Data Loss Prevention (DLP) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 35.38 Billion |

| Market Size (2030) | USD 94.09 Billion |

| Growth Rate (2025 - 2030) | 21.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Data Loss Prevention (DLP) Market Analysis by Mordor Intelligence

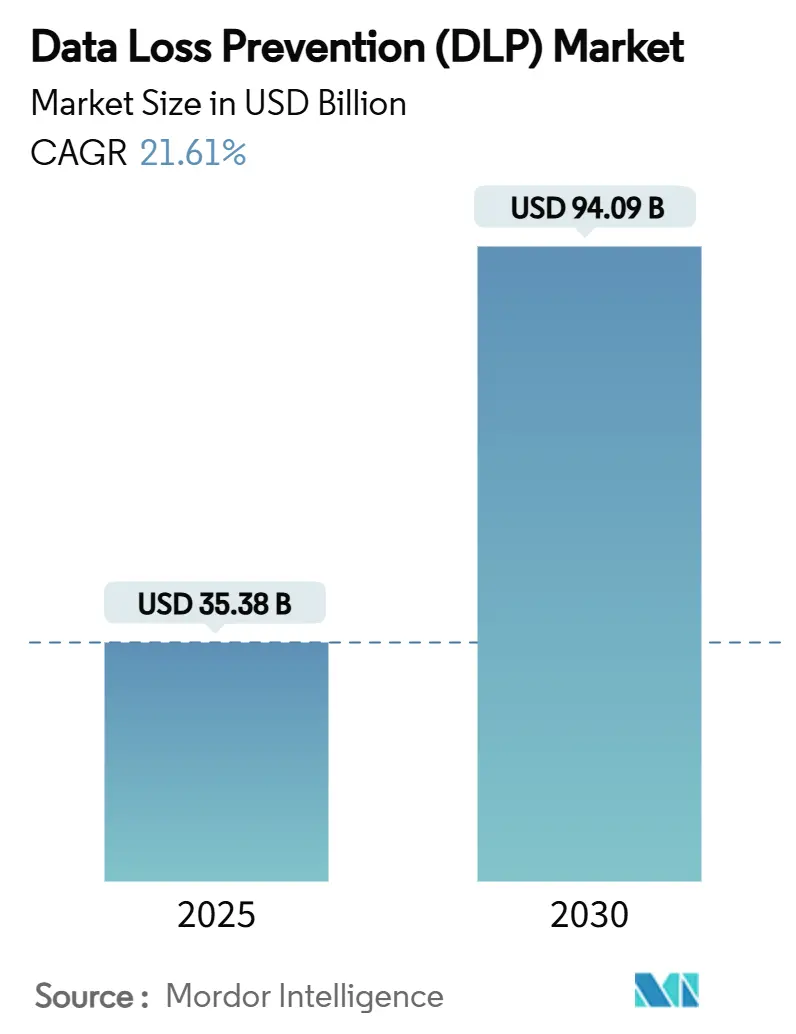

The data loss prevention market is valued at USD 35.38 billion in 2025 and is forecast to reach USD 94.09 billion by 2030, translating into a vigorous 21.61% CAGR over the period. Rapid expansion is rooted in mounting regulatory penalties, the dispersal of sensitive data across hybrid workplaces, and the embedding of DLP controls inside zero-trust and Secure Access Service Edge platforms. Artificial-intelligence policy tuning is further accelerating adoption by trimming false-positive rates and reducing analyst fatigue, while cloud-delivered deployment models deliver the elasticity enterprises need to secure distributed users. Vendor consolidation driven by acquisitions that fold DLP into broader data-security posture offerings underscores a strategic pivot toward unified platforms capable of discovery, classification, and protection across endpoints, networks, and multicloud estates.

Key Report Takeaways

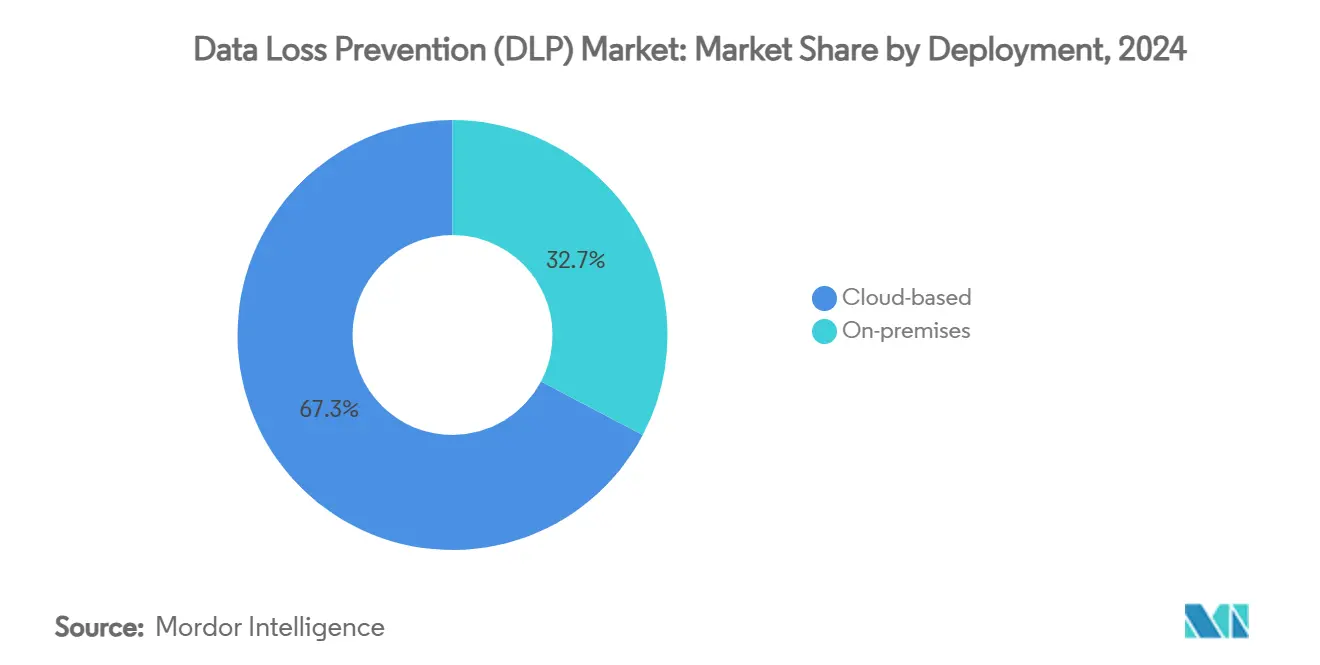

- By deployment, cloud-based models captured 67.3% of data loss prevention market share in 2024; on-premises lagged, yet cloud is projected to expand at 22.1% CAGR through 2030.

- By solution, endpoint DLP led with 46.7% share of the data loss prevention market size in 2024 and is advancing at a 22.4% CAGR to 2030.

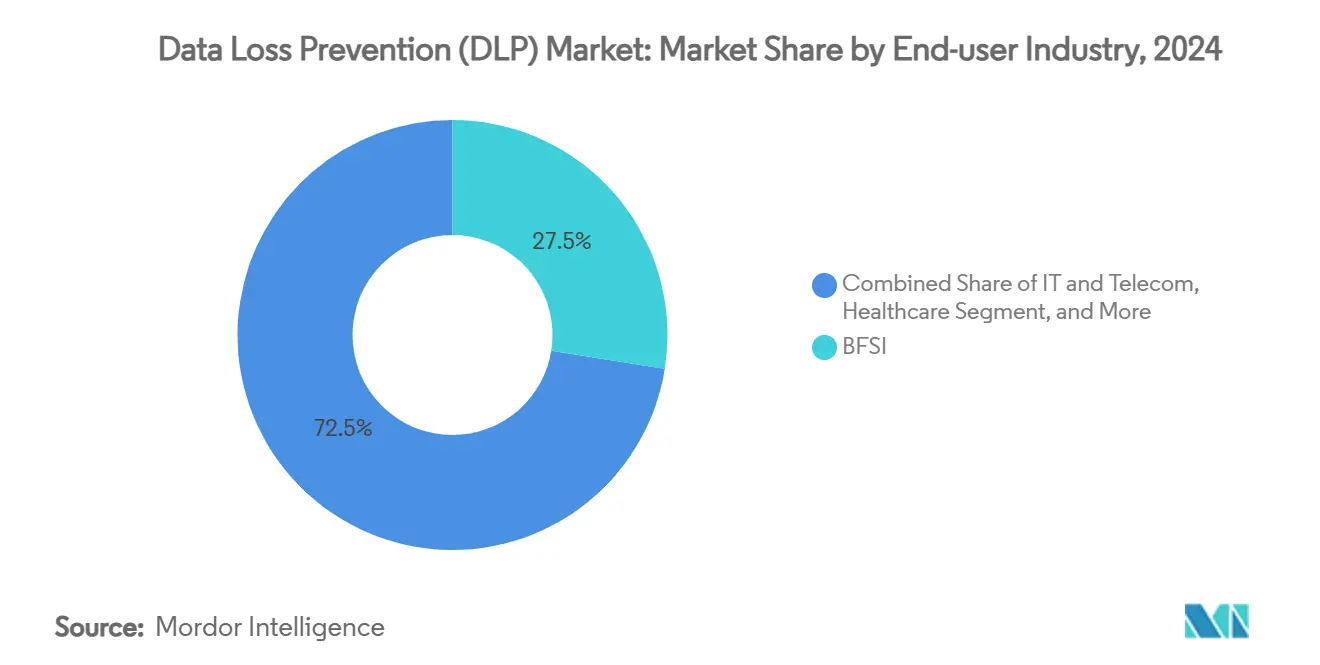

- By end-user industry, BFSI contributed 27.5% revenue in 2024, whereas manufacturing is projected to grow the fastest at 21.7% CAGR through 2030.

- By application, encryption commanded 23.5% share of the data loss prevention market size in 2024 while insider-risk analytics is forecast to grow at 23.2% CAGR to 2030.

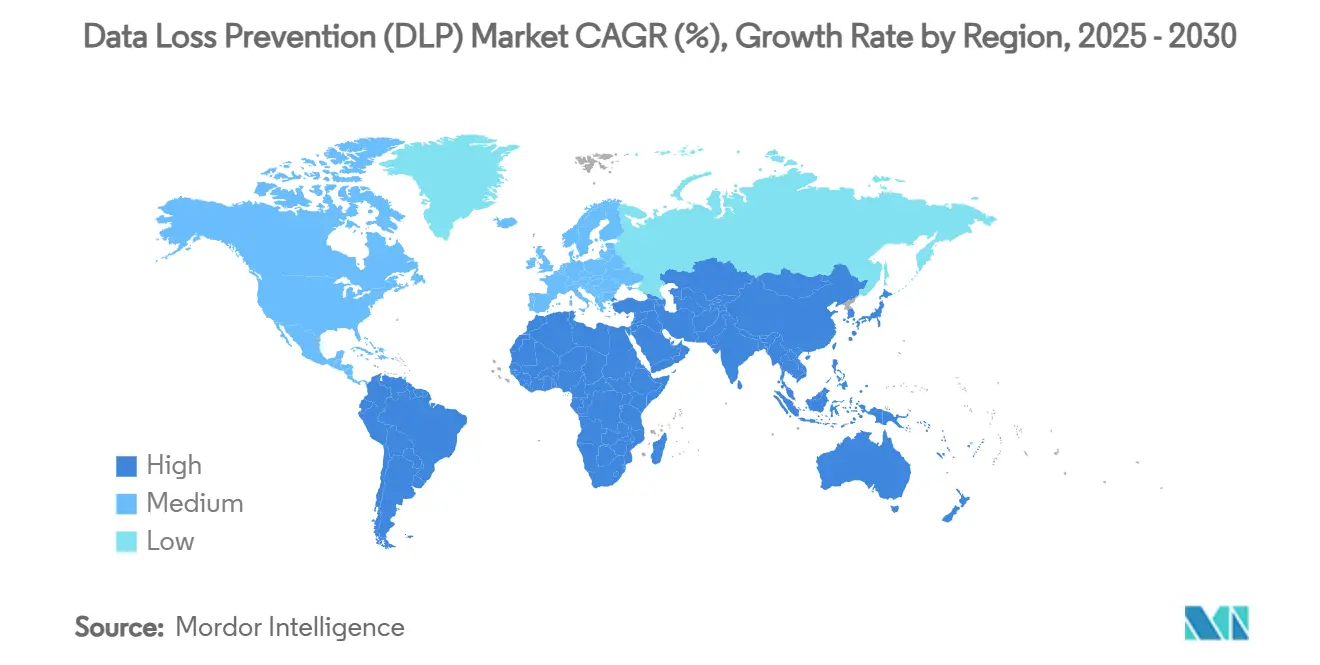

- By geography, North America held 24.2% share in 2024, whereas Asia-Pacific is set to register the highest 21.1% CAGR through 2030.

Global Data Loss Prevention (DLP) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cyber-breach fines under GDPR 2.0 and CCPA amendments | +4.2% | Global, with EU and California leading enforcement | Short term (≤ 2 years) |

| Hybrid-work data sprawl raising endpoint and cloud risk | +3.8% | Global, with North America and Europe most affected | Medium term (2-4 years) |

| Convergence of DLP with CASB and DSPM platforms | +3.1% | Global, with enterprise adoption concentrated in developed markets | Medium term (2-4 years) |

| AI-assisted policy tuning slashing false-positive rates | +2.9% | Global, with early adoption in tech-forward organizations | Long term (≥ 4 years) |

| Zero-trust and SASE road-maps mandating integrated DLP | +3.4% | Global, with government and financial sectors leading | Medium term (2-4 years) |

| Gen-AI code copilots creating new exfiltration vectors | +2.1% | Global, with software development organizations most impacted | Short term (≤ 2 years) |

Source: Mordor Intelligence

Escalating Cyber-Breach Fines Under GDPR 2.0 and CCPA Amendments

Maximum penalties are reshaping spending priorities: TikTok’s EUR 530 million (USD 624.18 million) fine in 2025 spotlighted regulators’ readiness to levy record sanctions for lax data-transfer controls.[1]Stephenson Harwood, “EU Regulators Impose Record TikTok Fine,” stephensonharwood.com In parallel, the UK Data (Use and Access) Bill tightens data-handling rules, and the EU AI Act introduces mandatory transparency audits, both driving proactive DLP investment. California’s latest CCPA amendments widen the definition of sensitive personal information and strengthen consumer rights, expanding compliance exposure for enterprises operating nationwide. Across jurisdictions, executives now view robust DLP capability as a demonstrable risk-mitigation measure rather than a discretionary cybersecurity layer, propelling the data loss prevention market toward accelerated growth.

Hybrid-Work Data Sprawl Raising Endpoint and Cloud Risk

IBM’s 2023 breach report revealed that 82% of incidents involved cloud-resident data, underscoring the erosion of perimeter defenses IBM. Employees increasingly use personal devices and unsanctioned SaaS tools, creating blind spots that traditional controls cannot monitor. In sectors such as manufacturing where operational technology merges with IT systems the attack surface widens as production gear becomes network-connected. Organizations therefore adopt endpoint DLP for device-level controls while extending cloud DLP rules across multiple providers, fuelling demand in the data loss prevention market.

Convergence of DLP with CASB and DSPM Platforms

Unified data-security clouds now merge discovery, classification, and real-time policy enforcement. Forcepoint’s Data Security Cloud integrates enterprise DLP with DSPM and data-detection-and-response analytics, replacing siloed tools.[2]Forcepoint, “Introducing Data Security Cloud,” forcepoint.comCisco layers DLP into its SASE stack, enabling single-policy administration across web, SaaS, and private applications Cisco. These architectures reduce operational friction and enable context-aware protection, spurring platform-based buying patterns that are redefining competitive dynamics in the data loss prevention market.

AI-Assisted Policy Tuning Slashing False-Positive Rates

Versa Networks applies cloud-scale machine learning pipelines to classify data and detect anomalies, lowering false alarms and freeing analyst bandwidth.[3]Versa Networks, “AI/ML-Powered DLP Pipeline,” versa-networks.com AI models refine policies continuously by learning from user behavior, thereby replacing static rule sets that often over-block legitimate traffic. The operational efficiency gains address a long-standing objection to DLP adoption and are elevating AI-native offerings in the data loss prevention industry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complexity and skills gap in multi-cloud roll-outs | -2.8% | Global, with smaller organizations most affected | Medium term (2-4 years) |

| High TCO for legacy on-prem policies | -2.1% | Developed markets with established IT infrastructure | Long term (≥ 4 years) |

| Privacy-by-design push limiting deep content inspection | -1.9% | EU and privacy-conscious jurisdictions | Medium term (2-4 years) |

| Sovereign-cloud mandates fragmenting global policy sets | -1.6% | Asia-Pacific and emerging markets with data localization laws | Long term (≥ 4 years) |

Source: Mordor Intelligence

Complexity and Skills Gap in Multi-Cloud Roll-Outs

Firms commonly operate three to five cloud platforms, each with unique access controls and encryption schemes. Security teams struggle to harmonize policies without dedicated expertise, lengthening deployment cycles and inflating operating costs. The shortage of cloud-security talent therefore restrains the pace at which the data loss prevention market can transition toward fully orchestrated multicloud protection.

High TCO for Legacy On-Prem Policies

Enterprises that invested heavily in on-site DLP a decade ago face steep migration bills as they pivot to cloud-first strategies. Policy conversion, system integration, and staff retraining add layers of direct and indirect cost. Many firms adopt hybrid architectures as a stop-gap, but this increases complexity, dampening near-term spending on next-generation offerings within the data loss prevention market.

Segment Analysis

By Deployment: Cloud Dominance Accelerates

Cloud-based deployment models secured 67.3% market share in 2024, and this segment is projected to sustain a 22.1% CAGR through 2030. The data loss prevention market size for cloud services will therefore scale in parallel with enterprise SASE adoption. Cloud delivery enables single console management and elastic policy enforcement across remote users, mitigating the burdens of patching and hardware refresh cycles. On-prem solutions persist in heavily regulated sectors such as defense or critical infrastructure where data must remain within physically controlled locations. Yet their relative growth is subdued because hybrid-work realities demand anywhere-access inspection that pure on-site deployments cannot deliver efficiently.

Cloudflare’s SASE framework illustrates how integrated DLP detects and blocks policy violations within secure web gateway and CASB streams, demonstrating the architectural preference shift toward converged services. Organizations scaling rapidly or dealing with seasonal data spikes benefit from metered consumption models that align cost with usage, thereby reinforcing the demand trajectory of the data loss prevention market.

By Solution: Endpoint DLP Leads Innovation

Endpoint controls accounted for 46.7% of revenue in 2024 and remain the fastest advancing solution at 22.4% CAGR, reflecting the surge in device-centric data handling. The rising prevalence of generative-AI coding assistants introduces novel exfiltration vectors that endpoint agents are uniquely positioned to intercept. Researchers demonstrated a “rules file backdoor” that smuggles secrets via benign-looking configuration files, bypassing conventional reviews. Vendors now embed behavioral AI to monitor clipboard use, screen capture, and code-generation patterns, increasing protection precision and powering growth in the data loss prevention market.

Network DLP preserves relevance for in-flight data scrutiny, especially in complex campus networks. Meanwhile, storage-centric tools protect high-volume file shares inside data centers. Nonetheless, enterprises gravitate toward endpoint-first strategies because employees engage with sensitive data directly on laptops, mobiles, and virtual desktops. Microsoft’s Purview suite extends endpoint policies into browser traffic and SaaS sessions, signalling how platform vendors fuse data governance with endpoint telemetry.

By End-User Industry: Manufacturing Emerges as Growth Leader

BFSI organizations held 27.5% of expenditure in 2024, cementing their position as the largest vertical for the data loss prevention market. Regulatory imperatives such as PCI DSS and Basel III compel banks and insurers to safeguard client records and transactional data. Manufacturing, however, is projected to register the highest 21.7% CAGR, driven by Industry 4.0 initiatives that connect operational assets to corporate IT networks. As smart factories generate proprietary process data and digital twins, intellectual-property leakage risk intensifies, prompting accelerated DLP roll-outs.

Technology and telecom firms remain early adopters due to high data velocity, while government agencies prioritize DLP to protect classified information. Healthcare providers, balancing data accessibility with HIPAA-like privacy commitments, increasingly deploy content-aware policies that distinguish between treatment-related sharing and unauthorized export. Across verticals, unified platforms that marry DLP with insider-risk management are gaining mindshare, reinforcing the expansion of the data loss prevention market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Insider-Risk Detection Gains Momentum

Encryption retained the single-largest application share at 23.5% in 2024 because it anchors data-at-rest and in-transit security across industries. Yet insider-risk analytics is expected to rise at 23.2% CAGR through 2030 as organizations grasp that trusted users can cause outsized harm. Fortinet’s FortiDLP combines AI-driven user-and-entity behavior analytics with SaaS visibility to surface anomalous activity from day one. Email and collaboration protection continue to address inadvertent leaks, whereas source-code governance safeguards intellectual-property lifecycles in software firms.

Emerging applications now include IoT data protection and blockchain-based integrity checks. These niches broaden the addressable scope, enlarging the data loss prevention market size as digital-transformation projects multiply. Cloud storage security also matures because enterprises demand native controls within object stores and file-sync services, ensuring consistent labeling and access governance regardless of repository.

Geography Analysis

North America commanded 24.2% of global revenue in 2024, anchored by stringent federal and state regulations plus a well-capitalized private sector that budgets for zero-trust programs. United States agencies embrace DLP inside SASE blueprints published by the Cybersecurity and Infrastructure Security Agency, while Canada’s privacy regime and Mexico’s expanding fintech ecosystem add regional momentum. High breach costs and mature cyber-insurance markets sustain a premium on advanced controls, consolidating North America’s role as a technology proving ground for the data loss prevention market.

Asia-Pacific is forecast to accelerate at 21.1% CAGR, catalyzed by rapid digitization and sovereign-cloud laws that mandate resident data storage. China’s Cybersecurity Law and India’s Digital Personal Data Protection Act compel localized policy orchestration, driving regional demand for cloud-delivered yet jurisdiction-aware solutions. Japan and South Korea deploy endpoint DLP to safeguard manufacturing know-how, while ASEAN economies leapfrog to cloud-native stacks that bundle DLP with secure web gateways. This regulatory and threat-exposure cocktail positions APAC as the most dynamic arena within the data loss prevention market.

Europe’s growth rests on GDPR enforcement and complementary statutes such as the Digital Operational Resilience Act, which raise minimum control baselines for financial entities. Germany and the United Kingdom anchor spending through robust banking and industrial sectors, whereas France advances sovereign-cloud projects that favor locally hosted DLP services. Southern European economies adopt DLP at a steadier pace, yet pan-EU privacy-by-design mandates universally influence vendor offerings. Data localization clauses inside cloud-outsourcing guidelines spur interest in platforms capable of maintaining policy fidelity across borders, sustaining incremental gains for the data loss prevention market.

Competitive Landscape

Vendor consolidation is reshaping competitive contours. Cyera’s USD 540 million funding and earlier purchase of Trail Security illustrate investor enthusiasm for AI-native platforms that converge data-security-posture management with adaptive DLP. Fortinet folded Next DLP into its Security Fabric, signaling a shift toward tightly integrated endpoint, network, and SASE controls. Forcepoint added Getvisibility to enhance discovery and response analytics, widening its data-security cloud portfolio. Established players such as Cisco and Microsoft exploit platform breadth, embedding DLP into collaboration suites and networking fabrics to address tool sprawl.

Emerging challengers differentiate through machine-learning policy optimization, low-touch deployment, and seamless multicloud connectors. They compete on speed to value—delivering pre-trained classifiers for personally identifiable information, payment data, and source code. White-space opportunity exists in verticalized offerings that contextualize controls for manufacturing, healthcare, and critical infrastructure. As Gartner sunset its standalone DLP Magic Quadrant, buyer evaluation gravitates toward outcome-centric metrics such as mean time to contain data exfiltration, favoring vendors that demonstrate measurable risk reduction in the data loss prevention market.

Partnerships with hyperscalers and SaaS providers are now pivotal. Joint reference architectures simplify integration and assure compliance with sovereign-cloud mandates. Competitive intensity will likely escalate as cloud-security-platform players vie to embed DLP into broader data-security fabrics, lowering the standalone addressable slice yet expanding overall coverage and reinforcing growth prospects for the data loss prevention industry.

Data Loss Prevention (DLP) Industry Leaders

-

Broadcom Inc.

-

Microsoft Corporation

-

GTB Technologies Inc.

-

CoSoSys Group

-

Digital Guardian (Fortra LLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Fortinet launched FortiDLP, integrating AI-enhanced insider-risk management and SaaS coverage.

- March 2025: Forcepoint acquired Getvisibility to expand AI-driven DSPM and data-detection capabilities.

- April 2025: Forcepoint unveiled the Data Security Cloud platform, unifying Enterprise DLP with continuous monitoring.

- May 2025: Fortra bought Lookout’s Cloud Security business, adding SSE and DSPM to Digital Guardian DLP.

Global Data Loss Prevention (DLP) Market Report Scope

The data loss prevention market is defined based on the revenues generated from the deployment of solutions, such as network DLP, endpoint DLP, and datacenter/ storage-based DLP through on-premise and cloud-based that are being used by various end-user industries, such as IT and telecommunication, BFSI, government, healthcare, manufacturing, retail and logistics, and other end-user industries across the globe. The analysis is based on the market insights captured through secondary research and the primaries.

The data loss prevention market is segmented by deployment (on-premise and cloud-based), solution (network DLP, endpoint DLP, datacenter/storage-based DLP), end-user industry (IT and telecommunication, BFSI, government, healthcare, manufacturing, retail, and logistics), and geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Rest of Europe], Asia-Pacific [China, Japan, India, Rest of Asia-Pacific], Latin America, and Middle East and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| By Deployment | On-premise | |||

| Cloud-based | ||||

| By Solution | Network DLP | |||

| Endpoint DLP | ||||

| Storage / Datacenter DLP | ||||

| Others | ||||

| By End-user Industry | BFSI | |||

| IT and Telecom | ||||

| Government and Defense | ||||

| Healthcare | ||||

| Retail and Logistics | ||||

| Manufacturing | ||||

| Others | ||||

| By Application | Cloud Storage Security | |||

| Email and Collaboration Protection | ||||

| IP Protection and Source-code Governance | ||||

| Others | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Southeast Asia | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Egypt | ||||

| Rest of Africa | ||||

| On-premise |

| Cloud-based |

| Network DLP |

| Endpoint DLP |

| Storage / Datacenter DLP |

| Others |

| BFSI |

| IT and Telecom |

| Government and Defense |

| Healthcare |

| Retail and Logistics |

| Manufacturing |

| Others |

| Cloud Storage Security |

| Email and Collaboration Protection |

| IP Protection and Source-code Governance |

| Others |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the data loss prevention market?

The market stands at USD 35.38 billion in 2025 and is forecast to reach USD 94.09 billion by 2030.

How fast is the data loss prevention market expected to grow?

It is projected to expand at a 21.61% compound annual growth rate between 2025 and 2030.

Why are cloud-based DLP deployments gaining so much traction?

Cloud models already hold 67.3% market share because they simplify policy enforcement for distributed users and integrate smoothly with zero-trust and SASE platforms.

Which industry vertical is showing the fastest DLP adoption?

Manufacturing is the fastest-growing vertical, registering a 21.7% CAGR as Industry 4.0 drives the need to protect connected intellectual property.