Air And Missile Defense Radar Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

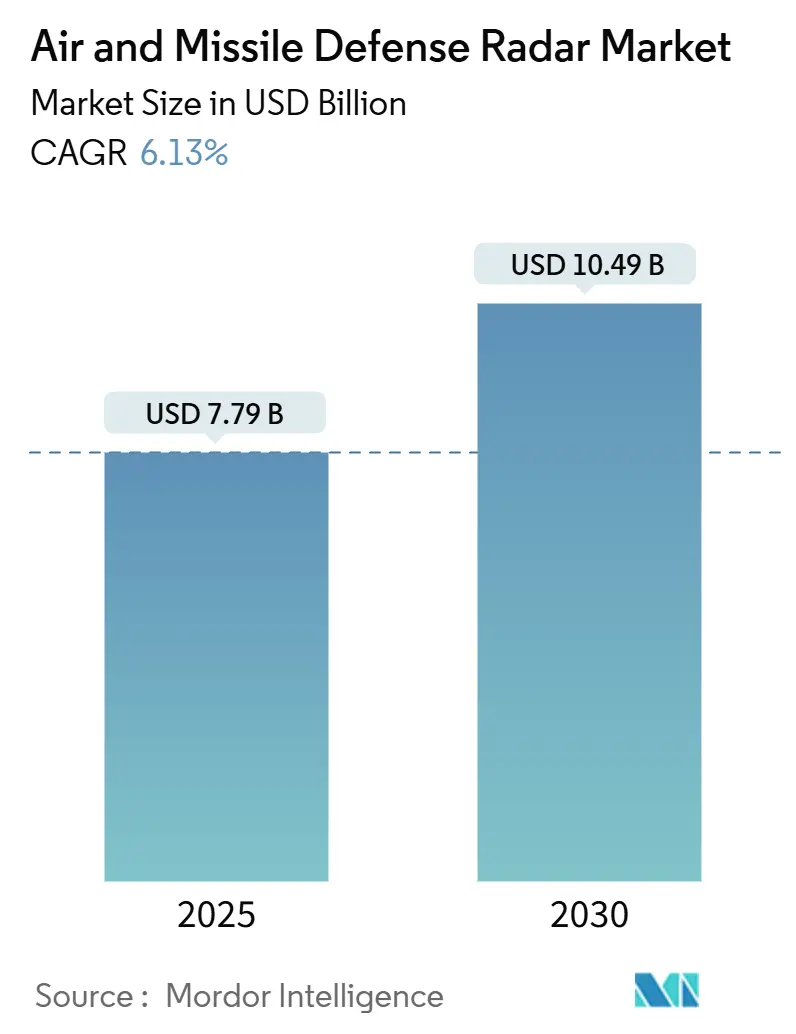

| Market Size (2025) | USD 7.79 Billion |

| Market Size (2030) | USD 10.49 Billion |

| Growth Rate (2025 - 2030) | 6.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air And Missile Defense Radar Market Analysis by Mordor Intelligence

The air and missile defense radar market size stands at USD 7.79 billion in 2025 and is projected to reach USD 10.49 billion by 2030, reflecting a 6.13% CAGR during the forecast period. Robust spending aimed at countering hypersonic, ballistic, and maneuverable missiles, accelerated fleet modernization across navies, and the pivot from mechanically scanned arrays to gallium-nitride (GaN) Active Electronically Scanned Array (AESA) architectures are the primary growth catalysts. Investments in artificial intelligence-enabled signal processing, multi-domain command-and-control frameworks, and layered counter-UAS portfolios further reinforce expansion prospects for the air and missile defense radar market. Defense agencies are also reallocating budgets toward software-defined upgrades that extend radar service life while enhancing resilience against electronic countermeasures. Finally, steady export demand from allied nations seeking interoperability with US and NATO systems underpins the near-term revenue outlook.

Key Report Takeaways

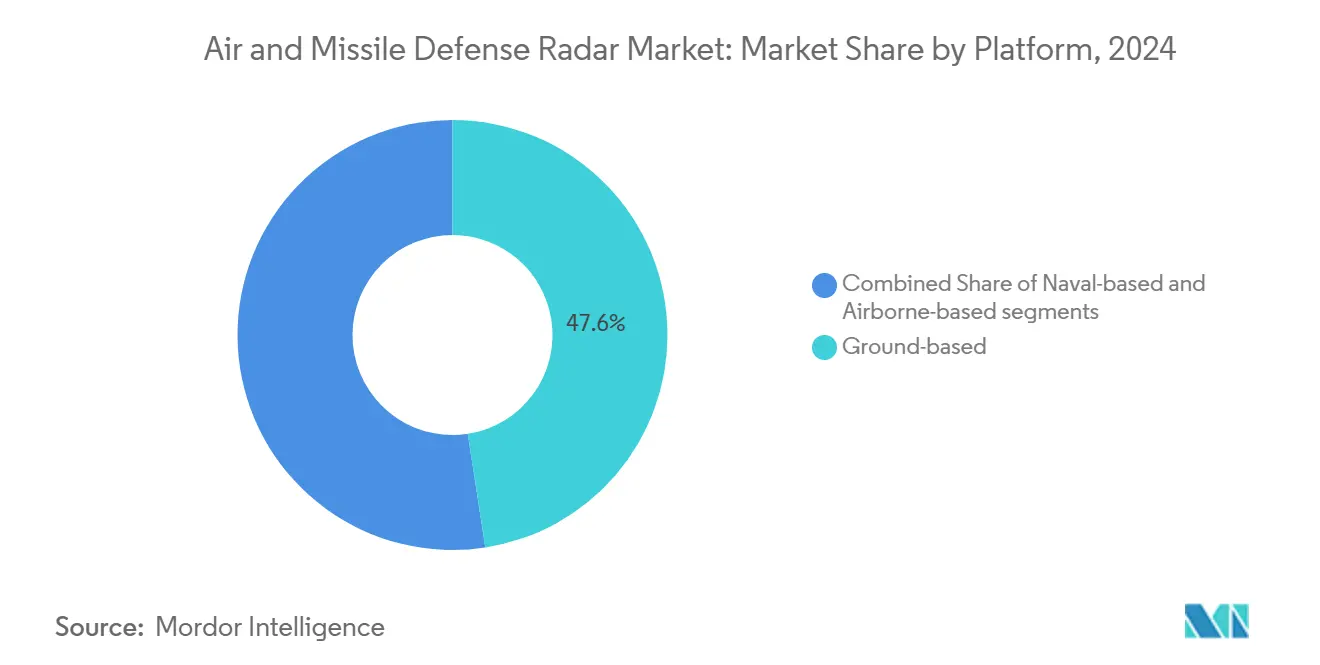

- By platform, ground-based radars led with 47.56% of the air and missile defense radar market share in 2024, while naval-based systems are advancing at a 6.78% CAGR to 2030.

- By range capability, long-range sensors commanded 49.24% of the air and missile defense radar market size in 2024; short-range solutions are forecasted to expand at a 6.81% CAGR through 2030.

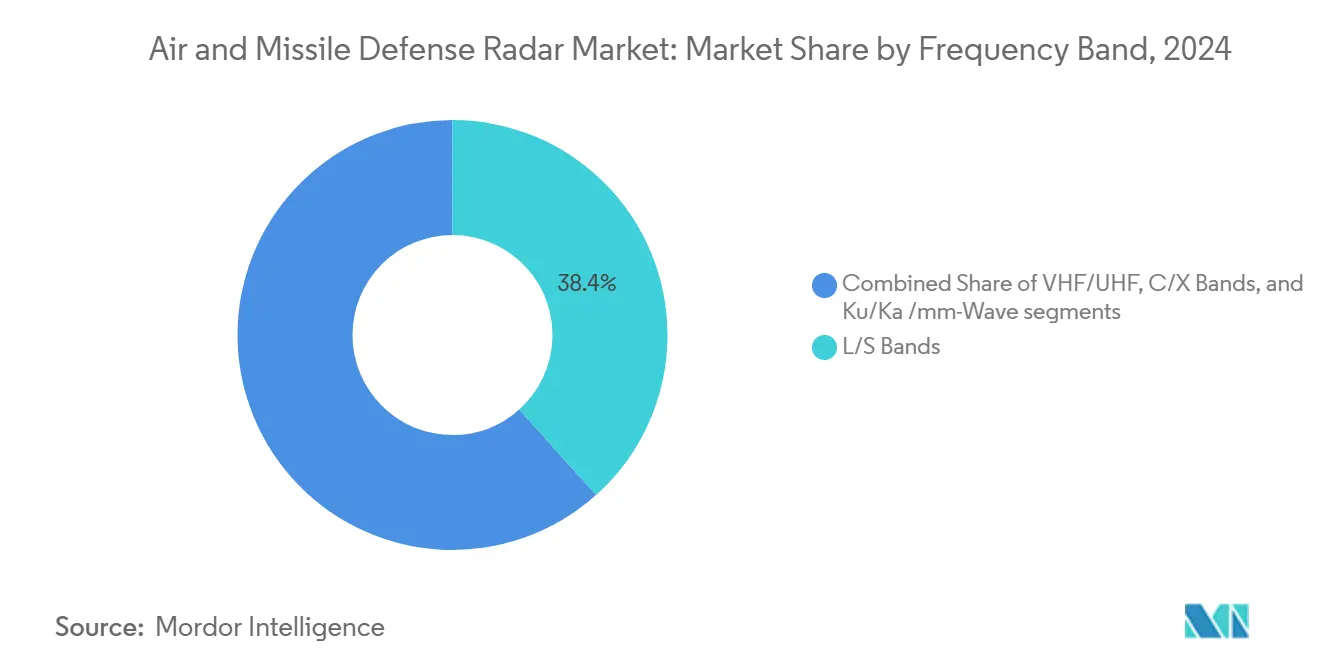

- By frequency band, L/S bands accounted for 38.37% share of the air and missile defense radar market in 2024, and Ku/Ka/mm-Wave technologies are growing at a 7.21% CAGR to 2030.

- By technology, AESA platforms captured 46.77% share and delivered the fastest 7.35% CAGR through 2030 within the air and missile defense radar market.

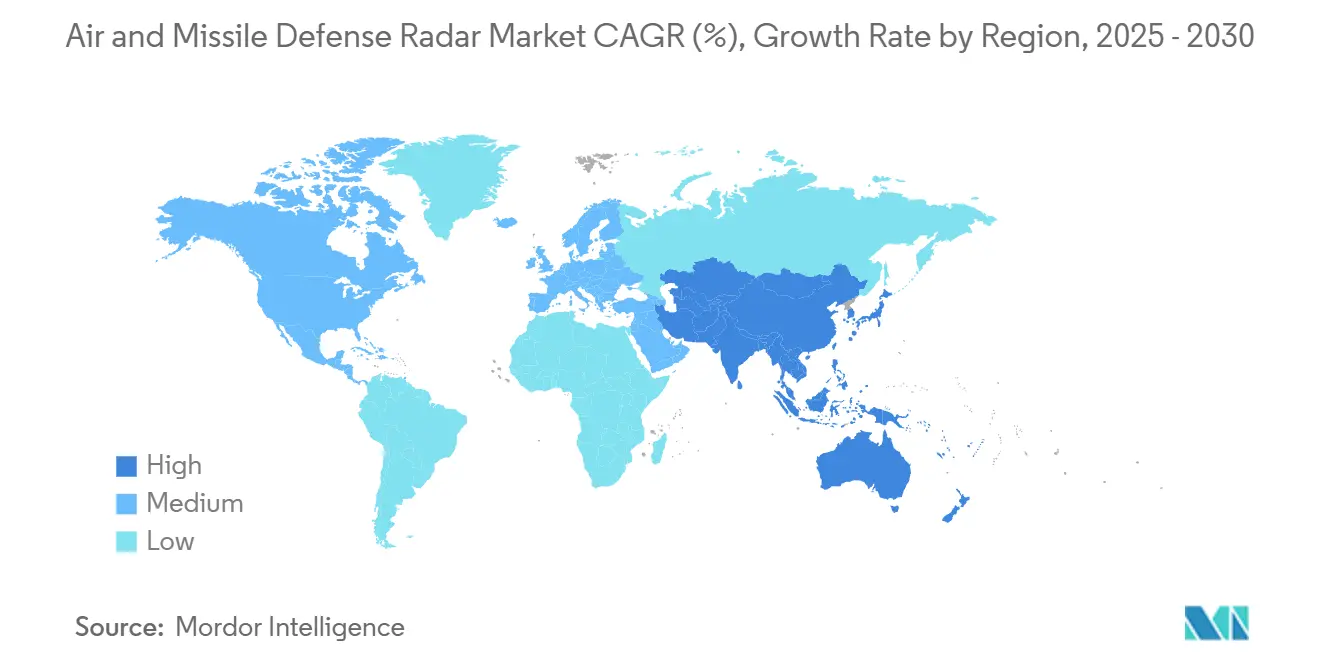

- By geography, North America held a 38.85% share of 2024 revenues, whereas Asia-Pacific registered the highest 7.01% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Air And Missile Defense Radar Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating threat from hypersonic, ballistic, and maneuverable missile systems | +1.2% | Global; high in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growing adoption of multi-domain integrated air and missile defense architectures | +0.9% | North America, Europe, expanding Asia-Pacific | Long term (≥4 years) |

| Technological shift toward GaN-based AESA radars offering full-spectrum 360° coverage | +1.1% | Global; led by North America, Europe | Medium term (2-4 years) |

| Rising demand for counter-UAS and layered air defense capabilities | +0.8% | Global; emphasis Middle East, Asia-Pacific | Short term (≤2 years) |

| Emergence of AI-driven radar data fusion for real time threat classification | +0.7% | North America and Europe, with Asia-Pacific adoption | Medium term (2-4 years) |

| Increasing emphasis on mobile, networked radar platforms for forward area surveillance | +0.6% | Global, with focus on contested regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Threat from Hypersonic, Ballistic, and Maneuverable Missile Systems

Hypersonic glide vehicles and maneuverable re-entry warheads travel at Mach 5+ and maneuver unpredictably, stretching legacy radar performance envelopes. Russian Kinzhal and Zircon deployments and China’s DF-ZF program spurred NATO nations to prioritize systems such as RTX Corporation’s AN/TPY-2, whose deliveries climbed 35% in 2024.[1]Missile Defense Agency, “FY 2025 Budget Overview,” mda.mil Layered architectures linking space-based infrared sensors with long-range ground radars extend warning times and enable earlier engagement windows. As a result, defense ministries require radars capable of 2,000 km detection coupled with high update rates to support interceptor cueing. This imperative continues accelerating procurement cycles across the air and missile defense radar market.

Growing Adoption of Multi-Domain Integrated Air and Missile Defense Architectures

Joint All-Domain Command and Control (JADC2) efforts demand radars that feed standardized, machine-readable tracks into shared battle-management networks.[2]U.S. Department of Defense, “Joint All-Domain Command and Control Strategy,” defense.gov Achieving this interoperability involves open data formats and standard waveforms across sensors commissioned decades apart. NATO’s Integrated Air and Missile Defense initiative mandates member radars to exchange real-time engagement-quality tracks. Northrop Grumman’s software-configurable G/ATOR illustrates radar adaptability by switching missions—from air-surveillance to counter-battery—via remote software loads. Seamless data fusion reshapes procurement specifications and reinforces data-centric doctrines that propel the air and missile defense radar market.

Technological Shift Toward GaN-Based AESA Radars Offering Full-Spectrum 360° Coverage

GaN transmit/receive modules deliver triple the power density of gallium arsenide devices and tolerate higher junction temperatures. Raytheon’s SPY-6 family demonstrates these advantages with scalable sub-array “building blocks” that provide full azimuth coverage and resist jamming. Commercial foundries like Wolfspeed and Qorvo have ramped military-grade GaN wafer output, shrinking costs and enhancing component reliability. Although typical air and missile defense radar market development programs require USD 500–800 million and four to six years of qualification, adopters gain multi-mission flexibility, graceful degradation through element-level failures, and simplified future upgrades through modular line replaceable units.

Rising Demand for Counter-UAS and Layered Air Defense Capabilities

Proliferation of quad-copters, fixed-wing drones, and low-slow targets reshapes site-defense planning. Radars must spot 0.01 m² cross-section drones operating below treetop height amid urban clutter. HENSOLDT’s passive-receiver TwInvis exploits commercial broadcast reflections to classify rotor-blade modulations, illustrating innovation beyond traditional monostatic radars. Militaries now field nested “dome-within-dome” configurations, combining short-range Ku-band sensors with medium-range C-band fire-control radars. This layered approach safeguards critical assets and expands addressable opportunities for the air and missile defense radar market.

Restraints Impact Analysis of Air And Missile Defense Radar Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procurement cost and long qualification timelines of next-gen AESA systems | −0.8% | Global; stringent on smaller budgets | Long term (≥4 years) |

| Frequency spectrum allocation constraints limiting radar deployment flexibility | −0.7% | Global; concentrated Asia-Pacific fabs | Short term (≤2 years) |

| Supply chain limitations for T/R modules and specialized semiconductor components | -0.7% | Global, concentrated in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Stringent cybersecurity compliance requirements delaying international exports | -0.4% | North America and Europe export markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procurement Cost and Protracted Qualification Timelines

A full-scale next-gen AESA system can range from USD 50 million to USD 200 million per installation, stretching strained budgets in emerging economies.[3]Government Accountability Office, “Weapon Systems Annual Assessment,” gao.gov Rigorous environmental, electromagnetic-compatibility, and software-safety testing extend program cycles to seven years, during which operational requirements often evolve. The US Army’s LTAMDS budget overran 40% in development, underscoring cost-escalation risk. Export buyers confront Foreign Military Sales procedures that layer an extra one-to two-year paperwork queue, slowing international revenues for the air and missile defense radar market.

Supply Chain Limitations for T/R Modules and Specialized Semiconductors

Advanced GaN wafers rely on limited foundry capacity in Taiwan and South Korea. Since 2024, lead times for radiation-hardened power amplifiers have stretched to 36 weeks as 5G and automotive demand have competed for substrate allocation. RTX Corporation cited 6–12-month shipment delays on multiple radar contracts, forcing inventory buffering and contract modifications. These disruptions constrain near-term production volumes and dampen air and missile defense radar market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Air And Missile Defense Radar Market Segment Analysis

By Platform:

Ground Systems Anchor Defense ArchitectureGround-based units provided 47.56% of 2024 revenues, cementing their role as backbone sensors that tie into fixed command centers and leverage unrestricted prime power. These platforms integrate seamlessly with interceptor batteries such as Patriot and THAAD, forming the core of layered homeland defense. The air and missile defense radar market benefits from incremental upgrades—antenna aperture expansions, digital-beam-forming retrofits, and AI-enabled clutter rejection—that extend installed-base relevance without complete system replacement. Forward-deployed mobile variants add tactical flexibility, allowing rapid redeployment to contested theaters.

Naval assets, meanwhile, are on track for the strongest 6.78% CAGR as maritime forces pursue holistic ship self-defense. Modular SPY-6 arrays aboard Flight III Arleigh Burke destroyers and the Royal Australian Navy’s Hobart-class upgrades illustrate fleet-wide rollouts. These sea-based radars require robust environmental sealing and stabilize their electronically steered beams despite pitch and roll, an engineering challenge that elevates contract values. Consequently, naval adoption materially widens the revenue pool for the air and missile defense radar market.

By Range Capability:

Long-Range Detection Drives LeadershipLong-range sensors constituted 49.24% of 2024 billings, mirroring strategic demands for 1,000 km+ surveillance that grants commanders crucial engagement lead-time. Systems like the AN/TPY-4 provide over-the-horizon cueing for exo-atmospheric interceptors and integrate with space-tracking constellations. The segment’s dominance ensures continuous procurement pipelines as hypersonic proliferation intensifies.

Short-range radars deliver the fastest 6.81% CAGR, propelled by counter-UAS, gap-filler, and point-defense programs. Low-power Ku-band sensors complement high-power L-band assets, enhancing low-altitude coverage across urban and mountainous terrain. This upswing enables diversified air and missile defense radar market revenue channels. It encourages small-form-factor innovations such as vehicle-mounted or tripod-based arrays for expeditionary forces.

By Frequency Band:

L/S Bands Lead While mm-Wave AcceleratesThe L/S spectrum retained a 38.37% share in 2024 owing to its balanced propagation, weather penetration, and respectable target resolution—even at extended distances. Mature components, proven signal-processing chains, and existing logistics make L/S upgrades cost-effective, sustaining recurring orders. Operators frequently pair L-band search radars with X-band fire-control channels, leveraging complementary physics.

Ku/Ka/mm-Wave radars are surging at 7.21% CAGR as GaN technology boosts power output and mitigates rain-fade losses. Their superior angular resolution is ideal for small cross-section threats, including swarming drones and cruise missiles flying nap-of-the-earth. Compact antennas facilitate installation on mobile launchers, broadening adoption across the air and missile defense radar market. Multi-band agility now appears on acquisition roadmaps, enabling radars to auto-select optimal frequencies based on mission dynamics.

By Technology:

AESA Dominance Accelerates InnovationAESA solutions controlled 46.77% of 2024 revenues and will compound at 7.35% CAGR through 2030. Thousands of solid-state T/R modules electronically steer beams within microseconds, supporting simultaneous search, track, and fire-control roles. Array element redundancy yields graceful degradation—if one module fails, performance tapers but the mission continues, a compelling value proposition for combat resilience.

Passive electronically scanned array (PESA) and mechanically steered architectures persist in cost-sensitive or specialty roles, yet their share declines as operators prioritize software-defined functionalities. AESA’s digital back-ends allow waveform updates via remote patches, speeding capability insertion and sustaining the air and missile defense radar market’s technology edge.

Geography Analysis

North America Air And Missile Defense Radar Market

North America generated 38.85% of 2024 turnover, fueled by the US Department of Defense's (DoD's) layered missile-defense roadmap that funds Ground-Based Midcourse Defense, THAAD, and SPY-6 procurement.[4]Defense Security Cooperation Agency, “FMS Programs 2025,” dsca.mil Canadian NORAD modernization budgets and Mexican counter-narcotics surveillance needs add incremental upside. Extensive foreign-military-sales (FMS) programs export US radars to allied nations, reinforcing revenue resilience for the air and missile defense radar market.

APAC Air And Missile Defense Radar Market

Asia-Pacific's 7.01% CAGR through 2030 is driven by Japan's Aegis Ashore deployments, India's Long-Range Tracking Radar program, and Australia's participation in trilateral missile-defense data-sharing under AUKUS. Indigenous capability builds—such as South Korea's KM-SAM AESA—illustrate regional commitment to technological sovereignty, deepening local supply chains, and increasing competitive intensity.

EMEA Air And Missile Defense Radar Market

Europe sustains steady demand via NATO interoperability mandates and pooled funding under the European Sky Shield Initiative. HENSOLDT, Thales, and Leonardo field scalable systems that dovetail with multinational command frameworks. Although the Middle East and Africa account for a smaller spending base, marquee contracts—Saudi Arabia's THAAD acquisition and UAE Patriot upgrades—underscore selective, high-value opportunities that buttress broader growth within the air and missile defense radar market.

Competitive Landscape

The air and missile defense radar market exhibits moderate concentration: RTX Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, and Leonardo S.p.A. collectively dominate multi-domain programs, leveraging integrated sensor-to-shooter portfolios and decades-old customer intimacy. Contract timelines stretch 10 to 15 years, reinforcing incumbency advantages and deterring new entrants. However, open-architecture mandates and modular designs lower integration barriers, enabling component specialists to capture subsystem niches.

Strategic themes revolve around GaN fabrication expansion, AI-powered track classification, and multi-mission re-programmability. RTX’s Massachusetts fab ramp-up lifted T/R module output 40% in 2024, underpinning SPY-6 and TPY-2 pipelines. Lockheed Martin’s USD 950 million THAAD upgrade integrates its interceptor and radar franchises, fortifying its share in exo-atmospheric defense. Emerging threats spur partnerships—Saab-Hanwha’s Korean AESA joint venture, HENSOLDT-Rheinmetall’s counter-UAS alliance—widening technology diffusion and bolstering optionality for defense ministries.

While top primes retain procurement primacy, value-chain whitespace persists in digital beamforming software, cyber-hardened signal processors, and lightweight composite radomes. Suppliers targeting these domains can secure footholds even as overall concentration persists within the air and missile defense radar market.

Air And Missile Defense Radar Industry Leaders

RTX Corporation

Lockheed Martin Corporation

Northrop Grumman Corporation

Thales Group

Leonardo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Air And Missile Defense Radar Market Companies Covered in this Report

- RTX Corporation

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Thales Group

- Leonardo S.p.A.

- Saab AB

- Israel Aerospace Industries Ltd.

- HENSOLDT AG

- BAE Systems plc

- Rheinmetall AG

- Hanwha Aerospace (Hanwha Corporation)

- Mitsubishi Electric Corporation

Recent Industry Developments in Air And Missile Defense Radar Market

- September 2025: RTX received a USD 1.7 billion contract from the US Army to deliver the Lower Tier Air and Missile Defense Sensor (LTAMDS), a new generation radar system.

- June 2025: RTX Corporation delivered the first AN/TPY-2 radar with a complete GaN-populated array to the US Missile Defense Agency. The AN/TPY-2 missile defense radar detects, tracks, and discriminates ballistic missiles during multiple flight phases to protect the US homeland and its allies.

- May 2025: Hanwha Systems secured a contract with South Korea's Agency for Defense Development (ADD) to develop a next-generation Multi-Function Radar (MFR) for the L-SAM-II system. The L-SAM-II represents the second phase of the Long-Range Surface-to-Air Missile program.

Global Air And Missile Defense Radar Market Report Scope

Segmentation Overview

| Ground-based |

| Naval-based |

| Airborne-based |

| Short |

| Medium |

| Long |

| VHF/UHF |

| L/S Bands |

| C/X Bands |

| Ku/Ka/mm-Wave |

| Active Electronically Scanned Array (AESA) |

| Passive Electronically Scanned Array (PESA) |

| Mechanically-Scanned and Hybrid |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Ground-based | ||

| Naval-based | |||

| Airborne-based | |||

| By Range Capability | Short | ||

| Medium | |||

| Long | |||

| By Frequency Band | VHF/UHF | ||

| L/S Bands | |||

| C/X Bands | |||

| Ku/Ka/mm-Wave | |||

| By Technology | Active Electronically Scanned Array (AESA) | ||

| Passive Electronically Scanned Array (PESA) | |||

| Mechanically-Scanned and Hybrid | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Air and Missile Defense Radar market by 2030?

The air and missile defense radar market is forecasted to reach USD 10.49 billion by 2030, growing at a 6.13% CAGR.

Which platform segment contributes the most revenue today?

Ground-based systems lead with 47.56% share of 2024 revenues due to their pivotal role in homeland and forward-deployed defense.

Which region is expanding fastest?

Asia-Pacific is advancing at a 7.01% CAGR through 2030, fueled by modernization programs in Japan, India and Australia.

Why are GaN-based AESA radars gaining traction?

GaN delivers higher power density, better thermal management and multi-beam agility, driving AESA adoption and a 7.35% CAGR through 2030.

How are supply chain challenges impacting deliveries?

Limited GaN wafer capacity and extended semiconductor lead times have stretched radar deliveries by up to 12 months since 2024.

What role do counter-UAS requirements play in new procurements?

Rising drone threats are boosting demand for short-range Ku/Ka-band radars, the fastest-growing range segment at a 6.81% CAGR.

Page last updated on: