Data Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

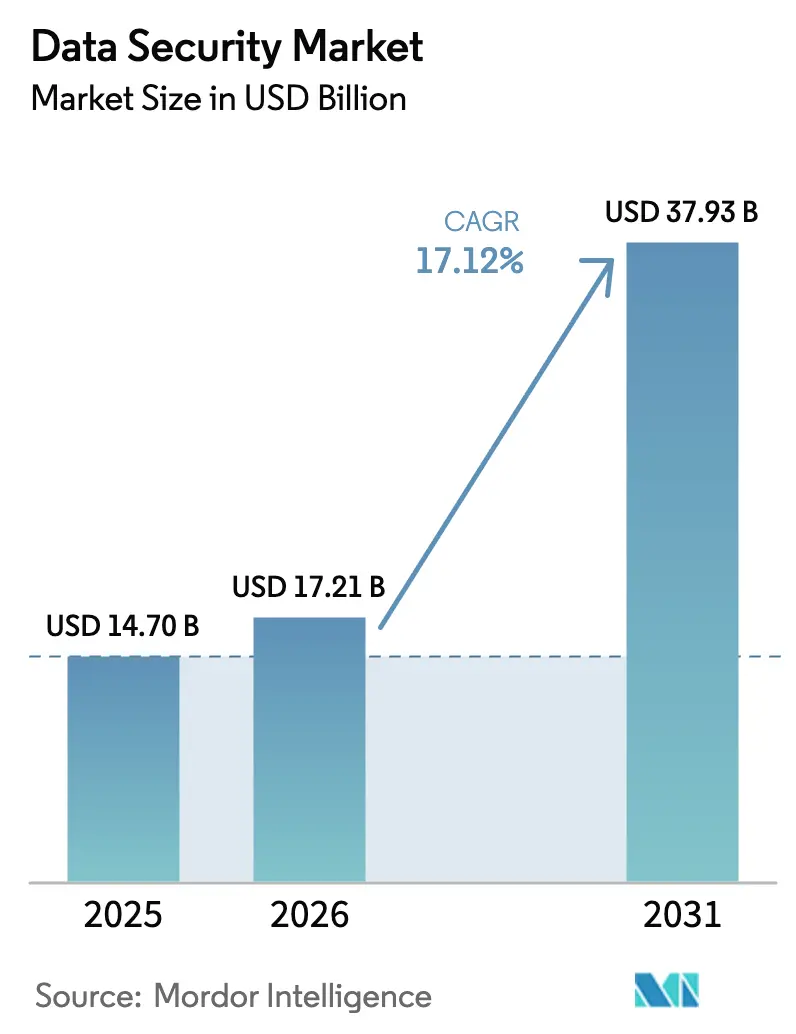

| Market Size (2026) | USD 17.21 Billion |

| Market Size (2031) | USD 37.93 Billion |

| Growth Rate (2026 - 2031) | 17.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Security Market Analysis by Mordor Intelligence

The data security market size was valued at USD 14.70 billion in 2025 and estimated to grow from USD 17.21 billion in 2026 to reach USD 37.93 billion by 2031, at a CAGR of 17.12% during the forecast period (2026-2031). The expansion is propelled by mounting cyber-attack sophistication, fast-evolving privacy mandates, and ballooning data volumes created across increasingly hybrid and multi-cloud infrastructures. Enterprises are modernizing cryptography in anticipation of quantum threats, embedding zero-trust controls across distributed workloads, and consolidating fragmented toolsets into unified policy frameworks. Service-led delivery models are gaining ground as skills shortages persist, and confidential computing is progressing from pilots to production, readying the ecosystem for data-in-use protection. Simultaneously, AI-driven lineage mapping is compressing breach dwell time and enabling continuous compliance, while tokenization is scaling across open-banking APIs and real-time payment rails.

Key Report Takeaways

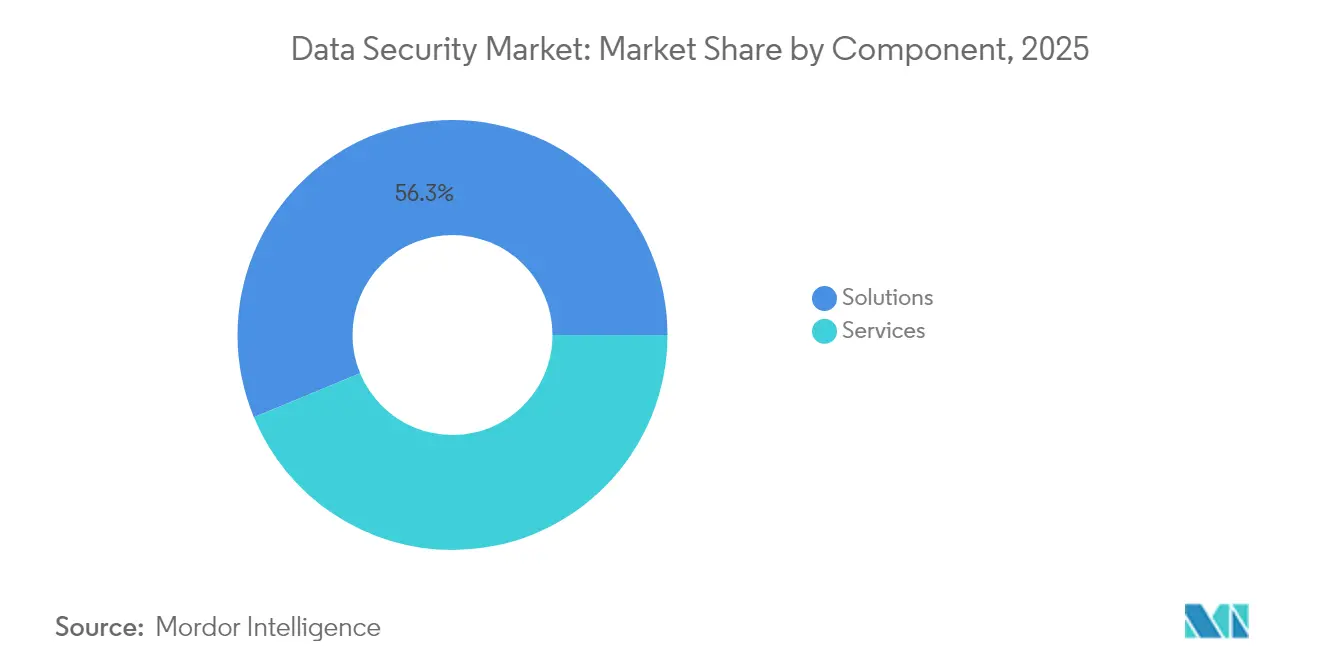

- By component, Solutions held 56.25% of the data security market share in 2025, while Services are on track to grow at 18.23% CAGR to 2031.

- By deployment mode, On-premises controlled 66.62% of the data security market size in 2025; Cloud deployments are projected to expand at 18.62% CAGR through 2031.

- By organization size, Large Enterprises captured 70.35% of the data security market size in 2025, yet the SME segment is forecast to post a 18.74% CAGR through 2031.

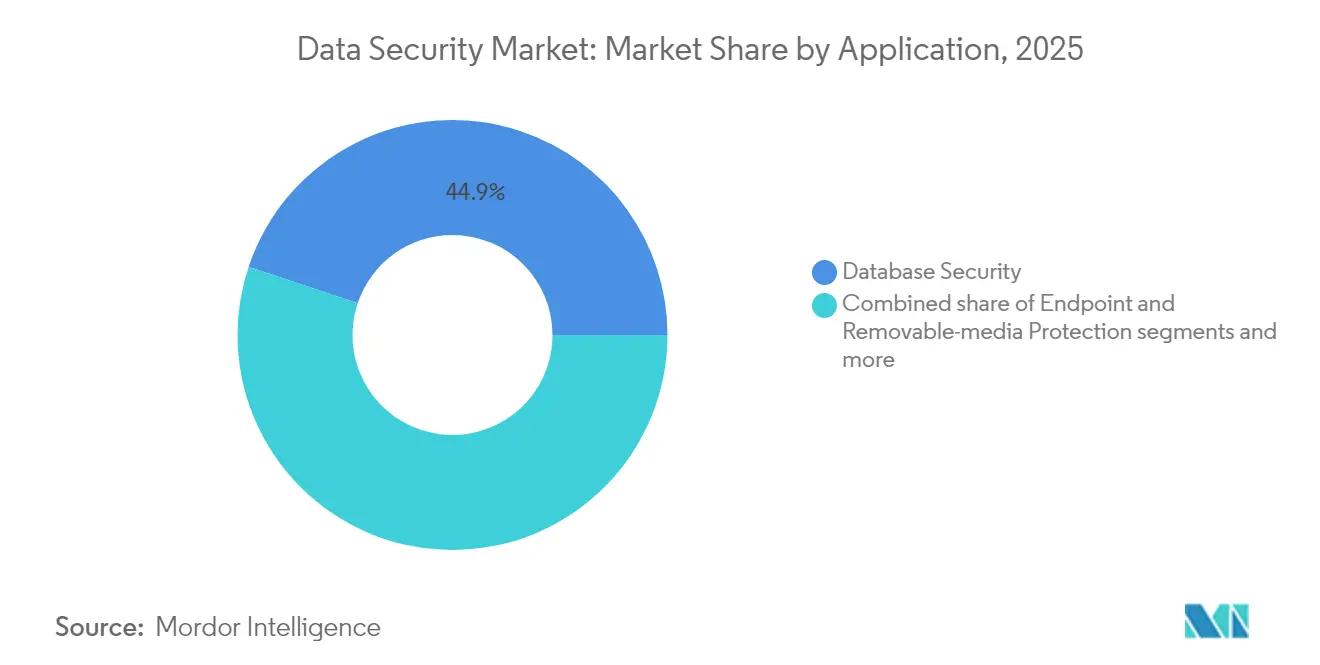

- By application, Database Security commanded 44.85% of the data security market size in 2025, whereas DevOps and Container Security is advancing at an 18.02% CAGR.

- By end-user industry, Banking, Financial Services and Insurance led with 22.35% of the data security market share in 2025; Healthcare and Life Sciences is expected to grow at 17.45% CAGR to 2031.

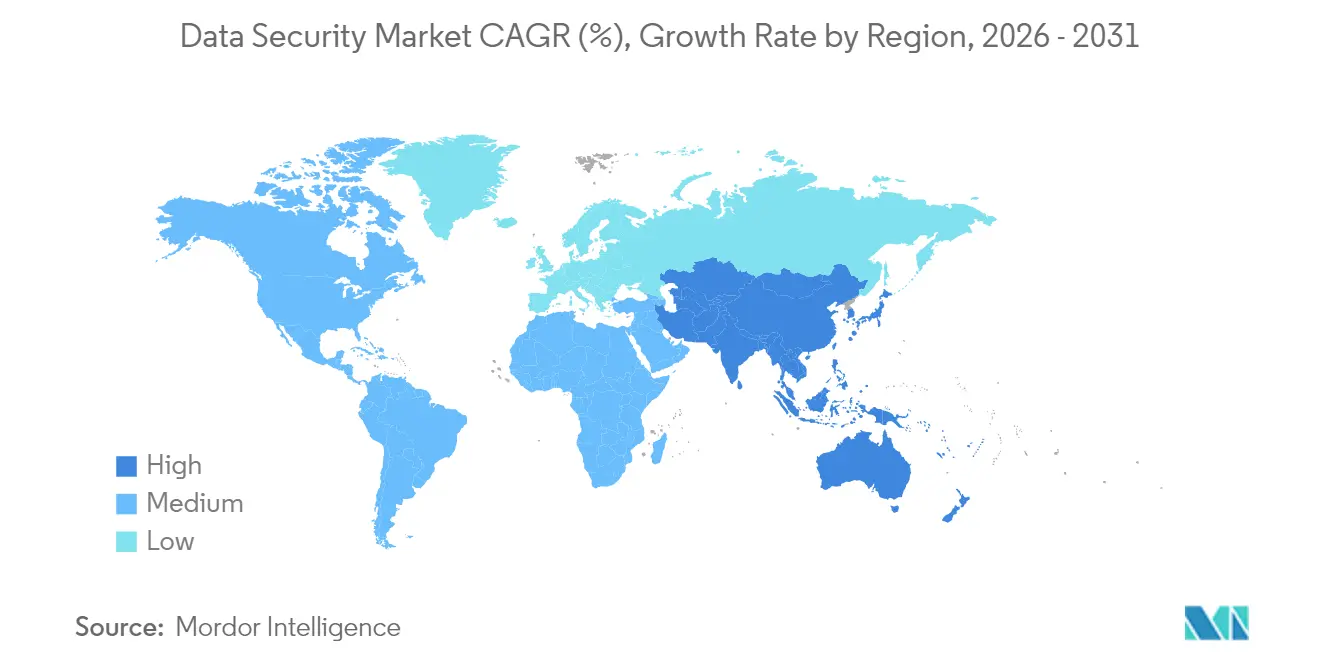

- By geography, North America retained 40.74% of the data security market size in 2025, and Asia-Pacific is forecast to progress at an 17.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acceleration of multi-cloud adoption drives demand for cloud-native data-centric security tools | +3.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Stricter privacy regimes mandate data discovery and classification solutions | +2.8% | Global, led by EU, expanding to Asia-Pacific and Americas | Short term (≤ 2 years) |

| Hardware-based confidential computing matures beyond pilots | +2.1% | North America & EU core markets, spillover to Asia-Pacific | Long term (≥ 4 years) |

| AI-assisted data lineage reduces breach dwell time and cuts compliance audit costs | +2.4% | Global, with early adoption in North America | Medium term (2-4 years) |

| Tokenisation gains traction in Open-Banking APIs and real-time payments rails | +1.9% | Europe and North America leading, Asia-Pacific following | Medium term (2-4 years) |

| Quantum-safe cryptography pilots in government and telecom sectors create new upgrade cycle | +1.8% | Government sectors globally, telecom in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acceleration of Multi-Cloud Adoption Drives Demand for Cloud-Native Data-Centric Security Tools

Eighty-two percent of breaches now involve cloud-hosted data, with average incident cost standing at USD 4.88 million.[1]IBM Corporation, “Cost of a Data Breach Report 2025,” ibm.com Traditional perimeter defenses lack visibility across AWS, Azure, and Google Cloud, prompting enterprises to consolidate controls into platforms that apply uniform policies across hybrid estates. Microsoft’s 2024 multicloud risk study highlights governance blind spots created by the shared-responsibility model, intensifying the push toward integrated, zero-trust architectures. Vendors providing continuous posture management, encryption key orchestration, and identity-centric segmentation are gaining preference as organizations recognize that scaling legacy point products will not secure cloud-native workloads. The result is a decisive shift in budget allocation toward solutions optimized for distributed, API-driven environments.

Stricter Privacy Regimes Mandate Data Discovery and Classification Solutions

Eighty percent of countries now enforce comprehensive data-protection statutes, and eight new U.S. state privacy laws took effect in 2025. Europe’s NIS2 Directive alone extends security obligations to about 300,000 entities, adding penalties up to EUR 10 million for non-compliance. Such breadth compels enterprises to move from reactive check-box compliance to real-time governance anchored in automated discovery, classification, and masking. Acute talent shortages aggravate the challenge; 73% of firms struggle to hire seasoned privacy engineers, so demand for low-touch machine-learning classifiers and policy engines is soaring. Vendors delivering high-fidelity scanning across structured and unstructured repositories while mapping attribute provenance are positioned to capture the surge in privacy-driven spend.

Hardware-Based Confidential Computing Matures Beyond Pilots

Trusted execution environments that shield data while in use are expanding beyond proof-of-concept status, with 86% of organizations planning to run generative-AI workloads in such enclaves. Financial-market infrastructures and telecoms are piloting quantum-safe crypto stacks, ensuring transaction integrity across future threat horizons.[2]BIS Innovation Hub, “Project FuSSE: Quantum-Safe Financial Transactions,” bis.org As Intel, AMD, and ARM embed secure memory isolation at the silicon layer, deployment friction falls, unlocking use cases in healthcare diagnostics, sovereign cloud analytics, and blockchain validation. Commercial platforms now support workload attestation and policy-based key release, enabling enterprises to process sensitive datasets in hosted clouds without exposing raw content to providers.

AI-Assisted Data Lineage Reduces Breach Dwell Time and Cuts Compliance Audit Costs

Generative-AI copilots embedded in tools such as IBM Guardium summarize risks, surface configuration drift, and propose remediation steps, compressing detection and response cycles. Continuous lineage graphs now auto-document data-flow dependencies across microservices, which simplifies evidence gathering for GDPR, HIPAA, and LGPD audits. Machine learning models label sensitive objects and auto-generate compliance artifacts, saving internal teams hundreds of staff-hours per audit window. As regulators increase scrutiny of real-time risk posture, organizations adopting AI-driven governance gain both operational resilience and cost advantages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High TCO of enterprise-wide data discovery for unstructured "dark data" | -1.4% | Global, particularly affecting mid-market enterprises | Short term (≤ 2 years) |

| Skills gap in privacy engineering and homomorphic encryption hampers deployments | -2.1% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Legacy mainframe and OT systems incompatible with modern zero-trust architectures | -1.6% | North America and Europe, with legacy industrial systems | Long term (≥ 4 years) |

| Fragmented regional data residency laws inflate compliance overhead | -1.3% | Global, particularly complex in Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skills Gap in Privacy Engineering and Homomorphic Encryption Hampers Deployments

The cybersecurity workforce deficit remains near 4 million roles, with demand for quantum-safe and differential-privacy specialists far outstripping supply. Organizations channel between USD 1.2 million and USD 2.7 million on privacy programs over three years yet still postpone advanced encryption projects due to staffing constraints. Economic headwinds have triggered hiring pauses that widen the capability gap. The scarcity presses enterprises to rely on managed services, delaying internal capacity building and lengthening deployment cycles for cutting-edge protections.

High TCO of Enterprise-Wide Data Discovery for Unstructured “Dark Data”

Proposed HIPAA Security Rule updates estimate first-year compliance outlays of USD 9.3 billion, with ongoing costs at USD 6.8 billion. SMEs lacking scale discover that scanning petabytes of legacy files, emails, and backups requires significant compute and licensing budgets. Forty percent of smaller firms experience cyber impacts but still underinvest in comprehensive discovery. As budgets remain flat, many companies prioritize targeted repositories, leaving swaths of unclassified content vulnerable and depressing near-term spending momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Acceleration Outpaces Solutions Growth

Solutions continued to contribute 56.25% of 2025 revenue, anchored by encryption, data-loss prevention, and database-protection suites that form the defensive core of the data security market. Nevertheless, managed and professional offerings are growing at an 18.23% CAGR as boards confront an acute talent shortage and shift toward outcome-based contracting models. Regulatory rollouts such as NIS2 are amplifying demand for readiness assessments and 24 × 7 security-operations coverage, positioning service providers as strategic partners. Cloud-centric platforms, tokenization for real-time payments, and quantum-ready encryption bundles are broadening the scope of managed portfolios, further diluting pure-software share.

The pivot from product to service also reflects buyer preference for scalable, OpEx-friendly consumption. Vendors embed incident-response retainers, compliance automation, and continuous posture management within subscription constructs. High-growth sub-segments include Data Security Posture Management, where managed detection cuts dwell time by 43%, and Advisory services guiding cryptographic modernization. As a result, the data security market is witnessing layered offerings that converge tooling, expertise, and program governance into unified SLAs.

By Deployment Mode: Cloud Gains Despite On-Premises Dominance

On-premises models retained 66.62% revenue in 2025, reflecting strict data-sovereignty regimes and mission-critical workloads that resist relocation. Yet the cloud share is expanding at 18.62% CAGR, underscoring hybrid realities where SaaS, PaaS, and container pipelines demand integrated protection layers across trust boundaries. The data security market size for cloud deployments is set to widen markedly, helped by confidential-computing safeguards that satisfy encryption-in-use mandates.

Enterprises adopt architecture splits: sensitive analytics run in private clouds or physical data centers, whereas customer-facing microservices leverage scalable public-cloud controls. Unified key-management and policy-orchestration tools bridge environments, reducing operational silos. Regulatory frameworks such as NIS2 award flexibility to entities that can prove real-time monitoring, which favors cloud-native analytics dashboards. Consequently, vendor roadmaps increasingly highlight agnostic control planes and host-based attestation that follow data wherever it resides.

By Organization Size: SME Segment Accelerates Despite Enterprise Dominance

Large Enterprises still contribute 70.35% of sector turnover, backed by expansive IT estates and baseline compliance obligations. Yet smaller firms represent the fastest-growing cohort at 18.74% CAGR, propelled by lower barriers to entry via SaaS security stacks. The data security market size for SMEs is rising as state-level privacy laws extend liability, compelling adoption of encryption and multi-factor authentication even in sub-1,000-employee environments.

Cloud subscriptions and managed-service bundles allow SMEs to tap enterprise-grade protections without capital expenditure. Payment tokenization rules and cyber-insurance prerequisites are additional adoption drivers. Vendors calibrate offerings, pre-configured policies, low-touch deployment, and consumption-based pricing, to match limited internal resources. These dynamics suggest that market expansion over the forecast horizon will rely heavily on volume growth in the under-served mid-market segment.

By Application: DevOps Security Emerges as Fastest-Growing Segment

Database Security formed 44.85% of 2025 spend, verifying its entrenched role in safeguarding structured data. DevOps and Container Security, however, is posting the quickest climb at 18.02% CAGR as microservices and infrastructure-as-code dominate software pipelines. The data security market size for DevOps workflows is set to swell alongside Kubernetes adoption, given container images’ high churn rate and the need for immutable infrastructure controls.

Tools that integrate least-privilege enforcement, secrets rotation, and runtime anomaly blocking directly into CI/CD stages are displacing bolt-on scanners. Endpoint and SaaS-suite protection continue to receive funding, yet growth is flatter compared with the spike in cloud-native development. Vendors that deliver frictionless plug-ins and policy-as-code modules are earning popularity among platform-engineering teams keen to maintain release velocity without sacrificing governance.

By End-User Industry: Healthcare Acceleration Driven by Regulatory Updates

The BFSI segment commanded 22.35% of 2025 revenue owing to high-value data assets and systemic regulatory scrutiny. Healthcare and Life Sciences is accelerating at 17.45% CAGR as ransomware volume targeting hospitals escalates and proposed HIPAA amendments oblige encryption-in-transit, multifactor authentication, and robust risk programs. The data security market share for healthcare workloads is climbing as breach notification penalties grow stricter and AI-diagnostics pipelines create fresh privacy concerns.

Manufacturing and critical-infrastructure operators are modernizing OT-edge security, while telecom carriers pilot quantum-safe cryptography to protect future 5G traffic. Retailers invest in tokenization for real-time payments and loyalty programs, reflecting consumer expectations for frictionless yet private transactions. Together, sectoral demand patterns illustrate that regulatory cadence and threat exposure shape spending intensity across verticals.

Geography Analysis

North America retained 40.74% of 2025 revenue, buoyed by early adoption of advanced analytics, strong venture funding, and a dense regulatory tapestry spanning federal and state mandates. Market depth is reinforced by widespread zero-trust rollouts and aggressive cloud-migration roadmaps across Fortune 500 organizations. Strategic investments by hyperscalers in post-quantum encryption and confidential computing are cementing the region’s technology leadership while catalyzing local ecosystems of niche security vendors.

Asia-Pacific is the fastest-growing geography at 17.88% CAGR through 2031. Digital transformation programs in China, India, and ASEAN stimulate enormous data creation, but strict residency provisions compel localized encryption and key-management solutions. National regulations, including China’s Personal Information Protection Law and Vietnam’s cybersecurity decrees, are spurring demand for on-shore data-protection facilities and sovereign-cloud architectures. Regional banks and e-commerce giants are driving tokenization and DSPM adoption to safeguard cross-border payment flows.

Europe records steady expansion, underpinned by the GDPR and, more recently, the NIS2 Directive, whose broadened scope captures utilities, medical device makers, and medium-sized service providers.Firms are bolstering incident-response playbooks, investing in encryption key escrow, and adopting AI-enabled breach-notification tools to meet the directive’s 24-hour reporting rule. Meanwhile, Middle East and Africa markets gain momentum as Saudi Arabia’s Personal Data Protection Law imposes fines up to SAR 25 million, prompting telcos and energy operators to uplift controls. South America is tightening oversight, with Brazil’s LGPD updates and Argentina’s revised sanction tiers generating incremental budget for discovery engines and privacy dashboards. These regional nuances together accentuate the global breadth of the data security market.

Competitive Landscape

The vendor arena is moderately fragmented, with top suppliers pursuing consolidation to present end-to-end value propositions. Technology giants such as Microsoft and IBM weave security into expansive cloud and data-platform portfolios, leveraging economies of scale and native integrations to lock in customers. Pure-play specialists, including Check Point and Palo Alto Networks, extend reach via targeted acquisitions in zero-trust and Data Security Posture Management, aiming to plug capability gaps and deepen cross-sell opportunities.

Startups remain influential, introducing AI-first analytics, automated policy generation, and quantum-safe algorithms that challenge incumbents’ roadmaps. Investor appetite for platform convergence underpins record-high deal sizes, exemplified by Google’s USD 32 billion purchase of Wiz that underscores hyperscaler ambitions to dominate multi-cloud defense. White-space avenues, notably confidential computing for AI inferencing and adaptive tokenization for instant payments, continue to attract venture funding.

Customers increasingly benchmark suppliers on measurable risk reduction and compliance automation. Offering breadth is no longer sufficient; demonstrable outcomes such as mean-time-to-detect improvement or automated audit evidence drive deal awards. Vendors demonstrating robust partner ecosystems, transparent API strategies, and rigorous secure-development lifecycles stand to differentiate as enterprises rationalize overlapping tools.

Data Security Industry Leaders

IBM Corporation

Microsoft Corporation

Oracle Corporation

Thales Group

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Google completed its USD 32 billion acquisition of Wiz, boosting Google Cloud’s multi-cloud security portfolio.

- April 2025: Kyndryl introduced Data Security Posture Management services built on Microsoft Purview to enhance hybrid protection.

- January 2025: Telefónica Tech and IBM partnered to deliver quantum-safe security solutions from Madrid labs.

- December 2024: Thales embedded data-risk intelligence into Imperva Data Security Fabric to counter rising threat volume.

- June 2024: Tenable entered late-stage talks to buy Eureka Security, targeting the fast-growing DSPM niche.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the data security market as all commercial revenues from software, hardware, and managed services that keep data safe at rest, in motion, and in use. This includes encryption, tokenization, and masking, key-management platforms, data loss prevention, backup and recovery, database activity monitoring, and data-centric access controls deployed on-premise, edge, or cloud environments across every major vertical.

Scope Exclusion: Offerings that secure only networks, endpoints, or facilities without acting directly on the data layer remain outside our scope.

Segmentation Overview

- By Component

- Solutions

- Data Encryption and Tokenisation

- Data Loss Prevention (DLP)

- Data Masking and Obfuscation

- Database Security

- Cloud Data Protection Platforms

- Services

- Professional Services

- Managed Security Services

- Solutions

- By Deployment Mode

- On-premises

- Cloud

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Application

- Database Security

- Endpoint and Removable-media Protection

- Big-Data / Analytics Workloads

- DevOps and Container Security

- SaaS and Collaboration Suites

- By End-user Industry

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- Retail and E-commerce

- Manufacturing and Industrial

- Government and Defense

- IT and Telecommunications

- Energy and Utilities

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed chief information security officers, cloud architects, data protection officers, and regional resellers spanning North America, Europe, and rapidly growing Asian markets. Their insights on price points, contract lengths, and migration hurdles calibrated our assumptions and closed data gaps revealed during the desk phase.

Desk Research

We began with authoritative public sources such as NIST SP-800 guidance, ENISA and US-CERT incident bulletins, GDPR penalty registers, and UN Comtrade shipment data that together outline attack patterns, regulatory thresholds, and hardware flows. Sector-specific associations, such as Cloud Security Alliance, International Association of Privacy Professionals, and FIDO Alliance, supplied adoption ratios, while company 10-Ks, investor decks, and Dow Jones Factiva news helped map vendor earnings. D&B Hoovers and Questel enriched our view of financials and emerging patents. These examples illustrate the breadth; many additional outlets informed data checks and context building.

Market-Sizing & Forecasting

We anchor totals with a top-down model that links global enterprise IT spend, breach cost per record, and the share of regulated workloads, then corroborate them through selective bottom-up roll-ups of encrypted database counts, average selling prices, and tender trackers. Inputs such as reported breach volumes, average data stored per employee, cloud storage expenditure, zero-trust rollout rates, and quantum-safe pilot activity feed a multivariate regression; scenario analysis frames uncertainty bands. Gap-filling draws on channel checks where disclosures are scant.

Data Validation & Update Cycle

Outputs pass three analyst reviews, followed by anomaly scans against Factiva news flow and independent KPIs. We refresh every twelve months, with interim updates triggered by major vendor restatements or landmark regulations so clients always receive the latest view.

Why Mordor's Database Security Baseline Commands Confidence

Estimates from different publishers often vary because each chooses distinct product mixes, price assumptions, refresh cadences, and currency treatments.

Key Gap Drivers include the tendency of some firms to fold log analytics suites or broad disaster recovery services into 'data security,' apply aggressive cloud mark-ups, or extend forecasts without re-checking breach statistics, whereas Mordor Intelligence limits coverage to true data layer controls and revisits variables annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.70 B (2025) | Mordor Intelligence | - |

| USD 27.40 B (2025) | Global Consultancy A | Blends big data analytics and DRaaS; limited primary validation |

| USD 24.13 B (2024) | Industry Journal B | Tracks only software; omits managed services and hardware HSMs |

The comparison shows that our disciplined scope selection, live primary feedback, and dual track modeling deliver a transparent, balanced baseline that decision makers can replicate with confidence.

Key Questions Answered in the Report

What is the current size of the data security market?

The market is valued at USD 17.21 billion in 2026 and is projected to reach USD 37.93 billion by 2031 at a 17.12% CAGR.

Which component segment is growing the fastest?

Services, encompassing managed and professional offerings, are expanding at an 18.23% CAGR as firms outsource expertise amid skills shortages.

Why is Asia-Pacific the fastest-growing region?

Rapid digital transformation, stringent data-residency rules, and evolving national privacy laws are driving an 17.88% CAGR in Asia-Pacific spending.

How are SMEs influencing market dynamics?

SMEs are adopting SaaS security tools and managed services, delivering a 18.74% CAGR for the segment despite limited internal resources.

What technologies are reshaping data protection strategies?

Confidential computing, quantum-safe cryptography, and AI-driven data lineage are emerging as key enablers of next-generation security posture.

Which industry is accelerating fastest after BFSI?

Healthcare and Life Sciences is growing at 17.45% CAGR, propelled by HIPAA modernization and a surge in ransomware targeting medical institutions.

Page last updated on: