Connective Tissue Disease Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

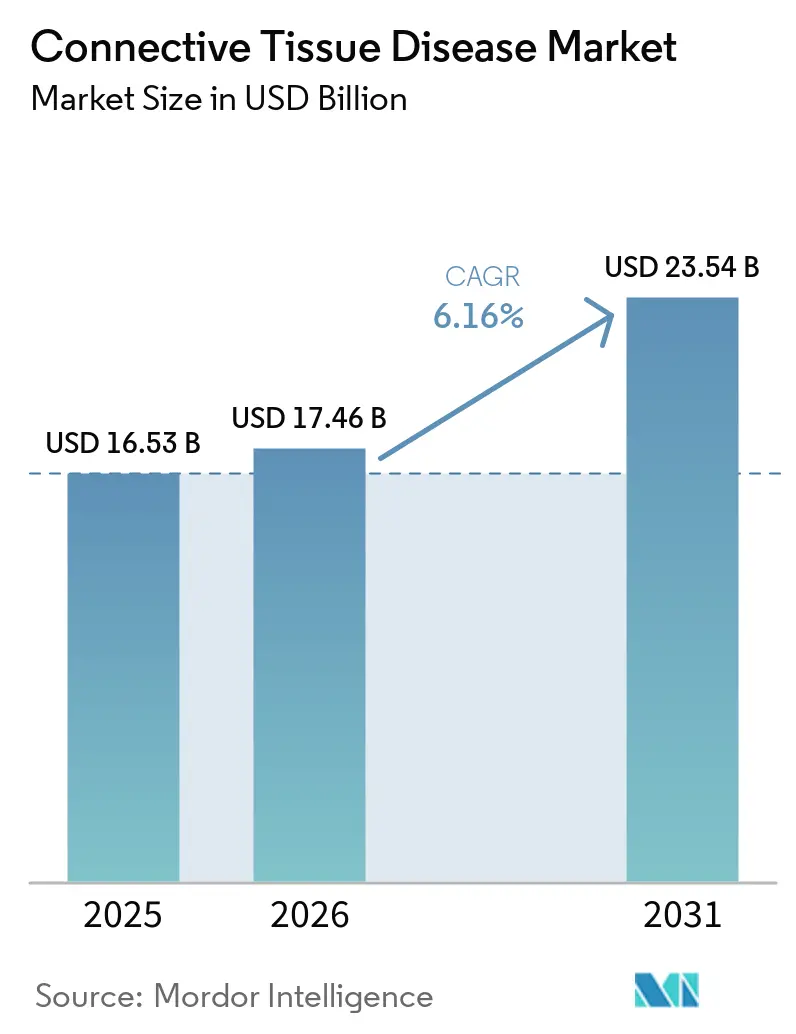

| Market Size (2026) | USD 17.46 Billion |

| Market Size (2031) | USD 23.54 Billion |

| Growth Rate (2026 - 2031) | 6.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Connective Tissue Disease Market Analysis by Mordor Intelligence

The Connective Tissue Disease Market size is expected to increase from USD 16.53 billion in 2025 to USD 17.46 billion in 2026 and reach USD 23.54 billion by 2031, growing at a CAGR of 6.16% over 2026-2031.

The connective tissue disease treatment market is expanding as the treated patient pool widens, specialist diagnosis improves, and biologic use continues to deepen across major autoimmune indications. Recent approvals for obinutuzumab in lupus nephritis and subcutaneous anifrolumab in systemic lupus erythematosus have widened the treatment toolkit and supported more targeted use in severe disease settings. Structured ILD screening and treatment guidance is also moving more connective tissue disease patients into earlier pulmonary evaluation and drug initiation, which supports steadier demand across rheumatology and lung-related care pathways. Competitive activity is shifting toward mechanism differentiation, route-of-administration convenience, and lifecycle management as large companies defend biologic franchises while newer programs move into refractory lupus and CTD-ILD care. Longer term, early cell therapy studies in refractory lupus suggest that the connective tissue disease treatment market could add a new high-acuity treatment layer if later-stage durability and delivery data remain favorable.

Key Report Takeaways

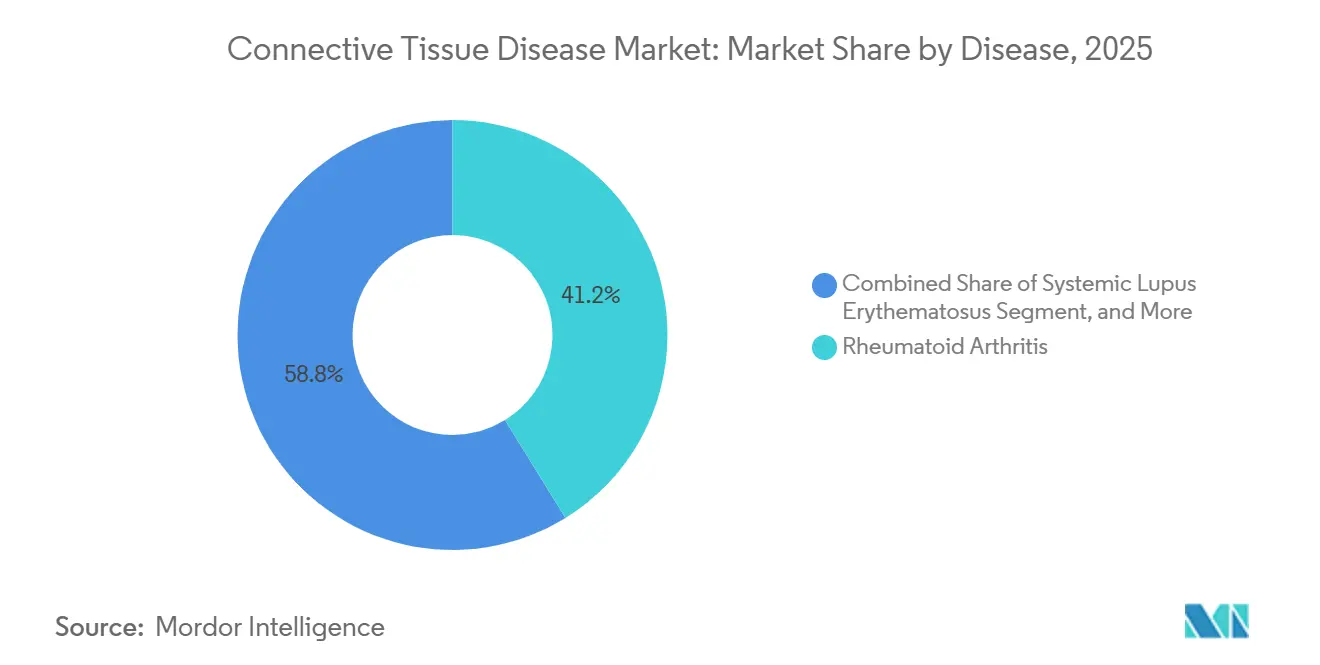

- By disease, rheumatoid arthritis held 41.23% revenue share in 2025, while systemic lupus erythematosus is forecast to expand at an 8.23% CAGR through 2031.

- By drug class, biopharmaceuticals accounted for 63.12% share of the connective tissue disease treatment market size in 2025, while pharmaceuticals are projected to grow at a 7.93% CAGR through 2031.

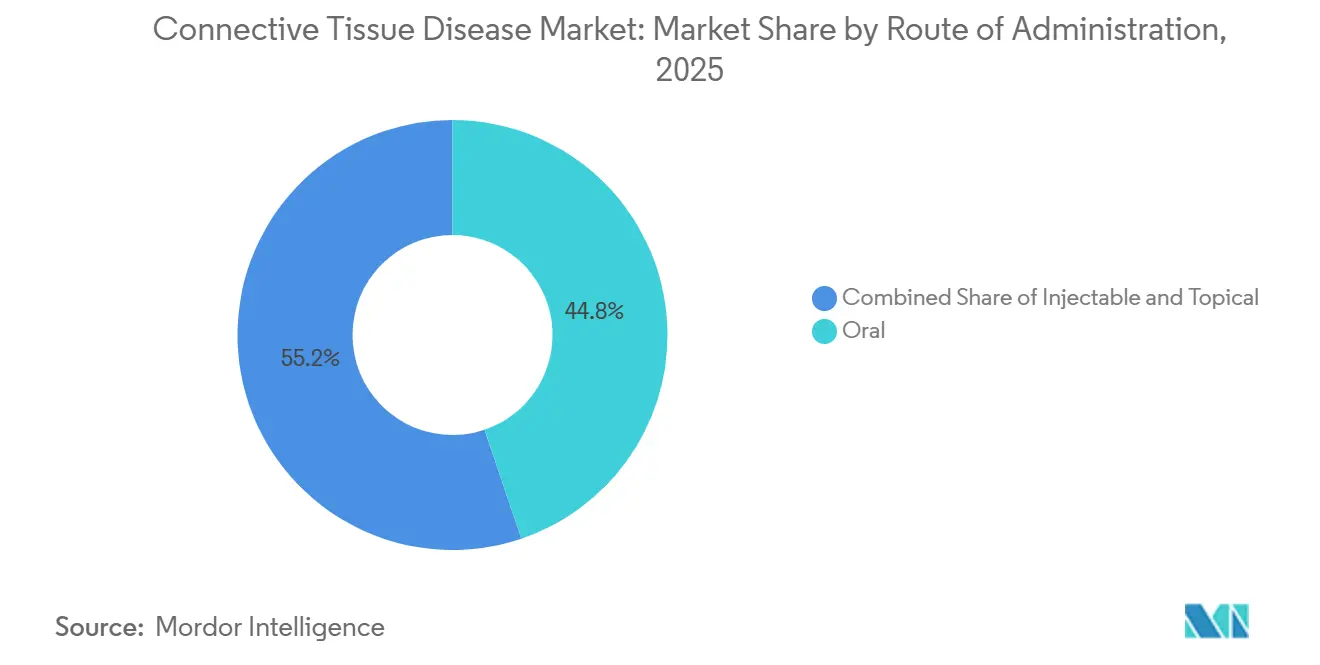

- By route of administration, oral therapies led with 44.76% revenue share in 2025, while injectables are forecast to advance at an 8.85% CAGR through 2031.

- By distribution channel, hospital pharmacies held 49.13% revenue share in 2025, while online pharmacies are projected to grow at a 10.02% CAGR through 2031.

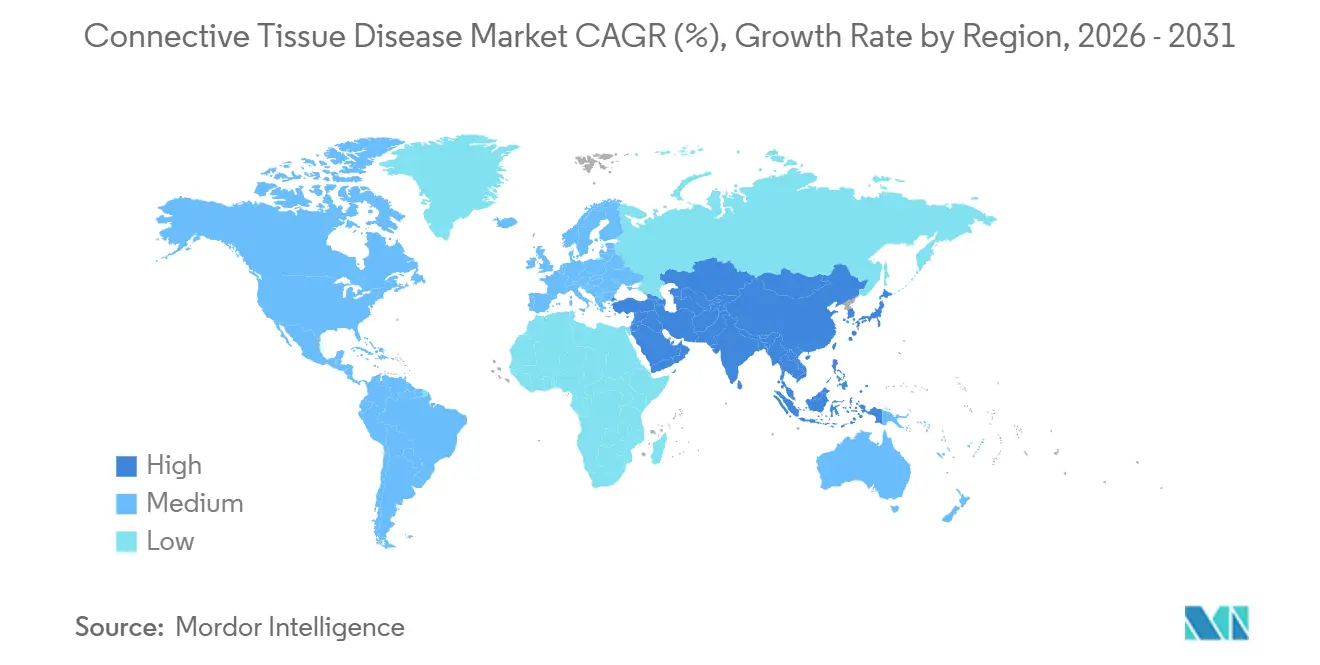

- By geography, North America held 43.62% share of the connective tissue disease treatment market size in 2025, while Asia-Pacific is forecast to expand at a 9.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Connective Tissue Disease Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diagnosed Autoimmune CTD Burden | +1.5% | Global, with concentrated gains in North America and East Asia | Medium term (2-4 years) |

| Biologics and Targeted Therapy Penetration | +1.2% | Global, with highest incremental uplift in Asia-Pacific and Latin America | Medium term (2-4 years) |

| New Options for Lupus Nephritis and SSc-ILD | +0.9% | North America and EU core, with spillover to Japan and South Korea | Short term (≤ 2 years) |

| ACR/CHEST ILD Screening Expansion | +0.7% | North America and EU, with early gains in Australia and Japan | Short term (≤ 2 years) to Medium term (2-4 years) |

| CAR-T Pipeline in Refractory Lupus | +0.5% | North America and EU initially, with Asia-Pacific in later years | Long term (≥ 4 years) |

| Home-Administration Expansion in Lupus Biologics | +0.4% | North America, EU, and Japan, with spillover to Australia and South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

New Options for Lupus Nephritis and SSc-ILD

Within the connective tissue disease treatment market, lupus nephritis is moving into a more competitive phase because obinutuzumab added a new anti-CD20 option in late 2025. FDA approval in October 2025 and European Commission approval in December 2025 gave clinicians a new option with phase 3 backing in active Class III and IV disease.[1]Roche, “FDA Approves Roche's Gazyva/Gazyvaro for the Treatment of Lupus Nephritis,” Roche, roche.com In REGENCY, 46.4% of patients achieved complete renal response versus 33.1% on standard therapy, which gave prescribers and payers a clearer basis for wider uptake. In SSc-ILD, 3-year SENSCIS-ON data supported continued nintedanib use, and a 2025 network meta-analysis ranked tocilizumab highest for slowing FVC decline across evaluated options. As these data accumulate, the connective tissue disease treatment market is moving away from narrow rescue options and toward more defined treatment pathways in lupus nephritis and fibrosing lung involvement.

ACR/CHEST ILD Screening Expansion

The connective tissue disease treatment market is also benefiting from a more structured ILD care pathway after the ACR and CHEST jointly set screening and monitoring recommendations for RA, SSc, IIM, MCTD, and Sjögren disease.[2]Sindhu Johnson, “2023 American College of Rheumatology and American College of Chest Physicians Guideline for the Screening and Monitoring of Interstitial Lung Disease in People With Systemic Autoimmune Rheumatic Diseases,” Arthritis & Rheumatology, doi.org The guideline recommends HRCT chest and pulmonary function testing at presentation for high-risk patients, which increases the chance that lung involvement is identified before advanced progression. It also supports close monitoring in the first year for IIM-ILD and SSc-ILD, which reduces the time between rheumatology follow-up and pulmonary referral. The companion treatment guideline names nintedanib and tocilizumab among conditional first-line options, so diagnosis is translating more directly into therapy selection. In Europe, the 2025 ERS and EULAR guidance widened this framework by including SLE and adding 25 PICO-based recommendations, which support reimbursement and practice alignment across the region.

CAR-T Pipeline in Refractory Lupus

In the connective tissue disease treatment market, cell therapy is moving from a narrow research theme toward a realistic future option for refractory lupus. A phase 1 Nature Medicine study of dual CD19 and BCMA autologous CAR-T in 15 refractory SLE patients reported 80% DORIS remission at 12 weeks with sustained immune reconstitution at a median 712-day follow-up.[3]Jingjing Feng, “Co-Infusion of CD19-Targeting and BCMA-Targeting CAR-T Cells for Treatment-Refractory Systemic Lupus Erythematosus, A Phase 1 Trial,” Nature Medicine, nature.com Another phase 1 study of allogeneic CD19-targeting T cells reported SRI-4 response in all 5 treated patients at 3 months and showed renal tissue recovery on biopsy. AbbVie reinforced the commercial relevance of this direction by agreeing to acquire Capstan Therapeutics for up to USD 2.1 billion in June 2025. If later studies confirm durability and scalable delivery, the connective tissue disease treatment market will open a new premium segment for severe disease that has not responded to repeated immunosuppression.

Home-Administration Expansion in Lupus Biologics

The connective tissue disease treatment market is also changing as lupus biologics move from infusion centers to home use. The FDA approved the Saphnelo Pen in April 2026, after EU approval in December 2025, which allows adult SLE patients to self-administer subcutaneous anifrolumab at home. In the TULIP-SC phase 3 study, 56.2% of patients reached BICLA response versus 34% on placebo at 52 weeks, and 29% reached DORIS remission. GSK also received FDA approval in June 2025 for the Benlysta autoinjector in pediatric lupus nephritis, which extended home biologic use into a high-need subgroup. As more patients shift to self-injection, the connective tissue disease treatment market should see lower delivery friction, broader specialist reach, and more growth through retail and specialty pharmacy channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Biologic and Specialty-Drug Costs | -1.0% | Global, most acute in the Middle East and Africa, South America, and parts of Asia-Pacific | Medium term (2-4 years) |

| Safety Monitoring Burden for JAKs and Immunosuppressants | -0.7% | North America and EU primarily, with expansion into Asia-Pacific | Short term (≤ 2 years) to Medium term (2-4 years) |

| Cell-Therapy Delivery and Long Follow-Up Constraints | -0.4% | Global, particularly limiting in low-resource settings | Long term (≥ 4 years) |

| Delayed Diagnosis in Overlap and Seronegative CTD Cases | -0.5% | Global, most pronounced in gatekeeper health systems | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Biologic and Specialty-Drug Costs

Even with broader treatment choice, the connective tissue disease treatment market still faces an access ceiling because biologics remain expensive for many patients. A 2025 systematic review in The American Journal of Managed Care found that more than 70% of U.S. dermatology patients cited high out-of-pocket costs as a main barrier to biologics for immune-mediated disease. The same cost pressure matters in CTD care because lupus, rheumatoid arthritis, and related disorders often require long treatment duration and repeated monitoring. Price negotiation and biosimilar entry can reduce acquisition cost, but they do not fully remove affordability gaps once co-pays, deductibles, and site-of-care charges are included. This means the connective tissue disease treatment market can expand clinically faster than it expands in real-world treated volume, especially in systems with tighter reimbursement controls.

Safety Monitoring Burden for JAKs and Immunosuppressants

The connective tissue disease treatment market also faces slower uptake in JAKs and some immunosuppressants because safety monitoring remains intensive. The 2025 XELJANZ prescribing information kept the boxed warning on major adverse cardiovascular events, malignancy, thrombosis, serious infection, and mortality. ORAL Surveillance showed hazard ratios of 1.4 for major adverse cardiovascular events and 1.9 for malignancy versus TNF blockers in higher-risk rheumatoid arthritis patients. ACR 2025 observational data found that cardiovascular comorbidity predicted adverse-event-related discontinuation with a hazard ratio of 4.1, and half of the discontinuations occurred within 1.65 years. In practice, repeated blood counts, lipid testing, and infection screening raise care complexity, which keeps part of the connective tissue disease treatment market cautious on broader JAK use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease: Lupus Nephritis Approvals Reshape Growth Dynamics

Rheumatoid arthritis held 41.23% of the connective tissue disease treatment market share in 2025, which gave the connective tissue disease treatment market its largest disease revenue base. That position reflects higher diagnosed volume, a mature biologic treatment pathway, and long-standing physician familiarity with DMARD and biologic sequencing. Systemic lupus erythematosus is projected to expand at 8.23% CAGR through 2031, making it the fastest-growing disease segment in the connective tissue disease treatment market. Late 2025 and 2026 approvals of obinutuzumab, subcutaneous anifrolumab, and the pediatric belimumab autoinjector widened options across lupus nephritis and broader SLE care. A phase 3 telitacicept study in China also reported 67.1% SRI-4 response versus 32.7% on placebo at 52 weeks, which shows that the SLE pipeline is deepening beyond current marketed agents.

In the connective tissue disease treatment market, scleroderma or systemic sclerosis is gaining support from a two-drug ILD treatment pattern built around nintedanib and tocilizumab. Sjögren's syndrome remains a clear white space because no biologic has global approval, which keeps interest high in BAFF-pathway and adjacent autoimmune programs. Polymyositis and dermatomyositis remain smaller segments, but the unmet need is acute because dermatomyositis patients waited a mean 24.3 weeks to diagnosis and were initially misdiagnosed in 34% of cases in a 2025 survey. Mixed connective tissue disease and undifferentiated CTD still rely heavily on therapies borrowed from adjacent indications, while new ILD screening protocols are improving the odds that these patients reach specialist care sooner.

By Drug Class: Biosimilar Volume Pressure Accelerates Pharmaceutical Innovation

Biopharmaceuticals accounted for 63.12% share of the connective tissue disease treatment market size in 2025, and biologics remained the main value driver in the connective tissue disease treatment market. TNF-alpha inhibitors, IL-6 receptor antagonists, and BLyS inhibitors anchor this category because they are used across larger disease pools and established treatment pathways. The class also benefits from repeated label expansion and more defined use in lupus nephritis and CTD-ILD. Japan's 2025 to 2026 PMDA cycle approved subcutaneous anifrolumab for SLE and new tocilizumab biosimilars, which support both innovation and lower-cost biologic access. This keeps biopharmaceuticals central even when price competition increases in mature markets.

Pharmaceuticals are projected to grow at 7.93% CAGR through 2031, which makes them the fastest-growing drug class in the connective tissue disease treatment market. JAK inhibitors and other immunosuppressants still have room to expand in settings where biologic penetration remains uneven, while NSAIDs, corticosteroids, and conventional DMARDs continue to support large prescription volumes. The PMDA also approved upadacitinib for giant cell arteritis in the 2025 to 2026 cycle, showing continued regulatory support for targeted oral immunology agents. At the same time, the April 2025 RINVOQ label and the October 2025 XELJANZ label keep monitoring obligations visible, which shapes how fast this part of the connective tissue disease treatment market can scale.

By Route of Administration: Subcutaneous Formulations Redefine Patient Access

Oral therapies held 44.76% of revenue in 2025, giving them the broadest route to market in the connective tissue disease treatment market. That share reflects daily use of methotrexate, hydroxychloroquine, leflunomide, corticosteroids, NSAIDs, and oral JAK inhibitors across several CTDs. Injectables are projected to grow at 8.85% CAGR through 2031, with subcutaneous formats leading the route shift in the connective tissue disease treatment market. The April 2026 Saphnelo Pen approval and the June 2025 Benlysta autoinjector approval show a clear push toward self-injection rather than clinic-only delivery. Real-world registry data also show that 36.2% of voclosporin-treated lupus nephritis patients received a concomitant biologic, which raises injectable use per treated patient.

In the connective tissue disease treatment market, topical products keep a small but steady role for cutaneous manifestations in dermatomyositis, discoid lupus, and related care needs. Intravenous therapy still matters for higher-acuity induction because obinutuzumab begins with a first-year four-dose IV schedule before twice-yearly maintenance. That means IV volumes are likely to remain relevant even as subcutaneous use expands. The 2026 TULIP-SC data and the broader remission-focused SLE treatment stance support more biologic initiation, which keeps injectable demand firm across care settings.

By Distribution Channel: Digital Pharmacies Gain Structural Share

Hospital pharmacies held 49.13% of revenue in 2025, reflecting their central role in the connective tissue disease treatment market for IV biologics, specialist supervision, and high-acuity monitoring. This channel remains important where induction dosing, infusion observation, or multidisciplinary review is built into routine care. Online pharmacies are projected to grow at 10% CAGR through 2031, making them the fastest-moving channel in the connective tissue disease treatment market. Their growth is tied to home-administration approvals, cold-chain fulfillment, and the wider use of specialty pharmacy coordination for chronic autoimmune care. As more lupus biologics move into self-use formats, refill logistics are becoming a more meaningful part of treatment continuity.

Retail pharmacies occupy the middle ground in the connective tissue disease treatment market because they suit stable oral therapies and selected specialty products once monitoring is established. They are positioned to benefit where outpatient chronic-disease management is expanding and where prescribers want local access for long-duration therapy. Even so, distribution is still shaped by product complexity, payer rules, and whether the drug needs chair time or nurse support. The balance across hospital, retail, and online dispensing is therefore shifting with formulation design rather than with a single channel replacing the others.

Geography Analysis

North America held 43.62% of the connective tissue disease treatment market share in 2025, which kept the region at the center of global revenue. The United States accounts for most of that base because specialist access, biologic availability, and reimbursement depth remain stronger than in many other regions. In 2026, FDA-backed product expansion is still widening the treatable pool, especially after approvals for subcutaneous anifrolumab and the pediatric belimumab autoinjector. The connective tissue disease treatment market in North America also benefits from clear guideline support for CTD-ILD screening and treatment, which helps move high-risk patients toward earlier intervention. This keeps the region strong in both established rheumatoid arthritis care and higher-growth lupus and ILD use cases.

Europe remains the second-largest regional block in the connective tissue disease treatment market, supported by broad specialist networks and a well-established biologic treatment base. The December 2025 European Commission approvals for Gazyvaro in lupus nephritis and subcutaneous Saphnelo in SLE added fresh momentum in severe lupus care. The 2025 ERS and EULAR CTD-ILD guideline also extended the policy framework to SLE, which supports more standardized lung screening and treatment decisions across the region. Western Europe is likely to remain the main demand center, while Southern and Eastern markets add incremental volume as biosimilar and monitoring pathways mature.

Asia-Pacific is projected to grow at 9.18% CAGR through 2031, making it the fastest-growing region in the connective tissue disease treatment market size. Japan is helping drive that pace because the PMDA approved subcutaneous anifrolumab for SLE, upadacitinib for giant cell arteritis, and new tocilizumab biosimilars in the 2025 to 2026 cycle. Regional disease detection is also improving, and a 2025 meta-analysis reported pooled systemic sclerosis incidence in Asia-Pacific at 3.20 per 100,000 person-years, with post-2013 criteria identifying far more cases than older definitions. China, South Korea, India, and Australia remain important volume opportunities for the connective tissue disease treatment market as biologic access and specialist diagnosis continue to widen. The Middle East, Africa, and South America still hold smaller shares, but they add gradual demand where public reimbursement and urban specialist capacity can support higher-cost autoimmune care.

Competitive Landscape

The connective tissue disease treatment market has a moderately concentrated top tier, with a handful of multinational companies controlling much of the highest-value biologic revenue. AbbVie, AstraZeneca, Bristol Myers Squibb, F. Hoffmann-La Roche, and GSK remain the most visible leaders because they combine marketed assets with pipeline depth. Competition in the connective tissue disease treatment market is no longer defined only by brand scale, because mechanism novelty and route convenience now shape positioning more directly. Large companies are defending established franchises while newer biotech firms push cell therapy, antibody engineering, and next-wave immunology platforms. This leaves the connective tissue disease treatment market relatively concentrated in premium biologics and much more fragmented in biosimilars and early-stage innovation.

AstraZeneca made one of the clearest commercial moves when the FDA approved the Saphnelo Pen in April 2026, turning an infusion-led SLE asset into a home-use product. Roche strengthened its lupus nephritis position through FDA approval in October 2025 and European Commission approval in December 2025 for obinutuzumab. GSK also reinforced its lupus franchise by winning FDA approval in June 2025 for the Benlysta autoinjector in pediatric lupus nephritis. These steps show that leaders in the connective tissue disease treatment market are trying to improve both mechanism coverage and delivery convenience. They also raise the bar for smaller entrants, which now need either clearer differentiation or better access economics to gain traction.

AbbVie's June 2025 agreement to acquire Capstan Therapeutics for up to USD 2.1 billion shows that the connective tissue disease treatment market is drawing large-cap investment into in vivo cell engineering. Bristol Myers Squibb has also kept a visible presence in refractory SLE through its phase 1 BMS-986353 program, where early abstract data showed meaningful SLEDAI-2K reduction and durable B-cell depletion. White space remains most visible in primary Sjögren's syndrome, MCTD, and undifferentiated CTD, where disease-specific biologic options are still limited or absent. As a result, the connective tissue disease treatment market should continue to reward companies that can pair clinical novelty with practical delivery and reimbursement execution.

Connective Tissue Disease Industry Leaders

Amgen Inc.

Bayer AG

Boehringer Ingelheim International GmbH

Eli Lilly and Company

GSK plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bristol Myers Squibb received European Commission approval for Sotyktu (deucravacitinib), the first selective oral TYK2 inhibitor for active psoriatic arthritis in adults, following US FDA approval in March 2026. The POETYK PsA trials showed ACR20 response of 54.2% versus 34.1% for placebo at Week 16, with benefits maintained through Week 52.

- April 2026: AstraZeneca received US FDA approval for the Saphnelo Pen (subcutaneous anifrolumab, 120 mg once weekly) for adult SLE, enabling at-home self-administration following EU approval in December 2025 and Canada approval in April 2026. The TULIP-SC Phase 3 trial demonstrated 56.2% BICLA response versus 34.0% placebo at 52 weeks.

- January 2026: TULIP-SC Phase 3 trial results for subcutaneous anifrolumab published in Arthritis & Rheumatology, confirming statistically significant DORIS remission (29.0% vs 14.7% placebo) and LLDAS attainment (40.1% vs 26.0%) at 52 weeks.

- December 2025: The European Commission approved Roche's Gazyva/Gazyvaro (obinutuzumab) for adults with active Class III/IV lupus nephritis, following FDA approval in October 2025. The REGENCY Phase 3 trial showed 46.4% complete renal response versus 33.1% on standard therapy.

Global Connective Tissue Disease Market Report Scope

Connective Tissue Diseases (CTDs) are a broad group of disorders, both genetic and autoimmune, that damage the structural proteins (collagen and elastin) supporting the body’s organs, skin, and joints.

The Connective Tissue Disease Treatment Market is segmented across multiple dimensions that reflect the diversity of autoimmune and inflammatory disorders and their therapeutic approaches. By disease type, it includes Rheumatoid Arthritis (RA), Systemic Lupus Erythematosus (SLE), Scleroderma, Polymyositis, Dermatomyositis, Sjögren’s Syndrome, Mixed Connective Tissue Disease (MCTD), and Undifferentiated Connective Tissue Disease (UCTD). By drug class, the market is divided into biopharmaceuticals and pharmaceuticals. In terms of route of administration, treatments are delivered via oral, injectable, and topical formulations. The distribution channels include hospital pharmacies, retail pharmacies, and online pharmacies. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, Middle East & Africa (MEA), and South America. Forecasts are provided in terms of market value (USD), outlining the expected financial trajectory of this therapeutic segment.

| Rheumatoid Arthritis |

| Systemic Lupus Erythematosus |

| Scleroderma / Systemic Sclerosis |

| Polymyositis |

| Dermatomyositis |

| Sjögren’s Syndrome |

| Mixed Connective Tissue Disease |

| Undifferentiated Connective Tissue Disease |

| Biopharmaceuticals | Biologics |

| Biosimilars | |

| Pharmaceuticals | NSAIDs |

| DMARDs | |

| Corticosteroids | |

| Immunosuppressants | |

| Antimalarial Drugs | |

| Other Pharmaceuticals |

| Oral | |

| Injectable | Intravenous |

| Subcutaneous | |

| Topical |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease | Rheumatoid Arthritis | |

| Systemic Lupus Erythematosus | ||

| Scleroderma / Systemic Sclerosis | ||

| Polymyositis | ||

| Dermatomyositis | ||

| Sjögren’s Syndrome | ||

| Mixed Connective Tissue Disease | ||

| Undifferentiated Connective Tissue Disease | ||

| By Drug Class | Biopharmaceuticals | Biologics |

| Biosimilars | ||

| Pharmaceuticals | NSAIDs | |

| DMARDs | ||

| Corticosteroids | ||

| Immunosuppressants | ||

| Antimalarial Drugs | ||

| Other Pharmaceuticals | ||

| By Route of Administration | Oral | |

| Injectable | Intravenous | |

| Subcutaneous | ||

| Topical | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value for connective tissue disease treatment by 2031?

The sector is forecast to reach USD 23.54 billion by 2031, rising from USD 17.46 billion in 2026 at a 6.16% CAGR.

Which disease segment is growing the fastest?

Systemic lupus erythematosus is the fastest-growing disease segment, with an expected 8.23% CAGR through 2031.

Why is lupus care gaining more commercial attention?

Recent approvals for obinutuzumab, subcutaneous anifrolumab, and the pediatric belimumab autoinjector have expanded treatment options and supported wider use in severe lupus settings.

Which drug class holds the largest revenue share?

Biopharmaceuticals led with 63.12% share in 2025, supported by biologics such as TNF-alpha inhibitors, IL-6 receptor antagonists, and BLyS inhibitors.

Which route of administration is expanding the fastest?

Injectables are forecast to grow at 8.85% CAGR through 2031, with subcutaneous self-administration driving much of that shift.

Page last updated on: