight private-medical insurance coverage pushes many cosmetic transactions into a direct-payment model that improves cash flow for practices.

Government-Backed Oral-Health Screening Programs

The national oral-health policy issued in December 2024 integrates preventive dentistry into primary-care clinics and mobile units, signaling a structural step change in how underserved communities will access basic services[2]Source: University of the Western Cape, “National Oral Health Policy 2024,” uwc.ac.za . Early roll-outs prioritize sealants, fluoride varnish, and portable diagnostic kits, expanding the addressable base for low-unit-price consumables such as sterilization pouches, disposable mirrors, and atraumatic restorative-treatment hand instruments. While budget constraints slow infrastructure build-out, the policy aligns oral health with broader non-communicable-disease strategies, ensuring stable line-item funding through the medium term. Equipment suppliers that package rugged, battery-operated devices for outreach settings are best placed to benefit.

Emergence of Chair-side CAD/CAM Systems

Single-visit ceramic restorations are redefining patient expectations in premium urban clinics as chair-side scanners and milling machines collapse traditional two-week crown cycles into a single sitting. Practices adopting these systems report 15-20% higher annual restoration volumes and incremental referrals from time-sensitive patients. Integrated milling units cut reliance on external labs that struggle with courier delays during rolling blackouts, a persistent operational risk cited by 75% of healthcare providers[1]Source: Medical Protection Society, “South African Clinicians Voice Concern on Power Outages,” medicalprotection.org . Financing arrangements that bundle scanners, mills, and software into predictable subscription models further lower the entry barrier, propelling near-term uptake.

Growing Medical-Tourism Flow from SADC Neighbors

Implant centers in Gauteng and Western Cape provinces welcome a steady inflow of patients from Namibia, Botswana, and Mozambique who seek globally aligned protocols at cost levels 20-40% below European benchmarks. High-margin implant cases drive procurement of piezo-surgical units, CBCT scanners, and tissue-regeneration biomaterials. Clinics tailor packages that combine dental therapy with safari or beach holidays, leveraging South Africa’s air-hub status and English-language advantage. This segment insulates practices from domestic consumer softness and encourages continuous investment in premium equipment to maintain international accreditation.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unequal Provincial Reimbursement Caps on Dental Benefits | -0.4% | National, with varying impact by province | Long term (≥ 4 years) |

| Persistent Load-Shedding Disrupting Imaging-Equipment Utilisation | -0.6% | National, with varying severity by region | Medium term (2-4 years) |

| Shortage of Qualified Dental Technicians & Hygienists Outside Metros | -0.5% | Rural and peri-urban areas | Long term (≥ 4 years) |

| Import Tariff Volatility for High-End Implant Components | -0.3% | National, with higher impact on specialist practices | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Load-Shedding Disrupting Imaging-Equipment Utilisation

Scheduled power cuts lasting four hours or longer force practices to cancel radiographic appointments, elongate treatment cycles, and raise maintenance costs for sensors and generators. A nationwide survey found 75% of clinicians cite load-shedding as the single biggest barrier to efficient service delivery. Smaller practices absorb revenue losses directly, while larger groups install lithium-ion UPS systems that add up-front capital costs and ongoing battery replacement expenses. The constraint pressures suppliers to redesign CBCT and panoramic units with lower kV draw and fast boot-up sequences, yet the lost chair time continues to pull CAGR downward through 2028 as grid stability improvements lag.

Shortage of Qualified Dental Technicians & Hygienists

South Africa will be short 486 dentists, 60 specialists, and hundreds of support staff by 2025 under current graduation rates. Rural districts suffer most, with only one dentist per 22,000 residents, versus one per 6,000 in metropolitan areas. Staffing deficits restrict operating hours, slow adoption of complex gear that needs trained operators, and limit the reach of mobile-unit programs championed by government. Solutions such as remote-design labs and AI-guided hygiene scheduling are emerging, yet the human-resource gap remains a long-term drag on expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Recurring Consumables Sustain Cash Flow but Digital Equipment Accelerates

Dental consumables commanded 55.68% share of the South Africa dental devices market in 2025, anchored by universal demand for gloves, burs, endodontic files, and luting cements. Recurring purchases protect practice revenue streams against economic volatility and capital-budget freezes. However, equipment lines are gaining momentum with a projected 3.12% CAGR to 2031, reflecting stronger appetite for digital X-ray sensors, laser units, and chair-side mills capable of mitigating laboratory delays. The South Africa dental devices market size attached to diagnostics equipment is expanding fastest within the equipment category as urban clinicians gravitate toward CBCT, digital panoramic, and DSLR imaging setups that enhance case planning. Load-shedding anxiety pushes buyers toward devices outfitted with built-in batteries or low-energy standby modes.

Growth in therapeutic equipment is led by CAD/CAM milling machines posting double-digit trajectories, driven by single-visit restoration economics and patient convenience. Practices calculate that every in-house milled crown offsets two courier trips amid fuel inflation and traffic congestion, bolstering profit margins. Implantology materials—especially tapered titanium fixtures and ceramic abutments—report robust uptake among medical-tourism clinics, benefiting from bundled surgical-guide packages optimized for digital workflows. Suppliers of traditional alginate and conventional impression trays face gradual erosion as intra-oral scanners penetrate mid-tier practices. Still, consumable orders remain resilient because scanner-enabled workflows transition demand toward scan bodies, model resins, and zirconia blocks rather than eliminating supply consumption altogether.

By Treatment: Prosthodontic Anchor Faces Orthodontic Momentum

Prosthodontic services retained 33.12% share of the South Africa dental devices market in 2025 thanks to the country’s high burden of tooth loss, trauma, and edentulous cases. Implant-supported restorations command premium fees and drive sales of surgical motors, implant kits, and ceramic blocks. Clear aligner programs, however, push orthodontics to the front of the growth curve with a 3.86% projected CAGR through 2031. Aggressive social-media marketing by aligner brands and reduced stigma around adult orthodontics have widened the pool of eligible patients, particularly in the 25- to 45-year age cohort. The shift favors digital scanners for orthodontic records and 3-D planning software that streamlines aligner fabrication.

Endodontic volumes stay stable as caries prevalence remains high, yet innovation focuses on reciprocating file systems that shorten chair time and reduce instrument fatigue—key in a context where operator throughput matters during intermittent power supply. Periodontic treatment adoption of diode lasers and ultrasonic scalers centers on boosting clinical efficiency and reducing post-operative discomfort, indirectly lifting patient retention. The South Africa dental devices market share held by implants and abutments continues to expand as tourism and demographic aging converge, creating spill-over demand for bone-graft materials and guided-surgery kits that integrate seamlessly with CBCT imaging.

By End User: Clinics Steer Procurement Agendas

Independent and corporate dental clinics together accounted for 52.10% of the South Africa dental devices market in 2025 and will progress at a 3.55% CAGR to 2031. The clinic segment controls chair time allocation decisions, making it the primary channel for manufacturers launching new technologies. Large chains apply strict supplier scorecards covering energy efficiency, digital workflow compatibility, and service-level agreements, thereby shaping industry standards.

Hospitals continue to purchase higher-priced CBCT suites for maxillofacial surgery and ER dental trauma cases, creating concentrated demand spikes rather than consistent order flows. Academic institutes occupy the technology vanguard, piloting AI-assisted diagnostics and 3-D bioprinting yet contributing limited revenue volume. That said, their endorsements often accelerate downstream adoption among private practices. Corporate chains’ push toward cloud-based inventory analytics creates opportunities for just-in-time consumable replenishment models that reduce stock-outs caused by transport delays during power cuts.

Geography Analysis

Urban hubs—Johannesburg, Cape Town, and Durban—act as proving grounds for digital workflows, capturing most early sales of chair-side mills, diode lasers, and CBCT equipment. Competitive density and higher disposable income allow clinics to charge premium fees that underwrite rapid return on investment. Robust fiber-optic infrastructure supports cloud-backed EMR adoption rates that now exceed 70% among urban specialists, enabling seamless file transfers to labs located in other provinces. Nonetheless, even top-tier clinics lose clinical hours when load-shedding synchronizes with peak appointment blocks, underscoring the universal dependence on reliable power.

Rural and peri-urban regions tell a contrasting story of skeletal workforces and minimal capital budgets. Here, the dentist-to-population ratio hovers near 1:22,000, compounding access barriers created by long travel distances and inconsistent electricity. Government-funded mobile dental units, each equipped with portable X-ray generators and chair-mounted batteries, attempt to bridge the gap by conducting screenings, extractions, and fluoride treatments. Suppliers that engineer lightweight, rugged devices rated for bumpy roads and limited technical support find a burgeoning niche.

Border areas such as Limpopo and Mpumalanga leverage proximity to SADC catchment zones to cultivate implant and cosmetic tourism. Clinics in these provinces stock advanced implant toolkits and cone-beam systems configured for quick scheduling windows that align with travelers’ short stays. Multilingual reception teams and price-transparent package deals help convert international inquiries into chair bookings. These regional patterns force manufacturers to diversify product portfolios: ultra-portable units for outreach, premium CBCT stacks for urban flagships, and mid-range scanners for suburban generalists.

Regulatory Landscape

Dental devices in South Africa are regulated by the South African Health Products Regulatory Authority (SAHPRA) under the Medicines and Related Substances Act, 1965 (Act 101 of 1965) and associated regulations (including Government Gazette No. 40480). SAHPRA uses a risk-based classification framework (Class A to D) and requires medical device establishment licensing for manufacturers, importers, distributors, and exporters, with quality-system expectations commonly anchored to ISO 13485. For higher-risk dental products such as surgically invasive, long-term devices (for example, many implants), classification and evidence requirements are more stringent, which affects time-to-market and dossier strategy for suppliers.

A key access lever is SAHPRA's reliance-based review pathway, updated in February 2026, which lets the authority leverage prior decisions from recognized jurisdictions for registration while keeping final determination. This links to expanding digital dentistry adoption, where AI/ML-enabled software and digital diagnostic tools still route through SAHPRA's classification and essential principles framework, and establishment licensing remains a prerequisite across the supply chain. For import-heavy categories, compliance readiness also extends to customs clearance and local post-market responsibilities, increasing the value of capable in-country distributors and service partners for equipment uptime and vigilance reporting.

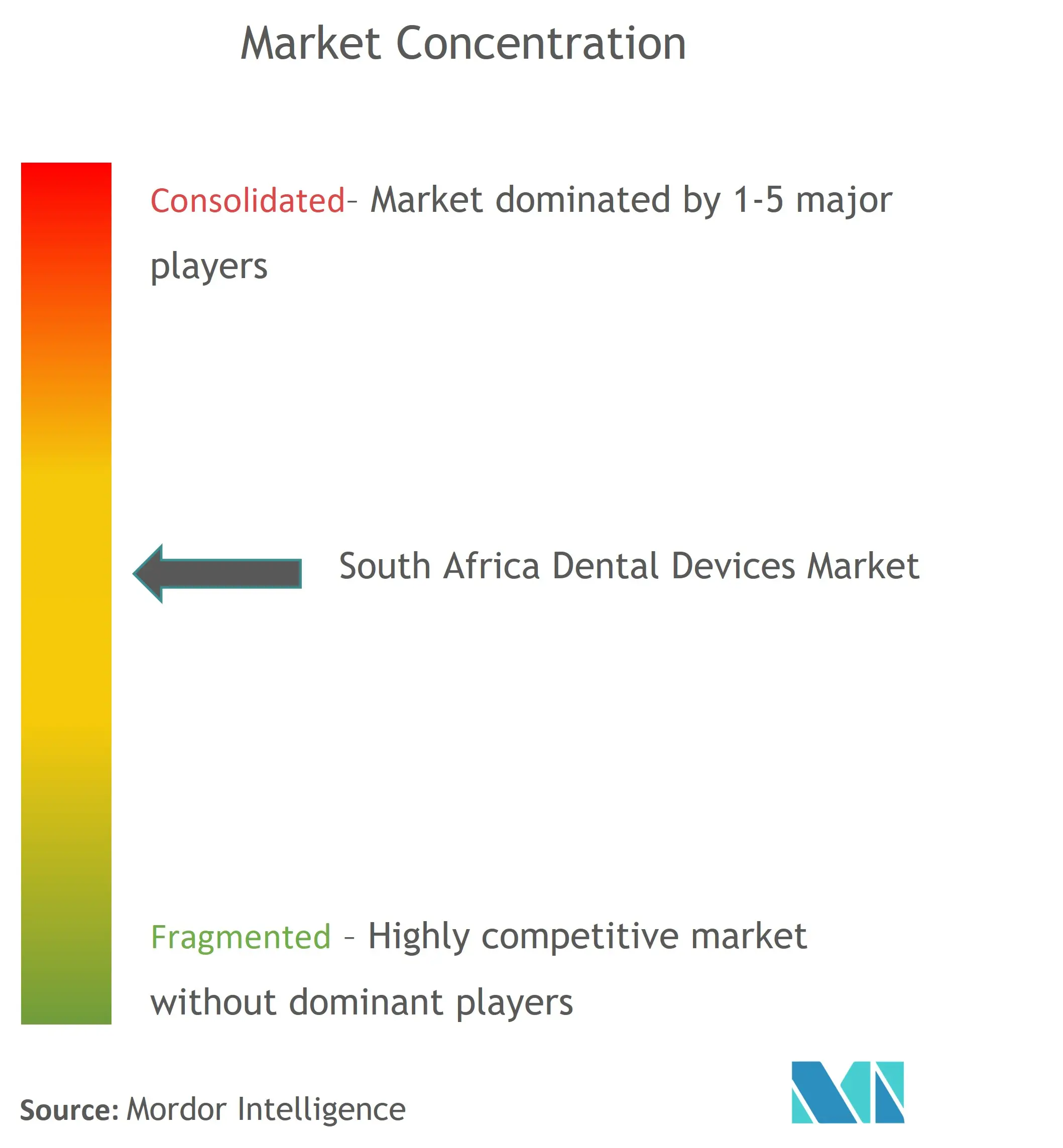

Competitive Landscape

Global leaders dominate high-specification equipment segments within the South Africa dental devices market, while local distributors remain critical gatekeepers for logistics, maintenance, and regulatory compliance. Dentsply Sirona, Straumann Group, and Henry Schein continue to leverage worldwide R&D pipelines, releasing update cycles that integrate cloud analytics and AI-driven restorative planning. Straumann’s enterprise-solutions division now targets Dental Service Organizations directly, bundling implants, scanners, and chair-side planning software under multiyear service contracts.

Domestic players focus on distributorship and niche manufacturing, with Southern Implants exporting biologically driven fixture designs made in Gauteng to more than 30 countries. Wright-Millners, the largest national distributor, operates regional depots that mitigate shipping slowdowns caused by road congestion or blackout-induced warehouse downtime. Foreign brands partner with these local channels to ensure same-day spare-parts availability, a key differentiator when clinics face revenue loss every hour a CBCT system sits idle.

Strategic investments increasingly center on power-stability features, remote diagnostics, and subscription-style consumable programs that smooth cash flows for operators navigating volatile exchange-rate swings. Dentsply Sirona’s 2025 restructuring prioritizes digital workflow expansion and cost control while sustaining R&D spending at roughly 4% of global net sales, underscoring the premium placed on innovation despite macroeconomic uncertainty. White-space opportunities persist for frugal-engineering devices capable of resilient performance under intermittent power and lean staffing.

South Africa Dental Devices Industry Leaders

3M

Straumann Holding AG

Dentsply Sirona

Henry Schein Inc.

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An opportunity is emerging in compliance-driven replacement and formalization of regulated imaging and digital workflows, particularly for dental X-ray and advanced radiology equipment where licensing and oversight are explicit. SAHPRA has previously flagged risks around importing and operating unlicensed dental X-ray equipment, which supports demand for compliant, fully documented systems and for distributors that can assist with licensing, installation, and servicing in clinics and hospitals. As chair-side CAD/CAM and digital impressions expand in major metros, suppliers that bundle scanners, mills, and software with validated quality and traceability documentation gain an advantage with corporate dental chains that standardize procurement and protocols.

Local capability building also creates whitespace for partnerships and localized production or assembly of select device and accessory categories as the regulatory system shifts toward structured, risk-based product registration. In May 2026, the University of Cape Town's Biomedical Engineering Research Centre secured a SAHPRA medical device manufacturing licence, indicating a practical route for research-led manufacturing and technology transfer into clinical settings. At the same time, SAHPRA guidance in April 2026 on licensing requirements for outsourced and contracted activities increases demand for licensed third-party services (packaging, sterilization, distribution), creating room for compliant local service providers to support device makers serving both premium urban clinics and outreach-oriented public programs.

Recent Industry Developments

- April 2026: Straumann Group reported continued execution around its digital ecosystem, including cloud-enabled platforms and intraoral scanning, as part of its Q1 2026 update. The emphasis on integrated digital workflows supports recurring revenue models and reinforces vendor pull-through for scanners and associated consumables used in guided surgery and prosthodontic cases in markets such as South Africa.

- December 2025: Henry Schein South Africa published clinical-use content highlighting 3M Scotchbond Universal Plus Adhesive and 3M RelyX Universal Resin Cement for posterior restorations. The communication supports adoption of standardized, simplified bonding and cementation protocols in private practices and chains, strengthening the consumables mix that underpins routine restorative volumes.

- October 2025: Henry Schein South Africa highlighted the availability of 3M Clinpro Clear Fluoride Treatment for local dental practitioners. This expands access to preventive-care consumables aligned with screening and prophylaxis workflows, supporting higher-throughput treatment models in clinics serving both private and broader community demand.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of dental devices sold and used in South Africa across routine diagnosis, treatment, and restoration work in dental care settings.

Scope exclusions: It excludes dental services revenue, general oral care consumer products, and dental education course fees.

Segmentation Overview

- By Product

- Diagnostics Equipment

- Dental Laser

- Soft Tissue Lasers

- Hard Tissue Lasers

- Radiology Equipment

- Extra Oral Radiology Equipment

- Intra-oral Radiology Equipment

- Dental Chair and Equipment

- Dental Laser

- Therapeutic Equipment

- Dental Hand Pieces

- Electrosurgical Systems

- CAD/CAM Systems

- Milling Equipment

- Casting Machine

- Other Therapeutic Equipments

- Dental Consumables

- Dental Biomaterial

- Dental Implants

- Crowns and Bridges

- Other Dental Consumables

- Other Dental Devices

- Diagnostics Equipment

- By Treatment

- Orthodontic

- Endodontic

- Peridontic

- Prosthodontic

- By End User

- Dental Hospitals

- Dental Clinics

- Academic & Research Institutes

- Academic & Research Institutes

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the country context and to anchor assumptions that are hard to get from a single dataset. We relied on public health and macro indicators, then linked them back to dental demand signals, such as treatment volumes and clinic activity.

Examples of sources used include national statistics releases from Statistics South Africa, public health updates from the National Department of Health, oral health and workforce references from the World Health Organization, and trade and tariff line information from ITC Trade Map and SARS customs guidance. We also reviewed company annual reports, investor presentations, product catalogs, and reputable press coverage to understand price bands, import dependence, and technology adoption. For targeted checks, we used paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment-level import and export data where available. The desk sources listed here are illustrative only, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on dental clinics, dental hospitals, labs, distributors, and dental trade participants to validate the device mix being purchased, plus the practical replacement and upgrade cycle. We also discussed pricing movement, imported product availability, and how load shedding and funding cycles influence ordering patterns across South Africa.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 16% | |

| Mid tier: 45% | Functional/Unit leaders: 33% | |

| Smaller Players: 18% | Managers: 51% |

Market-Sizing & Forecasting

Sizing started with a top-down demand pool build, where oral disease burden, treatment patterns, and the active base of dental practices were used to reconstruct yearly device consumption in value terms. Once the demand pool was framed, we checked it using selective bottom-up approximations, such as sampled average selling price ranges multiplied by expected unit volumes for common equipment and high-rotation consumables, followed by channel checks with distributors.

Key inputs used in the model included the installed base of dental chairs and imaging equipment, procedure mix shifts across restorative and orthodontic work, consumables usage per procedure, import exposure and landed cost sensitivity, and replacement timing for core equipment, which tends to cluster by clinic refurbishment cycles. Where direct unit visibility was limited, gaps were handled by using conservative proxy ratios from similar practice types, then correcting them through interview feedback until the totals aligned with observed purchase behavior.

For forecasting, we used scenario analysis supported by simple multivariate relationships, where procedure volume outlook, private healthcare spend trends, equipment replacement cycles, and currency-linked price movement were stress tested under base, conservative, and faster adoption cases. Assumptions were kept traceable, so a change in one driver, such as exchange rate pressure on imports, can be cleanly reflected in the final market path.

Data Validation & Update Cycle

Validation was done through multiple checks so that one weak data point could not swing the outcome. Model outputs were compared against independent signals like import intensity for device categories, reported clinic expansion activity, and reasonable spend per active practice, and then outliers were reviewed before internal sign-off.

When a major variance showed up, such as a sudden price jump or an unexpected demand dip, we re-contacted a small set of respondents to confirm whether it was temporary or structural. The report is refreshed annually, and interim updates are made when material events occur, such as policy shifts, sharp currency moves, or supply disruptions. Before delivery, a final analyst pass is completed so clients receive the latest updated view based on the most recent information available.

Mordor Intelligence's South Africa Dental Devices Market Estimate Compared With Other Published Estimates

Published market values for South Africa dental devices can look far apart, even when the topic name is the same, because firms do not always count the same products and buyer settings. Differences also come from how pricing is handled for imported items and from the year chosen as the reference point.

Some published figures broaden the scope by blending dental services revenue or by pulling in adjacent oral care consumer products, which can quickly lift the total. Others lean heavily on fast price growth and do not recheck it against distributor feedback and real replacement cycles, so the curve can move up quickly. Those add-on items sit outside the definition here. The device-only counting approach used by Mordor Intelligence keeps the total tied to equipment and consumables purchased for clinical dental use in South Africa.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 157.23 M (2025) | |

| Industry Publisher A | USD 273.00 M (2023) | Usually shown as a broader dental market view that can blend dental devices with dental care revenue or adjacent oral care categories, and the stated year and currency timing can also differ from device-only sizing. |

| Trade Data Digest B | USD 120.00 M (2024) | Often derived from selected import value lines, which can miss channel inventory movements, product reclassification across codes, and domestically distributed consumables that do not map cleanly to a narrow set of trade headings. |

The table mainly shows that higher figures tend to come from bundled definitions, and lower figures often reflect trade-only snapshots that undercount parts of the buying channel. By keeping the variables tied to procedure activity, installed base replacement, and realistic price movement, the resulting number stays transparent and repeatable for annual updates.

Key Questions Answered in the Report

What is the current South Africa Dental Devices Market size?

The South Africa Dental Devices Market is projected to register a CAGR of 2.82% during the forecast period (2026-2031)

Who are the key players in South Africa Dental Devices Market?

3M, Straumann Holding AG, Dentsply Sirona, Henry Schein Inc. and Zimmer Biomet are the major companies operating in the South Africa Dental Devices Market.

What years does this South Africa Dental Devices Market cover?

The report covers the South Africa Dental Devices Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the South Africa Dental Devices Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: