Critical Care Diagnostics Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

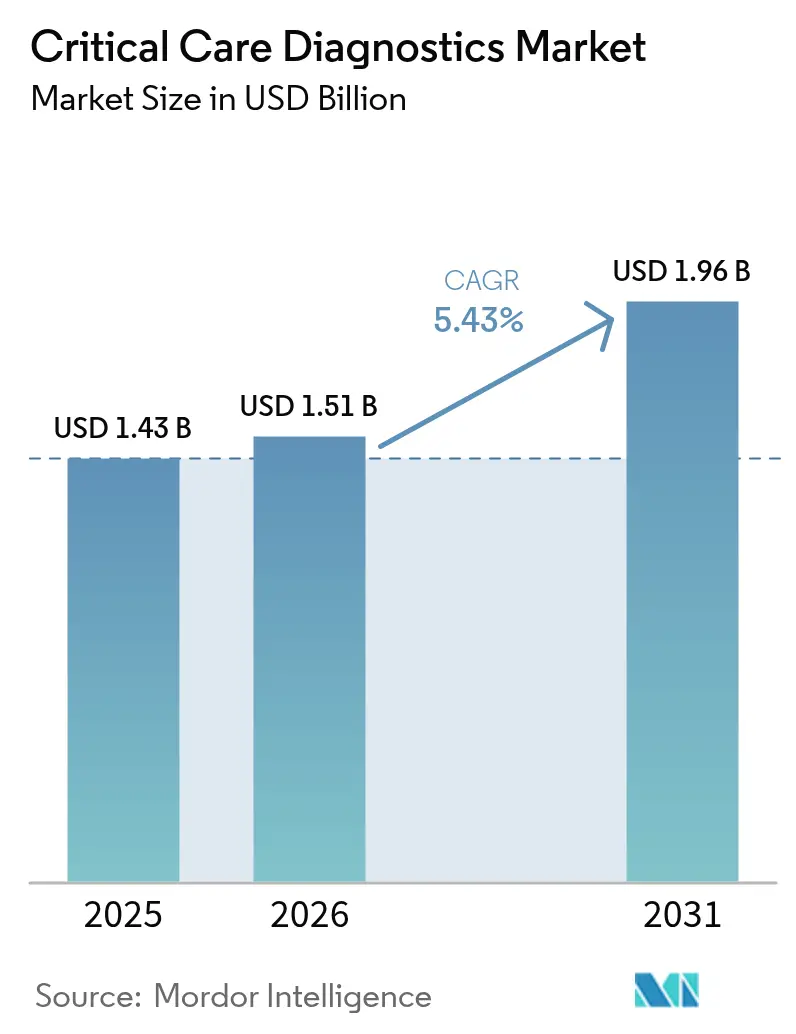

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 1.96 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

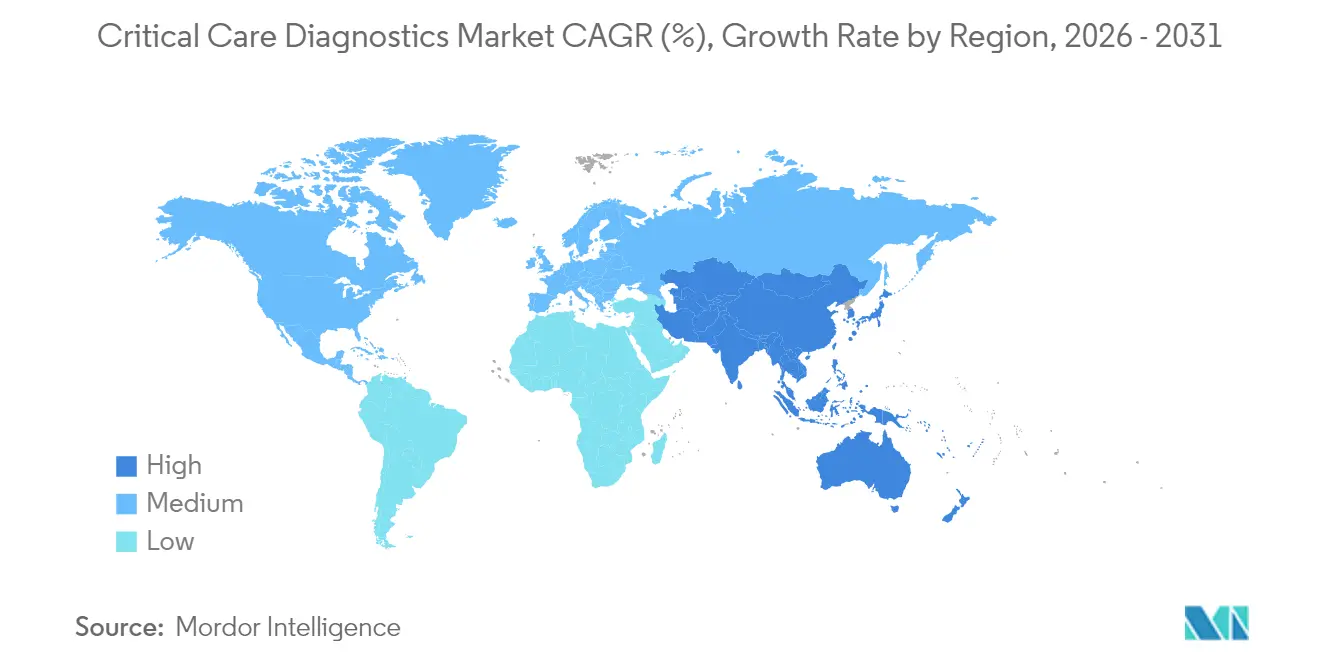

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

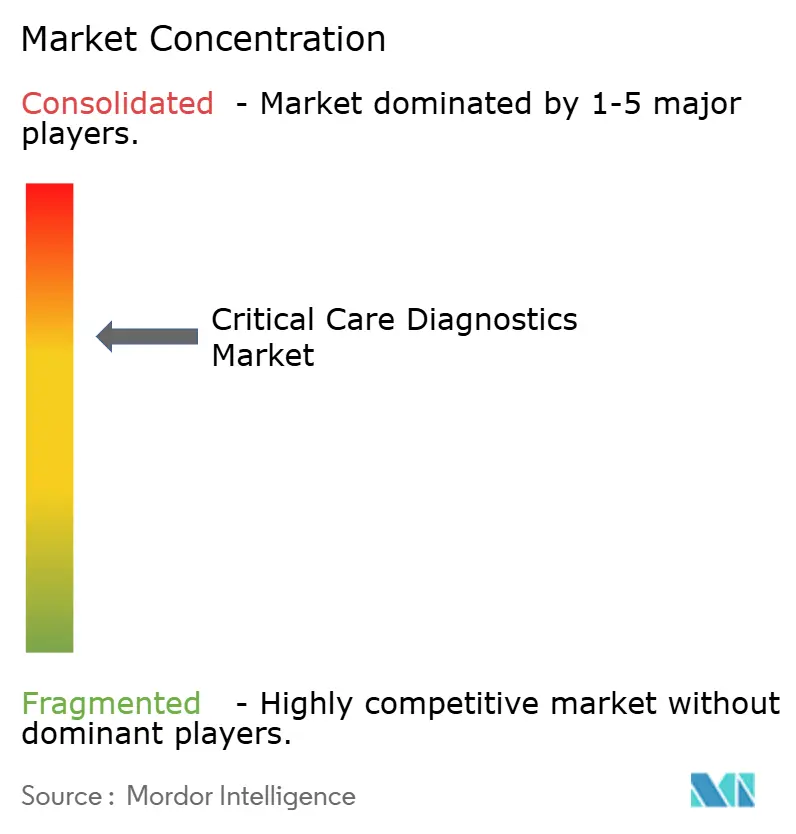

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Critical Care Diagnostics Market Analysis by Mordor Intelligence

The critical care diagnostics market size is expected to grow from USD 1.43 billion in 2025 to USD 1.51 billion in 2026 and is forecast to reach USD 1.96 billion by 2031 at 5.43% CAGR over 2026-2031. Intensifying demand for rapid triage inside intensive care units (ICUs), emergency departments and mobile ICUs keeps bedside analyzers at the center of hospital budgets. Growing sepsis, cardiovascular and acute respiratory caseloads reinforce purchasing momentum for instruments that cut result-turnaround from hours to single-digit minutes. Major health-system digitalization programs now seek analyzers that transmit structured data directly to electronic records while AI dashboards translate longitudinal biomarker trends into actionable care pathways. Capital continues to pour in from public infrastructure expansions across Asia-Pacific and from private-equity financing of start-ups with narrowly focused, ultra-fast pathogen and host-response assays, reshaping competitive dynamics and catalyzing device replacement cycles.

Key Report Takeaways

- By technology, point-of-care systems held 52.02% of critical care diagnostics market share in 2025, while AI-enabled decision-support software is projected to grow at a 7.66% CAGR through 2031.

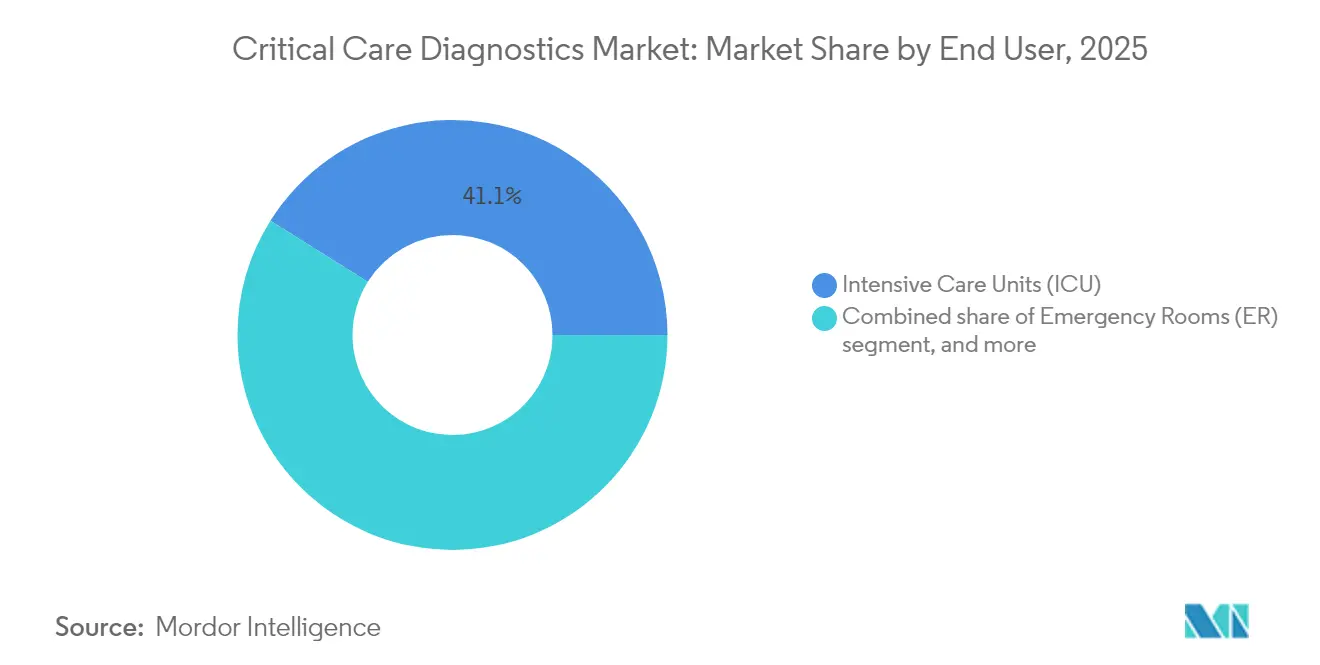

- By end user, ICUs accounted for 41.08% of the critical care diagnostics market size in 2025; ambulance and mobile ICUs are forecast to advance at an 8.56% CAGR between 2026-2031.

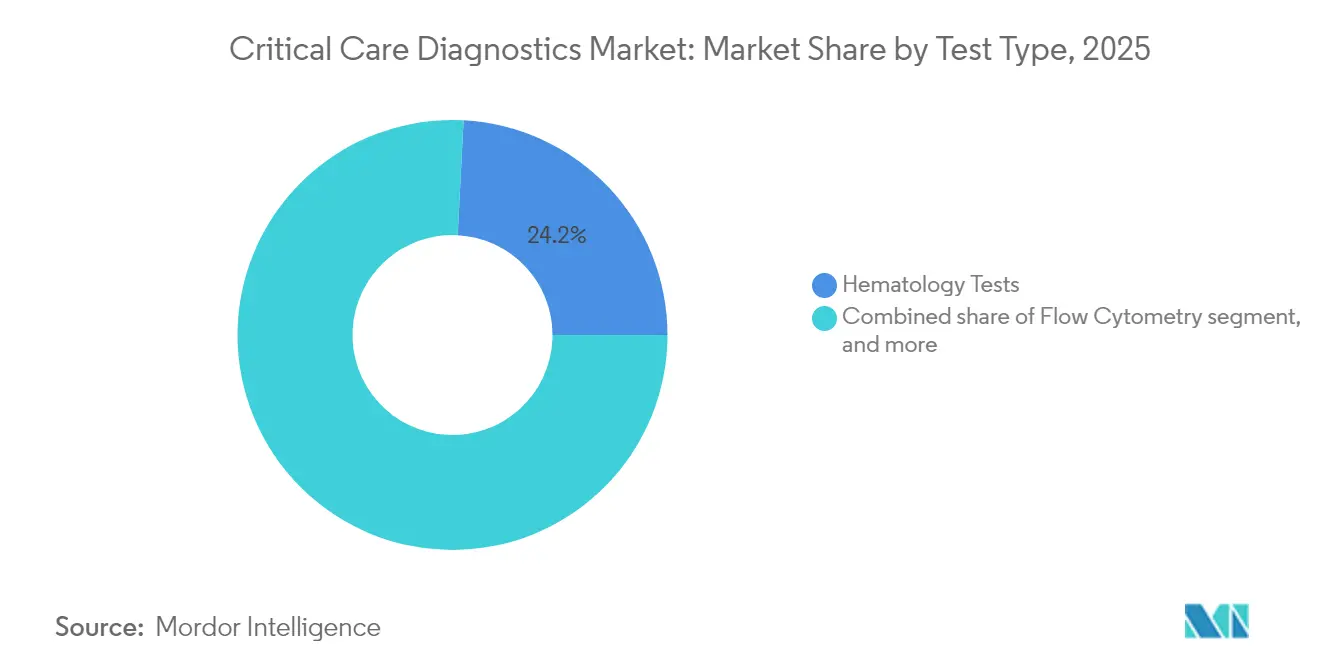

- By test type, hematology led with a 24.18% revenue share in 2025, whereas routine and special chemistry is expected to climb at a 7.54% CAGR to 2031.

- By sample type, whole-blood formats captured 39.95% of 2025 revenue. Plasma and serum applications are forecast to pace growth at an 8.12% CAGR through 2031.

- By geography, North America maintained 42.03% of 2025 revenue; Asia-Pacific is set to expand at a 6.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Critical Care Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of critical illnesses | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Expansion of point-of-care testing | +0.9% | Global, fastest in Asia-Pacific | Medium term (2-4 years) |

| Integration into connected ecosystems | +1.2% | North America, EU | Medium term (2-4 years) |

| Investments in intensive care infrastructure | +0.7% | China, India, MEA | Long term (≥ 4 years) |

| Continuous technology innovation | +0.6% | Global | Short term (≤ 2 years) |

| Value-based care focus on early decisions | +0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Critical Illnesses Requiring Rapid Diagnostics

Sepsis affects more than 1.7 million U.S. adults each year, and mortality jumps when diagnosis is delayed beyond six hours[1]Centers for Disease Control and Prevention, “Sepsis Data & Reports,” cdc.gov. FDA clearance of the MeMed BV host-response test in 2025 enables clinicians to distinguish bacterial from viral infections in under 20 minutes[2]U.S. Food & Drug Administration, “MeMed BV 510(k) Clearance,” fda.gov. Aging populations add multimorbidity to already complex ICU rosters, while emerging markets confront rising trauma and infectious-disease burdens. Predictive algorithms that track high-sensitivity troponin, lactate and procalcitonin can now warn of physiologic decline six to twelve hours before overt symptoms, improving outcomes and reducing resource utilization.

Expansion of Point-of-Care Testing in Acute Care Settings

Hand-held cartridge analyzers eliminate specimen shuttling that previously added 45-90 minutes to turnaround. Devices such as Nova Biomedical’s Stat Profile Prime Plus produce 11-parameter panels from 90 µL of capillary blood, preserving sample volume for hemodynamically unstable patients. Emergency rooms that migrated troponin assays from central labs to bedside platforms report 30-40% shorter throughput times. Portable molecular units introduced during the COVID-19 crisis now equip ambulances, allowing thrombolysis or antibiotic therapy to begin even before hospital doors open.

Integration of Diagnostics into Connected Hospital Ecosystems

Network-ready instruments stream results into electronic records and activate protocol-driven decision support. GE HealthCare’s collaboration with Amazon Web Services will embed generative-AI models that translate unstructured clinical notes into context-aware alerts. Hospitals using closed-loop dashboards have cut unplanned ICU readmissions by up to 20% and identified reagent wastage patterns that save hundreds of thousands of dollars annually.

Government and Private Investments in Intensive-Care Infrastructure

China’s five-year plan earmarks multibillion-dollar budgets for new tertiary hospitals, each demanding advanced diagnostics. India is rolling out mobile ICU fleets under public-private partnerships, creating high-volume demand for ruggedized analyzers. Private equity funneled more than USD 1 billion into sepsis and pathogen-detection start-ups in 2024, accelerating commercialization and compressing innovation timelines.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operational costs of advanced diagnostic platforms | −0.8% | Global, greatest effect in resource-constrained emerging markets | Medium term (2-4 years) |

| Limited skilled workforce in critical care laboratories | −0.5% | Global, especially rural and developing regions | Long term (≥ 4 years) |

| Regulatory and reimbursement uncertainties for novel tests | −0.4% | North America and European Union | Medium term (2-4 years) |

| Data security and privacy concerns in connected diagnostic devices | −0.3% | Global, most acute in highly digitalized healthcare systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Operational Costs of Advanced Diagnostic Platforms

AI-ready blood-gas workstations can cost more than USD 500,000 per unit, while service contracts add roughly 10% annually. Smaller community hospitals hesitate when test volumes cannot guarantee payback. Subscription or outcome-based pricing models have emerged, yet boards often demand multi-year evidence before committing.

Limited Skilled Workforce in Critical Care Laboratories

Technologist vacancy rates exceed 15% in many OECD countries. Sophisticated analyzers still require expertise for QC, cartridge calibration and middleware management. Remote command centers staffed by senior technologists can monitor satellite instruments, but broadband gaps limit reach in underserved regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Hematology Dominance with Chemistry Momentum

Hematology tests accounted for 24.18% of the critical care diagnostics market size in 2025, reflecting their role in transfusion decisions, coagulation surveillance and infection monitoring. Automated analyzers now deliver a complete blood count in under 60 seconds and link directly to transfusion-management software. Coagulation sub-panels have expanded with viscoelastic assays that track clot formation in real time, guiding targeted antifibrinolytic therapy during trauma resuscitation.

Routine and special chemistry is set to grow at a 7.54% CAGR, fueled by expanded panels covering high-sensitivity troponins, presepsin and metabolic stress markers that enable early deterioration prediction. Microbiology and molecular pathogen panels advance in tandem with antibiotic stewardship mandates, providing sub-hour susceptibility profiles that curtail broad-spectrum drug use. Flow cytometry retains value for immunosuppressed cohorts in transplant ICUs, while immunoprotein assays broaden with soluble CD14 variants that refine sepsis risk stratification. Collectively, these shifts align with clinician demand for multiplex dashboards that present holistic patient snapshots rather than isolated parameters, positioning integrated platforms at the forefront of procurement decisions.

By Technology: Point-of-Care Dominance Faces AI Disruption

Point-of-care devices generated 52.02% of 2025 revenue for the critical care diagnostics market and remain essential for collapsing turnaround times at the bedside. Cartridge-based blood-gas analyzers, handheld glucose-ketone meters and compact immunoassay instruments dominate purchase lists because they require minimal maintenance and fit seamlessly into high-acuity workflows.

Yet AI-enabled decision-support systems, projected to expand at a 7.66% CAGR, are reshaping buyer expectations. Middleware hubs equipped with neural networks continuously analyze longitudinal biomarker data to predict adverse events up to 12 hours in advance, triggering protocol-driven interventions. Central-lab analyzers still serve high-throughput needs, but increased decentralization means their future lies in hub-and-spoke architectures that support tiered care settings. Hybrid cloud infrastructures lower entry barriers for community hospitals by offloading computational demands, while cybersecurity enhancements address rising concern over patient-data breaches. Collectively, these developments forecast a technology mix where bedside hardware and cloud intelligence operate in lock-step to bolster clinical outcomes.

By End User: ICU Stronghold Meets Mobile Care Surge

ICUs held 41.08% of 2025 revenue, underscoring their continuous demand for rapid test menus ranging from arterial blood gases to complex coagulation arrays. Bedside analyzers run 24/7, feeding ventilator settings, vasopressor titrations and transfusion algorithms in real time. Operating rooms also contribute meaningful volumes as cardiac and neurosurgical teams adopt intraoperative viscoelastic testing to reduce allogeneic blood use. Ambulance and mobile ICUs, however, represent the fastest-growing end-user cohort with an 8.56% CAGR, driven by public programs that deploy portable analyzers capable of multiplex PCR and advanced chemistry in austere settings. Early stroke-care models outfit vehicles with CT scanners and blood-gas units, enabling alteplase administration within the first hour of symptom onset. Emergency departments continue to adopt dedicated point-of-care bays to mitigate central-lab bottlenecks amid rising patient inflows. Together, these shifts illustrate how the critical care diagnostics market is migrating from fixed ICUs toward a distributed network of care nodes where timely results guide life-saving interventions.

By Sample Type: Whole Blood Leads while Plasma Gains Speed

Whole-blood formats captured 39.95% of 2025 revenue, capitalizing on arterial and finger-stick sampling convenience that aligns with bedside workflow. Ultra-low-volume cartridges need less than 65 µL, allowing frequent monitoring of pediatric or hemodynamically fragile adults. Plasma and serum applications are forecast to pace growth at an 8.12% CAGR through 2031 as multiplex immunoassays optimize biomarker accuracy with centrifuged specimens. The availability of portable micro-centrifuges in ambulances supports pre-hospital plasma testing, an emerging component of stroke and MI triage protocols. Respiratory-secretion cartridges flourish amid near-patient molecular diagnostics for ventilator-associated pneumonia, while fingertip blood RNA tests approved by FDA in 2024 opened new frontiers for hepatitis C management. Capillary micro-sampling devices now integrate with telemedicine platforms, enabling remote clinicians to supervise sample collection and guide therapy adjustments for home-ventilated patients.

Geography Analysis

North America retained 42.03% of 2025 revenue, underpinned by advanced ICU bed density, expansive payer systems and streamlined FDA pathways that allow rapid device clearance. U.S. hospitals continue to integrate AI dashboards to comply with value-based reimbursement, while Canadian provincial tenders emphasize cartridge interoperability across dispersed care settings. Europe follows with robust demand driven by modernization programs and an aging demographic that elevates critical-illness incidence. Germany funds trauma networks that specify viscoelastic coagulation analyzers, and France invests in micro-fluidic molecular platforms to tackle antimicrobial resistance. The United Kingdom’s GBP 2.3 billion commitment to community diagnostic centers demonstrates a shift toward decentralized testing.

Asia-Pacific will lead growth at a 6.46% CAGR through 2031 as China and India channel multibillion-dollar budgets into new tertiary hospitals and mobile ICU fleets. Local joint-venture assembly lines reduce import duties, expanding accessibility for mid-tier hospitals. Japan refines AI-assisted sepsis alerts, while South Korea pioneers cloud-connected cardiac troponin networks across regional hospitals. In Southeast Asia, portable PCR and blood-gas analyzers equip rural clinics, bridging health-equity gaps for populations historically distant from laboratory services.

The Middle East and Africa benefit from oil-funded hospital projects in Gulf Cooperation Council states and donor-backed trauma centers in North Africa. South America records stable mid-single-digit gains, with Brazil deploying mobile stroke units fit with CT and blood-gas analyzers to address high cerebrovascular mortality. Together these geographic threads position the critical care diagnostics market for synchronized yet region-specific expansion over the forecast period.

Competitive Landscape

The critical care diagnostics market exhibits moderate consolidation: the five largest players captured slightly more than half of 2024 revenue. BD deepened its portfolio by acquiring Edwards Lifesciences’ Critical Care division for USD 4.2 billion in September 2024. Roche followed with a USD 295 million purchase of LumiraDx’s cartridge platform to extend its point-of-care immunoassay presence. Abbott, Siemens Healthineers and Danaher leverage broad analyzer suites across chemistry, hematology and molecular segments, bundling middleware licenses into multiyear reagent agreements that secure recurring revenue.

Strategic alliances complement M&A. GE HealthCare partners with AWS to infuse generative-AI into diagnostic workflows, while bioMérieux’s EUR 111 million purchase of SpinChip augments its micro-fluidic intellectual property. Start-ups such as Cytovale, Karius and Deepull attract venture capital by delivering ultra-fast sepsis or bloodstream-infection assays capable of decisively influencing early therapy choices. Regional manufacturers in China and India introduce cartridge analyzers at 20-30% lower cost, courting secondary hospitals balancing performance and affordability. In response, multinationals emphasize uptime guarantees, integrated service networks and cybersecurity certifications to defend share.

Price pressure intensifies as payers transition to bundled payments. Vendors now experiment with outcome-based contracts that peg subscription fees to sepsis-bundle compliance or ICU readmission reductions, aligning manufacturer incentives with hospital quality metrics. This evolution underscores a broader market pivot from standalone hardware sales toward data-driven, service-oriented ecosystems.

Critical Care Diagnostics Industry Leaders

Abbott

Becton, Dickinson & Company

F. Hoffmann-La Roche

Siemens Healthineers

bioMérieux

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Quest Diagnostics launched PCR testing for Oropouche virus across Latin America, strengthening public-health readiness and broadening its infectious-disease menu.

- July 2024: GE HealthCare partnered with AWS to develop generative-AI applications that interpret multisource medical data and accelerate diagnostic workflows.

- June 2024: FDA authorized Cepheid’s Xpert HCV RNA point-of-care assay, delivering fingertip-blood results in about one hour.

- May 2024: Karius received FDA Breakthrough Device designation for its metagenomic lung-infection test aimed at immunocompromised patients.

- May 2024: Nova Biomedical secured FDA clearance for the micro-sample mode on its Stat Profile Prime Plus analyzer.

- May 2024: Terumo Cardiovascular gained 510(k) clearance for the CDI OneView monitoring system, offering 22 intraoperative parameters.

Global Critical Care Diagnostics Market Report Scope

As per the scope, critical care refers to meeting the needs of patients who require immediate attention due to life-threatening health conditions, where the vital organs of the patient's body are at risk of failing. The treatment requires advanced therapeutic, monitoring, and diagnostic technology with the objective of stabilizing the functioning of the organs and improving patient conditions.

The Critical Care Diagnostics Market is Segmented by Test Type (Flow Cytometry, Hematology Test, Microbiology and Infectious Test, Coagulation Test, Immunoprotein, Routine, and Special Chemistry, and Others), End-User (Operating Room, Emergency Room, Intensive Care Unit, and Other), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (USD million) for the above segments.

| Flow Cytometry |

| Hematology Tests |

| Microbiology & Infectious Disease Tests |

| Coagulation Tests |

| Immunoprotein Assays |

| Routine & Special Chemistry |

| Other Test Types |

| Central-Lab Analyzers |

| Point-Of-Care Devices |

| Molecular Diagnostics (PCR/NGS) |

| Immunoassay Platforms |

| Microfluidic & Lab-On-Chip |

| AI-Enabled Decision-Support Systems |

| Intensive Care Units (ICU) |

| Emergency Rooms (ER) |

| Operating Rooms (OR) |

| Ambulance & Mobile ICUs |

| Other End User |

| Whole Blood |

| Plasma / Serum |

| Point-Of-Care Capillary |

| Respiratory Secretions |

| Other Sample Types |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Flow Cytometry | |

| Hematology Tests | ||

| Microbiology & Infectious Disease Tests | ||

| Coagulation Tests | ||

| Immunoprotein Assays | ||

| Routine & Special Chemistry | ||

| Other Test Types | ||

| By Technology | Central-Lab Analyzers | |

| Point-Of-Care Devices | ||

| Molecular Diagnostics (PCR/NGS) | ||

| Immunoassay Platforms | ||

| Microfluidic & Lab-On-Chip | ||

| AI-Enabled Decision-Support Systems | ||

| By End User | Intensive Care Units (ICU) | |

| Emergency Rooms (ER) | ||

| Operating Rooms (OR) | ||

| Ambulance & Mobile ICUs | ||

| Other End User | ||

| By Sample Type | Whole Blood | |

| Plasma / Serum | ||

| Point-Of-Care Capillary | ||

| Respiratory Secretions | ||

| Other Sample Types | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the critical care diagnostics market in 2026?

The critical care diagnostics market size is USD 1.51 billion in 2026.

What growth rate is expected through 2031?

Market revenue is projected to rise at a 5.43% CAGR between 2026 and 2031.

Which technology segment is expanding fastest?

AI-enabled decision-support software is forecast to grow at a 7.66% CAGR through 2031.

Which region will post the highest growth?

Asia-Pacific is expected to lead, registering a 6.46% CAGR through 2031.

How large is the point-of-care segment today?

Point-of-care systems account for 52.02% of 2025 global revenue.

Who are the leading companies?

BD, Roche, Abbott, Siemens Healthineers and Danaher together control roughly 55% of 2024 revenue.

Page last updated on: