Customer Experience Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

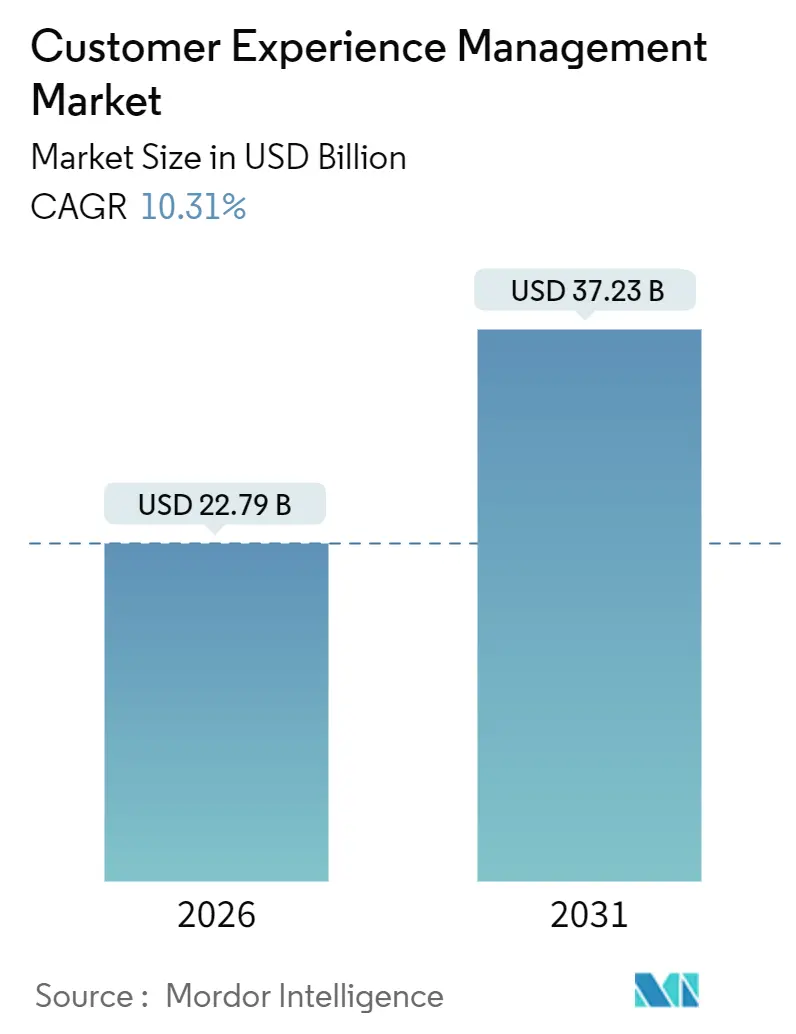

| Market Size (2026) | USD 22.79 Billion |

| Market Size (2031) | USD 37.23 Billion |

| Growth Rate (2026 - 2031) | 10.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Customer Experience Management Market Analysis by Mordor Intelligence

The customer experience management market size stands at USD 22.79 billion in 2026 and is projected to reach USD 37.23 billion by 2031, registering a 10.31% CAGR across the forecast period. Rising investments in predictive orchestration, the shift from third-party cookies to first-party data, and rapid advances in generative AI are redefining how enterprises collect, analyze, and act on feedback. Cloud delivery models shorten upgrade cycles, while agentic AI solutions automate routine service requests and free live agents for higher-value interactions. Companies are also embracing composable architectures that integrate best-of-breed modules without wholesale platform swaps. At the same time, privacy regulations and mounting security concerns push vendors to embed compliance controls and encryption by design, reinforcing buyer confidence.

Key Report Takeaways

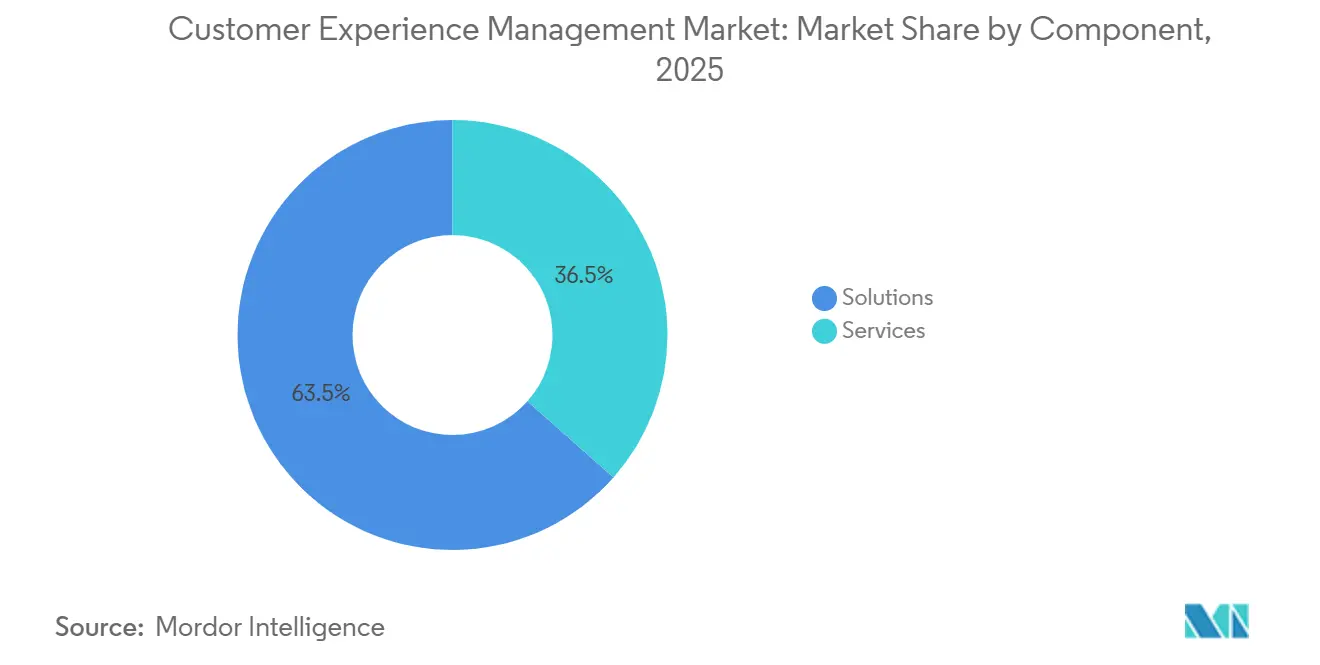

- By component, solutions led with 63.47% revenue in 2025, whereas services are advancing at an 11.03% CAGR to 2031.

- By deployment, cloud accounted for 77.39% share of the customer experience management market size in 2025 and is expanding at a 10.42% CAGR through 2031.

- By organization size, large enterprises commanded 60.76% of the customer experience management market share in 2025, while small and medium enterprises are growing at an 11.32% CAGR to 2031.

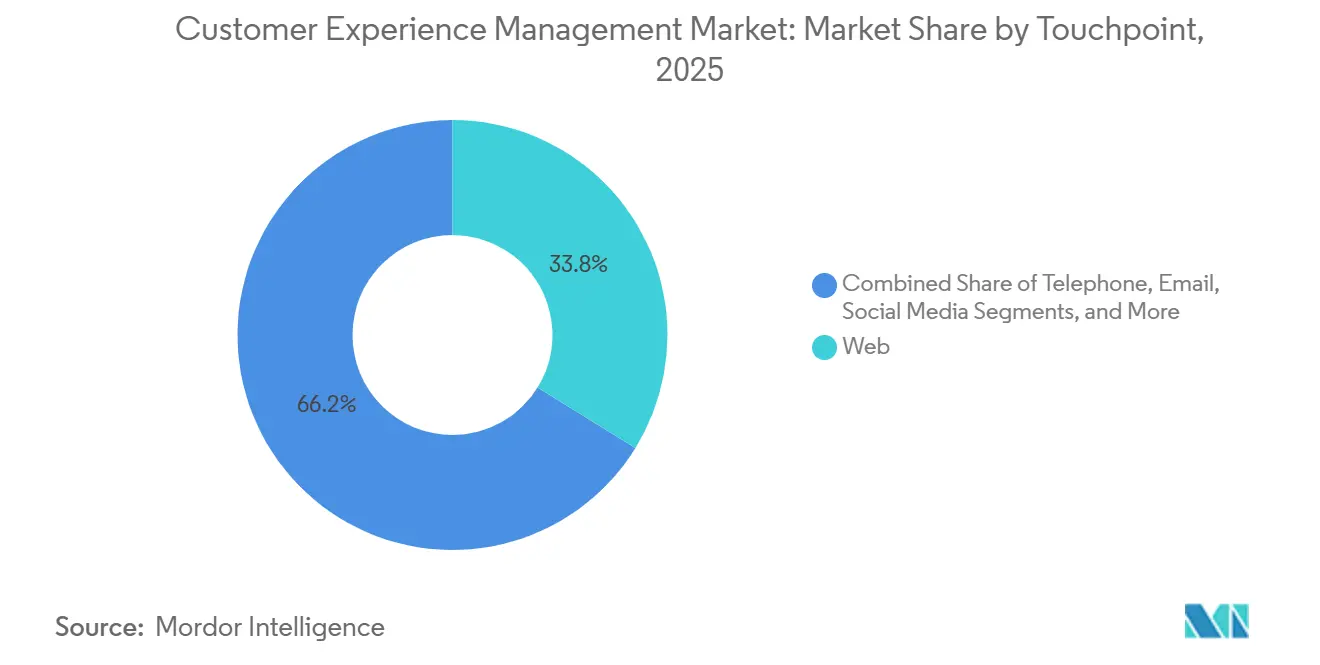

- By touchpoint, web dominated with 33.81% share in 2025; social media is forecast to expand at a 12.27% CAGR during 2026-2031.

- By application, retail and e-commerce held 22.68% revenue in 2025, whereas healthcare posts the fastest 11.86% CAGR to 2031.

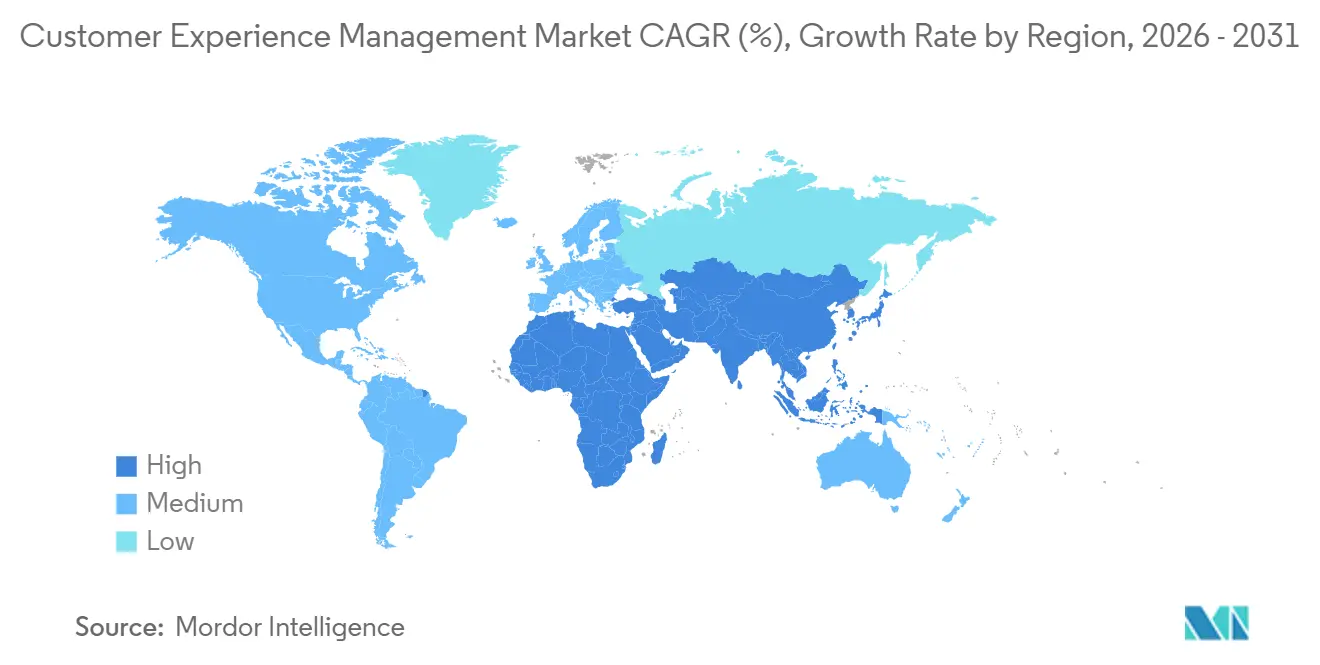

- By geography, North America captured 37.12% revenue in 2025; Asia Pacific leads expansion at a 12.06% CAGR for the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Customer Experience Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Cloud-Based Technology, Advanced Analytics, and Automation | +2.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Growing Demand for Personalized Customer Experience | +2.3% | Global, pronounced in Asia Pacific and North America | Long term (≥4 years) |

| Integration of AI-Powered Chatbots with Omnichannel CX Platforms | +2.1% | Global, early North America and Europe, rapid Asia Pacific | Short term (≤2 years) |

| Monetization of First-Party Data Amid Cookie Deprecation | +1.4% | North America and Europe | Short term (≤2 years) |

| Expansion of CX Analytics into Voice of the Employee Programs | +0.9% | North America and Europe, emerging Asia Pacific | Medium term (2-4 years) |

| Emergence of Customer Data Platforms for Real-Time Personalization | +1.6% | Global, strong in retail and e-commerce | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud-Based Technology, Advanced Analytics, and Automation

Subscription-based cloud platforms eliminate the capital cost of servers and accelerate feature releases, allowing vendors to push sentiment analysis, predictive routing, and proactive quality monitoring to customers without downtime.[1]Adobe Inc., “What Is Customer Experience Management,” business.adobe.com Elastic infrastructure scales automatically with interaction volume, and usage-aligned pricing appeals to mid-market firms that previously deferred CX upgrades. Machine-learning models now ingest voice, chat, and social posts to surface churn risks in near real time, letting brands intervene before dissatisfaction escalates. Automation extends beyond chatbots, coordinating case escalations and personalized offers across channels. As deployment cycles shrink from quarters to weeks, enterprises recalibrate ROI expectations toward continuous iteration rather than large one-time rollouts.

Growing Demand for Personalized Customer Experience

Consumers expect brands to recognize prior purchases, channel preferences, and real-time intent every time they engage. Unified profiles merge transaction data, behavioral signals, and declared preferences so recommendation engines can tailor content, adjust prices, and refine offers instantly.[2]Federal Trade Commission, “Privacy and Security,” ftc.gov Regulations such as GDPR and the California Consumer Privacy Act require explicit consent, forcing firms to balance personalization ambitions with transparency. Loyalty programs and progressive profiling incentivize users to share data directly, replacing third-party cookies with trusted first-party relationships. Outcomes include higher conversion rates, larger average order values, and deeper engagement that outlasts single promotions.

Integration of AI-Powered Chatbots with Omnichannel CX Platforms

Generative AI elevates chatbots from scripted responders to conversational agents that understand nuanced questions, access enterprise knowledge bases, and execute multi-step tasks without human input.[3]Zendesk Inc., “AI in Customer Service,” zendesk.com Context persists when a customer shifts from web chat to voice or messaging, avoiding repetitive data entry and reducing handle time. Tightly coupled customer data platforms let bots pull inventory, billing, and service histories to resolve up to 40% of inbound queries on first touch. Human agents then focus on emotionally charged, high-value cases, improving morale and service quality simultaneously.

Monetization of First-Party Data Amid Cookie Deprecation

With third-party cookies disappearing, firms are racing to build consented datasets inside customer data platforms that support segmentation, targeting, and outcome measurement without external brokers. Privacy-preserving techniques such as differential privacy allow aggregate analytics while masking individuals, maintaining compliance and customer trust. Industries with direct consumer relationships, retail, subscription media, banking, gain a competitive edge as they harvest richer behavioral and transactional insight. Transparent data usage policies coupled with clear value exchanges drive higher opt-in rates and create durable engagement loops.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and Data Security Issues | -1.2% | Global, stringent in Europe and North America | Long term (≥4 years) |

| Vendor Lock-In Across Multi-Cloud CX Stacks | -0.8% | Global, impacting complex architectures | Medium term (2-4 years) |

| Talent Shortage in Advanced CX Analytics and Data Science | -0.7% | Global, acute in North America and Europe | Long term (≥4 years) |

| High Total Cost of Ownership for End-to-End CX Suites in SMEs | -0.6% | Global, affecting small and medium enterprises | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Privacy and Data Security Issues

Large-scale breaches and stiff penalties transform privacy from compliance checkbox to board-level risk, as GDPR fines can reach 4% of global revenue and U.S. regulators acquire extended enforcement authority. Customer experience platforms consolidate payment, health, and location data, creating rich but attractive attack surfaces. Zero-trust security, encryption in motion and at rest, and continuous monitoring raise deployment complexity and prolong project timelines. Firms sometimes anonymize or aggregate data, but reduced granularity can blunt personalization precision and dilute insight quality.

Vendor Lock-In Across Multi-Cloud CX Stacks

Best-of-breed adoption can produce siloed data schemas and proprietary workflow engines that increase switching costs when performance disappoints.[4]Oracle Corporation, “What Is CRM,” oracle.com Migration often involves re-mapping millions of records, retraining staff, and renegotiating contracts, which encourages inertia even in the face of better alternatives. Adopting open standards and event-driven architectures mitigates lock-in but requires advanced integration skills. Enterprises therefore weigh flexibility against simplicity, selecting vendors that support transparent data export and composable modules to avoid long-term captivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Expand as Integration Complexity Rises

Solutions secured 63.47% revenue in 2025 thanks to experience analytics, journey mapping, and social listening modules that transform unstructured feedback into strategic insight. Services are poised for an 11.03% CAGR through 2031 as organizations need experts to meld cloud platforms with legacy CRM, customize dashboards, and operationalize insights. Professional services dominate early phases, guiding data migration, user training, and governance. Over time, managed services gain favor, offloading routine maintenance so internal teams can focus on strategy. Experience analytics now applies machine learning to predict churn and detect upsell moments, yet value creation still depends on analysts who translate model output into action. Customer journey mapping highlights friction and opportunity along multi-step paths, while real-time social monitoring sharpens brand response to emerging trends. The convergence of these functions into unified suites reduces point-solution sprawl, but seamless information flow keeps integration partners indispensable.

The customer experience management market continues to reward vendors that package robust API libraries and low-code connectors, letting partners orchestrate data across disparate systems. As more enterprises embrace end-to-end platforms, service providers move upstream, offering change-management guidance, value-realization analytics, and continuous optimization. The trend underpins double-digit growth for the services segment and cements its role as a critical enabler of long-term platform success.

By Deployment: Cloud Dominance Reflects Agility and Subscription Economics

Cloud deployments captured 77.39% revenue in 2025 and are expected to retain momentum with a 10.42% CAGR, propelled by operating-expense conversion, instant scalability, and continuous feature access. Vendors roll out new AI models, compliance updates, and UI enhancements with no customer downtime, removing upgrade headaches that plagued on-premise environments. Elastic capacity absorbs holiday peaks or viral campaigns without pre-purchasing excess hardware. Multi-tenant architecture lowers per-seat cost, letting mid-size firms tap enterprise-grade capabilities. Highly regulated sectors still maintain data residency or latency mandates, preserving a niche for on-premise or private cloud builds, but hybrid models bridge the gap by retaining sensitive data behind the firewall while analytics run in public clouds.

Competitive focus now shifts from infrastructure to analytics depth, integration breadth, and user experience. The customer experience management market size tied to cloud platforms benefits from faster onboarding and simplified proof-of-concepts, letting buyers test value quickly. Nonetheless, buyers scrutinize vendor service-level agreements, exit clauses, and data portability to avoid future constraints. Open APIs and event streaming frameworks thus become decisive in vendor selection.

By Organization Size: SMEs Embrace Modular Platforms to Level the Playing Field

Large enterprises owned 60.76% share in 2025, leveraging global footprints to negotiate enterprise licenses and implement cross-channel orchestration. Small and medium enterprises show an 11.32% CAGR trajectory, attracted by modular pricing, pre-configured templates, and rapid configuration options. Vendors disaggregate monolithic suites into chatbot, ticketing, or analytics modules that SMEs can activate as budgets allow. Subscription alignment with usage shields limited budgets from heavy upfront commitments. Pre-trained AI services for sentiment, intent, and routing bypass in-house data-science gaps, enabling smaller firms to match personalization quality seen at global brands.

Despite technology access parity, SMEs still grapple with change management, data hygiene, and skill shortages. Successful deployments involve gradual rollout, focused metrics, and staff upskilling. Vendors that provide guided onboarding, knowledge centers, and community support build loyalty and reduce churn. Over the forecast window, the customer experience management market will see SMEs driving incremental platform innovation as feedback loops from thousands of smaller deployments inform roadmap evolution.

By Touchpoint: Social Media Surges as Commerce and Support Converge

Web portals held 33.81% share in 2025, anchoring self-service knowledge, account management, and form-based interactions. Social media registers a robust 12.27% CAGR into 2031 as commerce, community, and customer care coalesce within Instagram, WeChat, and WhatsApp ecosystems. Brands embed product catalogs, checkout, and post-purchase support directly inside feeds, reducing friction and exploiting impulse purchases. Conversational commerce blends AI assistants and live agents to guide choices and resolve issues within a single thread. Voice and in-store channels retain importance for complex or emotion-laden engagements where live dialogue or tactile experience matters. Email endures for asynchronous exchanges that require detailed documentation.

Uniform customer context across channels remains the holy grail. The customer experience management market in social and messaging channels depends on API connectors, real-time data pipelines, and unified identity resolution to hand off context seamlessly. Companies that harmonize experience across web, social, and physical touchpoints see higher satisfaction and brand advocacy.

By Application: Healthcare Leads Growth as Experience Becomes a Competitive Differentiator

Retail and e-commerce generated 22.68% revenue in 2025 by deploying real-time personalization engines, abandoned-cart recovery flows, and loyalty campaigns that extend lifetime value. Healthcare accelerates at 11.86% CAGR as providers integrate patient portals, telehealth, and transparent billing to comply with regulation and win patient loyalty. Unified experience platforms overlay electronic health records with secure messaging and appointment scheduling, streamlining the care journey. Financial services adopt fraud monitoring chats and personalized advice tools to retain clients in markets where switching is easy. Telecommunications operators use predictive models to mitigate churn linked to service disruptions by proactively engaging customers.

Manufacturers extend experience management to distributors and service partners, recognizing downstream satisfaction drives upstream orders. Public agencies digitize citizen services, reducing queue times and boosting trust. Travel and transport companies deploy real-time disruption alerts, rebooking flows, and wallet-linked loyalty, raising retention in margin-thin industries. The customer experience management market thus spans consumer, enterprise, and public-sector domains, each with sector-specific workflows but unified by the need for frictionless, personalized engagement.

Geography Analysis

North America controlled 37.12% revenue in 2025, underpinned by early cloud migration, strict privacy laws, and competitive differentiation grounded in experience quality. Enterprises pioneer omnichannel orchestration, advanced analytics, and AI-driven automation to counter high labor costs and rising service expectations. Regulations such as the California Consumer Privacy Act compel transparency, driving investment in consent management and encryption. Europe follows with strong compliance culture anchored in GDPR, which sets global benchmarks for consent, portability, and breach notification. The continent’s linguistic and cultural diversity heightens demand for localization engines that adapt tone, offers, and workflows across markets.

Asia Pacific expands at a brisk 12.06% CAGR, propelled by mobile-first consumers, super-app ecosystems, and government stimuli that push digital commerce. China’s mini-program frameworks let brands launch full-fledged experiences inside WeChat without dedicated apps, while India’s Unified Payments Interface normalizes instant digital payments across urban and rural settings. Southeast Asian marketplaces integrate customer service chat, delivery tracking, and returns workflows directly into shopping apps, raising user expectations. The Middle East invests in smart city projects and tourism technology, prioritizing seamless digital touchpoints for residents and visitors alike. Africa’s growth remains tempered by network and payment infrastructure gaps, yet mobile money and social commerce foster leap-frog adoption.

These regional dynamics reinforce the customer experience management market’s need for flexible deployment, multi-lingual AI models, and compliance toolkits that adjust to local statutes. Vendors with global footprints forge regional data centers and tailored industry accelerators to secure mindshare and wallet share.

Competitive Landscape

The customer experience management market presents moderate concentration. Enterprise software majors such as Adobe, Salesforce, Oracle, and SAP extend core CRM offerings into experience analytics by funneling vast R&D budgets into AI, workflow orchestration, and industry templates. Specialist providers including Qualtrics, Medallia, and NICE counterbalance by focusing on depth in sentiment analytics, closed-loop actioning, and verticalized packages. Consolidation accelerates as both camps acquire niche players for conversational AI, workforce optimization, or social commerce features, yet the market remains open enough for regional and vertical innovators.

Competitive strategy centers on extensibility. Vendors court developers with open APIs, software development kits, and marketplace ecosystems that seed third-party connectors and micro-apps. Low-code configuration reduces deployment timelines from months to weeks, giving sellers a clear differentiator in proof-of-value cycles. Generative AI emerges as the new battleground, with pre-trained language and vision models that slash data-labeling overhead and deliver out-of-the-box insight. Governance and ethical AI assurances become decision criteria as customers seek transparency and bias mitigation.

Talent scarcity intensifies rivalry for data scientists and ML engineers who refine industry-specific models and maintain explainability. To offset resource constraints, vendors package pre-tuned vertical solutions, channel partnerships, and managed service offerings. Ultimately, long-term winners balance innovation velocity with open data policies that prevent lock-in, satisfying buyers wary of platform captivity.

Customer Experience Management Industry Leaders

Adobe Inc

Oracle Corporation

SAP SE

IBM Corporation

Avaya Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Zendesk completed its acquisition of Ultimate AI, integrating multilingual conversational agents that handle complex multi-turn dialogues across 109 languages.

- October 2025: Microsoft enriched Dynamics 365 Customer Service with Copilot-powered autonomous agents that resolve cases and update records automatically.

- September 2025: SAP embedded Joule generative AI into SAP Customer Experience, delivering predictive service recommendations and automated order management.

- August 2025: Genesys partnered with Google Cloud to add Vertex AI sentiment analysis and predictive routing to Genesys Cloud CX.

Global Customer Experience Management Market Report Scope

Customer experience management, abbreviated as CEM or CXM, is a collection of processes an organization utilizes to track, oversee, and organize the interactions between a customer and the company throughout the customer lifecycle. The scope of the study focuses on key regions such as North America, Europe, and Asia-Pacific, in addition to Latin America and Middle East & Africa.

The Customer Experience Management Market Report is Segmented by Component (Solutions including Experience Analytics, Customer Journey Mapping, Social Media Monitoring, Text and Speech Analytics; Services including Professional Services and Managed Services), Deployment (Cloud and On-Premise), Organization Size (Small and Medium Enterprises and Large Enterprises), Touchpoint (Telephone, Email, Web, Social Media, and Other Touchpoints), Application (Banking Financial Services and Insurance, Retail and E-Commerce, Information Technology and Telecommunication, Healthcare, Manufacturing, Government, Travel and Transportation, and Other Applications), and Geography (North America, Europe, Asia Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Experience Analytics |

| Customer Journey Mapping | |

| Social Media Monitoring | |

| Text and Speech Analytics | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-Premise |

| Small and Medium Enterprises |

| Large Enterprises |

| Telephone |

| Web |

| Social Media |

| Other Touchpoints |

| Banking, Financial Services, and Insurance |

| Retail and E-Commerce |

| Information Technology and Telecommunication |

| Healthcare |

| Manufacturing |

| Government |

| Travel and Transportation |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Sweden | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Solutions | Experience Analytics |

| Customer Journey Mapping | ||

| Social Media Monitoring | ||

| Text and Speech Analytics | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment | Cloud | |

| On-Premise | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Touchpoint | Telephone | |

| Web | ||

| Social Media | ||

| Other Touchpoints | ||

| By Application | Banking, Financial Services, and Insurance | |

| Retail and E-Commerce | ||

| Information Technology and Telecommunication | ||

| Healthcare | ||

| Manufacturing | ||

| Government | ||

| Travel and Transportation | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Sweden | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the customer experience management market in 2031?

The market is expected to reach USD 37.23 billion by 2031.

Which deployment model leads adoption of customer experience management platforms?

Cloud deployment captured 77.39% revenue in 2025 and continues to expand at a 10.42% CAGR.

Which region registers the fastest growth in customer experience investments?

Asia Pacific posts a 12.06% CAGR thanks to mobile-first consumers and government digital initiatives.

Which industry shows the strongest growth momentum for CX spending?

Healthcare advances at an 11.86% CAGR as patient portals, telehealth, and transparency mandates take hold.

Why are enterprises concerned about vendor lock-in in CX technology?

Proprietary APIs and data schemas can raise switching costs, so buyers favor open standards and modular architectures.

How does generative AI change customer service operations?

It powers autonomous agents that resolve routine cases, freeing human teams for complex issues and shortening handle times.

Page last updated on: