Market Overview

| Study Period | 2021 - 2031 |

|---|---|

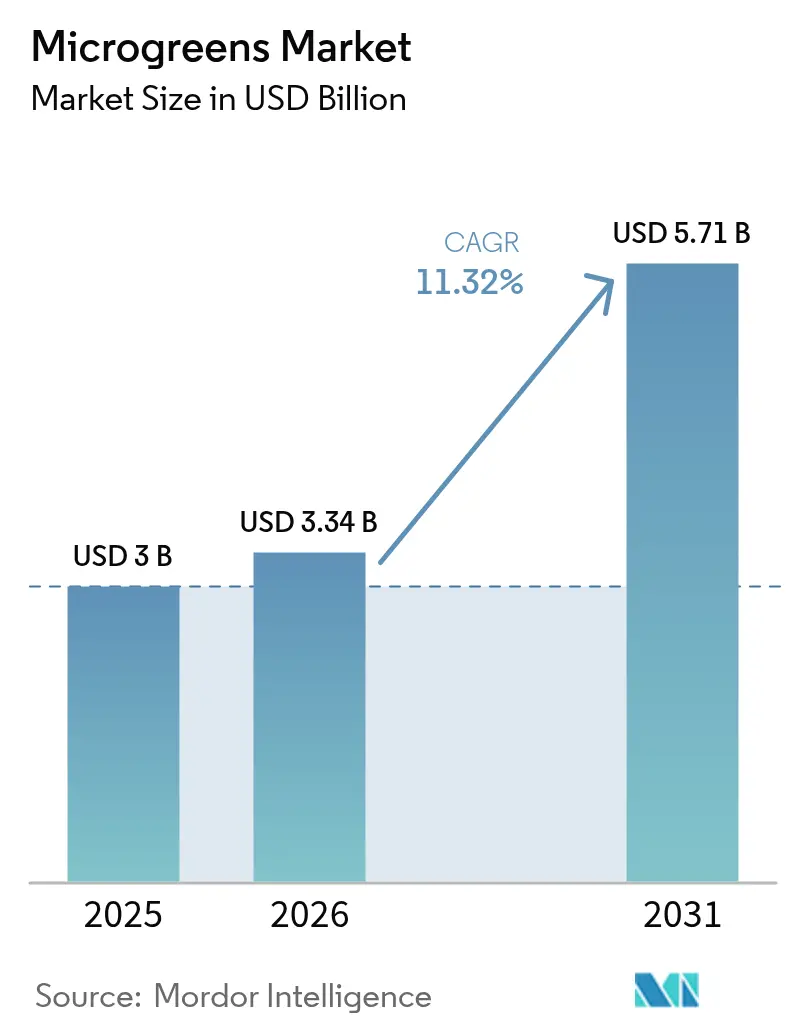

| Market Size (2026) | USD 3.34 Billion |

| Market Size (2031) | USD 5.71 Billion |

| Growth Rate (2026 - 2031) | 11.32% CAGR |

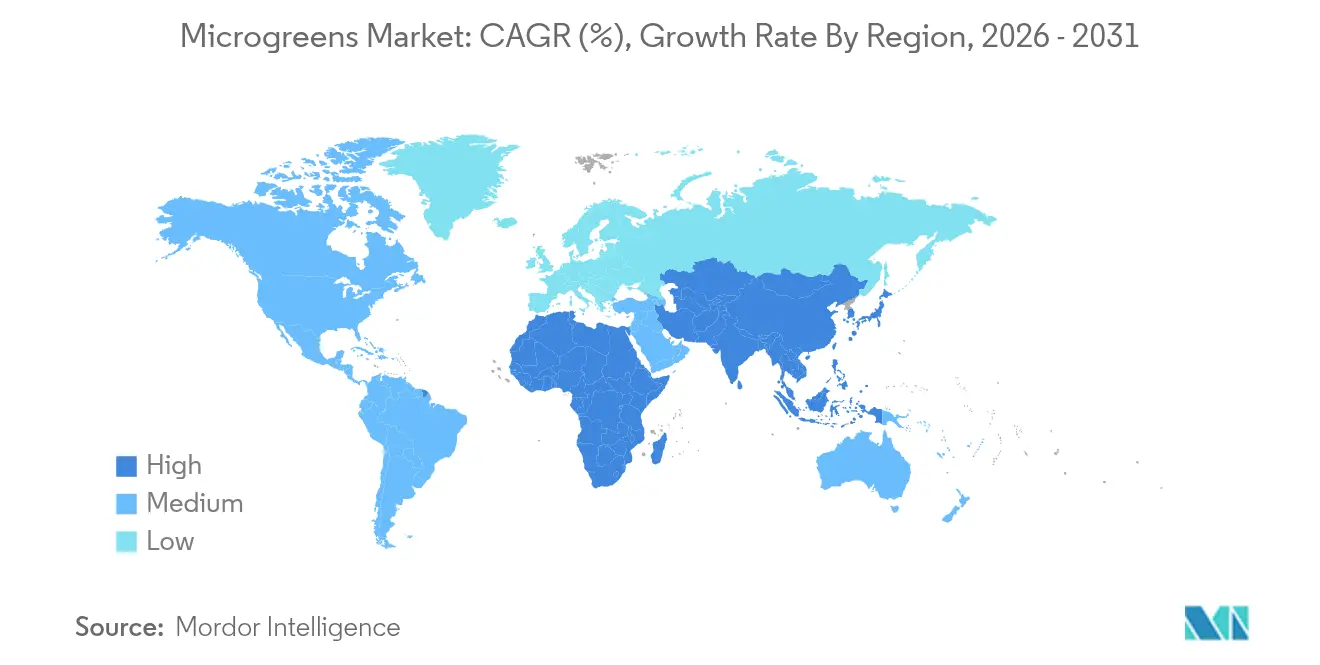

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

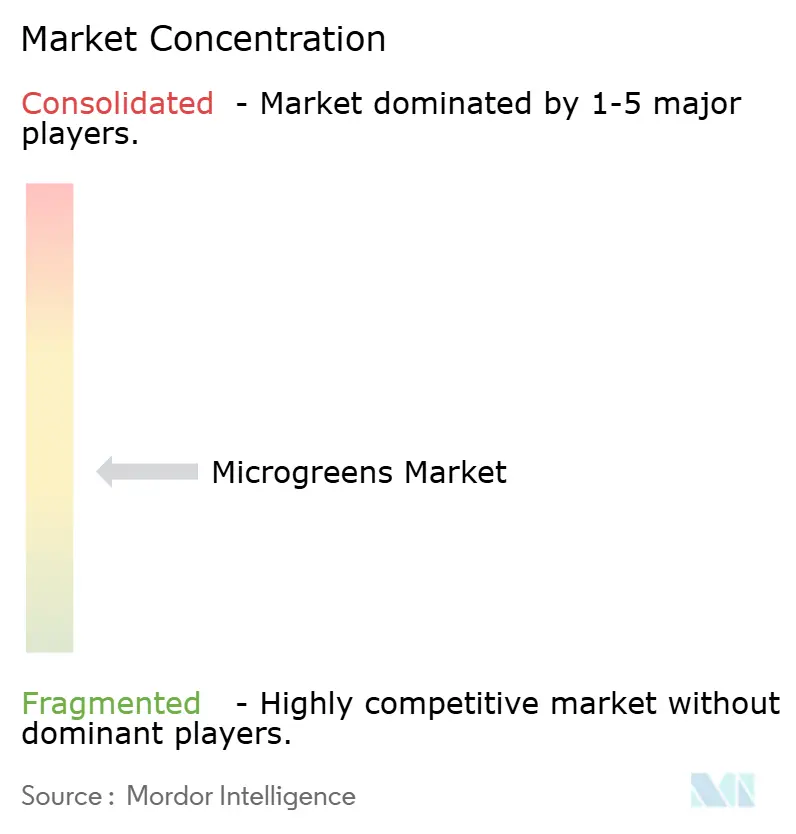

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microgreens Market Analysis by Mordor Intelligence

The microgreens market size was valued at USD 3.0 billion in 2025 and estimated to grow from USD 3.34 billion in 2026 to reach USD 5.71 billion by 2031, at a CAGR of 11.32% during the forecast period (2026-2031). Sustained in the microgreens market demand stems from consumers seeking nutrient-dense produce, producers upgrading to high-yield indoor systems, and retailers adding premium microgreen assortments to differentiate fresh-food aisles. Scientific evidence confirming that certain varieties hold 5-40 times the vitamin and antioxidant content of their mature counterparts keeps the microgreens market firmly positioned within functional foods. Technology convergence is another lift: AI-directed LED recipes are delivering energy savings close to 32% while vertical stacks achieve production densities up to 390-fold above field output. Localization strategies within the microgreens market that shorten supply chains and reduce spoilage further reinforce the economic appeal, and lunar agriculture trials scheduled for 2026 are catalyzing new precision-growing tools for terrestrial use. Altogether, the microgreens market continues to outpace broader controlled-environment agriculture segments and is on track for another multi-year run of double-digit expansion.

Key Report Takeaways

- By type, broccoli microgreens led with 27.45% revenue share in 2025; basil microgreens are projected to expand at a 14.57% CAGR through 2031.

- By farming method, indoor systems controlled 45.30% of the microgreens market share in 2025, while vertical farming is on course for the fastest 19.74% CAGR by 2031.

- By growth medium, peat moss accounted for a 33.20% slice of the microgreens market size in 2025, yet coconut coir shows the quickest 15.45% CAGR outlook.

- By distribution channel, restaurants held 51.10% microgreens market share in 2025, whereas online-to-door delivery is set to grow at an 17.95% CAGR through 2031.

- By region, North America commanded 42.40% of the microgreens market share in 2025, while Asia-Pacific is forecast to record a 12.85% CAGR-the highest among all regions.

- At the company level, AeroFarms, BrightFresh, Gotham Greens, Bowery Farming, and GoodLeaf collectively captured roughly 36% of global sales.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microgreens Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health-conscious consumers are demanding nutrient-dense foods | +2.1% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| Uptake of urban, indoor, and vertical farming infrastructures | +2.8% | Asia-Pacific core; spill-over to global urban hubs | Long term (≥ 4 years) |

| Fine-dining and premium culinary adoption worldwide | +1.6% | North America and Europe, growing in Asian metros | Short term (≤ 2 years) |

| Retail-chain private-label microgreen launches | +1.9% | North America and Europe, and early in Australia | Medium term (2–4 years) |

| Nanotechnology-enhanced substrates boost yield and nutrition | +1.2% | Global, early use in developed markets | Long term (≥ 4 years) |

| Microgreens selected for space-life support and astronaut menus | +0.8% | Global R and D led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Health-Conscious Consumers Demanding Nutrient-Dense Foods

Bean microgreens supply 80.45 mg/100 g of ascorbic acid—well above mature-plant levels—while their 8–21-day growth cycle supports year-round harvests. Urban dwellers facing micronutrient gaps view this concentration as worth a premium. Healthcare professionals increasingly cite microgreens when recommending functional foods that dovetail with preventive health budgets. Aging demographics magnify the pool of customers willing to invest in proven nutrition. Peer-reviewed links between routine intake and improved cardiovascular as well as glycemic markers spur repeat purchases among wellness-minded buyers. Together, these factors keep nutrition advocacy central to growth in the microgreens market messaging.

Uptake of Urban, Indoor, and Vertical Farming Infrastructures

The UAE’s plan to deploy more than 500 vertical farms within five years signals a USD 6.2 billion upside by 2030, with microgreens positioned as anchor crops thanks to their short growth cycles. Dutch innovator PlantLab closed EUR 20 million (USD 20 million) in 2024 to widen European capacity, underscoring investor belief in scalable models. IoT sensors now adjust humidity, CO₂, and airflow at the plant level, raising yield consistency while shrinking labor. Renewable-powered chillers and heat-exchange loops improve lifetime operating costs and answer carbon-footprint critiques. Municipal incentives that target food-miles reduction further tilt economics in favor of city-center production. Collectively, these inputs build a durable foundation for capacity expansion across the microgreens market in both mature and emerging regions.

Fine-Dining and Premium Culinary Adoption Worldwide

Chefs once used microgreens as garnish, yet they now deploy wasabi mustard, rainbow mixes, and shiso as flavor-dense centerpieces on entrées mpseeds.com. A National Restaurant Association survey shows that 51% of chefs rank microgreens as a primary trend shaping menus this year. Culinary institutes teach on-site cultivation, creating graduates who know crop-handling nuances and who actively request diverse varieties. Farm-to-kitchen deals guarantee chefs bespoke cultivars while giving growers stable forward contracts. High-margin tasting menus rely on sensory novelty, and microgreens deliver both color and intensified flavor that justify price premiums. As more fine-casual chains embrace the aesthetic, volume demand in the microgreens market shifts from niche to mainstream food service.

Retail-Chain Private-Label Microgreen Launches

BrightFresh hit 43 Costco stores in Southern California with its Supergreens Micro Medley and claims a near-40% regional share, demonstrating retailer confidence in house-brand microgreens. Walmart’s Marketside Beyond line uses closed-loop farms that cut water consumption by 90%, presenting sustainable sourcing to mass customers. Convenience giant 7-Eleven offers Plenty’s vertically farmed punnets across 1,300 California locations, expanding exposure past traditional grocery. Private labels improve margins while allowing retailers to steer specifications on pesticide-free or nutrient-verified claims. Shelf-life-extending packs reduce shrink, which cements microgreens as one of the freshest and most profitable items in produce.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short post-harvest shelf life and cold-chain gaps | -1.4% | Global, pronounced in developing regions | Short term (≤ 2 years) |

| High unit production costs for controlled-environment farming | -1.8% | Global, acute in high-electricity markets | Medium term (2–4 years) |

| Food-safety recalls linked to poor sanitation practices | -1.1% | Global, higher risk where oversight is weak | Short term (≤ 2 years) |

| Fragmented standards are delaying global organic certification | -0.9% | Global, notable in cross-border trade | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Food-Safety Recalls Linked to Poor Sanitation Practices

Sprout outbreaks of Salmonella and E. coli color regulators’ perception of similar production methods, even though no microgreens illnesses were logged from 1998–2017 extension.unr.edu. The FDA’s stronger organic enforcement, activated in 2024, adds documented hazard-analysis plans and lot-level traceability, raising compliance costs[1]Source: USDA Agricultural Marketing Service, “Strengthening Organic Enforcement Final Rule,” usda.gov. Growers now deploy antimicrobial root-zone washes and UV-C cabin tunnels to pre-empt contamination. Certifications such as GlobalGAP and SQF have become de facto tickets to retail distribution. On-farm automation reduces human touchpoints, cutting the probability of lapses. In parallel, space-crop sanitation protocols—originally devised for nutrient film technique in orbit—feed back to earth farms, offering validated pathogen-control blueprints.

Fragmented Standards Delaying Global Organic Certification

The European Union began insisting on electronic certificates for every organic import in 2025, complicating shipments from non-EU producers[2]Source: European Commission, “Electronic Certification for Organic Imports,” ec.europa.eu. Soilless microgreens often struggle to meet legacy soil-based rules, forcing dual audits or losing the organic label entirely. The United States allows hydroponic organics, yet Canada and parts of Asia do not, adding paperwork and slowing market entry. Multi-agency efforts aim to harmonize definitions under Codex guidelines, but philosophical divides over substrate use persist. Some regions now craft specific controlled-environment organic addenda, yet full synchronization may take years. During this gap, producers in the microgreens market invest in parallel certification tracks that inflate the cost per pound and delay global rollout plans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Broccoli Dominance Faces Basil Innovation

Broccoli microgreens controlled 27.45% of 2025 revenue within the microgreens market size, buoyed by 825.53 mg GAE/100 g total phenolics that support premium price points. Arugula retains a 14.70% share, leveraging its peppery kick that chefs prize for salads and pizzas. Radish lines capture 21.10%, especially in hydroponic channels, where quick germination validates aggressive planting densities.

Basil microgreens headline growth with a forecast 14.57% CAGR, reflecting culinary familiarity and aromatic punch that retail shoppers recognize quickly. Lettuce and chicory add 12.55%, offering gentle flavors that help first-time buyers. Specialty entries, fennel, pea, sorrel, and the still-controversial hemp microgreen, keep SKUs dynamic and inviting experimentation. Continuous breeding and seed-house collaborations within the microgreens industry open fresh cultivar cycles every season, keeping consumer curiosity alive and pricing resilient.

By Farming Method: Indoor Systems Enable Vertical Scaling

Indoor farms held 45.30% microgreens market share in 2025, anchored by climate-tight rooms that deliver uniform CO₂, lighting, and nutrient flow. These conditions produce leaves with consistent texture and color, vital for retailers who demand SKU-level predictability.

Vertical farms promise the fastest 19.74% CAGR through 2031 by multiplying square-foot output. AutoStore and OnePointOne’s fully robotic Arizona site packs trays into cubic lattices and snips product after 15 days, using 95% less water than field cultivation. Hybrid greenhouses that stack tiered towers beneath translucent roofing split the difference on capex, appealing to mid-tier investors. Meanwhile, container farms allow on-premise production at grocery backlots and campus food halls, shrinking last-mile challenges.

By Distribution Channel: Restaurant Dominance Meets Digital Disruption

Restaurants captured 51.10% microgreens market share in 2025, with chefs viewing vibrant coloration and flavor intensity as brand-signature elements. Direct grower links secure bespoke mixes that match seasonal menus and drive predictable off-take.

Digital commerce sits on an 17.95% CAGR runway, using subscription boxes and blockchain guarantees to satisfy consumer desire for traceable, pesticide-free greens. Hypermarkets hold 38.60%, where clamshell innovations extend shelf life to 14 days, improving inventory turns. Corporate cafeterias and school meal programs show latent demand, especially under wellness mandates. As logistics apps integrate cold-chain APIs, expect delivery windows under two hours that rival restaurant freshness.

By Growth Medium: Sustainable Substrates Drive Innovation

Peat moss held the largest 33.20% microgreens market share in 2025, thanks to moisture retention and pH buffering, yet emissions targets place it under scrutiny. Coconut coir is closing ground with a 15.45% CAGR, repurposing husk waste and delivering similar capillary action.

Soil-based trays maintain a 27.80% share in the microgreens market as organic growers defend the “grown-in-soil” narrative. Tissue-paper pads post 12.85% growth on low cost and sterility, useful for quick-turn microgreens. Bio-fiber mats spiked with nanoscale silica expand water-holding potential and promote microbial balance that reduces root disease. Aeroponic mist beds dodge the substrate debate altogether, though they demand tighter nutrient monitoring.

Geography Analysis

Asia-Pacific is the fastest-growing region in the microgreens market, logging a 12.85% CAGR through 2031 as urbanization and rising incomes align with government food-security grants. China’s USD 1.34 trillion fruit-and-vegetable economy offers a vast runway, and megacity pilots in Shanghai and Shenzhen now place vertical farms within city blocks to slash travel time. Singapore operates high-tech indoor hubs that export microgreens to Malaysia and Indonesia, cementing the city-state as a regional innovation lab. Australia, spurred by drought and salinity concerns, backs solar-powered greenhouse clusters in peri-urban zones, while India’s Bengaluru cluster champions low-capex rack farms aimed at hotel chains.

North America retained the largest contribution to the microgreens market size at 42.40% in 2025, reflecting mature retail penetration and robust food-service demand. Operators like AeroFarms, Gotham Greens, and Bowery Farming serve thousands of stores, and fresh financing helped GoodLeaf add 2,700 Canadian doors. Mexico leverages lower power costs and proximity to U.S. buyers, securing joint-venture supply agreements that bypass cross-border bottlenecks. Regional regulatory clarity on organic hydroponics supports premium positioning, although fragmented standards still challenge interstate logistics.

Europe is advancing at an 8.05% CAGR on the back of urban-agriculture subsidies and carbon-border adjustments that favor local production. Dutch pioneers such as PlantLab iterate on fully enclosed “Plant Production Units,” while Germany’s renewable-energy credits offset greenhouse inputs. Italy’s farm-to-table restaurants tout microgreens-topped dishes to culinary tourists. EU organic certificate digitization, active from 2025, may erect soft trade barriers that push supermarkets to source within the bloc. Elsewhere, the Middle East marshals sovereign-wealth capital, evidenced by a USD 180.5 million Pure Harvest raise in 2024 to build climate-tough facilities, and Africa is starting its 11.10% ascent as cold-chain corridors reach secondary cities.

Competitive Landscape

The microgreens market remains moderately fragmented; the five largest brands hold 36% of worldwide revenue. AeroFarms leverages aeroponic towers and AI growth recipes to hold a 9.5% share, reaching 2,000 retail doors after exiting Chapter 11 in 2025. BrightFresh dominates Southern California through an exclusive Costco tie-up, giving it an outsized lift in a dense buying hub. Gotham Greens expands east-coast hydroponic acreage and sells branded microgreens alongside full leaves, while Bowery Farming explores gene-edited seeds to shorten growth cycles.

The technology marks the competitive frontier. Automated harvesters, vision-guided grading, and blockchain batch codes combine to improve labor efficiency and traceability. Patent monitoring services count 247 active filings tied to LED spectra, bio-polymer mats, and shelf-life extenders, revealing an R&D arms race. Foodservice operators like Compass Group experiment with on-site grow walls to hedge supply risk, and agritech suppliers bundle turnkey farms for hotels and cruise ships.

M and A momentum builds: Local Bounti folded Pete’s into its footprint, securing extra West-coast volume; 80 Acres Farms bought Mother Raw to link fresh inputs with salad-dressing manufacturing; Elevate Farms teamed with Cultivatd for European rollout. Space-agriculture breakthroughs aimed at closed-loop nutrient systems hint at serial tech transfers that could compress operating costs for early adopters[3]Source: NASA, “Deep Space Food Challenge Phase II Winners,” nasa.gov.

Microgreens Industry Leaders

AeroFarms LLC

BrightFresh (Cox Enterprises))

GoodLeaf Farms ( TrueLeaf )

Gotham Greens

80 Acres Farms

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: AutoStore and OnePointOne launched the world’s first fully robotic vertical farm in Arizona, delivering microgreens to Whole Foods Market with 95% less water use.

- May 2025: Canada opened its first fully automated greenhouse in Ontario, highlighting labor-light, year-round microgreen output.

- March 2025: Oasthouse Ventures announced a USD 1.1 billion greenhouse in Virginia, adding 118 jobs and targeting completion in 2026.

- February 2025: 7-Eleven partnered with Plenty Unlimited to stock microgreens across 1,300 California convenience stores.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global microgreens market as the aggregate farm-gate value of freshly cut, vegetable, herb, and grain seedlings harvested between the cotyledon and first true-leaf stages and sold either loose or as living trays to retail, food-service, and direct-to-consumer channels.

Scope exclusions include sprout products, baby-leaf greens, powdered extracts, and sales of cultivation equipment, which are kept outside this value pool.

Segmentation Overview

- By Type

- Broccoli

- Lettuce and Chicory

- Arugula

- Basil

- Fennel

- Carrots

- Sunflower

- Radish

- Peas

- Other Types

- By Farming Method

- Indoor Farming

- Vertical Farming

- Commercial Greenhouses

- Other Farming Methods

- By Growth Medium

- Peat Moss

- Soil

- Coconut Coir

- Tissue Paper

- Other Growth Media

- By Distribution Channel

- Hypermarkets and Supermarkets

- Restaurants

- Other Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Chile

- Argentina

- Rest of South America

- Europe

- Netherlands

- Spain

- Germany

- France

- Rest of Europe

- Asia-Pacific

- China

- India

- Singapore

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with vertical-farm operators, greenhouse agronomists, specialty-produce buyers, and chef users across North America, Europe, and Asia. Their inputs on tray weights, spoilage rates, menu penetration, and forward contract pricing filled statistical gaps and helped us challenge early desk-research assumptions.

Desk Research

We began by aligning protected-cultivation acreage, customs headings for edible seedlings, and monthly price files from agencies such as USDA ERS, Eurostat, and the FAO. These series anchor supply and trade flows that our team at Mordor Intelligence later models against demand. Further context came from bulletins issued by the Indoor Farming Association, the Sustainable Restaurant Association, and selected peer-reviewed agronomy journals, which clarify channel mix and yield trends. Annual reports, investor decks, and news archives accessed through D&B Hoovers and Dow Jones Factiva supplied producer revenues, while Questel patent scans signaled upcoming varietal launches and LED efficiency gains. The sources listed here are illustrative, and numerous additional government and industry releases were reviewed for cross-checks.

Market-Sizing & Forecasting

A top-down construct multiplies average microgreen yield per square meter by protected-cultivation area in each country and then adjusts for net trade. Results are compared with selective bottom-up indicators, such as sampled farm sales, e-commerce basket audits, and channel checks, to fine-tune totals. Variables guiding the model include indoor-farm square footage growth, premium menu adoption rates, average selling price per pound, consumer health and wellness spending, and LED cost curves. Five-year outlooks rely on multivariate regression, with scenario envelopes vetted with our primary contacts. When bottom-up hints differ materially from the reconstructed demand pool, utilization factors are iterated before baseline lock-in.

Data Validation & Update Cycle

Mordor analysts run every draft through anomaly dashboards, peer reviews, and senior sign-off. The database refreshes annually, with mid-cycle updates triggered by material shifts such as phytosanitary bans or landmark funding rounds, ensuring clients receive the latest calibrated view.

Why Our Microgreens Baseline Commands Reliability

Estimates in this niche often diverge because publishers vary the produce list, apply different tray-to-weight factors, or refresh at uneven cadences.

Our disciplined scope, live channel checks, and yearly updates, we believe, keep the baseline grounded and decision-ready. Key gaps arise when others fold seed-kit retail, functional beverage extensions, or apply blanket price inflators without wholesale verification.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.0 B (2025) | Mordor Intelligence | |

| USD 2.79 B (2023) | Global Consultancy A | Older base year, excludes vertical-farm output |

| USD 4.10 B (2025) | Research Firm B | Bundles seed kits and powders, inflating totals |

These contrasts show that our measured scope and dual-path validation give stakeholders a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

How big is the microgreens market today?

The microgreens market size stands at USD 3.34 billion in 2026 and is projected to reach USD 5.71 billion by 2031, reflecting an 11.32% CAGR.

Which microgreen variety generates the most revenue?

Broccoli microgreens lead with a 27.45% share in 2025 thanks to the verified antioxidant density that commands premium pricing.

Why is vertical farming critical for microgreens producers?

Vertical farms offer production densities up to 390 times greater than field plots and are forecast to grow at a 19.74% CAGR through 2031, making them the fastest-expanding method in the microgreens market.

What is the primary cost challenge for indoor growers?

Electricity for LED lighting and climate control drives the largest operating expense, though next-generation LEDs and renewable-energy deals are cutting power needs by roughly 32%.

How vulnerable are microgreens to food-safety recalls?

Microgreens have no recorded outbreaks to date, but similarities to sprout production keep regulators attentive, and growers must adhere to strict sanitation and traceability rules to maintain trust.

Which region shows the fastest growth potential?

Asia-Pacific is projected to register the quickest 12.85% CAGR through 2031, propelled by urbanization, rising disposable income, and government-backed food-security programs.

Page last updated on: