Defense Tactical Video Data Link Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

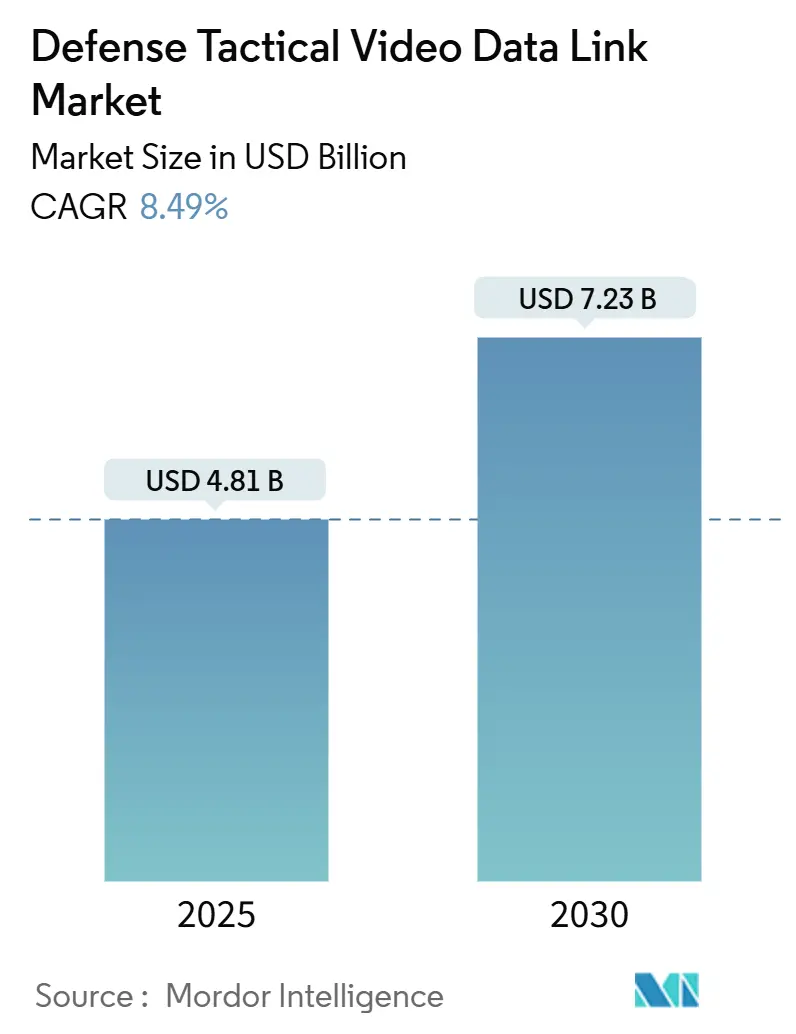

| Market Size (2025) | USD 4.81 Billion |

| Market Size (2030) | USD 7.23 Billion |

| Growth Rate (2025 - 2030) | 8.49% CAGR |

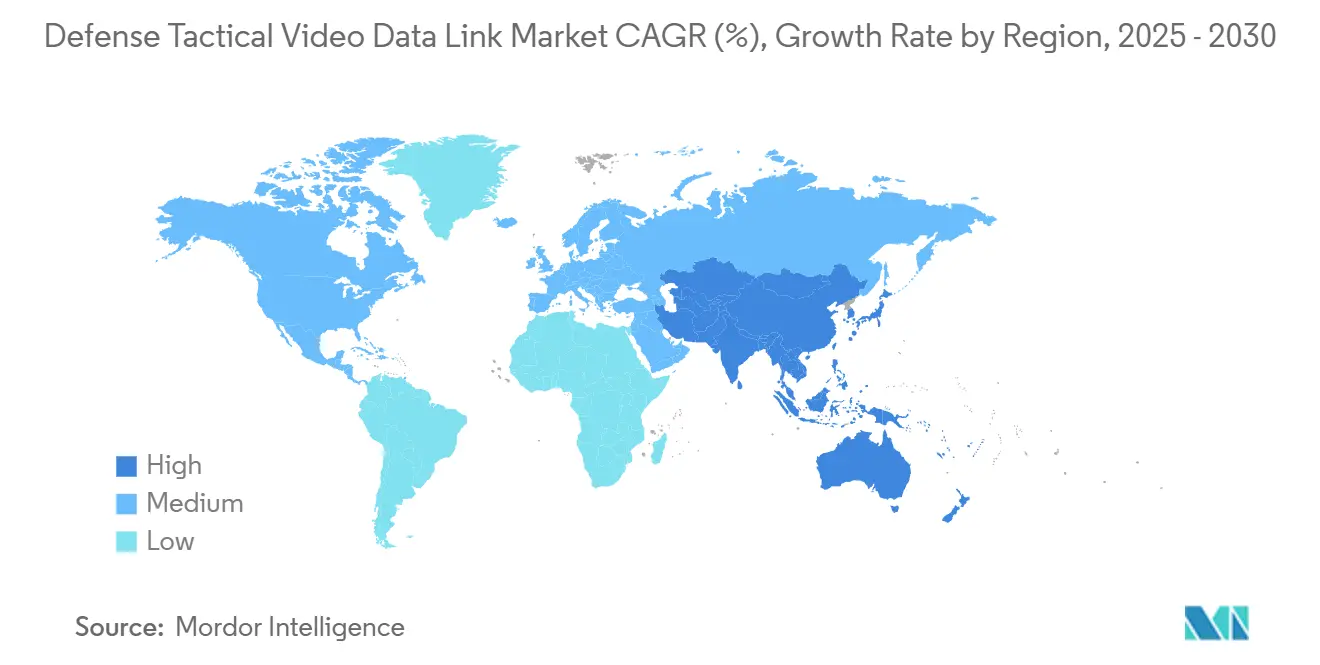

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Defense Tactical Video Data Link Market Analysis by Mordor Intelligence

The defense tactical video data link market size is currently valued at USD 4.81 billion, and it is forecasted to reach USD 7.23 billion by 2030, expanding at an 8.49% CAGR. This market size growth reflects the military’s pivot from voice-centric communications toward bandwidth-intensive, real-time video across multi-domain operations. Government programs such as the US Combined Joint All-Domain Command and Control (JADC2) initiative and allied digital-battlefield projects are accelerating demand for secure, low-latency video links. Platform electrification trends, edge-computing upgrades, and open-architecture mandates continue to reshape system design priorities, while battlefield digitization steadily expands the addressable defense tactical video data link market. Competitive dynamics increasingly reward vendors integrating artificial intelligence (AI) processing, frequency agility, and cyber-hardened encryption into modular products suitable for rapid technology refresh.

Key Report Takeaways

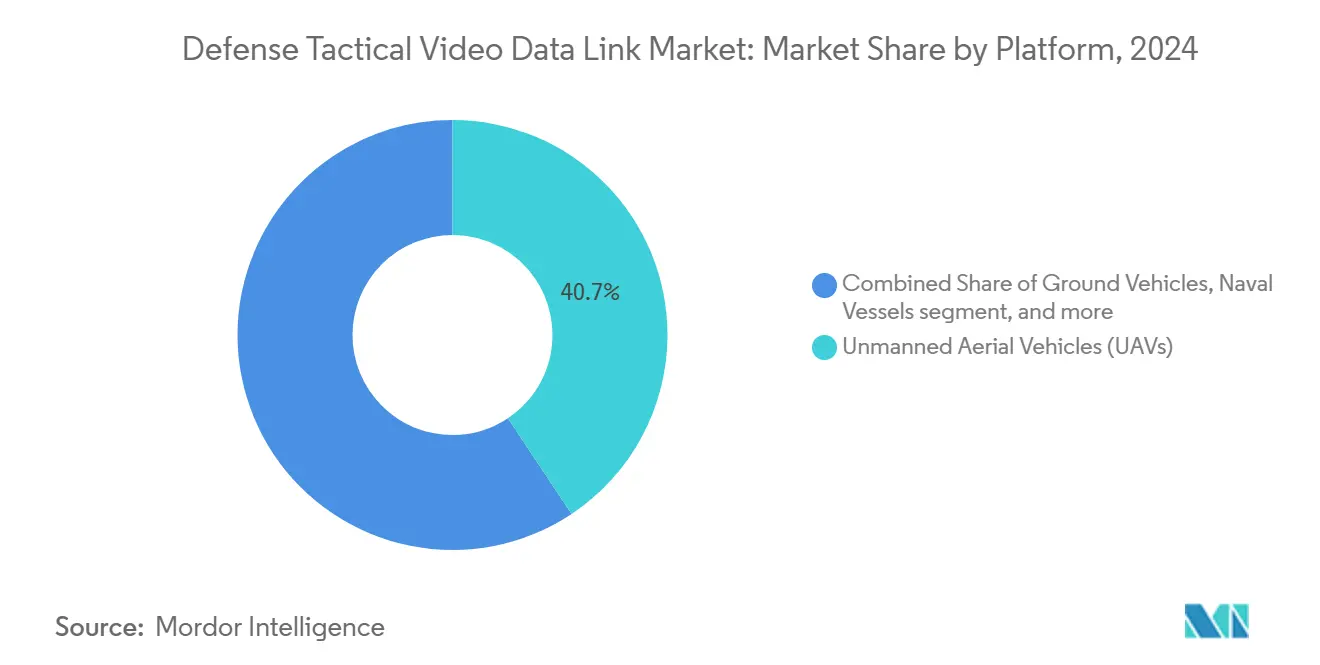

- By platform, UAVs led with 40.65% defense tactical video data link market share in 2024, whereas soldier-worn solutions are projected to advance at a 12.10% CAGR through 2030.

- By frequency band, Ku-band commanded 32.20% share of the defense tactical video data link market size in 2024, while optical/laser solutions are on track for a 13.50% CAGR to 2030.

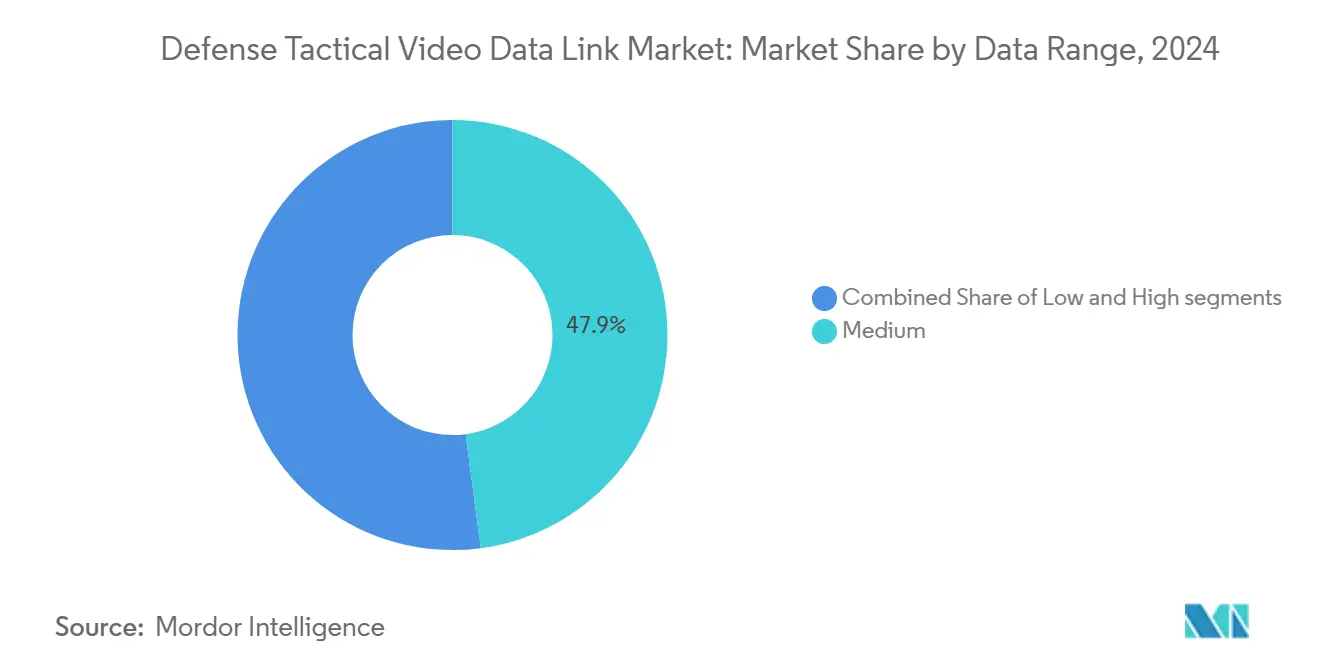

- By data-rate category, medium-rate links held 47.90% of the 2024 defense tactical video data link market; high-rate systems are forecasted to climb at 11.40% CAGR through 2030.

- By component, modems and routers accounted for a 31.55% share of the 2024 defense tactical video data link market size, yet software components will post a 12.75% CAGR by 2030.

- By end-user, the Air Force captured a 35.65% share in 2024, whereas the Army demand is set for a 9.70% CAGR over the same horizon.

- By geography, North America dominated with a 37.85% share in 2024; Asia-Pacific is projected to expand at a 10.65% CAGR through 2030.

Global Defense Tactical Video Data Link Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of UAV-borne ISR video feeds | +1.8% | Global; focus on North America and APAC | Medium term (2-4 years) |

| DoD network-centric modernization programs | +2.1% | North America primary; NATO secondary | Long term (≥ 4 years) |

| Rising defense spending on secure real-time C2 imagery | +1.5% | Global; led by APAC | Medium term (2-4 years) |

| SOSA/MOSA open-architecture mandates | +1.2% | North America and allies | Long term (≥ 4 years) |

| Edge-AI enabled micro-datalinks at squad level | +0.9% | North America and Europe | Short term (≤ 2 years) |

| Adoption of laser/optical tactical links | +0.8% | Global; R&D in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of UAV-borne ISR Video Feeds

Modern drones collect terabytes of full-motion video daily, pushing defense agencies to procure sub-second latency links that remain stable in contested spectra. Solutions like L3Harris’s dual-band VORTEX®x transceiver show how redundant pathways preserve continuous imagery even under heavy jamming.[1]Source: L3Harris Technologies, “VORTEX®x ISR Transceiver,” l3harris.com Demand accelerates further in Asia-Pacific, where regional tensions spur perpetual aerial surveillance. Militaries also layer adaptive compression and metadata tagging at the platform edge, raising bandwidth requirements but streamlining down-range analytics. As commanders tie video directly to targeting loops, mission success increasingly hinges on resilient UAV links that can switch frequencies or compression profiles in milliseconds. Together, these developments underpin the sustained expansion of the defense tactical video data link market.

DoD Network-Centric Modernization Programs

CJADC2 and NATO's companion efforts seek seamless video interoperability across air, ground, maritime, and space nodes. Software-defined networking and artificial intelligence tools let tactical radios negotiate modulation and prioritize streams on the fly.[2]Source: Dan Taylor, “Advanced communication systems to be provided to Israel by Elbit Systems,” militaryembedded.com The SOSA standard demands open interfaces, enabling smaller suppliers to bid software modules that plug into incumbent hardware. While commoditization pressure reduces margins on specific boards, value migrates to firmware that adapts to cyber threats or spectral congestion. Continuous network-centric upgrades through 2030 guarantee recurring procurement cycles, reinforcing long-run growth for the defense tactical video data link market.

Rising Defense Spending on Secure Real-time C2 Imagery

Asia-Pacific defense budgets are growing at 6.3% annually, with Japan alone lifting spending by 21% in 2025, and much of the increment funds secure imagery pipelines.[3]Source: Halna du Fretay, “Russia Trials Satellite Link to Extend Operational Reach of Long-Range Drones,” armyrecognition.com Procurement officers stipulate latency below 100 milliseconds and 99.9% availability, raising the bar for link redundancy, antenna design, and quantum-resistant encryption. High-reliability requirements also drive investment in directional arrays that thwart electronic-attack vectors. As real-time video becomes integral to maneuver warfare, spending patterns fuel the global defense tactical video data link market.

SOSA/MOSA Open-Architecture Mandates

SOSA compliance encourages swappable cards and reference backplanes that shorten upgrade cycles from a decade to two years. Component-level competition brings rapid insertion of advanced codecs, processors, and RF front ends while slashing total ownership costs. Vendors that deliver secure software waveforms gain leverage because commanders prefer to deploy new threat-adapted algorithms rather than replace entire radios. Over the long term, this mandate amplifies addressable volumes for interoperable solutions inside the defense tactical video data link market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum congestion and bandwidth allocation limits | −0.7% | Global; acute in dense zones | Long term (≥ 4 years) |

| SWaP-cost trade-offs on small platforms | −0.9% | Global; UAV and soldier gear | Medium term (2-4 years) |

| Lengthy cyber-security accreditation cycles | −0.6% | North America and NATO | Medium term (2-4 years) |

| Post-quantum crypto uncertainty | −0.4% | Global; high-security assets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Spectrum Congestion and Bandwidth Allocation Limits

Civilian 5G rollouts and multinational exercises crowd frequencies and force military planners to juggle dynamic spectrum access schemes. Although spectrum-sharing initiatives unlock revenue for regulators, they complicate real-time video connectivity in urban combat where dozens of emitters coexist. To cope, link designers incorporate cognitive radios that sense and hop channels automatically, but the added circuitry increases cost and integration risk. These structural bandwidth pressures temper expansion in specific defense tactical video data link market segments.

SWaP-Cost Trade-offs on Small Platforms

Every gram of payload cuts endurance for nano-drones, and each watt of thermal load shortens soldier battery life. Designers rely on gallium-nitride RF amplifiers to squeeze efficiency gains, yet these devices raise procurement price and require specialized cooling. Balancing range, resolution, and runtime remains difficult, particularly for soldier-worn headsets that must fit within helmet rails and weight limits. Such trade-offs slow adoption among cash-strapped units and moderate the overall defense tactical video data link market growth rate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: UAV Dominance Meets Soldier-Worn Upswing

UAVs captured 40.65% of the defense tactical video data link market share in 2024, reinforcing their role as primary ISR workhorses that stream full-motion video to ground controllers. High-altitude endurance aircraft and small quadcopters rely on multi-band datalinks that sustain picture clarity over hundreds of kilometers. Edge-AI upgrades at the airframe compress raw feeds, flag targets, and escalate bandwidth demand. Though smaller in absolute value, soldier-worn systems clock the highest 12.10% CAGR as armies equip every squad with smart helmets and chest-mounted transmitters. The Defense Tactical Video Data Link market size for soldier platforms is projected to expand steadily as augmented-reality overlays transition from prototypes to standard issue.

Consistent with distributed-operations doctrine, ground vehicles and naval vessels retrofit uplinks so commanders receive identical video cues seen by airborne assets. Airborne manned surveillance planes adopt multi-channel gateways that rebroadcast pictures onto satellite networks. The recent release of L3Harris’s compact VORTEX®x transceiver unlocks gigabit-class throughput in a form factor suitable for small vehicles. Over the forecast horizon, platform diversification helps sustain overall demand even as UAV saturation in mature forces levels off, ensuring ongoing opportunity across the defense tactical video data link market.

By Frequency Band: Ku-Band Strength Faces Optical Momentum

Ku-band links held a 32.20% share of the defense tactical video data link market in 2024 due to legacy satellite coverage and dependable rain-fade margins. Militaries prefer the band for theater-level backhaul, yet dispersal of jamming systems prompts interest in higher frequencies. Optical/laser terminals record the fastest 13.50% CAGR because photons offer immunity to RF denial and support multi-gigabit rates over line-of-sight distances. Defense buyers test Ka-band terminals for forthcoming medium-earth constellations that promise lower latency.

VHF/UHF channels remain vital for beyond-horizon scatter in mountainous zones, while L/S-band radios backstop command networks when satellite or optical links fail. Free-space laser demonstrations between SpaceX satellites and ground nodes show operational feasibility, nudging procurement toward hybrid RF-optical architectures. As regulatory bodies re-farm spectrum, the defense tactical video data link market experiences a gradual realignment but retains Ku-band supremacy in the near term.

By Data Rate: Medium-Rate Sweet Spot With High-Rate Surge

Medium-rate solutions between 10 Mbps and 100 Mbps controlled 47.90% of 2024 spending because they balance image clarity and power draw. Battlefield video often streams at 720p or 1080p in compressed form that fits within this envelope. High-rate links over 100 Mbps, however, are rising at 11.40% CAGR as forces integrate 360-degree cameras, multi-spectral sensors, and AI metadata that inflate throughput requirements. The defense tactical video data link market size for high-rate categories will accelerate further once low-cost laser terminals mature.

Low-rate systems stay relevant for covert applications where a reduced spectral signature is prized over resolution. Adaptive bit-rate technology embedded in modern modems lets operators throttle quality down during interference and surge back to HD once conditions improve. This elasticity sustains situational awareness while conserving power, reinforcing cross-segment demand within the defense tactical video data link market.

By Component: Modem Leadership While Software Outpaces

Modems and routers represented 31.55% of the 2024 revenue, reflecting their indispensable role in translating sensor output into transmission waveforms. Future-proof designs now integrate encryption, routing, and quality-of-service in a single board, cutting size and weight. Yet the fastest growth comes from software modules that deliver dynamic waveforms and network-management analytics at a 12.75% CAGR. Militaries value the ability to patch in new anti-jam protocols overnight rather than procure new chassis. The defense tactical video data link market share for pure software remains small but strategically important.

Hardware subsystems such as antennas evolve toward electronically steered arrays that maintain link lock even as vehicles turn. Gallium-nitride power amplifiers lift transmitter efficiency, offsetting thermal constraints on small airframes. Encryption cards migrate toward quantum-resistant algorithms as procurement officials future-proof classified traffic. These trends underscore a shift to modular stacks that speed iterative upgrades throughout the defense tactical video data link market.

By End-user: Air Force Scale, Army Growth

Air Force programs accounted for 35.65% of 2024 demand, anchored by expansive UAV fleets and airborne command posts. Ongoing replacement of legacy CDL radios with Link-16-compatible blocks underpins steady refresh spending. The Army leads momentum at 9.70% CAGR as dismounted units adopt helmet-mounted displays and squad-level cross-links that weave every soldier into a real-time video mesh. Navy projects focus on littoral combat ships and amphibious craft that require ship-to-shore imagery synchronization.

Joint operations doctrine blurs once rigid service boundaries, prompting planners to favor common datalink standards. Consequently, procurement volumes spread across all branches, bolstering the aggregate defense tactical video data link market. Emerging partner nations imitate US modernization patterns, further diversifying the end-user mix and reducing volatility tied to any single service’s budget cycle.

Geography Analysis

North America generated 37.85% of global revenue in 2024, anchored by multi-year US IDIQ contracts such as L3Harris’s USD 999 million MIDS-JTRS award. The region’s regulatory rigor, including ITAR, crypto modernization, and SOSA compliance, favors incumbents possessing cleared supply chains. Accelerated CJADC2 fielding will keep procurement steady through 2030, while Canada will invest in NORAD modernization, including optical SATCOM experiments.

Asia-Pacific posts the fastest 10.65% CAGR as Japan, Australia, and India prioritize maritime domain awareness amid regional tensions. Indigenous R&D centers collaborate with US primes under technology-transfer frameworks, aiming to field Ka-band and optical terminals suited to island and mountain geographies. Robust growth also stems from UAV adoption among coast guards and paramilitary forces seeking persistent surveillance.

Europe shows measured expansion under NATO interoperability drives. Programs like France’s Syracuse SATCOM renewal and the UK’s Morpheus battlefield network allocate funds to open-architecture video links. GDPR demands rigorous data-protection layers, shaping secure-by-design procurement. Meanwhile, Middle East modernization generates sporadic but sizeable contracts, e.g., Israel’s USD 130 million order for Elbit radios. At the same time, Africa remains an emerging market with pilot deployments funded by counter-terror grants.

Competitive Landscape

The defense tactical video data link market features a moderate concentration. L3Harris, Viasat, and BAE Systems capitalize on enterprise integration, lifecycle support, and cleared manufacturing lines. Mid-tier firms like HENSOLDT and Curtiss-Wright target European and APAC programs with SOSA-ready VPX cards and ruggedized modem blades. Start-ups specialize in optical relays, AI encoders, and modular cryptos, leveraging venture backing to out-innovate on narrow fronts.

Strategic moves underscore the race: BAE’s USD 85 million NTCDL win cements naval credentials; HENSOLDT’s DL-6000 launch broadens multi-platform appeal; SpaceX-Tesat’s laser demo seeds a new wave of hybrid terminals. Patent filings in beam-steered arrays and lattice-based crypto surge, signaling the next battle lines. Participation in SOSA and IEEE working groups becomes as crucial as R&D spend, providing early insight into reference designs that will shape solicitations.

Pricing power pivots on SWaP and open-architecture compliance—buyers can now benchmark VPX module costs across vendors, compressing margins on hardware. Value migrates to DevSecOps services that patch waveforms and AI models over-the-air. As a result, integrators bundle software subscriptions into hardware sales, smoothing revenue visibility while capturing analytics telemetry for predictive maintenance.

Defense Tactical Video Data Link Industry Leaders

L3Harris Technologies, Inc.

Viasat, Inc.

Curtiss-Wright Corporation

Thales Group

Elbit Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: HENSOLDT unveiled its sixth-generation data link solution, the DL-6000. A leading global provider of sensor solutions, HENSOLDT designed the DL-6000 to ensure top-tier security and reliability. This advanced system facilitates the smooth exchange of high-definition video and telemetry data over long distances and across various platforms.

- September 2024: L3Harris Technologies secured a USD 182 million IDIQ contract from the US Air Force to deliver advanced situational awareness capabilities. The contract includes providing Video Data Link (VDL) technologies, such as ROVER® 6S and Tactical Network ROVER® (TNR) 2, in collaboration with the Air Force Life Cycle Management Center.

Global Defense Tactical Video Data Link Market Report Scope

| Ground Vehicles |

| Military Aircraft |

| Unmanned Aerial Vehicles (UAVs) |

| Naval Vessels |

| Soldier-Worn |

| C-Band |

| Ku-Band |

| Ka-Band |

| L/S-Band |

| VHF/UHF |

| Optical/Laser |

| Low (Less than 10 Mbps) |

| Medium (10 to 100 Mbps) |

| High (More than 100 Mbps) |

| Transmitters |

| Receivers |

| Antennas |

| Modems and Routers |

| Encryption and Security Modules |

| Software (Waveforms, NMS) |

| Army |

| Navy |

| Air Force |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Ground Vehicles | ||

| Military Aircraft | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| Naval Vessels | |||

| Soldier-Worn | |||

| By Frequency Band | C-Band | ||

| Ku-Band | |||

| Ka-Band | |||

| L/S-Band | |||

| VHF/UHF | |||

| Optical/Laser | |||

| By Data Rate | Low (Less than 10 Mbps) | ||

| Medium (10 to 100 Mbps) | |||

| High (More than 100 Mbps) | |||

| By Component | Transmitters | ||

| Receivers | |||

| Antennas | |||

| Modems and Routers | |||

| Encryption and Security Modules | |||

| Software (Waveforms, NMS) | |||

| By End-user | Army | ||

| Navy | |||

| Air Force | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Defense Tactical Video Data Link market?

The defense tactical video data link market is valued at USD 4.81 billion in 2025 and is projected to reach USD 7.23 billion by 2030.

Which platform segment leads sales?

UAVs hold 40.65% of 2024 revenue, making them the largest segment.

Which region is expanding fastest?

Asia-Pacific shows the highest growth with a 10.65% CAGR through 2030.

Why are optical/laser links gaining attention?

They offer jam-resistant, gigabit-class throughput that addresses electronic warfare (EW) threats.

How does SOSA compliance affect procurement?

Open-architecture mandates favor modular, interoperable components, accelerating upgrade cycles and vendor competition.

Page last updated on: