Delhi-NCR Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

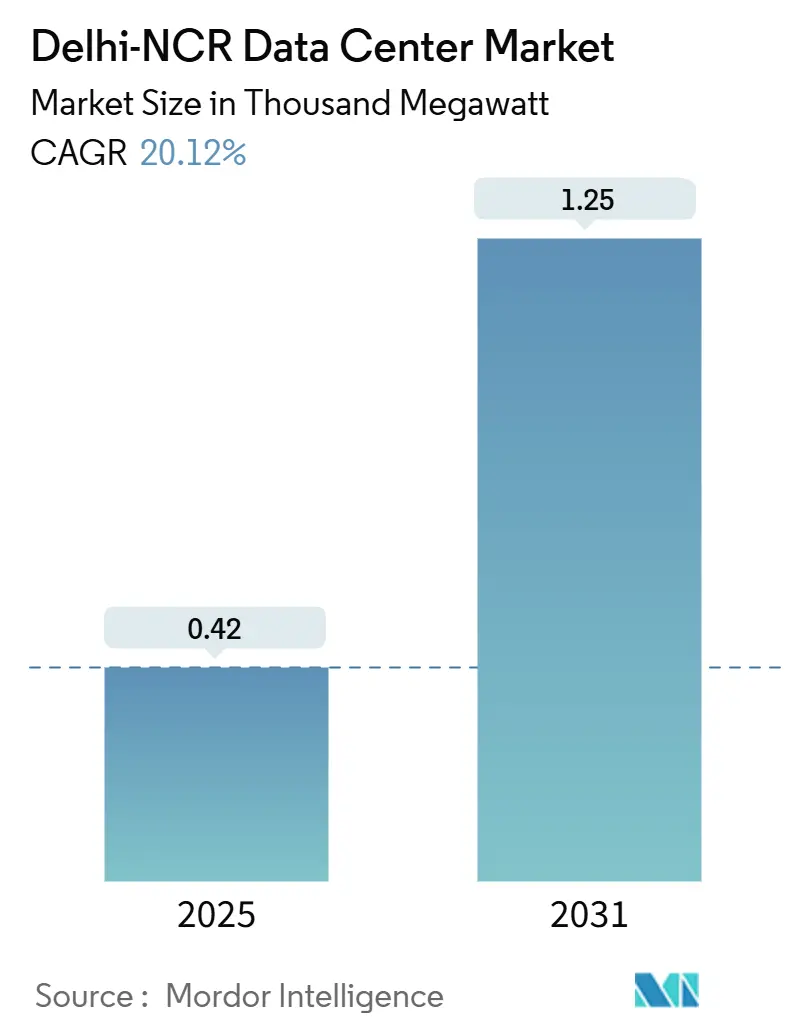

| Market Volume (2025) | 0.42 Thousand megawatt |

| Market Volume (2031) | 1.25 Thousand megawatt |

| Growth Rate (2025 - 2031) | 20.12% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Delhi-NCR Data Center Market Analysis by Mordor Intelligence

The Delhi-NCR data center market size stands at 418 MW in 2025 and is forecast to climb to 1,255.35 MW by 2031, representing a 20.12% CAGR. The Delhi-NCR data center market benefits from the convergence of cloud-first banking workloads, AI-led rack-density upgrades, and state-level incentives that lower entry barriers for hyperscale campuses. Large and Mega facilities dominate current demand because enterprises prefer consolidation that delivers economy-of-scale savings and streamlined security controls. Policy-driven data-localization mandates further anchor new capacity to domestic sites, while sustained fiber-network densification improves cross-connect efficiency for content, fintech, and edge deployments. Aggressive renewable-energy procurement targets likewise reposition the Delhi-NCR data center market as a proving ground for green-power purchase agreements and advanced cooling solutions that limit Power Usage Effectiveness (PUE) ratios.

Key Report Takeaways

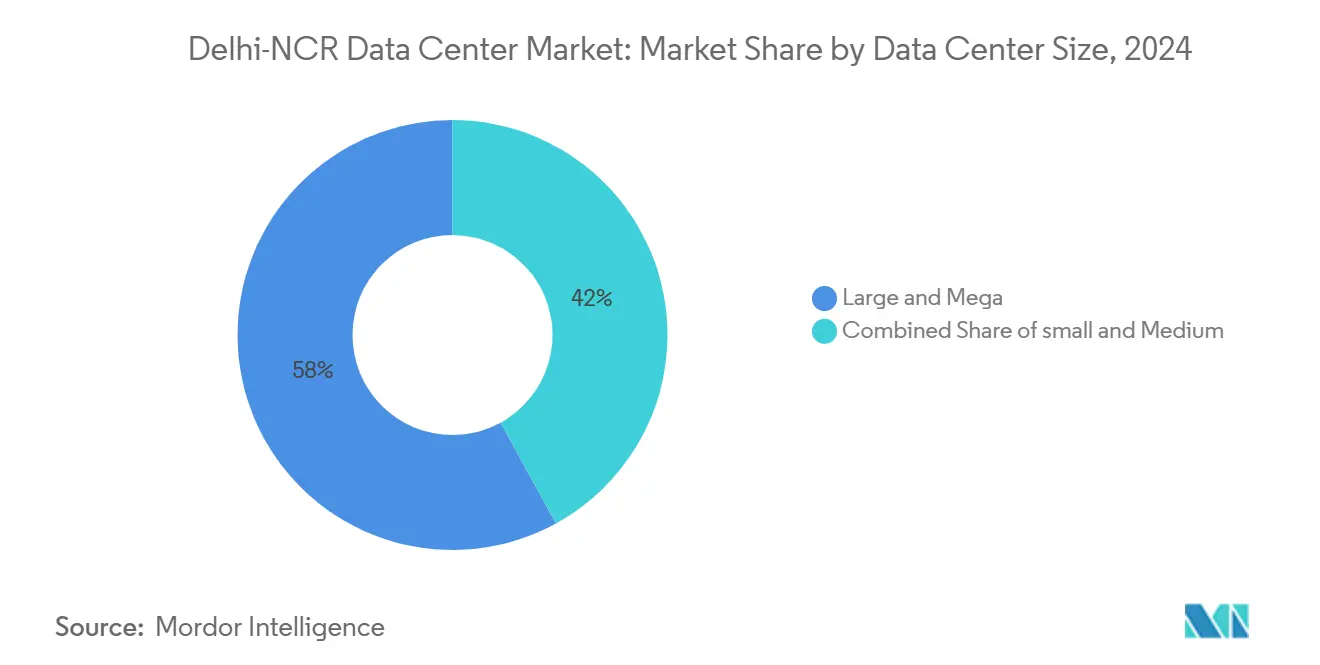

- By data center size, Large and Mega facilities captured a 58% Delhi-NCR data center market share in 2024 and the Mega category is projected to expand at a 20.5% CAGR through 2031.

- By tier standard, Tier III sites accounted for 61% of the Delhi-NCR data center market size in 2024, while Tier IV infrastructure is forecast to record a 21.12% CAGR to 2031.

- By absorption, Utilized capacity represented 84% of total load in 2024 and hyperscale colocation is advancing at a 22.6% CAGR through 2031.

Delhi-NCR Data Center Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising cloud-first demand from BFSI, media and OTT players | +4.2% | Delhi-NCR core and satellites | Medium term (2–4 years) |

| Aggressive renewable-power targets by DISCOMs and open-access corridors | +3.8% | Haryana, Uttar Pradesh, Delhi | Long term (≥4 years) |

| Edge-ready metro-fibre densification across Delhi-NCR | +3.1% | Urban Delhi-NCR and suburbs | Short term (≤2 years) |

| Incentives under Haryana and Uttar Pradesh data-center policies 2024 | +2.9% | Haryana and Uttar Pradesh corridors | Medium term (2–4 years) |

| AI/LLM rack-power densities driving ≥30 kW retrofits | +3.7% | Hyperscale campuses | Short term (≤2 years) |

| Cold-chain logistics pivot to data-powered automation hubs | +1.5% | NCR logistics zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Cloud-First Demand from BFSI, Media and OTT Players

Financial institutions now run community cloud cores that support IMPS and UPI services, a shift that drives sustained absorption for Tier III+ footprints offering rigorous security frameworks.[1]ESDS Software Solution Limited, Banking Community Cloud, esds.co.in Payment-system data must remain on domestic soil, which locks new workloads into the Delhi-NCR data center market. OTT platforms add further load because video streaming for more than 30 million local consumers requires low-latency nodes. Together these customer groups prioritize facilities close to financial exchanges, internet gateways, and content-delivery points, ensuring stable uptake of both retail and wholesale suites. The growth arc should persist as banks deploy active-active disaster-recovery nodes and as media firms push live-sports streams toward edge zones.

AI/LLM Rack-Power Densities Driving ≥30 kW White-Space Retrofits

Machine-learning servers equipped with GPUs demand two to three times the power envelope of legacy x86 racks. Operators are therefore retrofitting floors with immersion and direct-to-chip liquid cooling to hold PUE below design limits.[2]Vertiv, High-Density Cooling for AI/ML Workloads, vertiv.com STT GDC and Firmus demonstrated this pivot by launching Sustainable Metal Cloud, an immersion-cooled service for AI-centric workloads.[3]ST Telemedia Global Data Centres & Firmus Technologies, Sustainable Metal Cloud Partnership, firmus.co Higher densities change electrical topologies, raise backup-generator ratings, and require thicker busbars, which together increase capital intensity yet create premium pricing opportunities. Facility designs now feature flexible diverter-valve systems that let operators migrate between air and liquid regimes without downtime.

Edge-Ready Metro-Fibre Densification Across Delhi-NCR

Densely meshed fiber rings reduce round-trip times for 5G and industrial-IoT applications. Network builders are installing thousands of small cells connected by new 7,000-km metro loops, which give data-center tenants sub-2-millisecond paths to end users. Enhanced connectivity elevates the Delhi-NCR data center market’s attractiveness for real-time analytics, location-based advertising, and autonomous-vehicle off-board processing. Suburban fiber spurs in Noida and Gurgaon extend the addressable edge footprint, enabling distributed colocation pods that complement centralized hyperscale halls.

Incentives Under Haryana and Uttar Pradesh Data-Centre Policies 2024

The two states bundle land-use fast-tracking, stamp-duty concessions, and power-tariff rebates that lower the entry cost for greenfield campuses. Uttar Pradesh’s 21,000-hectare New Noida blueprint earmarks dedicated grids and dual-feed substations, while Haryana offers industrial parcels coupled with pre-approved feeder bays. These schemes shorten permitting cycles, smooth power interconnections, and de-risk investments for operators planning multi-building campuses over 10-year horizons. The policy frameworks also promote renewable-purchase obligations that dovetail with hyperscaler climate pledges.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Scarcity of contiguous 50-acre land parcels in core NCR | −2.8% | Delhi-NCR industrial zones | Medium term (2–4 years) |

| 220 kV grid-interconnection queues greater than 24 months | −3.2% | Suburban expansion belts | Long term (≥4 years) |

| Monsoon-driven flooding risk and CRZ clearances | −1.9% | Yamuna floodplains | Short term (≤2 years) |

| Shortfall of Uptime-Tier-certified commissioning engineers | −1.1% | NCR talent pool | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Contiguous 50-Acre Land Parcels in Core NCR

Hyperscale blueprints call for single-tenant campuses that sprawl across 50 acres or more, yet land banking in the urban core has tightened. Operators pivot to peripheral zones, but those sites often lack dark-fiber and dual-grid feeds, which raises backhaul and substation costs. New Noida’s special economic zone allocations will ease future scarcity, although the bulk of that acreage completed only after 2031, leaving interim shortages that pressure land values and push some builds toward tier-2 cities.

220 kV Grid-Interconnection Queues > 24 Months

Data-center megaprojects require dedicated high-voltage bays that presently face queue times exceeding two years. Delays stem from transmission expansion lagging behind surging metropolitan demand and from renewable-integration bottlenecks. Operators therefore invest in on-site gas turbines or interim 33 kV ties, measures that carry higher operating expenditures. Grid upgrade programs will eventually bridge the gap, yet timing uncertainty weighs on delivery schedules and inflates contingency budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Hyperscale Campuses Drive Market Evolution

Large and Mega facilities held 58% of the Delhi-NCR data center market in 2024, underscoring the swing toward consolidated estates that can deliver multi-megawatt suites to single tenants. The Delhi-NCR data center market size for the Mega segment is projected to advance at a 20.5% CAGR, the fastest among all size bands. Operators favor such campuses because shared chilled-water and substation assets unlock per-rack energy savings. Yotta’s 250 MW Greater Noida build typifies the scale now sought by cloud providers and AI labs.

Mega campuses also allow phased shell deployment that matches capacity with bookings, mitigating stranded-capital risk. High-density pods inside these builds rely on liquid cooling loops that reuse waste heat for office HVAC loads. Meanwhile, Small and Medium halls still find demand among edge workloads and localized disaster-recovery nodes, though their relative share is expected to slide as more enterprises exit legacy on-prem environments.

By Tier Standard: Tier IV Adoption Accelerates for Mission-Critical Workloads

Tier III captured 61% of the Delhi-NCR data center market size in 2024, but Tier IV is growing at a 21.12% CAGR as regulated sectors seek near-zero downtime. Financial-services and e-governance clients now write service-level agreements that specify 99.995% availability, pushing builders to adopt concurrently maintainable electrical paths and 2N+1 cooling redundancy. The Delhi-NCR data center market share of Tier IV halls will increase as operators leverage tax incentives that offset higher capex premiums.

Tier IV facilities integrate smart-bus couplers, static-switch boards, and AI-driven predictive-maintenance suites that cut mean-time-to-repair. Although Tier I and Tier II footprints persist for test-dev and archival loads, they are unlikely to capture new mission-critical contracts. Talent shortages in Uptime-certified commissioning add friction to Tier IV rollouts, but specialist firms are scaling training programs to close that gap.

By Absorption: Hyperscale Colocation Transforms Utilization Patterns

Utilized racks represented 84% of the Delhi-NCR data center market in 2024, signaling disciplined supply pipelines. Hyperscale colocation suites are forecast to log a 22.6% CAGR through 2030 as global cloud platforms press ahead with north-India availability zones. This sub-segment benefits from advance-lease models where clients underwrite multi-year power blocks before ground-breaking, which stabilizes developer cash flows.

Wholesale colocation maintains relevance for enterprises moving to private-cloud stacks that mirror public-cloud architectures yet sit behind dedicated firewalls. Non-utilized capacity remains near all-time lows because operators align shell releases with pre-commitments, avoiding speculative overbuilds. The Delhi-NCR data center industry, therefore, shows balanced supply-demand dynamics that limit vacancy risk.

Geography Analysis

Delhi, Gurgaon, and Noida anchor 14% of national installed IT load in 2025, making the corridor the second-largest cluster after Mumbai. The Delhi-NCR data center market benefits from proximity to federal ministries, stock exchanges, and the headquarters of more than 40 multinational banks. Noida’s Sector 150–167 tract leads fresh supply because it offers industrial-zoned parcels with direct access to 400 kV lines. Gurgaon remains attractive for fintech and media tenants that value short hop routes to the National Stock Exchange disaster-recovery vault.

Recent auctions by the Yamuna Expressway Industrial Development Authority fetched INR 220 crores for 200 acres earmarked for data-center use, signaling active land absorption. Yet climate-exposure mapping classifies parts of the Yamuna floodplain as high-risk, forcing new builds to raise plinth heights and install dual-sump pumping. Haryana complements its incentive plan with promises of 99.9% grid uptime, but practical delivery hinges on accelerated transmission reforms.

Delhi’s urban core is largely tapped out of large plots, steering hyperscale designs toward New Noida where the master plan allocates 21,000 hectares for digital infrastructure. However, last-mile fiber to those greenfield sites is still in rollout, and builders often co-fund ducts to maintain construction timetables. Overall the Delhi-NCR data center market retains cost advantages versus Mumbai on both land price and water-availability metrics, although higher ambient temperatures raise cooling loads during summer peaks.

Competitive Landscape

The Delhi-NCR data center market hosts a mix of global, regional, and telecom-affiliated operators. STT GDC tops the leaderboard with a 28% share following its USD 3.2 billion multiyear plan to add 550 MW across India. Yotta accelerates scale with a 250 MW Greater Noida campus that brings six interconnected buildings online in phases. Nxtra by Bharti Airtel leverages carrier network depth to target hybrid-cloud interconnection deals, while AdaniConneX positions sustainability as a differentiator through a USD 1.44 billion construction-finance line tied to renewable-energy milestones.

Strategic moves cluster around AI-ready white space, liquid-cooling retrofits, and corporate power-purchase agreements. STT GDC and Firmus launched Sustainable Metal Cloud to court GPU workloads, whereas Nxtra partners with renewable developers to reach 100% green power ahead of Schedule-III disclosures. Market rivalry also manifests in cross-connect pricing, with operators offering zero-cost cross-DC fibers to lock in multi-site customers. A notable barrier to entry remains the 24-month lead time for high-voltage interconnects, which favors incumbents that already hold grid allotments. The Delhi-NCR data center industry appears moderately concentrated but on a trajectory toward scale-driven consolidation.

Delhi-NCR Data Center Industry Leaders

STT Telemedia

CtrlS

NTT Data

Nxtra Data Limited

Yotta Infrastructure Solutions Llp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: MeitY restarted consultations on a national policy that introduces single-window clearances and Data-Centre Economic Zones, aimed at de-concentrating capacity beyond metros.

- July 2025: Cisco teamed with Reliance Jio to develop AI-ready facilities based on the Cisco 8000 portfolio.

- July 2025: NTT DATA named Alok Bajpai Managing Director for Global Data Centers India, reinforcing its metro-expansion roadmap.

- June 2024: STT GDC raised SGD 1.75 billion from a KKR-led consortium to expand global capacity beyond 1.7 GW

Delhi-NCR Data Center Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services.

The Delhi-NCR data center market is segmented by dc size (small, medium, large, massive, and mega), tier type (tier 1 and 2, tier 3, and tier 4), and absorption (utilized (colocation type (retail, wholescale, and hyperscale), end user (cloud and IT, telecom, media and entertainment, government, BFSI, manufacturing, and e-commerce)), and non-utilized). The market sizes and forecasts are provided in terms of value (MW) for all the above segments.

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User Industry | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End Users | ||

| By Data Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User Industry | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End Users | |||

Key Questions Answered in the Report

How large is the Delhi-NCR data center market in 2025?

Installed IT load is 418 MW in 2025 and is projected to grow at a 20.12% CAGR to 2031.

Which facility size segment is expanding the quickest in Delhi-NCR?

Mega data centers of at least 50 MW are forecast to expand at a 20.5% CAGR through 2030.

What share do Tier III sites hold within Delhi-NCR?

Tier III facilities accounted for 61% of total load in 2024.

Why are AI workloads changing data-center design requirements?

GPU-based clusters require ?30 kW per rack, prompting the adoption of liquid cooling and higher-capacity power trains.

Which policy incentives most benefit new builds?

Haryana and Uttar Pradesh policies of 2024 offer land-use fast tracking, stamp-duty rebates, and renewable-power integration support.

What is the main barrier to hyperscale expansion in the region?

Delays of more than 24 months in securing 220 kV grid interconnections prolong project timelines and raise costs.

Page last updated on: