Double-sided Tape Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.4 Billion |

| Market Size (2031) | USD 20.4 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

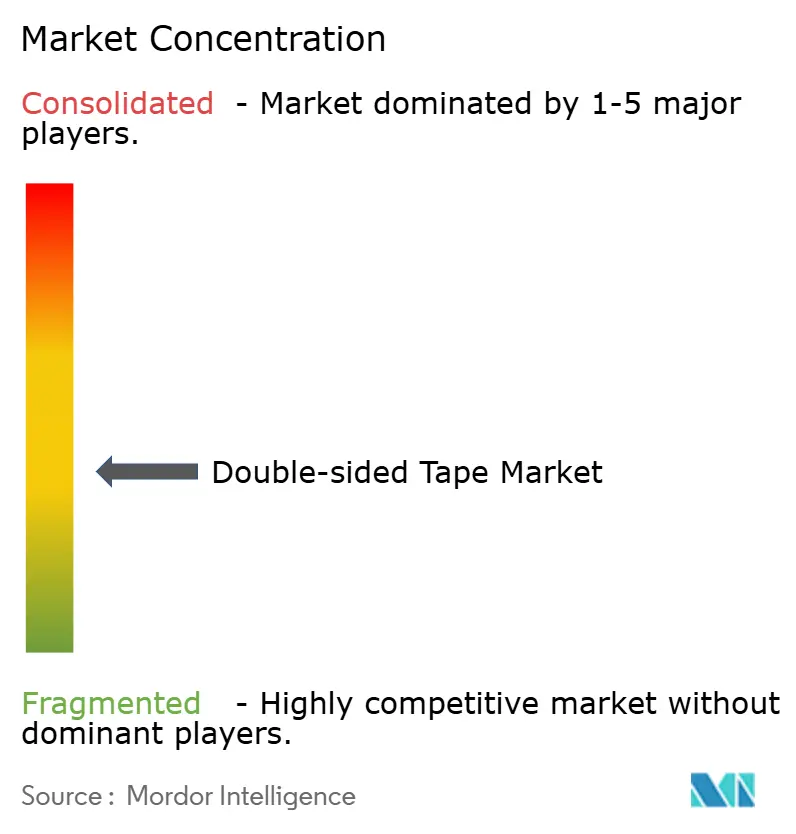

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Double-sided Tape Market Analysis by Mordor Intelligence

Double-sided Tape market size in 2026 is estimated at USD 15.4 billion, growing from 2025 value of USD 14.56 billion with 2031 projections showing USD 20.4 billion, growing at 5.78% CAGR over 2026-2031. Strong substitution of screws, rivets, and liquid adhesives in favor of pressure-sensitive bonding drives this expansion, while rapid automation in manufacturing lines heightens demand for clean, fast, and design-flexible attachment methods. Growing adoption of electric vehicles (EVs), the miniaturization of consumer electronics, and the shift toward modular construction intensify the need for tapes that combine mechanical strength with thermal, optical, and reworkable properties. Regulatory pressure on volatile organic compound (VOC) emissions spurs reformulation toward low-VOC chemistries, particularly acrylics, and stimulates premium pricing for high-performance grades. The competitive field remains moderately fragmented as global leaders scale R&D around multi-functional tapes and regional players concentrate on localized service, keeping price tension alive in commoditized SKUs.

Key Report Takeaways

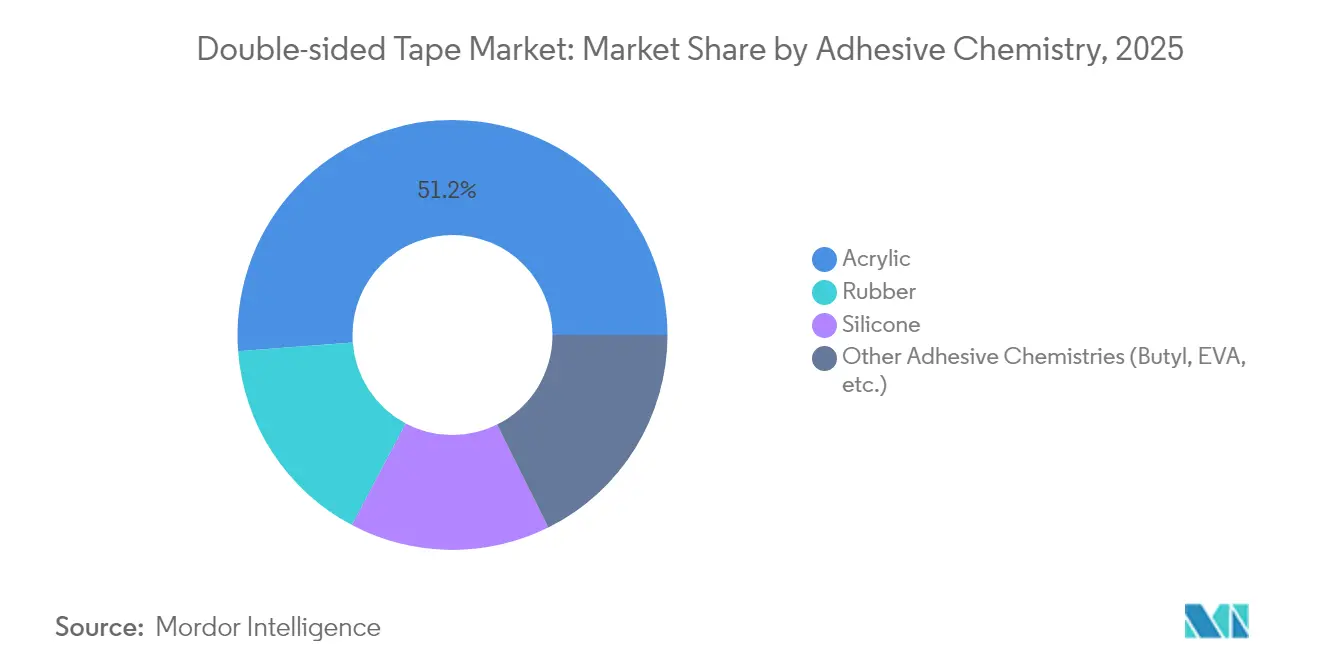

- By adhesive chemistry, acrylic tapes accounted for 51.20% of the double-sided tape market share in 2025, whereas butyl and EVA formulations are projected to post the fastest 6.92% CAGR through 2031.

- By backing material, foam held 29.74% revenue share of the double-sided tape market in 2025 and is forecast to extend at a 6.95% CAGR to 2031.

- By tape thickness, the 100–200 µm range commanded 47.20% share of the double-sided tape market size in 2025, while the below-100 µm segment is on track for the highest 6.55% CAGR to 2031.

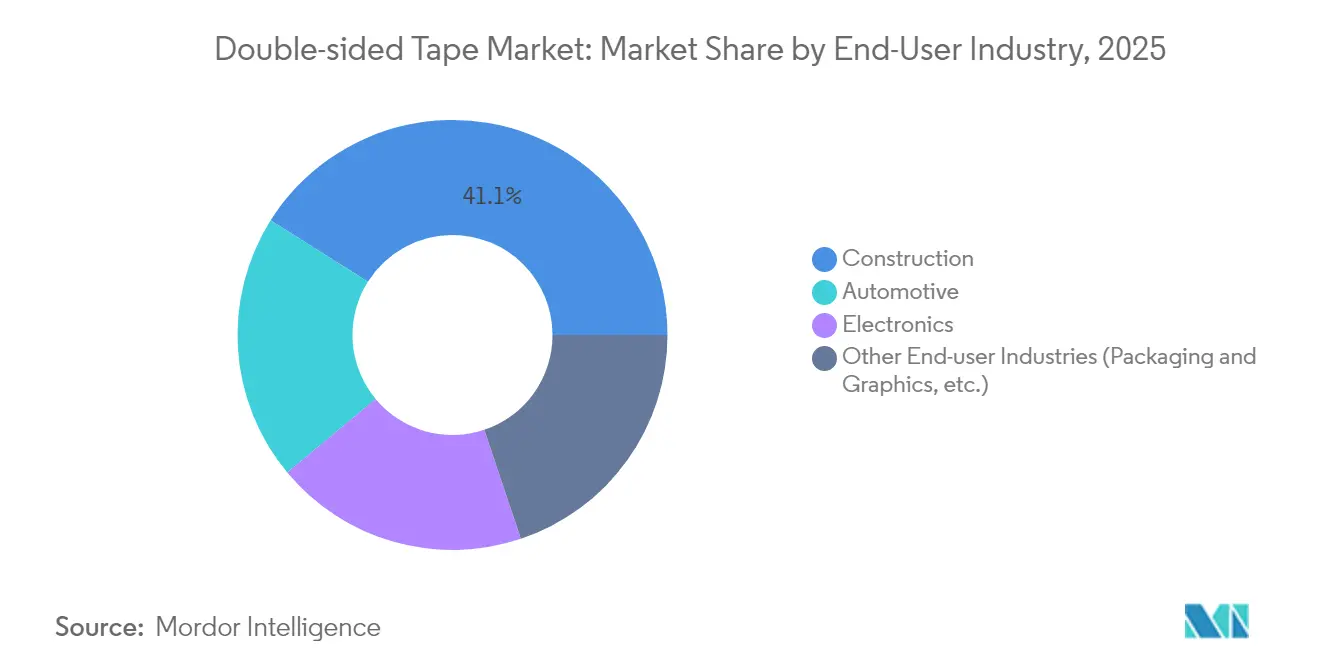

- By end-user industry, construction captured 41.05% revenue share in 2025 and is set to expand at a leading 7.02% CAGR over the forecast horizon.

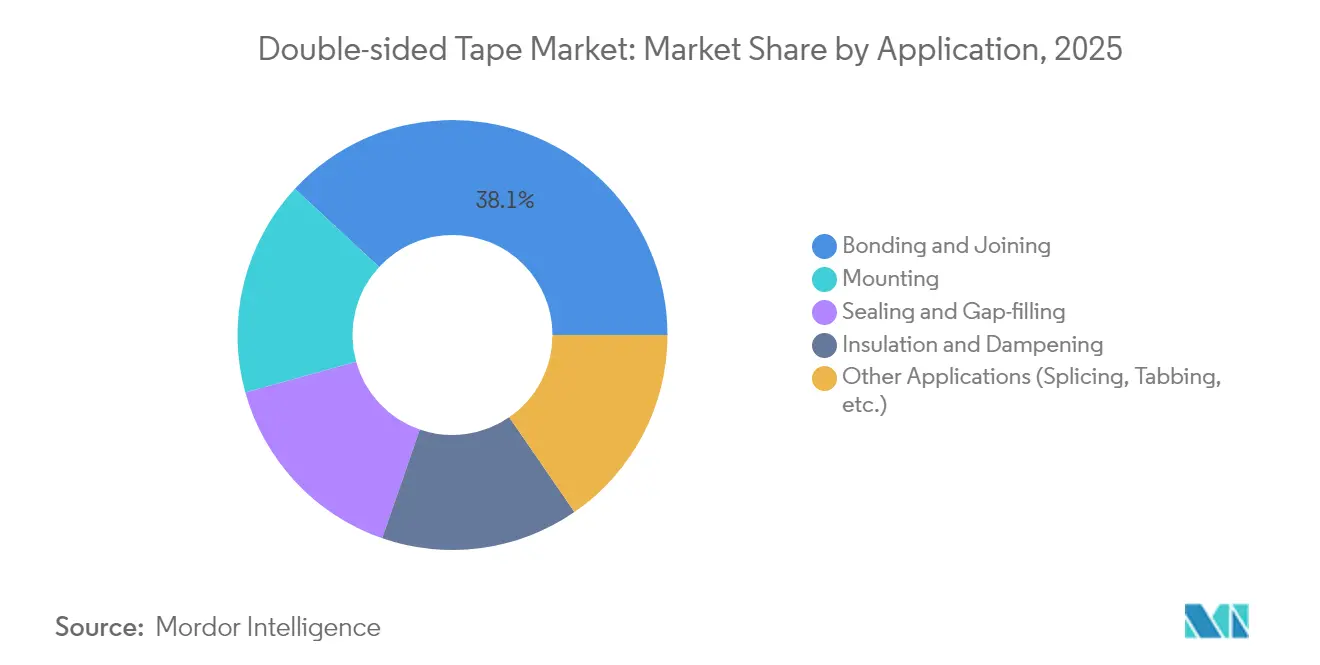

- By application, bonding and joining retained 38.10% of the double-sided tape market size in 2025, whereas mounting shows the quickest 6.96% CAGR through 2031.

- By geography, Asia-Pacific dominated with a 41.80% double-sided tape market share in 2025 and is anticipated to record the strongest 7.01% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Double-sided Tape Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing applications in indoor and outdoor construction | +1.50% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Automotive lightweighting requirements | +1.20% | Global, led by Europe and North America regulatory mandates | Long term (≥ 4 years) |

| Miniaturisation in consumer electronics assembly | +0.80% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Expansion of prefabricated/ modular buildings | +1.40% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| EV battery cell bonding and thermal-gap filling | +1.10% | Global, with early gains in China, Germany, United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Applications in Indoor and Outdoor Construction

Construction professionals replace screws and nails with pressure-sensitive tapes to avoid substrate damage and accelerate installation. Waterproof acrylic foam variants anchor façades and interior panels while meeting stringent building codes. Modular builders favor factory-applied tapes that assure consistent bond-line control and reduce on-site labor. Bio-based adhesives enter premium green projects that target lower embodied carbon. Foam-core formats accommodate uneven walls common in retrofits, boosting demand in Asia-Pacific’s urban renovation boom. Together, these trends lift construction-related orders for the double-sided tape market.

Automotive Lightweighting Requirements

Vehicle makers pursue adhesive bonding to remove rivets that add mass and cause galvanic corrosion. High-shear acrylic tapes bond aluminum roof panels to carbon-fiber frames in EVs, raising energy efficiency. In battery packs, thermally conductive tapes dissipate heat while isolating cells, aligning with strict interior VOC limits in China[1]tesa, “China tightens emission requirements for automotive interiors,” tesa.com . Growth accelerates in Europe where CO₂ mandates tighten, pushing OEMs toward lighter assemblies. Low-VOC chemistries secure interior cabin compliance without sacrificing peel strength. These dynamics underpin rising automotive intake in the double-sided tape market.

Miniaturisation in Consumer Electronics Assembly

Smartphones and wearables demand tape thicknesses down to 5 µm that still deliver shock absorption and optical clarity. Manufacturers integrate thermal or EMI shielding layers into the same ultra-thin construction to save space. Optically clear acrylics dominate flexible display laminations, keeping pixels bright even under repeated bending. Debond-on-demand designs simplify repair and recycling, supporting circular economy policies. Asia-Pacific’s dense electronics supply chain ensures rapid scale-up, raising regional consumption of premium micro-tapes.

EV Battery Cell Bonding and Thermal Gap-Filling

Next-generation battery packs require tapes that conduct heat away from cells without permitting current leakage. Silicone-acrylic hybrids meet these dual needs, securing foils while maintaining dielectric integrity. Leading EV assemblers in China and Germany integrate gap-fill tapes that shorten production cycles. OEM qualification protocols prioritize low outgassing to protect sensitive chemistries. Premium pricing follows the critical safety role these products play. As global EV volumes scale, thermal tapes emerge as a multibillion-dollar niche within the broader double-sided tape market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited high-temperature resistance of rubber-based tapes | -0.90% | Global, particularly affecting automotive and industrial applications | Medium term (2-4 years) |

| Petrochemical feed-stock price volatility | -0.70% | Global, with strongest impact on cost-sensitive applications | Short term (≤ 2 years) |

| Stricter VOC limits on solvent-based adhesive lines | -1.10% | North America & EU leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited High-temperature Resistance of Rubber-based Tapes

Standard rubber adhesives lose cohesion beyond 150 °C, restricting deployment near engines or industrial ovens. OEMs must shift to higher-priced silicone or acrylic versions, adding system cost. Battery makers require tapes that stay stable across wide thermal cycles, making rubber grades unsuitable. Research into hybrid polymers shows promise but remains expensive. As a result, cost-driven buyers hesitate to convert from mechanical fasteners where peak temperatures exceed limits, tempering overall uptake in the double-sided tape market.

Petrochemical Feed-stock Price Volatility

Ethylene, propylene, and VAM price swings squeeze tape producers who rely on these monomers. Raw-material surges cannot always be passed through to fixed annual contracts, compressing margins. Manufacturers hedge via long-term supply pacts and dual sourcing, yet still face inventory carrying costs. Recent carbon black hikes announced by Cabot Corporation illustrate the exposure of adhesive formulators to input inflation. Such volatility impedes capital budgeting and may slow expansion in the double-sided tape market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Adhesive Chemistry: Acrylic Dominance Faces Specialty Challenge

Acrylics held 51.20% of the double-sided tape market in 2025 thanks to broad compatibility with metals, plastics, and glass. Superior UV stability and optical clarity underpin leadership in consumer electronics and exterior automotive trims. Rubber grades retain share in budget packaging, while silicone excels in engine-bay and medical uses. Specialty butyl and EVA tapes are forecast for a 6.92% CAGR, propelled by EV battery encapsulation and high-temperature industrial lines. Modified acrylate systems that wet low-surface-energy polyolefins extend acrylic reach, preserving its anchor role.

Acrylic innovations target faster wet-out at low pressure, enabling high-speed robotic application. Suppliers also lower residual monomers to meet sub-70 g/L VOC caps in California. Hybrid silicone-acrylic platforms blend initial tack with 200 °C resistance to address electronic power modules. These improvements reinforce acrylic’s strategic edge even as niche chemistries capture emerging performance gaps within the double-sided tape market.

By Backing Material: Foam Leadership Drives Innovation

Foam substrates contributed 29.74% revenue in 2025 and are projected for the fastest 6.95% CAGR. Micro-cellular PE and acrylic foams equalize stress, fill gaps, and damp vibration, ideal for façade panels and EV battery housings. Film backings follow for camera module assembly, where dimensional stability prevails. Paper remains a low-cost liner in stationery and graphic arts, though it cedes ground to recyclable PET options.

Sustainability gains traction as Shurtape’s launch of 90% post-consumer recycled PET tape signals growing demand for circular backings. Foam suppliers lower density without sacrificing cohesion, trimming material use. Metal foil backings niche into EMI shielding of 5G antennas. Collectively, these advances widen addressable use-cases, reinforcing foam’s position in the double-sided tape market.

By Tape Thickness: Miniaturization Drives Thin Film Demand

The 100–200 µm range captured 47.20% share in 2025 by balancing handling ease with bond integrity across automotive and construction jobs. Less than 100 µm products are poised for a 6.55% CAGR as smartphones, foldable displays, and compact sensors shrink component stacks. Producers now extrude five-layer tapes down to 5 µm that still carry thermal fillers for heat spread.

Over-200 µm constructions persist where gap-fill and vibration-damping outweigh thickness constraints, such as HVAC duct bonding. Process engineers deploy vision systems that align thin tapes within ±25 µm, unlocking automated placement. This spectrum of thickness solutions ensures the double-sided tape market services both legacy and next-gen assembly lines.

By End-user Industry: Construction Leads Multi-sector Growth

Construction owned 41.05% share in 2025 and heads for a 7.02% CAGR, fueled by façade panels, flooring trims, and sanitary ware fixtures that favor invisible fasteners. Residential refurbishment in Asia and North America boosts sales of tape-based mounting kits. Automotive remains the second pillar as structural bonding and battery thermal interfaces multiply tape touchpoints. Electronics delivers high margins through specialty optical and EMI tapes embedded in cameras and foldable displays.

Packaging and graphics keep steady demand, though sustainable mandates shift volume toward waterborne acrylics. Across industries, ESG scrutiny speeds the transition from solventborne to low-VOC platforms, safeguarding growth momentum for the double-sided tape market.

By Application: Mounting Overtakes Traditional Bonding

Bonding and joining represented 38.10% of sales in 2025, yet mounting shows the fastest 6.96% CAGR. Manufacturers want reversible attachments that simplify upgrades and recycling. Optically clear mounting tapes fix display cover glass while permitting service disassembly. Reclosable fasteners appear on modular furniture and auto interior trims, reinforcing the circular economy thrust.

Gap-filling seals thrive on foam technology that cushions differential expansion in façade joints. Thermal interface mounting widens scope in power electronics, blending insulation with heat transfer. The surge of multifunctional solutions broadens the functional map for the double-sided tape market.

Geography Analysis

Asia-Pacific accounted for 41.80% of global revenue in 2025 and is forecast for a 7.01% CAGR through 2031. Expanding EV production, intensive electronics outsourcing, and urban infrastructure projects underpin this dual leadership. China’s output of adhesive-intensive battery packs and the proliferation of Japanese smart-device lines sustain high-volume uptake. tesa reinforced its regional presence by opening Mumbai and Bengaluru hubs to bolster automotive and electronics support.

North America follows with construction stimulus and the reshoring of electronics assembly. 3M’s USD 67 million upgrade in Nebraska adds industrial tape capacity that addresses regional supply resilience. Growing EV battery factories across the United States expand demand for high-heat tapes.

Europe emphasizes sustainability, pushing suppliers toward solvent-free lines aligned with the EU Green Deal. Germany’s adhesive market, valued near EUR 2 billion in 2024, benefits from booming DIY refurbishment and packaging activity.

South America, the Middle East, and Africa remain early in adoption but gain traction through infrastructure expansion and growing automotive assembly. Government incentives for local electronics manufacturing in Brazil and the United Arab Emirates open incremental channels for the double-sided tape market.

Competitive Landscape

The double-sided tape market is moderately fragmented. 3M, tesa, and Avery Dennison anchor global supply, leveraging patent portfolios and multi-continent plants. 3M highlights material-science breakthroughs in its 2023 annual report that anticipate faster-curing and higher-temperature grades. tesa focuses on debond-on-demand technologies that aid recyclability. Avery Dennison broadened its Core Series in 2023 with new double-sided constructions tailored to converter workflows.

Regional challengers sharpen competitive pressure. Nitto is investing in a USD 8 billion Kentucky facility to scale advanced materials for the United States market. Henkel inaugurated a Loctite production plant in India in July 2024 to localize automotive supply. M&A activity continues, shown by Ellsworth’s acquisition of TapeCase to extend converting capabilities.

Technology race themes include hybrid silicone-acrylic matrices, bio-based polymers, and multi-function tapes that merge bonding with thermal or EMI performance. Top players collectively hold under 40% revenue share, indicating space for niche specialists to thrive in customized substrates.

Double-sided Tape Industry Leaders

3M

AVERY DENNISON CORPORATION

Lohmann

Nitto Denko Corporation

tesa SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: tesa has opened new offices in Mumbai and Bengaluru, to enhance operations in western India and focus on the electronics and automotive sectors in southern India. This expansion will strengthen the double-sided tape market by improving accessibility, driving innovation, and addressing the increasing demand in these key industries.

- March 2023: Avery Dennison Performance Tapes has introduced four new tape constructions as part of its 2023 Core Series Portfolio. This portfolio offers a comprehensive range of adhesive technologies in various tape constructions. Among the newly added products is the Avery Dennison FT 8299, a double-sided tape.

Global Double-sided Tape Market Report Scope

The double-sided tape market report includes:

| Acrylic |

| Rubber |

| Silicone |

| Other Adhesive Chemistries (Butyl, EVA, etc.) |

| Foam |

| Film |

| Paper |

| Cloth |

| Metal Foil and Others |

| Less than 100 µm |

| 100 – 200 µm |

| Greater than 200 µm |

| Automotive |

| Construction |

| Electronics |

| Other End-user Industries (Packaging and Graphics, etc.) |

| Mounting |

| Bonding and Joining |

| Sealing and Gap-filling |

| Insulation and Dampening |

| Other Applications (Splicing, Tabbing, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Adhesive Chemistry | Acrylic | |

| Rubber | ||

| Silicone | ||

| Other Adhesive Chemistries (Butyl, EVA, etc.) | ||

| By Backing Material | Foam | |

| Film | ||

| Paper | ||

| Cloth | ||

| Metal Foil and Others | ||

| By Tape Thickness | Less than 100 µm | |

| 100 – 200 µm | ||

| Greater than 200 µm | ||

| By End-user Industry | Automotive | |

| Construction | ||

| Electronics | ||

| Other End-user Industries (Packaging and Graphics, etc.) | ||

| By Application | Mounting | |

| Bonding and Joining | ||

| Sealing and Gap-filling | ||

| Insulation and Dampening | ||

| Other Applications (Splicing, Tabbing, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the double-sided tape market?

The double-sided tape market size is USD 15.4 billion in 2026.

Which region leads the market?

Asia-Pacific holds 41.80% share and shows the fastest 7.01% CAGR through 2031.

Which end-user sector generates the most demand?rowing region in Double-sided Tape Market?

Construction leads with 41.05% revenue share and a 7.02% growth rate.

Why are acrylic adhesives dominant?

Acrylics balance adhesion, weatherability, and low VOCs, securing 51.20% market share in 2025.

What application segment is growing quickest?

Mounting solutions post the highest 6.96% CAGR as industries prioritize reversible assemblies.

Page last updated on: