Copper Pipes And Tubes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 5.22 Million tons |

| Market Volume (2031) | 6.26 Million tons |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

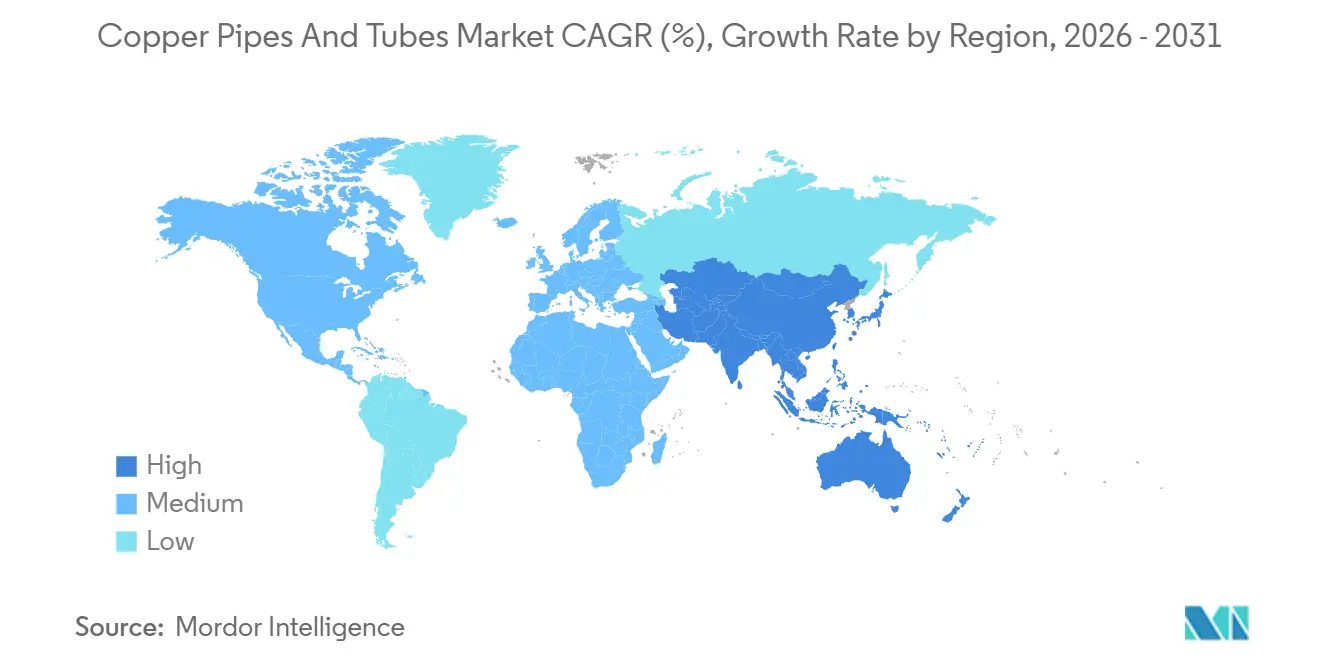

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

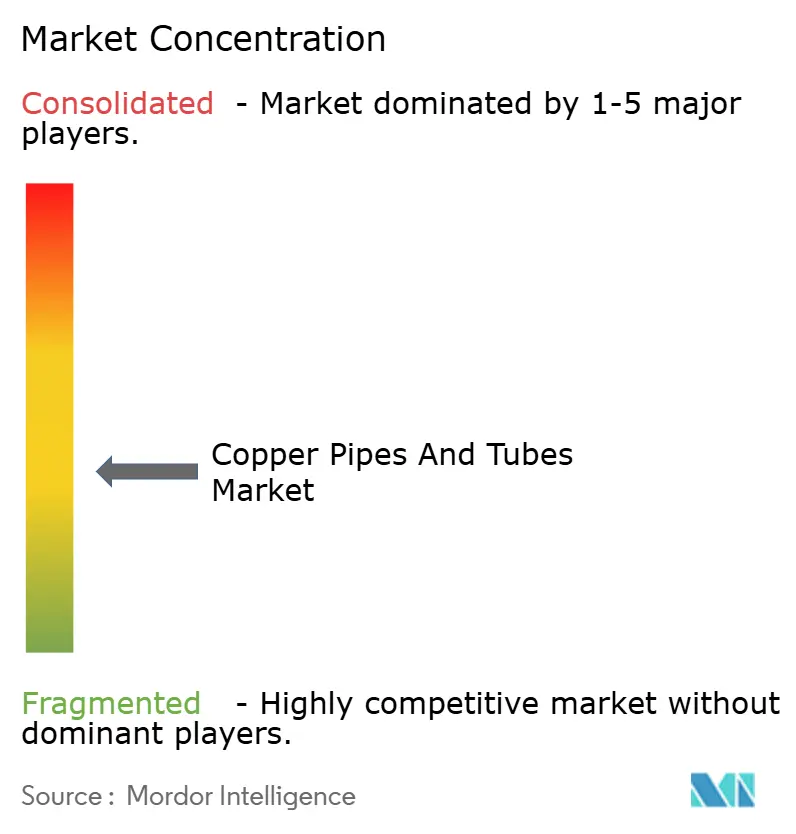

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Copper Pipes And Tubes Market Analysis by Mordor Intelligence

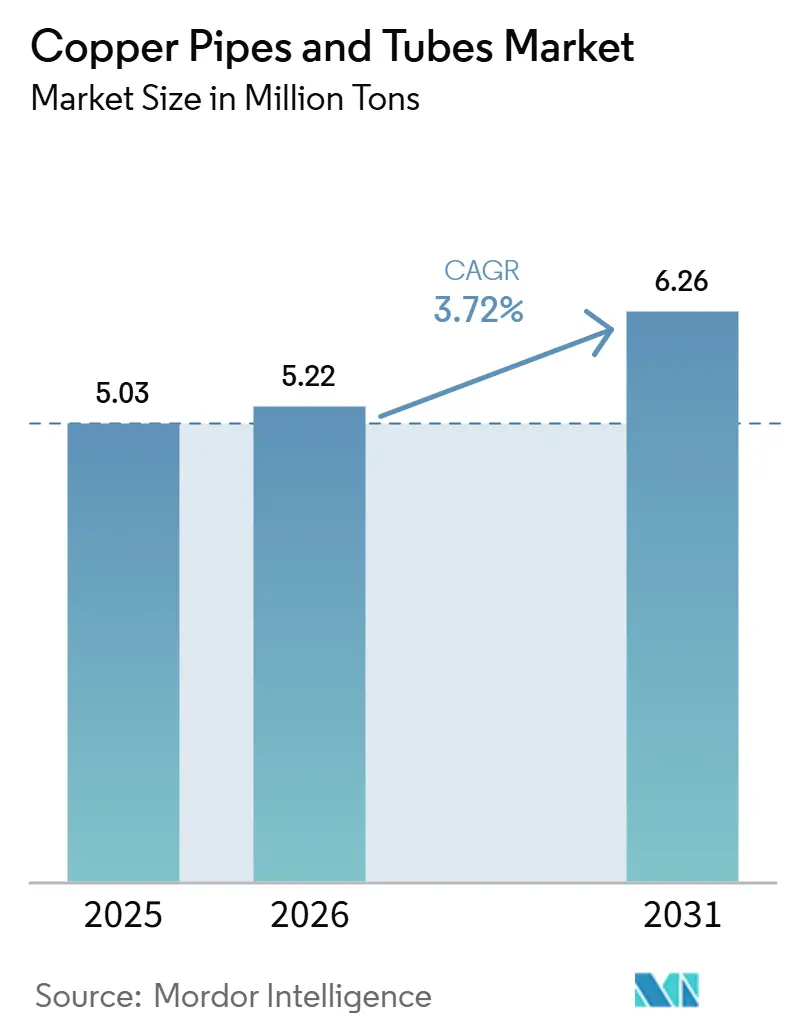

The Copper Pipes and Tubes Market size was valued at 5.03 million tons in 2025 and is estimated to grow from 5.22 million tons in 2026 to reach 6.26 million tons by 2031, at a CAGR of 3.72% during the forecast period (2026-2031). Policy-driven adjustments toward low-global warming potential (GWP) refrigerants in heat-exchange systems are increasing wall-thickness specifications. This change is driving demand for tons of material, even as aluminum micro-channel condensers gain market share in entry-level HVAC lines. Seamless tubes, without longitudinal welds, dominate pressure-critical applications by meeting American Society of Mechanical Engineers (ASME) B31.5 and American Society for Testing and Materials (ASTM) B280 standards. Investments in district cooling across Gulf states, along with appliance trade-in subsidies in China, are supporting regional growth. In North America, the reshoring of HVAC assembly is reducing lead times but increasing energy and labor costs. Supply dynamics remain constrained, with London Metal Exchange (LME) cash copper prices projected to average USD 12,000-14,500 per ton in 2025-2026. This trend is reducing smelter treatment charges and indicating potential feedstock constraints beyond 2027.

Key Report Takeaways

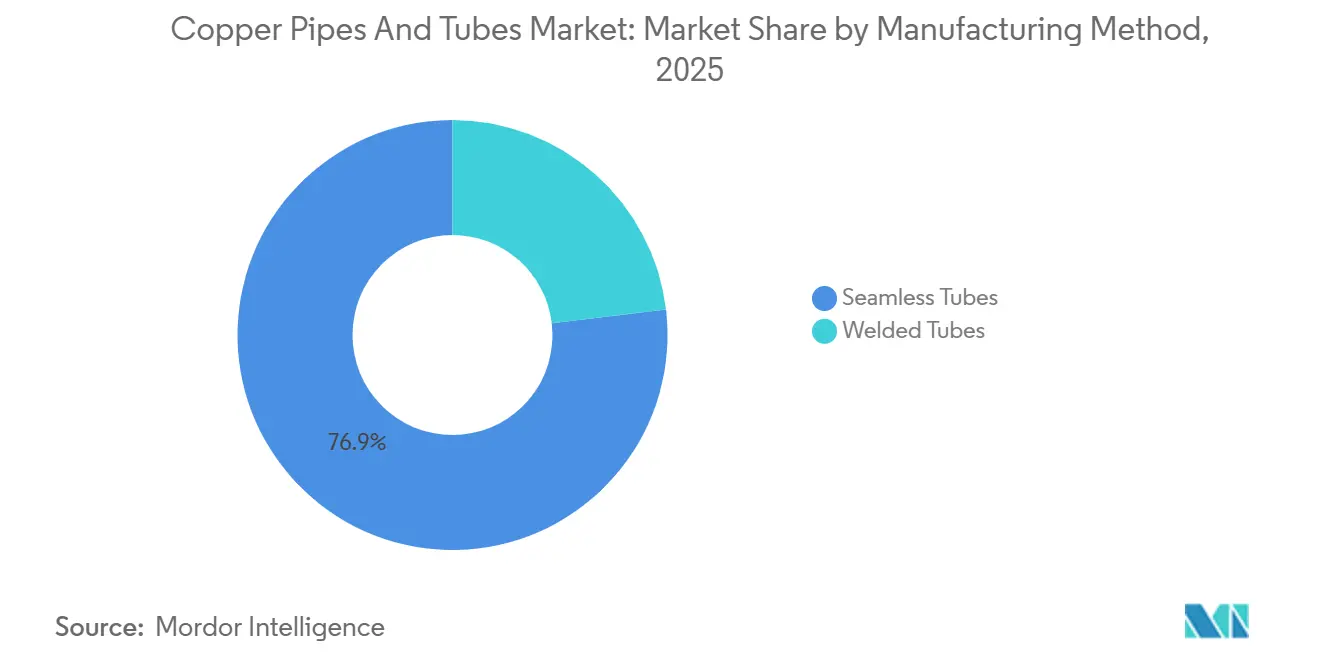

- By manufacturing method, seamless tubes led with 76.89% of the copper pipes and tubes market share in 2025 and will expand at a 4.03% CAGR through 2031.

- By type, straight-length pipes and tubes led with 59.92% of the copper pipes and tubes market share in 2025, while capillary tubes posted the highest 4.08% CAGR through 2031.

- By application, air-conditioning and refrigeration accounted for a 53.55% slice of the copper pipes and tubes market size in 2025, and district-cooling networks are slated to grow at 4.45% through 2031.

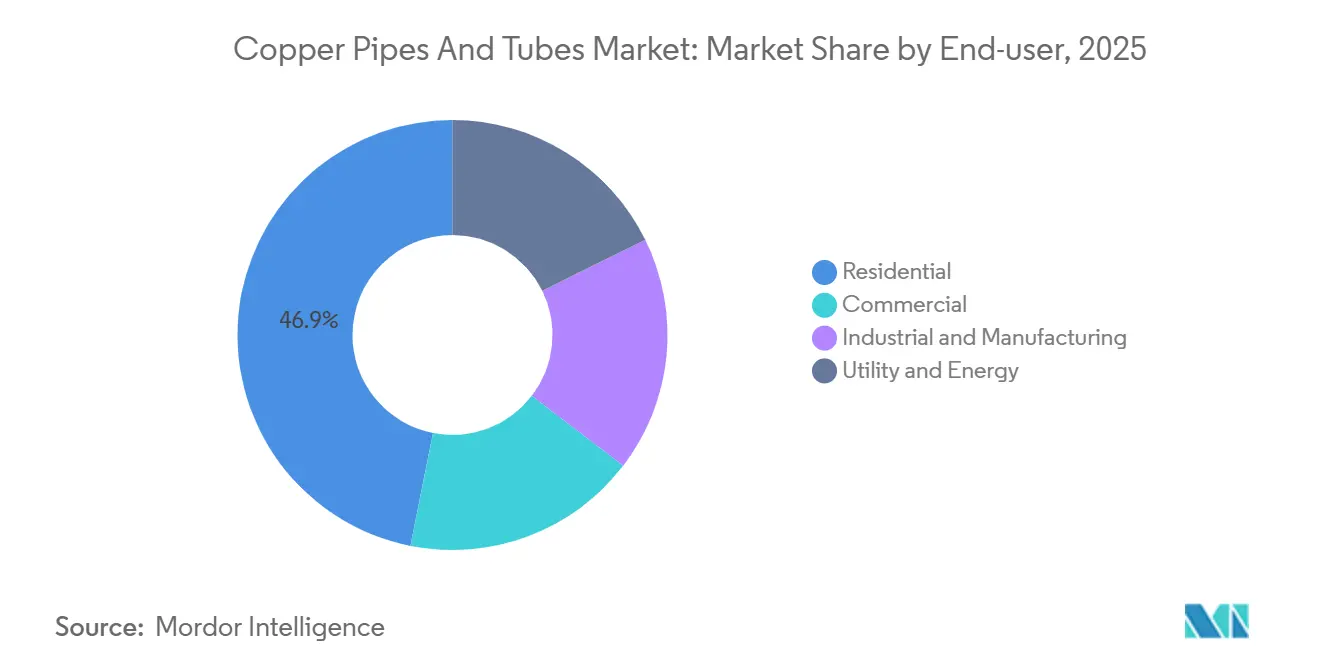

- By end-user, residential commanded 46.88% share of the copper pipes and tubes market in 2025; the utility and energy sector is projected to grow at a 4.83% CAGR to 2031.

- By geography, Asia-Pacific commanded exactly 50.11% of the 2025 volume, while it is forecast to advance at the fastest 4.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Copper Pipes And Tubes Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from HVAC and refrigeration applications | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of construction and infrastructure investment | +0.9% | Asia-Pacific (China, India, ASEAN), Middle East (GCC), North America | Long term (≥ 4 years) |

| Rising usage in renewable-energy and heat-pump systems | +0.7% | Europe, North America, Japan | Medium term (2-4 years) |

| Mandates for low-GWP refrigerants driving copper redesign | +0.8% | Global, led by EU and North America regulatory zones | Short term (≤ 2 years) |

| Reshoring of HVAC and heat-exchanger manufacturing | +0.5% | North America, with spillover to Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from HVAC and Refrigeration Applications

In 2025, air-conditioning and refrigeration accounted for 53.55% of the total volume, supported by replacement cycles and new constructions in tropical regions. China's "double-new" appliance initiative in March 2024, which subsidizes high-efficiency air-conditioners, has led to a nearly 20% year-on-year increase in copper-tube orders[1]Huaon Research, “China Copper Tube Demand Under ‘Double-New’ Program,” huaon.com. In Japan and South Korea, variable-refrigerant-flow (VRF) systems dominate the commercial heating, ventilation, and air conditioning (HVAC) landscape, requiring micro-grooved tubes that enhance the heat-transfer surface by approximately 18%. Adhering to American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) 15 and International Organization for Standardization (ISO) 5149 standards, original equipment manufacturers (OEMs) maintain flare joint tolerances within ±0.05 mm, effectively minimizing leak risks. The transition to R-32 in residential units elevates discharge pressure to nearly 2.6 megapascals (MPa), necessitating the use of ASTM B280 seamless tubes with 0.8 mm walls for 9.52 mm outer diameters.

Expansion of Construction and Infrastructure Investment

As urbanization accelerates in the Asia-Pacific and Gulf regions, there is a growing demand for plumbing and district cooling. India's Smart Cities Mission has driven an increase in Variable Refrigerant Volume (VRV) systems, with malls and IT parks opting for systems that utilize approximately 28% more copper per cooling ton than standard split units. In 2025, Empower expanded Dubai's district-cooling pipeline by 19 kilometers, managing 90 plants that cater to over 1,500 buildings[2]District Energy Association, “Business Bay Fifth Plant Contract,” districtenergy.org. Qatar Cool operates five plants serving more than 140 buildings, while Saudi Arabia's Diriyah Gate includes a 72,500-ton plant, leveraging large-diameter copper piping to minimize thermal loss across its expansive 7 square kilometer area.

Rising Usage in Renewable-Energy and Heat-Pump Systems

In 2025, European heat-pump installations increased by 11%, driven by boiler bans and retrofit grants ranging from 30-50% in Germany and France. Ground-source loops prefer seamless coils, as brazed joints can lead to galvanic corrosion. Japan's heat-pump market is projected to grow at a compound annual growth rate (CAGR) of over 3.6% through 2030, with finned copper being the preferred choice for rooftop condensers in densely populated urban areas. Solar-thermal collectors utilize Type L tubes, capable of withstanding 200 degrees Celsius stagnation, and Scandinavian geothermal projects benefit from pre-insulated coils, which can reduce on-site labor by up to 25%.

Mandates for Low-GWP Refrigerants Driving Copper Redesign

Starting in 2025, the European Union's (EU) F-Gas Regulation 2024/573 and the United States' (U.S.) The American Innovation and Manufacturing (AIM) Act will phase out R-410A, pushing OEMs towards A2L blends, which are slightly flammable and operate at 10-15% higher pressures than their predecessors. New compliance measures mandate leak sensors and charge caps, prompting manufacturers to reduce refrigerant inventory by 15-25%. This is achieved by using micro-grooved tubes, which enhance heat-transfer coefficients by 1.4 times. Investments in bright-annealing and nitrogen-purged drawing lines ensure oxide-free interiors, critical for preventing A2L decomposition at temperatures exceeding 120 degrees Celsius.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost vs. plastic and composite alternatives | -0.6% | Global, with acute pressure in cost-sensitive residential segments | Medium term (2-4 years) |

| Copper price volatility and supply-chain risk | -0.8% | Global, amplified in import-dependent regions (Europe, North America) | Short term (≤ 2 years) |

| Shift to aluminum micro-channel heat exchangers | -0.9% | North America, Europe, emerging in Asia-Pacific OEM product lines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost vs. Plastic and Composite Alternatives

By reducing brazing hours and simplifying handling, PEX (cross-linked polyethylene) and polypropylene press-fit pipes have lowered installed costs by approximately 45% compared to copper. PEX-A, recognized for its durability against freeze-thaw cycles and supported by 50-year warranties, is increasingly being utilized in North American retrofits. As of 2025, the hourly rates for skilled brazers exceeded USD 45, contributing to higher labor costs. While copper's antimicrobial properties maintain its relevance in healthcare and hospitality sectors, most codes now permit the use of PEX, provided chlorine residuals remain below 2 ppm. In 2025, with LME (London Metal Exchange) copper priced at approximately USD 14,500 per ton and HDPE (high-density polyethylene) resin at around USD 1,200, the material-cost ratio expanded to 12:1, driving the adoption of plastic alternatives.

Copper Price Volatility and Supply-Chain Risk

In 2025, LME's three-month copper prices rose to USD 4.49 per lb, influenced by mine disruptions that removed 400,000 tons of supply. As concentrate treatment charges dropped to near zero, smelters were unable to transfer ore costs to tube mills, compressing margins across the value chain. U.S. HVAC (heating, ventilation, and air conditioning) contractors reported an annual supply-chain friction cost of USD 67,000, which included hedging fees and emergency spot purchases. To mitigate volatility, vertically integrated recyclers, such as Wieland’s facility in Shelbyville, Kentucky, sourced 35% of their feedstock from post-consumer scrap, resulting in an EBITDA (earnings before interest, taxes, depreciation, and amortization) spread increase of approximately 250 basis points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Manufacturing Method: Seamless Dominates Pressure-Critical Roles

Seamless tubes, accounting for 76.89% of the 2025 volume, are projected to grow at a rate of 4.03% through 2031. This growth is driven by rising discharge pressures, a consequence of heat-pump usage and low-global warming potential (GWP) refrigerants. These seamless tubes dominate the copper pipes and tubes market, particularly in heating, ventilation, and air conditioning (HVAC), marine, and medical-gas circuits, where burst strengths need to exceed 4 MPa. While welded tubes offer a cost advantage in district-cooling water loops and plumbing risers, their longitudinal seam disqualifies them from use in American Society of Mechanical Engineers (ASME) B31.5 refrigerant lines. Wieland has invested USD 500 million in modernizing its East Alton facility, adding hot-rolling capabilities specifically for seamless tubes used in electric-vehicle battery cooling.

Seamless products have margins 15-20% higher than their welded counterparts, due to the costs associated with multi-pass drawing and plug-mill processes. However, this premium reduces for diameters exceeding 54 mm, where extrusion presses become less feasible. Continuous-strip welded lines operate at 7,000 tons per month, primarily catering to original equipment manufacturer (OEM) contracts for commodity refrigerators. As the market evolves, seamless tubes are set to command nearly four-fifths of the copper pipes and tubes market share by 2031.

By Type: Straight Lengths Lead, Capillary Tubes Accelerate

Straight-length pipes constituted 59.92% of the 2025 tonnage. Commercial installers prefer these rigid 6 m sections, as they reduce joint counts by a third. Level-wound coils, favored for their ease of retrofit in attics and crawlspaces, can cut labor hours by about 25%. While finned variants may have a smaller volume, they significantly enhance rooftop condensers by expanding the surface area eightfold. Capillary tubes are witnessing the fastest growth at a 4.08% compound annual growth rate (CAGR), driven by the adoption of inverter-driven variable-refrigerant-flow systems. These systems require precise refrigerant metering through 0.6-1.2 mm bores. Maintaining a precision calibration within ±5 mm is crucial, especially for evaporator superheats in the 3-5°C range, a standard for 65% of global residential air conditioning (AC) shipments in 2025 that were equipped with inverter compressors.

Custom profiles, such as flattened ovals tailored for automotive evaporators, command a 40-50% margin premium due to the need for specialized tooling. Mueller’s acquisition of Elkhart Products in 2024 brought in solder fittings, which conveniently bundle with straight tubes. This strategic move not only streamlines wholesaler procurement but also strengthens customer loyalty. Between 2026 and 2031, the market for capillary formats is set to outpace all other types, albeit starting from a smaller base.

By Application: District Cooling Emerges as Growth Frontier

While air-conditioning and refrigeration accounted for 53.55% of the 2025 volume, district-cooling lines are projected to grow at a 4.45% CAGR through 2031. This surge is attributed to Gulf utilities deploying centralized chilled-water networks, achieving up to a 30% reduction in peak electricity demand. Empower’s new 44,000-refrigeration ton (RT) Business Bay plant, with a connected capacity surpassing 320,000 RT, serves 1,500 buildings. Each of these buildings relies on copper-nickel (CuNi) 90/10 mains for its seawater-cooled condensers. Plumbing remains a significant sector, with Type L and Type K tubes not only meeting National Sanitation Foundation (NSF) 61 potable-water standards but also offering antimicrobial benefits, a necessity in healthcare settings. In industrial sectors, especially petrochemicals and food processing, finned copper is the preferred choice for heat-exchangers, ensuring superior thermal conductivity in circuits using glycol, brine, and condensate.

Transportation sectors, spanning automotive to marine, utilize micro-grooved and flattened tubes. These are essential for maximizing heat flux in confined spaces. In the medical field, gas networks rely on seamless Type K pipes, which undergo radiographic inspections to ensure leak-free oxygen service. As the copper pipes and tubes market diversifies, it is evident that sectors beyond HVAC, including new energy and specialized industrial processes, are set to contribute significantly.

By End-User: Utility Sector Accelerates on Heat-Pump Mandates

In 2025, residential end-users accounted for 46.88% of copper consumption. However, the utility and energy segment is on an upward trajectory, expected to grow at 4.83%. This growth is largely driven by subsidies in Europe and North America for grid-connected heat pumps, promoting low-carbon heating. Commercial entities, from offices to hotels, are increasingly adopting variable refrigerant volume (VRV) systems. These systems, while consuming 28% more copper per cooling-ton, offer an 18% energy saving, a trade-off made viable by rising carbon prices. Industrial facilities harness copper's thermal conductivity for process cooling, managing fluid temperatures between -40 °C and 150 °C. In Scandinavia, utility-scale heat-pump district heating systems require extensive kilometers of pre-insulated copper, ensuring efficient movement of low-grade waste heat.

In the Asia-Pacific, rapid urbanization is driving residential demand. Meanwhile, in North America, homeowners are replacing older AC units, particularly those pre-dating the Seasonal Energy Efficiency Ratio 2 (SEER2) standards introduced in January 2023. Highlighting the market's vitality, Zhejiang Hailiang reported a nearly 20% year-on-year surge in refrigeration-sector orders in Q1 2025, propelling its market share in China to over 40%.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 50.11% of the global volume and is projected to grow at a rate of 4.72% through 2031. In 2024, China produced 236,000 tons of tubes, marking a 5.4% increase, supported by refrigerator trade-in incentives extending into 2025. The artificial intelligence (AI)-enabled inspection lines at Ningbo Jintian demonstrate the region's advancements in productivity and quality. India's per-capita consumption of copper tubes is one-tenth of that in developed markets, indicating significant growth potential as heating, ventilation, and air conditioning (HVAC) penetration increases with the Smart Cities initiative. Japan and South Korea are diversifying copper applications into battery thermal management and semiconductor cleanrooms, reducing reliance on traditional air conditioning.

In North America, while the volume remained stable, aluminum micro-channel heat exchangers gained market share. Reshoring efforts are improving coordination between original equipment manufacturers (OEMs) and mills. Mitsubishi's plant in Kentucky and Mueller's expansion in Oklahoma are optimizing logistics, though both face domestic power tariffs that increase cost bases by 12-18%. Europe recorded an 11% growth in heat-pump installations in 2025. However, the adoption of plastic piping in radiant heating has moderated the demand for copper. Wieland's USD 27 million expansion in Montpelier, Ohio, reflects demand from both defense and renewable energy sectors.

The Middle East & Africa and South America represent smaller but growing markets. Dubai's Empower operates 90 plants, Qatar Cool manages a network spanning 140 buildings, and Saudi Arabia's large-scale projects, such as Diriyah Gate, are incorporating copper-alloy mains into district-cooling systems. In South America, despite challenges like currency devaluation, commercial retrofits are progressing, encouraging local scrap-fed mills to increase production. The copper pipes and tubes market remains concentrated in the Asia-Pacific region while experiencing faster growth in Gulf infrastructure projects.

Competitive Landscape

The copper pipes and tubes market is moderately fragmented. Mueller Industries, Wieland Group, Zhejiang Hailiang Co., Ltd., Aurubis AG, and FURUKAWA ELECTRIC CO., LTD., the five largest suppliers, account for an estimated 35-40% of global production volume. These suppliers have vertically integrated into scrap collection and rod casting to mitigate raw-material fluctuations. Aurubis’s USD 800 million Richmond recycling complex, operational since January 2026, processes 180,000 tons of multi-metal feed and targets an EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) of EUR 170 million (USD 195.78 million) by FY 2028. Technology upgrades focus on achieving oxide-free interiors through nitrogen-purged draws and AI (Artificial Intelligence)-assisted defect detection. This commitment to innovation is highlighted by Ningbo Jintian receiving a province-level AI benchmark award in February 2025.

New market entrants from India and Southeast Asia, including Uniflow and Mehta Tubes, are leveraging lower power tariffs to compete on pricing against established players. However, they face challenges in obtaining ASTM (American Society for Testing and Materials) B280 and EN (European Norm) 12735 certifications. Patent activity is increasing, particularly around micro-grooved geometries and internally enhanced tubes. Wieland’s “CuProLife” line, introduced in 2023, demonstrates sustainability by being entirely produced from recycled copper and meeting LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method) standards. In aerospace HVAC (Heating, Ventilation, and Air Conditioning) systems, hybrid copper-aluminum brazed assemblies are gaining adoption, as their weight savings justify the copper's higher cost. The industry's competitive strategies are increasingly focused on recycling initiatives, specialty alloys, and bundled downstream fittings, fostering loyalty among wholesalers.

Copper Pipes And Tubes Industry Leaders

Mueller Industries

Wieland Group

Zhejiang Hailiang Co., Ltd.

Aurubis AG

FURUKAWA ELECTRIC CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mueller Industries completed the acquisition of Bison Metals Technologies in Shawnee, Oklahoma, to expand its seamless-tube production capacity and secure a reliable domestic feedstock supply. This move is expected to strengthen its position in the copper pipes and tubes market.

- February 2026: Emirates Central Cooling Systems Corporation has awarded the design for its fifth district-cooling plant in Business Bay, with ground-breaking scheduled for Q4 2026. The project is expected to drive demand for copper pipes and tubes, which are essential components in district cooling systems due to their durability and thermal conductivity.

Global Copper Pipes And Tubes Market Report Scope

Copper pipes and tubes, made from durable and corrosion-resistant copper, are cylindrical conduits used for transporting fluids such as water and gas, and are integral to heating, ventilation, and air conditioning (HVAC) systems. Although the terms are often used interchangeably, tubes are sized by their outer diameter (OD) and are suited for flexible or specific applications. Pipes, on the other hand, are rigid, sized by their nominal internal diameter (ID), and primarily used in plumbing.

The copper pipes and tubes market is segmented by manufacturing method, type, application, end-user, and geography. By manufacturing method, the market is segmented into seamless tubes and welded tubes. By type, the market is segmented into straight-length pipes and tubes, level-wound coils (LWC), finned tubes, capillary tubes, and custom shapes/profiles. By application, the market is segmented into air-conditioning and refrigeration, plumbing and potable water, medical gas and vacuum systems, industrial heat exchangers, transportation (auto, rail, marine), and district cooling and heating networks. By end-user, the market is segmented into residential, commercial, industrial, manufacturing, and utility and energy. The report also covers the market size and forecasts for the copper pipes and tubes in 17 countries across major regions. The market sizes and forecasts are provided in terms of volume (Ton).

| Seamless Tubes |

| Welded Tubes |

| Straight-Length Pipes and Tubes |

| Level-Wound Coils (LWC) |

| Finned Tubes |

| Capillary Tubes |

| Custom Shapes/Profiles |

| Air-Conditioning and Refrigeration |

| Plumbing and Potable Water |

| Medical Gas and Vacuum Systems |

| Industrial Heat Exchangers |

| Transportation (Auto, Rail, Marine) |

| District Cooling and Heating Networks |

| Residential |

| Commercial |

| Industrial and Manufacturing |

| Utility and Energy |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle-East and Africa |

| By Manufacturing Method | Seamless Tubes | |

| Welded Tubes | ||

| By Type | Straight-Length Pipes and Tubes | |

| Level-Wound Coils (LWC) | ||

| Finned Tubes | ||

| Capillary Tubes | ||

| Custom Shapes/Profiles | ||

| By Application | Air-Conditioning and Refrigeration | |

| Plumbing and Potable Water | ||

| Medical Gas and Vacuum Systems | ||

| Industrial Heat Exchangers | ||

| Transportation (Auto, Rail, Marine) | ||

| District Cooling and Heating Networks | ||

| By End-user | Residential | |

| Commercial | ||

| Industrial and Manufacturing | ||

| Utility and Energy | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for copper pipes and tubes be by 2031?

The Copper Pipes and Tubes Market size was valued at 5.03 million tons in 2025 and is estimated to grow from 5.22 million tons in 2026 to reach 6.26 million tons by 2031, at a CAGR of 3.72% during the forecast period (2026-2031).

Which region will add the most incremental tonnage throughout the forecast period?

Asia-Pacific, projected to expand at a 4.72% CAGR on the back of China’s appliance incentives and India’s construction boom.

Why are seamless tubes preferred in HVAC refrigerant circuits?

They lack a longitudinal weld, giving higher burst strength that meets ASME B31.5 and ASTM B280 when operating pressures rise with low-GWP refrigerants.

What is the primary factor restraining copper tube growth in entry-level residential plumbing?

The installed cost gap versus PEX and polypropylene systems, which can be about 45% cheaper once labor is included.

Page last updated on: