Pipe Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.48 Billion |

| Market Size (2031) | USD 13.13 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

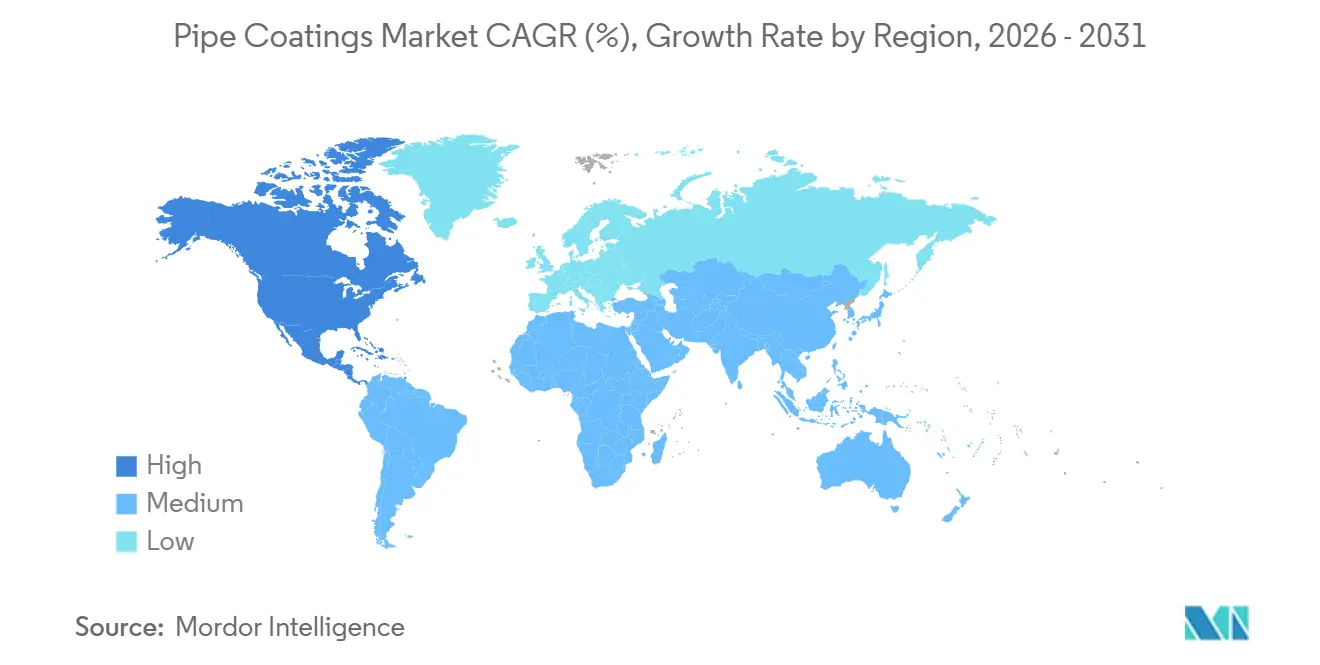

| Fastest Growing Market | North America |

| Largest Market | North America |

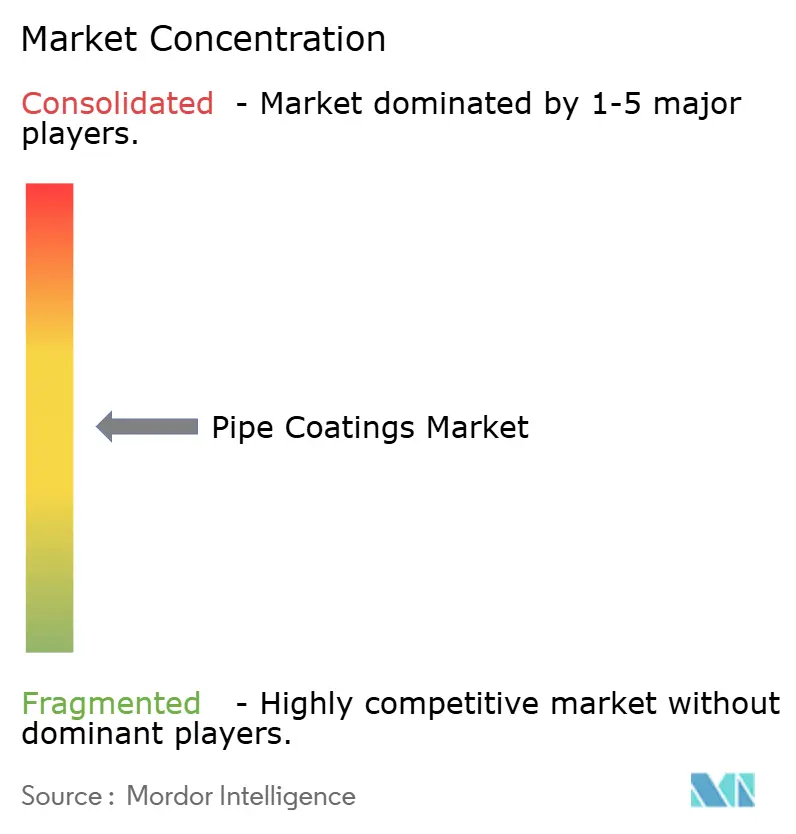

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pipe Coatings Market Analysis by Mordor Intelligence

The Pipe Coatings Market size is projected to expand from USD 10.02 billion in 2025 and USD 10.48 billion in 2026 to USD 13.13 billion by 2031, registering a CAGR of 4.61% between 2026 to 2031. Robust pipeline build-outs for shale gas in North America, large-scale oil and gas corridors in Asia-Pacific, and stricter corrosion-protection mandates for aging networks collectively underpin this steady expansion. Operators are prioritizing high-performance external systems to curb soil-side failures, while tightening volatile-organic-compound (VOC) rules in Europe and the United States accelerate the switch to water-borne and powder alternatives. Material innovation—most notably self-healing zinc-rich primers, graphene-reinforced barriers, and UV LED-curable field-joint products—continues to raise performance benchmarks and shorten maintenance cycles. Competitive strategies revolve around regional application hubs, vertical integration into field services, and portfolio realignment away from legacy coal-tar and asphalt enamels.

Key Report Takeaways

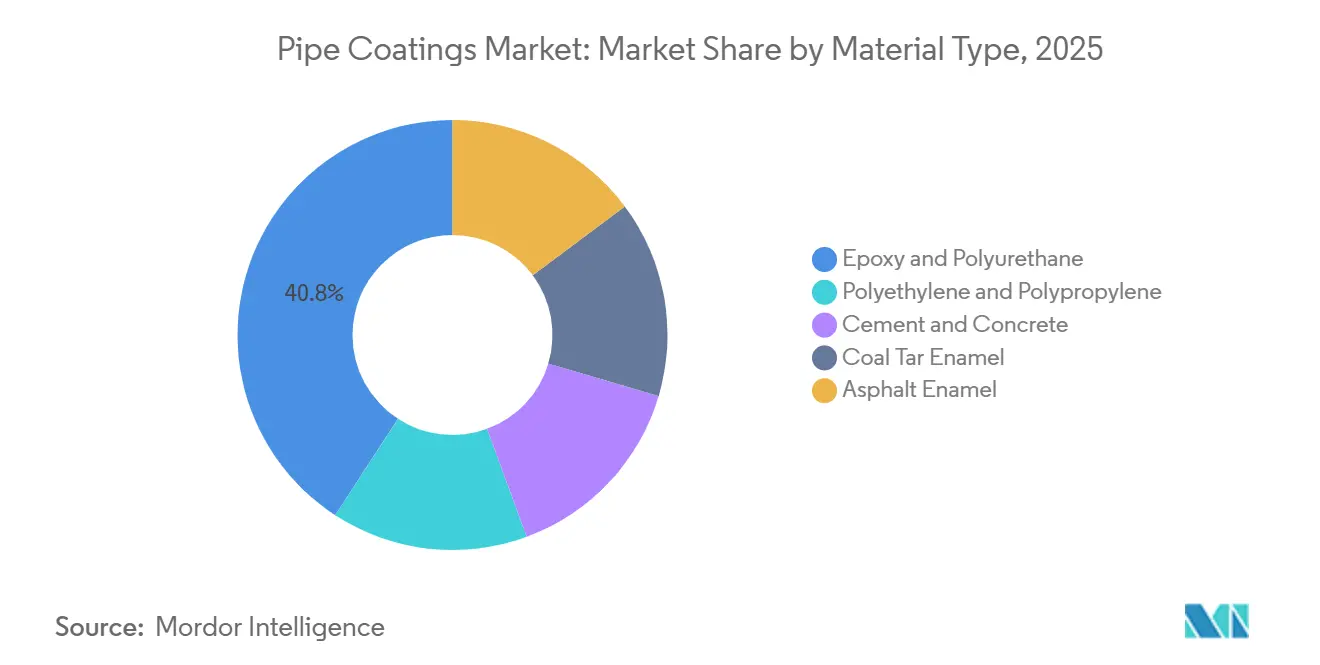

- By material type, epoxy and polyurethane led with 40.81% of the pipe coatings market share in 2025 and are forecast to expand at a 4.95% CAGR through 2031.

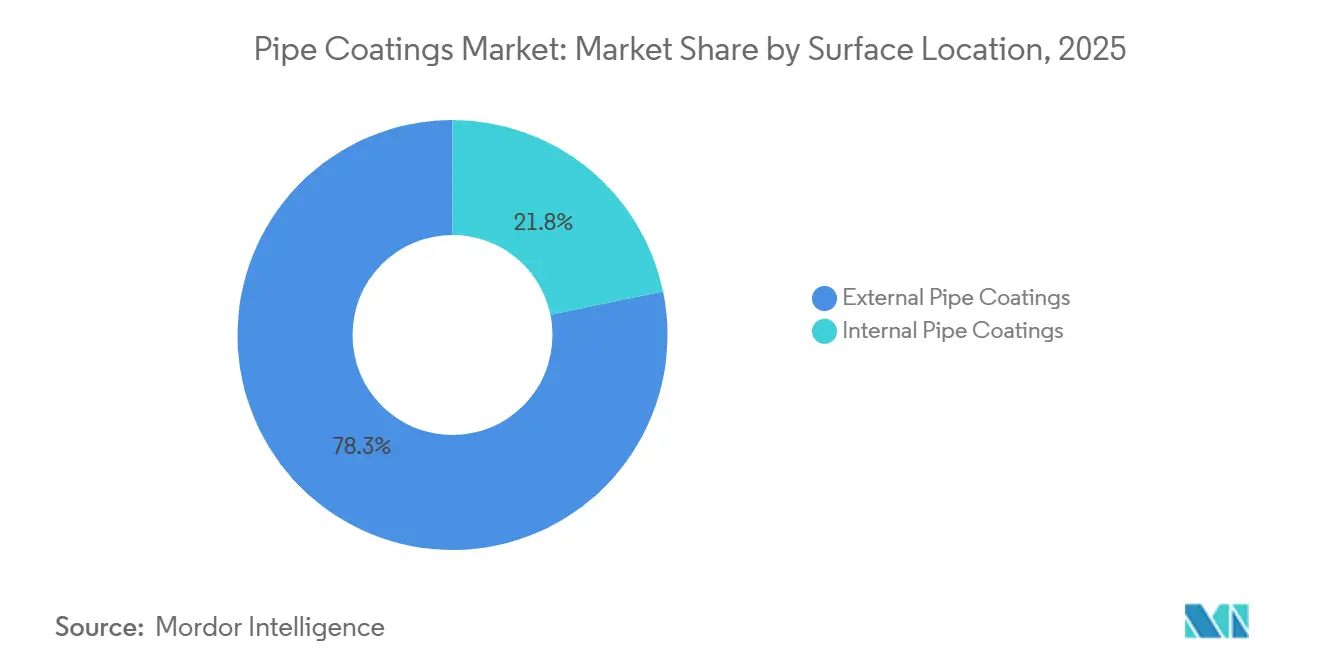

- By surface location, external coatings accounted for 78.25% of the pipe coatings market size in 2025 and are advancing at a 5.26% CAGR to 2031.

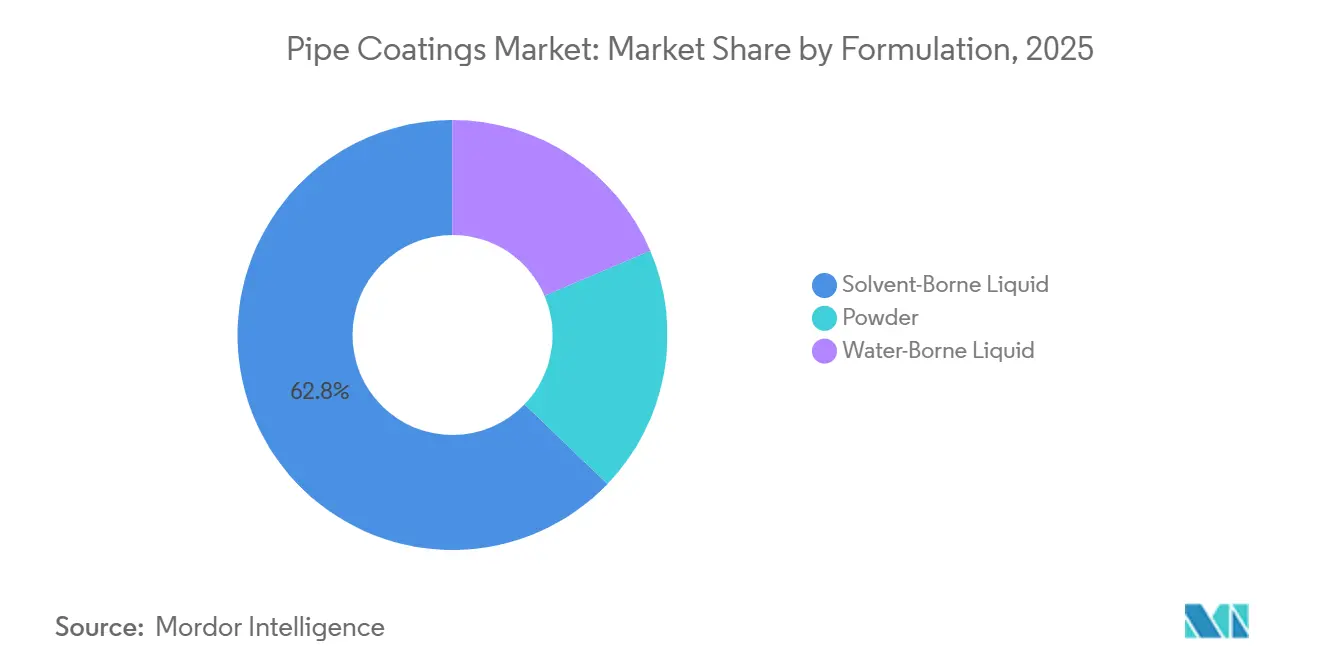

- By formulation, solvent-borne liquid held 62.81% share in 2025, whereas water-borne liquid is registering the fastest 5.12% CAGR to 2031.

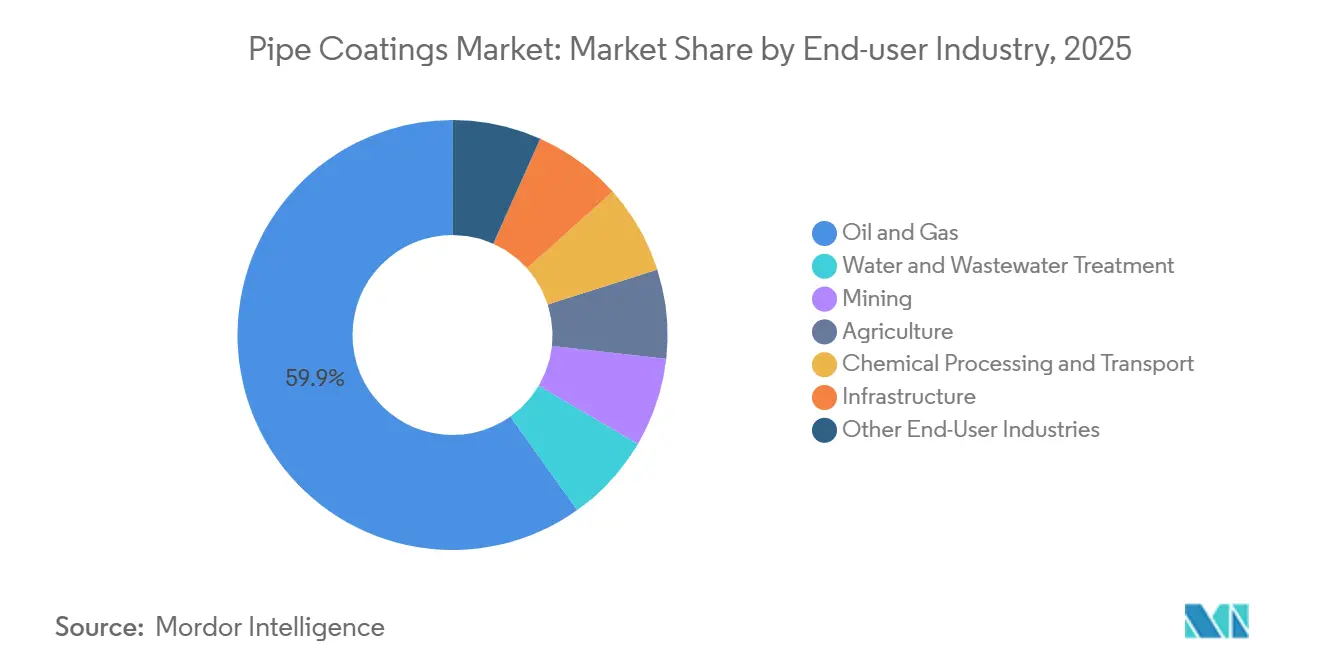

- By end-user industry, oil and gas commanded 59.85% of the pipe coatings market share in 2025 and is set to grow at a stronger 4.84% CAGR to 2031.

- By geography, North America captured 31.57% of the pipe coatings market in 2025 and is projected to log a 5.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pipe Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Shale Gas Capacity Additions Accelerating Maintenance Cycles | +0.9% | North America, with spillover to Canada and Mexico | Medium term (2-4 years) |

| Rising Adoption of High-Performance Coatings for Corrosion Protection in Pipelines | +1.2% | Global, with concentration in North America, Europe, and Middle East | Long term (≥ 4 years) |

| Growing Infrastructure and Industrialization in the Asia-Pacific Region | +1.1% | APAC core (China, India, ASEAN), spillover to South Asia | Long term (≥ 4 years) |

| Rise in Irrigation and Agricultural Activities in Southeast Asia | +0.4% | Southeast Asia (Indonesia, Vietnam, Thailand, Philippines) | Medium term (2-4 years) |

| Accelerating Demand for Energy Infrastructure in Europe | +0.8% | Europe, with concentration in Germany, Netherlands, Belgium, and Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Shale Gas Capacity Additions Accelerating Maintenance Cycles

Natural-gas pipeline construction in the United States added 17.8 billion cubic feet per day of capacity in 2024, compressing inspection intervals and pushing operators toward faster-curing fusion-bonded epoxy (FBE) and three-layer polyethylene systems. Federal Energy Regulatory Commission dockets list 127 additional projects spanning 15,000 miles, each subject to stringent Pipeline and Hazardous Materials Safety Administration integrity rules. To minimize downtime during tie-ins, suppliers are commercializing rapid-cure epoxies that achieve handling strength in less than 30 minutes. Liquids-rich shale plays such as the Marcellus and Haynesville introduce erosion-corrosion, elevating demand for abrasion-resistant overcoats. As a result, maintenance cycles that once stretched 10–15 years now average 7–10 years, creating recurring revenue streams for applicators concentrated in Texas, Oklahoma, and Pennsylvania.

Rising Adoption of High-Performance Coatings for Corrosion Protection in Pipelines

Corrosion drives roughly one-quarter of global pipeline failures, propelling uptake of advanced FBE, polyurethane, and zinc-rich systems that extend service life past 50 years under moderate soil conditions. Breakthroughs include zinc-based self-healing primers validated by the National Energy Technology Laboratory that galvanically repair micro-cracks, eliminating emergency recoats[1]National Energy Technology Laboratory, “Self-Healing Zinc-Rich Primers for Pipelines,” netl.doe.gov . Graphene-oxide and carbon-nanotube fillers cut water permeation by 40%, and UV LED-curable field-joint products shrink laydown schedules. Updated ISO 21809 standards published in 2024 tightened cathodic-disbondment thresholds, essentially phasing out coal-tar enamels for new builds. Middle-East operators are specifying high-temperature epoxies rated at 150 °C for sour-gas lines, a requirement that extends qualification cycles to 18 months.

Growing Infrastructure and Industrialization in the Asia-Pacific Region

China commissioned more than 4,000 kilometers of new pipelines in 2024, highlighted by the 5,111-kilometer China–Russia eastern-route gas trunkline that required over 2 million m² of three-layer polyethylene coating to resist permafrost and seismic stresses. India targets a gas network of 35,000 kilometers by 2030, supported by a 60% rise in demand to 103 billion m³ annually. Regional projects such as the Mumbai–Nagpur–Jharsuguda pipeline specify epoxy–polyurethane systems, while the Asian Development Bank anticipates USD 200 billion in yearly ASEAN infrastructure outlays, 40% earmarked for energy and water. Regulatory harmonization toward ISO 21809 and NACE SP0169 is trimming reliance on asphalt enamels that fall short on longevity.

Rise in Irrigation and Agricultural Activities in Southeast Asia

Government-backed irrigation upgrades across Vietnam, Thailand, Indonesia, and the Philippines are swapping open canals for pressurized steel and HDPE pipelines. Vietnam alone installed 1,200 kilometers in 2024, integrating epoxy linings to prevent contamination of fertilizer-laden waters. Thailand’s Royal Irrigation Department is retrofitting canals with FBE-coated buried lines to combat seepage losses that historically exceeded 30%. Seasonal wet–dry cycles accelerate delamination, prompting hybrid epoxy-polyurethane blends that absorb thermal expansion. The migration to pipe networks is most intense on Java and Sumatra, where land scarcity squeezes rice cultivation and demands efficient water delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Operational Challenges in Newly Discovered Energy Reserves | -0.5% | Arctic, ultra-deepwater Gulf of Mexico, offshore West Africa | Medium term (2-4 years) |

| Rising Adoption of Trenchless PE Pipe in Municipal Water Supply | -0.3% | North America and Europe, with early adoption in urban centers | Short term (≤ 2 years) |

| Competition from Renewable Energy Substitutes | -0.7% | Europe, North America, with early adoption in Scandinavia and California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Operational Challenges in Newly Discovered Energy Reserves

Ultra-deepwater fields at depths beyond 2,000 meters expose coatings to 3,000 psi hydrostatic pressure and near-freezing temperatures that accelerate cathodic disbondment. Arctic projects face freeze–thaw micro-cracking and permafrost-induced bending stress, limiting conventional epoxy performance. High-temperature sour-gas reservoirs such as Saudi Arabia’s Jafurah demand epoxies rated 150 °C and verified hydrogen-sulfide resistance, extending material qualification timelines and adding 20–40% to per-kilometer costs. Some operators gravitate toward corrosion-resistant alloys that bypass coatings, constraining market volume growth.

Rising Adoption of Trenchless PE Pipe in Municipal Water Supply

Municipal utilities in North America and Europe are increasingly turning to high-density polyethylene (HDPE) for trenchless rehabilitation because it offers 50-year service lives without exterior coatings. The U.S. Environmental Protection Agency’s latest needs survey earmarks USD 625 billion for drinking-water infrastructure, with a growing slice allocated to HDPE and PVC rather than coated steel[2]U.S. Environmental Protection Agency, “7th Drinking Water Infrastructure Needs Survey,” epa.gov . As urban dig-sites tighten, horizontal-directional drilling favors welded PE strings, suppressing demand for internal epoxy linings in distribution mains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Epoxy Formulations Anchor Market Share

Epoxy and polyurethane held 40.81% of the pipe coatings market in 2025, underlining their strong hold over high-pressure gas and sour-service pipelines. Fusion-bonded epoxy remains the go-to external solution, with field data confirming 50-year service life for moderate soils. Self-healing zinc-rich primers verified by NETL promise to trim recoating cycles and are drawing interest from North American and Middle-Eastern operators seeking life-cycle cost reductions. In contrast, coal-tar enamel is in structural decline following the 2024 ISO 21809 revision. Polyethylene and polypropylene tri-layer wraps dominate ultra-deepwater and Arctic deployments where flexibility and low-temperature resilience outweigh cost premiums.

Graphene-infused epoxies that slash water permeation by 40% are graduating from pilot to commercial scale in 2026. Polyethylene demand receives a lift from China’s permafrost corridors and Brazil’s pre-salt flowlines, whereas cement-mortar linings stay entrenched in large-diameter municipal mains. Suppliers are increasingly pairing powder-applied FBE primers with liquid polyurethane topcoats to achieve dual-layer protection without disrupting shop throughput.

By Surface Location: External Coatings Dominate on Soil-Side Priorities

External pipe coatings comprised 78.25% of 2025 revenue and are set to expand at a 5.26% CAGR, reflecting operator emphasis on soil-side corrosion, which is responsible for roughly one-fifth of pipeline failures. Cathodic-protection retrofits and drone-enabled inspection regimes are reinforcing demand, while tightening high-consequence-area rules in the United States accelerate recoating intervals. Internal linings retain a niche in water, chemical, and multiphase oil lines, where flow-efficiency improvements offset higher upfront costs.

Operators are trialing UV LED-curable overwraps for field-joint protection, cutting cure times from hours to minutes. Internal linings grow alongside U.S. lead-service-line removals and Asian city-gas expansion, though HDPE substitution in municipal water tempers upside. Advanced phenolic epoxies rated for 180 °C service are gaining share in ethylene and ammonia lines, where product purity is critical.

By Formulation: Solvent-Borne Liquids Face Environmental Headwinds

Solvent-borne liquid commanded a 62.81% share in 2025, buoyed by ease of application for field joints and repairs in remote oilfields. However, water-borne liquid is advancing at a 5.12% CAGR under VOC pressure from the European Industrial Emissions Directive, which caps emissions at 50 g/L. Powder coatings enjoy zero-VOC status but remain largely shop-applied due to oven-curing requirements.

Akzo Nobel and PPG have launched water-borne systems that meet ISO 21809 adhesion norms, eroding the historical performance gap with solvent-borne rivals. Middle-Eastern and Southeast Asian contractors still prefer solvent-borne liquids where ambient humidity and limited power supply complicate water-borne deployment.

By End-user Industry: Oil and Gas Sustains Leadership Amid Energy Transition

Oil and gas generated 59.85% of revenue in 2025 and continues to anchor demand despite the energy transition. Saudi Aramco’s USD 110 billion Jafurah unconventional program alone calls for more than 1,000 kilometers of high-temperature epoxy-covered lines. Deepwater tie-backs in the Gulf of Mexico and West Africa require tri-layer polypropylene for thermal insulation and hydrostatic resistance. The water and wastewater segment is the fastest-growing vertical as the U.S. EPA identifies USD 422.9 billion in pipe replacement needs and Europe accelerates lead-service-line retirement.

Mining tailings pipelines favor polyurethane topcoats to resist abrasion, while agricultural irrigation lines in Southeast Asia increasingly specify hybrid epoxy-polyurethane blends to manage thermal cycling.

Geography Analysis

North America maintained leadership with 31.57% share in 2025, underpinned by 17.8 billion cfd of new U.S. gas-pipeline capacity in 2024 and 127 additional projects in FERC queues. Trans Mountain’s expansion wrapped up in 2024, adding 590,000 bpd of epoxy-coated capacity between Alberta and British Columbia. Canada is also testing graphene-reinforced FBE on its Arctic-bound Mackenzie corridor, while Mexico’s Pemex plans to swap 500 kilometers of legacy steel lines for epoxy-polyurethane variants by 2027. Federal infrastructure grants worth USD 6 billion to modernize water mains further buoy internal lining demand across U.S. cities.

Asia-Pacific is closing the gap, anchored by China’s 5,111-kilometer eastern-route pipeline delivering 38 billion m³ per year and India’s goal of 35,000 kilometers of gas grid by 2030. ASEAN governments commit over USD 200 billion annually to energy and water projects, pushing the pipe coatings market in Indonesia, Vietnam, and Thailand into double-digit growth for municipal and irrigation lines. Powder coating adoption is rising in South Korea and Japan, where factory-prefabricated spools streamline labor and quality control.

Europe, while pivoting from hydrocarbons, channels substantial funds into hydrogen-ready lines. The European Hydrogen Backbone envisions 31,000 kilometers by 2040, providing a medium-term floor for demand even as fossil pipelines wane. Strict VOC caps propel water-borne uptake, and Germany’s offshore wind-to-X energy islands call for novel polyurethane formulations that withstand hydrogen embrittlement. South America’s growth stems from Brazil’s pre-salt cluster and Argentina’s Vaca Muerta shale, whereas African demand hinges on Nigerian LNG corridors and East African crude initiatives.

Competitive Landscape

The top five suppliers—PPG Industries, The Sherwin-Williams Company, Akzo Nobel, 3M, and Jotun—control roughly 45–50% of global revenue, giving the sector a moderate level of concentration. These majors leverage bulk raw-material contracts, regional application centers, and long-term maintenance frameworks to secure annuity-style cash flows. BASF’s EUR 7.7 billion carve-out of its coatings division to Carlyle in October 2025 marks a strategic retreat from commoditized architectural paints toward higher-margin industrial and protective niches. Sherwin-Williams expanded its South American footprint by acquiring BASF’s Brazilian decorative business for USD 1.15 billion, improving access to Petrobras-linked pipeline contractors.

Regional challengers in Southeast Asia and the Middle-East differentiate through agile technical support and shorter lead times for project-specific blends, chipping away at tier-one incumbents. Innovation themes include zinc-nanoparticle self-healing primers that NETL pilot-tested on Permian Basin lines and graphene-oxide hybrids moving into commercial batches in 2026. ISO 21809’s stricter 2024 update heightens entry barriers by mandating verified cathodic-disbondment data, favoring integrated suppliers with certified labs. M&A activity is expected to continue as majors shed non-core units and private equity funds pursue bolt-ons to build protective-coatings platforms.

Pipe Coatings Industry Leaders

Akzo Nobel N.V.

Jotun

PPG Industries, Inc.

The Sherwin-Williams Company

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Tenaris secured a contract to provide pipe coating services for the Búzios 11 project in offshore Brazil. The contract involved insulating 12 km of pipes using TenarisShawcor Marine 5-Layer Syntactic and Marine 5-Layer Solid coatings, which were applied at Confab, Tenaris’s facility in Pindamonhangaba, Brazil.

- April 2025: The Federal Government, through the Nigerian Content Development and Monitoring Board (NCDMB), commissioned Monarch Alloys Limited's pipe coating facility in Ikorodu, Lagos State. This initiative aimed to enhance local content in the oil and gas industry, reduce imports, and generate employment by offering 3LPE and concrete weight coatings for pipelines.

Global Pipe Coatings Market Report Scope

Pipe coatings are applied as a protective lining that helps in saving pipelines from the damaging effects of corrosion. Additionally, it provides longer life to the pipelines.

The pipe coatings market is segmented into material type, surface location, formulation, end-user industry, and geography. By material, the market is segmented into epoxy and polyurethane, polyethylene and polypropylene, cement and concrete, coal tar enamel, and asphalt enamel. By surface location, the market is segmented into external pipe coatings and internal pipe coatings. By formulation, the market is segmented into solvent-borne liquid, powder, and water-borne liquid. By end-user industry, the market is segmented into oil and gas, water and wastewater treatment, mining, agriculture, chemical processing and transport, infrastructure, and other end-user industries. The report also covers the market size and forecasts for the pipe coatings in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Epoxy and Polyurethane |

| Polyethylene and Polypropylene |

| Cement and Concrete |

| Coal Tar Enamel |

| Asphalt Enamel |

| External Pipe Coatings |

| Internal Pipe Coatings |

| Solvent-Borne Liquid |

| Powder |

| Water-Borne Liquid |

| Oil and Gas |

| Water and Wastewater Treatment |

| Mining |

| Agriculture |

| Chemical Processing and Transport |

| Infrastructure |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Epoxy and Polyurethane | |

| Polyethylene and Polypropylene | ||

| Cement and Concrete | ||

| Coal Tar Enamel | ||

| Asphalt Enamel | ||

| By Surface Location | External Pipe Coatings | |

| Internal Pipe Coatings | ||

| By Formulation | Solvent-Borne Liquid | |

| Powder | ||

| Water-Borne Liquid | ||

| By End-user Industry | Oil and Gas | |

| Water and Wastewater Treatment | ||

| Mining | ||

| Agriculture | ||

| Chemical Processing and Transport | ||

| Infrastructure | ||

| Other End-user Industries | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the pipe coatings market and its growth outlook?

The pipe coatings market size stands at USD 10.48 billion in 2026 and is projected to reach USD 13.13 billion by 2031 at a 4.61% CAGR.

Which segment holds the largest share in surface location in 2025?

External pipe coatings lead with 78.25% share in 2025 because operators focus on soil-side corrosion protection.

Why are epoxy and polyurethane systems preferred in high-pressure gas lines?

They combine strong adhesion, chemical resistance, and compatibility with cathodic protection, delivering service lives beyond 50 years.

How will hydrogen infrastructure influence coating demand?

Europe’s planned 31,000-kilometer hydrogen backbone will require specialized coatings that resist hydrogen embrittlement, creating a new medium-term market niche.

Page last updated on: