Bionematicides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 473 Million |

| Market Size (2031) | USD 705 Million |

| Growth Rate (2026 - 2031) | 8.30% CAGR |

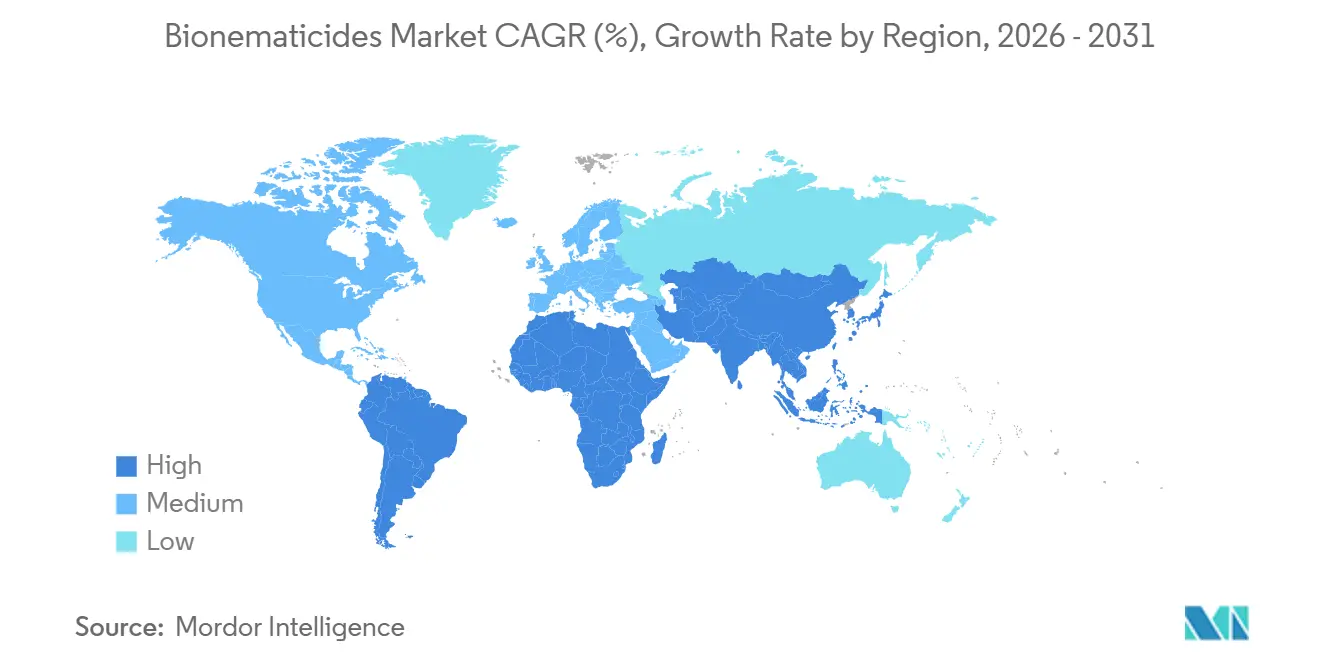

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bionematicides Market Analysis by Mordor Intelligence

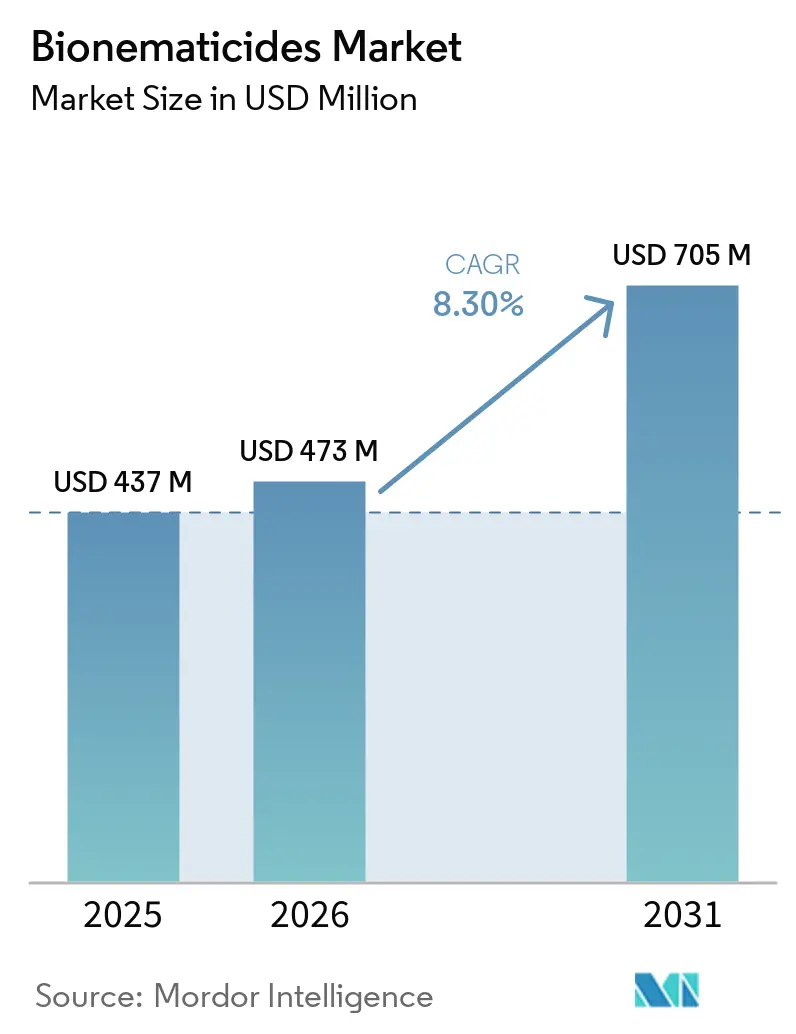

The bionematicides market size is valued at USD 437 million in 2025 and is anticipated to grow from USD 473 million in 2026 to USD 705 million by 2031, growing at a CAGR of 8.3% over 2026-2031. Rising organic-certified acreage, stricter curbs on highly toxic soil fumigants, and bundling of biological actives into commercial seed stacks are expanding demand of bionematicides in both row-crop and horticultural systems. Microbial products continue to dominate revenue, but biochemical and RNA-interference (RNAi) innovations are gaining traction as crop protection companies pursue multi-mode and species-specific suppression strategies. Shelf-stable dry formulations are unlocking warm-climate markets that lack cold-chain infrastructure, while soil-microbiome diagnostics and precision application tools are lifting field-level efficacy. Competitive intensity is moderate, yet venture-backed RNAi specialists and microbiome analytics start-ups are fragmenting the landscape, forcing incumbents to defend share through mergers, patents, and bundled product offerings.

Key Report Takeaways

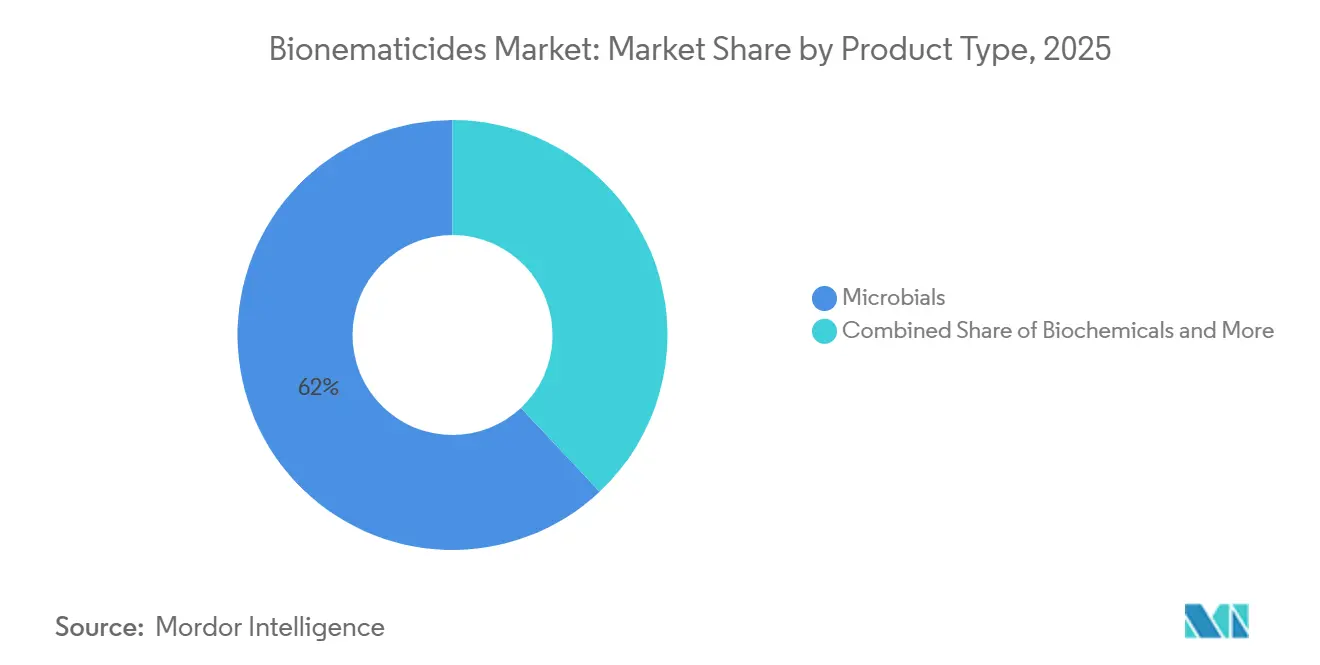

- By product type, microbials led with the largest share, accounting for 62% of the bionematicides market share in 2025, while biochemicals are forecast to expand at the fastest 9.4% CAGR through 2026-2031.

- By mode of application, soil treatment led with the largest share, accounting for 48% of the bionematicides market share in 2025, whereas seed treatment is projected to record the fastest 10.1% CAGR through 2026-2031.

- By crop, fruits and vegetables led with the largest share, accounting for 35% of the bionematicides market share in 2025, oilseeds and pulses are advancing at the fastest 11.5% CAGR through 2026-2031.

- By formulation, liquid suspensions led with the largest share, accounting for 55% of the bionematicides market share in 2025, yet dry granules and wettable powders are growing at the fastest 11.3% CAGR through 2026-2031.

- By infestation type, root-knot nematodes led with the largest share, accounting for 40% of the bionematicides market share in 2025, and cyst nematode segments are growing at the fastest 11.0% CAGR through 2026-2031.

- By geography, North America held the largest share, accounting for 40% of bionematicides market size in 2025, while Asia Pacific is projected to register the fastest 8.5% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bionematicides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in certified-organic farmland | +1.8% | North America, Europe, emerging South America, and the Asia-Pacific | Medium term (2-4 years) |

| Global phase-out of highly toxic chemical nematicides | +2.1% | Europe and North America leading, Asia-Pacific and South America following | Long term (≥4 years) |

| Lower research and registration cost for biologicals | +1.2% | North America and Europe, spillover to developing regions | Short term (≤2 years) |

| RNA-interference nematicides enabling species-specific control | +0.9% | Early adoption in North America and Europe | Long term (≥4 years) |

| Bundling of bionematicides in seed-treatment stacks | +1.5% | North America and South America are expanding worldwide | Medium term (2-4 years) |

| Soil-microbiome diagnostics optimizing application timing | +0.8% | Precision-ag hubs in North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growth in Certified-Organic Farmland

Global certified organic farmland grew from 96 million hectares in 2022 to nearly 99 million hectares in 2024, reflecting steady but slowing growth in organic agriculture, as per FiBL & IFOAM Organics International (2026). Organic standards prohibit synthetic fumigants, prompting growers to adopt biological nematode control. In California’s organic vegetable sector, Bacillus firmus and Purpureocillium lilacinum products are standard practice for root-knot suppression. Similar momentum is evident in the European Union, where in 2024, organically farmed land in the European Union reached 18.1 million hectares, accounting for 11.1% of total agricultural land[1]Source: European Commission, “Organic Farming,” ec.europa.eu. Organic area expansion has moderated but remains significant. Premium export pricing for residue-free produce is stimulating uptake in Brazil’s coffee and India’s spice belts.

Global Phase-Out of Highly Toxic Chemical Nematicides

Regulators are steadily withdrawing organophosphate and carbamate nematicides. While the EPA did not cancel nematicide active ingredients in 2026, registration reviews, product withdrawals, and rising compliance costs under FIFRA are gradually limiting the U.S. soil-applied nematicide portfolio[2]Source: United States Environmental Protection Agency, “Pesticides,” epa.gov . The European Commission maintains strict hazard-based cutoffs that deter re-registration of older fumigants. In 2024 and 2025, China progressed in phasing out high-toxicity pesticides, banning omethoate, carbofuran, methomyl, and aldicarb, effective by December 2025. Planned 2026 bans on phorate and isofenphos-methyl are driving a shift toward microbial nematicides and biopesticides. To support this, MARA approved five new biopesticides in late 2025, promoting green agricultural development. These concurrent moves underpin lasting substitution toward biological alternatives.

Lower Research and Registration Cost for Biologicals

Biological active ingredients skip costly mammalian toxicology and environmental fate studies required for new chemical entities. EPA’s biopesticide pathway typically costs USD 2-4 million, compared with USD 200-300 million for synthetic actives, allowing smaller innovators to commercialize more quickly. BASF SE, which invested EUR 919 million (USD 980 million) in agricultural research in 2024, is allocating a greater share to biologicals due to faster payback. FMC Corporation launched 40 biological products across 24 nations over five years by exploiting these streamlined approvals. The compressed cycle is widening product diversity and accelerating geographic rollout.

RNA-Interference Nematicides Enabling Species-Specific Control

Double-stranded RNA (dsRNA) technologies silence essential nematode genes without harming non-targets. Advancements in nematicides have focused on new chemical classes like cyclobutrifluram, a systemic non-fumigant nematicide approved by the U.S. EPA in late 2025 for soil and seed-applied nematode control. This sets a regulatory and technical benchmark for future RNAi solutions, including applications for fungi and mites. Greenhouse trials reported 89% mortality of Meloidogyne incognita using nano-enabled RNAi, outperforming current microbials. Syngenta’s TYMIRIUM technology is a synthetic nematicide and fungicide with cyclobutrifluram as its active ingredient. It disrupts mitochondrial respiration in nematodes and fungal pathogens like Fusarium, ensuring soil stability and prolonged root protection without RNA interference (RNAi) or microbial encapsulation. High production costs and cautious regulators confine market presence today, but falling synthesis prices after 2027 will unlock broader adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited shelf life and formulation stability | -1.4% | Warm-climate Asia-Pacific, the Middle East, and Africa | Medium term (2-4 years) |

| Farmer skepticism over field-level efficacy | -1.1% | Smallholder regions in Asia-Pacific, Africa, and South America | Short term (≤2 years) |

| Patent thickets around key microbial strains | -0.7% | North America and Europe | Long term (≥4 years) |

| Lack of harmonized import-tolerance standards | -0.6% | Global export trade corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Shelf Life and Formulation Stability

Many live microbial products require refrigeration below 10 °C and expire within 12 months, complicating distribution in tropical regions. Dry granules extend viability yet often sacrifice rapid field efficacy. Nano-encapsulation research has extended the viability of entomopathogenic nematodes to 18 months at ambient temperature, but commercial deployment remains limited. Manufacturers face higher spoilage rates in the Asia-Pacific and Africa, where cold storage is scarce. Stability breakthroughs are essential to unlock mass-market penetration.

Farmer Skepticism Over Field-Level Efficacy

Smallholder trials in India reported 45-68% root-knot reduction with Trichoderma products, compared with 82-89% with chemical standards, prompting growers to return to fumigants. Repeat-purchase rates for biologicals remain lower than for synthetics, reflecting perceived inconsistency. Demonstration plots in Brazil and Argentina benchmark biological and chemical options, but extension resources cover less than 15% of the target acreage. Companies are pairing biologicals with plant-growth metabolites to boost visible yield responses and strengthen loyalty. Consistent agronomy support is critical to close the trust gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Microbials Retain Dominance, Biochemicals Accelerate

Microbials accounted for the largest share, representing 62% of the 2025 bionematicides market, as Bacillus, Trichoderma, and Purpureocillium strains deliver broad soil colonization and rhizosphere activity. Biochemicals, including azadirachtin and terpenoids, are growing at a fastest 9.4% CAGR through 2026-2031, driven by resistance management goals and shelf-life advantages. Combined microbial-biochemical products are gaining share in premium fruit and vegetable markets where growers accept higher unit costs for season-long control. RNAi platforms such as TYMIRIUM are in early commercial phases, yet declining synthesis expenses should unlock meaningful uptake after 2027. The bionematicides market size for integrated microbial-biochemical products is projected to expand at double-digit rates through the forecast horizon.

Second-generation microbials emphasize metabolite co-production, as illustrated by BASF SE’s forthcoming Votivo Prime that couples Bacillus firmus with proprietary metabolites for lesion-nematode suppression. Field trials demonstrated a significant share of egg-hatch inhibition using nano-formulated terpenoids, surpassing fluopyram’s. Biochemicals also improve compatibility with drip irrigation systems, where particulate settling hinders the suspension of live cells. RNAi’s precision aligns with residue-sensitive export channels because gene silencing compounds degrade into benign nucleotides. Collectively, innovation is steering the bionematicides market toward multi-mode, shelf-stable, and species-specific portfolios.

By Mode of Application: Seed Treatment Expands Through Bundling

Soil treatments accounted for the largest share, with 48% of the 2025 bionematicides market size, driven by broadcast and banded applications in heavily infested row crops. Seed treatment is advancing at a fastest 10.1% CAGR through 2026-2031, as multinationals embed biologicals into proprietary coatings that deliver nematode, fungal, and insect protection in one pass. Corteva Agriscience LLC’s Lumialza and UPL’s NIMAXXA exemplify this bundling strategy that shifts application responsibility to seed providers. Foliar sprays remain niche for ornamentals and protected horticulture, whereas drip-irrigation injection appeals to greenhouse and high-tunnel vegetable producers. The bionematicides market for seed-treatment products is forecast to overtake soil-treatment products by 2030 as adoption accelerates in soybean, corn, and cotton systems.

Seed coating reduces dosage variability and enhances early-root colonization, boosting field consistency and farmer confidence. In no-till systems, seed treatments avoid soil-incorporation constraints and align with conservation farming practices. Drip injection of biological nematicides in California and Spain is more effective than broadcast sprays because it targets the rhizosphere. Drip systems provide a moist environment supporting strains like Purpureocillium lilacinum, achieving nematode reduction rates of 56% to 77% in field trials. Equipment compatibility and labor savings further incentivize the shift toward on-seed delivery. As proprietary stacks proliferate, independent formulators may face restricted market access unless they partner with major seed companies.

By Crop: Oilseeds and Pulses Present Fastest Growth

Fruits and vegetables accounted for the largest share, at 35%, of the bionematicide market size, because low nematode damage thresholds justify the use of premium biological inputs in tomatoes, peppers, and strawberries. Oilseeds and pulses are projected to expand at a fastest 11.5% CAGR through 2026-2031 as global demand for plant protein drives acreage increases in Brazil, India, and Canada. Cereals and grains accounted for a significant share of 2025 demand, driven by soybean cyst and cereal cyst nematode pressure. Turf and ornamentals remain a small but steady niche focused on golf courses and nurseries. Biological tools offer residue-free protection that aligns with stringent export limits for fresh produce, sustaining growth in high-value horticulture[3]Source: United States Department of Agriculture Economic Research Service, “Organic Production,” ers.usda.gov.

Brazilian soybean growers are estimated to grow around 45 million hectares in 2024, increasing hectares under biological nematode control to around 50% of total land used to meet European Union residue standards. India’s pulse acreage reached 29.5 million hectares in 2024, intensifying root-knot challenges and spurring demand for rotation-friendly microbials. Host-resistance erosion in soybean cyst nematode is shifting attention back to biological egg parasitism using Pasteuria and Bacillus strains. Fruits and vegetables command the highest per-hectare spend because of short pre-harvest intervals that preclude the use of chemical fumigants. Turf applications leverage Bacillus firmus to prevent phytotoxicity in ornamental landscapes.

By Formulation: Dry Granules Win Warm-Climate Markets

Liquid suspensions accounted for the largest share with 55% of the 2025 bionematicides market size, formulation revenue, prized for their ready-to-use convenience and compatibility with standard spray equipment. Dry granules and wettable powders are growing at the fastest 11.3% CAGR through 2026-2031, offering 18-24 month shelf life without refrigeration and addressing distribution hurdles in tropical regions. Shelf-stable powders such as Avodigen significantly reduce logistics costs compared to chilled liquids. Wettable powders offer rapid reconstitution and precision dosing but require extra mixing steps that some growers resist. The bionematicides market share for dry and powder formulations is climbing fastest in Asia-Pacific and Africa, where ambient temperatures exceed 30 °C for extended periods.

Encapsulation with xanthan gum and surfactants preserved 82% entomopathogenic nematode viability after 18 months, compared with 34% for conventional aqueous media. Manufacturers are also exploring water-dispersible granules that dissolve immediately in the spray tank, combining ease of handling with ambient stability. Liquid suspensions maintain an edge in precision-ag systems using variable-rate injectors that favor homogeneous fluids. Nevertheless, as cold-chain costs rise, warm-climate distributors increasingly favor powder and granule SKUs that minimize spoilage and warranty claims.

By Infestation Type: Cyst Nematodes Post Strongest Upside

Root-knot nematodes held a large 40% share of the 2025 bionematicides market size, due to their broad host range across vegetables and row crops. Cyst nematodes are projected to grow at a fastest 11.0% CAGR through 2026-2031, as soybean cyst populations overcome single-gene host resistance. Lesion nematodes pose emerging challenges in potatoes and carrots, while stubby-root and reniform species remain localized concerns. Biologicals that parasitize cyst eggs, such as Pasteuria nishizawae, achieved significant success in reductions in egg density in Midwest field trials, surpassing many chemical standards. The bionematicides industry is channeling more research funding into cyst-targeted microbes and RNAi constructs as genetic resistance erodes in key cultivars.

BASF SE’s pending Nemasphere trait complements biological rotations by retarding egg development inside soybean roots, enhancing overall suppression when stacked with external microbial products. Root-knot control remains a volume driver, especially in greenhouse vegetables, where enclosed conditions amplify population buildup. Lesion nematode management relies heavily on Trichoderma strains, but inconsistent colonization in deep soil layers limits performance, creating scope for advanced delivery systems. Diversifying infestation-type portfolios will be vital for suppliers seeking balanced revenue streams.

Geography Analysis

North America generated roughly 40% of 2025 global revenue, led by the United States, where expedited Environmental Protection Agency biopesticide reviews and large organic vegetable operations underpin adoption. In California, 12,000-15,000 hectares of organic tomatoes and 10,000 hectares of organic lettuce are grown. Purpureocillium lilacinum is widely used to control root-knot nematodes (Meloidogyne spp.) as part of an Integrated Pest Management (IPM) strategy with resistant varieties and crop rotation. Canada is scaling biologicals in potatoes and greenhouse vegetables under sustainable-agriculture grants, while Mexico’s protected-agriculture clusters are trialing drip-injected microbials for peppers and cucumbers. The bionematicides market in the region benefits from harmonized residue standards under the United States-Mexico-Canada Agreement, which lowers cross-border registration friction. However, farmer skepticism persists in some Midwestern row-crop systems where chemical fumigants remain legal and inexpensive.

Asia-Pacific is on track for an 8.5% CAGR as China and India expand subsidies for bio-inputs to satisfy export buyers’ residue limits. China placed five chemical nematicides on restricted schedules in 2025, nudging growers toward Bacillus-based options with lighter data packages. India promotes biological pest management through the National Mission on Natural Farming (NMNF), launched in November 2024 with an outlay of INR 24.81 billion (USD 295 million) for 2025-26. The mission targets 1 crore farmers and 10,000 Bio-input Resource Centers for localized, low-cost biological inputs. Japan’s organic vegetable acreage is rising rapidly each year in Hokkaido and Kyushu, driving demand for biologicals including bionematicides that meet Japanese Agricultural Standards. Australia is piloting Pasteuria and Trichoderma solutions for sugarcane and potatoes, but performance is inconsistent under drought conditions.

South America has recorded a rapid growth as Brazilian soybean and sugarcane growers integrate biological nematode management into no-till systems. Biological adoption covered a significant share of Brazil’s 45-million-hectare soybean area in 2025, driven by European Union import tolerances. Argentina’s wheat and corn producers leverage existing seed-treatment infrastructure to test Bacillus seed coatings, aiming to reduce in-furrow input costs. The European Union is projected to post a rapid CAGR under the Farm-to-Fork pesticide-reduction agenda. Germany, France, and Spain are front-runners in the use of vegetables and fruits. The Middle East and Africa are seeing significant growth in greenhouse vegetable and export horticulture, where residue-compliant pest control is in demand, though high prices and weak cold chains are tempering broader uptake.

Competitive Landscape

The top five suppliers, including BASF SE, Bayer AG, Syngenta Crop Protection AG, Corteva Agriscience LLC, and FMC Corporation, captured the majority share of 2025 revenue, indicating moderate concentration as emerging RNAi firms and diagnostic start-ups gain footholds. BASF SE’s March 2026 acquisition of AgBiTech broadens its biologicals platform beyond nematicides into virus-based insect control, signaling multinationals’ intent to offer multi-pest portfolios. Syngenta Crop Protection AG’s TYMIRIUM patents on dsRNA delivery require competitors to license the technology or pursue alternative delivery methods, thereby raising barriers to entry for smaller competitors. Corteva Agriscience LLC and FMC Corporation defend share through bundled seed-treatment stacks, tying biological actives to proprietary germplasm and distribution channels. Venture-funded firms such as GreenLight Biosciences target niche, species-specific segments but face scale-up and regulatory approval hurdles.

Innovation centers on extending shelf life, lowering dsRNA costs, and integrating microbiome analytics. Nano-encapsulation, metabolite co-formulation, and precision application software are core investment themes. Strategic alliances between crop-protection majors and biotech specialists accelerate pipeline filling. For instance, FMC Corporation’s 2024 Canadian deal with Novonesis grants exclusive distribution of microbial tools across FMC Corporation’s network. Patent thickets serve as defensive barriers, with Bacillus and Pasteuria patents extending beyond 2029 to maintain price premiums. Regional biological formulators leverage locally endemic strains with fewer global IP constraints.

Competitive pressures intensify as biologicals transition from niche organic input to mainstream integrated pest management. Farmers seek solutions that address multiple soil pathogens simultaneously, spurring suppliers to develop consortia products or cross-sell fungi and insect biologicals. Start-ups offering soil-microbiome diagnostics aim to bundle service contracts with product sales, capturing recurring revenue and embedding agronomic influence. Market entrants that deliver reliable efficacy, ambient stability, and seamless integration with existing agronomy programs will erode incumbent share over the next five years.

Bionematicides Industry Leaders

BASF SE

Bayer AG

Syngenta

Corteva Agriscience

FMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BASF SE launched Votivo Prime, pairing Bacillus firmus with proprietary metabolites for seed-treatment and in-furrow use at a global scale. Votivo Prime is a Bacillus firmus–based biological nematicide designed for seed and in‑furrow application. BASF’s scaling of this product underscores growing adoption of preventive, early‑season nematode control, particularly in soybean, cotton, and corn systems.

- June 2024: BASF SE’s Nemasphere soybean cyst nematode trait awaits U.S. approval. Nemasphere introduces genetic nematode resistance rather than a nematicide product. While not a direct nematicide, it affects long‑term demand dynamics, especially for soybean cyst nematode control, and reshapes integrated nematode‑management strategies.

- June 2024: FMC Corporation and Novonesis signed an exclusive Canadian distribution pact for microbial biosolutions. This partnership strengthens FMC’s biological soil‑health and microbial portfolio, some of which are relevant to nematode management.

Global Bionematicides Market Report Scope

Bionematicides are sustainable, environmentally friendly agricultural products derived from natural microorganisms, such as fungi and bacteria, or from plant-based compounds. They are used to effectively manage plant-parasitic nematodes. The Bionematicides Market Report is Segmented by Product Type (Microbials, Biochemicals, Integrated/Combined, Next-Generation RNAi Formulations), Mode of Application (Soil Treatment, Seed Treatment, Foliar Spray, Drip-Irrigation Injection), Crop (Fruits and Vegetables, Cereals and Grains, Oilseeds and Pulses, Turf, Ornamentals and Forage), Formulation (Liquid Suspensions, Dry Granules and Wettable Powders), Infestation Type (Root-knot Nematodes, Cyst Nematodes, Lesion Nematodes, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Microbials |

| Biochemicals |

| Integrated/Combined |

| Next-Generation RNAi Formulations |

| Soil Treatment |

| Seed Treatment |

| Foliar Spray |

| Drip-Irrigation Injection |

| Fruits and Vegetables |

| Cereals and Grains |

| Oilseeds and Pulses |

| Turf, Ornamentals and Forage |

| Liquid Suspensions |

| Dry Granules and Wettable Powders |

| Root-knot Nematodes |

| Cyst Nematodes |

| Lesion Nematodes |

| Others (Stubby-root, Reniform) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Product Type | Microbials | |

| Biochemicals | ||

| Integrated/Combined | ||

| Next-Generation RNAi Formulations | ||

| By Mode of Application | Soil Treatment | |

| Seed Treatment | ||

| Foliar Spray | ||

| Drip-Irrigation Injection | ||

| By Crop | Fruits and Vegetables | |

| Cereals and Grains | ||

| Oilseeds and Pulses | ||

| Turf, Ornamentals and Forage | ||

| By Formulation | Liquid Suspensions | |

| Dry Granules and Wettable Powders | ||

| By Infestation Type | Root-knot Nematodes | |

| Cyst Nematodes | ||

| Lesion Nematodes | ||

| Others (Stubby-root, Reniform) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the bionematicides market anticipated to grow between 2026 and 2031?

Revenue is forecast to rise from USD 473 million in 2026 to USD 705 million by 2031 at a 8.3% CAGR through 2026-2031.

Which product type currently leads global sales?

Microbial formulations account for largest share with 62% of 2025 revenue, owing to decades of proven field performance.

Why are seed-treatment bionematicides gaining popularity?

Bundling biologicals into proprietary coatings eliminates separate field passes and ensures uniform early-root protection, propelling a 10.1% CAGR through 2031.

Which crops offer the strongest growth opportunity?

Oilseeds and pulses are projected to expand at an 11.5% CAGR through 2026-2031, as plant protein demand accelerates and residue-free requirements tighten.

What limits adoption in tropical regions?

The short shelf life of liquid suspensions and the scarcity of refrigerated logistics hinder distribution, though dry granules and powders are addressing the gap.

Page last updated on: