Critical Communication Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

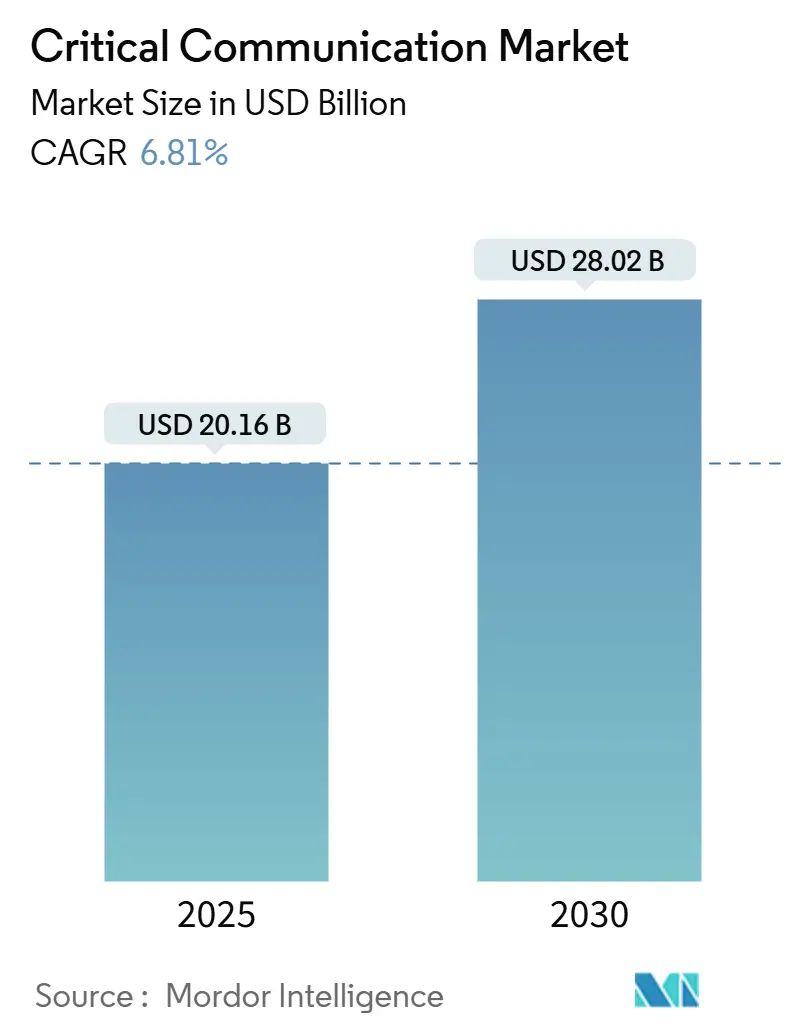

| Market Size (2025) | USD 20.16 Billion |

| Market Size (2030) | USD 28.02 Billion |

| Growth Rate (2025 - 2030) | 6.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Critical Communication Market Analysis by Mordor Intelligence

The critical communication market size stood at USD 20.16 billion in 2025 and is forecast to reach USD 28.02 billion by 2030, advancing at a 6.81% CAGR over the period. Rising investments in broadband public-safety networks, growing regulatory pressure for 99.999% uptime, and the shift from voice-centric Land Mobile Radio (LMR) to data-rich 5G Mission-Critical Services (MCX) have strengthened demand. The transition is accelerated by nationwide LTE/5G build-outs that enable network slicing and edge analytics, giving agencies new tools for situational awareness. Convergence of terrestrial and satellite networks is addressing coverage gaps in maritime and remote industrial sites, while artificial-intelligence (AI)-enabled dispatch platforms are reshaping procurement criteria toward multimedia analytics. Vendors have responded with hybrid private-commercial architectures and ruggedized edge nodes that keep services operational during core outages.

Key Report Takeaways

- By technology, LMR led with 57.46% of critical communication market share in 2024; 5G MCX is projected to expand at an 8.12% CAGR through 2030.

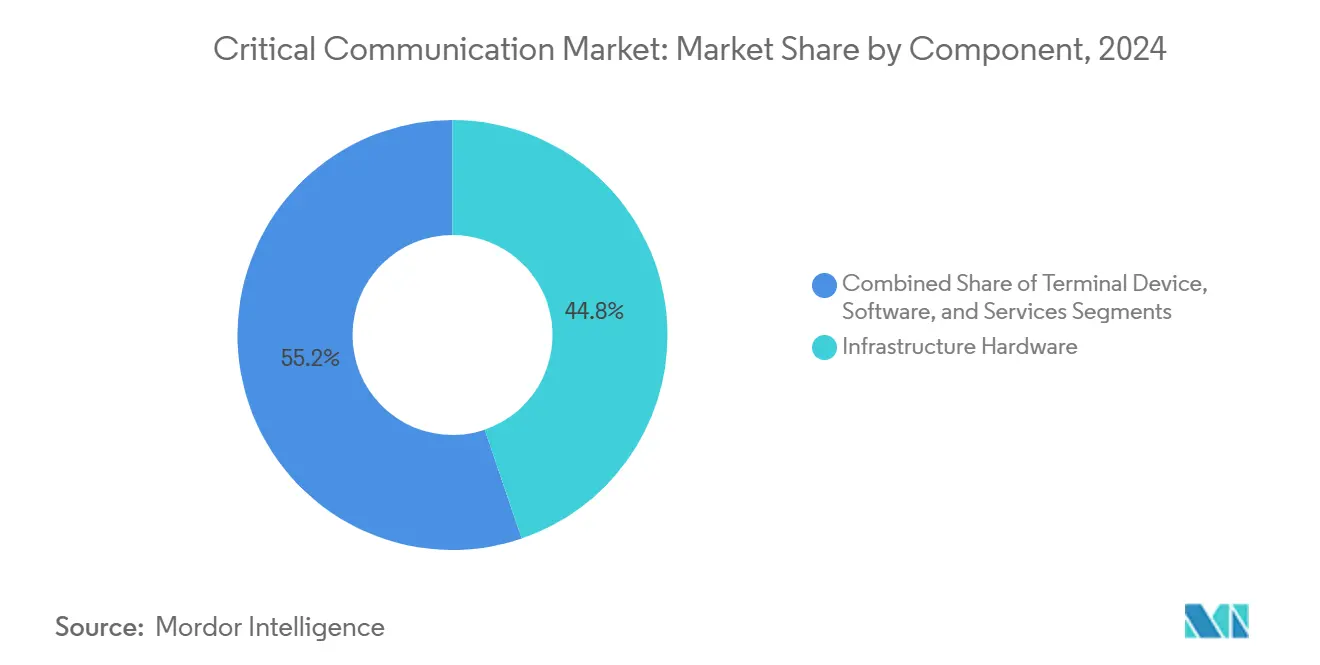

- By component, infrastructure hardware accounted for 44.78% share of the critical communication market size in 2024, while services register the fastest projected CAGR at 7.36%.

- By end-user industry, public safety and emergency services held 62.42% share in 2024; utilities and energy is forecast to advance at a 7.87% CAGR to 2030.

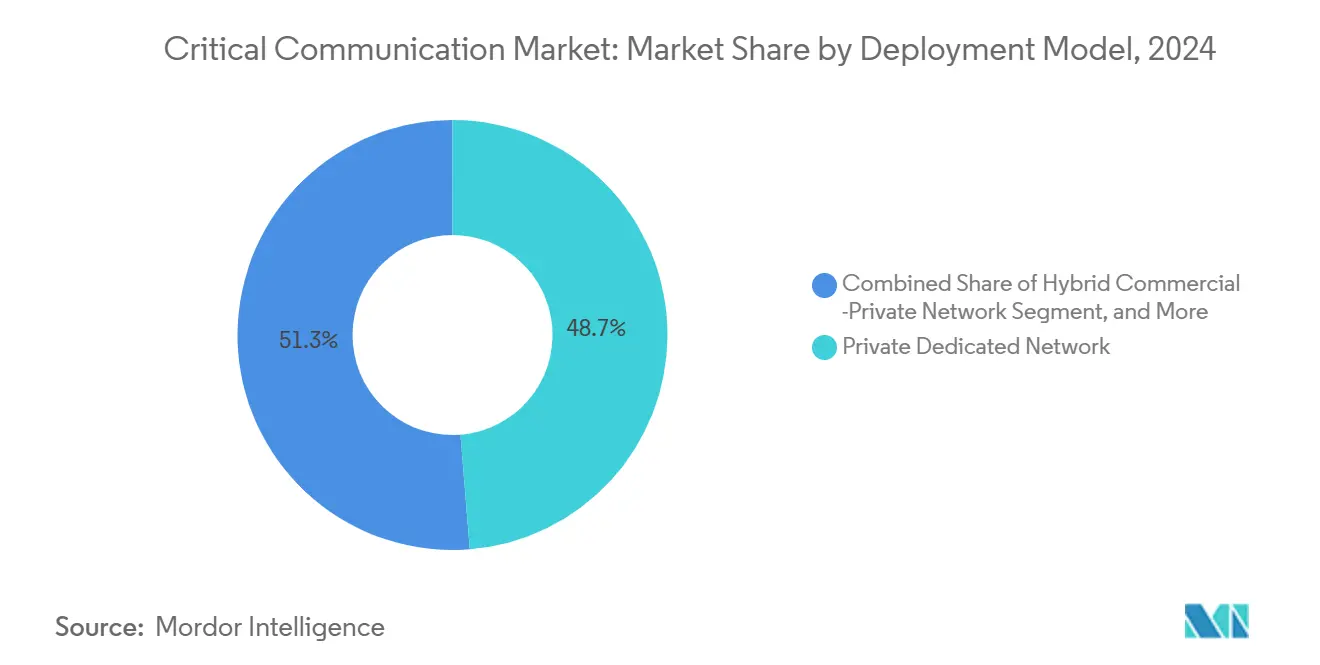

- By deployment model, private dedicated networks captured 48.73% share of the critical communication market size in 2024, whereas hybrid commercial-private models show the highest projected CAGR at 7.95%.

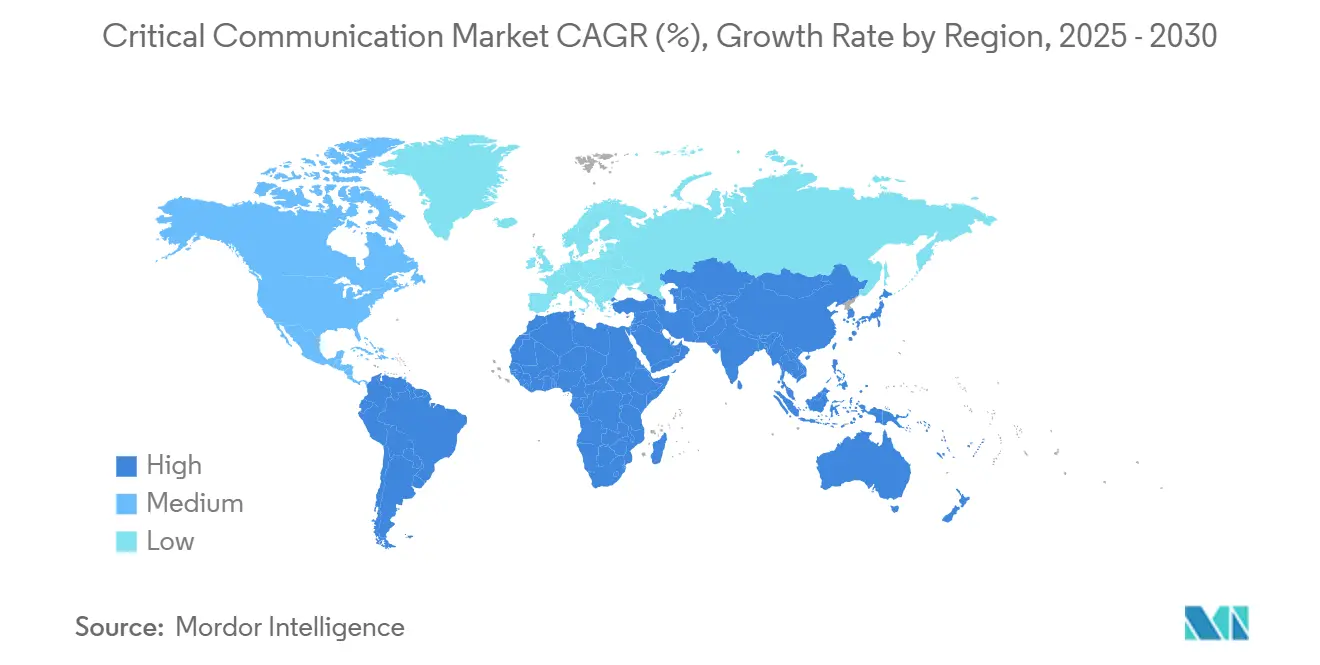

- By geography, North America commanded 34.93% of the critical communication market share in 2024; Asia-Pacific is the fastest-growing region with a 7.47% CAGR through 2030.

Global Critical Communication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide LTE/5G public-safety build-outs | +1.2% | North America, Europe, Asia Pacific core | Medium term (2-4 years) |

| Digital switchover of legacy LMR to P25/TETRA | +0.8% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Mandated PSBN uptime of 99.999% | +1.1% | North America, spill-over to Europe | Short term (≤ 2 years) |

| Edge-deployed AI situational-awareness apps driving MCX adoption | +1.4% | Global, early adoption in North America and Asia Pacific | Medium term (2-4 years) |

| Private 5G slices for critical infrastructure cyber-hardening | +0.9% | Asia Pacific core, North America, Europe | Medium term (2-4 years) |

| Global maritime GMDSS modernisation to LTE/5G NTN | +0.7% | Global, with emphasis on maritime regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nationwide LTE/5G public-safety build-outs

FirstNet invested USD 8 billion to add 1,000 cell sites by early 2025, pushing broadband coverage into rural and tribal zones.[1]AT&T, “1,000 New FirstNet Sites,” about.att.com Stand-alone 5G cores enable deterministic network slicing so agencies can lock-in quality-of-service levels once reserved for specialized LMR systems. Greater coverage fuels device uptake, and every new subscription raises revenues earmarked for further rural builds, creating a self-reinforcing growth loop. CBRS spectrum sharing keeps costs manageable for smaller departments that cannot win low-band auctions.[2]Federal Communications Commission, “Promoting Investment in the 3550-3700 MHz Band,” federalregister.gov Interoperability frameworks forged in North America are now being mirrored in Europe and Asia, accelerating global standard alignment.

Digital switchover of legacy LMR to P25/TETRA

Mandatory migration to Project 25 Phase 2 in North America and TETRA Evolution in Europe is driving an extended refresh cycle. Dual-mode radios allow users to roam between legacy and broadband systems, but gateways that translate circuit- to packet-switched calls add integration complexity. Agencies must pass multi-vendor interoperability tests before go-live, stretching procurement timelines. Nonetheless, newer digital radios offer stronger encryption and better audio in high-noise environments, prompting phased replacements even among budget-constrained departments. The overall effect is steady hardware sales plus rising demand for migration consulting services.

Mandated PSBN uptime of 99.999%

Regulations now limit network downtime to 5.26 minutes per year, forcing operators to deploy N+1 cores, diverse backhaul, and portable deployable network assets. Edge clouds host critical applications so field users can keep operating even if the main core fails. Satellite backhaul provides resilience at remote sites, and costs are dropping as new low-earth-orbit constellations gain scale. Equipment vendors offering proven redundancy designs enjoy a procurement edge, especially when they bundle automated fail-over orchestration in managed-service contracts.

Edge-deployed AI situational-awareness apps

AI modules running on tower-top servers now filter massive video and sensor streams before backhaul, cutting latency and traffic by half. Platforms like Motorola Solutions’ CommandCentral automatically prioritize calls and detect threats in live feeds, enabling dispatchers to intervene faster. Standardized APIs let third parties plug in domain-specific analytics, for example, chemical leak detection for utilities or fall detection for health responders. Agencies increasingly score vendor bids on AI capability as much as on basic voice performance, tilting market momentum toward software-centric suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum scarcity below 1 GHz | -0.6% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| High capex for nationwide trunked network refresh | -0.4% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Certification backlog for MCX-capable chipsets | -0.3% | Global, with regulatory variations by region | Short term (≤ 2 years) |

| Limited QoS guarantees on commercial 5G SA networks | -0.2% | Global, early 5G deployment regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Spectrum scarcity below 1 GHz

Sub-1 GHz bands excel at wide-area coverage, yet allocations remain contested among public-safety, broadcast, and commercial 4G/5G users. The 2024 United States National Spectrum Strategy admitted that current allotments cannot simultaneously support legacy LMR and new broadband needs.[3]National Telecommunications and Information Administration, “National Spectrum Strategy,” ntia.gov Agencies forced to shift up to CBRS or mmWave must densify infrastructure, multiplying tower counts and costs. Dynamic sharing frameworks promise relief but require complex interference-avoidance rules that slow rollouts. Europe faces similar congestion, with several member states delaying digital switchover until extra sub-1 GHz channels free up.

High capex for nationwide trunked network refresh

FirstNet’s USD 6.3 billion, 10-year upgrade budget highlights the magnitude of cash required for hardened sites, backup power, and secure cores. Smaller jurisdictions struggle to finance even partial modernizations, leading to patchwork systems that compromise mutual aid. Certification standards demand tougher radios and routers, boosting unit prices 30-50% over commercial gear. Managed-service contracts spread costs but lock agencies into vendors for years, posing obsolescence risks if standards evolve faster than expected.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services-led growth outperforms hardware replacement

Hardware such as eNBs, gNBs, and RF repeaters held 44.78% of critical communication market share in 2024. Managed and professional services, however, are projected to expand 7.36% annually as agencies outsource network operations to guarantee 99.999% availability. Multivendor integration complexity elevates demand for lifecycle management offerings that bundle performance metrics, security patching, and capacity upgrades into single contracts. Meanwhile, software subscriptions are becoming the revenue engine for suppliers; AI-driven dispatch analytics, for example, transform incident data into operational insights sold on tiered licenses.

Terminal devices are evolving into rugged smart-edge nodes carrying AI inference accelerators and multi-band antennas. Battery technology advances, especially silicon-anode cells, extend shift-length operating time despite heavier processing loads. Over time, the combined pull of device refresh cycles and recurring software fees positions services to outpace hardware revenue, establishing a stable annuity business for vendors and partners.

By Technology: Transition from LMR to 5G MCX gains momentum

LMR preserved 57.46% of the critical communication market size in 2024, underscoring its role as the reliability benchmark for voice in harsh conditions. Yet 5G MCX, growing at 8.12% CAGR, is rapidly redefining expectations with unified voice, data, and video on a single broadband platform. The integration of MCPTT, MCData, and MCVideo within 3GPP Release 17 devices eliminates multi-radio overhead, cutting total cost of ownership for agencies that previously ran parallel LMR and LTE networks. Satellite and other non-terrestrial links extend broadband coverage across oceans and deserts, a critical factor for coast guards and mining operators upgrading from HF radio.

Continued support for Digital Mobile Radio and NXDN in industrial settings illustrates a bifurcated landscape where simplicity and low cost still trump sophistication for some users. The coexistence of Wi-Fi 6E and private 5G inside buildings guarantees signal redundancy, while device makers race to certify tri-mode handhelds that can hop between LMR, LTE, and Wi-Fi without call drops. Over the forecast period, the critical communication market will witness legacy LMR volumes declining modestly, but complementary future-proof radios will keep the installed base significant even as broadband solutions dominate new orders.

By Deployment Model: Hybrid architectures optimize cost and priority access

Private dedicated setups captured 48.73% of critical communication market share in 2024, reflecting the historical need for full operational control. Hybrid commercial-private networks, up 7.95% CAGR, allow agencies to offload non-critical traffic onto commercial 5G while reserving isolated slices for emergencies. The model lowers capex yet adheres to stringent SLA terms that penalize outages. Edge compute clusters in police vehicles and fire stations ensure that high-priority applications continue functioning if commercial cores fail.

Public MNO mission-critical services find uptake among smaller departments that cannot finance their own spectrum or core, but reliability concerns linger. Regulators are drafting enforcement regimes to hold carriers accountable during crises, a move expected to unlock additional adoption in 2027-2030. Overall, flexible architectural choices align with budget realities while meeting uptime mandates, pushing the critical communication market toward dynamic multi-domain orchestration.

By End-User Industry: Utilities lead diversification beyond public safety

Public safety agencies commanded 62.42% share in 2024, but utilities and energy operators are adding momentum at a 7.87% CAGR as grid resilience priorities escalate. Smart-grid deployments require sub-50 millisecond latency for protection relays; private 5G slices guarantee this level while insulating operations from cyberattacks riding on public networks. Transmission-line teams leverage push-to-video for live fault inspection, cutting outage durations. Similar broadband demand is surfacing in wind-farm maintenance and offshore platforms where lone-worker safety regulations mandate real-time biometrics.

Defense and transportation sectors continue to pioneer hardened encryption and anti-jam waveforms that later filter into civilian products. Industrial manufacturing invests in private networks for robotics and predictive maintenance, fueling a secondary wave of demand for AI-enabled data analytics. As these verticals mature, the critical communication industry can claim a broader mission footprint, with public safety acting as anchor tenant but not sole growth engine.

Geography Analysis

North America retained 34.93% of critical communication market share in 2024 thanks to the United States’ FirstNet modernization and Canada’s P25 interoperability focus. The United States Department of Defense demonstrated dynamic spectrum sharing in the 3.1-3.45 GHz band, setting a global precedent for civil-military coexistence. Federal Communications Commission rulemakings on CBRS, 4.9 GHz, and UAS spectrum continued to expand resources for public-safety and critical-infrastructure users. Vendors in the region benefit from early 5G SA deployments, giving them a head start in certifying devices that meet MCX performance and cybersecurity requirements.

Asia Pacific posted the fastest CAGR at 7.47%. Japan liberalized local 5G spectrum, enabling factories and utility plants to roll out private broadband without carrier coordination. China’s industrial automation surge, amplified by state incentives, is fueling nationwide demand for private 5G and satellite backhaul in mining and oil fields. South Korea’s smart-city pilots integrate critical communication networks with traffic-management systems, showcasing multimedia dispatch at urban scale. Australia’s remote-area needs propel hybrid terrestrial-satellite solutions, while India’s Digital India blueprint earmarks spectrum for disaster-resilient communications, inviting cost-efficient multi-vendor solutions.

Europe balances harmonization and sovereignty. Germany’s Industry 4.0 leadership emphasizes private 5G inside automotive plants, while France requires domestic technology stacks for sensitive sectors. The European Union Critical Communication System initiative seeks to align cross-border interoperability, lowering procurement barriers. The United Kingdom, operating outside European Union rule-making, experiments with shared-access spectrum to speed deployments. Eastern European countries modernize networks largely with European vendors to reduce geopolitical risk, whereas the Nordics pilot non-terrestrial 5G links for energy and maritime operations. These diverse paths yield a fragmented but innovation-rich landscape that collectively advances the critical communication market.

Competitive Landscape

The market is moderately consolidated around long-established incumbents such as Motorola Solutions, Nokia, Ericsson, and L3Harris. These firms leverage legacy LMR installed bases, patent portfolios, and deep regulatory know-how to defend high-margin service contracts. However, software-defined radio startups and cloud-native MCX platform providers erode lock-in advantages by offering open-RAN gear and API-driven services. Acquisition trends reflect incumbent moves to secure AI analytics talent and edge-computing expertise, exemplified by Motorola Solutions’ purchase of machine-vision specialist Pelco in 2024.

Differentiation is shifting from radio hardware toward orchestration software that guarantees performance across hybrid networks. Vendors with proven network-slicing algorithms win large 5G MCX bids, while those emphasizing proprietary interfaces risk exclusion from multi-vendor RFPs. Patent race intensifies around deterministic 5G uplink scheduling, dynamic spectrum sharing, and secure key management. Regional players in Asia and Europe leverage local manufacturing incentives to gain share, especially in devices certified for explosive atmospheres or railways. The rise of open-source MCX stacks could slash entry barriers by 2027, making service quality and ecosystem partnerships key competitive levers.

White-space opportunities abound in industrial verticals where public-safety incumbents lack operational technology fluency. Edge AI for predictive maintenance and anomaly detection attracts cross-industry collaborations; Nokia and Rockwell Automation, for instance, combine 5G SA with manufacturing analytics for factory automation. As mission-critical and industrial requirements converge, vendor success will hinge on delivering vertical-specific software over resilient wireless backbones.

Critical Communication Industry Leaders

Motorola Solutions Inc.

Nokia Corporation

Huawei Technologies Co., Ltd.

L3Harris Technologies, Inc.

Hytera Communications Corporation Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AT&T completed 1,000 new FirstNet Band 14 sites across 46 United States states

- March 2025: FCC allocated 2360-2395 MHz spectrum for non-federal space-launch telemetry

- February 2025: FirstNet Authority and AT&T unveiled a USD 8 billion, 10-year upgrade plan for full 5G capability

- January 2025: FCC adopted dedicated 5030-5091 MHz rules for unmanned-aircraft control links

Global Critical Communication Market Report Scope

| Infrastructure Hardware (eNB/gNB, Core, Repeaters) |

| Terminal Devices (Hand-portable, Mobile, Wearable) |

| Software (MCX platforms, Dispatch, Analytics) |

| Services (Integration, Managed and Maintenance) |

| Land Mobile Radio (Analog, P25, TETRA, DMR, dPMR, NXDN) |

| Public-Safety LTE (3GPP Rel. 13-15) |

| 5G MCX (MCPTT, MCData, MCVideo) |

| Satellite and NTN Broadband |

| Wi-Fi 6/6E and Future Wi-Fi 7 for Critical Comms |

| Private Dedicated Network |

| Hybrid Commercial-Private Network |

| Public MNO Mission-Critical Service |

| Public-Safety and Emergency Services |

| Defence and Military |

| Utilities and Energy |

| Transportation and Logistics |

| Mining, Oil and Gas |

| Industrial Manufacturing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Infrastructure Hardware (eNB/gNB, Core, Repeaters) | ||

| Terminal Devices (Hand-portable, Mobile, Wearable) | |||

| Software (MCX platforms, Dispatch, Analytics) | |||

| Services (Integration, Managed and Maintenance) | |||

| By Technology | Land Mobile Radio (Analog, P25, TETRA, DMR, dPMR, NXDN) | ||

| Public-Safety LTE (3GPP Rel. 13-15) | |||

| 5G MCX (MCPTT, MCData, MCVideo) | |||

| Satellite and NTN Broadband | |||

| Wi-Fi 6/6E and Future Wi-Fi 7 for Critical Comms | |||

| By Deployment Model | Private Dedicated Network | ||

| Hybrid Commercial-Private Network | |||

| Public MNO Mission-Critical Service | |||

| By End-User Industry | Public-Safety and Emergency Services | ||

| Defence and Military | |||

| Utilities and Energy | |||

| Transportation and Logistics | |||

| Mining, Oil and Gas | |||

| Industrial Manufacturing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the critical communication market size in 2025?

It reached USD 20.16 billion in 2025.

How fast is the critical communication market expected to grow?

It is projected to expand at a 6.81% CAGR, hitting USD 28.02 billion by 2030.

Which technology segment is growing the quickest?

5G Mission-Critical Services shows the highest growth at an 8.12% CAGR through 2030.

Why are utilities adopting critical communication solutions?

Utilities seek cyber-hardened, low-latency networks for smart-grid operations, driving a 7.87% CAGR in that vertical.

What deployment model offers the best cost-performance mix?

Hybrid commercial-private networks balance capex savings with guaranteed slices, posting a 7.95% CAGR.

Which region will see the fastest growth by 2030?

Asia-Pacific leads with a 7.47% CAGR, spurred by local 5G spectrum liberalization and industrial automation.

Page last updated on: