Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

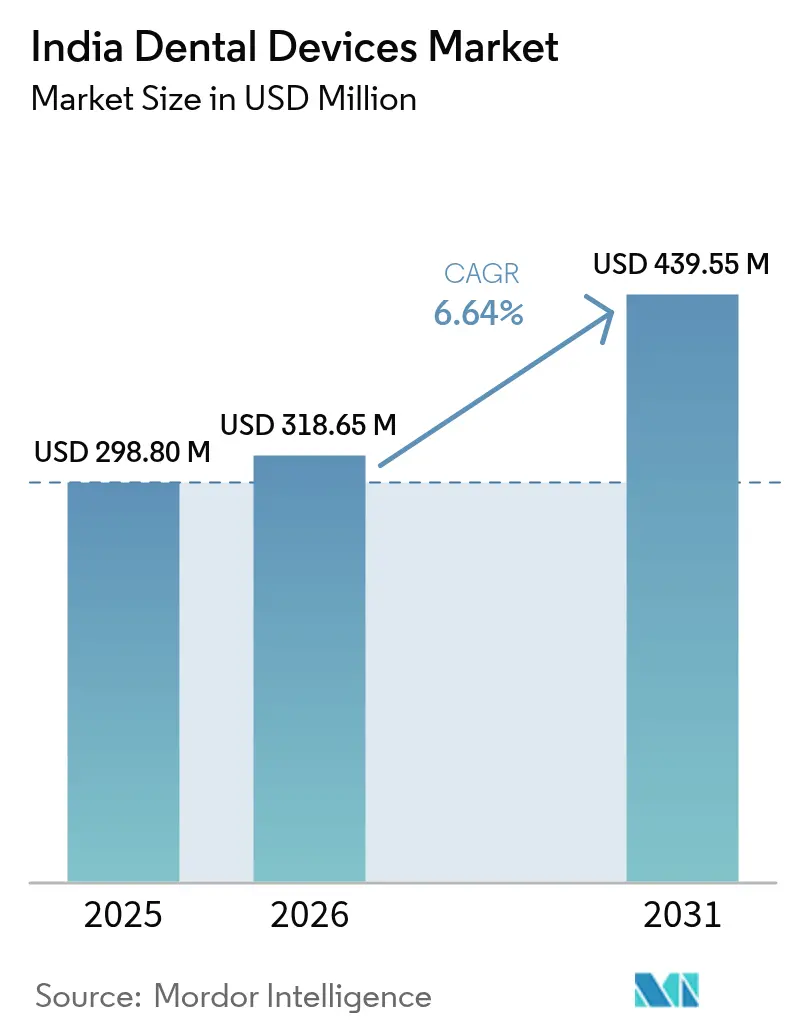

| Base Year Market Size (2025) | USD 298.80 Million |

| Market Size (2026) | USD 318.65 Million |

| Market Size (2031) | USD 439.55 Million |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Dental Devices Market Analysis by Mordor Intelligence

The India dental devices market size in 2026 is estimated at USD 318.65 million, growing from 2025 value of USD 298.80 million with 2031 projections showing USD 439.55 million, growing at 6.64% CAGR over 2026-2031. Continued growth reflects rising oral-health awareness, strengthening disposable incomes and an improving care-delivery infrastructure that extends from metropolitan hubs to semi-urban clusters. The India dental devices market is also benefiting from the government’s Production-Linked Incentive scheme, which is spurring domestic manufacturing capacity and lowering import dependence. Rapid adoption of digital workflows—particularly CAD/CAM milling, intra-oral scanning and 3-D printing—reinforces demand for precision equipment and premium consumables, while expanded social-media influence is lifting aesthetic procedures among urban millennials. Dental-tourism inflows into Goa and Karnataka are adding high-value procedure volumes, although inconsistent GST classification and a shortage of certified dental technicians still inhibit optimal growth trajectories for the India dental devices market.

Key Report Takeaways

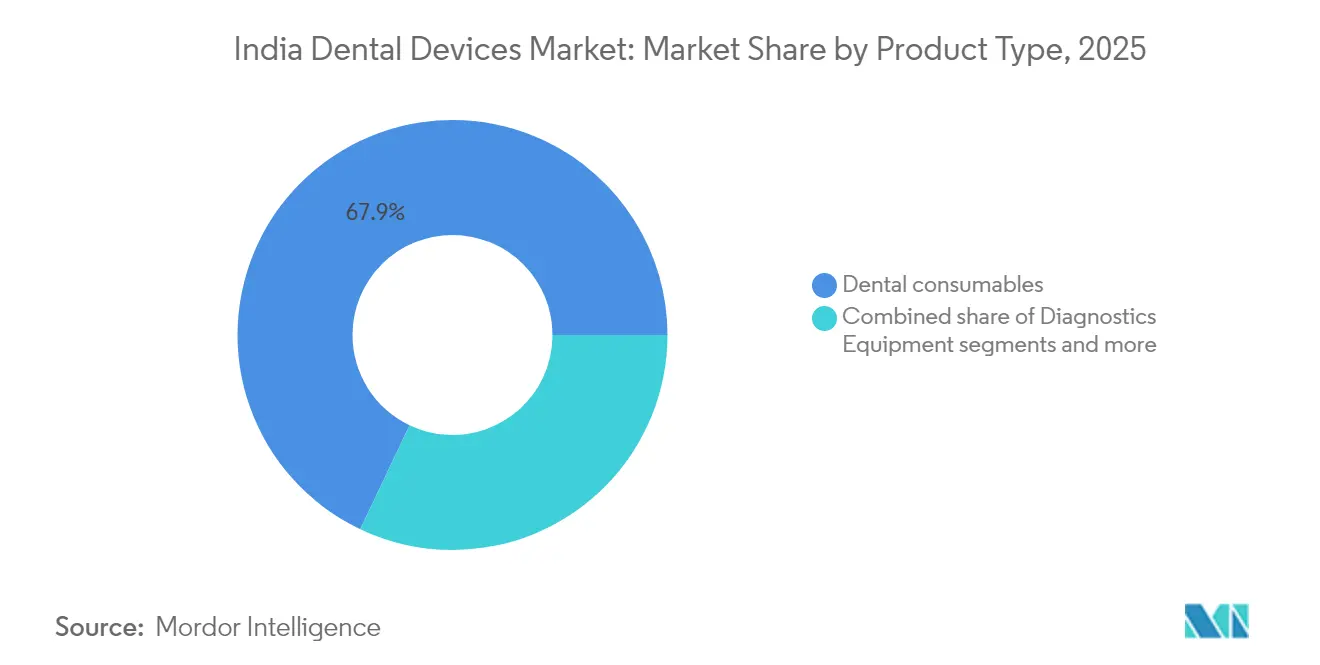

- By Product, dental consumables led with a 67.94% revenue share of the India dental devices market in 2025, while dental equipment is projected to advance at a 12.67% CAGR to 2031, the fastest growth among all product categories in the India dental devices market.

- By treatment, prosthodontic treatments captured 33.12% of the India dental devices market share in 2025, while orthodontic treatments are poised for a 13.44% CAGR through 2031.

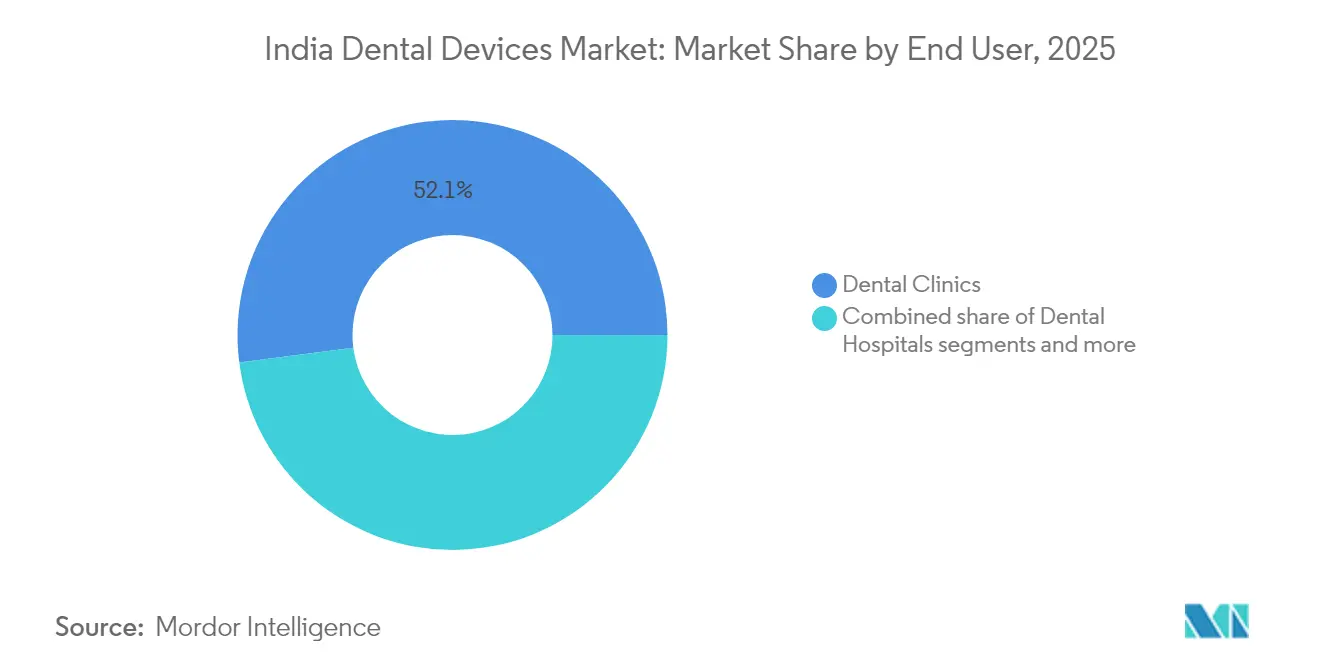

- By end user, dental clinics commanded 52.05% of the India dental devices market size in 2025 and are expected to grow at a 13.18% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Dental Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led National Oral Health Programme Raising Preventive Visits | +3.0% | National, with emphasis on underserved regions | Medium term (2-4 years) |

| Urban Millennials' Cosmetic Dentistry Boom Fueled by Social Media | +2.6% | Major metropolitan areas, tier-1 and tier-2 cities | Short term (≤ 2 years) |

| Ayushman Bharat & Private Dental Insurance Expanding Affordability | +2.0% | National, with initial impact in urban centers | Medium term (2-4 years) |

| Dental Tourism Hot-Spots in Goa & Karnataka Driving High-Value Procedures | +1.6% | Concentrated in Goa, Karnataka, Kerala, and Delhi NCR | Medium term (2-4 years) |

| PLI Scheme Catalyzing Domestic Manufacturing of Dental Equipment | +1.4% | National, with manufacturing hubs in Gujarat, Tamil Nadu, Karnataka | Long term (≥ 4 years) |

| Rapid Chair-side CAD/CAM & Intra-oral Scanner Adoption by Clinics | +1.3% | Urban centers and tier-1 cities, expanding to tier-2 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-led National Oral Health Programme Raising Preventive Visits

The National Oral Health Programme has undertaken 32.80 crore oral-cancer screenings under Ayushman Bharat, reinforcing routine preventive check-ups across 1,75,338 Ayushman Arogya Mandirs nationwide. This scale-up is fostering sustained demand for portable diagnostic devices that match rural deployment needs while remaining cost-efficient for public procurements. Standardized electronic health-record protocols within the Ayushman Bharat Digital Mission further stimulate adoption of digital imaging and chairside documentation systems, helping manufacturers of integrated equipment platforms secure multi-year procurement contracts. Although infrastructure gaps linger in remote districts, the momentum of state-wise roll-outs is expected to permeate smaller practices, thereby broadening the India dental devices market over the medium term.

Urban Millennials’ Cosmetic Dentistry Boom Fueled by Social Media

Urban millennials increasingly view dental care as an element of personal branding, accelerating elective procedures such as clear-aligner therapy and digital smile-design workflows. A recent cross-sectional study reported significantly higher awareness (41.22) and perception (42.18) scores for aligners among dental students compared with medical and paramedical peers, underscoring the readiness of future practitioners to champion aesthetic solutions. For manufacturers, this trend translates into brisk sales of high-translucency ceramic brackets, customized aligner workflows and chairside milling units that enable same-day veneers. Intensified social-media advertising, however, places pressure on clinics to consistently meet appearance-oriented expectations, making quality differentiation through advanced imaging and precise restorative materials critical to retaining clientele within the India dental devices market.

Ayushman Bharat & Private Dental Insurance Expanding Affordability

Ayushman Bharat has authorized 8.39 crore hospital admissions, providing a gateway for gradually integrating outpatient dental benefits. Private insurers are experimenting with limited OPD riders, but current penetration remains narrow, often covering only emergency oral-surgical admissions. Leading corporate chains have responded by offering bundled subscription plans and zero-interest payment options; Sabka Dentist’s network of 100 clinics has already delivered 10 million patient visits under such flexible models. Device suppliers that tier product lines across varying price points are better positioned to align with evolving reimbursement thresholds, expanding the addressable base of the India dental devices market across income segments.

Dental-Tourism Hot-Spots in Goa & Karnataka Driving High-Value Procedures

Goa and Karnataka routinely offer restorative and implant treatments at 80-90% lower fees than Western countries, enticing inbound patients seeking quality care at reduced costs. These states combine robust hospitality infrastructure with NABH-accredited clinics, attracting international clientele for full-mouth rehabilitation packages. The inflow is catalyzing demand for premium implant systems, high-strength zirconia blocks and advanced CBCT imaging units that meet international accreditation standards. Telerehabilitation follow-ups reduce revisit requirements, further increasing treatment volumes and enhancing the export earnings potential of the India dental devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortfall of Formally-Trained Dental Technicians | -1.8% | National, more severe in tier-2/3 cities and rural areas | Long term (≥ 4 years) |

| High Import Dependency Exposing Prices to INR/US$ Volatility | -1.7% | National, with greater impact on premium segment providers | Medium term (2-4 years) |

| Fragmented Single-Chair Clinic Base Limiting Cap-Ex Uptake | -1.5% | National, particularly in tier-2/3 cities and rural areas | Medium term (2-4 years) |

| Inconsistent GST Classification Raising Compliance Costs | -1.3% | National, with greater impact on SMEs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inconsistent GST Classification Raising Compliance Costs

Variable GST slabs and inverted-duty structures complicate supply-chain planning, especially for small and mid-sized manufacturers that frequently straddle multiple product codes. A recent Standing Committee report highlighted how inverted duties inflate working-capital needs and hamper competitiveness for locally-made handpieces and impression materials. For distributors, inconsistent input-tax credits slow inventory turnover, raising channel margins and ultimately equipment prices. The dental-trade associations continue lobbying for slab rationalization, but until harmonization materializes, compliance overheads are expected to temper profitability across the India dental devices market.

Shortfall of Formally-Trained Dental Technicians

India produces approximately 2,700 dental-laboratory technicians annually against an estimated requirement of 9,000, reinforcing a capacity bottleneck for precision prosthetics and orthodontic appliance fabrication. Curriculum shortfalls in CAD/CAM, 3-D printing and digital design restrict utilization of advanced milling centers to urban hubs where talent pools are concentrated. Equipment manufacturers have begun sponsoring chairside-assistant courses and technician apprenticeships, yet a nationwide upskilling agenda remains essential for full diffusion of digital workflows—particularly in tier-2 cities that represent the next expansion frontier for the India dental devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Digital Technologies Reshape Workflows

Dental consumables retained a 67.94% revenue share in 2025, driven by their recurrent usage pattern across routine and specialized cases. Equipment, however, is expected to climb at a 12.67% CAGR to 2031, the fastest pace within the India dental devices market. The shift stems from widespread deployment of chairside CAD/CAM mills, whose local assembly costs have fallen nearly 25% since domestic component sourcing under the PLI scheme began. The India dental devices market size for digital scanners reached USD 0.12 billion in 2025 and is projected to exceed USD 0.25 billion by 2031 as clinics pursue impression-free workflows. Innovative consumables such as bioactive restorative materials and nano-hydroxyapatite-enhanced composites are supporting value growth even as unit prices remain competitive.

Parallel advances within therapeutic equipment include electrosurgery units and sonic irrigation systems that quicken soft-tissue management, although penetration remains limited to multi-chair practices in metropolitan areas. Diagnostic gear, particularly panoramic and CBCT systems, is recording double-digit adoption as government screening initiatives and dental-tourism requirements emphasize radiographic accuracy. Domestic manufacturers have responded by scaling output; Dantech Digital Dental Solutions lifted daily prosthetic-manufacturing capacity from 200 to 1,000 units in 2025, demonstrating the maturation of India-based production ecosystems.

By Treatment: Aesthetics Drive Orthodontic Growth

Prosthodontics accounted for 33.12% of India dental devices market size in 2025, reflecting high edentulism rates among ageing cohorts. Orthodontics, however, is poised for a 13.44% CAGR to 2031, propelled by aligner adoption and peer-to-peer social validation. The India dental devices market share for aligner-supported orthodontics stood at 14.35% of total orthodontic spending in 2025 and is expected to surpass 23.6% by 2031 as product costs decline and financing options proliferate. Although some clinicians still debate the efficacy of aligners in complex malocclusions, hybrid protocols that combine limited fixed appliances with aligner finishing are broadening case applicability.

Endodontics remains a stable mid-growth segment, buoyed by single-visit root-canal techniques that employ rotary nickel-titanium files and warm vertical obturation units. Periodontics is gaining incremental traction through heightened awareness of oral-systemic links; surveys published in 2024 indicated that more than 45% of adults assessed in metropolitan screening camps exhibited some form of periodontal disease. Device makers offering ultrasonic scalers with built-in antimicrobial irrigation reservoirs find ready acceptance among periodontal specialists aiming to elevate maintenance therapy standards within the India dental devices market.

By End User: Corporate Chains Transform Clinic Segment

Dental clinics dominated with 52.05% of India dental devices market share in 2025 and are forecast to record a 13.18% CAGR through 2031. Corporate chains such as Clove Dental plan to scale to 100 sites in Mumbai and 30 in Ahmedabad by 2026, accelerating standardization of procurement protocols. Cluster-based expansion underpinned by centralized procurement grants suppliers streamlined access to high-volume accounts, though competitive tendering compresses margins. The India dental devices market size attributable to clinic chains is estimated at USD 0.16 billion in 2025 and could cross USD 0.29 billion by decade-end if current growth momentum holds.

Dental hospitals, while accounting for a smaller revenue slice, exert higher equipment intensity per chair, especially for advanced imaging and surgical suites. Academic institutions, through curriculum reforms such as the 2025 Research & Innovation Catalyst course, are embedding digital-dentistry competencies among undergraduates, thereby fostering early adopter culture for intra-oral scanning and in-office printing solutions. Vendors who invest in collaborative training programs with universities strengthen brand familiarity and future sales pipelines within the India dental devices market.

Geography Analysis

Metropolitan clusters—Delhi NCR, Mumbai, Bengaluru, Chennai and Hyderabad—command the lion’s share of premium equipment demand, underpinned by higher disposable incomes and dense specialist concentrations. Clove Dental’s footprint grew from 6 to 19 clinics in Ahmedabad during 2024, illustrating the pace at which organized players are penetrating tier-1 cities. Southern states, notably Karnataka and Kerala, have evolved into innovation hubs and dental-tourism magnets, buoyed by favorable state policies and proximity to quality technical institutes. Goa’s economic-diversification policy explicitly identifies medical tourism, including dental procedures, as a strategic growth pillar.

Western states such as Maharashtra and Gujarat benefit from industrial clusters that spur disposable incomes and private-insurance uptake, helping propel equipment sales in urban and peri-urban geographies. Conversely, rural belts grapple with infrastructural deficits despite the commissioning of 163,000 Health & Wellness Centres under Ayushman Bharat by December 2023. Teledentistry pilots funded by state governments are mitigating specialist shortages, allowing remote diagnosis and chairside guidance that, in turn, spurs procurement of portable radiovisiography units and cloud-enabled practice-management software.

Regulatory Landscape

Dental devices in India are regulated under the Drugs and Cosmetics Act, 1940 and the Medical Devices Rules, 2017. The framework uses risk-based classification (Class A to D) and requires licensing and registration overseen by CDSCO and the Ministry of Health and Family Welfare (MoHFW). Importers and manufacturers submit applications through the Online System for Medical Devices (OSDM) portal, which supports device registration and license applications and is being expanded through new online provisions.

In April 2026, MoHFW issued draft Medical Devices (Amendment) Rules, 2026 (G.S.R. 270(E)), proposing changes that tighten quality and traceability expectations. The draft includes updates around sterilization labeling and QMS compliance coverage for lower-risk categories. In June 2026, MoHFW also proposed reducing manufacturing license processing timelines for high-risk Class C and Class D devices, from 105 days to 90 days, aligning approvals with faster market entry for advanced equipment used in imaging, implantology, and surgical dentistry.

Value Chain Analysis

The India dental devices value chain starts with raw materials and precision components (metals, ceramics, polymers, electronics, and imaging subsystems), then moves through device design and manufacturing. It then progresses to QA/QMS and regulatory clearance under the Medical Devices Rules, 2017, followed by importation or domestic distribution into clinics, hospitals, and academic institutions. Advanced equipment categories, including digital imaging and CAD/CAM systems, rely more heavily on imported sub-assemblies, while consumables and selected small equipment lines draw from a broader domestic supplier base supported by industrial clusters and policy programs.

Commercialization is carried out via a multi-layer distribution network that includes national and regional dealers, institutional sales to corporate dental chains, and a growing B2B e-commerce layer that aggregates SKUs and improves last-mile reach for clinics outside major metros (for example, Dentalkart). On the demand side, procurement intensity is shaped by clinic consolidation and standardized purchasing at the chain level, while public-sector procurement is influenced by programs such as the National Oral Health Programme under the National Health Mission. Key friction points include compliance documentation and licensing throughput for regulated categories, working-capital pressure from GST classification variability, and the shortage of formally trained dental technicians that limits utilization of advanced lab and digital workflows beyond major urban hubs.

Competitive Landscape

The India dental devices market is moderately fragmented. Global majors—Dentsply Sirona, 3M India and Envista—capitalize on wide portfolios and established dealer networks to dominate premium implants, imaging and restorative segments. Domestic challengers leverage cost efficiencies; Laxmi Dental's IPO in January 2025 aimed to raise INR 698 crore for capacity expansion, signaling investor confidence in integrated, made-in-India supply chains. Digital adoption is an increasingly decisive differentiator: Dentalkart, an e-commerce platform hosting 22,000 SKUs, secured INR 85 crore in December 2024 to upgrade logistics and widen manufacturer reach.

Strategic alliances are on the rise. Geistlich's April 2025 acquisitions in Brazil and France reflect a push to enlarge biomaterials portfolios for emerging markets, including India. Multinationals often partner with local distributors for last-mile reach, while domestic firms sign technical-know-how agreements to upgrade product lines. In March 2024, the Production-Linked Incentive scheme inaugurated 13 device plants that anchor backward integration for consumables and small equipment and are reshaping supply cost dynamics; competition is most intense in consumables due to price sensitivity while brand loyalty remains strong for implants and endodontic files where clinical outcomes directly influence practitioner choice; and Clove Dental accelerated expansion toward 100 clinics in Mumbai and 30 in Ahmedabad.

India Dental Devices Industry Leaders

3M

Dentsply Sirona

GE Healthcare

Philips Healthcare

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Public procurement and primary-care deployment offer a concrete opportunity area, anchored in the National Oral Health Programme (NOHP) operating through National Health Mission processes. These channels fund equipment such as dental chairs and X-ray units for public facilities. As Ayushman Bharat scales preventive touchpoints through Ayushman Arogya Mandirs, suppliers that package portable diagnostics, digital documentation, and ruggedized equipment configurations for government tendering have a clearer path to volume placements, with downstream pull for restorative and endodontic workflows.

Adoption of premium devices and digital dentistry is also increasingly tied to standardization and skills development. In March 2026, India established the National Dental Commission, replacing the Dental Council of India, which strengthens oversight of education, ethics, and institutional quality. That change can improve readiness for CAD/CAM, imaging, and digital orthodontic workflows where trained operators are a key constraint. Outside major metros, private-sector whitespace remains visible in tier-2/3 cities, where fragmented single-chair practices limit capex and technician availability constrains lab throughput. Bundled plans and subscription-style affordability used by organized clinic networks create room for tiered equipment and consumables portfolios that fit price sensitivity while still supporting digital workflow adoption.

Recent Industry Developments

- May 2026: Laxmi Dental Limited launched i-Scope360, an AI-connected platform for remote patient dental monitoring in India. The introduction supports digitally enabled follow-ups and can increase utilization of connected intraoral and restorative workflows across distributed clinic footprints.

- May 2025: Clove Dental accelerated its West India expansion plan, targeting 100 clinics in Mumbai and 30 clinics in Ahmedabad by 2026. Larger standardized clinic networks strengthen centralized procurement, influencing channel strategies for imaging systems, chairs, and high-throughput consumables.

- January 2025: Laxmi Dental launched an INR 698 crore IPO to fund manufacturing capacity expansion and debt reduction. The fundraising underscored investor backing for made-in-India dental manufacturing and added momentum to localized production and supply-chain integration efforts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the India dental devices market is defined as the value of dental equipment, instruments, and consumables used for diagnosis, treatment, and restoration in dental care settings within India.

Scope exclusions: Purchases meant for personal home-use are excluded, as are any non-dental medical devices not used for oral procedures.

Segmentation Overview

- By Product

- General and Diagnostic Equipment

- Dental Lasers

- Soft Tissue Dental Lasers

- Hard Tissue Dental Lasers

- Radiology Equipment

- Dental Chair and Equipment

- Other General and Diagnostic Equipment

- Dental Lasers

- Dental Consumables

- Dental Biomaterial

- Dental Implants

- Crowns and Bridges

- Other Dental Consumables

- Other Dental Devices

- General and Diagnostic Equipment

- By Treatment

- Orthodontic

- Endodontic

- Periodontic

- Prosthodontic

- By End User

- Dental Hospitals and Clinics

- Academic and Research Institutions

- Other End Users

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the India dental care backdrop and to collect practical inputs that shape demand and pricing. Inputs were gathered from public sources such as Ministry of Health and Family Welfare releases, National Health Accounts, Ministry of Commerce and Industry trade statistics, official customs and tariff lines for relevant dental imports, and publications from dental councils and dental associations.

To reduce reliance on one data stream, we also reviewed company annual reports, investor presentations, product catalogs, and credible news coverage that points to clinic expansion, technology adoption, and price movements. In a few places, paid subscriptions were used only to cross-check company financials, patent activity, and shipment-level trade patterns where public disclosures were thin. These are not exhaustive, and other public and paid references were used to compile data, validate it, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating what is actually purchased and used across India, since channel structures and procedure mix can vary by city tier and care setting. We spoke with a mix of dental clinic administrators, procurement staff, distributors, and domain experts to confirm typical replacement cycles, pricing ranges, and how quickly digital dentistry tools are being adopted.

To keep assumptions grounded, we compared responses across major regions and across different facility types. Any outlier inputs were rechecked before being used in the final sizing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 18% | |

| Mid tier: 45% | Functional/Unit leaders: 37% | |

| Smaller Players: 21% | Managers: 45% |

Market-Sizing & Forecasting

Sizing was built using a mix of top-down and bottom-up logic so the totals remain grounded in real demand signals and can still be replicated. On the top-down side, we reconstructed the addressable pool using India dental care activity and supply indicators (clinic base growth, procedure mix, import intensity for key device groups, and typical replacement cycles), then translated those into spend by applying realistic price bands.

The totals were corroborated with selective bottom-up approximations where available, such as sampled distributor throughput checks and a limited roll-up of supplier revenues for products that are widely reported. These inputs helped adjust for gaps when direct visibility was uneven. Key model inputs included the share of procedures needing restorative and orthodontic supplies, adoption rates for imaging and CAD/CAM workflows, installed base of chairs and major equipment, average selling price movement by product group, and the split of demand between private clinics and institutional settings.

For forecasting, scenario analysis was used with a base case guided by expert views on clinic additions, premium procedure growth, and import and domestic supply shifts, then stress-tested with slower and faster adoption paths for higher-value equipment categories. Where bottom-up data was incomplete, conservative ranges were applied and then narrowed using interview-confirmed ranges so the final time series stayed consistent year to year.

Data Validation & Update Cycle

Validation was done through multiple checks so the market does not overreact to a single data point. Model outputs were compared against independent signals like trade movement direction, pricing commentary from channels, and changes in procedure demand seen by practitioners, and any large variance was investigated before finalizing.

Before sign-off, the work is reviewed in steps, where assumptions, conversions, and math checks are re-run, and the logic is challenged across categories that can be easily double-counted. Reports are refreshed annually, and if there is a material event (policy change, sharp currency movement, or demand disruption), key inputs are revisited and sources are re-contacted to confirm whether the impact should be reflected earlier. Right before delivery, a final review pass is completed so clients receive the most current view available.

Mordor Intelligence's India Dental Devices Market Estimate Compared With Other Published Estimates

Published market sizes for India dental devices can differ widely, even when the sources appear to cover the same space. The gaps typically come from what is counted as a dental device, which end-use settings are included, what year is treated as the current baseline, and how pricing is converted into USD.

The table shows a wide spread largely because some sources bundle a broader dental products basket or use a different base-year boundary, while only dental devices and consumables used in hospitals and clinics are counted in Mordor Intelligence's model. This avoids adding adjacent retail and non-clinical spends that can inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 318.65 M (2026) | |

| Industry Research Publisher A | USD 408.40 M (2024) | This figure is positioned as dental equipment only with a 2024 base year, so it can move higher on equipment-heavy mixes and is not aligned to a 2026 current-year view or a devices plus consumables scope. |

| Industry Research Publisher B | USD 1.10 B (2024) | This estimate appears to aggregate a wider dental devices basket and can include additional categories and end users beyond clinics and hospitals, which expands the counted spend compared with a tighter clinical-use definition. |

Taken together, the comparison points to scope and timing as the biggest drivers of the gap, followed by what gets treated as equipment-only versus a broader products bundle. By keeping inputs tied to clinic and hospital usage signals and then cross-checking them with channel feedback, the final number stays transparent, repeatable, and easier to reconcile with real purchasing behavior.

Key Questions Answered in the Report

What is the current India dental devices market size?

The India dental devices market size stands at USD 318.65 million in 2026.

How fast will the India dental devices market grow by 2031?

The market is projected to reach USD 439.55 million by 2031, reflecting a 6.64% CAGR.

Which product segment is expanding the quickest? Dental equipment, propelled by digital technologies, is forecast to rise at a 12.67% CAGR between 2026-2031.

Which product segment is expanding the quickest? Dental equipment, propelled by digital technologies, is forecast to rise at a 12.67% CAGR between 2026-2031.

Why are orthodontic devices gaining traction in India?

Rising aesthetic awareness among urban millennials and the convenience of clear-aligner therapy are expected to drive a 13.44% CAGR in orthodontic treatments.

Page last updated on: