Security Information And Event Management (SIEM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

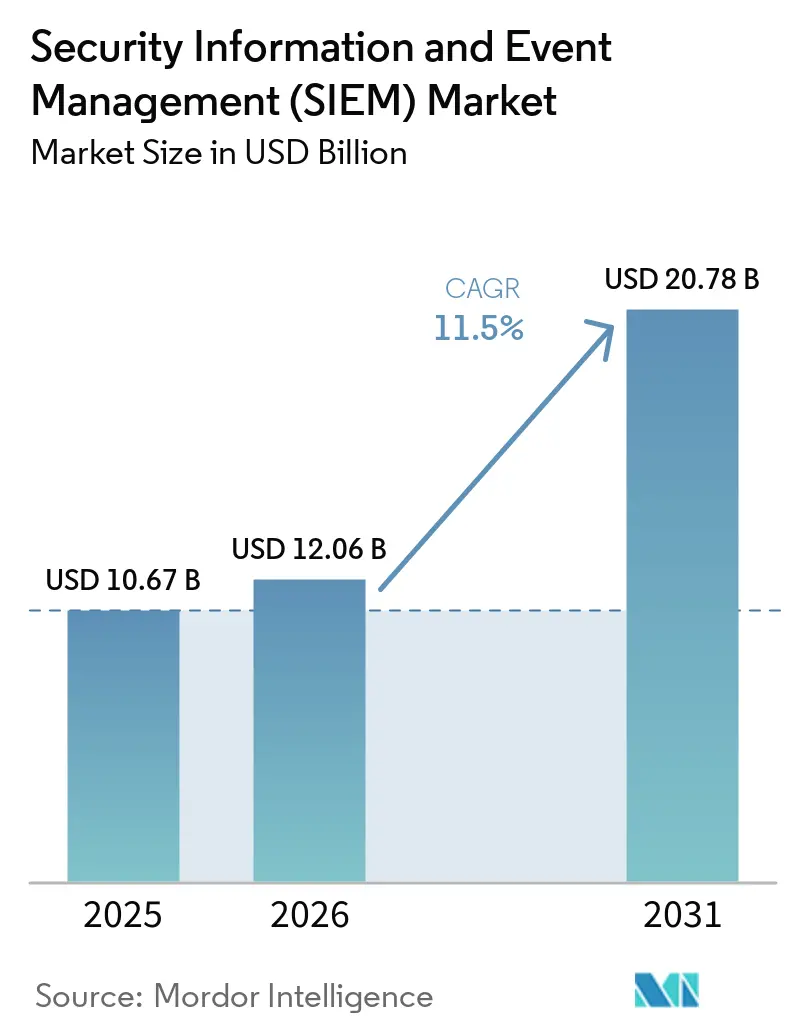

| Market Size (2026) | USD 12.06 Billion |

| Market Size (2031) | USD 20.78 Billion |

| Growth Rate (2026 - 2031) | 11.50% CAGR |

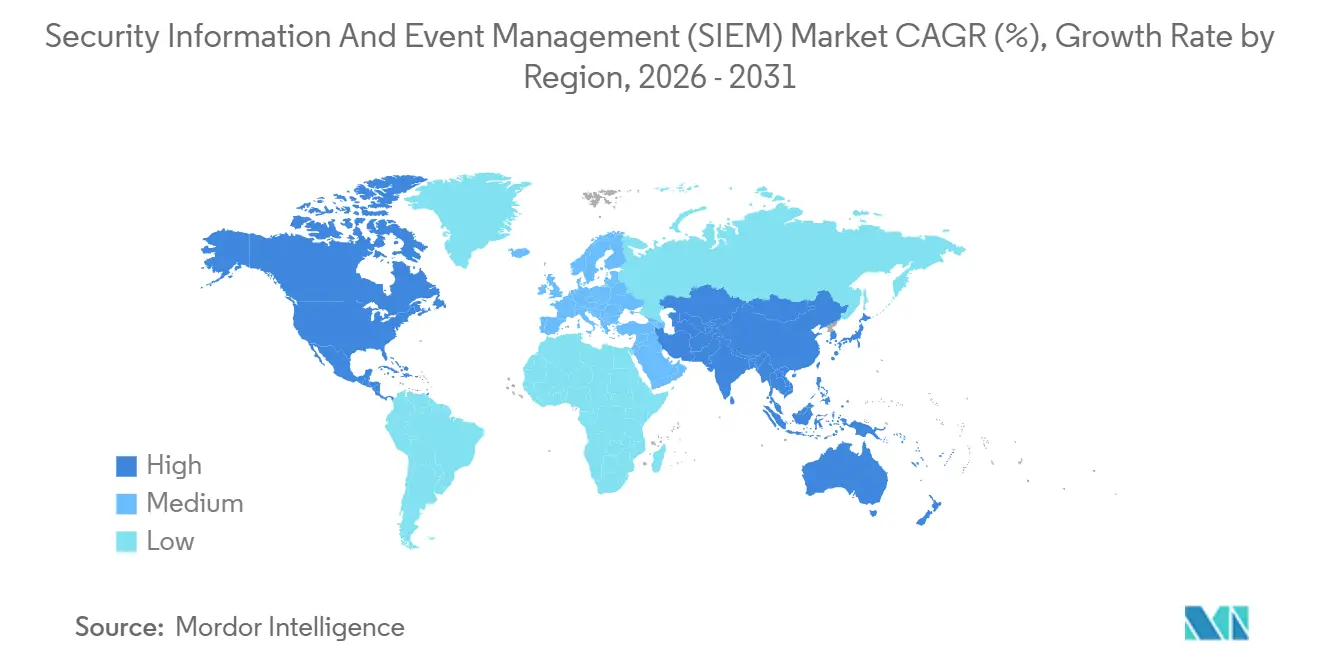

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

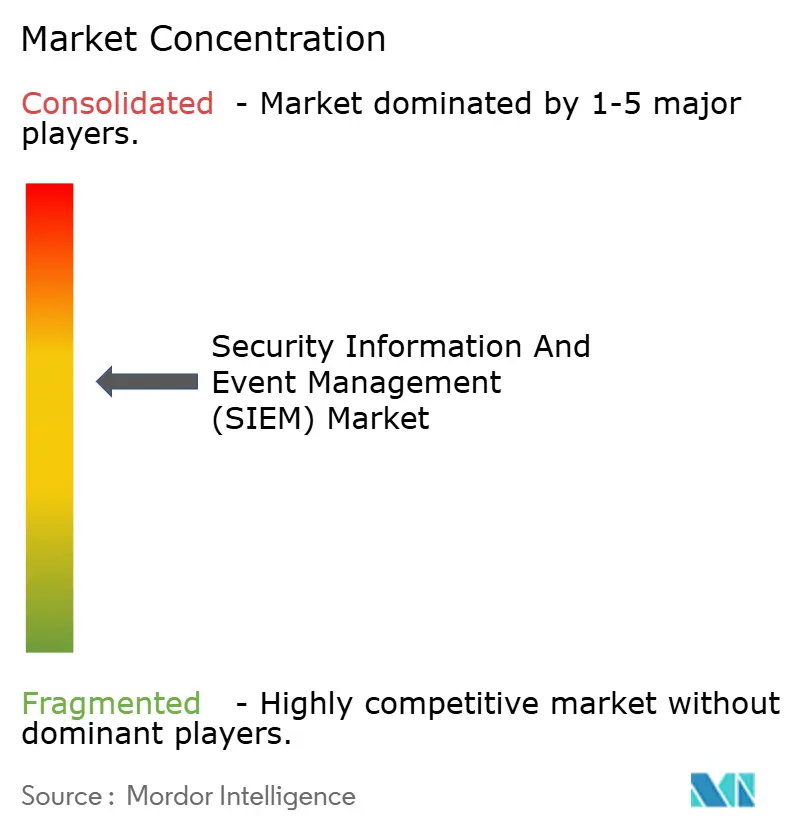

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Security Information And Event Management (SIEM) Market Analysis by Mordor Intelligence

The Security Information And Event Management Market size was valued at USD 10.67 billion in 2025 and is estimated to grow from USD 12.06 billion in 2026 to reach USD 20.78 billion by 2031, at a CAGR of 11.5% during the forecast period (2026-2031).

Mandatory log-retention rules, accelerated cloud migration, and increasingly sophisticated adversaries are converging, forcing organizations to modernize correlation engines and adopt analytics that can scale with exploding telemetry. On-premises platforms still dominate but cost pressure and elastic pricing are pushing enterprises toward cloud-native options, while mid-tier operators race to comply with European, North American, and Asia-Pacific disclosure laws that penalize delayed breach reporting. A parallel skills shortage is stoking demand for managed services, and AI-infused triage tools are improving analyst productivity by filtering low-value alerts. Together these forces support a robust outlook for the security information and event management (SIEM) market through the medium term.

Key Report Takeaways

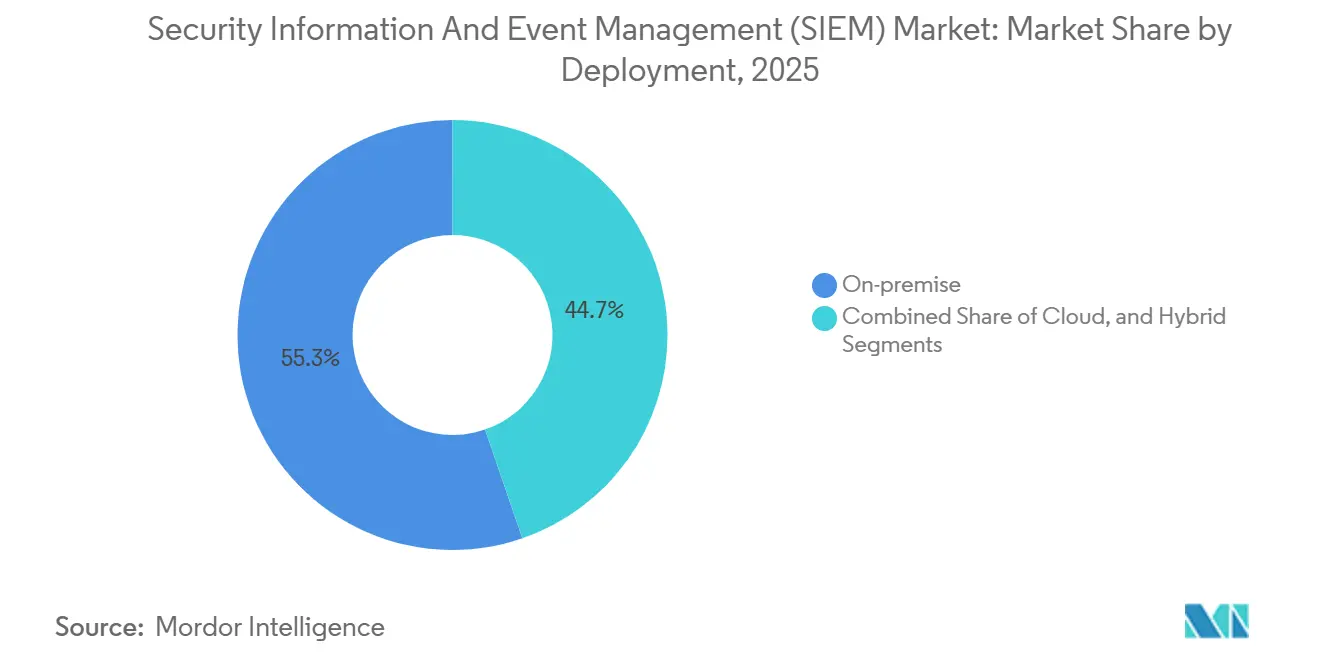

- By deployment, on-premises systems held 55.27% of the SIEM market share in 2025, while cloud implementations are advancing at a 12.84% CAGR through 2031.

- By architecture, legacy platforms retained 48.12% revenue share in 2025, yet cloud-native stacks are on track for 11.95% CAGR to 2031.

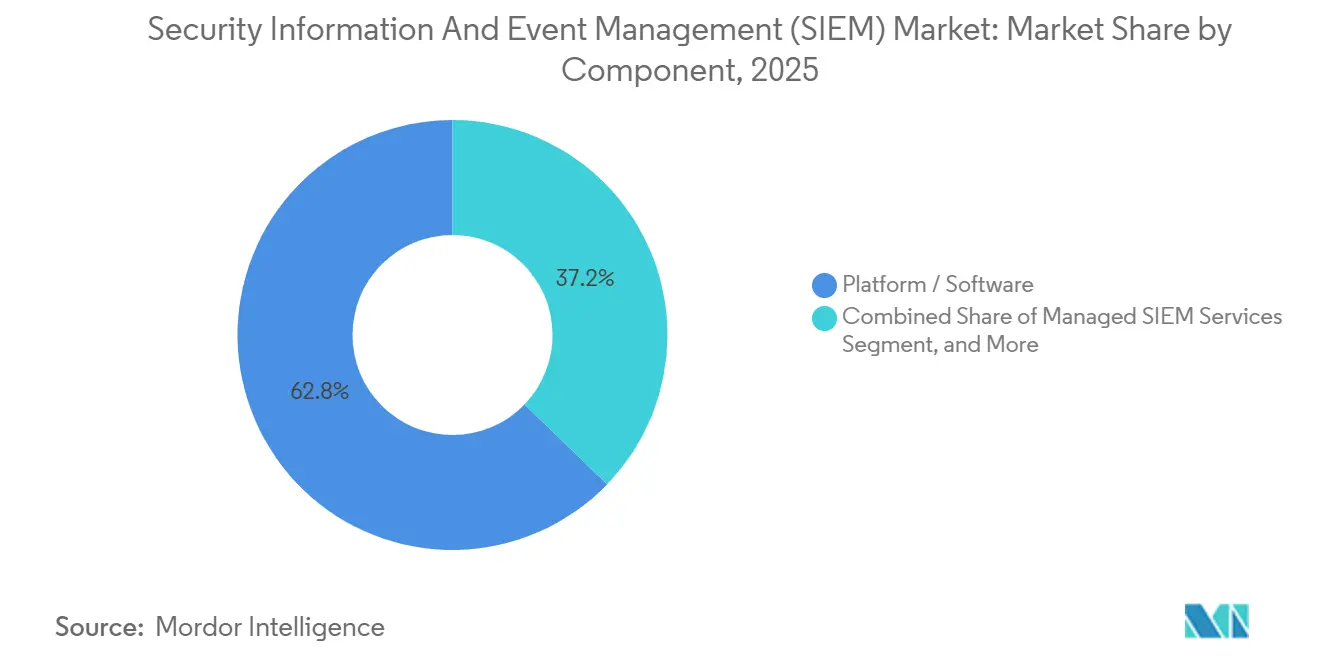

- By component, platform and software licenses captured 62.79% of 2025 value; managed services are growing at 12.03% through 2031.

- By organization size, large enterprises accounted for 65.39% of 2025 deployments, whereas SME adoption is projected to rise at 12.28% CAGR to 2031.

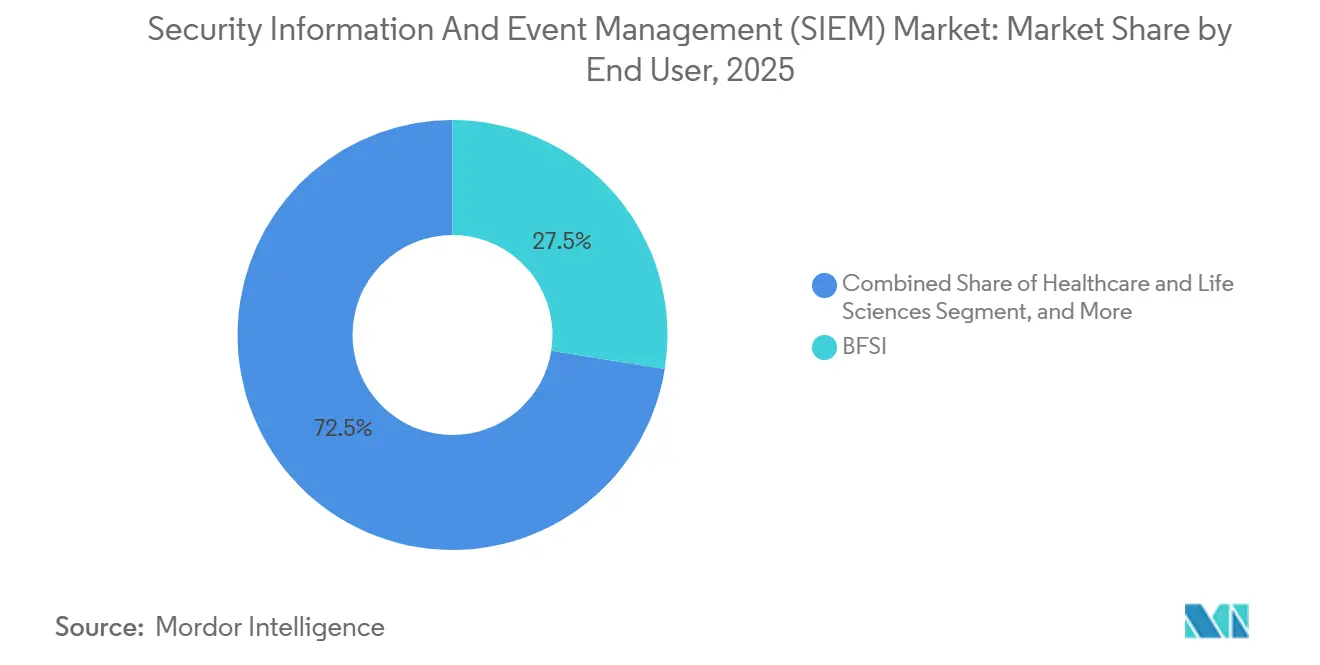

- By end-user vertical, BFSI led with 27.52% revenue in 2025, while healthcare is poised for the fastest 12.15% CAGR to 2031.

- By application, threat detection commanded 43.77% of the Security Information and Event Management market size in 2025 and cloud-workload monitoring is accelerating at a 12.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Security Information And Event Management (SIEM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exponential Growth of Security Telemetry Volumes | +2.30% | Global, highest in North America and Asia Pacific | Medium term (2-4 years) |

| Escalating Regulatory Penalties and Audit Frequency | +2.10% | Europe and North America, spreading to Asia Pacific hubs | Short term (≤ 2 years) |

| Accelerated Cloud and Hybrid Adoption of Enterprise Workloads | +1.90% | Global, led by North America and Europe | Medium term (2-4 years) |

| AI/ML-Infused Analytics Improve Signal-to-Noise Ratios | +1.70% | North America and Europe, early take-up in Asia Pacific | Long term (≥ 4 years) |

| Emergence of Security-Data-Pipeline Layer Reduces SIEM TCO | +1.40% | North America and Europe | Medium term (2-4 years) |

| Vendor Mega-Deals Trigger Refresh Cycles | +1.20% | Global, concentrated in large enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Exponential Growth of Security Telemetry Volumes

Organizations with more than 10,000 employees now ingest over 10 terabytes of log data each day, spanning endpoints, multi-cloud services, SaaS tools, and operational-technology networks. Microsoft reported that events processed by Sentinel surged 150% year-over-year during 2025, underscoring the strain on storage budgets when every log line is indexed.[1]Microsoft, “Microsoft Digital Defense Report 2024,” microsoft.com Tiered retention, hot-warm-cold storage, and streaming analytics pipelines are emerging as default design choices to keep costs in check. Remote work further amplifies the data flood, VPN authentications quintupled between 2024 and 2025, reshaping detection logic calibrated for fixed perimeters. Vendors that efficiently compress, normalize, and triage this torrent gain an edge, accelerating the security information and event management (SIEM) market.

Escalating Regulatory Penalties and Audit Frequency

Europe’s NIS2 directive became enforceable in October 2024 and allows fines of up to 2% of global revenue for inadequate incident logging. The Digital Operational Resilience Act obliges European financial entities to test SIEM-driven playbooks every quarter starting January 2025.[2]European Commission, “The NIS2 Directive,” Digital-strategy, europa.eu In the United States, SEC rules that took effect in late 2023 require public companies to disclose material cybersecurity incidents within four business days.[3]U.S. Securities and Exchange Commission, “Cybersecurity Disclosure Rules,” sec.gov These converging frameworks demand immutable, searchable event stores and real-time correlation, propelling procurement among both heavily regulated and adjacent sectors.

Accelerated Cloud and Hybrid Adoption of Enterprise Workloads

By 2025, 60% of enterprise compute had shifted to public cloud, scattering telemetry across AWS, Azure, and Google Cloud APIs. Cloud-native SIEMs eliminate agents and wire-up directly to provider event streams, cutting deployment from months to days. Hybrid models mix on-premises retention often required by data-sovereignty rules in China, India, and Russia with cloud compute to run analytics on demand. Normalizing heterogeneous schemas, correlating across diverse identities, and limiting latency when logs traverse regions are now core feature requirements that shape purchasing decisions in the security information and event management (SIEM) market.

AI/ML-Infused Analytics Improve Signal-to-Noise Ratios

Security teams still investigate thousands of alerts each day, yet only a sliver represents true threats. Google Chronicle infused Gemini large language models into threat-intelligence workflows in 2025, letting analysts ask plain-language questions about anomalies. Microsoft folded its Copilot assistant into Sentinel the same year, generating auto-summaries and guided response steps. These tools shorten mean-time-to-respond, mitigate analyst fatigue, and expand coverage despite workforce gaps, reinforcing demand for modern platforms in the SIEM market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership and Licensing Complexity | -1.80% | Global, acute for cost-sensitive SMEs | Short term (≤ 2 years) |

| Shortage of Skilled SOC Analysts | -1.50% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Data-Sovereignty Barriers to Central Log Aggregation | -0.90% | Asia Pacific, Middle East and Africa | Medium term (2-4 years) |

| Overlap with XDR/SOAR Platforms Delays Budget Approval | -0.70% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership and Licensing Complexity

Pay-by-ingest licensing means costs spike when cloud, IoT, or SaaS sources are activated, blindsiding finance teams. Enterprises that budgeted for 500 GB per day in 2024 saw usage balloon past 2 TB by 2025, quadrupling annual spend. Multi-year retention adds petabyte storage bills, and professional services for rule-tuning consume another quarter of total outlay. Vendors are countering with decoupled storage and compute, letting customers push raw data into cheap object repositories and pay only when queries or detections run, but that shift demands new skills in schema design and ad-hoc querying.

Shortage of Skilled SOC Analysts

ISC2 estimates a global shortfall of 4.8 million cybersecurity professionals as of 2024, creating a perpetual talent squeeze. Tier-1 analysts drown in alert queues, while tier-3 experts command premium salaries beyond SME budgets. Managed security service providers offer relief, yet shared-service models can delay investigation because external analysts lack institutional context. Automation, generative AI summaries, and pre-programmed playbooks ease the burden but still require seasoned oversight, limiting near-term gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Models Reshape TCO Calculations

Cloud deployments are expanding at a 12.84% CAGR through 2031, eclipsing the 11.50% trajectory of the overall Security Information and Event Management market. The elasticity of pay-per-use pricing and the elimination of hardware refresh cycles appeal to finance teams, while direct API integrations pull telemetry from serverless functions, container orchestrators, and SaaS tenants that legacy agents cannot instrument. On-premises systems still held 55.27% share in 2025, anchored by sunk investments and air-gapped defense networks. Hybrid models let regulated banks and healthcare providers keep sensitive logs in-country yet harness cloud compute bursts for advanced analytics.

The operating-expense advantage of cloud grows when enterprises recognize the staff hours required to patch, scale, and tune on-premises clusters. Public-cloud providers absorb infrastructure chores, letting internal teams focus on threat-hunting rather than disk provisioning. Data-localization laws complicate one-size-fits-all strategies, prompting federated designs where regional instances forward correlated alerts to a global view. This architectural flexibility is widening adoption among mid-size organizations, reinforcing the security information and event management (SIEM) market.

By SIEM Architecture: Next-Gen Platforms Disrupt Incumbents

Cloud-native and next-generation stacks are projected to grow at 11.95% through 2031, challenging the 48.12% foothold that legacy relational-database platforms enjoyed in 2025. Decoupled storage-compute designs let teams park raw logs in cheap object stores and spin up queries only during investigations, slicing infrastructure spend by as much as 60% according to 2025 vendor benchmarks. Open-source alternatives like Wazuh and Graylog appeal to budget-constrained agencies that need code transparency, but they require DIY connectors and round-the-clock maintenance.

Switching costs slow migration because enterprises have millions invested in custom correlation rules and analyst training. Nonetheless, Cisco’s USD 28 billion purchase of Splunk in March 2024 rattled installed-base confidence and triggered pilot programs with newer vendors. Cloud-native providers differentiate on rapid onboarding, AI-assisted triage, and consumption pricing. Legacy vendors are countering through managed deployment offerings and database re-platforming, but the momentum favours architectures built for elastic scale, lifting the security information and event management (SIEM) market size for modern solutions.

By Component: Managed Services Absorb Operational Burden

Managed SIEM offerings are advancing at 12.03% CAGR, outpacing the broader security information and event management (SIEM) market as companies grapple with staffing gaps. Platform and software still commanded 62.79% of 2025 revenue, but subscription models are replacing perpetual licenses, aligning cash outflows with ingested volume. MSSPs operate 24/7 centers, pooling analysts, threat-intel feeds, and orchestrated playbooks across dozens of clients to deliver economies of scale.

Professional services remain vital during the first year of deployment, covering integration with identity providers, EDR agents, and cloud-security posture tools. Once stabilized, many customers shift day-to-day monitoring to MSSPs to conserve scarce headcount. This blended model of internal ownership of tuning and external ownership of alert triage has become standard among Fortune 1000 organizations and is filtering down to mid-market firms, sustaining demand across all service tiers.

By Organization Size: SaaS Models Lower SME Entry Barriers

Large enterprises captured 65.39% of deployments in 2025, a reflection of regulatory exposure and sprawling attack surfaces. However, SMEs are forecast to grow at 12.28% CAGR through 2031 as cloud-native vendors offer starter tiers priced near USD 10,000 annually for modest data volumes. Consumption pricing lets smaller firms experiment without six-figure commitments, and turnkey connectors autoconfigure log sources for M365, Google Workspace, and popular CRM systems, compressing setup timelines.

Larger organizations wrestle with complex hybrid estates and multi-framework audit mandates, pushing them toward consolidated platforms that merge SIEM with extended detection and response. SMEs, in contrast, value simplicity and automated triage because they cannot lure experienced SOC analysts. As a result, the SIEM market now serves two distinct buyer personas, each driving innovation in usability and scale.

By End-User Industry: Healthcare Surges Amid Ransomware Wave

BFSI claimed 27.52% of 2025 spending, but healthcare is tipped for a market-leading 12.15% CAGR through 2031. Hospitals face a 128% year-over-year rise in ransomware aimed at electronic health record systems, motivating boards to invest in real-time correlation that spans IT and clinical devices. Financial institutions confront DDoS and synthetic-identity fraud that require cross-channel telemetry, while regulators mandate sub-daily incident reporting.

Industry-specific nuances shape platform selection: healthcare networks include legacy imaging devices that cannot host agents, manufacturing plants need support for industrial protocols, and telecom operators leverage SIEM both for their own estates and as a managed service revenue line. This diversity drives vendors to expand parser libraries and pre-built detection packs, broadening the Security Information and Event Management industry portfolio.

By Application: Cloud-Workload Monitoring Gains Urgency

Threat detection and analytics accounted for 43.77% of the Security Information and Event Management market size in 2025, yet cloud-workload monitoring will post the fastest 12.63% CAGR through 2031. Container orchestration, serverless functions, and infrastructure-as-code pipelines emit unique telemetry streams that traditional agents miss, pushing buyers toward platforms with direct hooks into AWS CloudTrail, Azure Monitor, and Google Cloud Logging.

Compliance management remains a steady driver as frameworks such as NIS2 and DORA introduce audit-trail mandates, but incident-response workflows are evolving fastest. Seamless hand-offs between SIEM alerts and security-orchestration playbooks now isolate compromised endpoints, revoke credentials, and notify regulators in minutes. IoT and OT monitoring rounds out growth, particularly in energy and utilities where industrial-control systems present high-impact targets.

Geography Analysis

North America generated 41.39% of 2025 revenue, propelled by SEC disclosure mandates that force near-real-time detection and four-day breach reporting. Public corporations accelerated decommissioning of on-premises stacks in favour of cloud-native services that integrate with SaaS and infrastructure logs at massive scale. Venture investment in cybersecurity startups and government spending on critical-infrastructure protection also reinforce the region’s primacy.

Europe commands sizable demand thanks to the overlapping weight of GDPR, NIS2, and DORA. More than 160,000 additional entities fell under NIS2 by late 2024, compelling mid-tier operators to adopt centralized log management despite budget constraints. Financial houses are automating quarterly resilience tests, and manufacturing exporters rely on SIEM analytics to certify supply-chain security for customers in strict security information and event management (SIEM) markets.

Asia Pacific leads growth at 12.72% CAGR as India, Indonesia, and Vietnam digitize payments and enforce data-localization. Chinese mandates keep logs onshore, prompting regional SIEM nodes that federate to a supervisory dashboard. Singapore is positioning as a cybersecurity hub, while Australia tightens critical-infrastructure laws after high-profile breaches. South America and the Middle East invest steadily in smart-city and e-government programs that expand telemetry but face currency volatility and skills gaps. Africa remains an emerging opportunity centered on South Africa, Nigeria, and Egypt, where telecom and banking sectors shoulder early adoption.

Competitive Landscape

In 2025 the top five vendors controlled roughly 55% of revenue, indicating moderate concentration in the security information and event management (SIEM) market. Cisco closed a USD 28 billion deal for Splunk in March 2024, integrating log analytics with network controls and igniting a wave of platform consolidation. Microsoft leveraged its Azure base to expand Sentinel workloads 150% year-over-year in 2025, bundling SIEM, XDR, and generative AI triage into a single license. Palo Alto Networks purchased IBM’s QRadar SaaS assets in November 2024, aiming to fold them into Cortex and simplify incident response across cloud and on-premises estates.

Mid-market challengers such as Securonix, Exabeam, and Devo differentiate on data-pipeline efficiency and consumption pricing attractive to organizations ingesting tens rather than hundreds of terabytes each day. Open-source options continue to gain footholds in government and cost-sensitive verticals, though the lack of managed support limits penetration in complex global environments. Vendors are racing to patent AI-based anomaly detection, natural-language search, and storage compression, signalling that differentiation will hinge on automation and total cost of ownership.

Operational-technology coverage remains a white-space where specialists can grow. Manufacturers and utilities need parsers for Modbus, DNP3, and OPC-UA and playbooks that align with NIST SP 800-82 guidance. Providers that build or acquire such capabilities stand to win share as critical-infrastructure regulations tighten. Overall, innovation pace and vendor consolidation will continue to shape the Security Information and Event Management market over the forecast horizon.

Security Information And Event Management (SIEM) Industry Leaders

Cisco Systems, Inc.

Microsoft Corporation

International Business Machines Corporation

Rapid7, Inc.

Fortinet, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Fortinet Q1 2025 revenue reached USD 1.54 billion with continued platform convergence momentum.

- May 2025: CrowdStrike LogScale crossed USD 220 million ARR driven by AI analytics.

- March 2025: SentinelOne enhanced AI-powered SIEM integrations for multicloud.

- March 2025: Elastic refined cloud SIEM pricing to ease ingestion cost concerns.

Global Security Information And Event Management (SIEM) Market Report Scope

Security information and event management is a sophisticated technology that includes mobile devices, cloud, third-party threat intelligence, and traditional sources, such as endpoints, firewalls, system logs, and directory services. SIEM is a tool for gathering data for threat analysis and detecting threats. It is based on real-time analysis of security alerts generated in an organization's IT network applications and infrastructure.

The Security Information and Event Management (SIEM) Market Report is Segmented by Deployment (On-Premise, Cloud, Hybrid), Architecture (Legacy, Cloud-Native, Open-Source), Component (Platform, Services, Managed Services), Organization Size (SME, Large Enterprises), End-User (BFSI, Retail, Government, Healthcare, Manufacturing, Energy, Telecom, Others), Application (Threat Detection, Compliance, Incident Response, Log Management, Cloud Security, IoT/OT Monitoring), and Geography (North America, South America, Europe, Middle East, Africa, Asia Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premise |

| Cloud |

| Hybrid |

| Legacy / Traditional SIEM |

| Cloud-Native / Next-Gen SIEM |

| Open-Source SIEM |

| Platform / Software |

| Professional Services |

| Managed SIEM Services (MSSP) |

| Small and Medium Enterprises |

| Large Enterprises |

| Banking, Financial Services and Insurance |

| Retail and E-Commerce |

| Government and Defense |

| Healthcare and Life Sciences |

| Manufacturing |

| Energy and Utilities |

| Telecom and IT |

| Other End-User Industries |

| Threat Detection and Analytics |

| Compliance and Audit Management |

| Incident Response and Forensics |

| Log Management and Reporting |

| Cloud-Workload Security Monitoring |

| IoT / OT Security Monitoring |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment | On-Premise | |

| Cloud | ||

| Hybrid | ||

| By SIEM Architecture | Legacy / Traditional SIEM | |

| Cloud-Native / Next-Gen SIEM | ||

| Open-Source SIEM | ||

| By Component | Platform / Software | |

| Professional Services | ||

| Managed SIEM Services (MSSP) | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-User Industry | Banking, Financial Services and Insurance | |

| Retail and E-Commerce | ||

| Government and Defense | ||

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Energy and Utilities | ||

| Telecom and IT | ||

| Other End-User Industries | ||

| By Application | Threat Detection and Analytics | |

| Compliance and Audit Management | ||

| Incident Response and Forensics | ||

| Log Management and Reporting | ||

| Cloud-Workload Security Monitoring | ||

| IoT / OT Security Monitoring | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the Security Information and Event Management market expected to grow to 2031?

The market is forecast to expand from USD 12.06 billion in 2026 to USD 20.78 billion by 2031, reflecting an 11.50% CAGR.

Which deployment model is expanding the quickest?

Cloud-based SIEM is the fastest, advancing at a 12.84% CAGR as buyers shift away from capital-intensive hardware.

Why are healthcare organizations increasing SIEM spending?

A 128% jump in ransomware incidents against electronic health record systems is driving hospitals to adopt real-time correlation and automated response.

What is the chief cost challenge for SIEM buyers?

Pay-by-ingest licensing combined with multi-year log-retention requirements can quadruple budgets when telemetry volumes surge.

How are regulations influencing SIEM adoption in Europe?

NIS2, DORA, and GDPR impose strict log-retention and rapid incident-reporting mandates, compelling thousands of additional entities to deploy modern SIEM tools.

What role does AI play in modern SIEM platforms?

Generative AI assistants summarize alerts, answer natural-language queries, and recommend remediation actions, reducing analyst workload and speeding response times.

Page last updated on: