Peptide Microarray Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

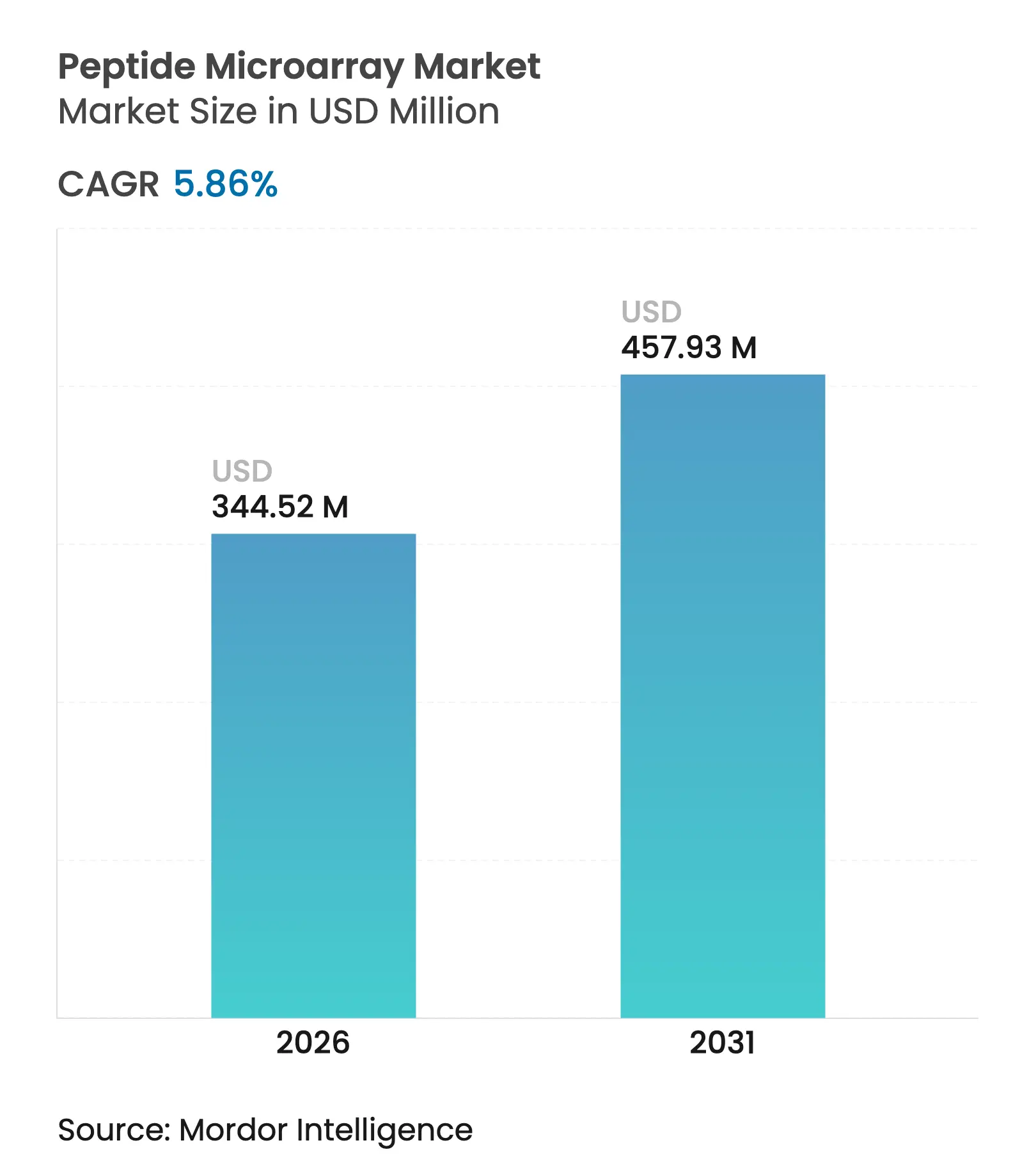

| Market Size (2026) | USD 344.52 Million |

| Market Size (2031) | USD 457.93 Million |

| Growth Rate (2026 - 2031) | 5.86 % CAGR |

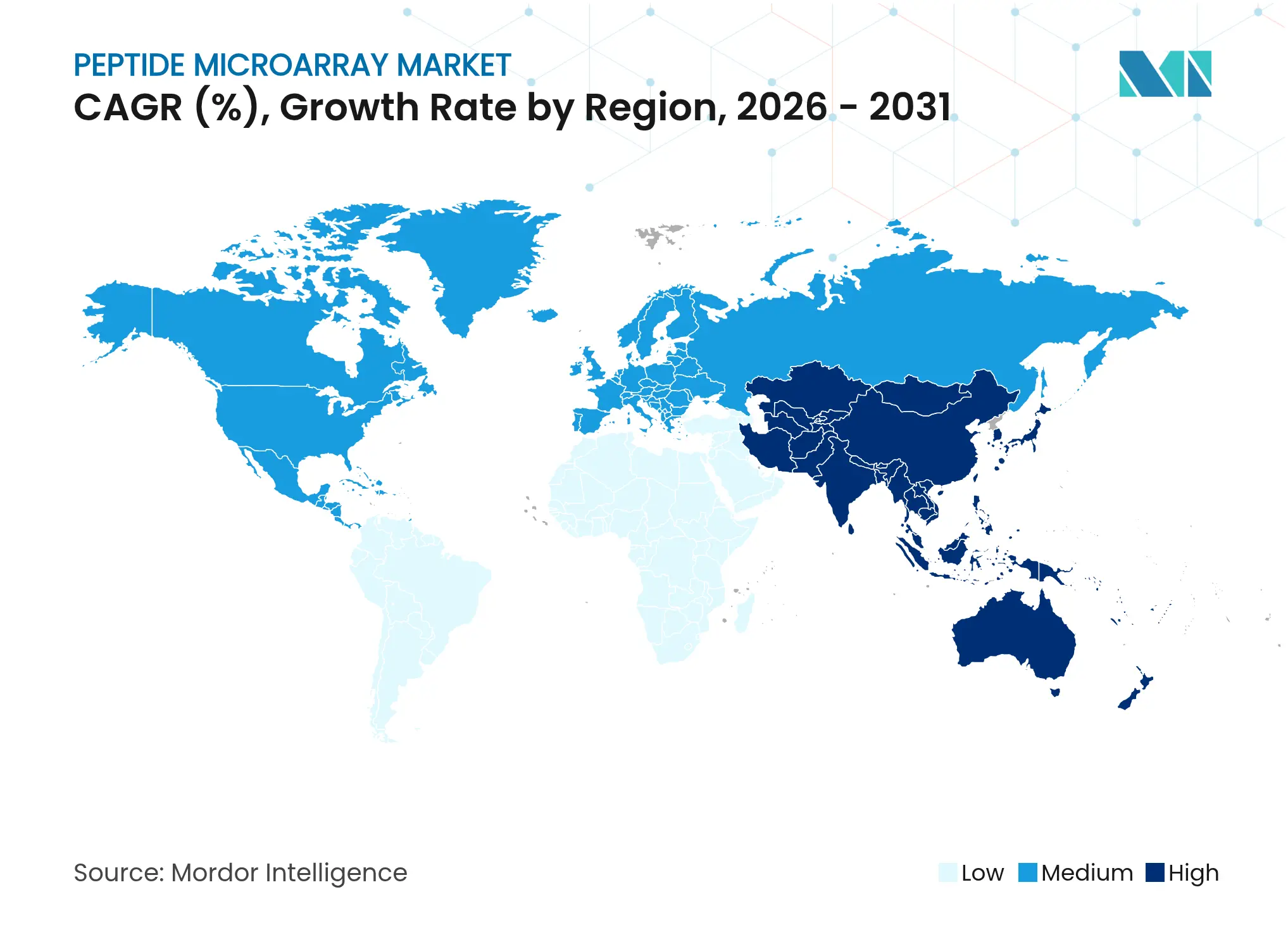

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Peptide Microarray Market Analysis by Mordor Intelligence

Peptide microarray market size in 2026 is estimated at USD 344.52 million, growing from 2025 value of USD 325.46 million with 2031 projections showing USD 457.93 million, growing at 5.86% CAGR over 2026-2031. Steady demand stems from high‐throughput epitope mapping for vaccine design, AI-guided antimicrobial peptide discovery, and multiplexed diagnostics that meet post-pandemic surveillance needs. Pharmaceutical companies favor peptide chips as they shorten early drug-screening cycles, while academic researchers apply them to profile complex antibody signatures across autoimmune, infectious, and oncology indications. Ongoing automation in solid-phase synthesis and laser printing now yields glass-slide arrays exceeding 300,000 spots, narrowing cost differentials with older protein arrays and widening adoption among mid-sized laboratories. Regionally, North America remains the largest buyer due to strong R&D funding and well-established regulatory pathways, whereas Asia-Pacific is scaling fastest as China and Japan pour capital into peptide CDMOs and precision-medicine start-ups. Competitive intensity is rising as instrumentation leaders make billion-dollar acquisitions to bolt on peptide capabilities and improve end-to-end portfolio depth.

Key Report Takeaways

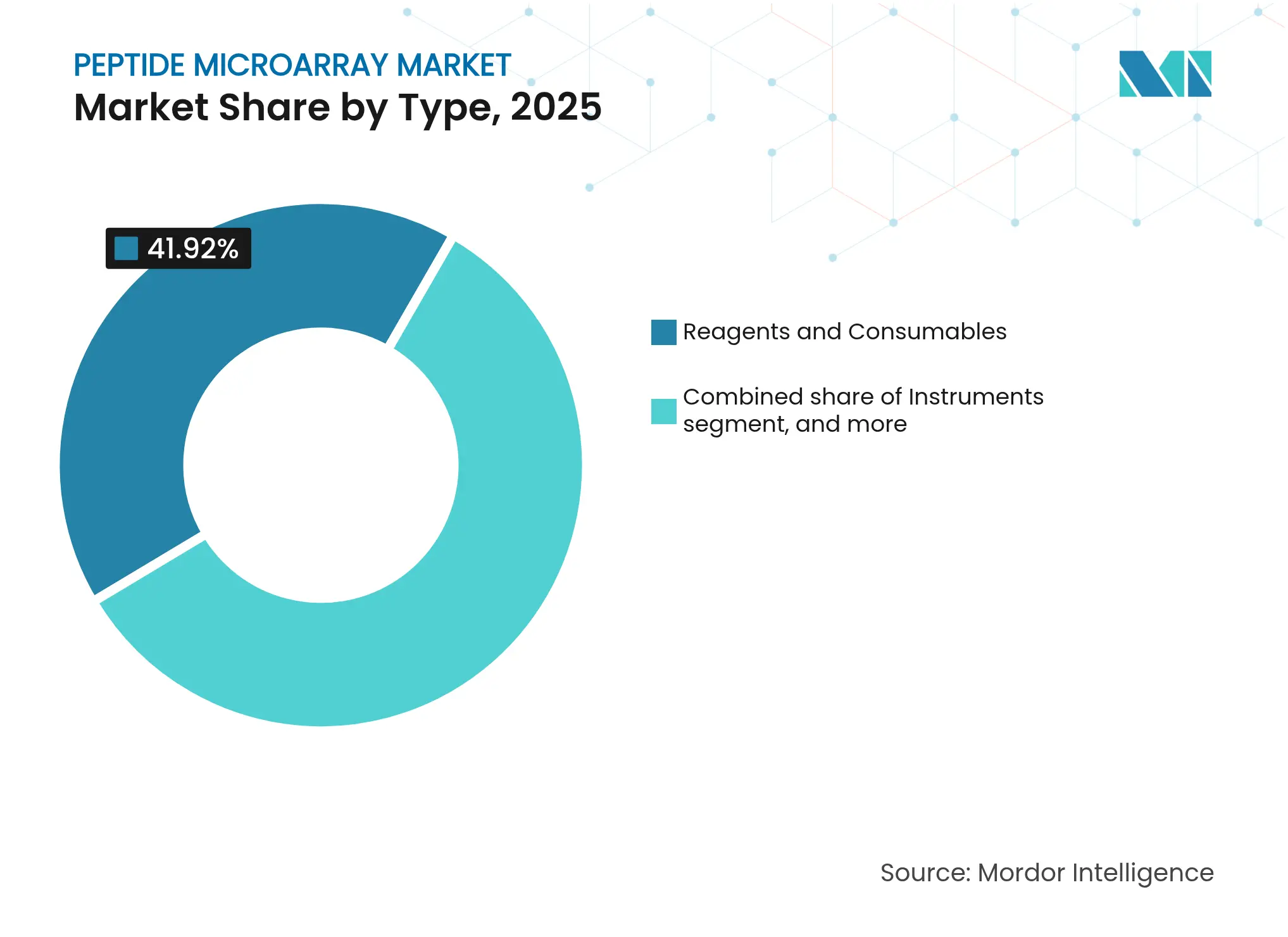

- By type, reagents and consumables led with 41.92% revenue share in 2025; software and analytics is projected to expand at an 8.12% CAGR to 2031.

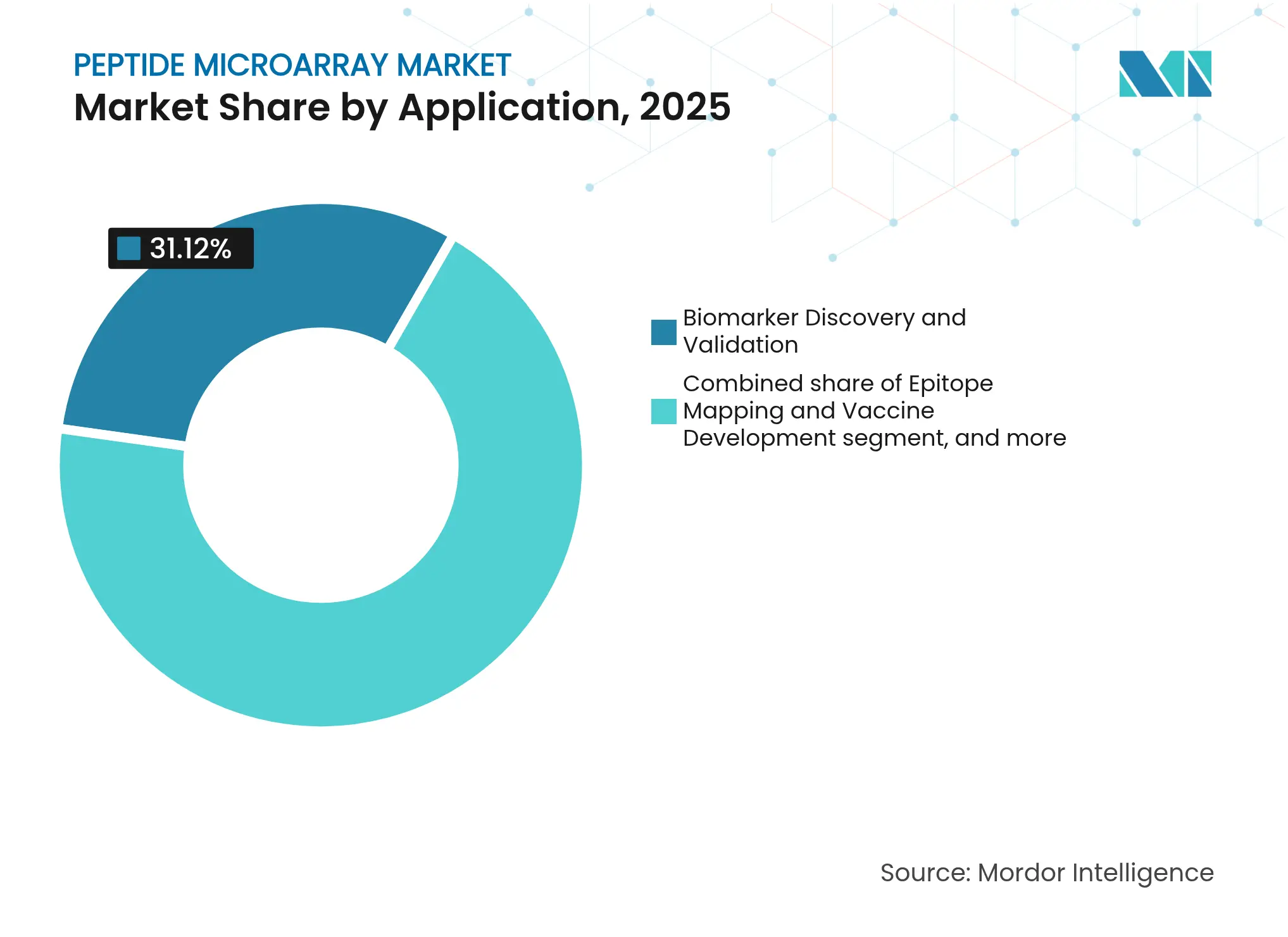

- By application, biomarker discovery and validation held 31.12% of the peptide microarray market size in 2025, while diagnostics is advancing at an 8.23% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies accounted for 45.98% peptide microarray market share in 2025; contract research organizations are recording the highest projected CAGR at 9.02% through 2031.

- By geography, North America dominated with 41.87% revenue share in 2025, whereas Asia-Pacific is forecast to grow at 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Peptide Microarray Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Global Burden Of Chronic And Infectious Diseases Rising Global Burden Of Chronic And Infectious Diseases | +1.8% | Global; acute in aging economies | Long term (≥ 4 years) | % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global; acute in aging economies | Impact Timeline:Long term (≥ 4 years) |

Technological Advances In High-Throughput Peptide Synthesis Technological Advances In High-Throughput Peptide Synthesis | +2.1% | North America, Europe; rapid uptake in Asia-Pacific | Medium term (2-4 years) | |||

Increasing Investment In Biomarker Discovery And Drug Development Increasing Investment In Biomarker Discovery And Drug Development | +1.5% | North America, Europe; emerging Asia-Pacific | Long term (≥ 4 years) | |||

Integration With Machine Learning For Rapid Epitope Mapping Integration With Machine Learning For Rapid Epitope Mapping | +2.3% | Technology hubs worldwide | Short term (≤ 2 years) | |||

Emergence Of Point-Of-Care Peptide Array Diagnostics Emergence Of Point-Of-Care Peptide Array Diagnostics | +1.2% | Resource-limited settings in emerging markets | Medium term (2-4 years) | |||

Growth Of Antimicrobial Resistance Surveillance Programs Growth Of Antimicrobial Resistance Surveillance Programs | +0.9% | Asia-Pacific, Africa high-AMR areas | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Global Burden of Chronic and Infectious Diseases

Growing incidence of autoimmune, oncologic, and emerging pathogen-driven diseases elevates demand for high-density peptide chips that can interrogate thousands of antigen–antibody interactions at once. Synthetic Lyme disease panels, for instance, achieved 95.5% sensitivity and 100% specificity, underlining superior diagnostic resolution over conventional ELISA formats[1]Rajesh Ghosh et al., “Synthetic Peptide Panel for Lyme Disease Diagnostics,” PLOS Pathogens, journals.plos.org. Health systems now pilot population-level screening programs that bank on peptide arrays’ multiplex capability to spot early biomarkers in a single drop of blood. Aging demographics, especially in the United States, Japan, and Germany, mean more multimorbidity cases, spurring hospitals to adopt microarrays for comprehensive immune profiling. Post-COVID surveillance grants also funnel capital into peptide-based assays that track variant-specific antibody escape. Together, the disease burden provides durable, long-horizon pull for the peptide microarray market.

Technological Advances in High-Throughput Peptide Synthesis

Laser-based printing and microwave-assisted solid-phase chemistry allow up to 300,000 discrete peptides per slide at purity levels surpassing 70%, compressing production cycles from weeks to days. Fully closed, GMP-compliant synthesizers introduced by CEM cut solvent use and reagent waste, aligning with stricter environmental standards while trimming unit cost per feature. Proprietary amino acid toners ensure on-the-fly coupling with minimal human handling, mitigating skilled-labor shortages in core labs. Such productivity gains let pharmaceutical teams screen broader libraries in parallel, freeing medicinal chemists to iterate faster on hit-to-lead workflows. They also let diagnostic kit makers lower price-per-test, broadening appeal in mid-income economies from Brazil to Thailand.

Increasing Investment in Biomarker Discovery and Drug Development

Regulators now tie expedited review pathways to biomarker-driven trial designs, prompting record venture and Big-Pharma outlays on discovery platforms. Therapeutic peptide sales are projected to climb from USD 41.44 billion in 2023 to USD 68.83 billion by 2028, mirroring surging demand for array-enabled target validation. Contract research organizations scale custom microarray offerings to capture overflow from in-house pharma labs seeking to cut fixed costs. The U.S. FDA’s green-light history—102 peptide drugs approved, 31 since 2018—reinforces commercial confidence and de-risks new candidates. Consequently, peptide microarray market adoption rises as a foundational element in translational pipelines.

Integration With Machine Learning for Rapid Epitope Mapping

Large-scale language and graph neural models now propose antimicrobial sequences with 94.4% laboratory-verified activity, trimming discovery loops from months to 48 days[2]Wang Jike et al., “AMP-Designer Enables Rapid Antimicrobial Peptide Discovery,” Cell Reports Methods, cell.com. When paired with peptide microarrays, AI tools sift terabytes of binding data to predict immunogenic hot spots and cross-reactivity risks upfront. Deep-learning classifiers surpass 80% accuracy in foreseeing peptide self-assembly, guiding researchers toward constructs with optimal stability. Diagnostic firms embed embedded AI modules in array scanners so clinicians receive annotated, therapy-actionable readouts in near real-time. The confluence of machine learning and dense peptide maps thus accelerates therapeutic design and supports the peptide microarray market’s technological edge.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Capital and Operating Costs of Peptide Microarray Platforms High Capital and Operating Costs of Peptide Microarray Platforms | –1.4% | Emerging markets and smaller institutions worldwide | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:–1.4% | Geographic Relevance:Emerging markets and smaller institutions worldwide | Impact Timeline:Long term (≥ 4 years) |

Ambiguous Regulatory and Reimbursement Frameworks Ambiguous Regulatory and Reimbursement Frameworks | –0.8% | North America, Europe; expanding Asia-Pacific | Medium term (2-4 years) | |||

Shortage of Skilled Bioinformatics Personnel for Data Analysis Shortage of Skilled Bioinformatics Personnel for Data Analysis | –0.7% | Global; most acute in developing regions | Medium term (2-4 years) | |||

Environmental Regulatory Pressure on Perfluorinated Slide Coatings Environmental Regulatory Pressure on Perfluorinated Slide Coatings | –0.5% | Europe, North America; increasingly global | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital and Operating Costs of Peptide Microarray Platforms

Turn-key peptide array workstations, consumables, annual service contracts, and skilled labor together eclipse USD 500,000 in year-one spend, deterring budget-constrained universities and start-ups. Reagent inflation since 2023—exacerbated by amino-acid precursor shortages—pushes per-array costs up 11%, offsetting some savings from synthesis automation. Life-science instrumentation revenues dipped 6.4% in 2023, highlighting broader funding headwinds. Without multi-year grant assurances, labs hesitate to lock into proprietary chemistries that risk obsolescence. These cost pressures particularly hamper the peptide microarray market’s spread in Latin America and parts of Africa, where capital budgets remain tight.

Ambiguous Regulatory and Reimbursement Frameworks

The FDA’s evolving stance on laboratory-developed tests obliges peptide array diagnostic providers to navigate uncertain predicate pathways, lengthening approval queues and inflating compliance budgets by an estimated 22%[3]Akhilesh Kumar Kuril, “Regulatory Landscape of LDTs,” U.S. Food & Drug Administration, fda.gov. Europe’s In Vitro Diagnostic Regulation further adds classification complexity, especially for multiplex assays lacking standardized validation templates. Payment codes for peptide panels are still absent in most reimbursement schedules, forcing hospitals to absorb costs or rely on research grants. The regulatory haze delays commercial launch decisions and tempers investor enthusiasm despite evident clinical utility.

Segment Analysis

By Type: Reagents Dominate While Software Accelerates Innovation

Reagents and consumables generated 41.92% of peptide microarray market revenue in 2025 as every experiment consumes amino-acid toners, coupling buffers, and slide-surface chemistries. The segment benefits from locked-in reorder cycles, yielding predictable cash flows for suppliers. Instruments contribute steady but slower gains, with automated laser-printing systems shortening array turnaround to under 48 hours. The peptide microarray market size for software and analytics, while still a smaller dollar pool, is forecast to expand fastest at an 8.12% CAGR as laboratories adopt AI-enabled design suites that cut bioinformatic bottlenecks. Open-source pipelines such as MARTin gain traction among academic core facilities seeking transparent algorithms and lower licensing fees. Service providers grow by offering outsource packages to mid-tier biotechs unwilling to self-install capital‐intensive hardware, turning expertise into high-margin revenue.

Demand for eco-friendly slide coatings spurs R&D in fluorine-free surfaces, a niche where start-ups compete against incumbents through patented silane chemistries. As sustainability rules tighten, the switch could re-rank suppliers and further segment the reagents arena. Overall, value creation is shifting from raw chemistry to integrated solutions that bundle wet-lab kits with cloud analytics, underscoring software’s rising strategic weight in the peptide microarray market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Biomarker Discovery Leads While Diagnostics Accelerate

Biomarker discovery held 31.12% of peptide microarray market share in 2025, underpinned by precision-medicine mandates that require high-content screens to stratify patient cohorts. Drug sponsors deploy multiplex arrays early to triage targets and associate gene mutations with downstream protein function. Diagnostics, though smaller today, is racing ahead at an 8.23% CAGR to 2031 as hospitals look beyond PCR for point-of-care pathogen ID and autoimmune profiling. Regulatory clarity around companion diagnostics is encouraging kit developers to validate peptide panels in parallel with therapeutic antibodies, shortening approval times once data packages converge.

Epitope-mapping projects—for influenza, RSV, and next-wave coronaviruses—win grants from CEPI and BARDA, ensuring sustained throughput for array fabs. Vaccine groups pair deep-mutational scans with peptide microarrays to chart escape mutations in silico, then confirm binding loss experimentally, compressing timelines to select broadly neutralizing antigens. Drug-screening teams harness AI-steered libraries to evaluate 10^6 structure variations on-chip, shifting bench chemists to higher-value lead-optimization tasks. The dual push from diagnostics and therapeutics therefore broadens the peptide microarray market’s addressable domain and buffers revenue against single-use-case swings.

Note: Segment shares of all individual segments available upon report purchase

By End User: Pharmaceutical Companies Lead While CROs Expand Rapidly

Pharmaceutical and biotechnology enterprises captured 45.98% of 2025 revenue as in-house discovery programs intensify around peptide-based antivirals, oncology vaccines, and hormone analogs. Large sponsors prefer owned instruments for IP security, helping equipment vendors secure multi-year maintenance streams. Academic institutes draw on federal grants and shared core centers to run collaborative immunology studies, yet budget volatility limits capital outlay. Contract research organizations represent the fastest riser, poised for 9.02% CAGR, because they pool specialized staff and high-throughput arrays to service smaller biotechs lacking wet-lab depth. Reference laboratories also expand as they build LDT pipelines targeting autoimmune panels, sepsis markers, and antimicrobial resistance surveillance.

Hospitals remain a nascent but strategic segment; once coding and reimbursement stabilize, tertiary centers are likely to adopt benchtop array readers for on-site serology triage. Service-based business models dominate early clinical rollouts, allowing care providers to outsource assay complexity while clinicians receive digitized reports integrated into electronic medical records. End-user dynamics thus reinforce a hybrid landscape where reagent recurring revenue and analytics subscriptions intertwine, shaping long-term monetization for the peptide microarray market.

Geography Analysis

North America generated 41.87% of global revenue in 2025 as the United States channeled NIH and BARDA grants into peptide array tooling for pandemic-preparedness projects. Canada’s Genomics Enterprise provided matched funding to academic-industry consortia seeking autoantibody signatures, while Mexico’s emerging biosimilar factories procured arrays for in-process impurity assays. High regulatory predictability and proximity to major instrument OEMs ease adoption across pharma and diagnostic labs. The region’s concentration of AI start-ups also accelerates software uptake, further reinforcing North American leadership in the peptide microarray market.

Asia-Pacific is projected to record the highest regional CAGR of 7.12% between 2026 and 2031. China’s CDMOs file increasing FDA Drug Master Files for peptide APIs, positioning the country as a cost-efficient manufacturing hub. National science funds underwrite multi-omic platforms in Shanghai and Shenzhen, and local governments offer tax incentives for high-tech instrumentation imports. Japan’s Kishida administration aims to double private biotech investment by 2028, channeling grants to antibody and peptide-vaccine ventures that require advanced microarrays. India’s biosimilar and vaccine exporters set up peptide design labs near Hyderabad’s Genome Valley, broadening regional demand.

Europe maintains steady mid-single-digit growth supported by Horizon Europe grants and strong biotech clusters in Germany, the United Kingdom, and France. While the EU’s In Vitro Diagnostic Regulation raises compliance costs, clear conformity assessment pathways ultimately benefit quality-driven suppliers. Nordic countries pilot peptide arrays for AMR surveillance under One-Health frameworks, opening niche opportunities. The Middle East and Africa, though smaller today, invest in pathogen watch programs, especially around MERS and Lassa fever, using array data to complement sequencing workflows. South America advances modestly as Brazil scales vaccine capacity, but macroeconomic swings temper capital spending, limiting faster penetration of the peptide microarray market.

Competitive Landscape

Market Concentration

The peptide microarray market remains moderately fragmented. Top five suppliers control just under 55% of global revenue, leaving room for specialists to thrive on custom synthesis and service contracts. Thermo Fisher Scientific’s USD 3.1 billion purchase of Olink widens its proteomics reach, letting it cross-sell arrays with proximity-extension assays. Agilent’s USD 925 million BioVectra acquisition boosts oligonucleotide and peptide GMP production, ensuring secure supply for its SurePrint platform. Merck KGaA leverages its Milli-Q lab water and Sigma-Aldrich reagents to bundle consumables at attractive pricing tiers. Niche innovators such as PEPperPRINT advance laser-printing density and partner with AI vendors for predictive epitope ranking.

Competitive pivots target greener slide chemistries, streamlined end-to-end automation, and cloud analytics dashboards with built-in regulatory documentation. Strategic alliances—ABB with Agilent on robotics, Analog Devices with Flagship Pioneering on bioelectronics—underline a shift toward platform convergence. Environmental legislation curbing perfluorinated coatings nudges incumbents to re-engineer surfaces, granting early-mover advantage to companies with fluorine-free IP. Start-ups exploit AI to democratize peptide design, potentially challenging incumbent reagent sales by generating leaner libraries with higher hit rates. Overall, suppliers differentiate on data-analysis depth, throughput, and regulatory readiness, shaping a competitive mosaic that keeps pricing pressure moderate while stimulating continuous innovation across the peptide microarray market.

Peptide Microarray Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: PEPperPRINT celebrated its 15th anniversary by launching an array printer capable of 300,000 peptide spots per slide, reducing cycle times to 40 hours.

- April 2025: BioSkryb Genomics and Tecan introduced a workflow merging ResolveOME kits with Uno Single Cell Dispensers, enabling sequencing-ready libraries in under ten hours.

- March 2025: Beckman Coulter Life Sciences collaborated with Rarity Bioscience on integrating flow cytometry and superRCA mutation detection for oncology panels.

- January 2025: BD and Biosero linked robotic cell-handling with BD flow cytometers to lower manual touchpoints in peptide screen workflows.

- January 2025: ABB Robotics and Agilent Technologies revealed a pact to integrate ABB robots with Agilent liquid handlers and scanners to automate peptide microarray preparation and imaging workflows.

- August 2024: Analog Devices partnered with Flagship Pioneering to accelerate digitized biological platforms, including AI-driven protein-sequencing modules complementary to peptide array readouts.

Table of Contents for Peptide Microarray Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Global Burden Of Chronic And Infectious Diseases

- 4.2.2Technological Advances In High-Throughput Peptide Synthesis

- 4.2.3Increasing Investment In Biomarker Discovery And Drug Development

- 4.2.4Integration With Machine Learning For Rapid Epitope Mapping

- 4.2.5Emergence Of Point-Of-Care Peptide Array Diagnostics

- 4.2.6Growth Of Antimicrobial Resistance Surveillance Programs

- 4.3Market Restraints

- 4.3.1High Capital And Operating Costs Of Peptide Microarray Platforms

- 4.3.2Ambiguous Regulatory And Reimbursement Frameworks

- 4.3.3Shortage Of Skilled Bioinformatics Personnel For Data Analysis

- 4.3.4Environmental Regulatory Pressure On Perfluorinated Slide Coatings

- 4.4Regulatory Landscape

- 4.5Porter's Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Type

- 5.1.1Instruments

- 5.1.2Reagents & Consumables

- 5.1.3Software & Analytics

- 5.1.4Services

- 5.2By Application

- 5.2.1Epitope Mapping & Vaccine Development

- 5.2.2Biomarker Discovery & Validation

- 5.2.3Diagnostics (Infectious & Autoimmune)

- 5.2.4Drug Screening & Lead-Optimization

- 5.3By End User

- 5.3.1Pharmaceutical & Biotechnology Companies

- 5.3.2Academic & Research Institutes

- 5.3.3Reference Laboratories & CROs

- 5.3.4Hospitals & Speciality Clinics

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1Arrayit Corporation

- 6.3.2JPT Peptide Technologies GmbH

- 6.3.3PEPperPRINT GmbH

- 6.3.4Merck KGaA (Millipore Sigma)

- 6.3.5Thermo Fisher Scientific (Affymetrix)

- 6.3.6Bio-Rad Laboratories

- 6.3.7Agilent Technologies

- 6.3.8Roche NimbleGen

- 6.3.9LC Sciences

- 6.3.10Grace Bio-Labs

- 6.3.11ProImmune Ltd

- 6.3.12Creative Biolabs

- 6.3.13Sengenics Corporation

- 6.3.14Intavis Bioanalytical Instruments

- 6.3.15Oxford Gene Technology

- 6.3.16Quantum-Slide Technologies

- 6.3.17Jerini Peptide Technologies

- 6.3.18GeneCopoeia

- 6.3.19RayBiotech Life

- 6.3.20Zyomyx Inc.

- 6.3.21CDI Labs

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Peptide Microarray Market Report Scope

As per the scope of the report, peptide microarrays are a powerful technology in the proteomics and clinical assays field that traces the binding activities, histone-modifying enzymes, and function of protein linkages on a large scale. Basically, a peptide microarray is a collection of peptides on glass or membrane, or plastic chip, which is also known as a peptide chip or peptide epitope microarray. Peptide microarrays are used to study the binding properties, activity, and function of protein-protein linkage in biology, diagnostics, antibody characterization, medicine, and pharmacology. The peptide microarray market is segmented by type (instruments, reagents, and services), end-user (hospitals, pharmaceutical, and biotechnology companies, research and academic institutes), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across the major regions globally. The report offers the values (USD million) for the above segments.