Cytokinins Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

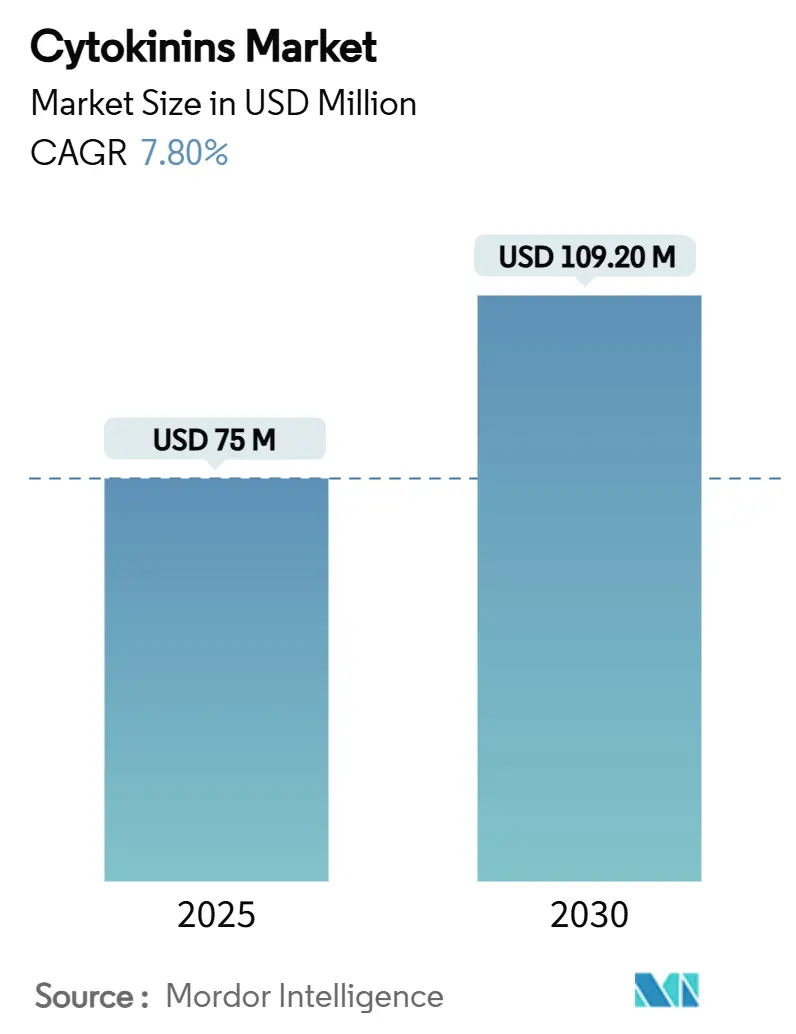

| Market Size (2025) | USD 75 Million |

| Market Size (2030) | USD 109.20 Million |

| Growth Rate (2025 - 2030) | 7.80% CAGR |

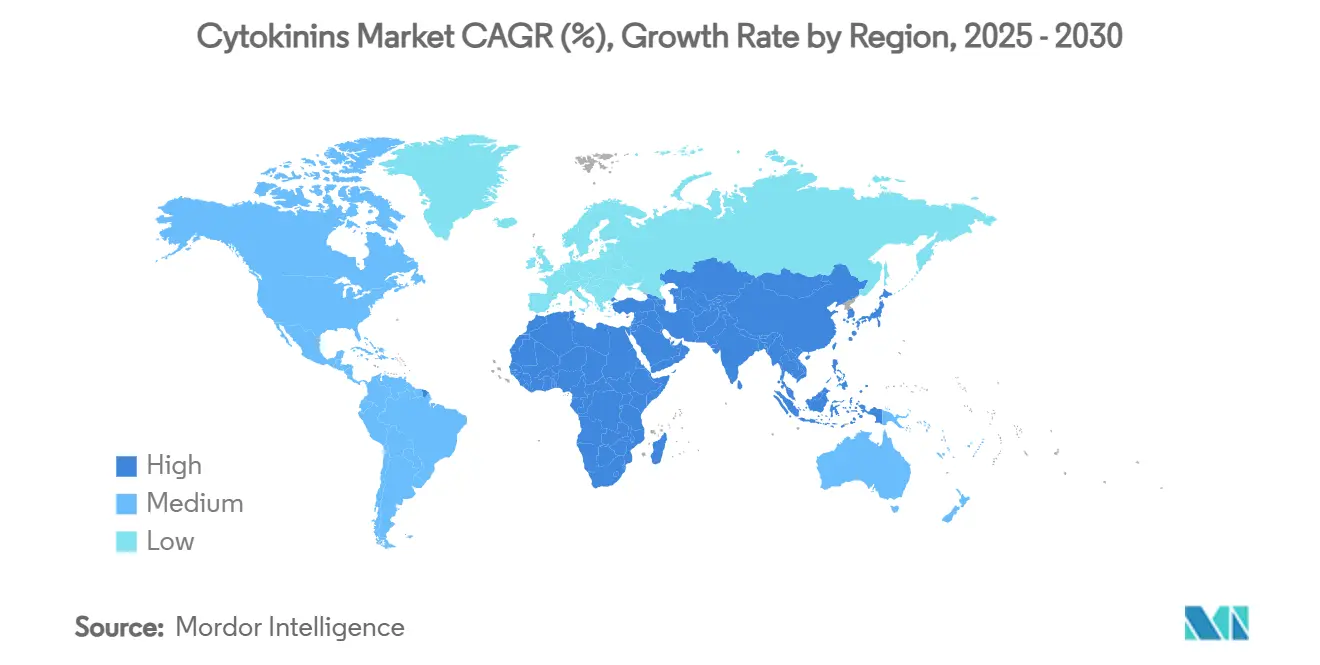

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cytokinins Market Analysis by Mordor Intelligence

The Cytokinins market size is estimated at USD 75.0 million in 2025 and is projected to reach USD 109.2 million by 2030, at a CAGR of 7.8% during the forecast period (2025-2030). Heightened adoption of precision-agriculture hardware, integration of cytokinin-enriched biostimulants into mainstream input programs, and mounting food-security pressures drive this steady trajectory. Synthetic molecules, such as 6-benzylaminopurine and kinetin, maintain demand leadership due to their proven field stability, while data-driven application scheduling safeguards a return on investment across diverse crop systems. Regional momentum varies, producers in North America leverage existing digital farming infrastructure, whereas growers in the Asia-Pacific accelerate the uptake of cytokinin inputs to boost smallholder productivity. Meanwhile, regulatory incentives favoring biological products and ongoing formulation advances broaden agronomic use cases, positioning the cytokinins market for sustained growth into the next decade.

Key Report Takeaways

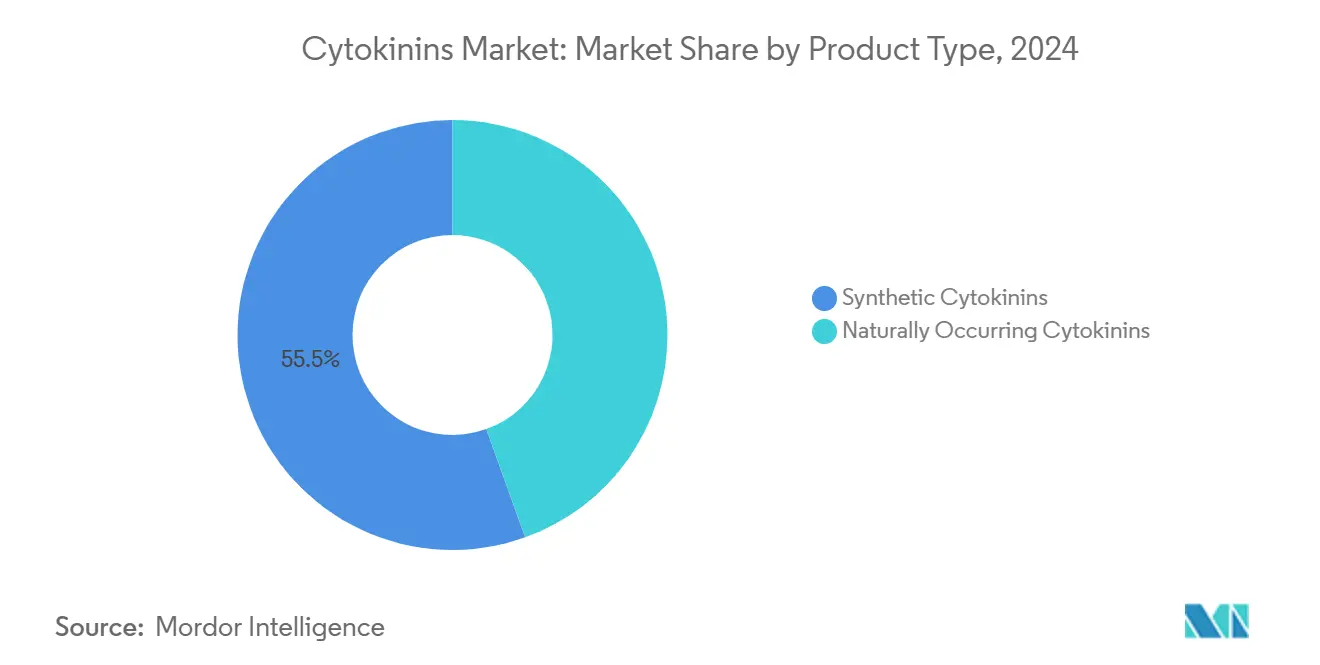

- By product type, synthetic cytokinins held 55.5% revenue share of the cytokinins market in 2024, and the segment is advancing at a 10.1% CAGR through 2030.

- By crop type, fruits and vegetables accounted for 38.4% of the cytokinins market size in 2024, while cereals and grains represent the fastest-growing segment with an 8.7% CAGR to 2030.

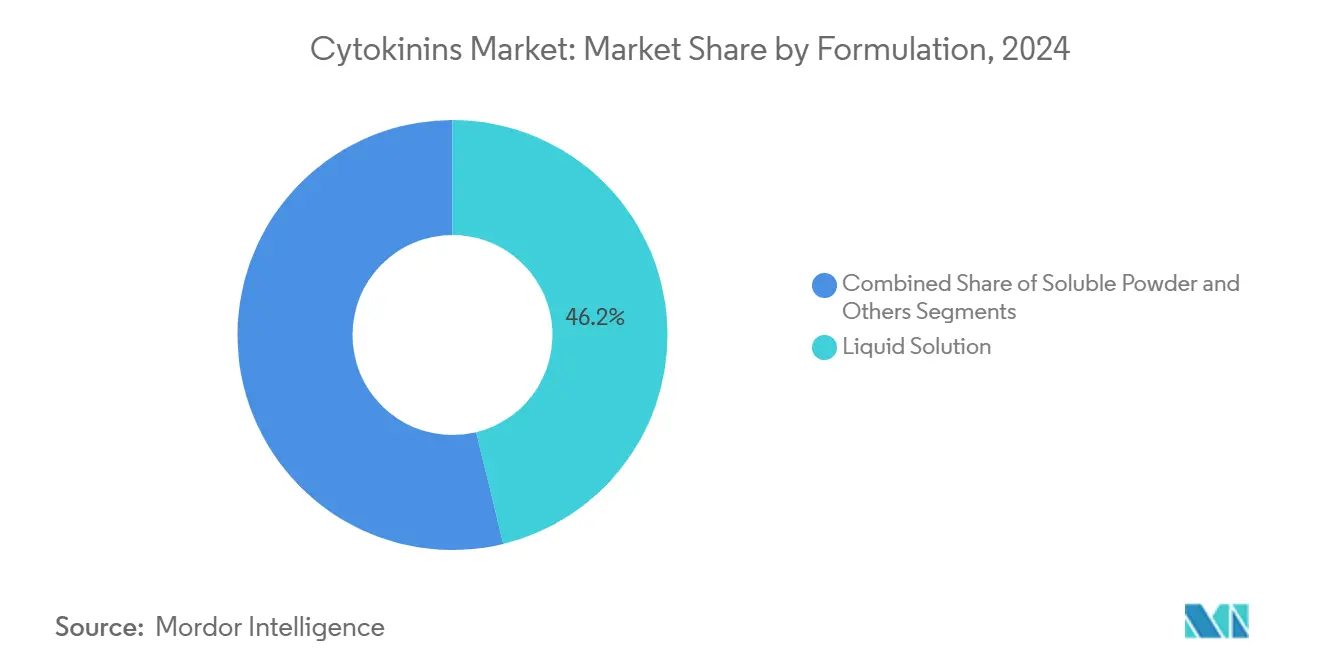

- By formulation, liquid solutions captured 46.2% of the cytokinins market share in 2024 and are projected to grow at a 9.6% CAGR over the forecast window.

- By mode of application, foliar sprays dominated with 49.3% share of the cytokinins market in 2024, while seed treatments are forecast to post a 10.3% CAGR through 2030.

- By geography, North America led with 41.5% revenue share in 2024, whereas Asia-Pacific is slated to register the quickest 9.2% CAGR to 2030.

Global Cytokinins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of plant growth regulators to boost yields | +2.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Surge in high-value horticulture and turf applications | +1.8% | North America and Europe core, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Preference for sustainable and residue-free inputs | +1.5% | Global, particularly strong in European Union and North America | Long term (≥ 4 years) |

| Formulation advances improving cytokinin stability | +1.2% | Global | Medium term (2-4 years) |

| Microbiome-derived cytokinin biostimulants emerging | +0.9% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Precision-ag analytics optimizing dosage windows | +0.7% | North America and Europe core, gradual Asia-Pacific adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Plant Growth Regulators to Boost Yields

Growers worldwide face unprecedented yield-intensification pressures, prompting wider reliance on plant growth regulators that deliver immediate harvest gains. Synthetic cytokinins already represent 35% of the broader plant-regulator segment, indicating their centrality in contemporary productivity strategies. When integrated with variable-rate spraying software, foliar cytokinin programs have raised corn output by 4.2 bushels per acre and soybean output by 1.9 bushels per acre, validating payback across broadacre operations. Adoption trajectories mirror global food-demand forecasts that call for a 70% jump in crop production by 2050, positioning the cytokinins market as a core enabler of yield intensification.

Surge in High-Value Horticulture and Turf Applications

Premium horticultural crops command price multiples that comfortably offset incremental biostimulant spend. EPA tolerance exemptions for 6-benzyladenine in apples and pears simplify residue compliance.[1]Source: Environmental Protection Agency, “6-Benzyladenine; Exemption from the Requirement of a Tolerance,” epa.gov In commercial floriculture, Configure-brand cytokinin sprays stimulate branching and flower count, securing higher auction values for ornamental stock. Turf managers deploy cytokinins to promote lateral shoot growth and rapid recovery on golf courses and stadium pitches, preserving surface aesthetics under intense traffic. These specialty use cases underpin recurring demand and underscore the value-creation potential of targeted cytokinin programs.

Preference for Sustainable and Residue-Free Inputs

The shift toward residue-free food systems spurs interest in biologically derived crop inputs. Cytokinins extracted from seaweed enjoy EPA tolerance exemptions, giving them a regulatory edge over synthetic pesticides. USDA approval of 6-benzyladenine in organic apple production unlocks an audience that previously relied on costly hand thinning.[2]Source: U.S. Department of Agriculture, “Technical Evaluation Report – 6-Benzyladenine,” usda.gov Industry sales data show biological product portfolios at leading crop-input companies rising at double-digit rates, affirming the pull of sustainability credentials in corporate purchasing decisions. Post-COVID agricultural policies favor biologicals, with major companies reporting double-digit growth in biological product sales. Farmers' adoption of environmentally compatible methods and inclusion of biostimulants in carbon-credit programs create favorable conditions for cytokinin products that reduce environmental impact.

Formulation Advances Improving Cytokinin Stability

Legacy cytokinin solutions experienced significant pH-induced degradation, which substantially limited their field effectiveness. Recent chemistry refinements now enable retention of more than 90% active concentration in alkaline tank mixes, effectively safeguarding performance under variable water quality conditions. The introduction of sustained-release polymers extends bioactivity windows, reducing application frequency and labor inputs. These technological improvements explain the strong market preference for liquid solutions, which combine ease of handling with newly secured shelf stability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent residue regulations worldwide | -1.4% | Global, particularly strict in EU and North America | Short term (≤ 2 years) |

| Competition from alternative biostimulants | -0.8% | Global | Medium term (2-4 years) |

| Volatile supply of adenine-based precursors | -0.6% | Global, with concentration in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Limited public Research and Development funding for staple-crop trials | -0.4% | Developing markets in Asia-Pacific and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Residue Regulations Worldwide

The European Food Safety Authority conducts exhaustive toxicological reviews before approving basic substances, extending filing timelines to as long as five years.[3]Source: European Food Safety Authority, “Review of the Basic Substances Chitosan and Chitosan Hydrochloride,” efsa.europa.eu Divergent maximum residue limits between jurisdictions complicate export logistics and raise compliance costs for multinational growers. Historical shipment detentions following minor exceedances underscore the commercial risk attached to inconsistent international standards. Manufacturers with legacy dossiers gain an advantage, while newcomers devote significant capital to residue studies and baseline monitoring to secure registrations.

Competition from Alternative Biostimulants

Humic-substance products outperform cytokinins in certain cereal systems by stimulating endogenous hormone pathways, eroding market share among value-oriented growers. Plant growth-promoting rhizobacteria that naturally release cytokinin analogues offer dual pest-suppression and growth-promotion benefits, lowering reliance on single-mode synthetic sprays. As capital flows into microbial-input start-ups, traditional cytokinin firms must prove superior cost-per-bushel returns to maintain relevance. Robust venture-capital inflows of USD 161 million in H1 2024 alone are accelerating the commercialization of next-generation microbial biostimulants that directly compete for farm-input budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Synthetic Cytokinins Remain the Performance Benchmark

Synthetic products generated 55.5% of the cytokinins market size in 2024 and will compound at 10.1% annually through 2030, reflecting unmatched shelf stability and uniform bioactivity across variable field conditions. Liquid formulations based on 6-benzylaminopurine deliver consistent yield gains in broadacre corn and soy programs, encouraging repeat purchase cycles. Regulatory clarity further supports growth, and many synthetic actives have longstanding tolerances, streamlining global distribution. Naturally occurring cytokinins occupy a niche within certified-organic operations where residue perceptions outweigh higher unit costs. Nonetheless, biologically sourced molecules gain traction where premium crop values offset price differentials, suggesting a diversified product mix rather than a binary market split. Ongoing CRISPR gene-editing initiatives targeting cytokinin oxidase genes in cereals foreshadow future interactions between external sprays and in-plant hormone management, keeping synthetic suppliers engaged with biotechnology partners.

Advances in N9-substituted aromatic compounds mitigate root-growth inhibition historically associated with high foliar doses, widening the agronomic envelope for synthetic offerings. As a result, growers in subtropical zones adopt synthetic programs earlier in the season to counter heat stress, driving incremental volume growth beyond temperate horticulture staples. Over the outlook period, strategic partnerships between active-ingredient manufacturers and precision-ag hardware firms will reinforce synthetic cytokinins’ central role in data-enabled plant-health management, supporting their dominant share of the cytokinins market.

By Crop Type: Specialty Produce Commands Premium Input Economics

Fruits and vegetables delivered 38.4% of overall revenue in 2024, and the segment’s higher value chain margins continue to justify intensive cytokinin regimens. Apple thinning, table-grape cluster management, and greenhouse pepper programs routinely incorporate 6-benzyladenine or forchlorfenuron sprays to synchronize maturation and elevate marketable yields. Cereals and grains, although currently holding a moderate market share, are projected to grow at a CAGR of 8.7% as large-scale producers increasingly adopt hormone interventions to stabilize yields in response to climatic variability. This uptake could eventually lift the cereals portion of the cytokinins market size above 25% by 2030.

Turf and ornamentals rely on cytokinin-driven branching and greening, sustaining demand in the landscaping and sports-turf niche. Oilseed and pulse applications remain nascent but demonstrate strong physiological responses under drought, hinting at diversification of revenue streams for cytokinin suppliers. Across crop categories, integrated pest-management programs bundle cytokinin sprays with fungicides and foliar nutrition, reinforcing stickiness and cross-selling potential for distributors.

By Formulation: Liquid Solutions Dominate Field Adoption Curves

Liquid solutions accounted for 46.2% of the cytokinins market share in 2024, reflecting the convenience of tank-mix compatibility with fertilizers and crop-protection products already used on the farm. Improved buffering agents now keep pH between 6.0 and 7.5 for up to nine months in storage, reducing dealer write-offs linked to seasonal inventory. Field trials in California almond orchards showed that fertigated liquid cytokinins cut application labor by 25% compared with foliar powders while delivering identical nut-set gains, encouraging broader irrigation-system integration. Refillable bag-in-box packaging is gaining traction among large distributors because it minimizes single-use plastics and meets retailer sustainability audits, further supporting the liquid segment’s momentum.

The segment’s outlook strengthens as nozzle technology evolves to create uniform droplet spectra that optimize leaf coverage and minimize drift losses. Drone-enabled ultra-low-volume application systems can deliver liquid cytokinin concentrates at rates down to 5 L/ha, expanding access for smallholder plots in Asia-Pacific where ground rigs are impractical. Regulatory moves in the European Union that mandate closed-transfer systems for certain agrochemicals favor liquids equipped with standardized quick-connect fittings over powders that still require open mixing. Collectively, these operational, environmental, and regulatory advantages underpin the segment’s forecast 9.6% CAGR, reinforcing liquid solutions as the backbone of day-to-day cytokinin programs within the broader cytokinins market.

By Mode of Application: Foliar Spray Retains Practical Primacy

Foliar treatments commanded 49.3% of 2024 revenues because producers can apply cytokinin solutions with the same ground or aerial rigs already used for fungicides and micronutrients. Variable-rate mapping modules tied to in-cab controllers adjust droplet output to canopy density, ensuring cost-efficient coverage across irregular field zones. Electrostatic nozzles, now common in North American vineyards, heighten leaf adhesion and cut active-ingredient losses, reinforcing foliar spray leadership within the cytokinins market. Because foliar programs bypass soil sorption and microbial breakdown, they deliver faster plant uptake an advantage that resonates with specialty-crop growers facing tight harvest schedules.

Seed treatment is the fastest-growing mode at a 10.3% CAGR through 2030, as coat-and-plant platforms deliver early-season vigor without extra field passes. Smart pelleting carriers release cytokinins in sync with radicle emergence, increasing stand uniformity under variable moisture conditions. This low-volume, closed-system approach aligns with tightening European operator-safety regulations and appeals to regenerative no-till adopters seeking to minimize soil disturbance. Together with precision foliar systems that can cut chemical volume by up to 90% through spot-spraying technology, the rapid rise of seed treatments illustrates how complementary delivery methods collectively expand the cytokinins market.

Geography Analysis

North America commanded 41.5% of global revenue in 2024, underpinned by precision-farming penetration levels topping 70% in row-crop areas, robust distributor networks, and regulatory regimes that expedite product label extensions. Advanced analytics platforms correlate vegetative-index data with cytokinin timing, amplifying yield gains and cementing brand loyalty among producers. The United States biostimulant sector demonstrates significant market potential, reflecting the region's growing acceptance and integration of biological inputs into conventional fertility programs.

Europe contributes a stable, mid-single-digit revenue slice, buoyed by Common Agricultural Policy incentives that reward sustainable input choices, stringent residue limits necessitate extensive dossier support, favoring multinationals with established compliance teams. Post-Brexit United Kingdom rules mirror EU maximum residue levels, preserving a harmonized market landscape for marquee cytokinin brands.

Asia-Pacific, with a forecast 9.2% CAGR through 2030, witnesses rapid adoption among fruit exporters in China, vineyard expansions in Australia, and greenhouse hubs across Japan and South Korea. Smallholder rice producers experiment with cytokinin seed priming to overcome panicle sterility in heat-stressed paddies, signalling future volume upside. South American growers deploy foliar cytokinin programs in soybean and cotton to synchronize maturity across expansive farm units, and Brazil’s continued agricultural frontier expansion underpins robust demand growth. The Middle East and Africa remain emerging frontiers. Horticultural clusters in Morocco and Kenya adopt hormone sprays to align produce quality with export standards, though infrastructural gaps currently restrict deeper penetration of the cytokinins market.

Competitive Landscape

The cytokinins market exhibits moderate concentration, with the top five companies controlling nearly 60% of revenue, granting them scale advantages in procurement, regulatory submissions, and cross-regional logistics. Global agrochemical majors Bayer, Syngenta Group, Corteva, BASF, and UPL bundle cytokinin actives with fungicide and insecticide offerings, simplifying procurement for growers. Mid-tier specialists such as Valent BioSciences and OMEX Agriculture focus on bespoke formulations tailored to high-value horticulture, leveraging agility to capture niche share.

Product strategy increasingly prioritizes biological portfolios, leading firms to report double-digit biological growth as end-users pivot toward sustainability credentials. BASF’s upcoming launch of six new actives in Brazil underscores ongoing pipeline investment targeted at expanding South American footprint. Simultaneously, merger and acquisition activities are consolidating expertise as Corteva's acquisition of Symborg has enhanced microbial capabilities, while the integration of Stoller is driving diversification within the hormonal portfolio.

Technology partnerships represent a concurrent focus. Equipment makers embed crop-model algorithms into sprayers to deliver site-specific cytokinin dosing, channeling proprietary usage data back to input suppliers. Firms able to quantify per-acre profit uplift secure premium pricing and deepen advisory relationships. Meanwhile, disruptors in the microbiome arena court venture capital to commercialize in situ cytokinin production strains, posing a long-run substitution threat to conventional formulations yet also opening co-development pathways for established players.

Cytokinins Industry Leaders

BASF SE

Corteva Agriscience

Valent BioSciences LLC (Sumitomo Chemical Co., Ltd.)

Bayer AG

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Syngenta opened a 22,000 m² biologicals production facility in Orangeburg, South Carolina. The facility can produce 16,000 metric tons of biostimulants annually, including cytokinin-based products that improve crop growth and stress tolerance. This facility adds to Syngenta's existing production network in Brazil, Italy, India, and Norway, expanding its capabilities in sustainable agriculture solutions.

- April 2025: BASF India acquired a 100% stake in BASF Agricultural Solutions India, integrating its crop protection and biologicals operations. This acquisition expanded BASF's plant growth regulator portfolio, which includes cytokinins that improve crop productivity and resilience.

- February 2024: Corteva Agriscience marked the first anniversary of its Symborg and Stoller acquisitions by establishing Corteva Biologicals, which focuses on sustainable crop solutions. The company's product portfolio includes X-Cyte, a cytokinin-based solution that promotes cell division, shoot growth, and stress tolerance in major crops.

- January 2023: Sumitomo Chemical acquired a United States based biostimulant company to expand its Biorationals business and strengthen its global presence in sustainable agriculture. The acquisition enhanced Sumitomo's cytokinin-based portfolio through Valent BioSciences, which includes products like Promalin and ProTone for fruit development and shoot growth.

Global Cytokinins Market Report Scope

| Naturally Occurring Cytokinins | Zeatin |

| Isopentenyladenine | |

| Synthetic Cytokinins | 6-Benzylaminopurine (6-BA) |

| Kinetin | |

| Thidiazuron |

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Turf and Ornamentals |

| Others |

| Soluble Powder |

| Liquid Solution |

| Others |

| Foliar Spray |

| Soil Treatment |

| Seed Treatment |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Naturally Occurring Cytokinins | Zeatin |

| Isopentenyladenine | ||

| Synthetic Cytokinins | 6-Benzylaminopurine (6-BA) | |

| Kinetin | ||

| Thidiazuron | ||

| By Crop Type | Cereals and Grains | |

| Fruits and Vegetables | ||

| Oilseeds and Pulses | ||

| Turf and Ornamentals | ||

| Others | ||

| By Formulation | Soluble Powder | |

| Liquid Solution | ||

| Others | ||

| By Mode of Application | Foliar Spray | |

| Soil Treatment | ||

| Seed Treatment | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the cytokinins market and forecast market size?

The cytokinins market size reached USD 75.0 million in 2025 and is projected to grow to USD 109.2 million by 2030.

Which product type dominates the cytokinins market?

Synthetic cytokinins held 55.5% market share in 2024 and lead growth with a forecast 10.1% CAGR through 2030.

Why are fruits and vegetables major users of cytokinins?

High-value horticultural crops justify premium input costs, while cytokinin treatments improve fruit set, cluster management, and overall quality, supporting a 38.4% revenue share in 2024.

Which region is expanding fastest in cytokinin adoption?

Asia-Pacific exhibits the highest regional CAGR at 9.2% to 2030, driven by rapid farm modernization and yield-optimization initiatives.

How are formulation advances shaping market preferences?

Improved liquid-solution stability and emerging sustained-release technologies enhance application convenience, steering 46.2% of 2024 revenue toward liquid products.

What is the main regulatory challenge for cytokinin suppliers?

Stringent residue limits, especially in the European Union and North America, extend approval timelines and elevate compliance costs for new formulations.

Page last updated on: