Consumer Integrated Circuits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

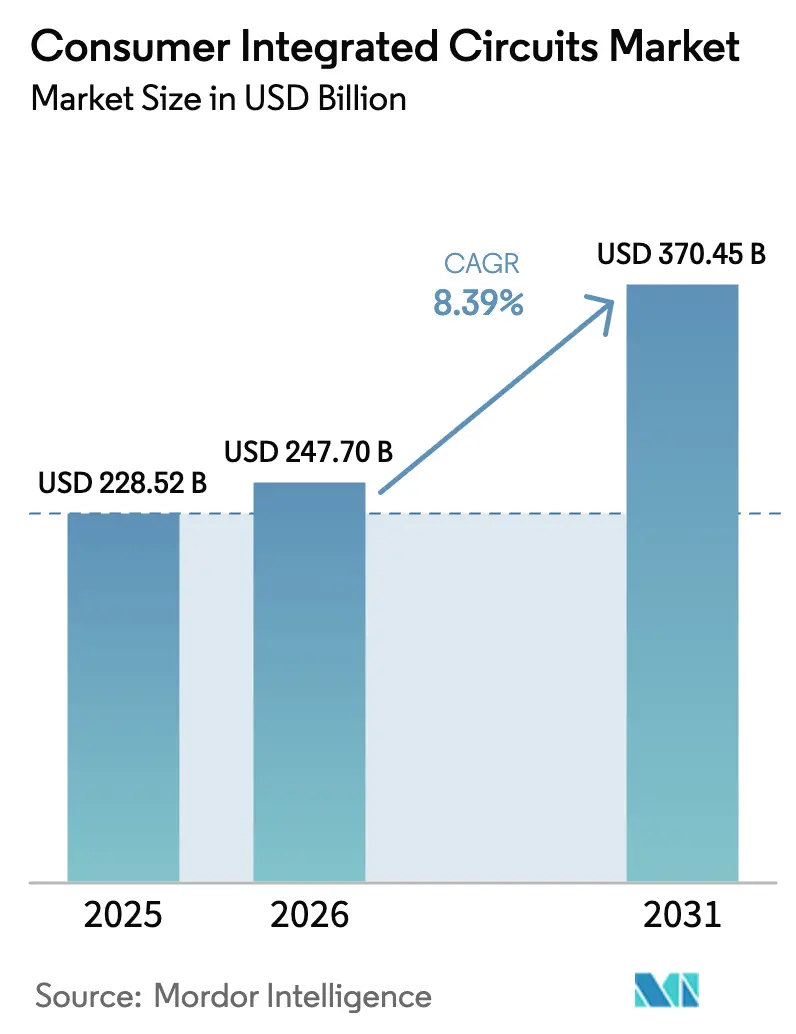

| Market Size (2026) | USD 247.7 Billion |

| Market Size (2031) | USD 370.45 Billion |

| Growth Rate (2026 - 2031) | 8.39% CAGR |

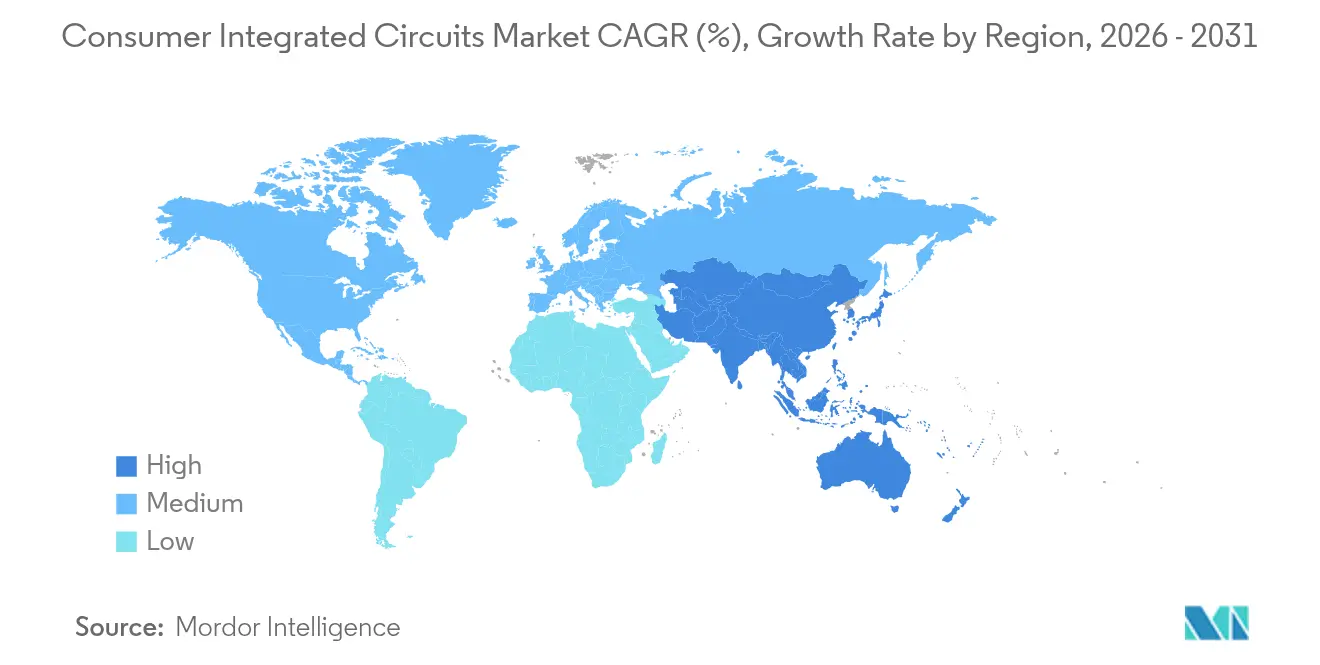

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

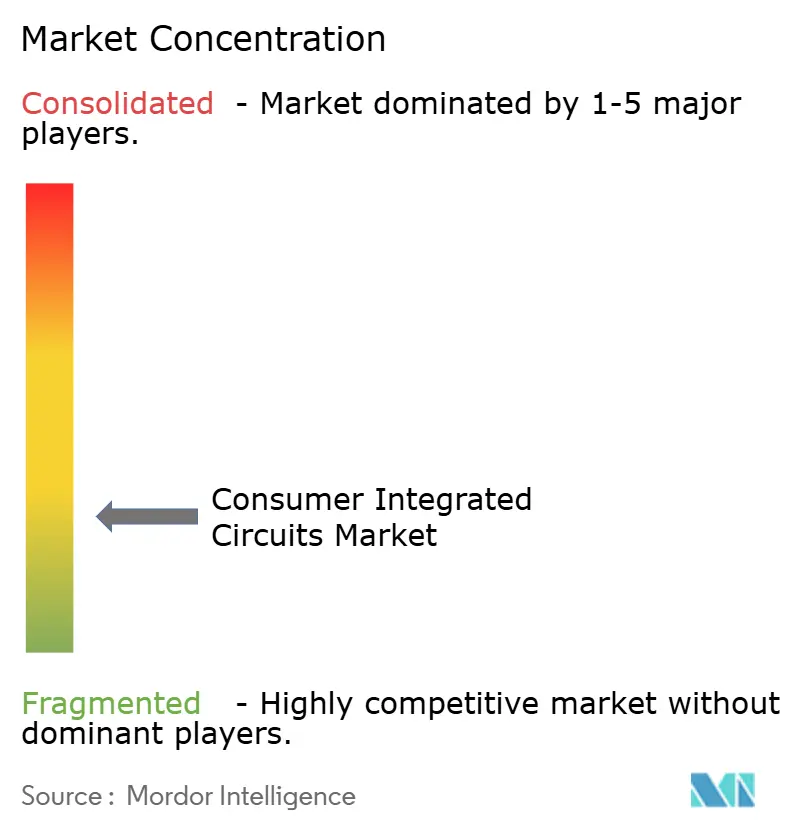

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Integrated Circuits Market Analysis by Mordor Intelligence

The consumer integrated circuit market size was valued at USD 228.52 billion in 2025 and estimated to grow from USD 247.7 billion in 2026 to reach USD 370.45 billion by 2031, at a CAGR of 8.39% during the forecast period (2026-2031). The up-cycle aligns with the semiconductor sector’s rebound as global revenue grew 17% in 2024, propelled by artificial-intelligence chips and memory resurgence.[1]Nasdaq Research Team, “202405 Semiconductor Research – NQSSSE v2,” nasdaq.com Growth benefited from AI-ready consumer devices, rapid migration to advanced manufacturing nodes, and the expanding smart-home ecosystem across mature economies. Asia-Pacific dominated the consumer integrated circuit market with 65.4% value share in 2024 and led expansion at 12.1% CAGR through 2030, a position bolstered by China’s self-sufficiency drive that targets 70% domestic output by 2025. Memory ICs captured the largest product slice at 34.4%, buoyed by high-bandwidth memory (HBM) adoption in AI systems, whereas Logic ICs posted the fastest 11.8% CAGR on the back of accelerating AI-accelerator demand. Smartphones remained the primary revenue engine with 47.6% share, yet wearables and hearables delivered the liveliest growth at 14.2% CAGR, underscoring a pivot toward ultra-low-power AI processing in compact form factors.

Key Report Takeaways

- By IC type, Memory retained 34.02% of the consumer integrated circuit market share in 2025, while Logic is forecast to expand at 11.56% CAGR to 2031.

- By technology node, the 28-45 nm segment led with 28.86% revenue share in 2025; ≤5 nm nodes are expected to rise at an 18.18% CAGR through 2031.

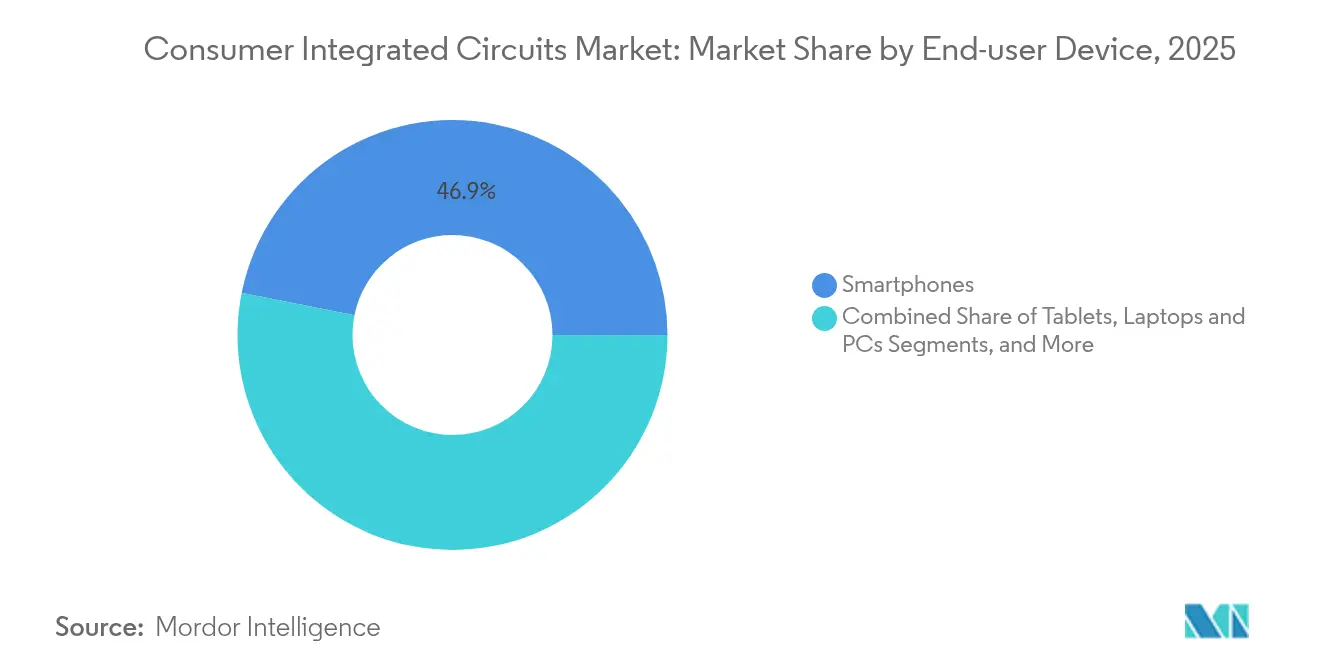

- By end-user device, smartphones accounted for 46.85% of the consumer integrated circuit market size in 2025, whereas wearables and hearables advanced at 13.94% CAGR to 2031.

- By wafer size, 12-inch wafers commanded 70.88% share of the consumer integrated circuit market in 2025; 8-inch capacity registers an 10.86% CAGR through 2031.

- By geography, Asia-Pacific held a 64.85% share in 2025 and also represents the fastest-expanding regional cluster at 11.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Consumer Integrated Circuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-home chipset attach-rate surge across North America and the EU | +1.8% | North America & EU | Medium term (2-4 years) |

| Sub-7 nm mobile SoC demand catalysed by Android flagship launches | +2.1% | Global, with a concentration in APAC | Short term (≤ 2 years) |

| Wearable IC design wins among fab-lite vendors in APAC | +1.2% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Government semiconductor self-sufficiency push in China is elevating local CIC volume | +1.6% | China, with regional supply chain effects | Long term (≥ 4 years) |

| High-bandwidth memory (HBM) adoption in gaming consoles and 8K TVs | +0.9% | Global, led by North America and the EU | Medium term (2-4 years) |

| Rapid OLED TV penetration driving advanced video-processor IC orders | +1.1% | Global, with premium segment focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smart-home Chipset Attach-rate Surge Across North America and EU

Manufacturers dramatically increased the silicon content per device as Wi-Fi, Bluetooth, and Thread converged inside single SoCs that shipped in 2025. Silicon Labs introduced a concurrent-protocol platform enabling simultaneous tri-radio operation, easing interoperability headaches for appliance makers. Qualcomm expanded edge AI capabilities by embedding generative models directly into its QCS8550 smart-home processor, reducing reliance on cloud inference. Matter’s install base is forecast to surpass 5.5 billion compliant devices by 2030, which will multiply demand for certified connectivity chips. As each connected appliance required additional processing and radio front-end circuits, the consumer integrated circuit market realized higher average content per unit.

Sub-7 nm Mobile SoC Demand Catalysed by Android Flagship Launches

Flagship Android vendors adopted 3 nm processors in 2025 to counter Apple’s performance leadership, driving brisk allocations at TSMC’s cutting-edge lines. Qualcomm’s Snapdragon 8 Elite 2 leveraged 3 nm transistors to secure 25% CPU and 30% GPU improvements over the prior generation, a milestone echoed by rival products from MediaTek. Apple’s in-house C1 modem debuted in the iPhone 16e the same year, confirming a broader shift toward vertically integrated chipsets that enlarge logic silicon demand per handset. This technology race enriched the consumer integrated circuit market as leading-edge wafer volume expanded.

Wearable IC Design Wins Among Fab-lite Vendors in APAC

Fab-lite specialists exploited advanced low-power design to capture design wins in hearables and smart rings. Ambiq’s Apollo510 microcontroller delivered 30 × energy efficiency gains while supporting on-device AI inference, lengthening battery life in smartwatches and fitness bands. Partnerships such as Bravechip-Ambiq lowered the bill-of-materials by 30% through chiplets tailored for smart rings, adding momentum to ultra-compact form factors. The proliferating design activity among Asian vendors deepened regional supply networks, further anchoring Asia-Pacific’s leadership within the consumer integrated circuit market.

Government Semiconductor Self-sufficiency Push in China

China accelerated capital deployment through a USD 47.5 billion fund that targeted domestic fabs and equipment suppliers in response to ongoing export controls. Local capacity was projected to climb 14% in 2025, prioritizing consumer electronics nodes where lithography restrictions bite less severely. The policy created a domestic demand pull and secured long-term wafer commitments, enlarging the consumer integrated circuit market base within mainland China and neighboring supply hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Yield deterioration below 5 nm increases per-die cost | -1.4% | Global, concentrated in advanced foundries | Short term (≤ 2 years) |

| Consumer-electronics demand cyclicality post-COVID inventory overhang | -0.8% | Global, particularly North America and the EU | Medium term (2-4 years) |

| Cap-ex inflation for fabless tape-outs at advanced nodes | -1.1% | Global, affecting fabless companies | Medium term (2-4 years) |

| Logistics bottlenecks in OSAT (outsourced assembly and test) capacity | -0.6% | APAC core, with global supply chain effects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Yield Deterioration Below 5 nm Increasing Per-die Cost

Sub-5 nm fabrication confronted acute defectivity. Intel’s 18A line reported yields below 10%, rendering nine of ten dies unusable for volume shipment.[2]Business World Reporters, “Intel’s 18A Node Struggles With Sub-10% Yields,” businessworld.in Samsung’s 2 nm Gate-All-Around technology trailed at 10-20% yield while TSMC kept a 60-70% advantage, widening per-die cost gaps. TSMC announced 5-10% price hikes on 3 nm wafers beginning January 2025 to offset scrap costs, lifting end-device bill-of-materials inside the consumer integrated circuit market.

Consumer-electronics Demand Cyclicality Post-COVID Inventory Overhang

Inventory corrections persisted into 2024 when OLED TV shipments slid 29% year-on-year, a signal of lingering demand softness in premium consumer devices. Component buyers wrestled with divergent trends: labor expenses stayed elevated for contract manufacturers even as material price pressure receded, clouding margin forecasts. Uneven recovery forced IC suppliers to modulate capacity expansion, tempering near-term volumes inside the consumer integrated circuit market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IC Type: Memory Dominance Meets Logic Acceleration

Memory products generated 34.02% of 2025 revenue, anchoring the consumer integrated circuit market thanks to high-bandwidth memory shipments that accelerated AI training throughput. Samsung’s 36 GB HBM3E stacks hit 1.28 TB/s bandwidth, positioning HBM as a premium component for consumer gaming consoles and 8K TVs. Logic ICs advanced at an 11.56% CAGR as AI accelerators proliferated in smartphones, PCs, and edge devices. Analog circuits remained indispensable for power management, while microcontrollers and DSPs met embedded-control needs across household appliances.

HBM capacity is slated to expand its DRAM slice from under 5% in 2023 to beyond 20% mid-decade, shifting revenue mix inside the consumer integrated circuit market. Micron’s HBM3E trimmed power draw by 30% and sliced AI training time by more than 30%, enhancing total cost of ownership for consumer AI workloads. Competitive stakes grew as Samsung, SK Hynix, and Micron contested market leadership with a reported 40%, 30% and 26% share split, respectively, underscoring rising concentration in premium memory segments.

By Technology Node: Advanced Nodes Drive Innovation

The 28-45 nm bracket commanded 28.86% of the 2025 value because it balanced cost and performance for cameras, TVs, and smart-home controllers. Simultaneously, ≤5 nm nodes delivered the highest 18.18% CAGR, propelling the consumer integrated circuit market size for flagship smartphones and AI PCs. TSMC’s Arizona plant began 4 nm mass output for Apple and NVIDIA in January 2025, accelerating the transition to 3 nm and eventually 2 nm processes.

Advanced packaging gained relevance as chiplet architectures offset monolithic scaling limits. The United States committed USD 3 billion to domestic advanced-packaging R&D, validating long-term demand for 3D integration. TSMC’s 3DFabric Memory Alliance partnered with DRAM makers to guarantee compatibility, further expanding the consumer integrated circuit market share for heterogeneous solutions.

By End-user Device: Smartphones Lead, Wearables Surge

Smartphones accounted for 46.85% revenue in 2025, confirming their anchor role in the consumer integrated circuit market. Apple’s A18 Pro, fabricated on second-generation 3 nm, delivered 30% CPU uplift and 40% GPU efficiency, sustaining silicon content growth per handset. Wearables and hearables posted a 13.94% CAGR, propelled by AI-enabled audio and continual health sensing. Tablets, laptops, and PCs preserved relevance for productivity, while TVs embraced sophisticated video-processor ICs to enable 8K playback and real-time upscaling.

Gaming consoles illustrated soaring semiconductor complexity as the PlayStation 5 Pro integrated 18 Gbps GDDR6 and advanced ray tracing, lifting memory and GPU requirements. Qualcomm’s home-appliance platform facilitated local speech-AI functions, advancing smart-device autonomy and reinforcing growth prospects for the consumer integrated circuit market.

By Wafer Size: 12-inch Dominance with 8-inch Growth

Twelve-inch (300 mm) wafers supplied 70.88% of 2025 shipments, validating scale economies vital for the consumer integrated circuit market. Eight-inch fabs saw an 10.86% CAGR through 2031 as automotive, industrial, and IoT sectors sought mature-node economics. SEMI projected global fab capacity to climb 6% in 2024 and 7% in 2025, topping 33.7 million 200 mm-equivalent wafers per month.

Leading-edge capacity (≤5 nm) expanded 13% during 2024, though Chinese producers pivoted to mature lines constrained by lithography restrictions, yet lucrative for consumer ICs. DRAM capacity added 9% in both 2024 and 2025 to satisfy AI memory appetite, whereas 3D NAND recovery remained slow amid oversupplies. The wafer-size landscape underlines capital discipline and strategic balancing of new versus mature process investments across the consumer integrated circuit market.

Geography Analysis

Asia-Pacific captured 64.85% of global revenue in 2025 and is projected to compound at 11.88% annually through 2031. China led regional demand and capacity growth as its self-reliance program injected USD 47.5 billion into domestic fabs, pushing the consumer integrated circuit market size upward despite export-control friction. Taiwan sustained foundry primacy as TSMC’s USD 165 billion Arizona plant came online, underpinning secure supply for global clients. South Korea continued to dominate HBM and NAND output, while Japan leveraged state subsidies worth USD 25.7 billion to revitalize lithography and materials capabilities.

North America benefited from the USD 52.7 billion CHIPS Act, which incentivised new fabs and advanced-packaging hubs, amplifying the domestic share of the consumer integrated circuit market. Europe pursued a 20% global semiconductor share target by 2030 via its EUR 43 billion (USD 50.56 billion) European Chips Act, with Germany and France attracting flagship facilities. South America and the Middle East & Africa remained nascent yet promising as consumer electronics penetration rose and local governments explored incentive schemes to seed assembly and test operations. Regional supply chains showed increasing diversification as customers sought geographic redundancy to mitigate geopolitical risk. Partnerships between Asian fabs and Western OSAT providers illustrated a shift toward dual-source strategies, ensuring resilience in the consumer integrated circuit market. The trend also fostered knowledge transfer and elevated technical standards in emerging hubs.

Competitive Landscape

The consumer integrated circuit market displayed fragmented in 2025. Device and platform vendors pursued vertical integration to protect differentiation and margin. Apple’s in-house C1 modem signified strategic autonomy from external modem suppliers, a move mirrored by Google’s Tensor program and Samsung’s Exynos diversification. Qualcomm broadened its footprint with a USD 2.4 billion deal to acquire Alphawave Semi in September 2025, securing high-performance interconnect IP for data-center AI silicon.

Back-end services remained consolidated: ASE, Amkor, JCET, SPIL, and PTI shared 84% OSAT revenue, enabling scale benefits and bargaining power over materials suppliers.[4]UTAC Group, “Top 10 OSAT Companies,” utmel.com Strategic alliances intensified; Qualcomm partnered with STMicroelectronics to fuse AI-enabled radios with STM32 microcontrollers for IoT applications, underscoring ecosystem collaborations that stretch beyond traditional supplier-buyer relations.

Emerging disruptors stemmed from fab-lite players in China and Taiwan that specialise in ultra-low-power AI and multi-protocol connectivity. These challengers targeted white-space niches such as hearable audio SoCs and AI wearables, adding competitive tension to established brands. Technology differentiation pivoted toward power-efficient AI, advanced packaging, and heterogeneous compute, shaping purchase criteria across the consumer integrated circuit market.

Consumer Integrated Circuits Industry Leaders

Texas Instruments Inc

STMicroelectronics N.V.

Infineon Technologies AG

Intel Corporation

Analog Devices Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Apple released its C1 modem inside iPhone 16e, furthering vertical integration in radio technology.

- January 2025: TSMC commenced 4 nm mass production at its Arizona fab for Apple and NVIDIA, accelerating the shift to 3 nm and 2 nm nodes.

- December 2024: Syntiant completed a USD 150 million purchase of Knowles’ Consumer MEMS Microphones business, bolstering edge-AI audio portfolios.

- September 2024: Qualcomm agreed to acquire Alphawave Semi for USD 2.4 billion to deepen low-power data-center computing capabilities, pending regulatory approval in early 2026.

Global Consumer Integrated Circuits Market Report Scope

An integrated circuit (IC) consolidates various electronic components, like transistors, resistors, and capacitors, onto a single semiconductor chip. This compact device is the cornerstone of contemporary electronic systems, delivering functionality and processing power efficiently. Integrated circuits (ICs) are known for low power consumption and minimal heat generation, enhancing energy efficiency. Moreover, their ability to be mass-produced at a lower cost translates to more affordable electronic devices for consumers.

The study tracks the revenue accrued through the sale of integrated cicruits products by various players globally. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report's scope encompasses market sizing and forecasts for the various market segments.

The consumer integrated circuits market is segmented by type (analog IC, logic IC, memory, and micro [microprocessors (MPU), microcontrollers (MCU), and digital signal processors]), and by geography (United States, Europe, Japan, China, Korea, Taiwan, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Analog IC | |

| Logic IC | |

| Memory IC | |

| Micro IC | Microprocessors (MPU) |

| Microcontrollers (MCU) | |

| Digital Signal Processors (DSP) |

| >45 nm |

| 28 – 45 nm |

| 16 / 14 nm |

| 10 / 7 nm |

| ≤5 nm |

| Smartphones |

| Tablets |

| Laptops and PCs |

| Wearables and Hearables |

| TVs and Set-top Boxes |

| Gaming Consoles |

| Smart Home Appliances |

| ≤ 6-inch |

| 8-inch (200 mm) |

| 12-inch and Above (300 mm +) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| South Korea | ||

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Mexico | ||

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By IC Type | Analog IC | ||

| Logic IC | |||

| Memory IC | |||

| Micro IC | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors (DSP) | |||

| By Technology Node | >45 nm | ||

| 28 – 45 nm | |||

| 16 / 14 nm | |||

| 10 / 7 nm | |||

| ≤5 nm | |||

| By End-user Device | Smartphones | ||

| Tablets | |||

| Laptops and PCs | |||

| Wearables and Hearables | |||

| TVs and Set-top Boxes | |||

| Gaming Consoles | |||

| Smart Home Appliances | |||

| By Wafer Size | ≤ 6-inch | ||

| 8-inch (200 mm) | |||

| 12-inch and Above (300 mm +) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Nordics | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Taiwan | |||

| South Korea | |||

| Japan | |||

| India | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Mexico | |||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the consumer integrated circuit market, and how large will it become by 2031?

The market stood at USD 247.7 billion in 2026 and is projected to reach USD 370.45 billion by 2031, reflecting an 8.39% CAGR.

Which product segment is expanding the fastest?

Logic ICs lead growth with an 11.56% CAGR through 2031, powered by rising demand for AI accelerators in consumer devices.

Which region contributes the most to industry revenue today?

Asia-Pacific held 64.85% of global revenue in 2025 and also posts the strongest 11.88% CAGR through 2031.

What is the single most influential driver of market growth?

Surging shipments of sub-7 nm mobile SoCs for flagship smartphones are adding +2.1% to the overall market CAGR by boosting leading-edge wafer demand.

What key risk could slow near-term expansion?

Yield deterioration below 5 nm remains the largest restraint, trimming 1.4% from forecast CAGR by raising per-die costs at advanced nodes.

Page last updated on: