Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

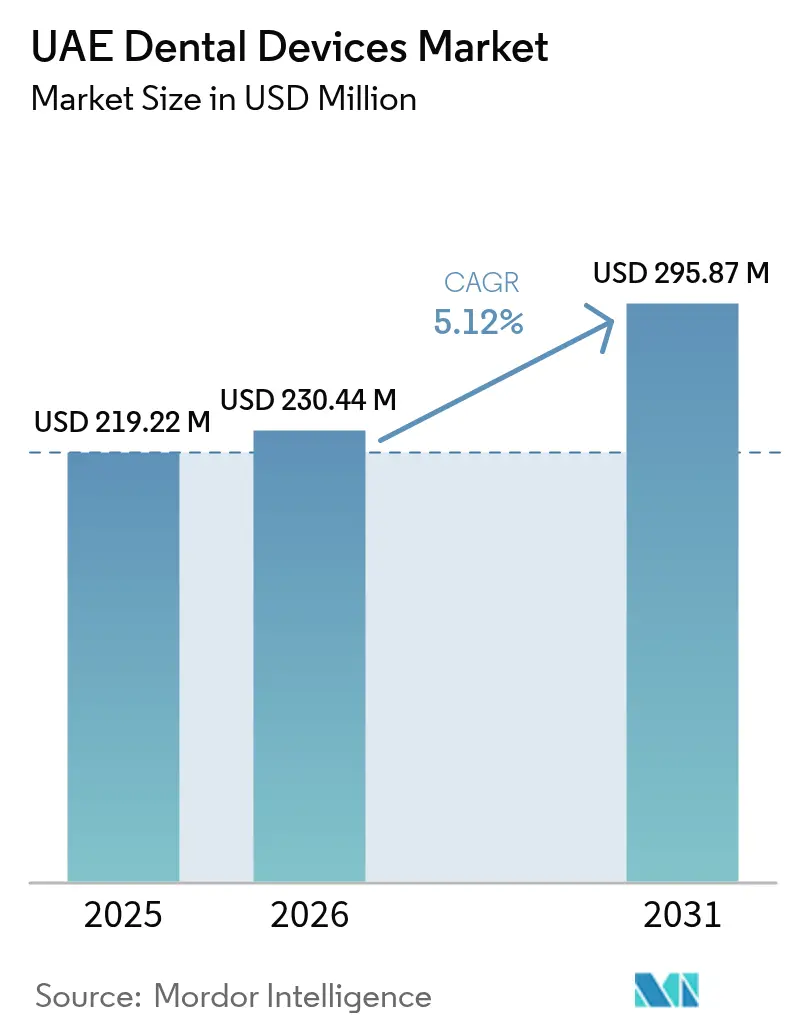

| Base Year Market Size (2025) | USD 219.22 Million |

| Market Size (2026) | USD 230.44 Million |

| Market Size (2031) | USD 295.87 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Dental Devices Market Analysis by Mordor Intelligence

UAE dental devices market size in 2026 is estimated at USD 230.44 million, growing from 2025 value of USD 219.22 million with 2031 projections showing USD 295.87 million, growing at 5.12% CAGR over 2026-2031. Mandatory health-insurance coverage expands the insured population and drives spending on complex dental procedures that rely on sophisticated imaging, CAD/CAM milling and in-chair sterilization equipment. Medical-tourism flows add premium demand for cosmetic treatments such as same-day veneers and clear aligners, magnifying the need for rapid-turnaround devices in both private and public settings. Government programs promoting advanced-technology adoption, free-zone incentives for localized manufacturing and ready access to capital from Mubadala and other state-linked funds further reinforce the growth trajectory. At the same time, geographic service gaps in newly urbanized districts of Dubai and the Northern Emirates create white-space opportunities for mobile or compact units capable of delivering high-throughput care in constrained spaces. Competitive intensity remains moderate, with multinational OEMs and agile local distributors balancing price, service and digital-workflow integration to differentiate offerings.

Key Report Takeaways

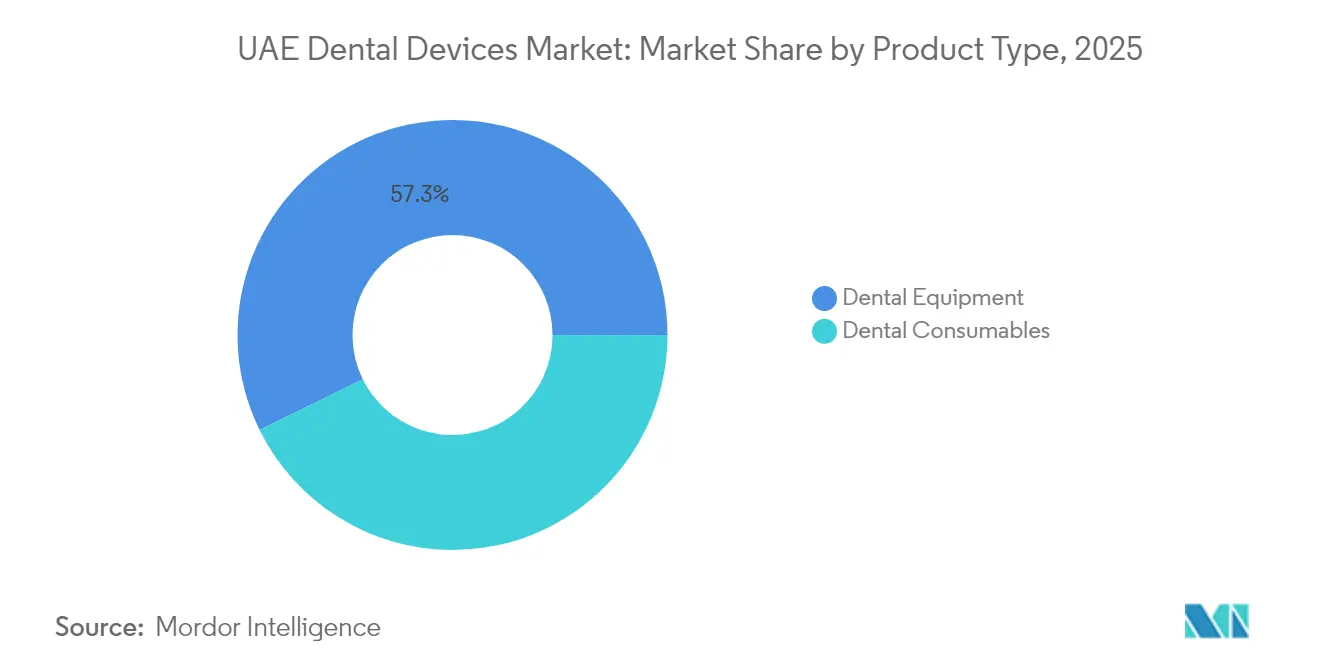

- By product category, dental equipment accounted for 57.28% of UAE dental devices market share in 2025.

- By treatment type, prosthodontic procedures are expanding at a 5.74% CAGR through 2031, the fastest among all treatment categories in the UAE dental devices market.

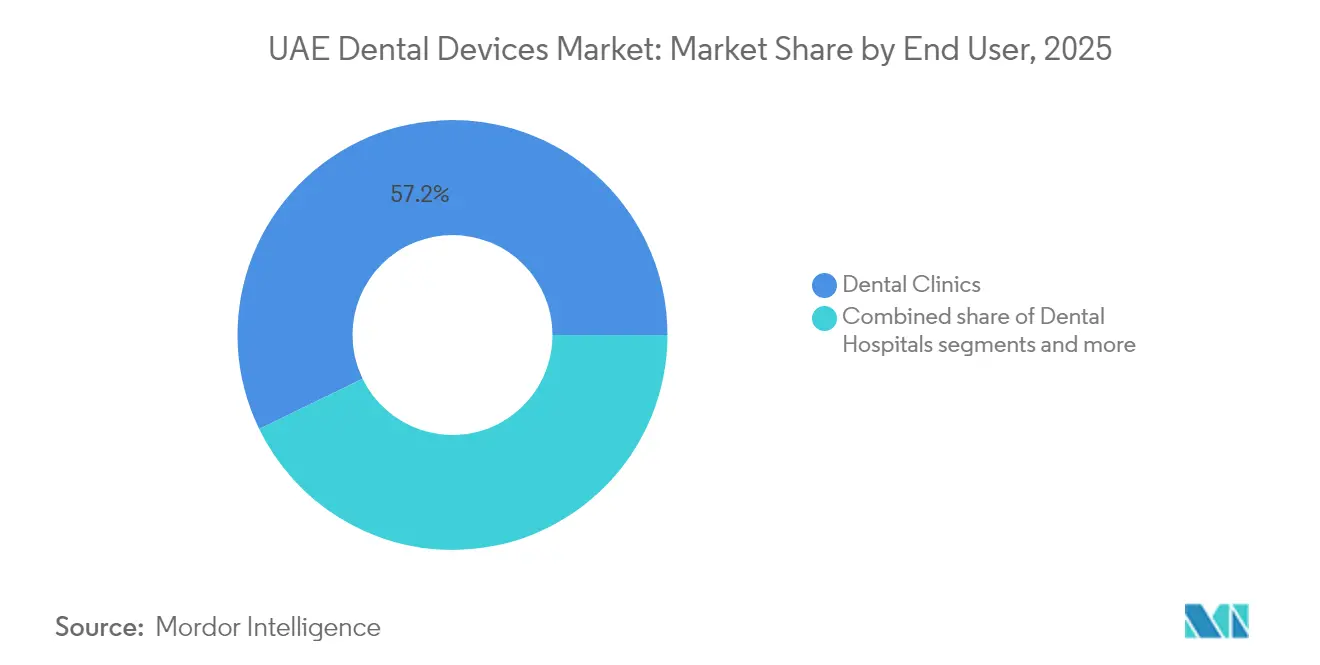

- By end user, dental clinics captured 57.21% of UAE dental devices market size in 2025 and are growing at a 5.28% CAGR through the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Dental Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory health-insurance coverage | +1.2% | Nationwide, strongest in Dubai & Abu Dhabi | Medium term (2-4 years) |

| Rapid influx of dental tourists | +0.9% | Dubai core, spillover to Northern Emirates | Short term (≤ 2 years) |

| Government incentives for local manufacture | +0.7% | JAFZA, Dubai Healthcare City, KEZAD | Long term (≥ 4 years) |

| Digital-workflow adoption | +1.1% | Nationwide, early adoption in Dubai & Sharjah | Medium term (2-4 years) |

| 3-D printed aligner hubs | +0.5% | Dubai & Abu Dhabi free zones | Long term (≥ 4 years) |

| Emirati R&D grants for AI diagnostics | +0.4% | Academic centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Health-Insurance Coverage Spurs Spend on Complex Dental Procedures

The UAE’s universal-insurance mandate offers basic coverage caps ranging from AED 500 to AED 4,500 per year for routine dentistry but excludes high-margin orthodontic and prosthodontic procedures. Clinics therefore emphasize AI-guided diagnostics and chairside CAD/CAM systems that raise per-visit revenue while meeting insurer documentation standards. Coinsurance rates of 20-30% make patients more outcome-sensitive, encouraging providers to adopt devices that shorten chair time and boost treatment predictability. Federal licensing rules oblige private facilities to install certified X-ray generators, sterilizers and emergency equipment, creating a fixed baseline for procurement . Reimbursement cycles averaging 120 days push clinics toward leasing or vendor-financed equipment that smooths cash-flow volatility.

Rapid Influx of Dental Tourists Seeking High-End Cosmetic Treatments

Dubai captured AED 1.4 billion in dental-related medical-tourism revenue in 2024, and the Dubai Health Authority targets USD 708 million by 2030. International patients schedule concentrated treatment plans, necessitating intraoral scanners, high-speed milling units and on-site 3-D printers that enable same-day crowns, veneers and aligners. Affluent visitors pay premium rates, supporting adoption of AI-enhanced visualization, digital-smile-design software and end-to-end cloud workflows. The 168+ facilities in Dubai Healthcare City catalyze equipment standardization and shared training, accelerating technology diffusion.

Government Incentives for Local Manufacture of Medical Devices

The “Make it in the Emirates” program grants 100% foreign ownership, multi-year tax holidays and fast-track customs clearance in JAFZA, DHCC and KEZAD. These measures trim landed costs for digital sensors, autoclaves and consumables by up to 25% and reduce import lead times. The Emirates Drug Corporation aims to unify device registration, potentially shortening approval processes for locally assembled models. Mubadala-backed capital vehicles co-invest with foreign OEMs to build production lines that serve GCC markets, reinforcing the UAE dental devices market as a regional export base.

Digital-Workflow Adoption (CAD/CAM, 3-D Printing) Across UAE Clinics

Intraoral-scanner penetration exceeded 50% in Dubai’s private clinics during 2025, and AI plug-ins now ship as default features on high-end CAD/CAM platforms. The University Dental Hospital Sharjah maintains throughput of 150 patients per day with 124 chairs by leveraging staggered digital-workflow scheduling. Cloud-based imaging and practice-management systems run on UAE sovereign Azure zones, ensuring data residency and cyber-resilience while facilitating remote treatment planning and predictive device maintenance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import tariffs & registration fees on small-batch devices | -0.8% | UAE National, particularly affecting smaller clinics | Short term (≤ 2 years) |

| Shortage of UAE-licensed dental technologists and hygienists | -0.6% | UAE National, acute in Northern Emirates | Medium term (2-4 years) |

| Patient price-sensitivity for premium consumables despite insurance | -0.4% | UAE National, stronger in price-conscious segments | Medium term (2-4 years) |

| Limited sterilizer capacity slows clinical throughput | -0.3% | Dubai and Abu Dhabi high-volume clinics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Import Tariffs & Registration Fees on Small-Batch Devices

A 5% CIF duty applies unless exemptions are documented, while the 12-digit HS code adopted in 2025 lengthens documentation requirements. Registration fees of AED 1,000 per SKU distort the economics of low-volume imports such as niche orthodontic pliers or surgical microscopes. VAT adds a further 5% overhead, pressuring price-sensitive clinics outside Dubai. Standardization of the Emirates Drug Corporation portal should streamline approvals, yet transitional confusion prolongs customs dwell times.

Shortage of UAE-Licensed Dental Technologists and Hygienists

Dentist density is high at 0.9 per 1,000 population, but auxiliary staff remain limited due to longer certification timelines and high expatriate turnover. Clinics in Sharjah and Fujairah underuse chairside milling systems when trained CAD/CAM operators leave after visa expiration. Abu Dhabi’s Department of Health now mandates extended supervised practice for overseas graduates, escalating onboarding costs. University surveys reveal 51% of students plan specializations, yet capacity constraints in postgraduate seats slow pipeline growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Equipment Dominance Drives Digital Transformation

UAE dental devices market size for equipment stood at USD 125.57 million in 2025 and is projected to expand at a 5.66% CAGR. Diagnostic imaging—digital radiography, CBCT scanners and handheld X-ray units—accounts for the largest revenue slice as clinics replace film with flat-panel sensors. Therapeutic devices such as chairside milling machines, soft-tissue lasers and piezosurgery units follow closely, propelled by demand for same-day restorations. Vendors bundle training and predictive-maintenance software, converting one-time sales into subscription streams. Dental consumables rank second in absolute revenue, led by implant fixtures, bone-graft materials and hybrid ceramic blocks. Local distributors differentiate by warehousing stock in bonded free-zone facilities, ensuring same-day delivery. Niche devices—air-abrasion units, surgical microscopes—grow slowly due to limited local KOL advocacy and longer regulatory review cycles.

The decline in per-unit prices for entry-level cameras and scanners widens the addressable base among small clinics, but premium-tier platforms still command strong margins when bundled with AI analytics. Supplier competition intensifies in service contracts, with Dentsply Sirona and Planmeca offering 48-hour parts-replacement guarantees, while local firms such as Dubai Medical Equipment L.L.C provide Arabic-language support and zero-interest installment plans.

By Treatment: Prosthodontic Growth Outpaces Orthodontic Leadership

Orthodontic procedures retained a 38.15% share of 2025 revenue in the UAE dental devices market, buoyed by clear-aligner popularity among expatriate teenagers and young professionals. Yet prosthodontics leads in growth, expanding at 5.74% CAGR as demand for implant-supported dentures, full-arch restorations and zirconia bridges rises with the aging expatriate population. The shift requires CBCT scanners, guided-surgery kits and lab-grade 3-D printers. Endodontic and periodontic services show steady growth in medically necessary care; MOHAP reimbursement schedules cover root-canal instrumentation and periodontal laser therapy, supporting device demand in these categories. Treatment-mix diversification elevates cross-training needs; practices once dedicated to orthodontics now invest in implant motors and surgical navigation, raising average capital outlay per chair.

University data indicate a growing pipeline of prosthodontists and endodontists, aligning future workforce supply with device adoption trajectories. Meanwhile, aligner labs’ proximity lowers treatment costs, sustaining orthodontic case volumes even as prosthodontics accelerates.

By End User: Clinic Efficiency Drives Market Concentration

Clinics held 57.21% of UAE dental devices market size in 2025 thanks to regulatory frameworks that favor private investment and patient preference for shorter wait times. Clusters such as Dubai Healthcare City leverage shared digital platforms, reducing per-practice IT overhead. Partnerships like DHCC–KLAIM enable next-day invoicing, freeing working capital for equipment upgrades DHCC.AE. Clinics report that AI-based treatment-planning modules cut average chair time by 17%, justifying purchases of premium imaging and sterilization equipment. Hospitals command a smaller yet strategic share, focusing on complex maxillofacial cases requiring integrated OR and ICU capabilities. Academic and research institutes constitute a niche but influential segment; simulation labs, haptic trainers and spectroscopic imaging receive steady funding from federal research budgets.

The evolving mix underscores the importance of flexible financing. OEMs offer lease-to-own models with embedded analytics dashboards that alert technicians to preventive-maintenance windows, reducing downtime in high-volume practices

Geography Analysis

Dubai and Abu Dhabi generate the bulk of revenue for the UAE dental devices market, leveraging flagship ecosystems like Dubai Healthcare City and the Abu Dhabi Health Services network. Dubai’s top ranking in the Medical Tourism Index sustains a pipeline of high-value cosmetic cases that require latest-generation scanners and milling units. Abu Dhabi invests heavily in AI research through MBZUAI, catalyzing early adoption of AI-assisted radiology platforms within hospital dental departments.

Sharjah, Ajman and Fujairah exhibit rapid percentage growth albeit from smaller bases. The University of Sharjah adds demand for didactic simulators and research-grade sensors. In Ajman, clinic chains expand into fast-growing suburbs, purchasing compact CBCT units that fit within limited floor plans. Dubai’s 2030 services gap projects shortages of 2,160 outpatient rooms in districts such as Deira, Nahda and Dubai Land, driving orders for mobile sterilization carts and portable imaging systems BMCHSERVRES.BIOMEDCENTRAL.COM.

Free-zone logistics hubs—including JAFZA and KEZAD—enable just-in-time inventory management, reducing capital tied up in stock and encouraging distributors to maintain wider SKU assortments. Northern Emirates operators benefit from lower real-estate costs but lag in advanced-equipment penetration, presenting a receptive audience for entry-level digital workflows with upgrade paths. Regulatory overlaps persist during the Emirates Drug Corporation transition, but unified labeling and eIFU policies should ease multi-emirate distribution in the medium term.

Competitive Landscape

International brands continue to launch portfolio upgrades in the UAE dental devices market, but service responsiveness often determines final purchase decisions. Local distributors such as Gulf Medical Equipment LLC maintain same-day couriers between JAFZA warehouses and Dubai Healthcare City, giving them a timing edge over global OEM depots that sit in Europe or Singapore. These distributors also offer Arabic-language e-learning portals and in-clinic calibration visits that larger manufacturers rarely bundle without extra fees. Mobile service fleets equipped with 3-D-printed spare parts have gained traction, especially in Sharjah and Ajman where road time adds cost to downtime.Pricing dynamics in the UAE dental devices market increasingly hinge on software lock-ins rather than hardware margins. Henry Schein One ties annual cloud-analytics subscriptions to bulk orders of sterilizers and imaging plates, converting clinics into lifetime clients when data records cannot be migrated easily. Planmeca responds with open-file standards, courting multi-vendor practices that resist single-suite ecosystems. Align Technology leverages its regional aligner-printing hub to bundle iTero scanners and weekly remote-coaching modules, an approach that raises total contract value despite competitive scanner discounts. Meanwhile, Dentsply Sirona positions its Primescan 2 as the high-throughput nucleus of a full “digital-chair” workflow that spans imaging, milling and polishing within a single appointment slot.

Regulatory fluency remains a sustainable differentiator across the UAE dental devices market. Distributors who submit device folders through the new Emirates Drug Corporation sandbox are reporting approval cycles trimmed from 120 days to fewer than 60 days. Faster launches translate into six-month selling head starts for hot categories such as UV-resin printers and AI-enabled periapical cameras. As the regulator introduces e-IFU mandates, vendors offering Arabic and English manuals within a single QR code save clinics printing costs and earn goodwill with inspectors. Rising interest in green health-care procurement further widens the moat for suppliers that quantify device carbon footprints, a criterion now embedded in several Abu Dhabi hospital tenders.

UAE Dental Devices Industry Leaders

Dentsply Sirona

3M Company

ZimVie Inc.

Dubai Medical Equipment LLC

Advanced Healthcare Medical Equipment LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Abu Dhabi Department of Health updated its Clinical Training Program guidelines for healthcare graduates, requiring supervised clinical practice and updated registration procedures. The program modifications affect dental education infrastructure and equipment requirements at UAE academic institutions.

- April 2024: UAE Embassy published comprehensive white paper on advanced technology cooperation with the United States, outlining strategic framework includes investments in medical imaging, CAD/CAM dental design capabilities, and AI-driven diagnostics through collaborations with Microsoft, OpenAI, and NVIDIA.

UAE Dental Devices Market Report Scope

As per the scope of the report, dental instruments are tools that dental professionals use to provide dental treatment. They include tools to examine, manipulate, treat, restore, and remove teeth and surrounding oral structures. Standard instruments are used to examine, restore, extract teeth, and manipulate tissues.

The UAE Dental Devices Market is Segmented by Product Type (General and Diagnostic Equipment (Dental Implants, Crown and Bridge, Dental Laser, and Other General and Diagnostics Equipment), Radiology Equipment, Dental Biomaterial, Dental Chair and Equipment, Dental Consumables, and Other Dental Devices), Treatment (Orthodontic, Endodontic, Periodontic, and Prosthodontic), End User (Hospitals, Clinics, and Other End Users). The report offers the value (in USD million) for the above segments.

By Product

| Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | ||

| Radiology Equipment | Extra-oral Radiology Equipment | |

| Intra-oral Radiology Equipment | ||

| Dental Chair & Equipment | ||

| Therapeutic Equipment | Dental Hand Pieces | |

| Electrosurgical Systems | ||

| CAD/CAM Systems | ||

| Milling Equipment | ||

| Casting Machine | ||

| Other Therapeutic Equipments | ||

| Dental Consumables | Dental Biomaterial | |

| Dental Implants | ||

| Crowns & Bridges | ||

| Other Dental Consumables | ||

| Other Dental Devices | ||

By Treatment

| Orthodontic |

| Endodontic |

| Periodontic |

| Prosthodontic |

By End User

| Dental Hospitals |

| Dental Clinics |

| Academic & Research Institutes |

| By Product | Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | |||

| Radiology Equipment | Extra-oral Radiology Equipment | ||

| Intra-oral Radiology Equipment | |||

| Dental Chair & Equipment | |||

| Therapeutic Equipment | Dental Hand Pieces | ||

| Electrosurgical Systems | |||

| CAD/CAM Systems | |||

| Milling Equipment | |||

| Casting Machine | |||

| Other Therapeutic Equipments | |||

| Dental Consumables | Dental Biomaterial | ||

| Dental Implants | |||

| Crowns & Bridges | |||

| Other Dental Consumables | |||

| Other Dental Devices | |||

| By Treatment | Orthodontic | ||

| Endodontic | |||

| Periodontic | |||

| Prosthodontic | |||

| By End User | Dental Hospitals | ||

| Dental Clinics | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

How large will the UAE dental devices market be by 2031?

It is forecast to reach USD 295.87 million, advancing at a 5.12% CAGR.

Which segment currently drives the most spending?

Dental equipment holds 57.28% of 2025 revenue, led by digital imaging and chairside milling units.

Why is prosthodontics growing faster than other treatments?

Rising demand for implant-supported dentures and full-arch restorations among aging expatriates pushes prosthodontic procedures at a 5.74% CAGR.

What role do free zones play in device supply?

JAFZA, DHCC and KEZAD offer 100% foreign ownership and tax relief, lowering landed costs by up to 25% and speeding customs clearance.

How does the new Emirates Drug Corporation affect approvals?

Early adopters report device clearance times shrinking to below 60 days, accelerating product launches nationwide.

Page last updated on: