Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 740 Billion |

| Market Size (2026) | USD 0.77 Billion |

| Market Size (2031) | USD 0.96 Billion |

| Growth Rate (2026 - 2031) | 4.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Dental Devices Market Analysis by Mordor Intelligence

The Latin America Dental Devices Market size was valued at USD 740 million in 2025 and estimated to grow from USD 770 million in 2026 to reach USD 960 million by 2031, at a CAGR of 4.46% during the forecast period (2026-2031).

Demand is underpinned by an expanding private-clinic ecosystem, rising patient preference for digital workflows and supportive regulatory reforms in Brazil that shorten product-approval timelines. Dental service organizations (DSOs) continue consolidating independent practices, placing large multi-site orders and driving manufacturer interest in bundled equipment-and-training contracts. Currency volatility remains the principal cost headwind because most high-end devices are imported and invoiced in US dollars. Nevertheless, the pipeline of digital radiology, chairside CAD/CAM and 3-D printers is strengthening as manufacturers tailor price tiers and financing packages to the Latin American dental equipment market, signalling sustained mid-single-digit growth through 2030.

Key Report Takeaways

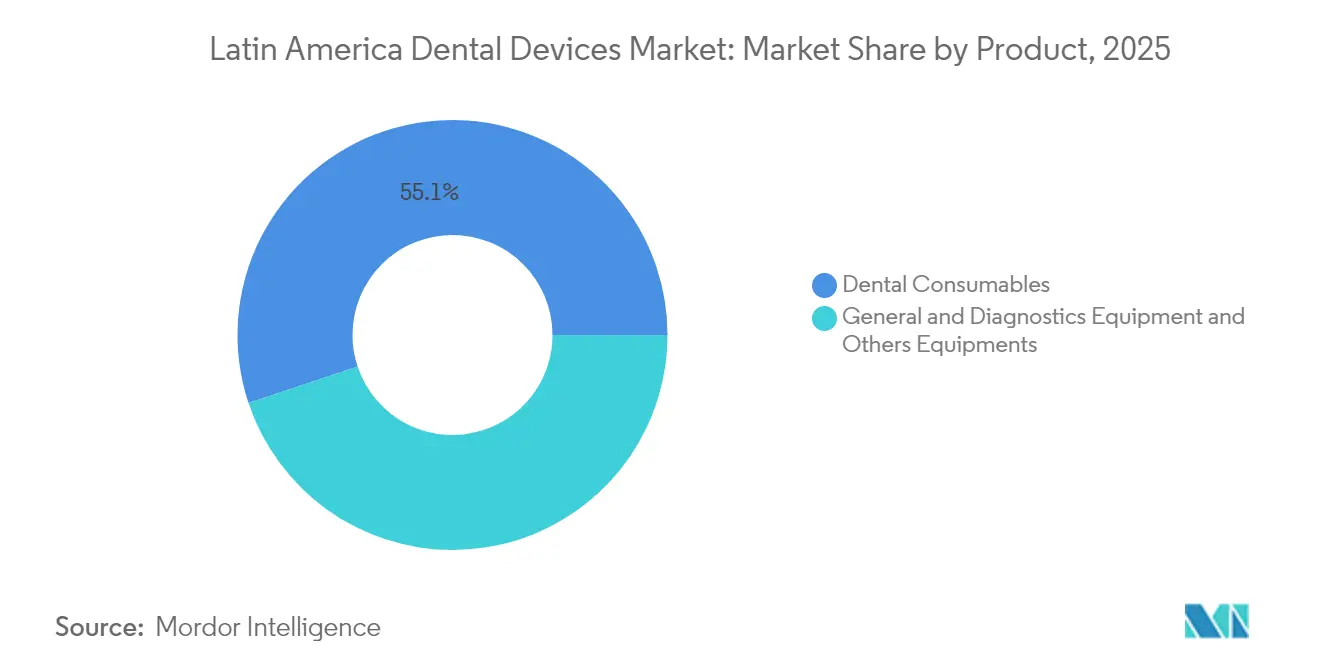

- By product category, dental consumables led with 55.12% revenue share in 2025; digital diagnostic equipment is projected to expand at a 5.05% CAGR to 2031.

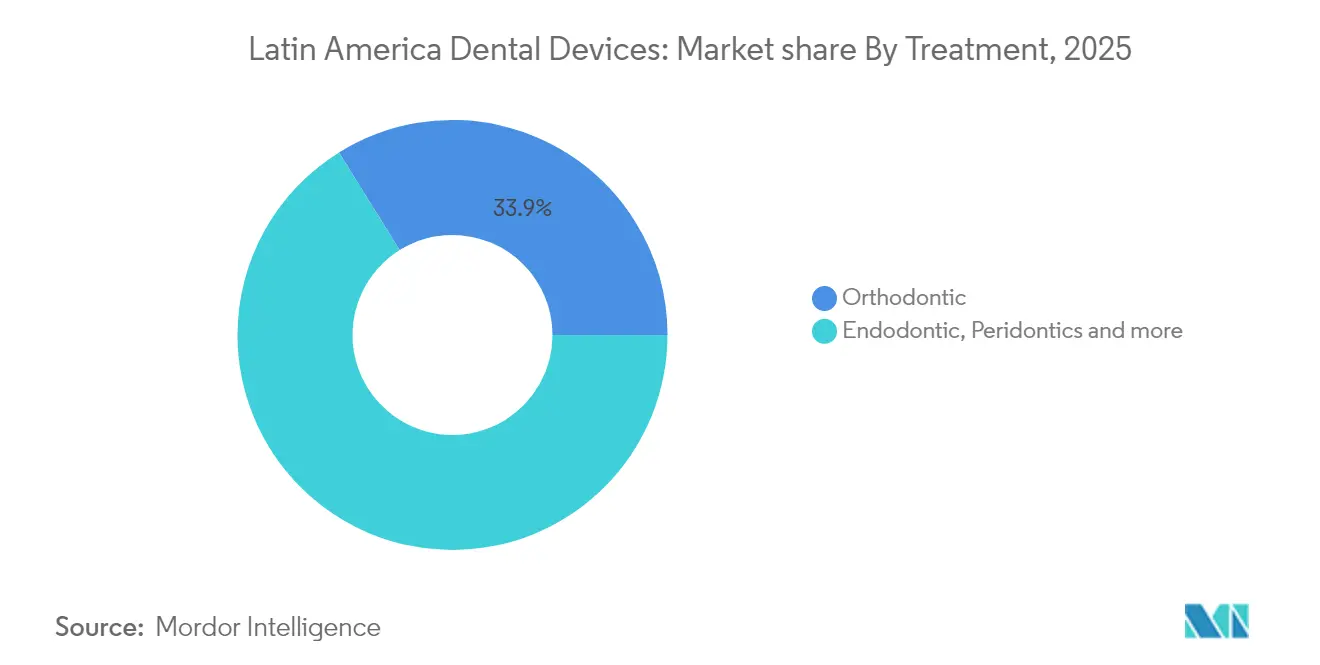

- By treatment type, orthodontic procedures held 33.85% of the Latin American dental equipment market share in 2025, while prosthodontic care is forecast to post the fastest 5.53% CAGR through 2031.

- By end user, dental hospitals accounted for 45.10% share of the Latin American dental equipment market size in 2025 and dental clinics are set to advance at a 5.78% CAGR between 2026-2031.

- By geography, Brazil commanded 35.20% share in 2025; Colombia is projected to outpace the regional average with a 6.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Latin America Dental Devices Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in dental tourism in Brazil & Mexico | 1.20% | Brazil, Mexico, Colombia | Medium term (2-4 years) |

| Expansion of private DSO networks | 0.90% | Brazil, Mexico, Colombia | Long term (≥4 years) |

| CAD/CAM & 3-D-printing lab adoption | 1.00% | Brazil, Chile, Colombia | Medium term (2-4 years) |

| Teledentistry roll-outs | 0.70% | Brazil, Mexico, Argentina | Short term (≤2 years) |

| Mercosur tariff cuts on digital radiology | 0.50% | Brazil, Argentina, Uruguay, Paraguay | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rise in Dental Tourism in Brazil & Mexico Driving High-end Device Sales

Patient inflows from the United States and Canada are prompting clinics to differentiate through premium intraoral scanners, chairside milling machines and implant surgery units. Annual global dental-tourism volumes reached 3–4 million by 2024, and the Latin American dental equipment market benefits directly because half of these travelers select Brazil or Mexico. Clinics in Bogotá and Medellín are replicating this strategy, investing in CBCT scanners that enhance treatment planning accuracy. Equipment acquisitions increasingly emphasize visible, patient-facing technologies that serve as marketing assets as much as clinical tools. The competitive response from manufacturers is to extend deferred-payment schemes linked to tourism seasonality, thereby mitigating foreign-exchange risk for practices. Collectively, tourism-driven spending is lifting the premium sub-segment’s contribution to the Latin American dental equipment market.

Expansion of Private DSO Networks Boosting Bulk Equipment Procurement

DSOs use group purchasing contracts to secure double-digit discounts on dental units, imaging suites and sterilization systems. The DSO model accounted for 64% of new-practice openings in 2024, up from 15% a decade earlier, reshaping supplier negotiations. Regional leaders bundle after-sales service and remote-monitoring software to standardize clinical quality across sites, an approach that reduces unplanned downtime and strengthens vendor lock-in. For manufacturers, multi-year framework agreements with DSOs flatten quarterly order volatility and improve volume forecasting. This trend is structurally positive for the Latin American dental equipment market because it raises replacement-cycle predictability and accelerates uptake of digitally-integrated platforms.

CAD/CAM & 3-D-Printing Lab Rise in Adoption

Laboratories adopting chairside CAD/CAM and polymer-as-well-as-metal 3-D printers cut prosthesis turnaround times from days to hours, reducing patient revisits and material waste. Latin American labs processed 85,000 digital impressions in 2024, a jump of 42% year-on-year, as academies partnered with vendors to upskill technicians. This shift spurs demand for auxiliary curing units, design software licences and intraoral scanners that feed the digital workflow. Private equity funds are financing lab modernization across Brazil and Chile, betting on a payback period shortened by higher case throughput. Scaling digital production is therefore a major engine of value creation in the Latin American dental equipment market.

Teledentistry Roll-outs Fueling Portable Diagnostic Device Uptake

Post-pandemic regulatory frameworks now allow remote triage and follow-up in Brazil and Chile, driving procurement of handheld X-ray sensors, wireless intraoral cameras and tablet-based charting systems. Around 30% of dentists surveyed in 2024 used teledentistry platforms for at least five hours monthly, double the 2021 level jada.org. Real-time image transfer demands devices with integrated AI that flags carious lesions, thus shortening chair time during in-person appointments. Regions with sparse specialist coverage such as Argentina’s Patagonia are piloting store-and-forward models supported by public telehealth grants. Collectively, these projects open a fresh channel for entry-level diagnostic brands, expanding the overall Latin American dental equipment market.

Restraints Impact Analysis of Latin America Dental Devices Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brazil ANVISA registration delays | −0.8% | Brazil | Medium term (2-4 years) |

| High after-sales service costs | −0.6% | Latin America (region-wide) | Long term (≥4 years) |

| FX volatility inflating imported CBCT costs | −0.7% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Patchy implant reimbursement | −0.5% | Mexico, Brazil, Chile | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Brazil ANVISA Registration Delays (12-18 months)

Although recent reforms target a 60-day fast-track for lower-risk categories, Class III and IV dental devices still face lengthy dossier reviews. Intermediate manufacturers often defer launches because bridging studies and local biocompatibility tests inflate pre-market budgets. Larger multinationals mitigate the delay by parallel filing strategies, yet the inventory cost of holding non-approved stock drags on margins. The bottleneck reduces competitive price pressure in Brazil and slows availability of cutting-edge products, shaving growth from the Latin American dental equipment market.

FX Volatility Inflating Imported Cone-Beam CT Costs

Regional currencies depreciated 11% against the US dollar, on average, between Q4 2023 and Q4 2024. Because CBCT scanners exceed USD 150,000 per unit, even modest swings raise landed costs by thousands of dollars. Distributors react by shortening quotation validity to 15 days and promoting lease-to-own structures denominated in local currency. Some clinics postpone adoption altogether, stretching the equipment replacement cycle beyond seven years. Until macroeconomic stability returns, large capital-item turnover in the Latin American dental equipment market will remain below potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Latin America Dental Devices Market Segment Analysis

By Product:

Digital Solutions Reshape Procurement PatternsDental consumables led revenue in 2024 owing to their high-frequency usage, yet capital equipment categories are catching up as digital workflows become mainstream. Chairside CAD/CAM systems and polymer-resin 3-D printers recorded a regional shipment jump that translated into a 23% annual sales expansion. Panoramic and cephalometric radiology still dominate imaging spend, but intraoral sensors are closing the gap because cloud-based storage lowers IT overhead for smaller practices. Manufacturers bundle software upgrades with sterilizers and compressors, ensuring that integrated suites remain attractive against piecemeal hardware purchases. Consequently, digital platforms are set to outpace traditional instrumentation, reinforcing the supply-chain pivot toward high-margin service contracts within the Latin American dental equipment market.

Adoption speed varies: Chile and Colombia moved fastest thanks to favorable import-duty structures, while cost-sensitive markets such as Peru focus on refurbished units. Firmware standardization across scanners, milling machines and curing ovens is improving cross-compatibility, reducing chairside errors and raising case throughput. Local assemblers in Brazil are adding open-architecture modules to capture labs seeking vendor-agnostic solutions. Overall, product-level innovation is aligned with the twin goals of shortening treatment timelines and monetizing practice downtime—drivers that keep the Latin American dental equipment market on a steady growth trajectory.

By Treatment:

Aesthetic Demand Reshaping Procedure MixOrthodontic treatments accounted for 33.85% of the Latin American dental equipment market size in 2025 because clear-aligner penetration accelerated among young adults. Align Technology’s incremental expansion of its Invisalign portfolio into mid-tier price points fuelled demand for chairside scanners and polishing systems that deliver faster turnaround. Prosthodontic care, supported by advanced implant surfaces and zirconia milling, is on course for the fastest 5.53% CAGR through 2031 as populations age and edentulism rates remain high.

Periodontic and endodontic segments benefit from adjunctive lasers that shorten operating times, yet their aggregate share trails aesthetic-driven specialties. Digital planning tools now integrate occlusal schemes and implant angles into one dashboard, enhancing interdisciplinary coordination. Treatment diversification is thus increasingly data-centric, reinforcing equipment purchases that plug directly into patient-management ecosystems— a dynamic that enlarges the Latin American dental equipment market.

By End User:

Private Clinics Accelerate Equipment RefreshDental hospitals held 45.10% of the Latin American dental equipment market share in 2025, leveraging teaching affiliations and multi-disciplinary case loads to justify CBCT, surgical microscopes and custom implant libraries. Private clinics are closing the gap, forecast at a 5.78% CAGR to 2031 as DSOs finance bulk upgrades and brand-agnostic service contracts.

Academic institutes continue acting as validation partners, but budget constraints push them toward equipment-leasing consortia. Public-sector procurement focuses on low-maintenance units adapted to rural outreach programs, indirectly stimulating demand for portable chairs and battery-powered scalers. Overall, end-user purchasing decisions are converging on scalable, software-upgradable systems—traits that extend revenue visibility for suppliers across the Latin American dental equipment market.

Geography Analysis

Brazil Dental Devices Market

Brazil anchors the Latin American dental equipment market through its workforce of roughly 270,000 dentists and an extensive domestic manufacturing base that includes Dental Morelli and Alliage SA. Recent ANVISA reforms promise faster market access for digital radiology suites, encouraging both global and local suppliers to accelerate product launches. The country also captures inbound dental tourism, especially for implantology, pushing high-spec CBCT and chairside milling systems into mainstream adoption. Despite periodic currency swings, vendor-financed leasing mitigates cap-ex pressures for private clinics in São Paulo and Rio de Janeiro.

Mexico Dental Devices Market

Mexico ranks second, benefiting from cross-border patient flows and a mature private-insurance segment willing to pay for premium restorative work. Permanent approval of telehealth since 2022 supports hybrid care models that depend on portable imaging sensors and cloud-enabled practice-management software. Import reliance remains high because local manufacturing focuses on consumables, yet the US-Mexico-Canada Agreement (USMCA) ensures smoother customs clearance for North American brands targeting the Latin American dental equipment market.

Colombia Dental Devices Market

Colombia is the fastest-growing geography, propelled by healthcare reforms that reward preventive dentistry and insurance packages that include implant coverage. Clinics in Bogotá and Medellín use competitive pricing—often 50–70% below North American tariffs—to bolster international patient volumes. The influx of foreign exchange finances investment in CBCT, implant-surgery motors and intraoral scanners, positioning Colombia to gradually upgrade from mid-tier to premium equipment segments.

Competitive Landscape

Global firms such as Dentsply Sirona, Straumann Group and Envista Holdings dominate sophisticated product niches, leveraging embedded software ecosystems and robust training platforms. Regional specialists like Dental Morelli and Gnatus Equipamentos match competitive price points in entry-level chairs and compressors, while maintaining local service networks prized by budget-constrained clinics. The blended landscape drives continuous product iteration—illustrated by Straumann’s Virtuo Vivo scanner gains in Brazil, Chile and Peru.

Strategic moves show a pivot toward digital integration. Envista invested USD 25 million in clinician-education hubs, reinforcing loyalty to its DTX Studio suite. Henry Schein’s BOLD+1 plan diversifies sourcing to hedge tariff exposure and channels savings into in-house practice-management software. Start-ups specializing in AI-powered radiographic triage partner with established distributors to piggy-back on installed fleets, injecting fresh competition into the Latin American dental equipment market.

M&A remains selective: larger players eye regional manufacturers for faster ANVISA pathways, while local firms court outside funding to expand into diagnostics. Overall, rivalry centres on bringing end-to-end digital workflows under a single brand umbrella—a differentiation that resonates with DSOs standardizing technology stacks across multiple Latin American countries.

Latin America Dental Devices Industry Leaders

3M

Dentsply Sirona

Straumann Group

Zimmer Biomet

Dentium

- *Disclaimer: Major Players sorted in no particular order

Latin America Dental Devices Market Companies Covered in this Report

- Dentsply Sirona

- Straumann Group

- Envista Holdings Corp.

- Align Technology

- Planmeca

- 3M Oral Care

- Ivoclar Vivadent

- Carestream Dental

- A-dec

- GC Corporation

- Coltene Holding

- Vatech Co. Ltd.

- BIOLASE Inc.

- Osstem Implant Co. Ltd.

- Henry Schein

- Dental Morelli Ltda.

- Alliage SA

- Gnatus Equipamentos

- S.I.N. Implant System

- FGM Dental Group

- Bionnovation Biomedical

Recent Industry Developments in Latin America Dental Devices Market

- January 2026: São Paulo's CIOSP (International Dental Congress of São Paulo) 2026 attracted over 100,000 attendees and hundreds of exhibitors. The presence of numerous local implant manufacturers highlighted Brazil's advanced dental manufacturing capabilities.

- December 2024: Straumann Group opened Costa Rica operations, extending its footprint beyond Mexico, Colombia and Chile.

- May 2024: ArcomedLab reached 700 craniomaxillofacial implants using PEEK and titanium 3-D printing, partnering with Latin American universities.

Latin America Dental Devices Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the Latin America dental devices market as all professional equipment and consumables, diagnostic imaging units, CAD/CAM systems, lasers, implants, biomaterials, handpieces, and related accessories sold to clinics, hospitals, and teaching centers across Brazil, Mexico, Argentina, Chile, Peru, and neighboring nations.

Scope exclusion: over-the-counter oral-care goods, home-use whitening kits, and stand-alone dental services are not assessed.

Segments Covered in This Report

- By Product

- General and Diagnostics Equipment

- Dental Laser

- Soft Tissue Lasers

- Hard Tissue Lasers

- Radiology Equipment

- Extra Oral Radiology Equipment

- Intra-oral Radiology Equipment

- Dental Chair and Equipment

- Other General and Diagnostic equipment

- Dental Laser

- Dental Consumables

- Dental Biomaterial

- Dental Implants

- Crowns and Bridges

- Other Dental Consumables

- Other Dental Devices

- General and Diagnostics Equipment

- By Treatment

- Orthodontic

- Endodontic

- Peridontic

- Prosthodontic

- By End User

- Dental Hospitals

- Dental Clinics

- Academic & Research Institutes

- By Country

- Brazil

- Mexico

- Argentina

- Chile

- Peru

- Rest of Latin America

Data Sources, Market Sizing, and Validation

Primary Research

We interviewed prosthodontists, clinic procurement heads, and distributors in Brazil, Mexico, and Colombia to refine procedure volumes, ASP shifts, and regulatory bottlenecks. Short surveys among younger orthodontists confirmed rising intra-oral scanner adoption.

Desk Research

Our team begins with high-integrity public data from PAHO disease surveys, national customs dashboards, UN Comtrade, and ministries of health, enhancing these with annual reports and clinical papers that track digital dentistry uptake. Paid repositories such as D&B Hoovers, Dow Jones Factiva, and Questel's patent analytics widen the lens, while bulletins from regional dental associations supply shipment hints. The sources named are illustrative; many additional references underpin the dataset.

Market-Sizing & Forecasting

A top-down model converts import values and local production counts into unit volumes and weighted prices, then aligns them with treated patient pools drawn from caries and edentulism prevalence. Select bottom-up supplier roll-ups and channel checks, this is where Mordor Intelligence cross-checks numbers, adjust segment totals. Key drivers tracked include dentist-per-capita ratios, chair utilization, elective implant penetration, currency-adjusted ASP trends, and reimbursement ceilings. A multivariate regression projects demand, and scenario analysis stress-tests exchange-rate and tourism swings. Gaps such as informal imports are bridged through expert-agreed heuristics.

Data Validation & Update Cycle

Outputs pass variance checks against historical series and new filings before double-layer analyst review. Reports refresh annually, with interim updates for material policy or macro events, so clients always receive the latest view.

How Mordor Intelligence's Latin America Dental Devices Market Size Compares to Other Published Estimates

Published figures vary because publishers mix device groups, apply different price deflators, and refresh at uneven intervals. We flag these factors so users grasp the roots of divergence.

Differences most often stem from whether consumables are counted, how gray-market inflows are handled, and if the 2025 post-pandemic ordering spike is treated as structural. Mordor Intelligence covers the full mix, normalizes prices, and refreshes yearly; some consultancies rely on two-year-old shipment surveys or track equipment only.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.74 Bn (2025) | Mordor Intelligence | - |

| USD 1.47 Bn (2024) | Global Consultancy A | List prices used; smaller clinics in Peru omitted |

| USD 2.80 Bn (2024) | Industry Association B | Includes consumer whitening kits; growth projected from import CAGR only |

In short, Mordor's disciplined scope choice, blended modeling, and rapid refresh give stakeholders a dependable, transparent baseline.

Key Questions Answered in the Report

What is the value of the Latin American dental equipment market in 2026?

The market stands at USD 770 million in 2026.

How fast is the market expected to grow through 2031?

It is projected to expand at a 4.46% CAGR, reaching USD 960 million by 2031 during the forecast period (2026-2031).

Which product segment currently generates the most revenue?

Dental consumables lead with 55.12% of total revenue in 2025.

Which country will post the quickest growth between 2026 and 2031?

Colombia is forecast to register a 6.95% CAGR, making it the region’s fastest-growing market during 2026-2031.

What role does currency volatility play in equipment purchases?

Exchange-rate swings inflate prices of imported high-value devices such as CBCT scanners, often delaying large capital purchases.

Which technologies are set to drive future demand?

• Chairside CAD/CAM systems, 3-D printers, AI-enabled imaging, and portable devices linked to teledentistry platforms are expected to underpin growth.

Page last updated on: