Denim Finishing Agents Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

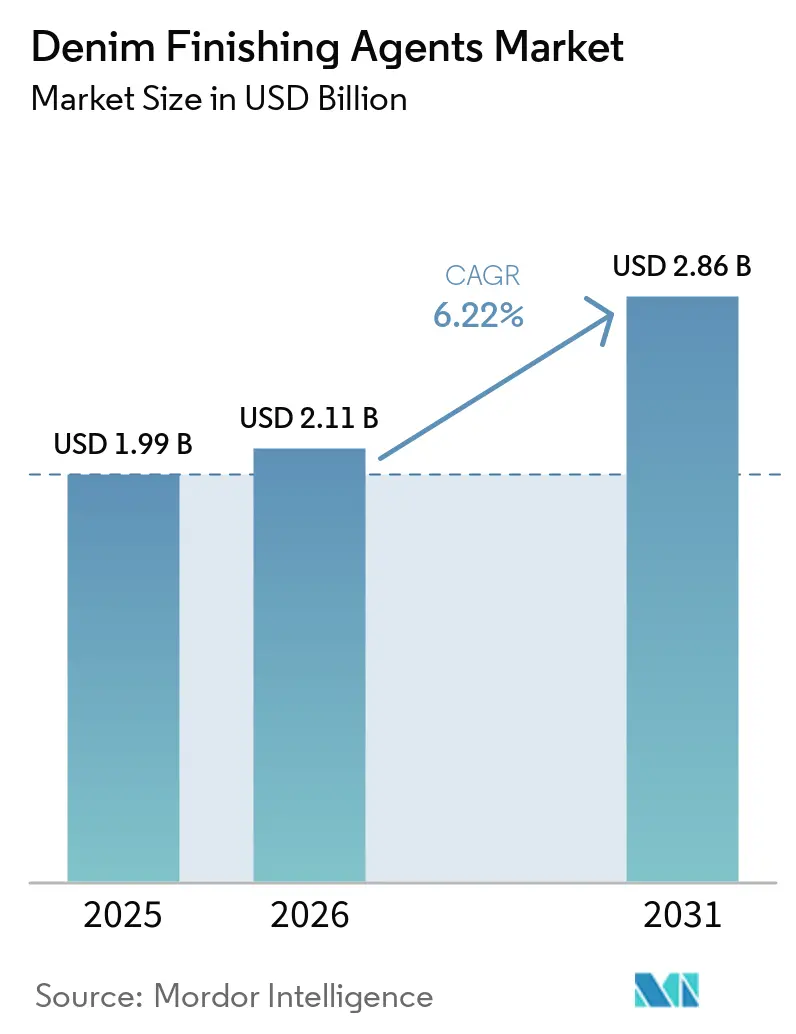

| Market Size (2026) | USD 2.11 Billion |

| Market Size (2031) | USD 2.86 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

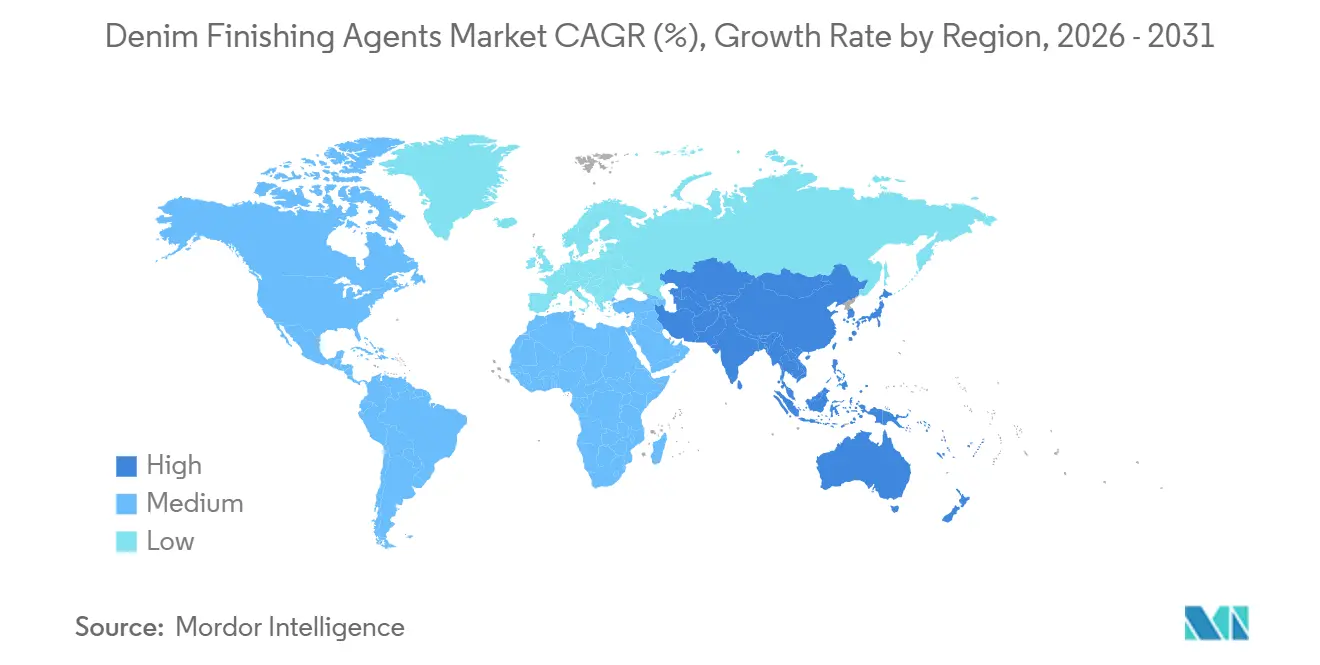

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

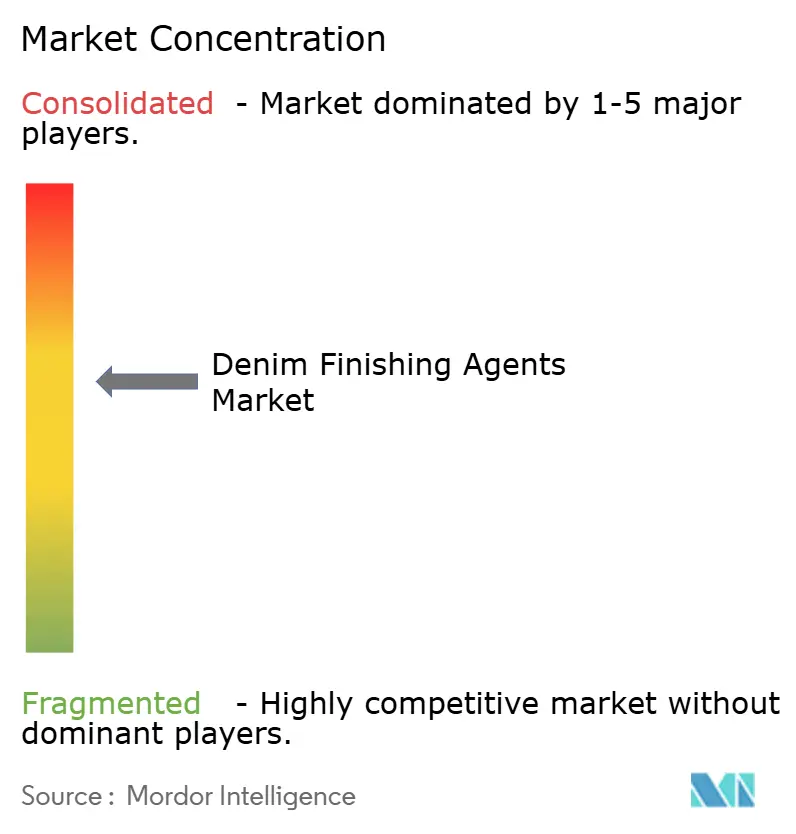

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denim Finishing Agents Market Analysis by Mordor Intelligence

The Denim Finishing Agents Market size is expected to grow from USD 1.99 billion in 2025 to USD 2.11 billion in 2026 and is forecast to reach USD 2.86 billion by 2031 at 6.22% CAGR over 2026-2031. The consistent demand for water- and energy-efficient enzyme formulations, the implementation of mandatory carbon-label audits in Europe, and increasing raw material costs for silicone-based chemistry are influencing procurement toward bio-based alternatives. Brands are facilitating this transition by specifying inputs compliant with Zero Discharge of Hazardous Chemicals (ZDHC) Manufacturing Restricted Substances List (MRSL) 3.1, which significantly reduces formaldehyde and aromatic amine residues. In the Asia-Pacific region, mills are adopting laser and ozone technologies to minimize pumice usage, thereby increasing the demand for dispersants and ozone neutralizers designed for waterless finishing processes. Additionally, strategic investments in artificial intelligence (AI)-enabled digital dosing platforms are reducing chemical overuse, creating challenges for suppliers without sensor-driven service models due to tighter operating margins.

Key Report Takeaways

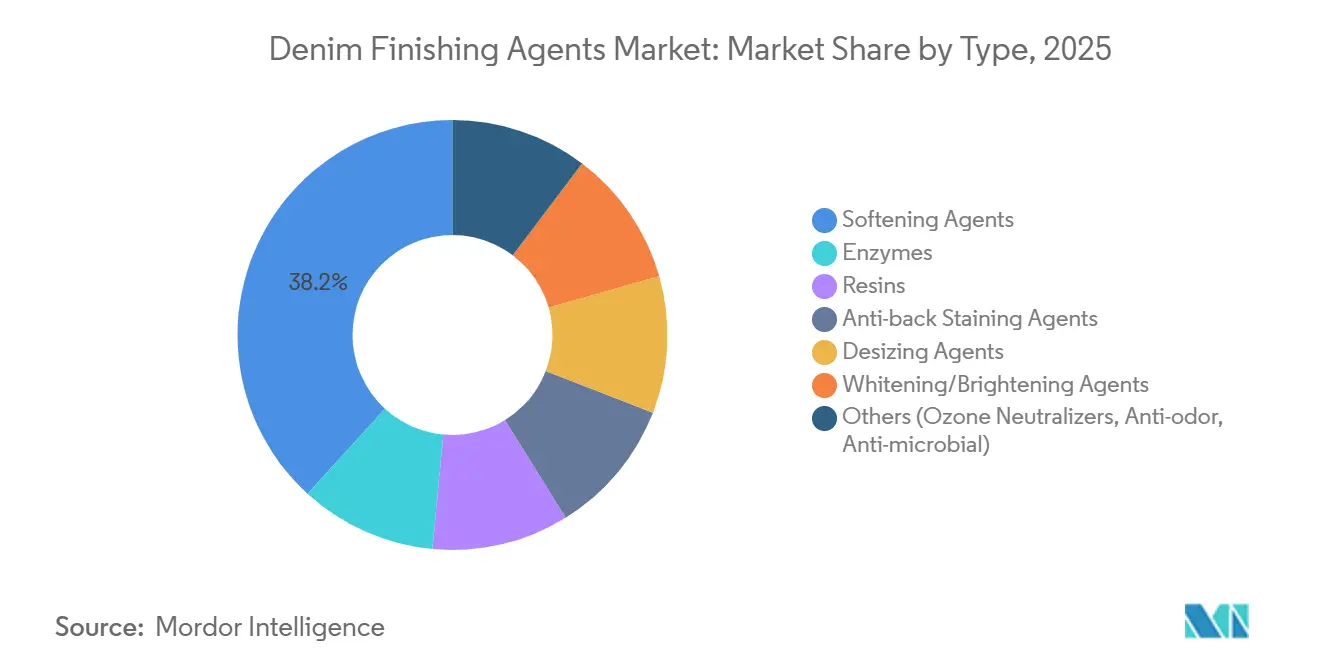

- By type, softening agents led with 38.22% revenue share in 2025, while enzymes are projected to expand at a 6.58% CAGR through 2031.

- By chemistry, silicone formulations commanded 40.46% of the Denim finishing agents market share in 2025, yet enzyme and other bio-based inputs are expected to grow at a 6.69% CAGR during 2026-2031.

- By application stage, stone washing accounted for 54.35% of 2025 volume, but laser and ozone finishing are foreseen to advance at a 6.45% CAGR through 2031.

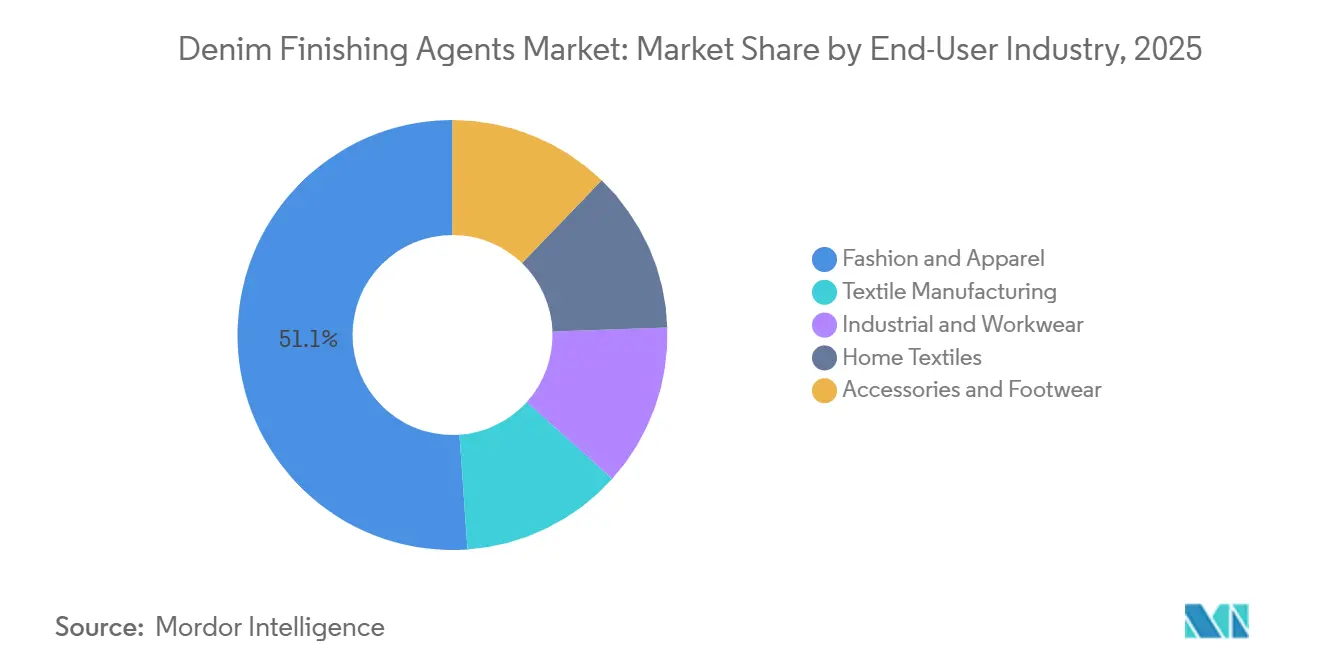

- By end-user industry, fashion and apparel held 51.11% of the Denim finishing agents market size in 2025 and is forecast to grow at a 7.12% CAGR through 2031.

- By geography, Asia-Pacific captured 43.34% revenue share in 2025 and is set to grow at 6.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Denim Finishing Agents Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global denim consumption in fashion and casual wear | +1.8% | Global, with a concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Shift toward sustainable and bio-based chemical agents | +1.5% | North America & EU core, spill-over to APAC premium segments | Long term (≥ 4 years) |

| Demand for customized soft-touch and sensory denim | +1.2% | Global, led by fashion hubs in Italy, Turkey, and premium Asian mills | Medium term (2-4 years) |

| Laser / ozone finishing boosting specialty-chem demand | +1.0% | APAC core (China, Bangladesh, Vietnam), expanding to South America | Short term (≤ 2 years) |

| AI-driven digital dosing platforms optimize chemical use | +0.7% | North America & EU early adopters, APAC scale deployment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Denim Consumption in Fashion and Casual Wear

Global denim fabric production has increased, with mills in the Asia-Pacific region contributing nearly two-thirds of the total output. The shift toward relaxed dress codes and the repositioning of denim as a lifestyle staple, rather than solely workwear, continue to drive growth in the denim finishing agents market. Fast-fashion brands have reduced design-to-shelf cycles to under four weeks, fueling demand for modular enzyme blends that enable wash houses to switch finishes rapidly. In 2025, Vietnam produced 495 million meters of denim, marking a 10% increase as brands diversified their sourcing away from China. Similarly, India experienced a 10% rise in production, reaching 1.65 billion meters, supported by increasing orders from the European Union (EU)[1]Editorial Team, “India Denim Statistics 2025,” Textile Commissioner of India, txcindia.gov.in .

Shift Toward Sustainable and Bio-Based Chemical Agents

Enzyme-based and other bio-based chemistries are experiencing the fastest growth in the denim finishing agents market as retailers increasingly adopt verified low-impact inputs. Archroma’s FiberColors line, which converts 50% wool waste into reactive dyes, reduces water usage by 30% compared to petrochemical alternatives[2]Archroma Communications, “FiberColors® Launch at Kingpins,” Archroma, archroma.com. Novozymes has introduced laccase variants that oxidize indigo without the use of sodium hydrosulfite, reducing effluent Chemical Oxygen Demand (COD) by up to 50%. However, mills face a 15-20% price premium for Global Organic Textile Standard (GOTS)-certified agents, which poses challenges in price-sensitive regions like Bangladesh. BASF’s Loopamid, a polyamide 6 (PA6) polymer derived from post-consumer textiles, highlights a broader commitment among suppliers to circular feedstocks.

Demand for Customized Soft-Touch and Sensory Denim

The market for softening agents is evolving, with a division emerging between commodity silicones and high-performance nano-dispersions that prevent migration. Premium mills in Italy and Turkey are combining enzyme washes, resin coatings, and nano-silicone topcoats to achieve retail mark-ups of 20-30%. In April 2026, Wacker Chemie increased silicone-emulsion prices due to feedstock disruptions in the Middle East. In response, CHT Germany introduced a biodegradable polyethylene-wax dispersion that replicates the tactile properties of dimethicone while meeting Organization for Economic Co-operation and Development (OECD) 301B biodegradability criteria. These innovations are driving the denim finishing agents market toward safer and more premium tactile effects.

Laser and Ozone Finishing Boosting Specialty-Chem Demand

Laser and ozone finishing represent the fastest-growing application stage, reducing water usage by 90% and eliminating pumice dust risks. Jeanologia’s EVO laser system has expanded its presence to 120 production lines in Bangladesh, up from 85 in 2024, following mandates from brands like Levi’s and H&M for waterless finishing. Ozone processes require neutralizers and dispersants, such as polyvinylpyrrolidone, to prevent indigo back-staining, thereby broadening the scope of services offered by formulators. By the end of 2025, China scaled its ozone finishing capacity to an equivalent of 800 million meters, driven by stricter discharge quotas.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of certified biodegradable alternatives | -0.9% | Global, acute in price-sensitive APAC and South America segments | Medium term (2-4 years) |

| Volatile supply of specialty silicones and enzymes | -0.6% | Global, with acute pressure in the EU and North America | Short term (≤ 2 years) |

| Mandatory traceability / carbon-label audits raise compliance costs | -0.5% | EU and North America core, expanding to APAC export-oriented mills | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Certified Biodegradable Alternatives

Global Organic Textile Standard (GOTS) certification involves recurring audit fees, creating challenges for mills operating on EBITDA margins below 5%. Similarly, Bluesign approval requires an application fee and annual renewal costs. Certified enzyme blends are priced 18-25% higher than conventional cellulase, requiring Southeast Asian mills to carefully evaluate compliance and profitability. However, Archroma’s Denim HALO has demonstrated that 40-56% water savings can offset a 12-15% price increase when supported by long-term brand contracts.

Volatile Supply of Specialty Silicones and Enzymes

Wacker Chemie’s mid-single-digit price increase in April 2026 reflects constrained silicone supply, influenced by high crude oil costs and logistics challenges in the Middle East. Similarly, enzyme markets face supply pressures following the Novozymes-Chr. The Hansen merger, which extended custom lead times to 12 weeks. To address these risks, mills adopt dual-sourcing strategies or switch to fatty-acid ester softeners, though these alternatives may not meet premium sensory requirements. Such supply volatility limits growth in the Denim finishing agents market in the short term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Enzymes Gain as Stone-Wash Fades

Enzymes are expected to achieve the fastest growth with a 6.58% Compound Annual Growth Rate (CAGR), while softening agents are projected to maintain the largest share, accounting for 38.22% of the Denim finishing agents market revenue in 2025. Mills increasingly prefer cellulase and laccase blends over pumice, reducing water consumption and minimizing health risks for workers. The market share for resins remains stable, with formaldehyde-free variants catering to crease-retention applications. Demand for anti-back-staining agents is rising, particularly in laser workflows, which are prone to indigo redeposition.

Archroma’s Denim HALO enzyme package has demonstrated a reduction in process time by up to 30%, driving adoption in markets like Turkey and Bangladesh. Similarly, Novozymes’ Primagreen has shortened production cycles, enabling mills to increase throughput without additional capital investment. Desizing and whitening agents are aligned with overall denim production trends, though concerns over European Union (EU) toxicity regulations are prompting a shift toward plant-based alternatives.

By Chemistry: Bio-Based Formulations Outpace Silicone

Silicones are projected to hold a 40.46% share of the Denim finishing agents market in 2025, but enzyme-based and other bio-based formulations are forecast to achieve the highest growth, with a 6.69% CAGR. Non-silicone fatty-acid esters and polyethylene waxes are gaining traction in regions where EU restrictions on cyclic siloxanes are in place. Nano and polymer dispersions, such as polyurethane and acrylic copolymers, are increasingly used to deliver a premium finish without migration issues.

CHT Germany GmbH’s biodegradable polyethylene-wax dispersion is gaining popularity among U.S. outdoor brands, while BASF’s loopamid PA6 enables resin coatings free from virgin petrochemicals. Although certification costs remain a barrier to widespread adoption, transparency is becoming a critical requirement in the Denim finishing agents industry.

By Application Stage: Laser and Ozone Disrupt Stone Wash

Stone washing is expected to retain 54.35% of the market volume in 2025, but laser and ozone finishing technologies are projected to grow at the highest CAGR of 6.45%. The market for enzyme washing continues to expand as mills seek vintage aesthetics with reduced mechanical stress. Resin coatings remain relevant for achieving deep colors and crease retention, although the demand for formaldehyde-free solutions is increasing.

In 2025, Bangladesh added 35 new EVO laser units, driving local demand for indigo dispersants and ozone neutralizers. China’s ozone-wash capacity has reached 800 million meters annually, supporting regional growth. Smaller mills, unable to afford laser kits costing over USD 150,000, are expected to sustain demand for enzyme washing throughout the forecast period.

By End User: Fashion Drives Premium Finish Demand

The fashion and apparel segment accounted for 51.11% of market revenue in 2025 and is anticipated to grow at the fastest CAGR of 7.12%, ensuring continued expansion of the Denim finishing agents market. Direct-to-consumer business models enable brands to invest in differentiated, soft-touch, and sustainable finishes that command premium pricing. Textile manufacturing aligns with global denim production, while industrial workwear emphasizes functional finishes, such as anti-microbials, supported by TANATEX’s Fresche partnership.

Home textiles remain a niche segment but benefit from trends in designer furniture featuring indigo upholstery. Accessories and footwear, though smaller in scale, are growing above the market average as brands incorporate denim aesthetics into non-apparel products, further expanding the Denim finishing agents market.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 43.34% of global revenue, driven by 3.0 billion meters of production from China and 1.65 billion meters from India. Bangladesh and Vietnam each achieved a 10% growth in output, supported by foreign investments seeking diversified supply chains. Emerging ASEAN (Association of Southeast Asian Nations) markets, including Cambodia and Indonesia, are attracting mid-tier mills, while Thailand benefits from Kemira’s planned capacity expansion in 2025. The Asia-Pacific market is projected to grow at a rate of 6.56% through 2031.

North America remains the second-largest market, supported by near-shoring initiatives and brand requirements for ZDHC (Zero Discharge of Hazardous Chemicals)-approved chemical processes. Europe, while experiencing slower volumetric growth, continues to influence global standards through REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) siloxane restrictions and France’s mandatory environmental labeling policy, set to take effect in October 2026. South America shows modest growth, highlighted by Solvay’s facility upgrade in Brazil, reflecting confidence in localized specialty supply. The Middle East and Africa play a smaller role, with the exception of Turkey, which capitalizes on its export access to the EU (European Union) and integrates Archroma’s circular dyes to meet buyer requirements.

Competitive Landscape

The denim finishing agents market is moderately consolidated. Archroma's FiberColors launch in April 2026, in collaboration with ORTA Anadolu, supports the adoption of circular dyes. The acquisition of DyStar by Zhejiang Longsheng for USD 688.88 million in January 2026 enhances integrated supply chains in Asia.

Fineotex, Bozzetto, TANATEX, and Zydex focus on agility and niche specializations to remain competitive. Fineotex's new 15,000 metric tons per annum (MTPA) plant in Gujarat, combined with artificial intelligence (AI)-based dosing system rollouts, positions the company for growth. The integration of technology, such as specialty formulations with digital sensors and dosing software, acts as a differentiator, enabling suppliers to maintain stronger relationships with mills. Additionally, ongoing compliance costs for Zero Discharge of Hazardous Chemicals (ZDHC) Gateway, ranging from USD 500-2,000 annually per product, favor larger players capable of managing these expenses.

Denim Finishing Agents Industry Leaders

Archroma

CHT Germany GmbH

RUDOLF Holding SE & Co. KG

DyStar Singapore Pte Ltd

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Archroma and ORTA Anadolu introduced FiberColors denim at Kingpins Amsterdam, reporting a 30% reduction in water consumption. This innovation is attributed to the use of advanced denim finishing agents, which optimize resource efficiency during production.

- March 2026: Shin-Etsu has allocated USD 3.4 billion to expand its polyvinyl chloride (PVC) complex in Louisiana, with plans to include capacity for specialty silicone intermediates. These intermediates are critical components in the production of denim finishing agents, which enhance the durability and appearance of denim fabrics. The expansion aims to meet the growing demand for high-performance materials in textile applications, including denim manufacturing.

Global Denim Finishing Agents Market Report Scope

Denim finishing agents are chemical substances, enzymes, or polymers used on denim garments to modify their appearance, texture, and performance. These agents convert raw denim into softer and distressed products through processes such as enzyme washing, bleaching, and softening to achieve specific aesthetics.

The denim finishing agents market is segmented by type, chemistry, application Stage, end-user industry, and geography. By type, the market is segmented into softening agents, enzymes, resins, anti-back-staining agents, desizing agents, whitening/brightening agents, and others (ozone neutralizers, anti-odor, anti-microbial). By chemistry, the market is segmented into silicone, non-silicone (fatty acid, polyethylene), enzyme/bio-based, and nano and polymer dispersions. By the application Stage, the market is segmented into stone washing, enzyme washing, resin coating/over-dye, laser/ozone finishing, and garment washing and soft-finish. By end-user industry, the market is segmented into fashion and apparel, textile manufacturing, industrial and workwear, home textiles, and accessories and footwear. The report also covers the market size and forecasts for denim finishing agents in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Softening Agents |

| Enzymes |

| Resins |

| Anti-back Staining Agents |

| Desizing Agents |

| Whitening/Brightening Agents |

| Others (Ozone Neutralizers, Anti-odor, Anti-microbial) |

| Silicone |

| Non-silicone (fatty acid, polyethylene) |

| Enzyme/Bio-based |

| Nano and Polymer dispersions |

| Stone Washing |

| Enzyme Washing |

| Resin Coating/Over-dye |

| Laser/Ozone Finishing |

| Garment Washing and Soft-finish |

| Fashion and Apparel |

| Textile Manufacturing |

| Industrial and Workwear |

| Home Textiles |

| Accessories and Footwear |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Softening Agents | |

| Enzymes | ||

| Resins | ||

| Anti-back Staining Agents | ||

| Desizing Agents | ||

| Whitening/Brightening Agents | ||

| Others (Ozone Neutralizers, Anti-odor, Anti-microbial) | ||

| By Chemistry | Silicone | |

| Non-silicone (fatty acid, polyethylene) | ||

| Enzyme/Bio-based | ||

| Nano and Polymer dispersions | ||

| By Application Stage | Stone Washing | |

| Enzyme Washing | ||

| Resin Coating/Over-dye | ||

| Laser/Ozone Finishing | ||

| Garment Washing and Soft-finish | ||

| By End-user Industry | Fashion and Apparel | |

| Textile Manufacturing | ||

| Industrial and Workwear | ||

| Home Textiles | ||

| Accessories and Footwear | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Denim Finishing Agents Market?

The Denim Finishing Agents Market size is expected to grow from USD 1.99 billion in 2025 to USD 2.11 billion in 2026 and is forecast to reach USD 2.86 billion by 2031 at 6.22% CAGR over 2026-2031.

Which segment grows fastest by application stage?

Laser and ozone finishing is forecast to post the quickest 6.45% CAGR as mills eliminate pumice and reduce water use.

Why are bio-based chemistries gaining traction?

Retailer sustainability mandates and EU regulations are pushing mills to adopt enzyme and other bio-based agents that cut water, energy, and chemical footprints.

Which region leads demand?

Asia-Pacific accounted for 43.34% of 2025 revenue and kept the growth lead due to China, India, Bangladesh, and Vietnam’s expanding denim output.

Page last updated on: