Pipe Insulation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

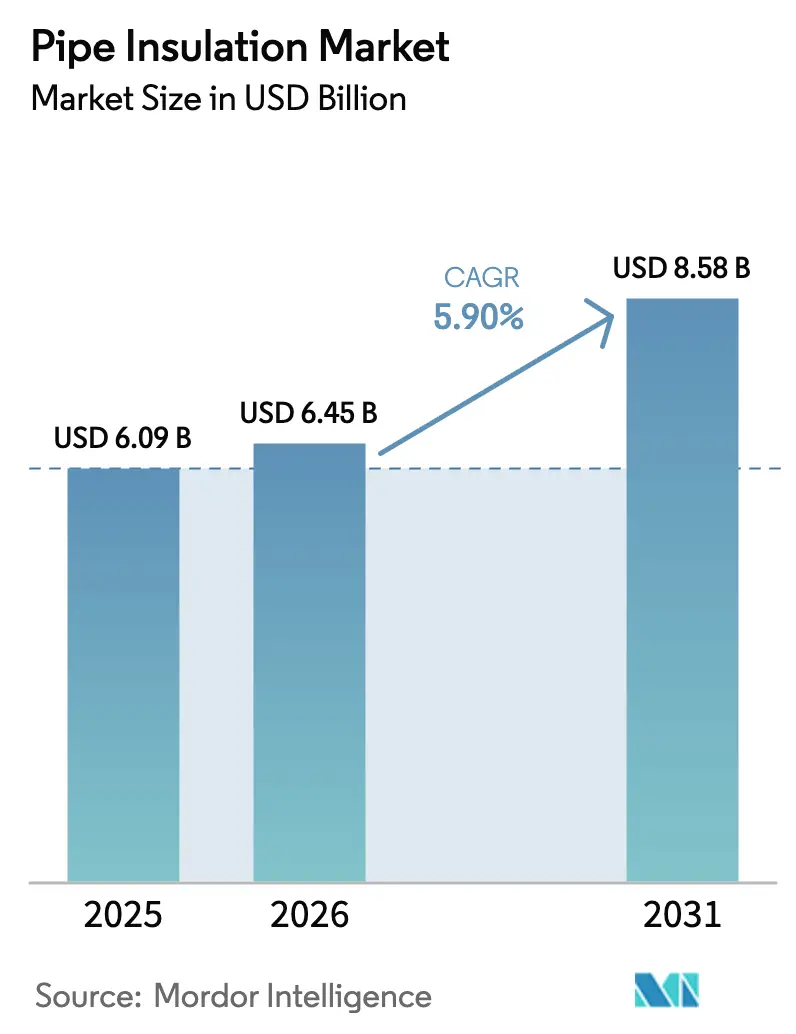

| Market Size (2026) | USD 6.45 Billion |

| Market Size (2031) | USD 8.58 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pipe Insulation Market Analysis by Mordor Intelligence

Pipe Insulation market size in 2026 is estimated at USD 6.45 billion, growing from 2025 value of USD 6.09 billion with 2031 projections showing USD 8.58 billion, growing at 5.90% CAGR over 2026-2031. Tighter building‐energy codes, industrial decarbonization mandates, and a wave of infrastructure upgrades keep the pipe insulation industry on a firm growth footing. North American and European building regulations demand thicker, higher-performance insulation, while Asia-Pacific governments link public-sector lending to demonstrable energy-savings targets. LNG export capacity additions and fourth-generation district heating networks extend the addressable opportunity well beyond conventional buildings. Competitive intensity has risen as large incumbents consolidate regional players, invest in smart-sensor platforms, and license advanced aerogel technologies. Although price volatility for petrochemical feedstocks and the spread of thin-wall plastic piping temper short-term margins, manufacturers with diversified materials portfolios and prefabricated installation solutions remain positioned to capture upside as global carbon-neutrality timetables accelerate.

Key Report Takeaways

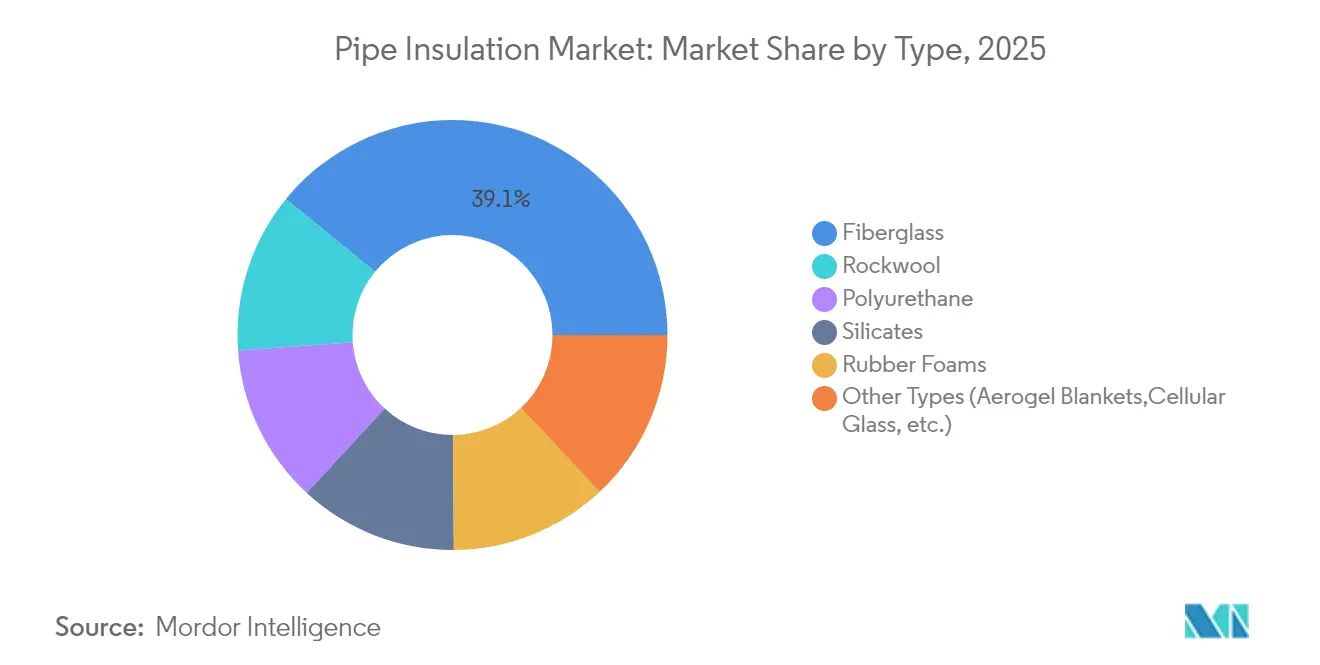

- By type, fiberglass held 39.10% of pipe insulation market share in 2025, while other types are expanding at a 7.13% CAGR through 2031.

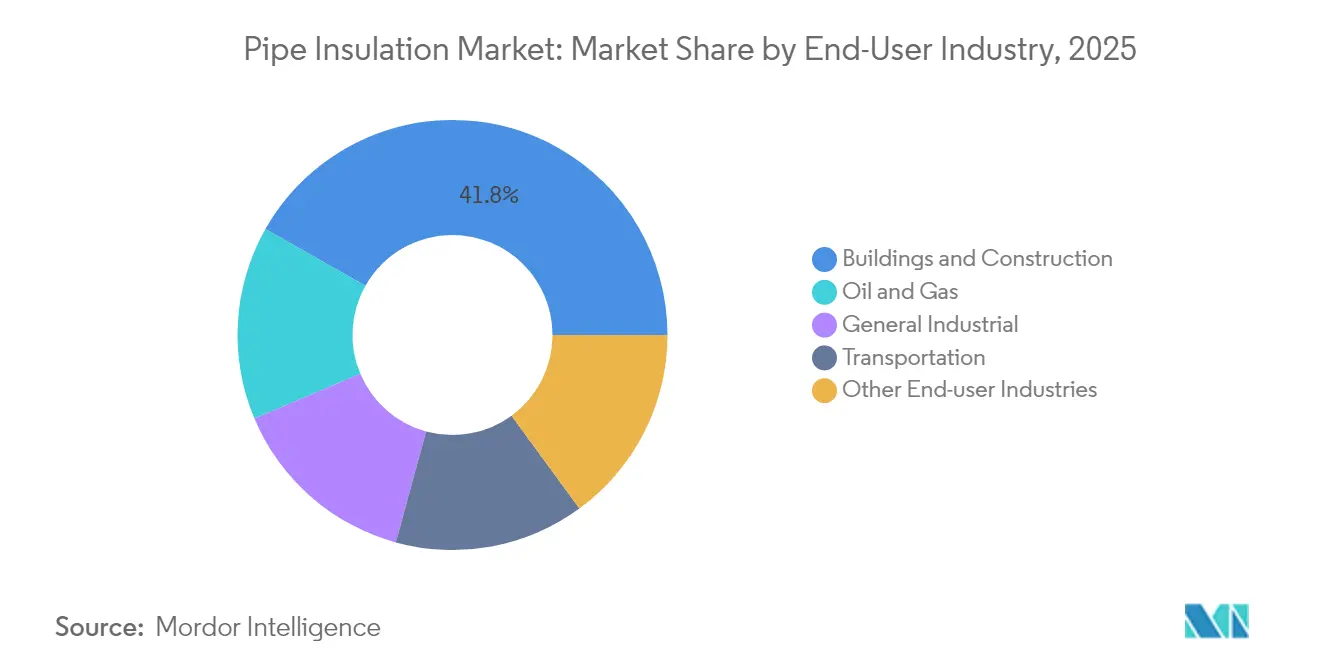

- By end-user industry, buildings and construction accounted for 41.80% of pipe insulation market size in 2025; other end-use industries are forecast to expand at a 6.95% CAGR to 2031.

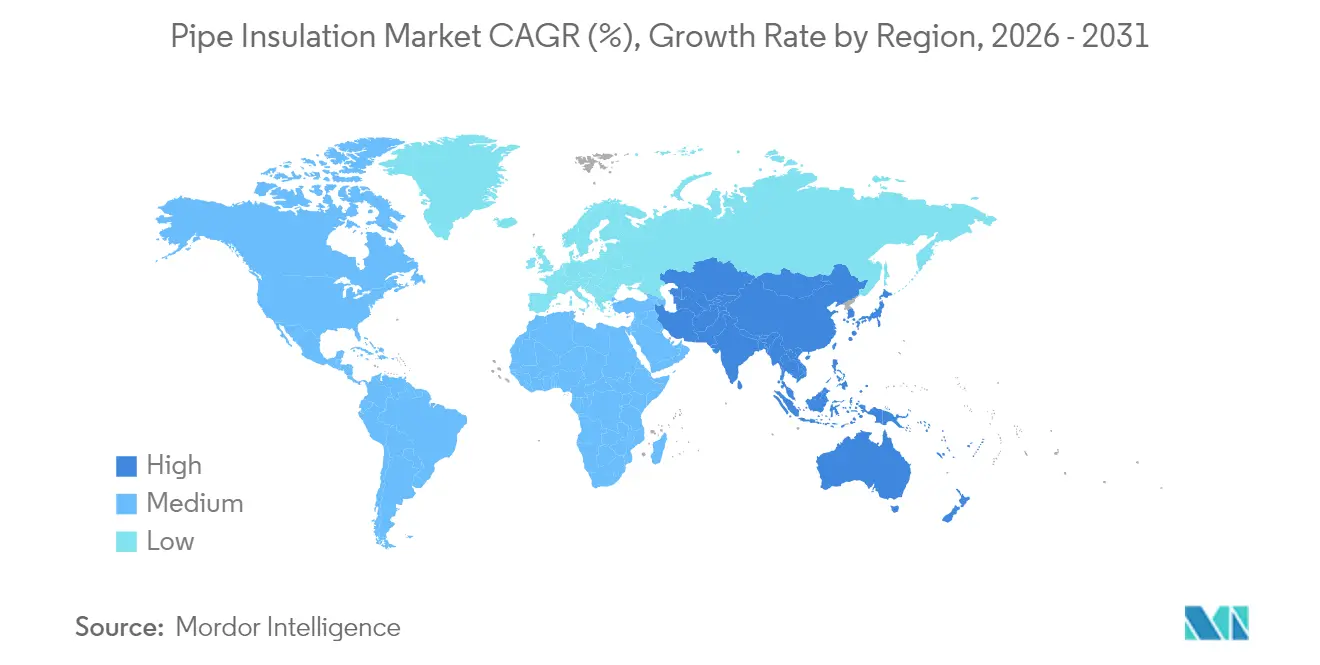

- By geography, Asia-Pacific commanded 46.80% of pipe insulation market share in 2025 and is advancing at a 6.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pipe Insulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent energy-efficiency building codes | +1.8% | Global; early adoption in North America and EU | Medium term (2-4 years) |

| LNG and cryogenic pipeline expansion | +1.2% | Asia-Pacific and North America | Long term (≥ 4 years) |

| District heating and cooling investments | +0.9% | Europe and North America; emerging in Asia-Pacific | Medium term (2-4 years) |

| Smart insulation with embedded sensors | +0.7% | Global; led by developed markets | Long term (≥ 4 years) |

| Carbon-pricing-driven industrial retrofits | +0.6% | EU and North America; expanding in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Energy-Efficiency Building Codes

Building codes are turning pipe insulation from a discretionary line item into a legal requirement. The 2024 International Energy Conservation Code (IECC) mandates thicknesses of up to 5 inches for hot-water pipelines, a rule expected to cut residential site-energy use by 7.80% in the United States. California’s Title 24 and similar European directives specify minimum R-values, effectively sidelining low-performance wraps[1]Energy Code Ace, “Section 120.3 – Requirements for Pipe Insulation,” energycodeace.com. With 14 U.S. states already on the 2024 IECC path, Northeast Energy Efficiency Partnerships forecasts 6.80% source-energy savings for early adopters. Commercial facilities mirror these requirements, pushing owners to favor lifecycle energy savings over upfront costs—another lever that expands the pipe insulation market.

Expansion of LNG and Cryogenic Pipeline Projects

Liquefied-natural-gas export terminals alo ng the U.S. Gulf Coast require more than 19,800 miles of new or replacement piping, much of it designed for -160 °C operating temperatures. Ambient-pressure aerogel pipe-in-pipe designs cut installation costs while keeping contraction stresses within allowable limits. As Asia-Pacific commissions floating LNG hubs, demand for long‐run subsea insulation miles pushes premium material pricing. Manufacturers with cryogenic-grade polyurethane or cellular glass lines enjoy margin upside and early-mover contracts on multi-year megaprojects.

Surging District Heating and Cooling Investments

Europe hosts 19,037 district-heating networks supplying 77.3 million residents, with renewable and waste heat covering 42.6% of demand. Fourth-generation systems operate at 70 °C or below, lowering thermal losses but lengthening network pipe runs—both factors lifting insulation volume requirements across the pipe insulation industry. In 2024 alone, European Commission instruments unlocked billions in concessional financing for new heat grids. District cooling, already serving 200 networks with 8% annual sales growth, adds summertime demand cycles that favor moisture-resistant rubber foams. These multilayer projects ensure steady call-offs for both pre-insulated steel pipe and flexible polymer bundles.

Smart Insulation with Embedded Sensors

IoT-enabled wraps change the value proposition from passive thermal barrier to active condition-monitoring node. Trisense’s Fusion 310 sensor embeds Nordic’s nRF9160 cellular SiP inside the jacketing, offering up to a decade of battery life for corrosion-under-insulation (CUI) alerts marking a shift in the pipe insulation industry. WFS Technologies pushes subsea coverage to 150 m through its Seatooth PipeLogger platform, giving offshore operators real-time temperature profiles. The global CUI remediation bill exceeds USD 7 billion annually, so operators willingly pay premiums for predictive analytics packages bundled with insulation contracts. This digital shift blurs lines between material suppliers, IIoT integrators, and data-analysis firms—widening competitive moats for early movers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installed cost and labor intensity | -1.1% | Global; acute in high-wage economies | Short term (≤ 2 years) |

| Volatile petrochemical feedstock prices | -0.8% | Regions dependent on imported naphtha | Short term (≤ 2 years) |

| Shift to thin-wall plastic piping | -0.5% | North America and Europe; emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Installed Cost and Labour Intensity

Field application of spray polyurethane foam and multi-layer jacketing requires certified crews and specialized rigs, pushing installation charges above USD 15/linear foot in large metro markets creating cost pressures within the pipe insulation industry. Although energy bills can drop 30% post-retrofit, Better Buildings Neighborhood data show that every USD 1 invested yields only USD 0.08 in first-year savings, stretching homeowner payback horizons. Prefabricated pipe spools partially solve the skills gap, yet transport limits hamper uptake for diameters above 12 inches. Labor scarcity is most acute in Northern Europe, where aging tradespeople retire faster than apprentices enter vocational programs. Producers respond with snap-fit mineral-fiber shells and self-adhesive aerogel wraps that cut site labor by up to 40%, but widespread adoption lags.

Volatile Petrochemical Feedstock Prices

Polyethylene feedstocks rose 3 ¢/lb in 2024, while polypropylene whipsawed on propane-dehydrogenation outages, impacting cost structures across the pipe insulation industry and shaving margins for foam extruders. MDI monomer supply, essential for rigid PU foam, tracks benzene and toluene, whose forward curves remain backwardated on Middle East geopolitical risks[2]. Alberta forecasts 5–7% annual demand growth for MDI/TDI yet flags feedstock shortfalls without new aromatics crackers . Manufacturers hedge with long-dated offtake contracts and develop bio-based polyols, but raw-material price shocks still flow into bid sheets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fiberglass Dominance Faces Advanced Material Challenge

Fiberglass maintained the leading 39.10% pipe insulation market share in 2025, underpinned by low cost and a λ-value near 0.04 W/(m·K). Rockwool leverages inherent fire resistance and circularity claims; the brand’s 2023 sales translated to anticipated lifetime energy savings of 818 TWh. Silicate wraps own niche refinery and power-plant lines above 600 °C, while rigid polyurethane foams post sub-0.02 W/(m·K) conductivities in bio-based formulations. Rubber foams remain HVAC staples because they flex with thermal cycling.

Other Types—primarily aerogel blankets and cellular glass—grow fastest at 7.13% CAGR through 2031 as mega-projects demand ultra-low heat loss. Next-gen Si₃N₄-reinforced aerogels come in at densities as low as 0.033 g/cm³ withstanding 893 °C differentials. Cellular glass appeals to LNG and cryogenic pipelines for zero water absorption and 100-year design life. Higher capex is offset by maintenance savings, leading process owners to specify performance-based tenders that favor premium materials.

By End-User Industry: Industrial Applications Drive Innovation

Buildings and construction contributed 41.80% to pipe insulation market size in 2025, propelled by stricter IECC codes and Europe’s 3% annual renovation ambition. Retrofits shift toward prefabricated jacketing modules that cut tenant downtime.

Other end-user industries—power generation, chemical processing, and district energy—expand at a 6.95% CAGR as operators chase decarbonization credits. Thermal-battery pilots and hydrogen co-firing turbines specify smart insulation wraps with embedded CUI monitoring, turning maintenance from reactive to predictive. In chemicals, every 1 °C reduction in line losses can shave 0.4% off annual fuel input, a fact now baked into ESG scorecards. These sectors thus form the proving ground for materials innovation.

Geography Analysis

Asia-Pacific dominates the pipe insulation market, pairing volume scale with policy support. Chinese provincial authorities now tie building permits to verified thermal-energy models, and the national Three-Year Action Plan for energy conservation identifies pipework insulation as a Tier-1 measure. India’s renewable-integration drive requires process industries to cut steam line losses, sending demand toward laminated mineral-fiber shells. The Asian Development Bank’s blended-financing tools de-risk greenfield heat-network projects, assuring steady material off-take.

North America benefits from LNG pipeline rollouts and code updates. The U.S. DOE’s confirmation of 7.80% residential energy savings from the 2024 IECC emboldens states to adopt without lengthy cost-effectiveness debates. Federal tax credits covering 30% of insulation spend further shorten paybacks. Canadian provinces tap low-interest retrofit loans, while industrial players in Alberta hedge feedstock volatility by switching to higher-efficiency jacketing to buffer fuel bills.

Europe’s ambition is to treble district cooling pipes by 2042 in cities like Paris, intertwining with the EU Renovation Wave that targets 35 million building upgrades by 2030 in the pipe insulation industry. Scandinavian markets trial carbon-negative insulation made with biogenic binders, providing early revenue for specialty manufacturers. Utilities bundle insulation contracts with heat-pump procurement, shifting supplier negotiations toward total-cost-of-ownership metrics.

Competitive Landscape

The pipe insulation market remains moderately fragmented: the top five vendors collectively control roughly 45% of global revenue. Armacell leverages its flexible elastomeric foam franchise while investing in IoT modules that pair with its jacketing. Kingspan scales extruded polyisocyanurate boards worldwide, capturing retrofit projects where space constraints demand high R per inch. Owens Corning cross-sells fiberglass pipe wraps into its building-envelope channel. Saint-Gobain, through CertainTeed, committed USD 400 million to expand North American roofing and insulation capacity, signaling a strategy to lock in distribution reach.

M&A activity accelerated: Holcim acquired OX Engineered Products for USD 136 million to bolt expanded-polystyrene know-how onto its decarbonized-cement platform. TopBuild agreed to purchase Shannon Global Energy Solutions to deepen industrial-insulation exposure. Installed Building Products closed three tuck-ins, broadening geographic coverage across the U.S. Southeast.

Technology differentiation sharpens competition within the pipe insulation industry. Aerogel start-ups secure patent positions on Si₃N₄ nanofiber composites, attracting venture funding. Legacy firms respond by partnering with sensor vendors: Armacell integrates edge-AI boards for moisture detection, while Johns Manville builds digital twins around its Climate Pro line. Environmental-product declarations become table stakes, pushing smaller regional players to find niche fire-rating or acoustic-damping angles.

Pipe Insulation Industry Leaders

Armacell

Owens Corning

Kingspan Group

Johns Manville

Rockwool International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Saint-Gobain is building a low-carbon rockwool insulation factory in Leicestershire, UK, set to open in 2027. Powered by renewable energy and using electric melting, it will produce 50,000 tonnes annually, supporting the company’s 2050 net-zero goal.

- May 2025: Knauf Insulation, Inc. expanded its portfolio of products with Asthma and Allergy Friendly® Certification. The newly certified Knauf Performance+® insulation products include Performance+® Earthwool® 1000˚ Pipe Insulation, Pipe and Tank Insulation, and KwikFlex® Pipe and Tank Insulation with Ecose.

Global Pipe Insulation Market Report Scope

The Pipe Insulation market report include:

| Fiberglass |

| Rockwool |

| Silicates |

| Polyurethane |

| Rubber Foams |

| Other Types (Aerogel Blankets,Cellular Glass, etc.) |

| Buildings and Construction |

| Oil and Gas |

| Transportation |

| General Industrial |

| Other End-user Industries (Power Generation and Utilities, Chemical and Petrochemical Processing, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Fiberglass | |

| Rockwool | ||

| Silicates | ||

| Polyurethane | ||

| Rubber Foams | ||

| Other Types (Aerogel Blankets,Cellular Glass, etc.) | ||

| By End-User Industry | Buildings and Construction | |

| Oil and Gas | ||

| Transportation | ||

| General Industrial | ||

| Other End-user Industries (Power Generation and Utilities, Chemical and Petrochemical Processing, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the pipe insulation market?

The pipe insulation market size is USD 6.45 billion in 2026 and is expected to reach USD 8.58 billion by 2031

Which region leads the pipe insulation market?

Asia-Pacific holds the largest share at 46.80% in 2025, propelled by massive infrastructure investment and stricter efficiency codes.

Which material type dominates the pipe insulation market?

Fiberglass remains the leading material, accounting for 39.10% of global revenue in 2025 thanks to its cost-performance balance.

How do smart insulation systems add value?

Embedded sensors enable real-time corrosion and temperature monitoring, reducing maintenance costs and preventing failures in industrial pipelines.

What are the main growth drivers for pipe insulation?

Key drivers include stringent building energy codes, LNG and cryogenic pipeline expansion, district heating investments, IoT-enabled smart wraps, and carbon-pricing-induced retrofits.

Page last updated on: