Carbon Fiber Tape Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

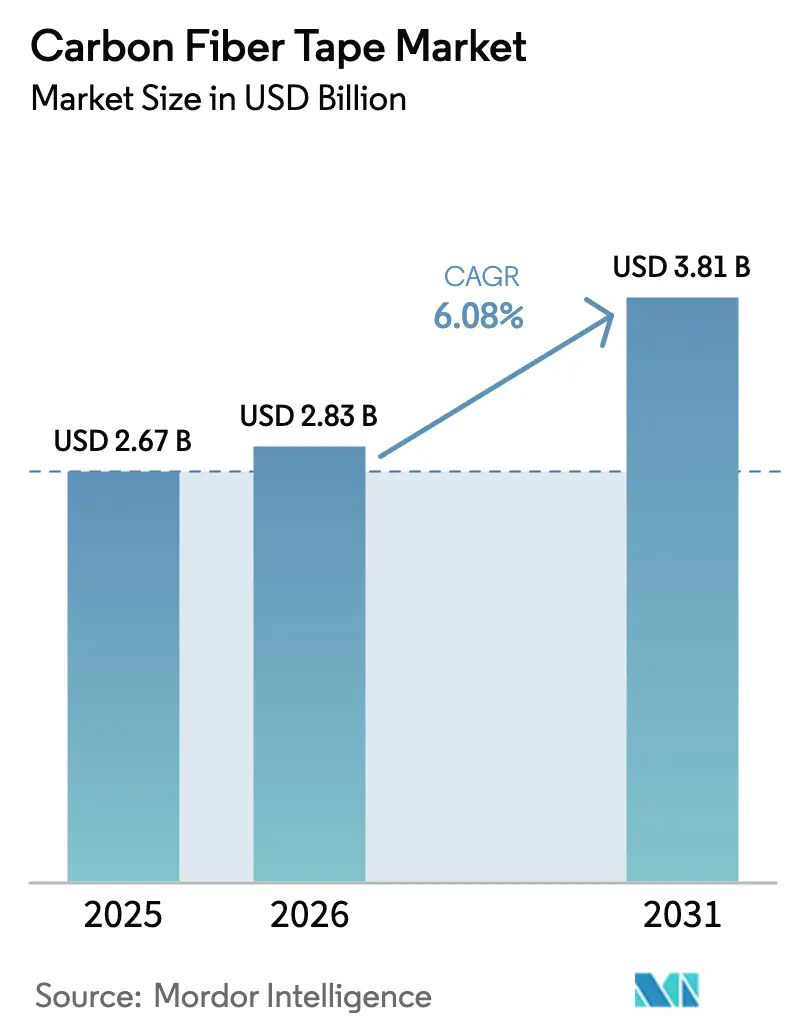

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 3.81 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carbon Fiber Tape Market Analysis by Mordor Intelligence

The Carbon Fiber Tape market size is expected to grow from USD 2.67 billion in 2025 to USD 2.83 billion in 2026 and is forecast to reach USD 3.81 billion by 2031 at 6.08% CAGR over 2026-2031. The outlook is anchored in the aerospace sector’s continuing transition from aluminum to composites, the scale-up of next-generation single-aisle programs, and the rapid diffusion of automated fiber placement systems that favor tape formats for speed and lay-up accuracy. Hot-melt prepreg processes are expanding because they combine precise resin control with solvent-free operations, while wind-turbine blade lengthening and cryogenic hydrogen storage provide fresh volume opportunities. Supply-side strategies now hinge on vertical integration to manage precursor volatility and on rapid qualification pathways that shorten time-to-market for thicker laminates.

Key Report Takeaways

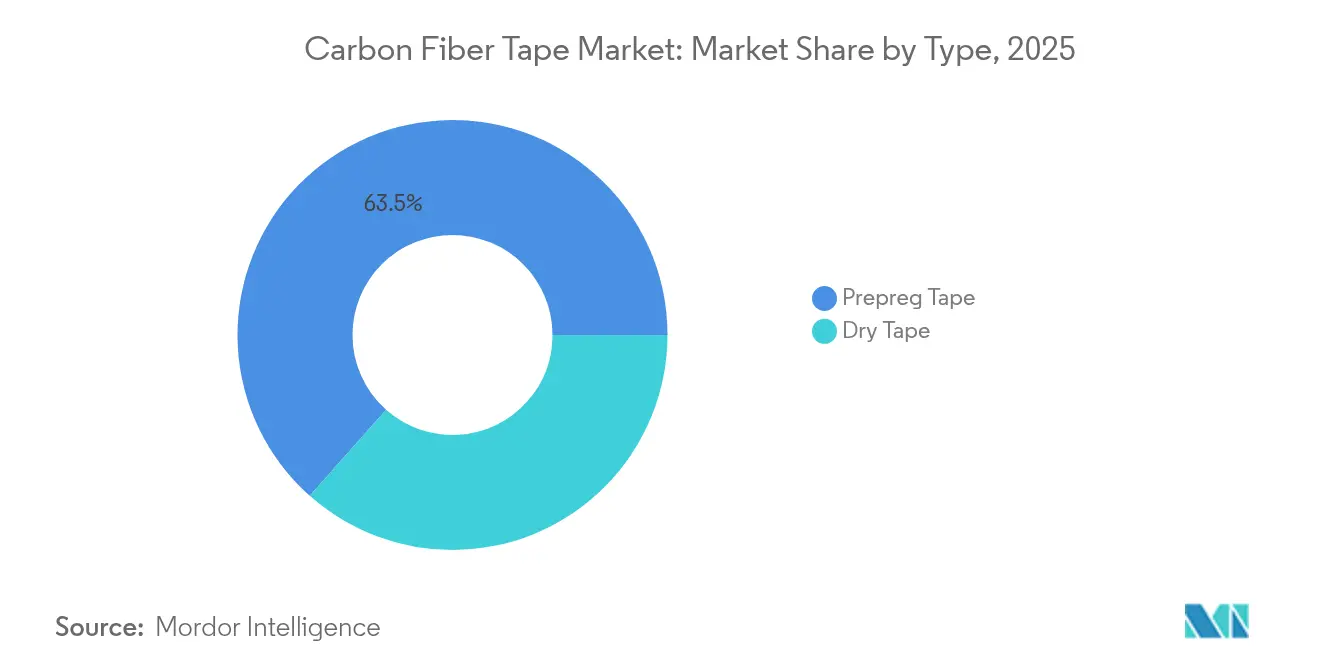

- By type, prepreg tape captured 63.45% of the carbon fiber tape market share in 2025, while dry tape posted the fastest 6.72% CAGR through 2031.

- By resin type, epoxy accounted for the largest share of 48.75% in 2025; while other resin types posted the fastest CAGR of 6.85% through 2031.

- By manufacturing process, hot-melt prepreg accounted for 51.25% of the carbon fiber tape market size in 2025 and is projected to grow at 6.68% CAGR to 2031.

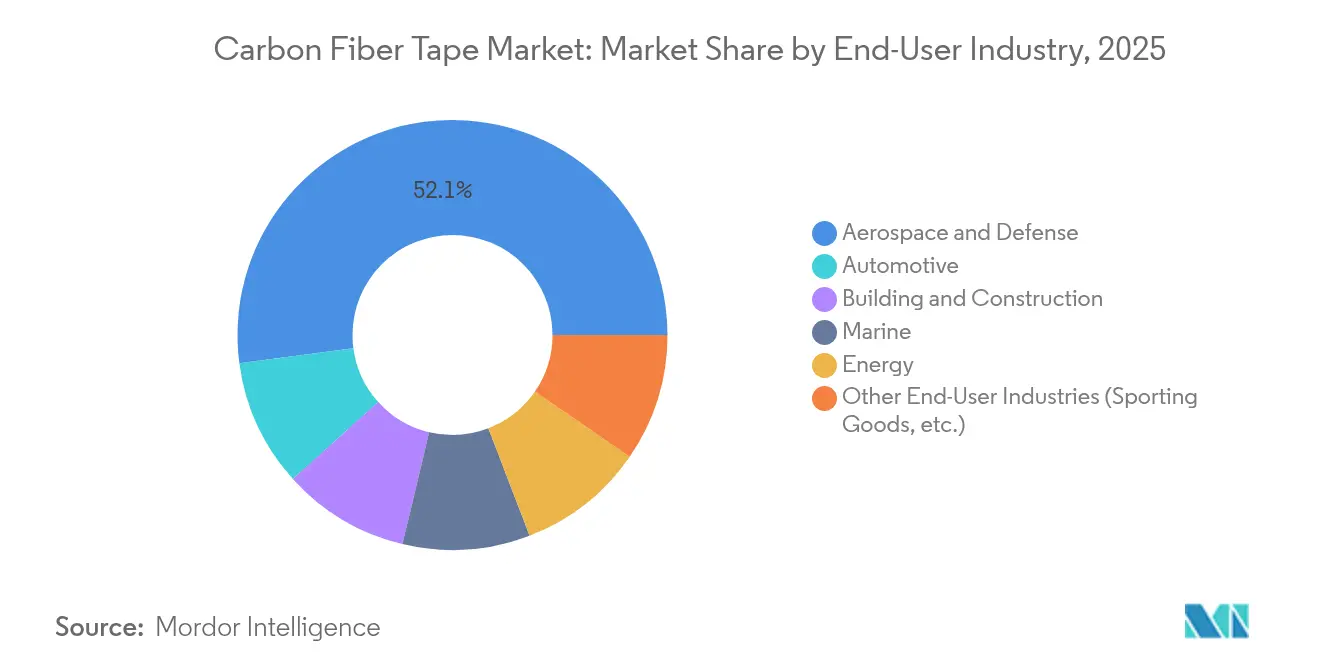

- By end-user industry, the aerospace and defense segment held 52.10% revenue share of the carbon fiber tape market in 2025 and is advancing at a 6.89% CAGR through 2031.

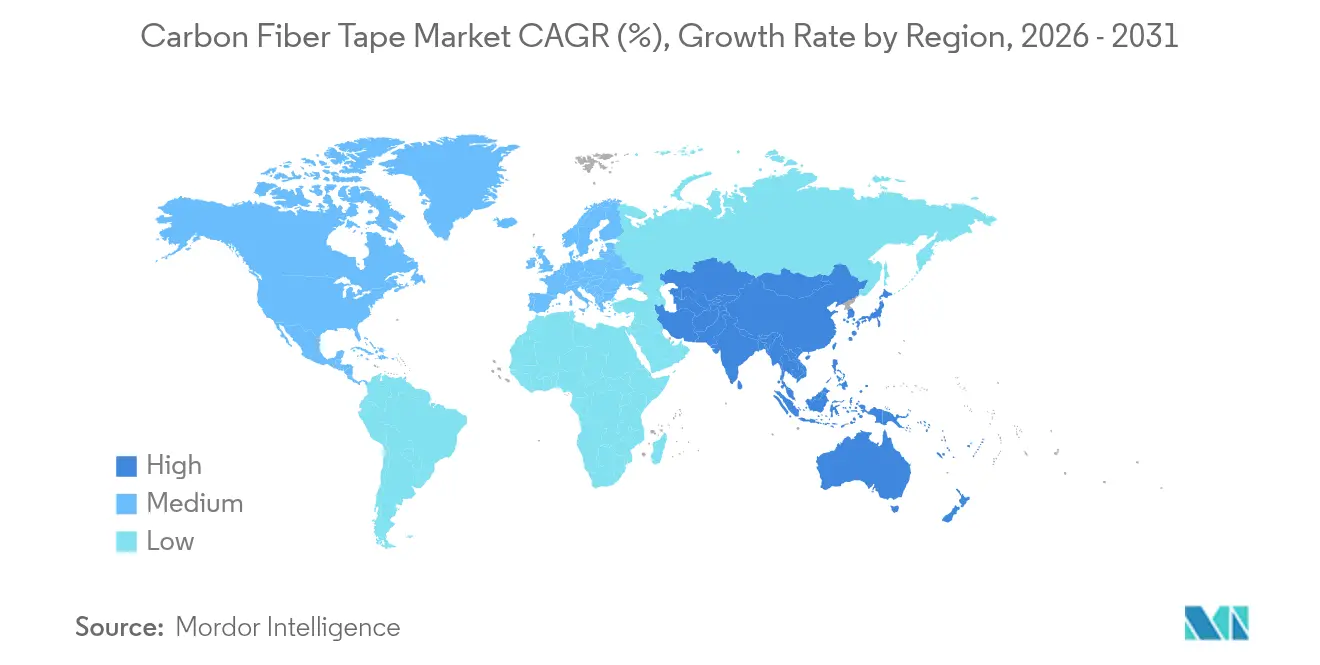

- By region, Asia-Pacific led with 36.40% share of the carbon fiber tape market size in 2025, and the region is set to expand at 6.57% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Carbon Fiber Tape Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging aerospace demand for lightweight primary structures | +1.8% | Global; North America & Europe | Medium term (2-4 years) |

| Ramp-up of next-gen single-aisle aircraft production | +1.5% | Global; North America & Europe | Short term (≤ 2 years) |

| Automotive shift to carbon fiber reinforced plastics for EV range extension | +1.2% | Global; Asia-Pacific & Europe | Long term (≥ 4 years) |

| Wind-turbine blade lengthening needs high-modulus tapes | +0.9% | Global; Europe & Asia-Pacific | Medium term (2-4 years) |

| Cryogenic hydrogen tank winding for zero-carbon aviation | +0.7% | Global; Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Aerospace Demand for Lightweight Primary Structures

Commercial and defense airframers are replacing metallic wing spars, fuselage skins, and floor beams with carbon fiber tape lay-ups that deliver durability alongside 20% weight savings, a metric validated by the Boeing 787 and Airbus A350 programs[1]National Composites Centre, “Lightweight Structures in Commercial Aircraft,” nccuk.com. Automated fiber placement cells amplify demand because they require uniform tape widths and consistent tack to achieve high deposition rates without defects. NASA’s HiCAM initiative, which pairs Toray’s carbon fiber with rapid-cure prepregs, exemplifies how public-private research is compressing cycle times for wide-body and single-aisle structures. As qualification datasets mature, more primary structures migrate to tape-based designs, securing long-run growth for certified suppliers.

Ramp-up of Next-Gen Single-Aisle Aircraft Production

Airbus and Boeing have committed to double-digit monthly build-rates for the A320neo and 737 MAX families. These narrow-body programs consume large volumes of secondary and interior composite parts that are increasingly manufactured from tape because of its predictable fiber orientation and minimal material wastage. Equipment provider MTorres has introduced dry-fiber tape formats that enable producers to infuse resin in-house, cutting raw material costs by up to 50% while safeguarding mechanical performance. With total carbon fiber consumption in commercial aerospace projected to climb from 16,500 t in 2021 to 29,100 t by 2026, tape is positioned as the dominant intermediate form feeding the supply chains of tier-1 and tier-2 suppliers.

Automotive Shift to Carbon Fiber Reinforced Plastics for EV Range Extension

Battery packs add substantial mass to electric vehicles, prompting automakers to adopt carbon fiber tape in body-in-white, roof, and door architectures to reclaim driving range. Tesla’s Model S Plaid and BMW’s high-end EV lines already integrate composite panels that slash component mass by 40–50% relative to aluminum. Regulatory support in Europe following the withdrawal of proposed carbon fiber restrictions safeguards the material’s availability for mass-market adoption. Thermoplastic tape variants that allow over-molding and recycling appeal to high-volume plants, while large-tow grades keep cost curves within automotive targets.

Wind-Turbine Blade Lengthening Needs High-Modulus Tapes

Onshore and offshore turbines above the 10 MW class deploy blades exceeding 100 m length; spar caps reinforced with high-modulus carbon fiber tape supply the stiffness needed to avoid tower strikes under gust loading. LM Wind Power’s 88.4 m prototype showed that hybrid carbon-glass caps trimmed mass while meeting fatigue criteria. The U.S. Department of Energy later confirmed that heavy-tow carbon fiber can lower overall blade weight by 25%, easing transport and installation[2]U.S. Department of Energy, “Optimized Carbon Fiber for Wind Turbine Blades,” energy.gov . Volume requirements in wind create attractive scale for mid-grade tape producers, nudging the supply base to expand pultrusion and unidirectional tape output.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High precursor and processing costs | -1.4% | Global; cost-sensitive markets | Short term (≤ 2 years) |

| Feedstock price and energy-cost volatility | -0.8% | Global; Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Regulatory qualification bottlenecks for thick laminates | -0.6% | Global; aerospace applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Precursor and Processing Costs

Polyacrylonitrile accounts for half to three-quarters of finished fiber price, and the multi-stage oxidation/carbonization route is power intensive, leaving producers exposed to energy spikes. Market prices average USD 15 kg for industrial grades and exceed USD 85,000 t for aerospace classes, levels that restrain penetration into cost-sensitive sectors such as standard-range passenger cars. Research at the University of Limerick demonstrated microwave carbonization that could cut energy use by 70%, but commercialization remains distant. Until lignin-based or other low-cost precursors reach scale, tape producers must pursue incremental process yields and vertical integration to manage margin compression.

Feedstock Price and Energy-Cost Volatility

Spot carbon fiber prices in China dropped from USD 33 kg in 2022 to USD 18 kg in 2024 as surplus capacity met soft demand, underscoring the material’s vulnerability to cyclical swings. Because furnaces run at 1,000 °C +, electricity price increases immediately erode margins, especially in Asia-Pacific clusters where power tariffs can vary widely. Producers are relocating or adding furnaces in regions with low-carbon, low-cost grids to stabilise operating economics and hedge geopolitical risks highlighted by recent supply chain disruptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Prepreg Dominance Drives Quality Standards

Prepreg variants held 63.45% carbon fiber tape market share in 2025 because they deliver uniform resin content, stable tack, and predictable cure profiles that aerospace primes specify for primary structures. Dry tape, in contrast, posted a leading 6.72% CAGR and is gaining acceptance as automated fiber placement systems mature and as tier-1 suppliers appreciate the logistics benefits of ambient storage. The cost differential widens as high-volume programs exploit in-line resin infusion, positioning dry tape as the economical alternative for secondary parts.

Prepreg’s foothold is defended by refinements such as extended out-time and tougher resin chemistries that raise damage tolerance in thicker laminates. However, dry tape vendors answer with proprietary sizing agents that enhance resin wet-out and with slit-tape formats down to 3 mm that allow precise steering around tight radii. Tape lines that can switch between prepreg and dry, depending on order mix, provide supply flexibility coveted by vertically integrated producers serving both aerospace and wind customers.

By Resin Type: Epoxy Leadership Faces Thermoplastic Challenge

Epoxy systems constituted 48.75% of global volume in 2025, reflecting decades of certification data and proven performance at service temperatures up to 120 °C. Their dominance also mirrors well-developed supply networks that support just-in-time deliveries to both tier-1 and tier-2 aerospace fabricators. The “other resins” basket, which includes thermoplastic families such as PEEK and PPS, is expanding at 6.85% CAGR as automotive and hydrogen tank applications require fast processing and recyclability.

Epoxy suppliers continue to engineer fracture-toughened grades and snap-cure formulations that can be out-of-autoclave processed. Thermoplastic innovators respond with lower-melt-viscosity matrices that facilitate consolidation at sub-400 °C and with carbon-fiber-reinforced unidirectional tapes suitable for over-molding into hybrid structures. Polyamide and vinyl ester occupy niche marine and chemical containment roles, while bio-based options remain pre-commercial but are attracting automotive OEM pilots that seek end-of-life circularity.

By Manufacturing Process: Hot-Melt Prepreg Balances Performance and Efficiency

Hot-melt lines delivered 51.25% revenue share in 2025 and are expected to advance 6.68% CAGR through 2031. Because resin is applied as a molten film, volatile emissions are eliminated, and resin/fiber ratio accuracy reaches ±1%, an advantage for design allowables. The process also aligns with fully enclosed, digitalised production cells that capture process parameters needed for aerospace traceability.

Solvent dip routes continue where legacy chemistries require, for instance high-temperature polyimide matrices. Resin transfer infusion grows fastest in large wind or marine structures, where lengthy flow paths can be accommodated in modular molds. Breakthroughs such as lignin-precursor carbon and multifunctional tapes that double as current collectors or structural batteries signal future disruption as they mature beyond laboratory scale.

By End-User Industry: Aerospace Dominance Extends Across Growth Metrics

The aerospace and defense community consumed 52.10% of global tonnage in 2025 and is accelerating at 6.89% CAGR, sustained by single-aisle production ramps and stealth platform refresh programs. Price premiums remain acceptable because every kilogram removed can yield fuel savings over an aircraft’s 20-year life. Automotive ranks a distant second but is moving quickly as EV platforms demand lighter bodies to offset battery packs. Wind energy is the volume wildcard: each incremental meter of blade length requires significantly more spar cap material, and carbon tape’s high modulus prevents deflection-induced tower strikes. Construction interest is nascent yet tangible, especially for seismic-retrofit wraps and prefabricated façade elements where weight savings simplify installation. Marine adoption continues in performance yachts and crew transfer vessels, while sporting goods remain a profitable but relatively small slice.

Geography Analysis

Asia-Pacific held 36.40% carbon fiber tape market size in 2025 thanks to the intersection of large-scale fiber production in China, robust wind-turbine build-out, and growing domestic aerospace programs. The region’s 6.57% CAGR reflects government incentives for renewable capacity and state-sponsored aircraft such as COMAC’s C919, which adopt significant composite content. Japanese players Toray and Mitsubishi anchor high-performance fiber output, while South Korean and Indian firms scale mid-grade capacities to service regional mobility and energy demand.

North America follows closely, underpinned by Boeing’s assembly lines, a resilient defense budget, and federal funding into hydrogen-powered flight demonstrators. The United States also hosts many automated fiber placement technology suppliers, giving regional converters first access to next-generation deposition heads. Canada leverages a cluster of tier-2 aerospace fabricators, and Mexico emerges as a cost-competitive site for automotive composite parts shipped into U.S. OEMs. Europe commands balanced demand across aerospace, premium automotive, and wind energy. The EU’s supportive stance on carbon composites, reaffirmed after the shelved restriction proposal, sustains adoption in both road and aviation segments. Germany’s OEMs lead vehicle integration projects; the United Kingdom and France anchor wide-body airframe expertise; and Spain’s coastal corridor benefits from large offshore wind deployments. Nordic nations inject momentum through aggressive renewable targets that mandate ever-larger blades, while Eastern Europe offers competitive labor for composite component assembly.

Competitive Landscape

The carbon fiber tape market is moderately consolidated around a handful of vertically integrated groups. Toray Industries, Hexcel Corporation, and SGL Carbon maintain closed-loop control from precursor through finished tape, enabling tight quality governance and cost visibility. Second-tier specialists such as Gurit and NTPT focus on ultra-thin tape slitting, serving luxury goods and sporting equipment where aesthetics and lay-up precision command premiums.

Leading suppliers differentiate via process automation, with multiple firms investing in high-speed slitters, laser steering, and in-line ultrasonic inspection that detects gaps or overlaps below 0.3 mm. Hexcel’s continuous-tow placement portfolio exemplifies how equipment and material portfolios combine into turnkey offerings attractive to airframe primes. Toray has introduced porous carbon fiber variants that open hybrid markets in filtration and energy storage, illustrating how core technology can spin out adjacencies.

Cost discipline is equally strategic. SGL Carbon and Chinese challengers are experimenting with lignin and pitch precursors to cut variable cost, while resin formulators push snap-cure systems that lower autoclave time by 30%. Certification datasets collected over decades remain potent entry barriers; newcomers must finance extensive allowables programs before becoming Airbus or Boeing qualified. Consequently, partnership models—material supplier plus design-build specialist plus OEM—are gaining favor, allowing risk-sharing while accelerating qualification.

Carbon Fiber Tape Industry Leaders

Solvay

Hexcel Corporation

TORAY INDUSTRIES, INC,

SABIC

Teijin Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Porsche researchers have developed TABASKO, an acronym for “tape-based carbon fibre lightweight construction.” It is a polypropylene film with embedded carbon fibre strands, enhancing strength and reducing weight when integrated into components.

- May 2025: McLaren Automotive has introduced an aerospace composite manufacturing technique adapted for high-volume supercar production. The Automated Rapid Tape (ART) method, implemented at McLaren's Composites Technology Centre (MCTC) in Sheffield, UK, produces carbon fibre structures optimised for lightness, stiffness, and strength while reducing material waste.

Global Carbon Fiber Tape Market Report Scope

The Carbon Fiber Tape report includes:

| Prepreg Tape |

| Dry Tape |

| Epoxy |

| Polyamide |

| Vinyl Ester |

| Polyurethane |

| Other Resin Types (Thermoplastic (PEEK, PPS), etc.) |

| Hot-Melt Prepreg |

| Solvent Dip |

| Automated Fiber Placement (AFP) |

| Resin Transfer Infusion |

| Aerospace and Defense |

| Automotive |

| Building and Construction |

| Marine |

| Energy |

| Other End-User Industries (Sporting Goods, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Prepreg Tape | |

| Dry Tape | ||

| By Resin Type | Epoxy | |

| Polyamide | ||

| Vinyl Ester | ||

| Polyurethane | ||

| Other Resin Types (Thermoplastic (PEEK, PPS), etc.) | ||

| By Manufacturing Process | Hot-Melt Prepreg | |

| Solvent Dip | ||

| Automated Fiber Placement (AFP) | ||

| Resin Transfer Infusion | ||

| By End-user Industry | Aerospace and Defense | |

| Automotive | ||

| Building and Construction | ||

| Marine | ||

| Energy | ||

| Other End-User Industries (Sporting Goods, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Carbon Fiber Tape Market size?

The carbon fiber tape market size reached USD 2.83 billion in 2026 and is forecast to grow to USD 3.81 billion by 2031 at a 6.08% CAGR.

Which segment holds the largest share of the carbon fiber tape market?

Prepreg tape led with 63.45% market share in 2025 because aerospace manufacturers prefer its consistent resin content and mechanical reliability.

Which region is growing fastest in the carbon fiber tape market?

Asia-Pacific is expanding at 6.57% CAGR through 2031, propelled by wind-energy build-outs and emerging aircraft programs across China, India, and Southeast Asia.

Why are automotive OEMs adopting carbon fiber tape?

Electric vehicles benefit from 40–50% weight reductions versus aluminum parts, which helps extend driving range without redesigning battery packs.

Page last updated on: