Corrugated Pipe Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 16.33 Billion |

| Market Size (2031) | USD 20.71 Billion |

| Growth Rate (2026 - 2031) | 4.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

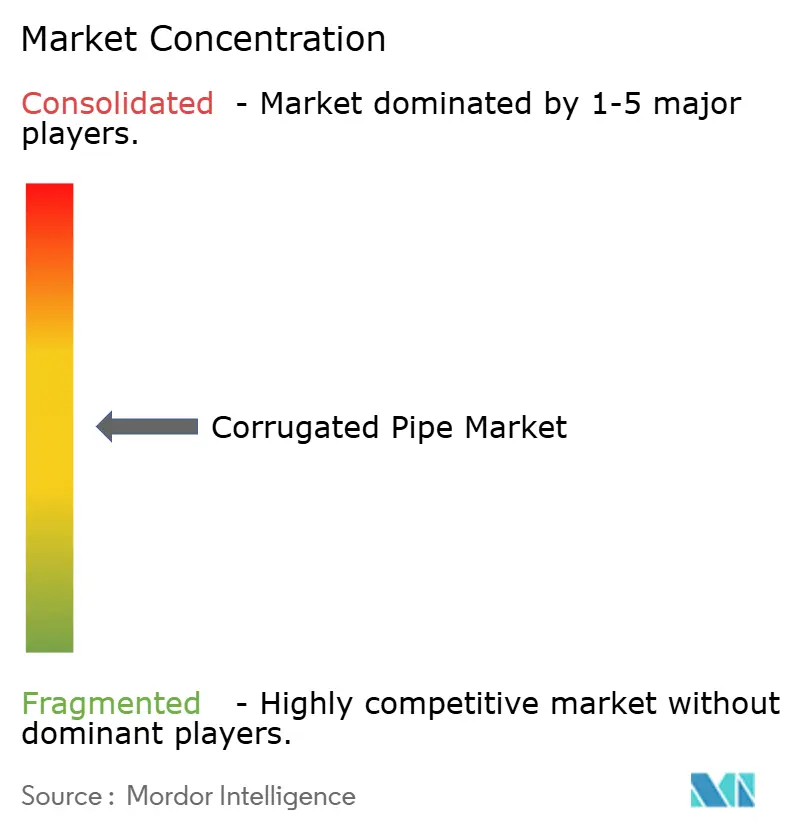

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corrugated Pipe Market Analysis by Mordor Intelligence

The Corrugated Pipe Market size is projected to be USD 15.57 billion in 2025, USD 16.33 billion in 2026, and reach USD 20.71 billion by 2031, growing at a CAGR of 4.87% from 2026 to 2031. Aging municipal culverts, stricter storm-water rules, and increasing recycled-resin mandates are driving demand in both developed and emerging regions. High-density polyethylene (HDPE) continues to be the primary material due to its chemical resistance and low installation costs, while aluminum pipes are preferred for coastal projects requiring corrosion protection. Double-wall configurations dominate sales volumes, but steel-reinforced polyethylene is gaining popularity in deep-fill highway applications that require higher ring stiffness. Procurement practices are evolving as agencies bundle culvert replacement with pavement overlays, shortening bid cycles and benefiting suppliers with local inventory. Technological advancements, such as distributed acoustic sensing embedded in pipe walls, provide asset owners with real-time insights into soil settlement and joint displacement.

Key Report Takeaways

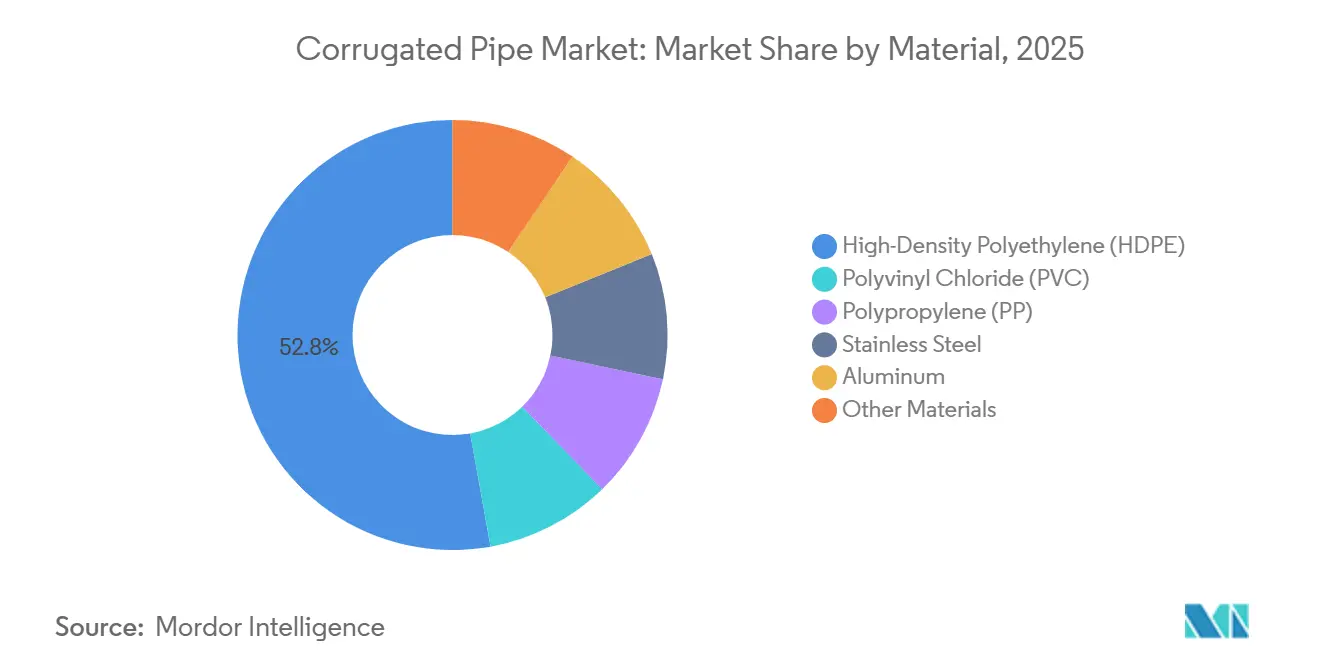

- By material, high-density polyethylene (HDPE) led with 52.82% of the corrugated pipe market share in 2025, while aluminum is forecast to grow at a 4.93% CAGR through 2031.

- By wall structure, double-wall corrugated held 46.00% of the corrugated pipe market share in 2025, and steel-reinforced PE spiral pipes are projected to expand at a 5.20% CAGR through 2031.

- By diameter, less than 300 mm (small) captured 42.67% of the corrugated pipe market share in 2025, whereas the greater than 600 mm (large) segment is set to advance at a 5.56% CAGR through 2031.

- By application, drainage and sewage accounted for 38.05% of the corrugated pipe market share in 2025, while storm-water management is on track for a 5.74% CAGR through 2031.

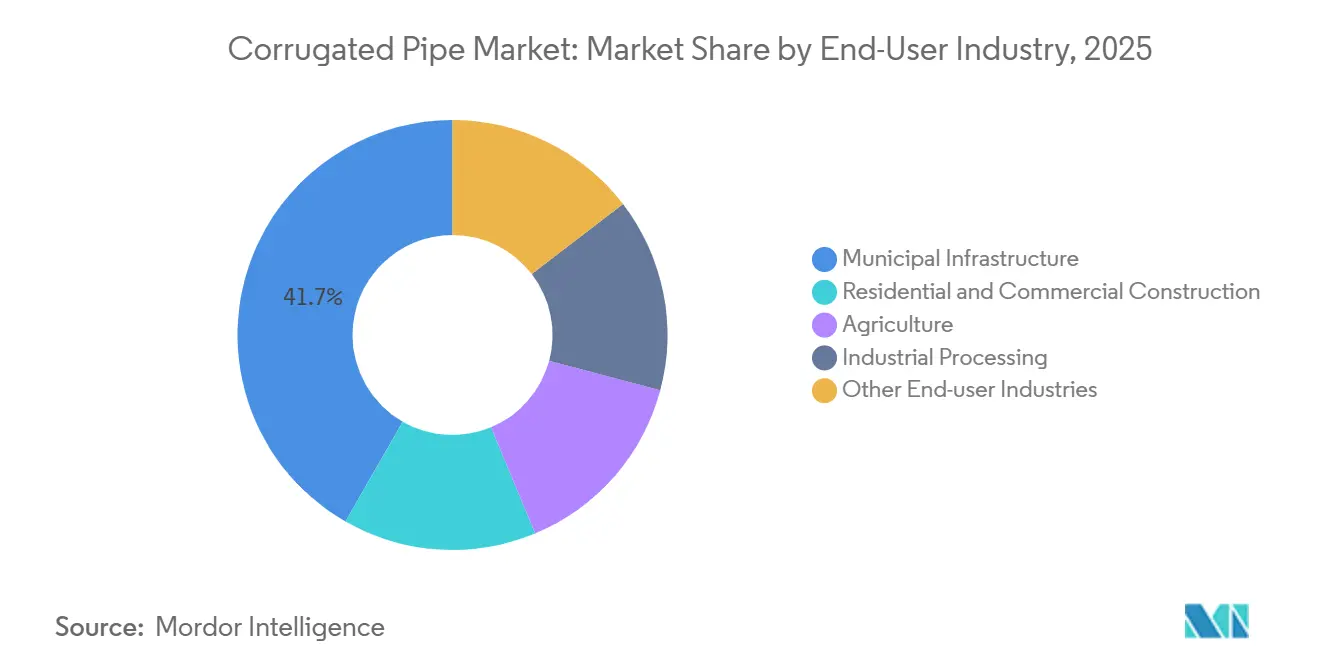

- By end-user industry, municipal infrastructure contributed 41.72% of of the corrugated pipe market share in 2025, and agriculture is positioned for a 5.33% CAGR through 2031.

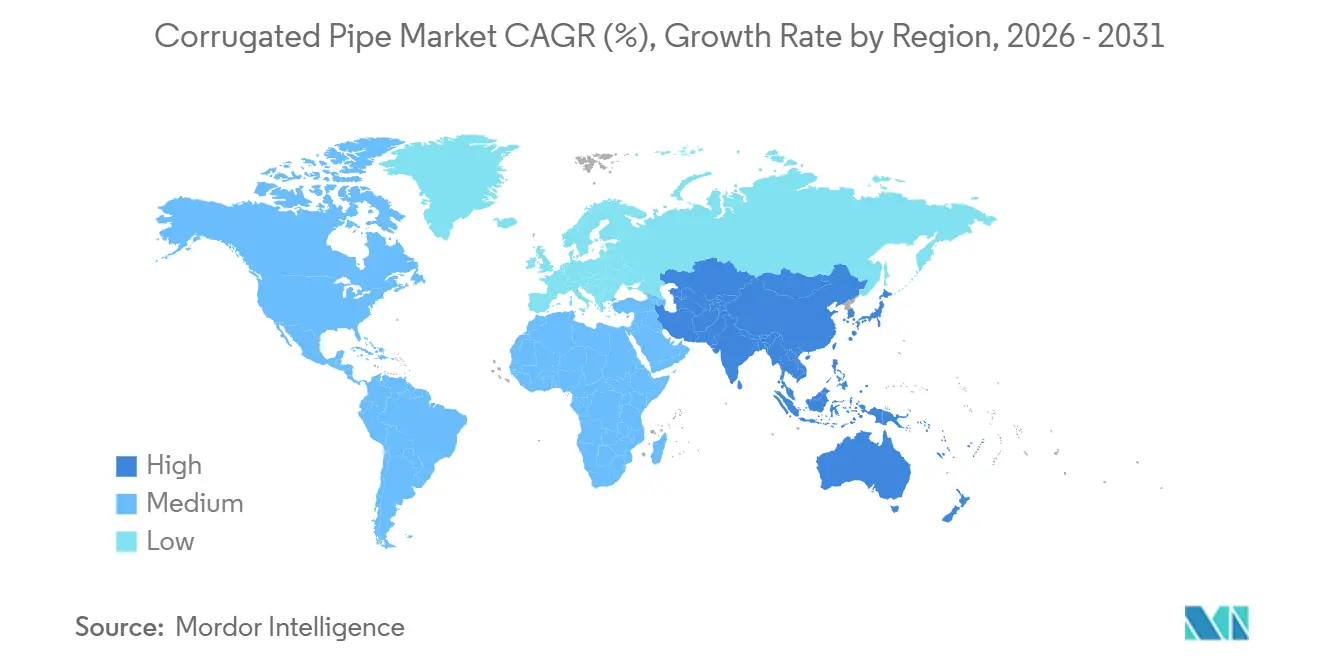

- By geography, Asia-Pacific commanded 46.03% of the corrugated pipe market share in 2025 and is forecast to expand at a 5.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Corrugated Pipe Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure investments in drainage and road networks | +1.2% | Global, with peak intensity in APAC and North America | Medium term (2-4 years) |

| Demand for lightweight, durable and cost-effective pipes | +0.9% | Global | Long term (≥ 4 years) |

| Stricter storm-water runoff compliance mandates | +0.8% | North America and EU, spillover to APAC coastal cities | Short term (≤ 2 years) |

| Recycled-HDPE adoption in decarbonization programs | +0.7% | EU core, North America, APAC manufacturing hubs | Medium term (2-4 years) |

| Edge-powered IoT leak-detection corridors | +0.3% | North America and EU pilot cities | Long term (≥ 4 years) |

| EV gigafactory chemical-waste channels need corrosion-resistant conduits | +0.2% | APAC (China, South Korea), North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Investments in Drainage and Road Networks

Public-works budgets are increasingly focused on asset preservation rather than new highway construction. The U.S. Bipartisan Infrastructure Law allocates USD 110 billion to roads and bridges, with culvert replacement specifically included as a line item. Concord, Massachusetts, has reported that emergency culvert repairs are displacing other maintenance tasks, a trend observed nationwide[1]Town of Concord Public Works, “Director’s Report March 2026,” concordma.gov. India’s National Infrastructure Pipeline prioritizes investments in rural roads and urban drainage, resulting in steady demand for small-diameter pipes in tier-2 and tier-3 cities. Agencies are increasingly aligning culvert work with pavement overlays, reducing bid windows and favoring suppliers with regional warehouses for just-in-time delivery. This approach minimizes traffic disruptions and shifts procurement preferences toward manufacturers with local stock availability.

Demand for Lightweight, Durable and Cost-Effective Pipes

Corrugated pipes, which are 60% to 70% lighter than reinforced-concrete alternatives, significantly reduce crane rental and labor costs, particularly in remote areas. In 2025, the Minnesota Department of Transportation confirmed that recycled-HDPE pipes perform comparably to virgin-resin pipes in terms of ring stiffness and long-term deflection. Trenchless installation methods further enhance cost efficiency by allowing pipes to be installed through existing alignments, avoiding expensive street restoration in urban areas. A 2025 life-cycle study revealed that HDPE drainage systems have 40% lower embodied carbon compared to concrete when transportation and installation energy are considered. Contractors increasingly prefer plastic pipes despite higher per-meter costs, as total installed costs remain lower. This trend is expected to grow as post-consumer resin supply stabilizes and price premiums decrease.

Stricter Storm-Water Runoff Compliance Mandates

Climate-driven storms are exceeding the design capacity of legacy drainage systems. The European Union’s PPWR 2025/40 regulation mandates recyclable product designs with verified recycled content[2]European Commission, “Packaging and Packaging Waste Regulation 2025/40,” europa.eu. In the United States, the EPA’s updated NPDES permits require post-construction controls for projects over one acre, increasing demand for perforated pipes that facilitate on-site runoff infiltration. Builders are increasingly adopting turnkey storm-water modules based on corrugated HDPE chambers, which come with pre-certified flow data. This documentation accelerates permitting processes and reduces engineering costs, providing a competitive advantage to suppliers that integrate hydraulic modeling with their product offerings.

Recycled-HDPE Adoption in Decarbonization Programs

Regulators and corporations are incorporating carbon scores into public tenders. AASHTO’s 2024 update to specification M294 established melt-flow and density parameters for recycled content, reducing uncertainty for highway agencies. In 2025, the Minnesota Department of Transportation confirmed that pipes made with 50% post-consumer recycled (PCR) HDPE showed no significant performance differences. A 2026 study by Next Sustainability calculated a 22% reduction in greenhouse gas emissions when PCR content reached 30% of the resin mix. Resin producers are increasingly entering long-term agreements with municipal waste processors to secure feedstock, bypassing traditional brokers and mitigating risks associated with crude-oil price volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile HDPE, PVC and metal feedstock prices | -0.6% | Global | Short term (≤ 2 years) |

| Plastic-waste and end-of-life recycling concerns | -0.4% | EU, North America, APAC urban centers | Medium term (2-4 years) |

| Fire-safety codes limiting plastic conduit in high-rise builds | -0.2% | North America and EU metropolitan areas | Long term (≥ 4 years) |

| Emergence of cellular-concrete pipes eroding cost advantage | -0.3% | EU, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile HDPE, PVC and Metal Feedstock Prices

Pipe contracts often lock prices six to twelve months in advance. Price spikes in ethylene or aluminum can force fabricators to either renegotiate contracts or absorb losses. For instance, a 15% increase in aluminum prices in early 2025 led several producers to withdraw from fixed-price bids. Index-linked pricing clauses are now appearing in U.S. municipal tenders, but smaller towns with limited procurement expertise often delay projects until prices stabilize. This volatility disrupts production schedules, increases overtime costs, and reduces plant utilization rates.

Plastic-Waste and End-of-Life Recycling Concerns

Municipalities promoting circular economies face challenges in recycling corrugated pipes, which have a service life of 50 years. Currently, most retired pipes end up in construction debris sites due to high cleaning costs associated with soil contamination, which exceed the cost of virgin resin. The European Union’s PPWR mandates member states to establish take-back schemes by 2030, but current disposal fees undermine the total cost-of-ownership benefits of plastic pipes. Pilot programs in Germany and the Netherlands have demonstrated the feasibility of mechanical recycling, but scaling these efforts remains a significant challenge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: HDPE Dominance Meets Aluminum’s Coastal Surge

In 2025, high-density polyethylene (HDPE) captured 52.82% of the corrugated pipe market revenue, reflecting its optimal balance of strength, flexibility, and cost. Aluminum is anticipated to grow at the fastest rate, with a 4.93% CAGR through 2031, driven by the demand for corrosion-resistant systems in coastal cities and chemical plants. Polyvinyl chloride (PVC) continues to hold its position in gravity sewers that must adhere to flame-spread codes, while polypropylene is utilized in process-water lines requiring heat resistance. Stainless steel and fiber-reinforced composites cater to niche applications where hygiene or electromagnetic transparency justify higher costs.

MnDOT demonstrated in 2025 that pipes manufactured with 50% post-consumer HDPE met AASHTO M294 ring-stiffness criteria, opening up large public contracts requiring recycled content. On the metals side, updates to ASTM B745 standardized corrugation profiles and joint geometries, reducing fabrication costs and enabling aluminum to be priced closer to coated steel. Material selection now diverges: cost-sensitive municipal buyers prefer recycled-content HDPE, while projects in saline or acidic environments are willing to pay a 30% premium for aluminum or stainless steel.

By Wall Structure: Double-Wall Efficiency and Steel-Reinforced Strength

Double-wall corrugated pipes accounted for 46.00% of the market share in 2025, attributed to their lightweight design and smooth inner bore, which minimizes hydraulic losses. Steel-reinforced polyethylene (PE) spiral pipes are projected to grow at a 5.20% CAGR through 2031, driven by the need for higher load ratings in culverts under deep fills by highway agencies. Single-wall pipes remain widely used in farm drainage applications, where affordability outweighs structural requirements. Perforated variants are commonly employed in infiltration basins and green roofs mandated by urban runoff regulations.

Contech’s Spirolite liner system incorporates steel into a PE spiral profile, enabling trenchless rehabilitation of deteriorating concrete sewers and reducing project costs by up to 60%. International standards such as ISO 9969 for ring stiffness harmonize testing, allowing contractors to source materials interchangeably across borders. The competitive landscape is divided: steel-reinforced spirals secure high-profile infrastructure projects, while double-wall HDPE dominates price-sensitive residential and light-commercial markets.

By Diameter: Small-Bore Volume and Large-Diameter Growth

Pipes with diameters less than 300 mm (small-bore) represented 42.67% of shipments in 2025, primarily serving residential foundation drains and field tiles. Pipes with diameters greater than 600 mm (large-bore) are expected to grow at a 5.56% CAGR from 2026 to 2031, driven by the need for larger trunk sewers to accommodate climate-adjusted design storms. Large-diameter HDPE and steel-reinforced pipes weigh half as much as comparable concrete culverts, reducing the need for heavy equipment and lowering civil works costs.

The Los Angeles County Metropolitan Storm-water Infrastructure District’s 2026-2030 plan highlights the replacement of 225 aging metal culverts, many between 900 mm and 1,500 mm in diameter, underscoring the growing demand for large-diameter pipes. Small-bore products maintain their leadership due to high-speed extrusion processes that produce 200-meter coils, reducing joint counts and speeding up installation. The market is segmented by value chain focus: small pipes compete on logistics, while large pipes emphasize structural and hydraulic performance.

By Application: Storm-Water Management Leads Growth

Drainage and sewage applications contributed 38.05% of the corrugated pipe market revenue in 2025. Storm-water management is the fastest-growing segment, with a projected 5.74% CAGR through 2031, driven by regulatory requirements for on-site water retention. Cable protection continues to grow steadily, supported by fiber-to-home rollouts and 5G network expansion. Industrial applications include chemical drains and cooling systems.

Advanced Drainage Systems has shipped over 850,000 modular storm-water units featuring corrugated chambers, demonstrating the shift toward engineered solutions over commodity pipes. The U.S. Environmental Protection Agency’s (EPA) post-construction runoff regulations provide a stable demand base, insulating this segment from housing market fluctuations. Suppliers offering bundled solutions, including hydraulic software, prefabrication, and installation training, secure repeat business and higher margins.

By End-user Industry: Municipal Infrastructure Drive Revenue, Agriculture Drives Pace

Municipal infrastructure accounted for 41.72% of market revenue in 2025, reflecting ongoing sewer and culvert rehabilitation programs. Agriculture is expected to grow at a 5.33% CAGR through 2031, as farmers adopt subsurface drainage systems to optimize yields in water-scarce regions. Residential and commercial construction demand is tied to building permits and favors smaller diameters for foundation and roof drainage. Industrial plants are willing to pay premiums for smart pipes with embedded sensors to minimize downtime.

India’s Union Budget 2024-25 allocated INR 11.11 lakh crore (USD 133 billion) to infrastructure, with significant investments in rural roads and irrigation projects that rely on corrugated pipes. Industrial end-users are piloting fiber-optic monitoring systems to detect leaks early, demonstrating that digital features can increase product value even in cost-sensitive markets.

Geography Analysis

Asia-Pacific held 46.03% of global revenue in 2025 and is forecast to grow at a 5.62% CAGR through 2031. China’s sponge-city directive makes permeable infrastructure mandatory in 30 pilot metros and stimulates procurement of perforated HDPE basins that recharge aquifers rather than overload treatment plants. India’s National Infrastructure Pipeline funds rural roads and urban drainage, channeling steady demand for small- and medium-diameter pipes. Japan and South Korea replace corroded steel culverts with HDPE in coastal prefectures, while ASEAN nations expand drainage to reduce flood risk, often financed by multilateral banks that favor standardized thermoplastic systems.

North America follows with a substantial value share. The U.S. Bipartisan Infrastructure Law provides USD 110 billion for roads and bridges, much allocated to culvert replacement. Canadian provinces focus on asset preservation, substituting HDPE for deteriorated galvanized steel. Mexico’s near-shoring boom drives new industrial parks that need large-diameter drainage. Demand is evolving from pure volume toward engineered services such as trenchless rehab and digital inspection, giving incumbents a service-based moat.

Europe shows slower top-line growth yet leads in regulatory stringency. The PPWR 2025/40 compels recycled content, rewarding suppliers with closed-loop agreements. Germany and the Netherlands pilot take-back programs for end-of-life pipes, while Eastern European nations leverage EU cohesion funds to upgrade rural drainage with HDPE. South America’s expansion centers on Brazil and Argentina, though currency swings and tariffs moderate import appetite. In the Middle-East and Africa, Saudi Arabia’s Vision 2030 infrastructure push and South Africa’s water-loss programs lift orders for corrosion-resistant aluminum and stainless-steel pipes despite smaller overall volumes.

Competitive Landscape

The corrugated pipe market features moderate concentration. Advanced Drainage Systems, JM Eagle, and Wavin anchor North America and Europe through vertically integrated resin compounding, extrusion, and distribution networks. Advanced Drainage Systems posted USD 753 million in net sales for Q2 FY 2025, confirming robust retrofit demand. Armtec dominates Canada by leveraging local resin supply and proximity to provincial road agencies, trimming freight costs. Emerging players such as Pars Ethylene Kish in Iran and DAYU Group in China win domestic bids through price competitiveness, yet lack the third-party certifications needed for EU tenders.

Technology adoption creates a new frontier. Fiber-optic strain gauges embedded in HDPE walls deliver continuous strain and leak data, as validated by a 2022 CivilEng study. Companies that bundle sensors, cloud dashboards, and analytics turn commodity pipe into a SaaS-like service that commands premium pricing. ISO 9969 and EN 13476 certification has become the passport to European public procurement, raising entry barriers for uncertified manufacturers. The market also sees investments in inline laser profilometry and real-time wall-thickness control that cut scrap and ensure tight tolerances, separating tier-one extruders from regional contract shops.

Large firms secure recycled-resin supply chains to buffer raw-material shocks. ADS’s multi-year deal with a municipal waste processor aims for 40% recycled content by 2028, reducing exposure to petroleum price swings. Regional specialists counter with rapid prototyping of custom corrugation patterns and on-site technical crews that resolve issues within hours, a response time that large multinationals often cannot match.

Corrugated Pipe Industry Leaders

Advanced Drainage Systems

Contech Engineered Solutions LLC

JM EAGLE, INC.

PIPELIFE INTERNATIONAL GmbH

FRÄNKISCHE Rohrwerke Gebr. Kirchner GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: A study conducted in Minnesota found that corrugated high-density polyethylene (HDPE) pipes containing recycled materials performed similarly to pipes made entirely from virgin materials. The research assessed 36-inch pipes with 60% recycled content installed beneath a highway, demonstrating their compliance with AASHTO standards while contributing to carbon footprint reduction.

- May 2025: SIBUR introduced a new high-strength grade of polypropylene, PPI003 EX, specifically developed for manufacturing corrugated pipes used in sewer and drainage systems. This grade was designed to meet the demand for domestically produced raw materials in Russia, serving as a replacement for imported alternatives and ensuring a lifespan of over 50 years for the pipes made from it.

Global Corrugated Pipe Market Report Scope

Corrugated pipes are flexible and durable, featuring a wavy exterior and a smooth interior. They are designed to provide high mechanical strength and efficient flow. Typically manufactured from PE/PP or PVC, these pipes are commonly used in underground drainage, sewage systems, agriculture, and electrical cable management, owing to their flexibility and capacity to withstand heavy earth loads.

The Corrugated Pipes Market is segmented into material, wall structure, diameter, application, end-user industry, and geography. By material, the market is segmented into high-density polyethylene (HDPE), polyvinyl chloride (PVC), polypropylene (PP), stainless steel, aluminum, and other materials. By wall structure, the market is segmented into double-wall corrugated, single-wall corrugated, steel-reinforced PE spiral, and perforated and slotted variants. By diameter, the market is segmented into less than 300 mm (small), 300–600 mm (medium), and greater than 600 mm (large). By application, the market is segmented into drainage and sewage, storm-water management, cable and fiber-optic protection, culverts and roads, and industrial and agricultural uses. By end-user industry, the market is segmented into municipal infrastructure, residential and commercial construction, agriculture, industrial processing, and other end-user industries. The report also covers the market size and forecasts for corrugated pipes in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| High-Density Polyethylene (HDPE) |

| Polyvinyl Chloride (PVC) |

| Polypropylene (PP) |

| Stainless Steel |

| Aluminum |

| Other Materials |

| Double-Wall Corrugated |

| Single-Wall Corrugated |

| Steel-Reinforced PE Spiral |

| Perforated and Slotted Variants |

| Less than 300 mm (Small) |

| 300-600 mm (Medium) |

| Greater than 600 mm (Large) |

| Drainage and Sewage |

| Storm-Water Management |

| Cable and Fiber-Optic Protection |

| Culverts and Roads |

| Industrial and Agricultural Uses |

| Municipal Infrastructure |

| Residential and Commercial Construction |

| Agriculture |

| Industrial Processing |

| Other End-user Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material | High-Density Polyethylene (HDPE) | |

| Polyvinyl Chloride (PVC) | ||

| Polypropylene (PP) | ||

| Stainless Steel | ||

| Aluminum | ||

| Other Materials | ||

| By Wall Structure | Double-Wall Corrugated | |

| Single-Wall Corrugated | ||

| Steel-Reinforced PE Spiral | ||

| Perforated and Slotted Variants | ||

| By Diameter | Less than 300 mm (Small) | |

| 300-600 mm (Medium) | ||

| Greater than 600 mm (Large) | ||

| By Application | Drainage and Sewage | |

| Storm-Water Management | ||

| Cable and Fiber-Optic Protection | ||

| Culverts and Roads | ||

| Industrial and Agricultural Uses | ||

| By End-user Industry | Municipal Infrastructure | |

| Residential and Commercial Construction | ||

| Agriculture | ||

| Industrial Processing | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the corrugated pipe market?

The corrugated pipe market size stands at USD 16.33 billion in 2026 and is expected to reach USD 20.71 billion by 2031, reflecting a 4.87% CAGR over 2026-2031.

Which material dominates demand for corrugated pipes in 2025?

High-Density Polyethylene (HDPE) leads with 52.82% revenue share in 2025 because it balances durability, flexibility, and cost.

Which application segment is expanding the fastest through 2031?

Storm-water management is forecast to grow at a 5.74% CAGR through 2031 as new runoff regulations drive adoption of perforated drainage systems.

Why is Asia-Pacific the largest regional market for corrugated pipes?

Massive infrastructure spending in China and India plus coastal retrofit programs in Japan and South Korea together give the region 46.03% revenue share in 2025 and the quickest 5.62% CAGR through 2031.

Page last updated on: