Unidirectional Tape Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

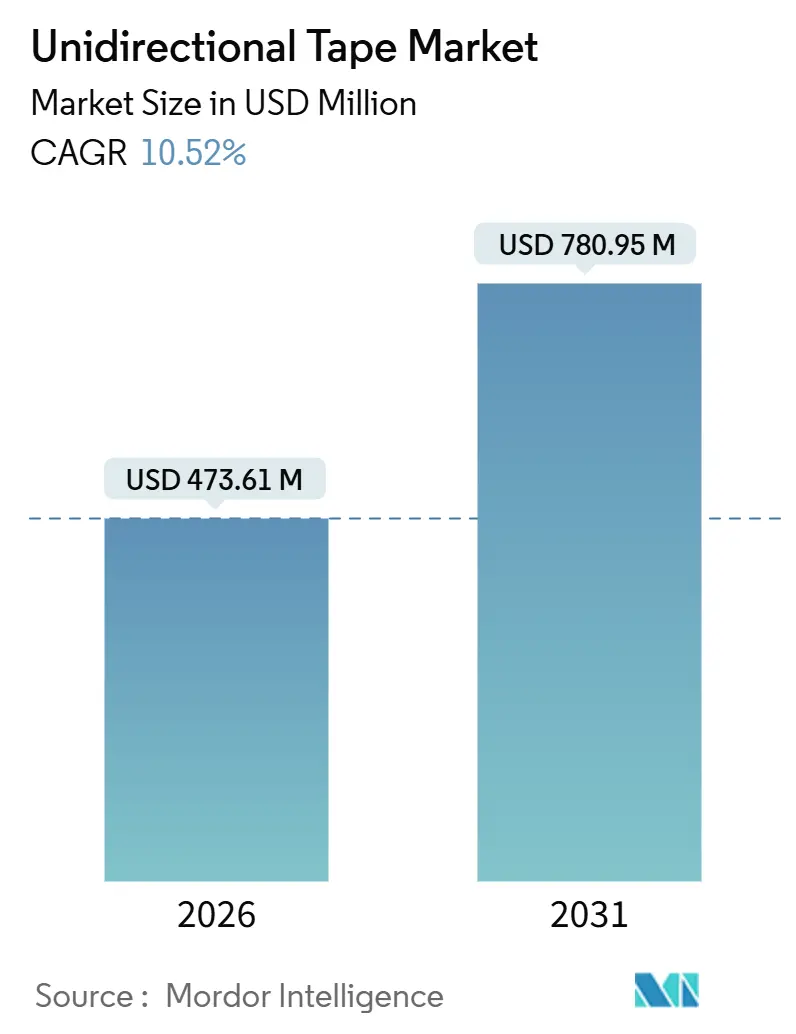

| Market Size (2026) | USD 473.61 Million |

| Market Size (2031) | USD 780.95 Million |

| Growth Rate (2026 - 2031) | 10.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

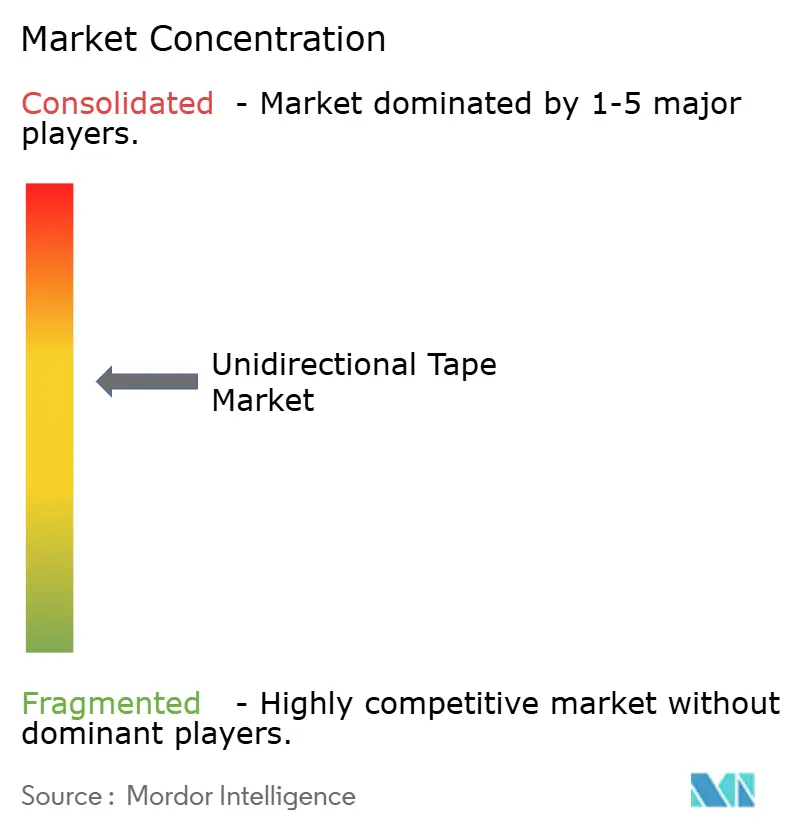

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unidirectional Tape Market Analysis by Mordor Intelligence

The Unidirectional Tape Market size is estimated at USD 473.61 million in 2026, and is expected to reach USD 780.95 million by 2031, at a CAGR of 10.52% during the forecast period (2026-2031). Continuous demand from aerospace primes, automotive OEMs, and wind-turbine manufacturers to cut structural weight while improving production efficiency anchors this momentum. Carbon fiber remains the reinforcement mainstay for high-performance applications, though glass fiber is rising quickly in offshore wind blades thanks to its cost advantage and acceptable modulus. Polyamide matrices dominate automotive crash structures, whereas thermoplastic PEEK is gaining favor in high-temperature aerospace ducts. Asia-Pacific has emerged as the production center of gravity on the back of Chinese wind-blade investments and Japanese carbon-fiber capacity expansions. Meanwhile, recent patent activity in thermoplastic consolidation hints at a race among incumbents to secure intellectual property around faster, out-of-autoclave processing routes.

Key Report Takeaways

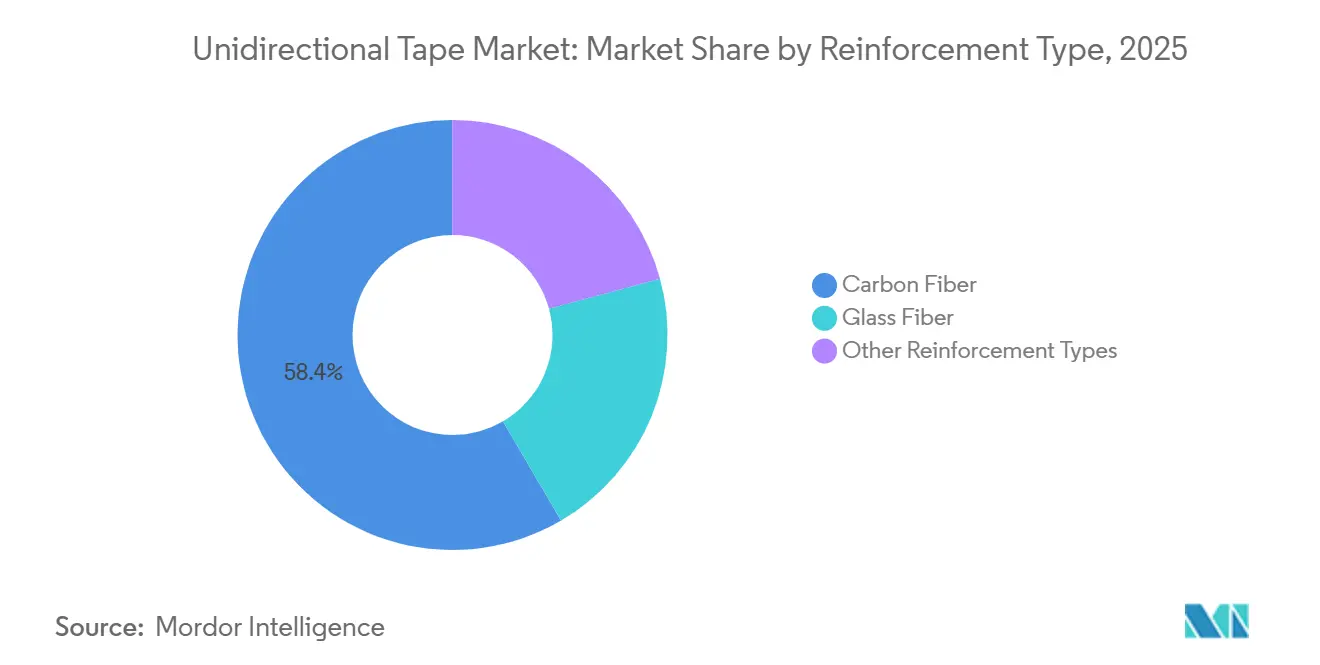

- By reinforcement type, carbon fiber led with 58.42% revenue share in 2025; glass fiber is poised to grow at 9.25% CAGR through 2031.

- By backing material, polyamide captured a 31.36% share in 2025; PEEK is projected to expand at a 9.68% CAGR to 2031.

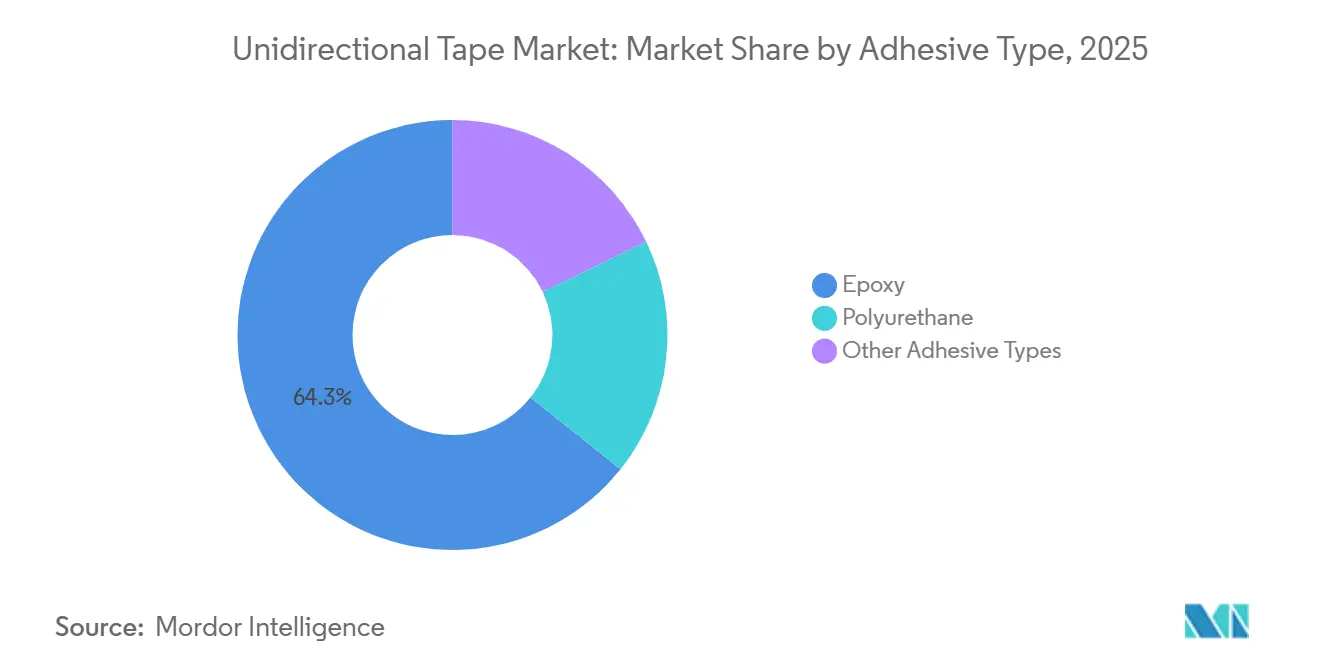

- By adhesive type, epoxy accounted for 64.27% of the 2025 volume; polyurethane is advancing at a 9.12% CAGR through 2031.

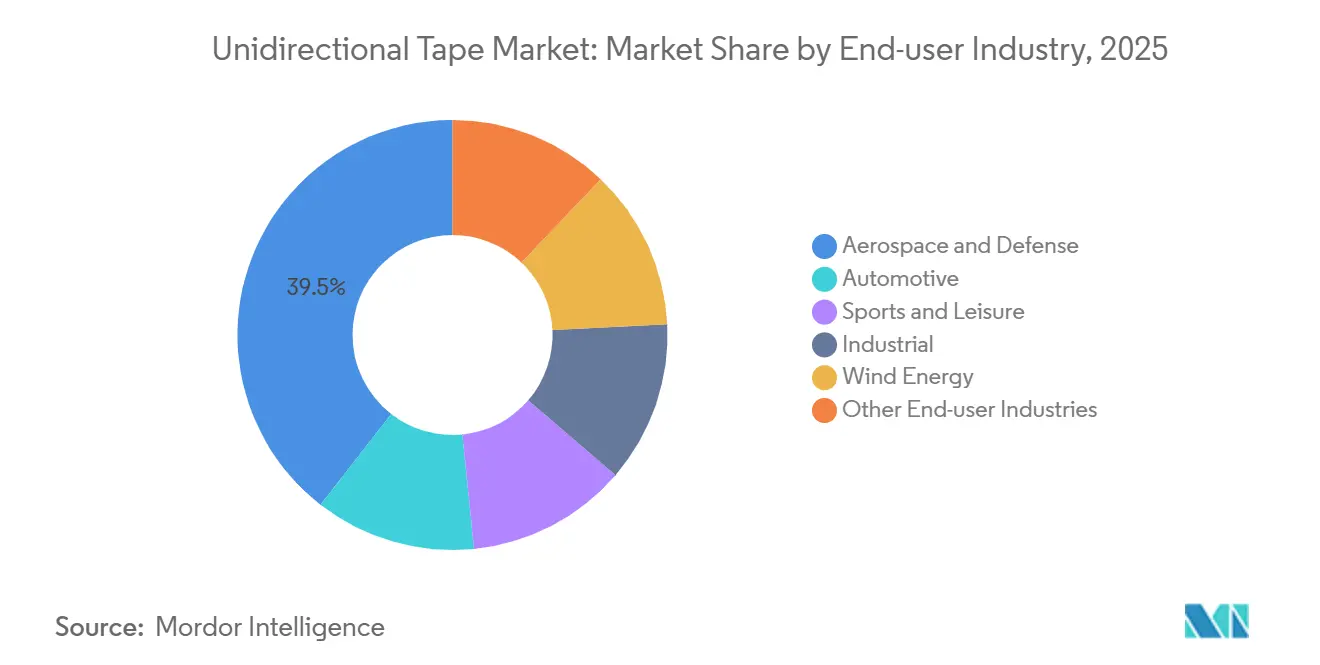

- By end-user industry, the aerospace and defense segment commanded 39.48% revenue share in 2025 and is forecast to grow at 10.69% CAGR to 2031.

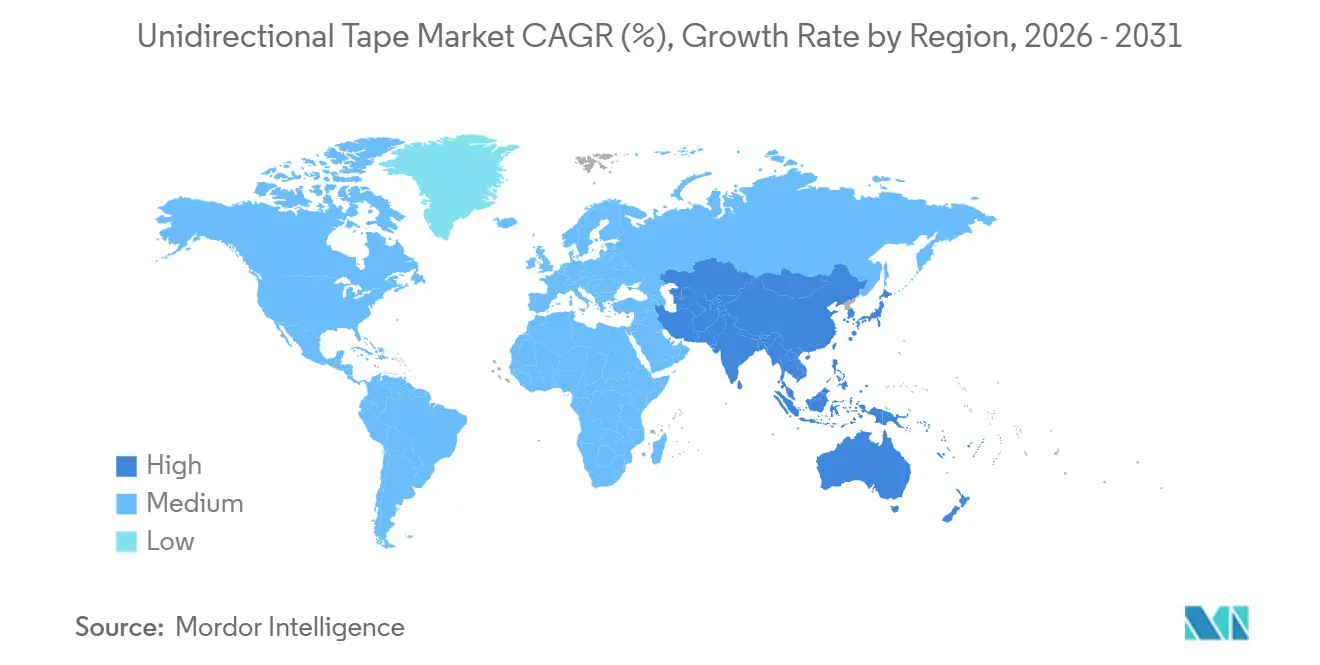

- By geography, Asia-Pacific held a 44.53% share in 2025; it is projected to rise at a 10.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Unidirectional Tape Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging composite demand in next-gen narrow-body aircraft | +2.8% | Global concentration in North America and Europe | Medium term (2-4 years) |

| Aggressive OEM lightweighting targets for 800 V EV platforms | +2.3% | APAC core, spillover to North America and Europe | Short term (≤ 2 years) |

| Rise of automated tape-laying lines in Chinese wind-blade factories | +1.9% | APAC (China dominant), secondary impact in India | Medium term (2-4 years) |

| Certification of thermoplastic tapes for hydrogen pressure vessels | +1.4% | Japan, South Korea, Germany, California (US) | Long term (≥ 4 years) |

| Defense need for radar-transparent structures and stealth kits | +1.2% | North America, Europe, Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Composite Demand in Next-Gen Narrow-Body Aircraft

Programs like the Airbus A321XLR and Boeing 737 MAX are increasingly using carbon-fiber tape in their fuselage panels, spars, and floor beams to reduce airframe weight. NASA's HiCAM trials demonstrated that automated tape-laying can significantly reduce the cycle time for fuselage sections, highlighting its potential for high-rate production[1]NASA, “High-Rate Composite Aircraft Manufacturing,” nasa.gov. Suppliers with established databases gain an advantage due to qualifications under FAA AC 20-107B and EASA AMC 20-29, creating a protective barrier for existing players. Given that narrow-body jets represent a significant portion of anticipated future deliveries, even slight increases in composite content lead to substantial demand in the unidirectional tapes market. Anticipated certification milestones in 2026-2027 further bolster demand projections.

Aggressive OEM Lightweighting Targets for 800 V EV Platforms

Premium carmakers, targeting a 500 km range with 800 V architectures, are pushing for a reduction in battery-enclosure mass. Recent crash tests on the Lucid Air have showcased a breakthrough: thermoplastic tapes can craft intricate tray shapes that achieve the stiffness of stamped steel, but at a significantly lower weight. However, the high capital costs pose a challenge for Tier-2 adoption. Each AFP cell commands a high price, and the programming demands significant labor. In response, Chinese OEMs are taking the reins by vertically integrating tape production, managing to cut part costs. This move solidifies Asia's lead in the burgeoning unidirectional tapes market.

Rise of Automated Tape-Laying Lines in Chinese Wind-Blade Factories

In Jiangsu and Tianjin, robotic tape-laying cells are now applying glass-fiber tapes, making hand layup uneconomical for offshore turbines with blade lengths surpassing 115 m. This shift results in a significant reduction in labor content and a measurable improvement in fiber alignment, enhancing blade quality. The use of polyamide and polypropylene matrices facilitates in-situ consolidation, cutting trimming cycle times substantially. India's Suzlon is adopting this model, signaling a regional trend that bolsters the unidirectional tapes market throughout Asia.

Certification of Thermoplastic Unidirectional Tapes for Hydrogen Pressure Vessels

Type IV hydrogen tanks must survive cycles at high pressure per ISO 19881. Toyota and Hyundai trials with PEEK-backed tapes show assembly-time cuts through in-situ welding, while maintaining burst pressure. European PED 2014/68/EU certification, a lengthy process, remains a gatekeeper, yet once cleared, thermoplastic tapes could open a sizeable niche for the unidirectional tapes market in fuel-cell mobility.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent carbon-fiber price volatility tied to PAN precursor supply | −1.6% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Low pull-through rates of AFP equipment among Tier-2 auto suppliers | −1.1% | North America and Europe | Medium term (2-4 years) |

| Recycling and end-of-life mandates tightening in EU | −0.8% | Europe, spillover to UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Carbon-Fiber Price Volatility Tied to PAN Precursor Supply

After China imposed export curbs in 2024, spot prices for PAN surged, driven by China's dominant share in the market[2]Mitsubishi Chemical, “PAN Precursor Supply Chain,” mitsubishichem.com. In 2025, Hexcel and SGL Carbon experienced a drop in gross margins, unable to hedge against losses due to their fixed-price aerospace contracts. While new precursor lines set to debut in 2027 offer some respite, the 30-month lead times combined with geopolitical uncertainties ensure continued volatility in the cost base of the unidirectional tapes market.

Low Pull-Through Rates of AFP Equipment Among Tier-2 Auto Suppliers

AFP cells pose a financial challenge for Tier-2 suppliers, who operate on slim net margins. Design modifications necessitate expensive re-validations, constraining composite specifications on platforms with diverse mixes. In both Germany and the U.S., labor unions push back against automation, resulting in underutilized equipment and a hesitance to invest. In contrast, counterparts in Asia benefit from government subsidies that can cover a significant portion of their equipment expenses, amplifying the competitive divide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Reinforcement Type: Carbon Fiber Dominates, Glass Fiber Gains in Wind

Carbon fiber captured 58.42% of 2025 revenue, highlighting its significance in aerospace primary structures, where its fatigue resistance justifies a premium. Both Boeing's 787 and Airbus's A350 heavily utilize carbon-fiber tape for their wing spars and fuselage frames. Glass fiber, though less stiff, is surging at 9.25% CAGR. This rise is driven by the offshore wind blades exceeding 115 m in length, which necessitates cost-effective spar-cap materials. Consequently, the market size for unidirectional tapes in the glass-fiber segment is set to expand steadily through 2031. Hybrid carbon-glass tapes, like Hexcel's HiTape, strike a balance between cost and modulus, finding their niche in automotive battery enclosures.

In emerging markets, Chinese turbine OEMs are opting for glass-fiber tapes in their 8-12 MW platforms, a trend echoed by Indian manufacturers. While aramid and basalt fibers cater to niche markets—primarily ballistic armor and high-temperature industrial applications—together they hold a modest share. Given these market dynamics, while carbon fiber is poised to maintain its dominance, the absolute tonnage gains of glass fiber will play a crucial role in shaping the unidirectional tapes market in the coming five years.

By Backing Material: Polyamide Leads, PEEK Surges in High-Temperature Niches

Polyamide backing held 31.36% of 2025 demand due to its balanced processing window, impact toughness, and moisture resistance, traits suited for automotive crash structures. PEEK is expanding at 9.68% CAGR as engine-bay brackets and bleed-air ducts migrate to thermoplastics capable of withstanding 200 °C continuous temperatures. The unidirectional tapes market share for PEEK applications should therefore expand gradually, especially after aerospace certifications are finalized in 2027.

Polypropylene remains popular where cost trumps performance, for example, in wind-blade shear webs. PPS and PC round out the portfolio with specialty applications in chemical processing and electronics. Solvay’s KetaSpire PEEK is also penetrating downhole oil-and-gas tools, underscoring the widening high-temperature envelope for thermoplastic tapes.

By Adhesive Type: Epoxy Dominates, Polyurethane Gains in Automotive

Epoxy systems accounted for 64.27% of 2025 volume, underscoring their mechanical reliability and the extensive material databases built over decades of aerospace service. Yet polyurethane formulations are advancing at a 9.12% CAGR. Their advantage lies in an 80-100 °C curing range, enabling energy-efficient aluminum tooling—a significant perk for automotive Tier-1 suppliers. While the market for polyurethane-bonded unidirectional tapes remains modest, it's poised for substantial growth with the rollout of 800 V EV platforms.

Though phenolics and bismaleimides cater to high-temperature applications, their market share remains limited due to challenges like brittleness and processing intricacies. Notably, Henkel’s Loctite polyurethanes are being tested for hybrid joints that combine composites and steel, addressing a common issue where epoxies struggle: differential thermal expansion.

By End-User Industry: Aerospace and Defense Leads, Wind Energy Accelerates

The aerospace and defense segment contributed 39.48% of 2025 revenue and is projected to grow at a 10.69% CAGR to 2031, fueled by narrow-body production ramp-ups and stealth-oriented defense programs. Automotive adoption is clustered among premium EVs but will climb as cost curves on thermoplastics bend downward. Wind energy already represents the second-largest slice, and the unidirectional tapes market size for offshore blade applications will expand with every turbine power-rating jump. Sports and leisure remain high-margin niches, whereas industrial cylinders and marine structures add steady, if smaller, volume growth.

Geography Analysis

Asia-Pacific generated 44.53% of 2025 revenue and is projected to grow at a 10.88% CAGR to 2031, driven by China's extensive wind-blade production, Japan's advancements in carbon-fiber technology, and South Korea's adoption of EV battery trays. In Jiangsu, automated tape-laying cells achieved high fiber alignment consistency, minimizing waste and solidifying China's cost advantage. Toray's facility in Ehime bolsters regional supply, while a new tape line in Hyderabad caters to India's domestic aerospace needs. Although smaller ASEAN markets currently rely on imports, they stand poised to adapt swiftly, especially as the demand for battery-electric two-wheelers rises, further boosting the unidirectional tapes market.

North America accounted for a notable share of the 2025 revenue. Boeing's Everett facility, as the 737 MAX production stabilizes, utilizes a significant amount of carbon-fiber tape annually. Additionally, Lockheed Martin's F-35 and MQ-25 programs bolster defense demand. Yet, the automotive sector hesitates: both General Motors and Ford point to high recycling costs and inconsistent material pricing as concerns. Meanwhile, Mexico's expanding carbon-fiber hub in Querétaro hints at a diversifying supply chain, potentially benefiting the United States' electric truck initiatives.

Europe represented a considerable portion of the 2025 demand. Composite consumption remains anchored at Airbus facilities in Toulouse and Broughton, despite recyclability pressures from the End-of-Life Vehicles Directive. While German OEMs experiment with carbon-fiber battery trays for their premium models, widespread adoption hinges on achieving cost parity. Post-Brexit tariffs have squeezed margins for the United Kingdom converters, particularly affecting SMEs. In a notable shift, Spanish and Danish factories, pivoting to tape-laying, are now catering to 15 MW offshore turbines, a move likely to bolster the continent's unidirectional tapes market.

South America and the Middle East-Africa, together contributing a smaller share in 2025, exhibit emerging potential. While Embraer's E2 jets utilize locally produced prepregs, Saudi Arabia's NEOM is exploring hydrogen cylinders, potentially requiring thermoplastic tapes. Though these regional initiatives are modest, they diversify the unidirectional tapes industry's landscape and hold promise for growth as infrastructure develops.

Value Chain Analysis

The unidirectional tape value chain starts with reinforcement suppliers, including carbon fiber, glass fiber, and niche aramid and basalt. Feedstocks tied to PAN supply dynamics support carbon-fiber production, while resin and adhesive suppliers provide epoxy systems and thermoplastics such as PA, PEEK, PPS, and PP. Tape producers convert these inputs through fiber spreading and handling, impregnation using melt or powder routes, consolidation, and controlled cooling to produce slit tape formats and qualified material systems suited to demanding aerospace and high-rate industrial use.

Downstream, converters and Tier suppliers combine tapes with AFP/ATL and press-forming equipment to supply formed parts into aerospace and defense, automotive, wind energy, and industrial cylinder applications. Key bottlenecks sit in resin viscosity control during impregnation, fiber-alignment discipline to limit scrap, and qualification work that ties material suppliers, processors, and end users together. As a result, tape manufacturers increasingly coordinate with automation and equipment vendors, while out-of-autoclave processing development focuses on improving throughput and reducing part cost.

Competitive Landscape

The unidirectional tapes market is moderately consolidated. Regional specialists capture high-margin sports segments by leveraging spread-tow aesthetics. Chinese challengers leverage subsidies to underprice incumbents in wind energy and automotive, yet lack AS9100 certification for aerospace entry. The white space includes hydrogen and CNG pressure vessels, corrosion-proof marine structures, and lightweight urban-air-mobility airframes. Suppliers able to bundle material supply with process know-how stand to earn a premium as automation proliferates.

Unidirectional Tape Industry Leaders

TORAY INDUSTRIES INC.

Hexcel Corporation

TEIJIN LIMITED

Solvay

SABIC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space concentrates where thermoplastic unidirectional tapes can replace multi-step metal or thermoset layups with faster welding and in-situ consolidation, particularly in hydrogen and CNG pressure vessels (Type IV, aligned to ISO 19881 test needs) and in high-rate aerospace structures where qualification data packages can reduce friction for adoption. Outside these areas, demand expansion is also supported by wind-blade applications above 115 m, where automated tape-laying in Chinese factories is already changing labor content and improving fiber-alignment consistency. Premium EV battery enclosures offer another channel, as 800 V platform lightweighting targets push composite tray architectures.

In Europe, the opportunity is more immediate in efficiency and recyclability-focused product and process choices than in pure volume growth. AVK reported European composites production down 3% in 2025 to 2,281 kilotons. Thermoplastic composites totaled 1,329 kilotons in 2025, down from 1,368 kilotons in 2024, but still accounted for 58.3% of the European composites market, leaving a large installed thermoplastic base that can be served with lower-energy curing routes, automated forming, and recycled-content or circular feedstock initiatives as OEMs and Tier suppliers respond to tightening end-of-life expectations.

Recent Industry Developments

- June 2026: Toray Performance Materials Corporation introduced Stratex 2300r, a unidirectional carbon fiber composite incorporating post-consumer recycled PET content. The launch extends recycled-content positioning into unidirectional composite formats used in industrial and transportation structures, supporting customer programs that balance performance requirements with circularity goals.

- March 2026: Teijin Carbon announced full commercial availability of its expanded Tenax Next product line, including offerings tied to circular feedstock-based carbon materials. Broadening the commercial portfolio strengthens sourcing options for converters and OEMs seeking lower-footprint composite solutions while staying within established performance envelopes.

- September 2025: Teijin Carbon disclosed NCAMP qualification activity for Tenax IMS65 E23 24K non-crimp fabrics and woven unidirectional materials paired with Syensqo PRISM EP2400 epoxy resin system for VARTM infusion. The qualification pathway supports faster aerospace and defense adoption by reducing re-qualification effort across programs that depend on standardized, independently reviewed material and process data.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the unidirectional tape market is defined as revenues generated from UD composite tapes that align continuous fibers in one direction and are sold for structural reinforcement across industrial end uses.

Scope exclusions: It excludes finished composite parts, in-house tape production that is not sold, and general adhesive tapes used mainly for bonding or packaging.

Segmentation Overview

- By Reinforcement Type

- Glass Fiber

- Carbon Fiber

- Other Reinforcement Types

- By Backing Material

- Polyether Ether Ketone (PEEK)

- Polyamide (PA)

- Polypropylene (PP)

- Polycarbonate (PC)

- Polyphenylene Sulfide (PPS)

- Other Backing Materials

- By Adhesive Type

- Epoxy

- Polyurethane

- Other Adhesive Types

- By End-user Industry

- Aerospace and Defense

- Automotive

- Sports and Leisure

- Industrial

- Wind Energy

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by building a clean fact base on composites and end-use demand, since UD tape volumes are closely tied to aerospace build rates, vehicle lightweighting, and wind blade manufacturing. We reviewed public sources such as USGS materials statistics, UN Comtrade trade flows, US International Trade Commission data, and OECD industrial indicators to capture directional movement in relevant inputs.

To tie demand to realistic pricing, we also relied on sources such as SEC filings and annual reports, investor presentations, customs and trade releases, and technical papers from journals focused on composites and polymer processing. Patent databases were used to identify new resin systems and processing routes that can shift adoption, including higher temperature thermoplastics. Where needed, paid subscriptions for company financials and intelligence, patent databases, and import and export shipment-level views were used for cross-checks. These desk sources are illustrative only, and we also used other public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with UD tape manufacturers, raw material suppliers, converters, and downstream users that specify or purchase these tapes for components. Respondent input was used to sharpen assumptions on how qualification cycles differ by region and how pricing practices are handled across APAC, EMEA, and the Americas so regional production intensity can be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 15% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 36% | EMEA: 36% |

| Smaller Players: 18% | Managers: 49% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where end-use production and build indicators are converted into an addressable demand pool for UD tape, and then translated into value using typical usage rates and observed price bands. We then checked the totals through selective bottom-up approximations, where sampled supplier revenues, channel discussions, and ASP multiplied by estimated volume ranges were used to sanity-test key applications.

A few practical inputs that mattered in the model included aircraft and defense production cycles, automotive lightweighting penetration (especially in structural and semi-structural parts), wind turbine blade additions, and the split between carbon fiber and glass fiber reinforcement. We also tracked resin and backing preferences, including PPS, PP, and higher temperature families like PAEK/PA, because that mix affects achievable pricing and qualification timelines.

For forecasting, scenario analysis was used so base case growth could be tied to realistic adoption steps and capacity readiness, and then adjusted based on what interviewees expected for program ramp-ups and substitution rates. Where bottom-up data was missing for smaller applications, gaps were handled by using conservative penetration ranges, then rebalancing totals to match the broader demand pool checks.

Data Validation & Update Cycle

Outputs were validated through multiple checks, including cross-comparing implied tape demand against end-use production signals and checking whether the resulting ASP path stayed within interview-supported ranges. When a region or application showed an unusual jump, the drivers were re-tested and the underlying assumptions were reviewed again before sign-off.

A multi-step analyst review is followed, and follow-up calls are triggered when a key input changes materially, such as resin availability, major capacity expansions, or sudden shifts in aerospace or wind orders. The report is refreshed annually, with interim updates for material events, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Unidirectional Tape Market Size Measured Against Other Published Estimates

It is common to see different market sizes for UD tapes because publishers do not always use the same year, the same boundaries of what counts as UD tape revenue, or the same way of translating volume into value. Currency timing, the assumed adoption pace in aerospace and automotive, and how long qualification delays are modeled can also move the totals.

Key gaps usually come from whether thermoset and thermoplastic tapes are both counted, whether internal consumption is treated as market revenue, and how fast pricing is assumed to change as resin mix shifts toward higher temperature grades. By tracking end-use build indicators and refreshing ASP bands with interview checks, Mordor Intelligence keeps the model tied to sellable UD tape revenues rather than broader composite materials value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 473.61 M (2026) | |

| Global Consultancy A | USD 320.30 M (2024) | Uses an earlier base year and a shorter forecast window, and the value conversion can differ if volume-to-revenue uses aggressive ramp assumptions for automotive and aerospace adoption by 2025. |

| Industry Publisher B | USD 371.13 M (2025) | Starts from a 2025 base and often applies faster long-range growth to 2035, which can inflate near-term sizing if qualification lead times and regional capacity constraints are not tightened. |

The spread in reported values is mainly explained by base-year choice, scope boundaries around what is counted as market revenue, and how adoption and pricing are stepped forward over time. In our approach, the inputs are kept simple and traceable, so the final number can be followed back to clear demand signals and realistic price logic.

Key Questions Answered in the Report

What is the projected value of the unidirectional tapes market in 2031?

The sector is forecast to reach USD 780.95 million by 2031, expanding at a 10.52% CAGR, from USD 473.61 million in 2026.

Which reinforcement dominates current demand for unidirectional tapes?

Carbon fiber leads, representing 58.42% of 2025 revenue, due to its high stiffness-to-weight ratio.

Why is Asia-Pacific the largest regional consumer?

Chinese wind-blade automation, Japanese carbon-fiber capacity, and South Korean EV platforms combine to give the region a 44.53% share in 2025 with the fastest 10.88% CAGR outlook.

What challenges affect unidirectional tape adoption in Europe?

Tightened recyclability rules, limited composite recycling infrastructure, and carbon-fiber price volatility constrain broader uptake.

Which adhesive chemistry is gaining traction beyond epoxy?

Polyurethane tapes are growing at a 9.12% CAGR as their lower cure temperature reduces energy costs for automotive Tier-1 suppliers.

Page last updated on: