Gibberellins Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

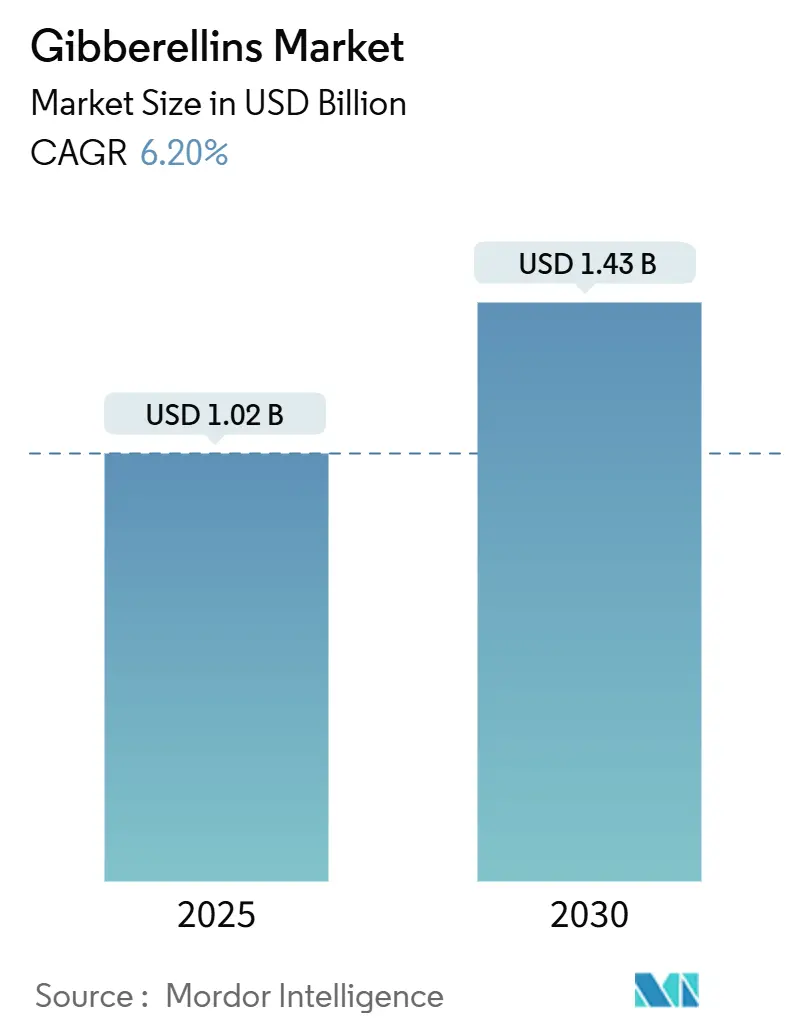

| Market Size (2025) | USD 1.02 Billion |

| Market Size (2030) | USD 1.43 Billion |

| Growth Rate (2025 - 2030) | 6.20% CAGR |

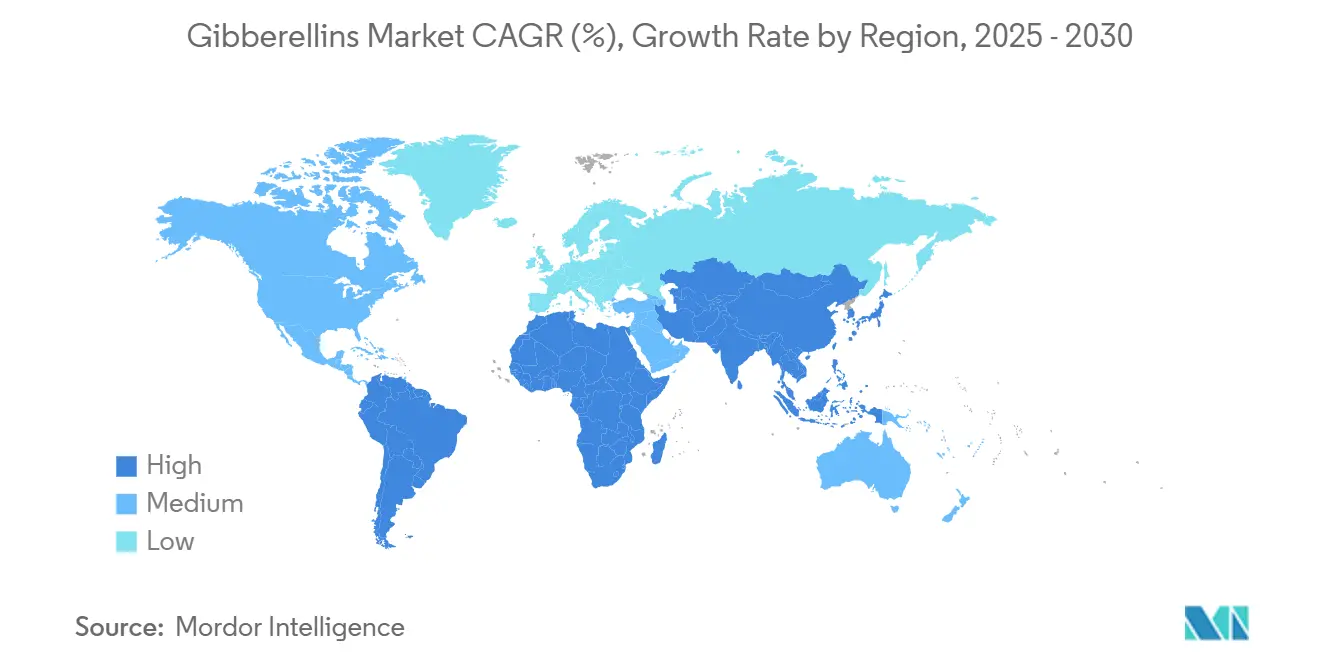

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gibberellins Market Analysis by Mordor Intelligence

The gibberellins market size is estimated at USD 1.02 billion in 2025 and is projected to reach USD 1.43 billion by 2030, representing a 6.2% CAGR over the forecast period. Market expansion is driven by cost-cutting breakthroughs in microbial fermentation, which lowered GA3 production costs by 30% in 2024, as well as rising adoption in premium horticulture and growing penetration in cannabis cultivation. Commercial growers recognize the ability of gibberellins to boost fruit size, uniformity, and shelf life, which directly translates into price premiums. The increase in sugarcane acreage, tied to bioethanol mandates and widespread government yield enhancement programs in cereals, has created steady demand. Competitive intensity remains moderate, allowing scale leaders to pursue cost leadership while nimble biotechnology start-ups introduce specialty formulations that command higher margins. Regional dynamics reinforce the upside. The Asia-Pacific region benefits from manufacturing scale and policy support, North America leverages precision farming and cannabis legalization, and Brazil fuels demand through bioethanol expansion.

Key Report Takeaways

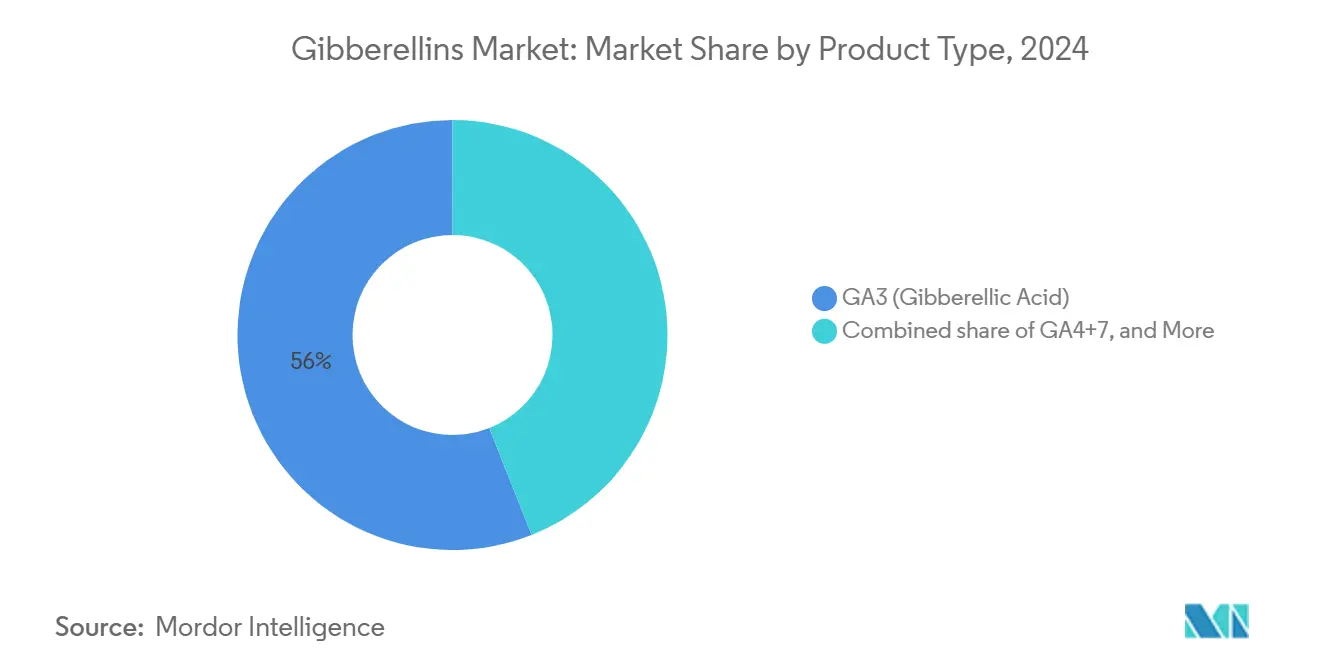

- By product type, GA3 held 56% gibberellins market share in 2024, while GA4+7 is forecast to grow at 8.6% CAGR through 2030.

- By formulation, liquid solutions led with 63% revenue in 2024, and granules and tablets are projected to expand at a 7.4% CAGR to 2030.

- By crop type, fruits and vegetables accounted for 42.5% of the gibberellins market size in 2024, whereas cannabis cultivation is advancing at 12.5% CAGR through 2030.

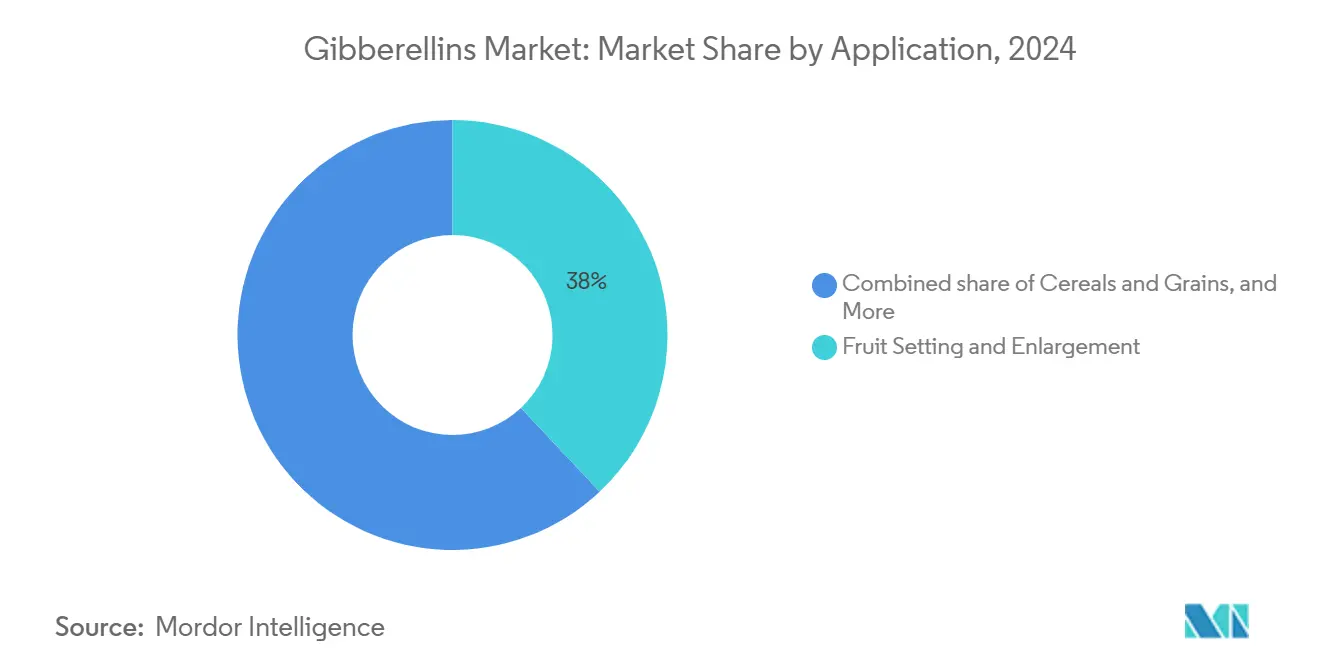

- By application, fruit setting and enlargement controlled 38% share of the gibberellins market size in 2024, while seed treatment and germination are set to rise at 9.8% CAGR to 2030.

- By source, microbial fermentation accounted for 64% of the gibberellins market in 2024, which is projected to grow at a CAGR of 7.2% during the forecast period.

- By geography, Asia-Pacific captured the largest share of 32% in 2024 and is expanding at 7.2% CAGR through 2030.

- The five leading market players are Valent BioSciences (Sumitomo Chemical Co., Ltd.), Sichuan Guoguang Agrochemical Group, UPL Ltd, Nufarm Limited, and Jiangsu Fengyuan Bioengineering, collectively holding around 61% share of the gibberellins market in 2024.

Global Gibberellins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-value horticultural crops | +1.8% | Global, North America, and Europe focus | Medium term (2-4 years) |

| Growing preference for organic plant growth regulators | +1.2% | Europe and North America, emerging Asia-Pacific | Long term (≥ 4 years) |

| Expanding sugarcane acreage for bioethanol targets | +0.9% | Brazil, India, Thailand, and Southeast Asia | Medium term (2-4 years) |

| Government programs for yield enhancement in cereals | +0.7% | India, China, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Integration of gibberellins in cannabis cultivation protocols | +0.5% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Cost-reduction breakthroughs in GA3 fermentation processes | +0.4% | Global, Asia-Pacific production hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Value Horticultural Crops

Premium fruit and vegetable growers rely on gibberellins to enhance size, firmness, and visual appeal, attributes that win supermarket shelf space and consumer loyalty. Shine Muscat grapes treated with GA3 showed a 25% jump in fructose and glucose content, allowing growers to command higher unit prices. Ornamental producers apply gibberellins to regulate plant height and flowering cycles, keeping greenhouse capacity fully utilized year-round. Citrus exporters use GA3 to delay senescence, safeguarding fruit value during transcontinental shipping [1]Source: University of Florida Institute of Food and Agricultural Sciences, “GA3 Post-harvest Citrus Management,” ufl.edu. As global produce trade expands and buyers reward consistent quality, horticulture applications will stay a prime revenue engine for the gibberellins market.

Growing Preference for Organic Plant Growth Regulators

Regulators and consumers alike now favor naturally derived inputs. The United States Environmental Protection Agency exempts gibberellins from tolerance limits, easing organic certification pathways [2]Source: Environmental Protection Agency, “Tolerance Exemption for Gibberellins,” epa.gov. The European Union’s fertilizer regulation promotes recycled and bio-based inputs, cementing demand for fermentation-derived gibberellins that satisfy both eco-labeling and performance metrics. Major retailers have instituted supplier scorecards that link shelf placement to verified sustainable practices, effectively making bio-based PGRs a license to operate for export-oriented growers.

Expanding Sugarcane Acreage for Bioethanol Targets

Brazil's RenovaBio program and India's ethanol blending target of 20% by 2027, which was achieved ahead of schedule in 2025, are driving significant expansion in sugarcane cultivation. This growth is contributing to increased adoption of gibberellins, which enhance stem elongation and sucrose accumulation. Field trials have demonstrated yield improvements of 12-18%, boosting feedstock efficiency for mills operating under carbon intensity regulations. Additionally, the development of mechanization-compatible sugarcane varieties optimized for gibberellin responsiveness is further encouraging adoption in countries such as Thailand and Vietnam.

Integration of Gibberellins in Cannabis Cultivation Protocols

Legalization in North America and parts of Europe has drawn commercial growers to hormones that regulate plant architecture, shorten vegetative phases, and optimize cannabinoid profiles. Indoor facilities apply precise GA4 and GA7 ratios for canopy control, maximizing grams per square foot and return on LED lighting investments. This niche segment posts the fastest growth rate in the gibberellins market and is anticipated to expand into medical cannabis programs across Asia-Pacific.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations on PGR residues | -0.8% | Europe and North America, spillover via export standards | Long term (≥ 4 years) |

| Availability of synthetic low-cost alternatives | -0.6% | Global, acute in price-sensitive regions | Medium term (2-4 years) |

| Supply constraints of Fusarium fujikuroi strains | -0.4% | Global, and Asia-Pacific hubs | Short term (≤ 2 years) |

| Cold-chain challenges for GA formulations in emerging markets | -0.3% | Sub-Saharan Africa, Southeast Asia, and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations on PGR Residues

Regulatory agencies worldwide have implemented stricter testing requirements for plant growth regulator residues, with maximum residue limits becoming more restrictive across major agricultural markets. The European Union's farm-to-fork strategy emphasizes reducing chemical inputs, which creates compliance challenges for gibberellin applications in export-oriented production [3]Source: European Commission, “Farm to Fork Strategy,” ec.europa.eu . Current testing protocols require detection capabilities at parts-per-billion levels, increasing compliance costs and creating market access barriers for producers in regions with limited analytical infrastructure. Food safety authorities in major importing countries have implemented harmonized residue standards that set global benchmarks, requiring producers to adopt application protocols that prioritize residue minimization over yield optimization. These regulatory changes provide competitive advantages to companies developing gibberellin formulations with enhanced biodegradation properties and improved application timing protocols that reduce residue accumulation in harvested products.

Availability of Synthetic Low-Cost Alternatives

Chemical synthesis routes for gibberellin production provide cost advantages in markets where regulatory approval processes favor established synthetic compounds over fermentation-derived alternatives. Manufacturers utilize expired patents to produce synthetic gibberellins at competitive prices, particularly in regions where organic certification offers minimal market premiums. The cost advantage increases as synthetic production achieves economies of scale that fermentation processes cannot match, especially in commodity crop applications where price is the primary consideration. However, synthetic alternatives face stricter regulatory oversight regarding environmental impact and worker safety, which may restrict their future market presence. This creates a divided market where premium applications favor fermentation-derived products while commodity applications remain price-sensitive, requiring manufacturers to develop strategies that serve both segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: GA3 Dominance Faces Specialized Challenge

GA3 held a 56% share of the gibberellins market in 2024, reflecting its decades-long record for fruit set, stem elongation, and seed germination. Its broad crop label portfolio and abundant safety data have built strong distributor confidence. However, GA4+7 is growing at 8.6% CAGR on the back of malting and post-harvest applications that reward precise hormone ratios. Specialty brewers and maltsters report enzyme efficiency gains that justify premium GA4+7 pricing, offsetting its higher production complexity.

Other niche gibberellins capture attention where unique physiological responses are needed. Indoor cannabis operators tailor custom blends that steer internode length and terpene expression, while strawberry growers experiment with GA9 permutations to synchronize flowering. Biotechnology advances in strain engineering now permit economical output of once scarce variants, widening the competitive canvas. As growers pivot to precision agronomy, manufacturers that supply a full spectrum of hormones stand to consolidate their share.

By Formulation: Liquid Solutions Lead Innovation

Liquid formulations commanded roughly 63% of the gibberellins market in 2024. Farmers value their tank-mix flexibility and accuracy when applying through drip or foliar systems. Formulators are investing in chelated adjuvants and pH buffers that boost uptake and tolerance under variable water quality. Ambient-stable liquids target tropical markets lacking refrigerated storage, extending shelf life from 6 to 18 months.

Powders remain relevant where inland logistics favor solids, and their cost structure suits cooperatives pooling large orders. Granular and tablet formats cater to nursery and turf professionals who prefer slow-release packages that minimize labor. Innovations in hot-melt extrusion and polymer encapsulation are blending efficacy with durability, pushing these segments toward 7.4% CAGR growth through 2030.

By Crop Type: Cannabis Emerges as Growth Driver

Fruits and vegetables accounted for 42.5% of the gibberellins market size in 2024, thereby uplifting orchard revenues by enhancing quality and color uniformity. Exporters of grapes, citrus, and cherries rely on GA3 to extend shipping windows without incurring cold injuries. Yet cannabis remains the fastest growing with a 12.5% CAGR to 2030. Legalization triggers facility build-outs where every square foot must produce high cannabinoid mass. Precise gibberellin scheduling shortens vegetative cycles, resulting in an additional harvest per year in multi-tier vertical farms.

Cereals, grains, and oilseeds utilize gibberellins to mitigate lodging and drought stress, rather than chasing premiums, creating a value narrative centered on reducing climate risk. Ornamentals and turfgrass continue to experience steady demand from landscaping projects and golf course upgrades, tied to the rebound in tourism.

By Application: Seed Treatment Gains Momentum

Fruit setting and enlargement captured 38% of the gibberellins market size in 2024, driven by well-established return metrics. A USD 70 per acre spray often nets USD 400 in incremental fruit revenue for table grapes. Seed treatment is the fastest-growing slice at 9.8% CAGR. Treating seed kernels ensures uniform emergence, which is critical for mechanical harvesting and high-density planting systems. Input distributors bundle gibberellin coatings with fungicides and micronutrients, boosting per-bag value.

Post-harvest dips delay rind aging in citrus and maintain brightness in apple skin, reducing retail shrink. Maltsters rely on GA4+7 to standardize alpha-amylase levels, keeping beer flavor stable across batches. Sugarcane attracts GA3 protocols that stretch internode spacing, enhancing sucrose tonnage and feedstock economics for ethanol refineries.

By Source: Fermentation Technology Advances

Microbial fermentation dominates gibberellin production with 64% of the market share in 2024, leveraging Fusarium fujikuroi strains that have been optimized through decades of biotechnology development. Recent advances in fermentation process control have reduced production costs by 25-30% while improving product consistency and reducing environmental impact. The fermentation approach aligns with sustainability trends and organic certification requirements that favor naturally-derived inputs over synthetic alternatives, driving its growth with a CAGR of 7.2% during the forecast period. Strain development programs now focus on enhancing productivity and reducing substrate requirements, addressing supply chain vulnerabilities that have historically constrained production capacity.

Semi-synthetic chemical production maintains market presence in applications where cost considerations outweigh sustainability preferences, particularly in commodity crop segments where price sensitivity limits adoption of premium-priced fermentation products. The chemical synthesis route offers advantages in production scalability and inventory management, enabling manufacturers to respond quickly to demand fluctuations without the lead times associated with fermentation processes. However, regulatory trends increasingly favor fermentation-derived products, creating long-term competitive advantages for companies with advanced biotechnology capabilities. The source segmentation reflects broader agricultural industry trends toward sustainable production methods that align with consumer preferences and regulatory requirements.

Geography Analysis

Asia-Pacific led the gibberellins market in 2024 with a share of 32% and shows the fastest 7.2% CAGR toward 2030. China’s pesticide sector transformed over four decades into a biotechnology powerhouse, exporting fermentation-grade GA3 worldwide. India’s government disbursed subsidies for plant growth regulators under its National Food Security Mission, spurring domestic demand and small-pack innovations tailored to marginal farmers.

North America ranked second as precision agriculture platforms and high-value fruit crops justify premium formulations. Indoor cannabis complexes from California to Ontario adopted multi-hormone regimens to drive productivity under LED lighting. Regulatory flexibility toward bio-based inputs adds momentum, positioning fermentation-derived products over synthetic rivals.

Europe accounted for a significant growth, constrained by stringent residue ceilings yet propelled by organic acreage expansion under the Green Deal. Suppliers meeting the European Union's eco-label criteria enjoy price premiums, compensating for slower volume uptake. South America delivered a significant growth as Brazil’s ethanol program scaled cane planting and Argentina chased export premiums in lemons and blueberries. Africa and the Middle East remain nascent but are incorporating gibberellins into cereal yield-gap initiatives funded by multilateral donors.

Competitive Landscape

The gibberellins market maintains moderate concentration, with leading companies controlling 61% of the market share in 2024. Valent BioSciences (Sumitomo Chemical Co., Ltd.) holds cost leadership in GA3 bulk supply through its integrated fermentation operations and global regulatory compliance. Sichuan Guoguang Agrochemical Group expanded its production capacity by 30% in 2024, supported by provincial incentives for green chemistry. UPL Ltd and Nufarm Limited enhanced their biologicals segments and distribution networks through strategic acquisitions in the crop protection sector.

Corteva Agriscience expanded its biologicals portfolio by acquiring Stoller Group and Symborg in January 2025, adding USD 200 million in revenue and gaining access to complementary microbial strains. Research and development priorities include improving fermentation strain yields, developing formulations to reduce residues, and creating controlled-release carriers suitable for warm climates.

Strategic partnerships between multinational companies and regional manufacturers create hybrid competitive models that combine global capabilities with local market expertise. These partnerships enable efficient market entry in emerging economies where distribution networks and regulatory relationships determine success. The growing collaboration between Chinese fermentation companies and Western formulators indicates an evolving global technology market that strengthens supply chain integration.

Gibberellins Industry Leaders

Valent BioSciences (Sumitomo Chemical Co., Ltd.)

Sichuan Guoguang Agrochemical Group

Jiangsu Fengyuan Bioengineering

UPL Ltd

Nufarm Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2023: Corteva Agriscience acquired Symborg, a microbiological technologies company based in Murcia, Spain, and Stoller, an agricultural biologicals company based in Houston, Texas. These acquisitions enhanced Corteva's presence in the biologicals market and expanded its gibberellins research and development capabilities.

- March 2023: Sumitomo Chemical India Ltd. introduced Promalin, a plant growth regulator for apple cultivation in Shimla. The product, developed by Valent Biosciences (USA), contains gibberellins GA4+7 and cytokinin 6-benzyladenine. These compounds improve fruit size, shape, weight, and quality through cell division and expansion stimulation.

- March 2023: Researchers from the SMART DiSTAP group and Temasek Life Sciences Laboratory developed a nanosensor that detects and differentiates between gibberellins GA3 and GA4 in real-time within living plants without damaging them. This advancement in detection technology enables improved monitoring of gibberellins, which can affect application methods, product development, and demand patterns in precision agriculture.

Global Gibberellins Market Report Scope

| GA3 (Gibberellic Acid) |

| GA4+7 |

| Other Gibberellins |

| Liquid |

| Powder |

| Tablet/Granule |

| Fruits and Vegetables |

| Cereals and Grains |

| Pulses and Oilseeds |

| Turf and Ornamentals |

| Plantation and Specialty Crops |

| Cannabis |

| Fruit Setting and Enlargement |

| Seed Treatment and Germination |

| Malting of Barley |

| Sugarcane Yield Enhancement |

| Post-harvest Treatments |

| Microbial Fermentation |

| Semi-synthetic Chemical |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | GA3 (Gibberellic Acid) | |

| GA4+7 | ||

| Other Gibberellins | ||

| By Formulation | Liquid | |

| Powder | ||

| Tablet/Granule | ||

| By Crop Type | Fruits and Vegetables | |

| Cereals and Grains | ||

| Pulses and Oilseeds | ||

| Turf and Ornamentals | ||

| Plantation and Specialty Crops | ||

| Cannabis | ||

| By Application | Fruit Setting and Enlargement | |

| Seed Treatment and Germination | ||

| Malting of Barley | ||

| Sugarcane Yield Enhancement | ||

| Post-harvest Treatments | ||

| By Source | Microbial Fermentation | |

| Semi-synthetic Chemical | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the gibberellins market?

The gibberellins market stands at USD 1.02 billion in 2025.

Which region dominates the gibberellins market?

Asia-Pacific holds the largest share and is also the fastest-growing region with a 7.2% CAGR through 2030.

Which product type commands the greatest market share?

GA3 remains the leading product, accounting for 56% of gibberellins market share in 2024.

What application segment is growing the fastest?

Seed treatment and germination is projected to grow at 9.8% CAGR, the fastest among all application segments.

Page last updated on: