Data Converter Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

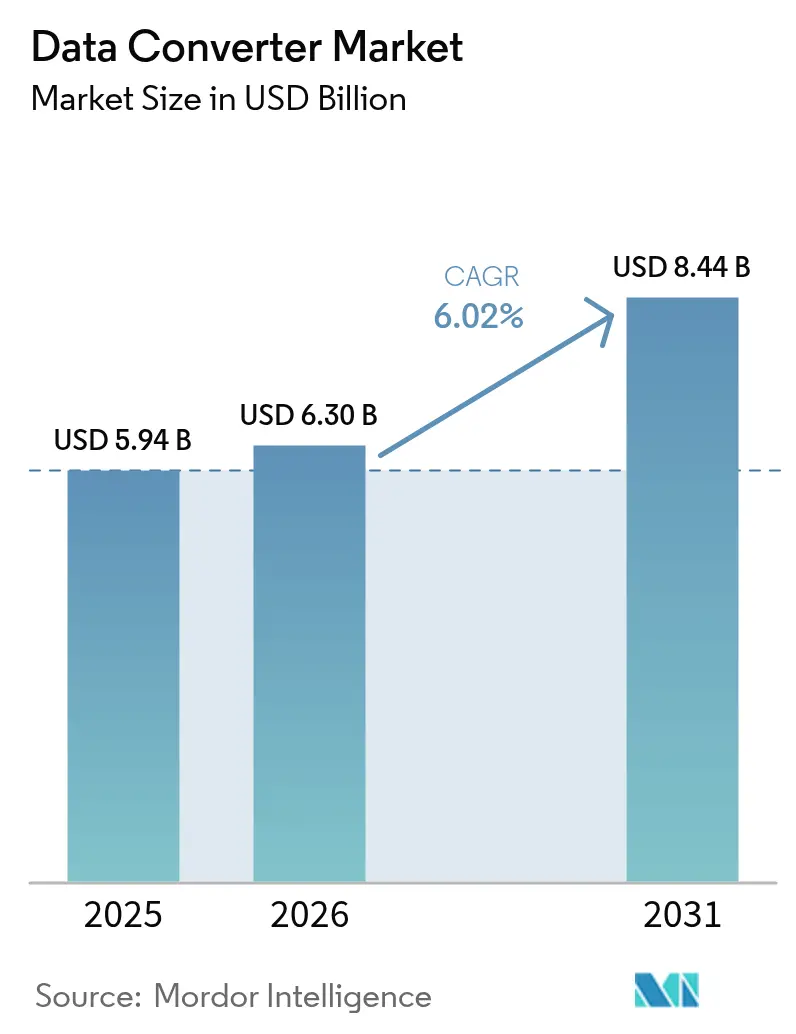

| Market Size (2026) | USD 6.3 Billion |

| Market Size (2031) | USD 8.44 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Converter Market Analysis by Mordor Intelligence

The data converter market size is expected to grow from USD 5.94 billion in 2025 to USD 6.3 billion in 2026 and is forecast to reach USD 8.44 billion by 2031 at 6.02% CAGR over 2026-2031. Intensifying 5G roll-outs, the shift toward vehicle electrification, and rising demand for edge AI processing continue to reinforce the indispensability of high-performance converters across telecommunications, automotive, and industrial ecosystems. System architects increasingly favor integrated mixed-signal solutions to shorten design cycles and lower power budgets, while ongoing foundry capacity constraints impose supply-side discipline that supports pricing power for differentiated devices. Competitive intensity revolves around achieving higher resolution with smaller die sizes, and advanced packaging innovations such as system-in-package (SiP) modules are gaining traction as a route to further integration. Regional growth momentum remains strongest in Asia-Pacific, where deep semiconductor value-chain roots and rapid 5G adoption accelerate converter deployments.

Key Report Takeaways

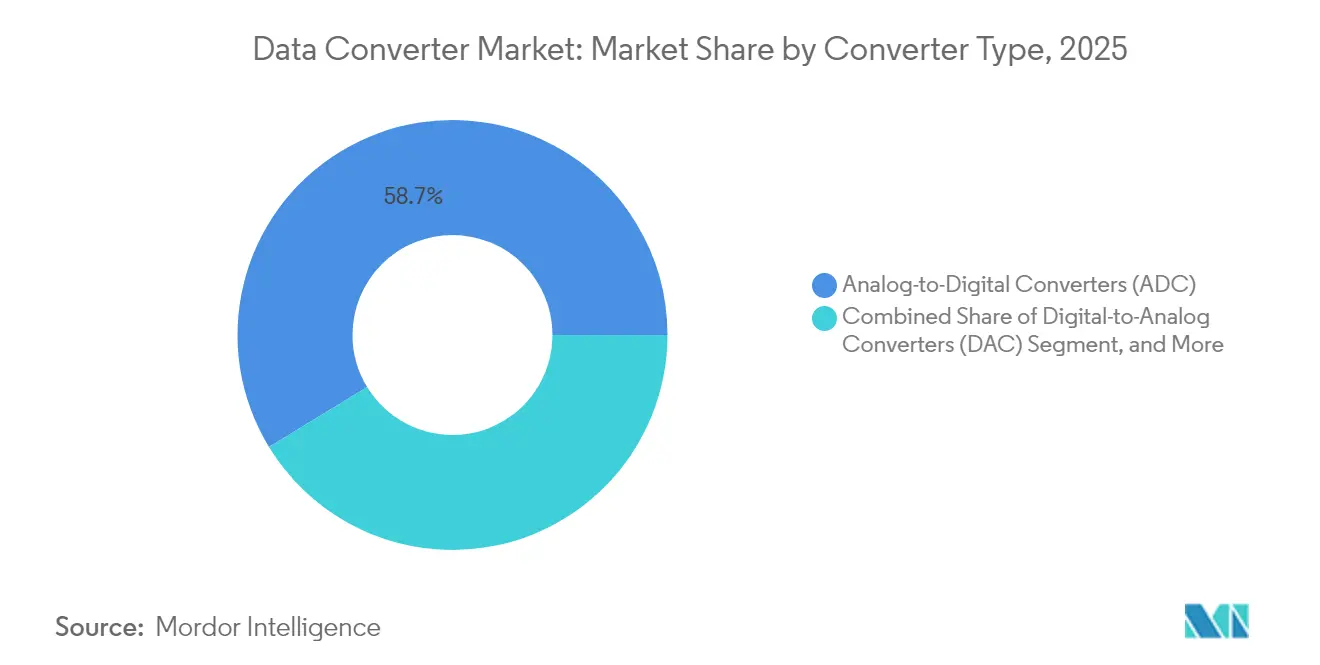

- By converter type, analog-to-digital converters led with 58.72% of the data converter market share in 2025, whereas mixed-signal converters are on track for a 7.48% CAGR through 2031.

- By resolution, 10-12-bit devices accounted for 37.85% of the data converter market size in 2025, while >16-bit precision converters are projected to expand at an 7.86% CAGR to 2031.

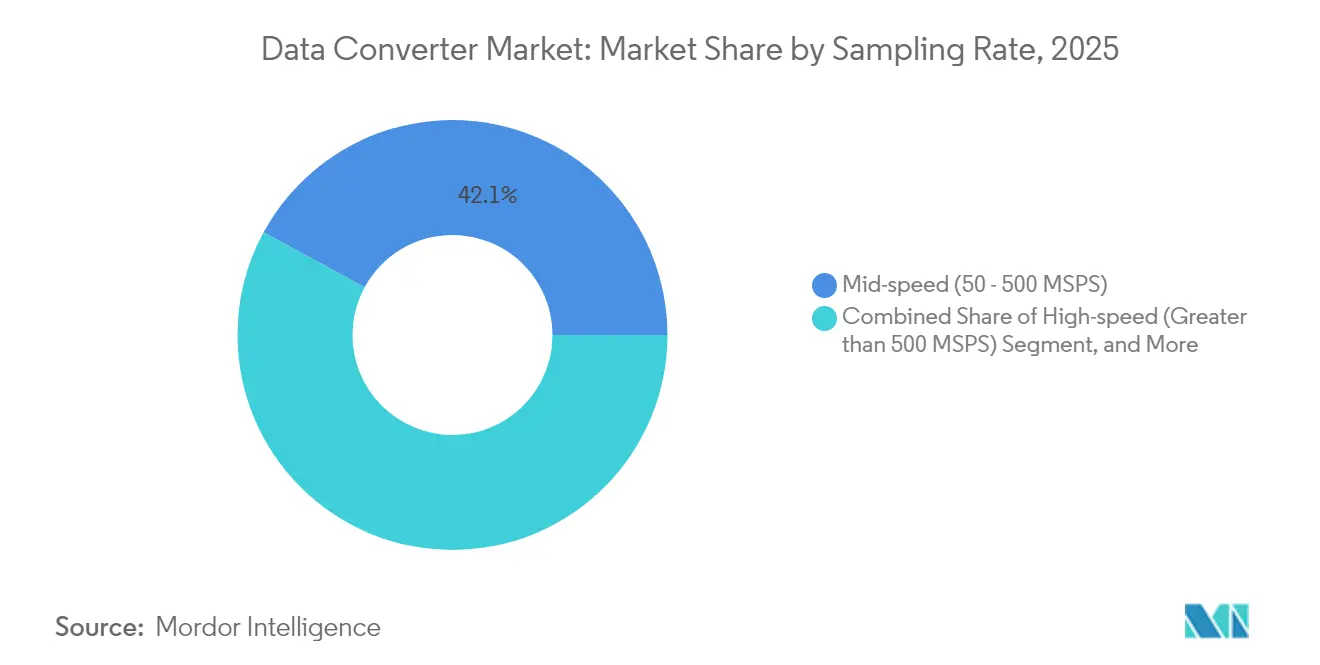

- By sampling rate, mid-speed (50-500 MSPS) parts held 42.08% of the data converter market share in 2025; high-speed devices above 500 MSPS are poised for an 7.95% CAGR through 2031.

- By end-user industry, telecommunications applications captured a 25.44% of the data converter market share, whereas automotive demand is advancing at a 6.92% CAGR through 2031.

- By geography, Asia-Pacific commanded 40.12% of the data converter market share in 2025 and is forecast to progress at a 6.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Converter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G infrastructure boom | +1.8% | Global (APAC, North America lead) | Medium term (2-4 years) |

| Higher resolution in medical imaging | +1.2% | North America, Europe, APAC | Long term (≥ 4 years) |

| Automotive electrification | +1.5% | Global (Europe, China spearhead) | Medium term (2-4 years) |

| Edge AI hardware accelerators | +1.0% | North America, APAC core | Short term (≤ 2 years) |

| Ultra-low-power IoT sensor nodes | +0.8% | Global industrial installations | Long term (≥ 4 years) |

| Radiation-hardened defense demand | +0.4% | North America, Europe, select APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G Infrastructure

Massive MIMO architectures in 5G base stations call for multi-gigahertz ADC and DAC channels with spurious-free dynamic range above 60 dB, forcing converter makers to optimize linearity without ballooning power budgets.[1]IEEE Xplore, “A 14-bit 75-MS/s Pipelined ADC,” ieeexplore.ieee.org Governments earmarked USD 24.4 billion in China, USD 13.1 billion in the United States, and USD 10.8 billion across Europe for 5G deployments in 2024, concentrating demand on high-speed, high-resolution parts that strain specialty analog foundry capacity. Software-defined radio platforms add further complexity because equipment makers now require 14-16-bit resolution at multi-GSPS rates within a single system-on-chip, spurring premium pricing for devices that combine speed with programmable flexibility.[2]Monolithic Power Systems, “High-Speed ADCs for Broadband Communications,” monolithicpower.com Vendors able to supply monolithic solutions that integrate RF front ends alongside high-speed converters are securing multi-year supply agreements with telecom OEMs seeking to simplify procurement and ensure long-term support.

Rising Resolution Requirements in Medical Imaging

MRI, CT, and next-generation ultrasound modalities increasingly depend on 16-24-bit delta-sigma ADCs to deliver enhanced dynamic range and noise performance that meet AI-enabled diagnostic standards. Ultrasound consoles typically operate between 40 MHz and 200 MHz sampling rates, and any signal degradation directly compromises machine learning algorithms that now underpin anomaly detection workflows. Regulators scrutinize converter specifications during FDA 510(k) submissions, motivating OEMs to select devices with documented clinical performance histories and extensive in-field operating data. Delta-sigma topologies are favored because their inherent noise-shaping characteristics minimize analog filtering requirements, allowing designers to shorten validation cycles while maintaining patient-safety thresholds. Suppliers addressing this niche bolster revenue resiliency because medical devices follow seven-to-ten-year product lifecycles that insulate demand from short-term economic swings.

Shift Toward Electrification in Automotive Systems

Electric vehicle powertrains rely on 12-16-bit ADCs that maintain ±1 LSB accuracy across −40 °C to +125 °C while simultaneously monitoring hundreds of battery cells at millisecond cadence.[3]Analog Devices, “Corporate Investor Presentation Q4 2024,” analog.com ADAS functions integrate camera, radar, and LiDAR inputs that each demand converter architectures tailored to unique frequency bands, creating incremental design-win opportunities per vehicle. Automotive qualification through AEC-Q100 extends development cycles by up to two years, favoring suppliers with in-house test capacity and established functional-safety documentation. As battery capacities climb, automakers adopt multi-channel delta-sigma converters that deliver synchronized sampling for cell-balancing algorithms, driving volume growth for devices offering embedded diagnostics. Policy mandates in Europe and China accelerate platform refresh cycles, elevating converter attach rates per vehicle even when global auto sales plateau.

Growth of Edge AI Hardware Accelerators

Wearables and industrial sensor nodes now embed micro-watt neural engines that require ultra-low-power ADCs capable of toggling between sub-40 µA idle modes and full-resolution bursts, a design envelope exemplified by AKM’s AK5707ECB, which trims detection current by 70% from prior generations. Energy-harvesting power budgets drive adoption of converters with dynamic power scaling and on-chip digital filtering to reduce external component counts. Edge inferencing workloads are sensitive to quantization noise; hence, 16-bit resolution has become the baseline even in battery-powered devices, opening a lucrative segment for delta-sigma architectures optimized for low pass-band ripple. Semiconductor vendors bundle reference designs that pair microcontrollers with matched ADCs, shrinking time-to-prototype for start-ups deploying vision and acoustic anomaly detection at the edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal-noise ceiling at high speed | −0.9% | Global high-speed applications | Short term (≤ 2 years) |

| Foundry supply-chain cyclicality | −1.2% | Global (Taiwan, South Korea hubs) | Medium term (2-4 years) |

| Mixed-signal SoC design complexity | −0.7% | Global | Long term (≥ 4 years) |

| Evolving RF emission compliance costs | −0.5% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Thermal-Noise Limitations at Higher Sampling Rates

As converter sampling speeds eclipse 1 GSPS, fundamental thermal noise rises proportionally with bandwidth, setting a floor near −174 dBm/Hz and limiting achievable signal-to-noise ratios. Designers attempt to circumvent the barrier through time-interleaved architectures, yet mismatch and calibration overheads inflate silicon area and power consumption. Migrating to sub-28 nm nodes improves intrinsic device noise but drives up wafer costs and yield risk, constraining accessibility for mid-volume industrial customers. The physics-driven ceiling, therefore, tempers growth in bleeding-edge segments, steering some OEMs toward alternative system architectures that relax converter performance demands.

Supply-Chain Cyclicality of Specialty Foundries

Analog processes optimized for high-accuracy data converters make up a fraction of global wafer starts, and capacity allocation swings behind more profitable digital logic runs whenever demand spikes for memory or AI accelerators. Geographic concentration in Taiwan and South Korea exposes converter vendors to geopolitical and climate-related disruptions that can extend lead times beyond 40 weeks. To hedge risk, tier-one suppliers pre-book capacity under multi-year agreements, an approach that ties up working capital and reduces flexibility. Emerging multi-project wafer services only partly offset the imbalance because they cater to prototypes rather than high-volume production, leaving the market vulnerable to cyclical undersupply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Converter Type: Mixed-Signal Integration Drives Growth

Analog-to-digital converters retain primacy with 58.72% of the data converter market share in 2025 as telecom, medical, and industrial systems depend on precise digitization for every signal chain step. Device counts per system stay elevated even as integration rises, maintaining a large installed base. Mixed-signal converters, however, represent the clear growth vector with a 7.48% CAGR to 2031 because they collapse discrete ADC and DAC channels into a single package, saving board area and trimming bill-of-materials cost. The trend dovetails with wider adoption of system-in-package modules, enabling OEMs to combine converter cores with power management and interface logic under one substrate. As a result, the data converter market is witnessing a heavier R&D focus on mixed-signal devices that embed self-calibration engines, temperature sensors, and on-chip voltage references to enhance field reliability.

System integrators in automotive and industrial segments value the diagnostic features implicit in mixed-signal designs because they facilitate predictive maintenance programs without external circuitry. Texas Instruments’ 16-channel DAC60516 exemplifies the direction, coupling a 12-bit DAC array with an internal 2.5 V reference to cut peripheral components by up to 30%. Over the forecast horizon, mixed-signal solutions are projected to capture incremental sockets once reserved for separate ADC/DAC pairs, reinforcing their status as the most dynamic portion of the data converter market.

By Resolution: Precision Applications Accelerate >16-Bit Adoption

10-12-bit devices commanded 37.85% revenue in 2025, serving mainstream wireless infrastructure and consumer electronics where moderate dynamic range satisfies most modulation and audio requirements. At the premium end, >16-bit converters are pacing the field with an 7.86% CAGR to 2031, reflecting intensified demand from MRI scanners, geophysical instruments, and factory automation rigs that must measure signals buried in sub-microvolt noise. The data converter market size for high-precision segments is therefore projected to expand rapidly despite their smaller volume base because average selling prices sit several multiples above lower-resolution alternatives.

Advances in calibration algorithms and digital error correction now permit >16-bit parts to operate from 2.5 V supplies without sacrificing linearity, broadening their compatibility with modern low-power logic and reducing the need for expensive analog signal conditioning. Nisshinbo Micro Devices’ pin-compatible 16-, 20-, and 24-bit NA220x family lets OEMs tier performance grades across a single PCB layout, materially shrinking qualification cycles. Ongoing shrinkage in cost per resolution step will continue to erode the ≤8-bit niche, which is increasingly confined to legacy applications.

By Sampling Rate: High-Speed Segment Leads Growth Trajectory

Mid-speed converters between 50 MSPS and 500 MSPS held 42.08% of 2025 revenue, reflecting a broad user base across industrial automation, ultrasound, and traditional telecom baseband functions. Yet devices running beyond 500 MSPS are forecast to log an 7.95% CAGR through 2031 as massive MIMO, phased-array radar, and software-defined instrumentation migrate to multi-gigahertz instantaneous bandwidths. The data converter market size for high-speed categories will consequently outpace unit growth, given their elevated price points and complex packaging requirements.

Recent IEEE work demonstrates 200 MSPS pipeline ADCs achieving 44 fJ per conversion step, an efficiency milestone that underscores the pace of innovation at the performance frontier. Competition in this bracket revolves around time-interleaving, current-mode residue amplification, and advanced clock-distribution techniques that suppress aperture jitter. Suppliers capable of shipping converters with embedded digital down-conversion and JESD204 interfaces are winning sockets because they reduce FPGA gate consumption downstream.

By End-User Industry: Automotive Emerges as Growth Leader

Telecommunications applications accounted for 25.44% of global revenue in 2025 because every base station, optical modem, and microwave backhaul link employs multiple signal-chain converters. The data converter market continues to count operators’ capex cycles as its single largest demand driver. Automotive, however, is advancing at a 6.92% CAGR through 2031, propelled by electrified powertrains, sensor fusion, and the transition from driver assistance to partial autonomy. Converters per vehicle increase as OEMs add battery-state monitoring, motor-control feedback loops, and redundant perception channels, shifting the mix toward higher reliability, AEC-Q100-grade components.

Regulatory pushes for zero-emission fleets and mandatory safety packages in Europe, China, and North America create structural demand insulation even when macroeconomic conditions soften. Converter suppliers that offer scalable families spanning 10- to 24-bit resolution and fault-diagnostic registers are best placed to command design wins across multiple vehicle platforms. Industrial automation and test equipment remain steady contributors, but price erosion moderates their revenue trajectory relative to high-growth verticals.

Geography Analysis

Asia-Pacific retained leadership with a 40.12% revenue contribution in 2025 and is projected to register a 6.73% CAGR through 2031, supported by China’s investments in domestic wafer fabrication, Japan’s metrology expertise, and South Korea’s advanced packaging capacity. Power-efficient mixed-signal converters that address both consumer and industrial demand profiles find ready adoption across regional OEMs, which favor local supply ecosystems to tighten inventory cycles. Regional governments underwrite semiconductor self-reliance programs that further accelerate the adoption of high-performance converters in communications infrastructure and AIoT edge devices.

North America ranks second by revenue and continues to manifest strong pull from defense electronics, broadband roll-outs, and life-science instrumentation. Converters that meet radiation-tolerant profiles or satisfy FDA design dossiers attract pricing premiums, mitigating cyclicality in consumer and handset demand. A vibrant fabless community centered in Silicon Valley and Austin sustains a healthy pipeline of start-ups targeting specialized converter architectures, reinforcing overall regional dynamism in the data converter market.

Europe leverages leadership in automotive, industrial automation, and renewable-energy applications that specify stringent functional-safety and electromagnetic-compatibility criteria. Although the region trails in raw semiconductor fabrication capacity, policy initiatives such as the European Chips Act aim to stimulate local analog process development, potentially shortening future supply chains. Converters supporting ISO 26262 automotive compliance and IEC 61000 immunity standards enjoy favored status among Tier-1 suppliers, ensuring sustained share for vendors attuned to European norms. Emerging regions in South America and the Middle East, and Africa record double-digit unit growth from a small base, but infrastructure deficits and currency volatility continue to temper absolute revenue expansion.

Competitive Landscape

The data converter market exhibits moderate concentration, with incumbent suppliers leveraging deep intellectual-property portfolios and long-lived customer relationships to defend share. Analog Devices posted USD 10.39 billion in trailing-12-month revenue, growing 18.6% year-over-year, while Texas Instruments recorded USD 4.15 billion in Q3 2024, reflecting softness in consumer end-markets. Product roadmaps converge on higher channel counts, integrated references, and on-chip calibration engines that widen performance margins without pushing power draw beyond thermal design limits.

Strategic M&A remains a preferred route for capability expansion. Analog Devices’ November 2024 acquisition of Flex Logix injects embedded-FPGA know-how that helps fuse data-converter front ends with programmable AI accelerators, cutting memory latency for edge inference workloads. ON Semiconductor’s purchase of SWIR Vision Systems widens its sensor portfolio and informs converter specifications optimized for short-wave infrared imaging. These moves illustrate an industry pivot toward vertically integrated signal-chain solutions rather than point products.

Technology differentiation now hinges on process-node selection, package configuration, and digital companion IP. Vendors exploiting wafer-level chip-scale packaging can place converters closer to antenna or sensor interfaces, trimming parasitics and elevating effective resolution. Delta-sigma architectures continue to gain traction in precision markets because noise-shaping profiles align with low-frequency measurement demands while relaxing analog anti-alias filter design. Suppliers that own both catalog product lines and application-specific custom-ASIC channels mitigate revenue volatility and preserve gross margins through pricing segmentation.

Data Converter Industry Leaders

Analog Devices, Inc.

Microchip Technology Inc.

STMicroelectronics N.V.

NXP Semiconductors N.V.

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Monolithic Power Systems released the MDC91256 256-channel current-input ADC with selectable 20- or 16-bit resolution for large sensor arrays.

- March 2025: Analog Devices launched the ADAQ4216 µModule data-acquisition system, integrating signal conditioning, ADC, and DSP in a compact footprint.

- March 2025: Texas Instruments expanded its isolated delta-sigma modulator line with the AMC0x36 series for industrial energy metering.

- December 2024: Texas Instruments unveiled the ADS127L21B 24-bit delta-sigma ADC tuned for seismology instrumentation.

Global Data Converter Market Report Scope

A data converter is an electronic circuit that converts analog signals to digital and vice-versa. It is majorly used for end-user applications, such as automotive and telecommunication, which drives the market.

The data converter market is segmented by type (analog to digital converter and digital to analog converter), end user (automotive, telecommunication, consumer electronics, industrial, medical, and other end users), and geography (North America (United States, Canada), Europe (Germany, United Kingdom, France, Italy, and Rest of Europe), Asia Pacific (India, China, Japan, and Rest of Asia-Pacific), and Rest of the World).

The market sizes and forecasts are provided in terms of value in USD million for all the above segments.

| Analog-to-Digital Converters (ADC) |

| Digital-to-Analog Converters (DAC) |

| Mixed-Signal Converters (ADC + DAC) |

| Less than equal to 8-bit |

| 10 - 12-bit |

| 14 - 16-bit |

| Greater than 16-bit |

| High-speed (Greater than 500 MSPS) |

| Mid-speed (50 - 500 MSPS) |

| Low-speed (Less than 50 MSPS) |

| Telecommunications |

| Automotive |

| Industrial Automation and Test |

| Consumer Electronics |

| Medical and Healthcare |

| Aerospace and Defense |

| Other End-user Industries (Energy, Research Labs) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Converter Type | Analog-to-Digital Converters (ADC) | |

| Digital-to-Analog Converters (DAC) | ||

| Mixed-Signal Converters (ADC + DAC) | ||

| By Resolution | Less than equal to 8-bit | |

| 10 - 12-bit | ||

| 14 - 16-bit | ||

| Greater than 16-bit | ||

| By Sampling Rate | High-speed (Greater than 500 MSPS) | |

| Mid-speed (50 - 500 MSPS) | ||

| Low-speed (Less than 50 MSPS) | ||

| By End-User Industry | Telecommunications | |

| Automotive | ||

| Industrial Automation and Test | ||

| Consumer Electronics | ||

| Medical and Healthcare | ||

| Aerospace and Defense | ||

| Other End-user Industries (Energy, Research Labs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the data converter market expected to grow through 2031?

It is projected to expand from USD 6.3 billion in 2026 to USD 8.44 billion by 2031, registering a 6.02% CAGR.

Which resolution tier is growing the quickest?

Converters offering more than 16 bits of resolution are forecast to record an 7.86% CAGR through 2031 as imaging and instrumentation demand higher dynamic range.

What vertical will add the most new converter revenue?

Automotive electronics, boosted by EV battery management and ADAS sensor fusion, is advancing at a 6.92% CAGR and will contribute the largest incremental gains over the forecast period.

Why is Asia-Pacific the leading region?

Deep semiconductor manufacturing capacity, rapid 5G deployments, and strong domestic electronics production give Asia-Pacific 40.12% revenue share with a projected 6.73% CAGR.

How are suppliers mitigating foundry bottlenecks?

Leading vendors lock in multi-year wafer agreements, diversify across multiple specialty fabs, and invest in advanced packaging to maximize die-yield efficiency.

Page last updated on: