Dental Anesthetics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

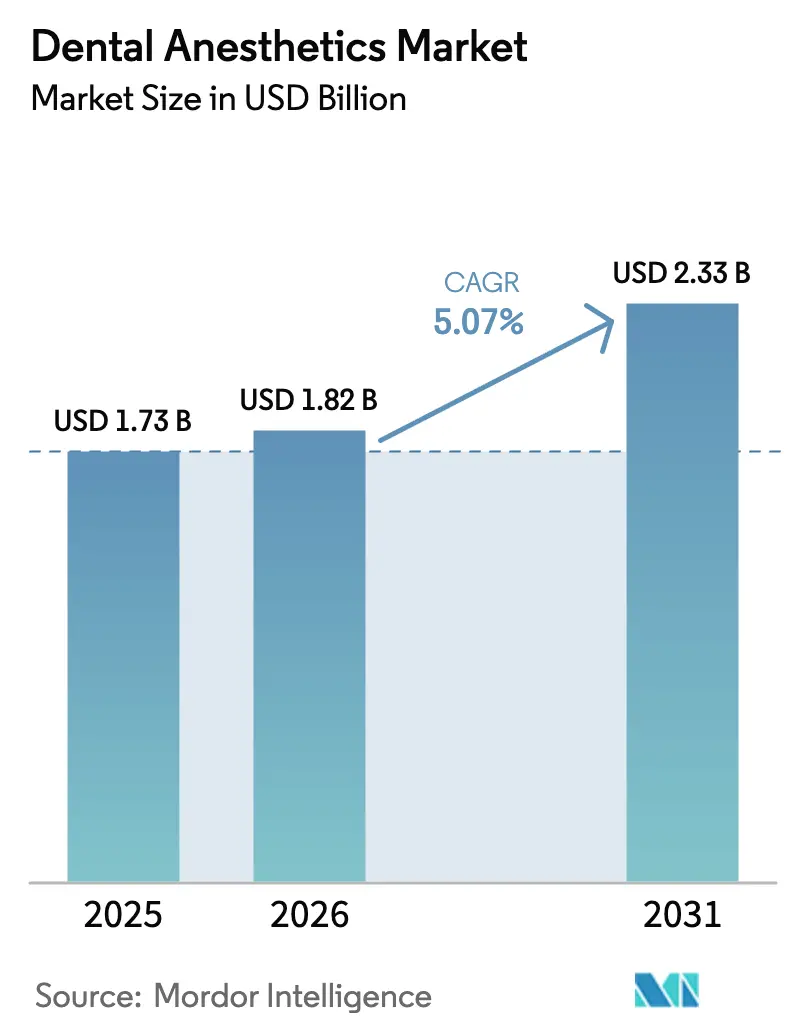

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.33 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Anesthetics Market Analysis by Mordor Intelligence

The dental anesthetics market size was valued at USD 1.73 billion in 2025 and estimated to grow from USD 1.82 billion in 2026 to reach USD 2.33 billion by 2031, at a CAGR of 5.07% during the forecast period (2026-2031). Steady expansion is linked to the global surge in oral disease, the mainstreaming of technology-enabled delivery systems, and broader access to quality dental care in emerging economies. Computer-controlled dosing, buffered formulations, and needle-free alternatives are changing long-standing clinical routines, while sustainability targets push manufacturers to curb nitrous oxide emissions. Demand for longer-acting local agents is rising as single-visit CAD/CAM procedures lengthen chair time. Geopolitical supply risks, highlighted by recent nitrous oxide shortages, encourage clinics to diversify sourcing and adopt lower-risk agents. Environmental policy, particularly in Europe, further accelerates the shift from high-impact inhalational gases toward greener analgesic options.

Key Report Takeaways

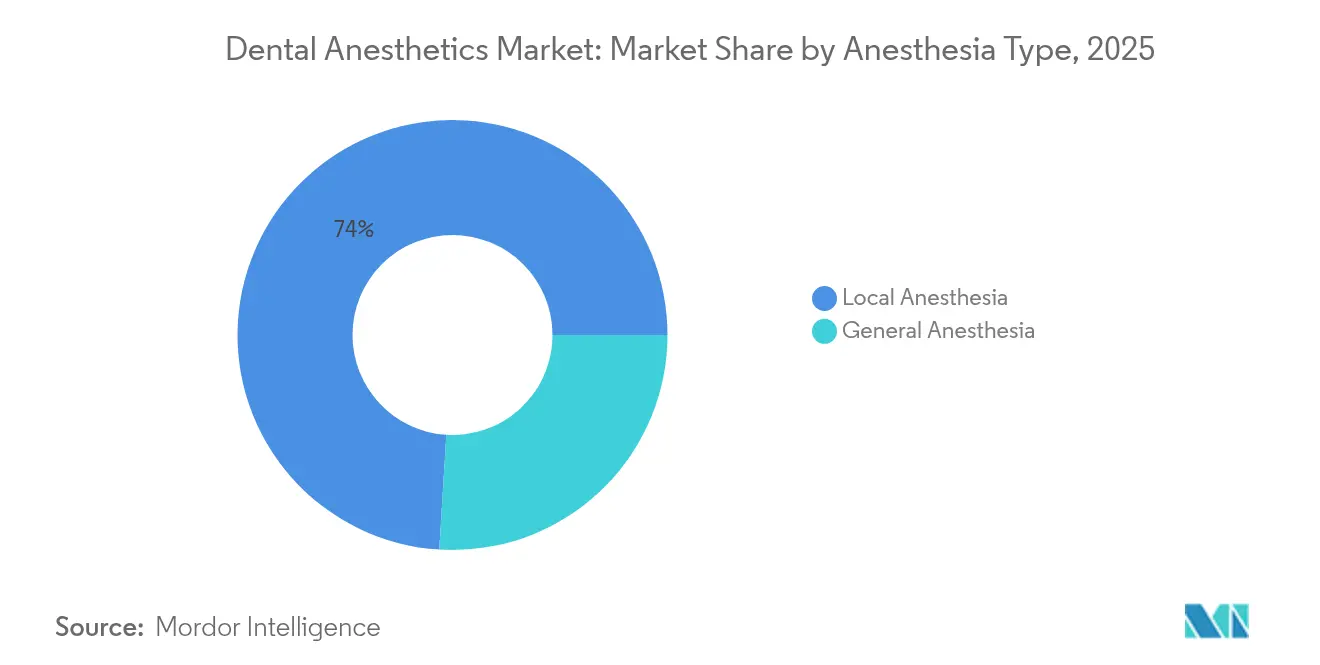

- By anesthesia type, local formulations led with 74.02% of the dental anesthetics market share in 2025; general anesthesia is poised for the fastest 7.31% CAGR through 2031.

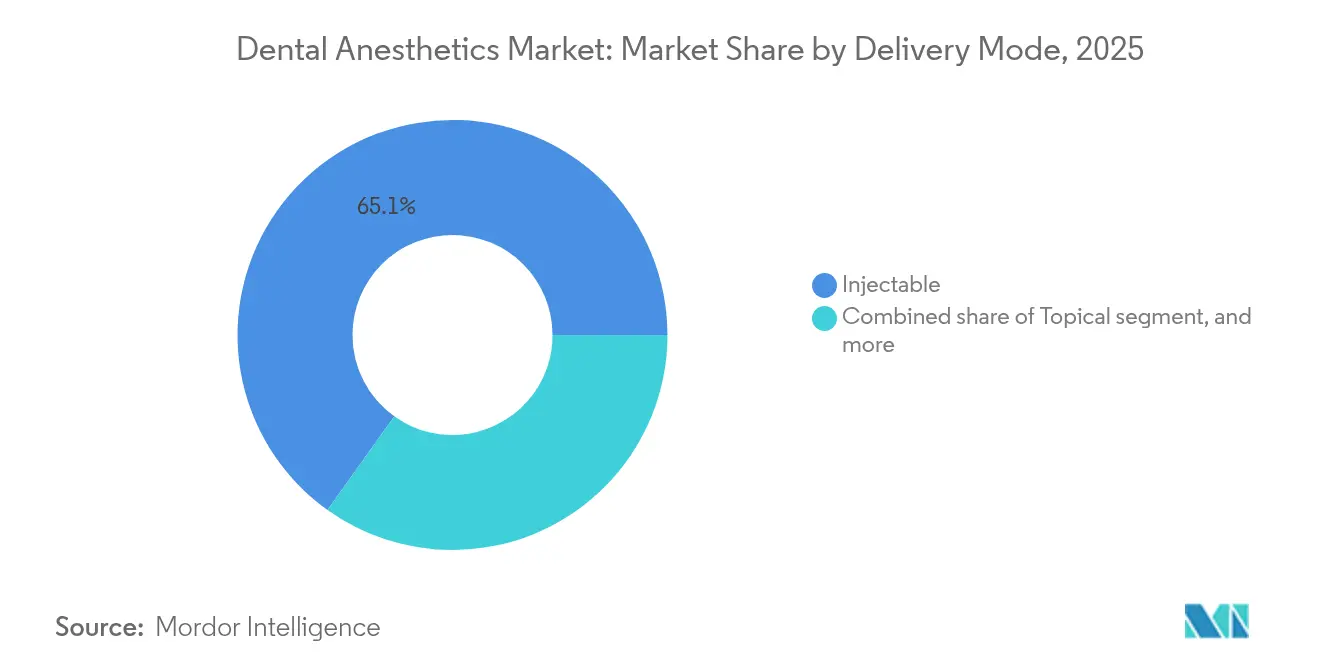

- By delivery mode, injectable products retained 65.12% of 2025 revenue, while computer-controlled local anesthetic delivery systems are set to expand at a 7.78% CAGR to 2031.

- By end-user, dental clinics accounted for 61.05% of 2025 revenue; ambulatory surgical centers will post the highest 8.29% CAGR through 2031.

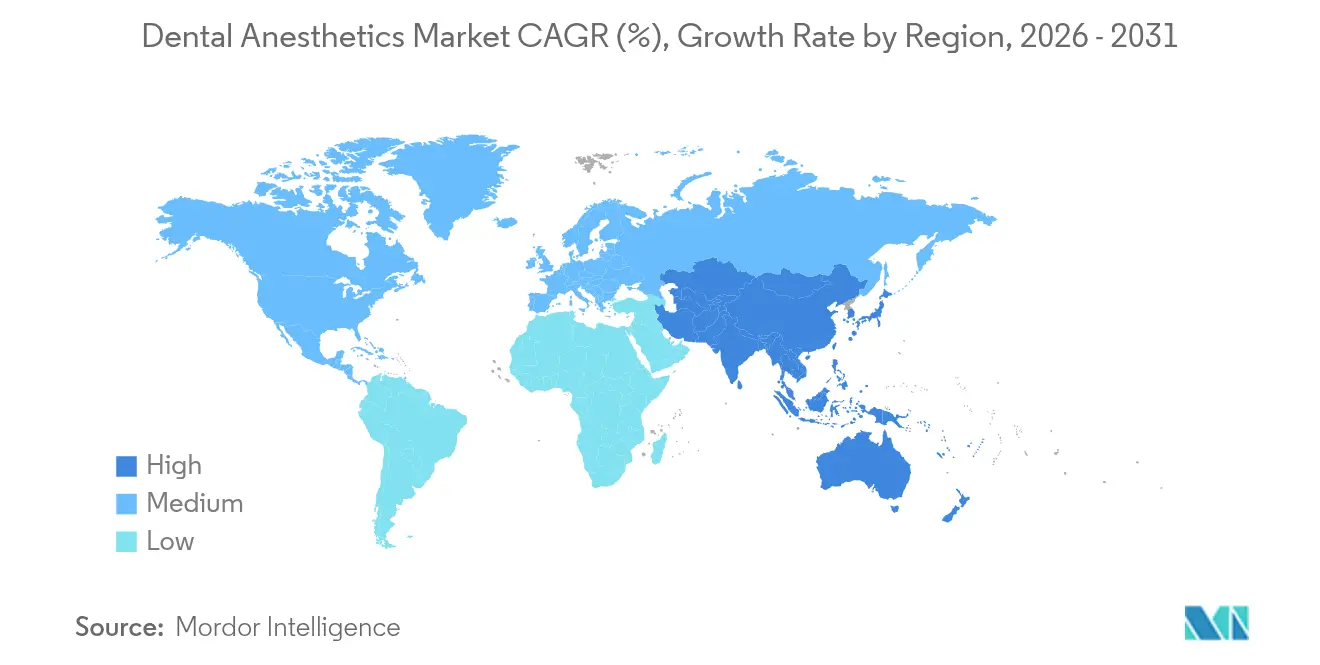

- By geography, North America held 41.72% of revenue in 2025, whereas Asia-Pacific is projected to register a 6.32% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Anesthetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of oral diseases worldwide | +1.2% | Global; strongest in Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Growing volume of dental surgical procedures | +1.0% | North America and Europe; expanding in Asia-Pacific | Medium term (2-4 years) |

| Expansion of cosmetic and aesthetic dentistry | +0.8% | North America and Europe; urban centers in Asia-Pacific | Medium term (2-4 years) |

| Increasing access to dental care in emerging economies | +1.1% | Core in Asia-Pacific; spill-over to Latin America and MEA | Long term (≥ 4 years) |

| Technological advancements in buffered and needle-free systems | +0.7% | Global; early adoption in North America | Short term (≤ 2 years) |

| Emergence of chairside analytics optimizing dosage and inventory | +0.4% | North America and Europe; gradual uptake in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Oral Diseases Worldwide

Global periodontal and caries prevalence surpasses 3.5 billion cases, generating sustained procedural volumes that rely on safe, rapid-acting anesthesia[1]World Health Organization, “Oral Health,” who.int. Lifestyle shifts in emerging markets heighten sugar intake and smoking rates, pushing younger cohorts toward earlier intervention cycles. The World Health Organization’s call for oral health inclusion in universal care programs expands subsidized treatment lists, further lifting anesthetic demand. Advanced 5.6% lidocaine aerosol has demonstrated significant pain reduction during periodontal debridement, enabling immediate treatment without waiting periods. Comorbidity links between diabetes, cardiovascular disease, and periodontitis require modified epinephrine concentrations, spurring therapeutic innovation. As refined analgesic protocols allow deeper and longer interventions, clinicians uncover latent pathology during the same session, creating a reinforcing treatment loop.

Growing Volume of Dental Surgical Procedures

Digitally guided implantology and CAD/CAM restorations permit multiple treatments in one sitting, lengthening anesthetic duration requirements. Older adults with implant-supported prostheses drive higher bone graft and sinus lift volumes, where articaine achieves 90% buccal infiltration success against 70% for traditional mepivacaine after failed nerve blocks[2]Journal of Conservative Dentistry and Endodontics, “Efficacy of Articaine Infiltration,” jcde.in. Ambulatory surgical centers favor anesthetic regimes that enable same-day discharge, reinforcing uptake of fast-wear-off agents with predictable recovery profiles. Full-arch implant workflows executed in a single visit necessitate mid-procedure top-ups, fuelling demand for computer-controlled systems that keep plasma levels within a narrow therapeutic window. Data-driven chairside analytics help calibrate doses based on patient weight and procedure time, minimizing toxicity risk while optimizing inventory.

Expansion of Cosmetic and Aesthetic Dentistry

Elective veneer, crown lengthening, and gum contouring procedures require absolute comfort and minimal tissue distortion for accurate shade and margin evaluation. Buffered lidocaine solutions reach physiologic pH, cutting injection pain scores by up to 50% and allowing preparation to begin within seconds. High-income urban patients share treatment experiences on social platforms, pressuring clinics to adopt needle-free devices that create a differentiating service narrative. Premium aesthetic practices deploy bundled comfort packages, blending topical spray, interactive sedation music, and computer-controlled delivery, which lifts referral rates and offsets higher per-procedure costs. As cosmetic caseloads grow, segment revenue becomes a reliable hedge against insurance reimbursement ceilings in general dentistry.

Technological Advances in Buffered and Needle-Free Delivery Systems

Roughly 58% of dental patients report injection anxiety, compelling innovators to eliminate the needle as a pain vector. Buffered cartridges stabilize solution pH to mirror physiologic values, decreasing the sting associated with acidic agents while maintaining shelf stability. Nuralyte’s LED-light platform achieves regional numbness in 20 seconds, potentially transforming pediatric and special-needs care where cooperation is limited. Computer-controlled systems deliver microliter increments, smoothing injection pressure and enhancing patient perception; pediatric trials record markedly lower pain ratings using the Wand relative to standard syringes. Kovanaze tetracaine-oxymetazoline nasal spray provides maxillary anterior anesthesia without palatal injections, posting high success in restorative dentistry. These innovations widen practice differentiation and bolster patient retention.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse events and safety concerns associated with anesthetics | −0.6% | Global; heightened scrutiny in North America and Europe | Short term (≤ 2 years) |

| Stringent regulatory and quality compliance requirements | −0.4% | North America and Europe; extending to Asia-Pacific | Medium term (2-4 years) |

| Volatility in active pharmaceutical ingredient supply chains | −0.3% | Global; most acute in regions reliant on single-source imports | Short term (≤ 2 years) |

| Environmental sustainability pressure on inhalation agents | −0.2% | Europe in lead; rising influence in North America and Oceania | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Events and Safety Concerns Associated with Anesthetics

Although only 29 articaine allergies were reported over 25 years, high-profile cases foster clinician caution. Local anesthetic systemic toxicity remains a critical worry, with cardiovascular depression linked to intravascular injection, especially in underweight children and frail seniors. Surveys reveal that merely 50.1% of dentists know the correct epinephrine route during anaphylaxis and only 43.5% stock emergency doses, exposing liability gaps[3]BDJ Open, “Dentist Preparedness for Anaphylaxis,” nature.com. Benzocaine-induced methemoglobinemia further dampens topical uptake, prompting regulators to mandate stronger package warnings. These incidents slow early adoption of new agents as practitioners default to familiar products with well-documented safety profiles.

Stringent Regulatory and Quality Compliance Requirements

The FDA’s 2024 draft guidance on composite resins and curing lights signaled wider scrutiny that now encompasses anesthetic delivery devices. State boards add another compliance tier; Florida’s graded permit structure forces multi-state groups to navigate complex licensure matrices. Domestic sourcing initiatives for active ingredients inflate costs but reduce geopolitical exposure as nitrous oxide shortages persist. Smaller innovators face steep validation budgets to meet ISO 13485 and Good Manufacturing Practice standards, often partnering with contract developers to bridge the gap. Mandatory training modules for advanced sedation elongate clinician onboarding, tempering the pace of novel device penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Anesthesia Type: Local Dominance Faces General Anesthesia Surge

Local formulations secured 74.02% of revenue in 2025, underscoring their indispensability for everyday restorative and endodontic care. Articaine’s superior cortical bone diffusion yields 95.92% success in pediatric molar therapy, outstripping lidocaine’s 77.55% clearance. Despite niche methemoglobinemia concerns, prilocaine remains favored for infiltration in short procedures. The dental anesthetics market size for local agents is projected to rise with the growing adoption of buffered cartridges that shorten onset and limit post-operative numbness.

General anesthesia, advancing at a 7.31% CAGR, answers the rising need for complex oral reconstruction and high-anxiety patient segments. Propofol’s quick emergence and recovery profile dominate adult protocols, whereas ketamine-propofol blends lessen stress responses in children. Conscious sedation with midazolam enables 91% case completion in adults wary of invasive jaw surgery. As case complexity climbs, the dental anesthetics market continues to diversify toward multimodal regimens that merge local blocks with intravenous agents for comprehensive comfort.

By Delivery Mode: Injectable Systems Face Digital Disruption

Injectable products retained 65.12% of 2025 turnover because clinicians are skilled with carpule syringes and procurement channels remain entrenched. Buffered solutions and retractable safety needles address pain and sharps injury risks, sustaining demand. Yet computer-controlled local anesthetic delivery units display the strongest 7.78% CAGR, leveraging microprocessor dosing that reduces injection pressure, noise, and tissue trauma. The dental anesthetics market size for digital systems is expected to broaden as their capital cost falls and as same-day procedures proliferate.

Needle-free innovation garners attention; Nuralyte’s light-based platform and Kovanaze nasal spray exemplify a future with zero puncture anxiety. Topical aerosols such as 5.6% lidocaine extend beyond pre-injection to serve as stand-alone agents for supragingival scaling. Environment-focused providers are piloting methoxyflurane inhalers that deliver analgesia while emitting 117 times less greenhouse gas than nitrous oxide. The evolving delivery mix showcases how the dental anesthetics market pivots toward precision, sustainability, and patient-centric care.

By End User: Ambulatory Centers Challenge Clinic Dominance

High-street dental clinics controlled 61.05% of global revenue in 2025, buoyed by continuous patient flow and diverse treatment offerings. The dental anesthetics market share for clinics remains solid, yet their growth curve moderates as urban penetration approaches saturation. Clinics are adopting point-of-care analytics to fine-tune anesthetic stock, minimizing wastage while meeting just-in-time delivery expectations.

Ambulatory surgical centers, expanding at an 8.29% CAGR, capitalize on bundled pricing and high-throughput implant programs that demand reliable anesthesia solutions. Extended hours and efficient turnover create predictable consumption profiles that favor bulk contract purchasing. Hospitals maintain a foothold for trauma and oncology cases requiring general anesthesia plus advanced airway management, while academic institutes remain the testbeds for novel agents before commercial rollout.

Geography Analysis

North America commanded 41.72% of revenue in 2025, underpinned by robust insurance coverage and early adopter mindsets that favor computer-controlled devices. Suzetrigine’s FDA approval in January 2025 further expands the therapeutic toolbox, offering non-opioid analgesia that reduces residual numbness and aligns with national opioid-reduction goals. Regional CAGR of 4.98% to 2031 will stem chiefly from technology upgrades rather than first-time access.

Europe shows steady demand growth as public payers integrate cosmetic add-ons under supplemental plans, encouraging clinics to upgrade comfort protocols. Environmental policy leads the region to phase out desflurane and investigate methoxyflurane as a greener substitute, lowering anesthetic gas emissions by 117 fold compared with nitrous oxide. Older demographics broaden the caseload needing sedation for lengthy prosthetic work, adding volume stability.

Asia-Pacific is expected to post the fastest 6.32% CAGR, propelled by China’s clinic expansion and India’s rural oral-health outreach. Japanese geriatric multimorbidity calls for customized anesthetic dosing, driving uptake of chairside monitoring and propofol-based short-stay protocols. Government scholarship programs enlarge the anesthesia workforce, raising the skill ceiling for advanced delivery systems. Rapid urbanization and social media influence raise patient expectations, making comfort-centric technologies a competitive necessity.

Competitive Landscape

The market remains moderately fragmented, with no single vendor exceeding a one-quarter revenue stake. Septodont, Dentsply Sirona, and Hikma Pharmaceuticals anchor the premium segment by pairing legacy formulations with next-generation delivery add-ons. Septodont’s January 2025 investment in Balanced Pharma aims to commercialize multiday pain-relief anesthetics that extend beyond the dental chair and reduce opioid prescriptions. Smaller innovators target narrow niches such as LED-induced anesthesia and nasal sprays, often partnering for regulatory navigation.

Environmental stewardship is a rising differentiator. Firms able to supply low-impact inhalation agents gain tender advantages with hospital groups committed to net-zero roadmaps. Supply-chain resilience is equally crucial; the Ukraine conflict curtailed ammonium nitrate, trimming nitrous oxide output and prompting clinics to seek dual sources. Companies with diversified regional fill-finish plants insulate clients from geopolitical volatility.

Digital integration forms the third competitive pillar. Vendors embedding cloud-based analytics into delivery units allow practitioners to track dosage, wastage, and patient outcomes, informing evidence-based procurement. This data loop strengthens brand stickiness and positions suppliers as technology partners rather than commodity sellers. Combined, these dynamics ensure sustained investment in R&D, M&A, and sustainability initiatives across the dental anesthetics market.

Dental Anesthetics Industry Leaders

Dentsply Sirona

Septodont

Henry Schein Inc.

Hikma Pharmaceuticals

Pierrel SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Septodont invested in Balanced Pharma and appointed Atif Zia to BPI’s board, advancing multiday pain-relief and enhanced local anesthesia programs.

- January 2025: FDA cleared Suzetrigine, a Nav1.8-selective analgesic by Vertex Pharmaceuticals, for post-surgical dental pain management.

- September 2024: Laxmi Dental Limited filed an INR 1,500 million IPO to fund capacity expansion and R&D.

- July 2024: FDA issued draft guidance for composite resin devices and curing lights, signaling broader dental device oversight.

- June 2024: NHS confirmed plans to retire desflurane anesthetic due to environmental concerns.

Global Dental Anesthetics Market Report Scope

As per the scope of the report, dental anesthetics are used to prevent pain in the mouth during dental procedures. Common procedures that typically require anesthesia include tooth extractions, wisdom teeth removal, root canals, and cavity fillings.

The dental anesthetics market is segmented into anesthesia type, end user, and geography. By anesthesia type, the market is segmented into local anesthesia and general anesthesia. The local anesthesia segment includes lidocaine, mepivacaine, prilocaine, articaine, and others. The general anesthesia segment includes propofol, midazolam, diazepam, methohexital, and others. By end user, the market is segmented into hospitals, dental clinics, and others. The other end users include multi-specialty clinics and dental laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market sizing and forecasts were made for each segment based on value (USD).

| Local Anesthesia | Lidocaine |

| Mepivacaine | |

| Prilocaine | |

| Articaine | |

| Other Types | |

| General Anesthesia | Propofol |

| Midazolam | |

| Diazepam | |

| Other Types |

| Injectable |

| Topical (Gels, Sprays, Patches) |

| Inhalation & Conscious-Sedation Agents |

| Computer-Controlled Local Anesthetic Delivery (CCLAD) |

| Emerging Electronic / Needle-Free Systems |

| Hospitals |

| Dental Clinics |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Anesthesia Type | Local Anesthesia | Lidocaine |

| Mepivacaine | ||

| Prilocaine | ||

| Articaine | ||

| Other Types | ||

| General Anesthesia | Propofol | |

| Midazolam | ||

| Diazepam | ||

| Other Types | ||

| By Delivery Mode | Injectable | |

| Topical (Gels, Sprays, Patches) | ||

| Inhalation & Conscious-Sedation Agents | ||

| Computer-Controlled Local Anesthetic Delivery (CCLAD) | ||

| Emerging Electronic / Needle-Free Systems | ||

| By End User | Hospitals | |

| Dental Clinics | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the dental anesthetics market?

The dental anesthetics market is valued at USD 1.82 billion in 2026 and is projected to reach USD 2.33 billion by 2031 at a 5.07% CAGR.

Which anesthesia type holds the largest share?

Local anesthesia leads the market with a 74.02% share in 2025 due to its routine use in restorative and endodontic care.

Which delivery mode is expanding fastest?

Computer-controlled local anesthetic delivery systems are advancing at a 7.78% CAGR as clinicians seek precision and improved patient comfort.

Why is Asia-Pacific the fastest-growing region?

Healthcare modernization, a growing middle class, and increasing awareness of oral health drive a 6.32% CAGR in Asia-Pacific through 2031.

How are environmental policies influencing the dental anesthetics market?

Sustainability pressures are steering clinics away from high-impact nitrous oxide toward lower-carbon options such as methoxyflurane, fostering product innovation and procurement shifts.

Page last updated on: