Data Governance Market Size and Share

Market Overview

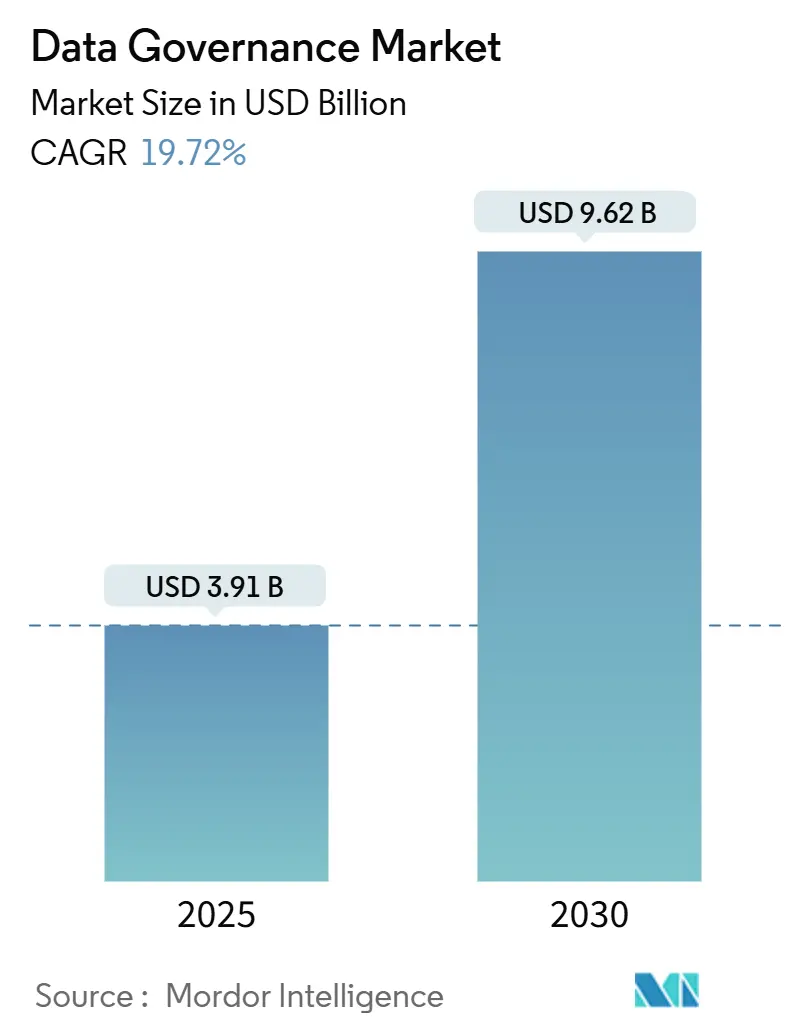

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 3.91 Billion |

| Market Size (2030) | USD 9.62 Billion |

| Growth Rate (2025 - 2030) | 19.72% CAGR |

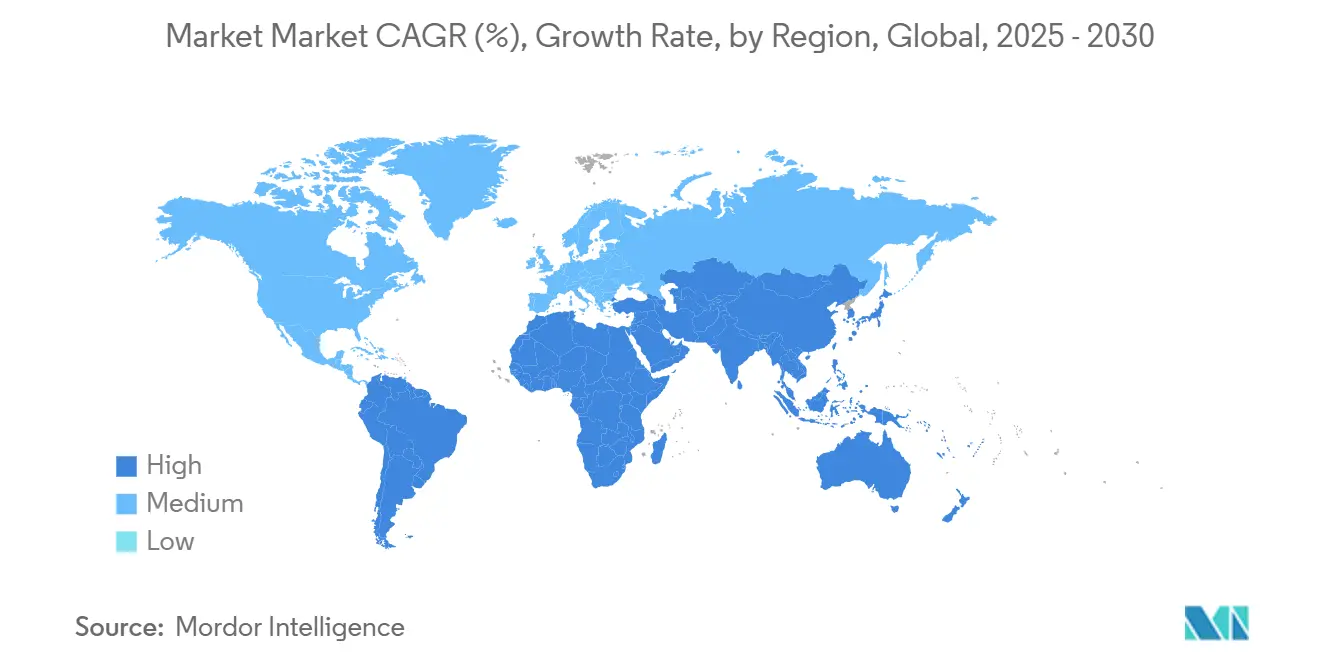

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Data Governance Market Analysis by Mordor Intelligence

The data governance market sized is estimated at USD3.91 billion in 2025 and is forecast to reach USD 9.62 billion by 2030, reflecting a 19.72% CAGR. The surge is underpinned by stricter regulatory mandates, accelerating cloud adoption, and the growing realization that well-governed data is crucial for trustworthy AI, real-time payments, and cross-border commerce. Financial institutions, healthcare providers, and manufacturers are broadening investments as penalties for breaches escalate and as business models shift toward data monetization. Vendors are embedding AI into lineage and catalog tools to automate classification tasks, while buyers emphasize deployment flexibility that supports sovereign-cloud and hybrid architectures. The data governance market is therefore evolving from compliance-focused point solutions to integrated platforms that orchestrate quality, security, and accountability across dispersed data estates.

Key Report Takeaways

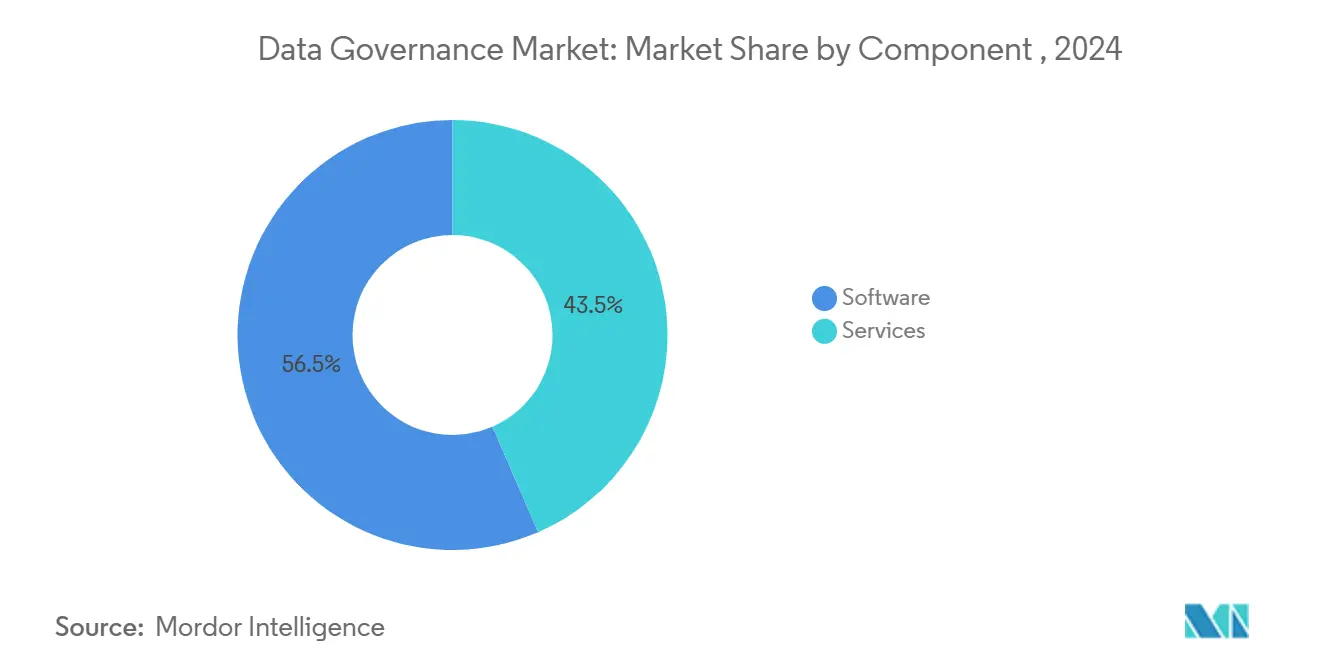

- By component, software held 57.1% of the data governance market share in 2024, whereas services are projected to expand at 23.4% CAGR through 2030.

- By deployment, on-premise installations accounted for 53.6% share of the data governance market size in 2024, while cloud implementations are set to advance at a 22.8% CAGR between 2025-2030.

- By organization size, large enterprises controlled 68% of the data governance market share in 2024; small and medium enterprises will grow fastest at a 24.6% CAGR to 2030.

- By business function, IT and Operations led with 41% revenue share in 2024; the Marketing and Sales segment is forecast to post a 25.2% CAGR through 2030.

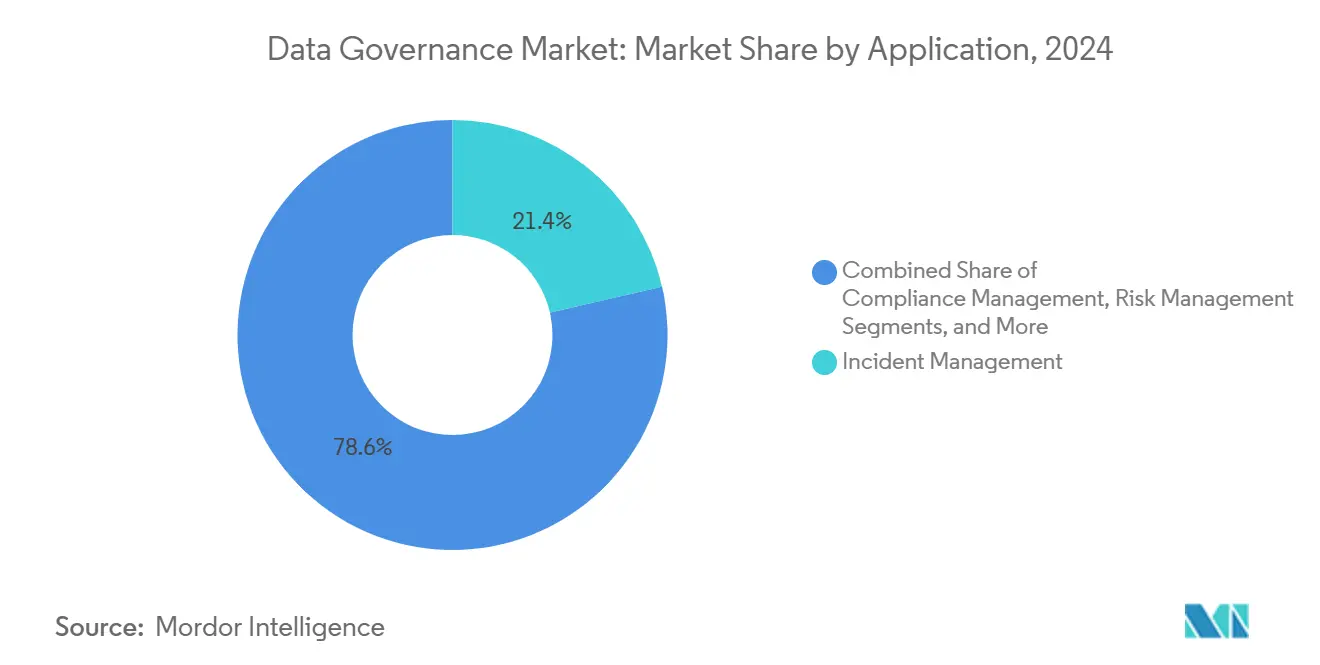

- By application, compliance management commanded 38.5% of the data governance market size in 2024, while incident management is poised for a 21.4% CAGR during 2025-2030.

- By end-user industry, BFSI captured 24.7% of the data governance market share in 2024; Healthcare and Life Sciences is advancing at a 23.8% CAGR through 2030.

- By geography, North America dominated with 35.6% market share in 2024; Asia will expand at a 26.3% CAGR during the forecast horizon.

- IBM, Microsoft, Oracle, SAP, Collibra, Informatica, and Alation collectively controlled roughly 34% of global revenue in 2024, underscoring a moderately fragmented arena.

Global Data Governance Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU AI Act and Global AI-Regulation Requiring Explainable Data Lineage | +5.8% | Europe, North America, global spillover | Medium term (2-4 years) |

| FedNow and Real-Time Payment Rails Forcing Sub-Millisecond Data Integrity in North-American BFSI | +3.2% | North America, with gradual adoption in Europe | Short term (≤ 2 years) |

| APAC Sovereign-Cloud Mandates (e.g., India DPDP Act) Accelerating In-Country Data Catalog Investments | +4.7% | Asia, Middle East, with compliance implications globally | Medium term (2-4 years) |

| Retail-Media Monetisation Elevating Product-Master Data Quality Spend | +2.9% | North America, Europe, developed APAC markets | Medium term (2-4 years) |

| Edge Analytics in Manufacturing 4.0 Demands Near-Edge Metadata Federation | +2.1% | Europe, North America, industrialized APAC | Long term (≥ 4 years) |

Source: Mordor Intelligence

EU AI Act and Global AI-Regulation Requiring Explainable Data Lineage

The EU AI Act, effective August 2024, obliges companies deploying high-risk AI to document data origins, transformations, and quality metrics. Failure can trigger fines up to USD 39.82 million or 7% of global turnover, pushing enterprises to adopt advanced lineage platforms that illustrate end-to-end data flows. Vendors are integrating model-level metadata with traditional catalog systems so that auditors can trace training sets and detect bias. Multinationals anticipate similar provisions in Brazil and Canada, turning compliance into a global requirement. These pressures elevate demand for tools that link datasets, models, and business outcomes in a single governance workspace. As a result, the data governance market is pivoting toward solutions that fuse AI oversight with conventional stewardship capabilities.

FedNow and Real-Time Payment Rails Forcing Sub-Millisecond Data Integrity in North-American BFSI

The FedNow Service went live in July 2023 and now operates 24/7 across participating banks. Sub-millisecond settlement demands pristine data quality and continuous lineage to satisfy anti-money-laundering checks without slowing transactions. Institutions are deploying AI-enabled screening and enrichment pipelines to flag anomalies instantly. Legacy batch-oriented compliance stacks cannot keep pace, so banks are modernizing metadata repositories and automating control tests. This driver accelerates subscription revenue for cloud-native governance vendors that can embed rules directly into payment workflows. It also spurs consulting engagements aimed at retrofitting lineage tools to mainframe cores, a lucrative niche within the wider data governance market.

APAC Sovereign-Cloud Mandates Accelerating In-Country Data Catalog Investments

India’s Digital Personal Data Protection Act obliges significant data fiduciaries to process and store citizen data domestically, employing a ‘negative list’ for restricted transfers. Similar provisions are surfacing in Indonesia and Saudi Arabia. Enterprises respond by standing up regional instances of data catalogs and lineage services deployed on sovereign clouds. Vendors that offer flexible tenancy models and automated localization flags are capturing disproportionate growth across the data governance market.

Retail-Media Monetization Elevating Product-Master Data Quality Spend

Major retailers are converting first-party shopper data into advertising inventory, a business that hinges on accurate product, pricing, and consent metadata. Advertisers demand unified taxonomies and privacy compliance, driving investments in master data governance and collaboration portals.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Enterprise-Scale Data Lineage Tooling in Tier-1 Banks | -2.4% | North America, Europe, developed APAC markets | Medium term (2-4 years) |

| Talent Shortage of Certified Data Stewards and DCAM Practitioners | -3.1% | Global, with severe impact in emerging markets | Short term (≤ 2 years) |

| Legacy Mainframe Interoperability Issues Limiting Real-Time Governance in Defense Agencies | -1.8% | North America, Europe | Medium term (2-4 years) |

Source: Mordor Intelligence

High Total Cost of Ownership for Enterprise-Scale Data Lineage Tooling

Tier-1 banks grapple with multi-million-dollar annual outlays for licenses, integration, and hardware refresh when rolling out enterprise lineage platforms. An Aalto University study confirms that integration with legacy systems and the absence of standards inflate timelines and budgets. Some institutions resort to manual mapping to lower expenses, slowing full-fledged deployments. Vendors respond with modular pricing and consumption-based cloud editions, yet sticker shock remains a prominent brake on expansion within the data governance market.

Talent Shortage of Certified Data Stewards and DCAM Practitioners

Only 36 organizations had joined the EDM Council’s Data Excellence Program by February 2025, underscoring limited certified talent worldwide. Scarcity inflates salaries and elongates project schedules. Emerging economies feel the pinch most acutely, where competition for scarce expertise pits local firms against multinationals. Managed services and low-code automation tools are gaining popularity as stop-gap measures, though they cannot fully offset the skill deficit.

Segment Analysis

By Component: Software Dominates While Services Accelerate

Software solutions accounted for 57.1% of revenue in 2024, anchoring the data governance market with capabilities that automate policy enforcement, metadata harvesting, and lineage visualization. AI-driven classification and anomaly detection are now baseline features, helping organizations comply with the EU AI Act and FedNow directives in real time. The data governance market size for software is projected to deepen as vendors embed model-governance modules that audit AI pipelines.

Services, encompassing implementation, training, and managed operations, are forecast to expand at 23.4% CAGR. Talent shortages and rising regulatory complexity push organizations to outsource framework design and day-to-day stewardship. Managed services providers are layering SLAs for data quality and consent compliance, differentiating themselves in a fragmented services arena.

Growth in services is also propelled by industry-specific advisory packages. Banking clients demand lineage accelerators pre-mapped to BCBS 239, while healthcare buyers request HIPAA-ready templates. This vertical tailoring leaves room for boutique consultancies alongside global system integrators. Consequently, the data governance market continues shifting from purely licensing models toward mixed recurring revenue streams.

By Deployment: On-Premise Persistence Amid Cloud Acceleration

On-premise deployments retained a 53.6% share in 2024 as financial services and healthcare firms insist on local control over sensitive records. Mainframe coexistence and regulated workloads reinforce datacenter preferences despite broader enterprise migration to SaaS. The data governance market share for on-premise solutions is expected to erode gradually as cloud security certifications widen.

Cloud governance tools are advancing at 22.8% CAGR, driven by sovereign-cloud mandates and remote-work norms. Frameworks such as the EDM Council’s CDMC provide best practices that reassure auditors. Hybrid patterns dominate: sensitive golden records sit on-premise, while catalog search, quality rules, and reporting run in the cloud. Vendors compete on cross-plane policy orchestration that keeps controls consistent across locations, a capability now essential to win enterprise contracts.

By Organization Size: Large Enterprises Lead While SMEs Accelerate

Large enterprises held 68% of spending in 2024 due to complex data estates and multi-jurisdiction compliance exposure. Many have formal Data Councils and enterprise architects who mandate stewardship frameworks, as illustrated in DSM-Firmenich’s 2024 report.

SMEs represent the fastest-growing cohort at 24.6% CAGR. Cloud-delivered catalogs with usage-based fees lower barriers, while pre-configured rule libraries shrink set-up time. Case studies reveal that SMEs adopting structured governance cut project overruns by 40% and boost employee satisfaction by 30%. This democratization widens the addressable data governance market.

Budget-constrained SMEs often start with targeted initiatives such as consent management, then iterate toward full frameworks. Vendors courting this segment emphasize low-code policy design and community support to fill knowledge gaps. Large enterprises, by contrast, prioritize lineage depth and cross-cloud enforcement, driving demand for high-end modules and professional services.

By Business Function: IT Operations Dominates, Marketing Surges

IT and Operations teams anchored 41% of deployments in 2024. Their stewardship of infrastructure makes them logical custodians of governance tooling, especially for master data and security policies. Federated operating models are emerging, allocating domain ownership to business units while central IT supplies guardrails. Stibo Systems notes automated governance and data productization as defining 2025 trends.

Marketing and Sales investments will grow at 25.2% CAGR through 2030. The demise of third-party cookies forces publishers and brands to better curate first-party datasets, elevating governance to a revenue driver. These teams require fine-grained consent flags and identity resolution that feed personalization engines without breaching privacy law, thereby broadening the data governance market.

Legal and Compliance groups maintain oversight on policy scope, while Finance gains from governed data to reduce close cycles. Human Resources is adopting governance to handle sensitive employee records, especially following hybrid work patterns. Collectively, these dynamics transform governance from an IT-centric discipline into a cross-functional imperative.

By Application: Compliance Management Necessity, Incident Management Growth

Compliance management dominates governance applications with a 38.5% market share in 2024, reflecting the regulatory pressures driving initial governance investments across industries. Organizations implement governance frameworks primarily to demonstrate compliance with regulations like GDPR, CCPA, and industry-specific requirements such as HIPAA in healthcare or BCBS 239 in banking. The EU AI Act has further expanded compliance requirements, mandating robust governance for organizations deploying high-risk AI systems. According to Collibra, the AI Act imposes significant compliance obligations based on risk levels, with penalties for non-compliance reaching up to EUR 35 million (USD 40.49 million) or 7% of global turnover.

Incident management applications are experiencing the fastest growth at 21.4% CAGR (2025-2030), as organizations recognize the critical role of governance in preventing, detecting, and responding to data breaches and quality issues. Effective incident management requires comprehensive data lineage to understand impact scope, clear ownership definitions to establish responsibility, and documented procedures for remediation. According to Helix International, poor data governance cost Citibank a USD 400 million fine, illustrating the financial risks associated with inadequate governance frameworks.

Risk management applications leverage governance capabilities to identify and mitigate data-related risks, while audit management functions ensure ongoing compliance and control effectiveness. Data quality management applications focus on establishing and maintaining standards for accuracy, completeness, and consistency across enterprise data assets. The integration of these application areas is creating more comprehensive governance platforms that address multiple use cases through shared capabilities like metadata management, lineage tracking, and policy enforcement.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: BFSI Leadership, Healthcare Acceleration

BFSI sectors held 24.7% market share in 2024. Basel and FedNow compliance, along with anti-fraud analytics, demand granular lineage and immutable audit trails. Banks deploying real-time rails also invest in AI-assisted sanctions screening that leans on governed reference data, reinforcing spend within the data governance market.

Healthcare and Life Sciences will grow at 23.8% CAGR as electronic health records and AI-driven diagnostics proliferate. IBM stresses that lineage safeguards clinical decision support accuracy and meets HIPAA obligations. Interoperability initiatives like FHIR amplify the need for harmonized metadata, boosting license revenue for catalog vendors.

Telecom, Government, and Manufacturing buyers exhibit rising demand tied to 5G, digital sovereignty, and Industry 4.0, respectively. Edge analytics in factories and defense modernization programs opens adjacent opportunities for specialized governance frameworks designed for low-latency and air-gapped networks.

Geography Analysis

North America commanded 35.6% revenue in 2024, supported by mature digital-transformation investments and frameworks such as the Federal Enterprise Architecture that emphasize FedRAMP-aligned governance. Financial institutions racing to integrate FedNow exemplify how regulatory deadlines catalyze spending. AI safety rule-making by the National Institute of Standards and Technology further spurs platform enhancements. The data governance market size in the region benefits from dense ecosystems of consultants and hyperscale cloud providers that embed stewardship capabilities natively.

Asia is the fastest-growing region at 26.3% CAGR. India’s DPDP Act reshapes data flows, while China’s draft negative list for data exports tightens local hosting requirements. These statutes propel investments in sovereign-cloud catalogs capable of enforcing locale-specific retention policies. Japan and South Korea refine existing directives to match global benchmarks, amplifying cross-border alignment. Multinationals now budget region-specific governance clusters, enlarging the addressable data governance market.

Europe retains significant scale through the GDPR and newly enacted EU AI Act. The European Data Governance Act stimulates sectoral data spaces in health, energy, and mobility, fostering demand for interoperable metadata standards [2]David Talaga, “AI and Data Compliance: How the AI Act Will Impact Your Organization,” Collibra, collibra.com . The Middle East and Africa are earlier in their maturity curve but are accelerating, driven by smart-city projects and Gulf Cooperation Council data-sovereignty rules. Canada’s national roadmap pinpoints 35 standardization gaps, prompting federally funded pilots [3]Standards Council of Canada, “Canadian Data Governance Standardization Roadmap,” scc-ccn.ca . Together, these dynamics produce a geographically diverse but regulatory-driven expansion path for the data governance market.

Competitive Landscape

Competitive Landscape

Competition is moderately fragmented. Enterprise software giants such as IBM, Microsoft, Oracle, and SAP bundle governance into sprawling data management suites, leveraging installed bases for upselling. Specialized vendors like Collibra, Informatica, Alation, and BigID focus on deep lineage, cataloging, and privacy tooling, often integrating with larger platforms via open APIs. CRN’s 2025 Big Data 100 lists Actian, Denodo, and Talend among integration-centric providers that complement governance rollouts.

Strategic differentiation centers on AI automation, domain-specific accelerators, and hybrid deployment agility. Collibra’s January 2025 launch of AI governance extensions underscores vendor moves to marry model oversight with classical metadata stewardship. OpenText’s absorption of Micro Focus beefed up legacy-system connectors, attacking an interoperability pain point in defense and manufacturing. Vendors also partner with hyperscalers to offer reference architectures pre-certified for sovereignty zones, streamlining procurement for regulated buyers.

Managed services are rising as talent shortages persist. IBM’s Data and AI business and Accenture’s Applied Intelligence practice package run-operate models that guarantee lineage coverage levels. Boutique players supply DCAM coaching and interim data-officer staffing. White-space opportunities lie in edge-native governance for IoT and integrated policy engines spanning multicloud estates, areas where current offerings remain nascent. Consolidation is expected as larger providers acquire niche capabilities to deliver end-to-end governance fabric across the expanding data governance market.

Data Governance Industry Leaders

-

Collibra NV

-

TIBCO Software Inc.

-

Alation Inc.

-

Microsoft Corporation

-

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Perforce issued an analysis outlining how the EU AI Act reshapes enterprise data oversight, stressing privacy-by-design policies.

- March 2025: Access Now provided feedback on India’s draft DPDP Rules 2025, advocating clearer consent-manager roles and robust erasure protocols.

- February 2025: EDM Council marked the first anniversary of its Data Excellence Program, counting 36 member firms that benchmark governance maturity against DCAM best practices.

- January 2025: The Observer Research Foundation released “Privacy in Practice,” offering operational roadmaps for DPDP Act compliance.

Global Data Governance Market Report Scope

Data governance solutions perform crucial functions such as establishing data management guidelines, implementing protocols to address data discrepancies, and empowering businesses to make informed decisions by leveraging top-tier data quality.

The data governance market is segmented by deployment (cloud and on-premise), organization size (large-scale business and small- and medium-scale business), component (software and service), business function (operation and IT, legal, finance, and other business functions), end-user industry (IT and telecom, healthcare, retail, defense, BFSI, and other end-user industries), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Component | Software | Data Quality and Profiling Tools | |

| Metadata Management and Data Catalog | |||

| Master Data Management | |||

| Data Lineage and Impact Analysis | |||

| Data Security and Privacy Governance | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment | Cloud | ||

| On-Premise | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Business Function | IT and Operations | ||

| Legal and Compliance | |||

| Finance and Risk | |||

| Marketing and Sales | |||

| Human Resources | |||

| Other Functions | |||

| By Application | Compliance Management | ||

| Risk Management | |||

| Audit Management | |||

| Incident Management | |||

| Data Quality Management | |||

| Other Applications | |||

| By End-user Industry | BFSI | ||

| IT and Telecom | |||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Government and Defense | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Media and Entertainment | |||

| Other Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Latin America | Brazil | ||

| Argentina | |||

| Chile | |||

| Mexico | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Sweden | |||

| Norway | |||

| Finland | |||

| Denmark | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Southeast Asia | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East | GCC (Saudi Arabia, UAE, Qatar) | ||

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

| Software | Data Quality and Profiling Tools |

| Metadata Management and Data Catalog | |

| Master Data Management | |

| Data Lineage and Impact Analysis | |

| Data Security and Privacy Governance | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Operations |

| Legal and Compliance |

| Finance and Risk |

| Marketing and Sales |

| Human Resources |

| Other Functions |

| Compliance Management |

| Risk Management |

| Audit Management |

| Incident Management |

| Data Quality Management |

| Other Applications |

| BFSI |

| IT and Telecom |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Government and Defense |

| Manufacturing |

| Energy and Utilities |

| Media and Entertainment |

| Other Industries |

| North America | United States |

| Canada | |

| Latin America | Brazil |

| Argentina | |

| Chile | |

| Mexico | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Norway | |

| Finland | |

| Denmark | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Southeast Asia | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | GCC (Saudi Arabia, UAE, Qatar) |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

Key Questions Answered in the Report

What is the current size of the data governance market and how fast is it growing?

The market is valued at USD3.91 billion in 2025 and is expected to expand at a 19.72% CAGR to reach USD9.62 billion by 2030.

Which region leads the data governance market today?

North America holds 35.6% of global revenue in 2024, driven by stringent regulations and advanced digital-transformation projects.

Which industry spends the most on data governance solutions?

Banking, Financial Services, and Insurance (BFSI) commanded 24.7% market share in 2024 due to real-time payment rails and strict compliance mandates.

How are new regulations such as the EU AI Act impacting demand?

The EU AI Act requires detailed data lineage and explainability for high-risk AI, adding +5.8% to forecast CAGR and prompting rapid adoption of advanced lineage tools.

Why are services growing faster than software in this space?

A shortage of certified data stewards and complex regulatory demands push organizations to seek external expertise, fueling a 23.4% CAGR for services through 2030.

What deployment model is gaining the most momentum?

Cloud-based governance is rising at a 22.8% CAGR as firms adopt sovereign-cloud and hybrid architectures to meet localization rules and scale rapidly.

Page last updated on: June 19, 2025