Tubular Membrane Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

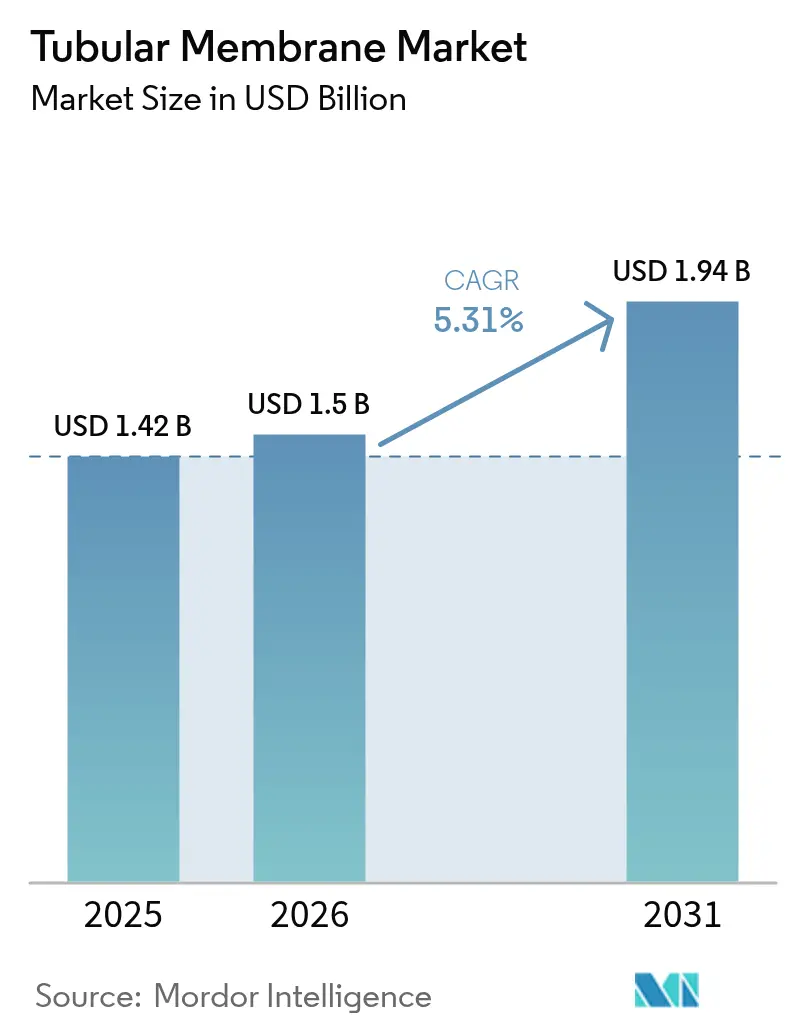

| Market Size (2026) | USD 1.5 Billion |

| Market Size (2031) | USD 1.94 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tubular Membrane Market Analysis by Mordor Intelligence

Tubular Membrane Market size in 2026 is estimated at USD 1.5 billion, growing from 2025 value of USD 1.42 billion with 2031 projections showing USD 1.94 billion, growing at 5.31% CAGR over 2026-2031. A convergence of stricter discharge rules, rising industrial water-recycling targets and the proven resilience of tubular designs under high-solids loading drives near-term demand. Municipal utilities account for the largest installed base because membrane bioreactors (MBRs) combine biological treatment and microfiltration in one compact train, helping utilities meet emerging potable-reuse regulations while optimizing energy use. Industrial operators, led by the chemical and petrochemical sectors, are upgrading legacy plants to comply with tougher chemical oxygen demand (COD) and emerging contaminant limits, a trend reinforced by the technology’s strong fouling resistance in oily, saline and abrasive streams. Material science advances—especially nanocomposite PVDF and rapidly maturing ceramic modules—reduce lifecycle costs and widen the operating envelope, while forward-osmosis pilots reveal a pathway toward low-pressure, resource-recovery schemes. At the same time, global equipment suppliers accelerate merger activity to gain scale, geographic reach and integrated services capabilities that de-risk adoption for end users.

Key Report Takeaways

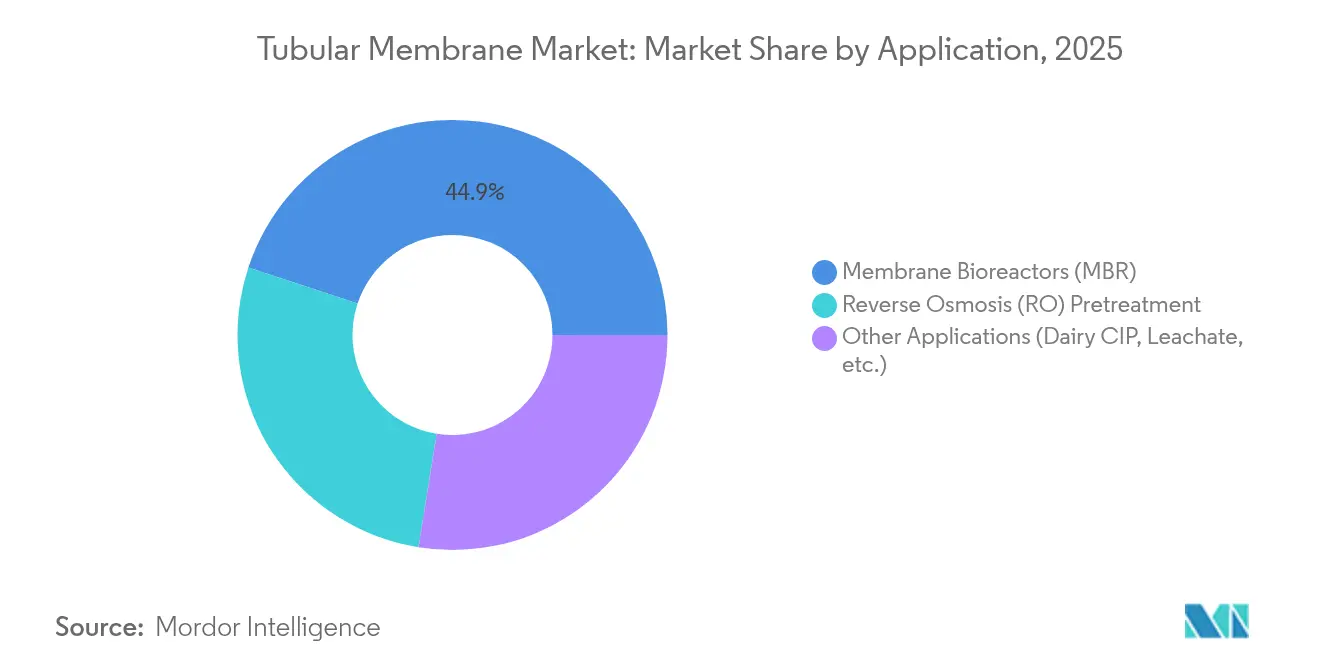

- By application, membrane bioreactors held 44.92% of the tubular membrane market share in 2025, whereas reverse-osmosis pretreatment is projected to advance at a 5.82% CAGR through 2031.

- By membrane material, PVDF modules accounted for 50.35% of the tubular membrane market size in 2025 and ceramic units are poised to expand at a 5.69% CAGR between 2026-2031.

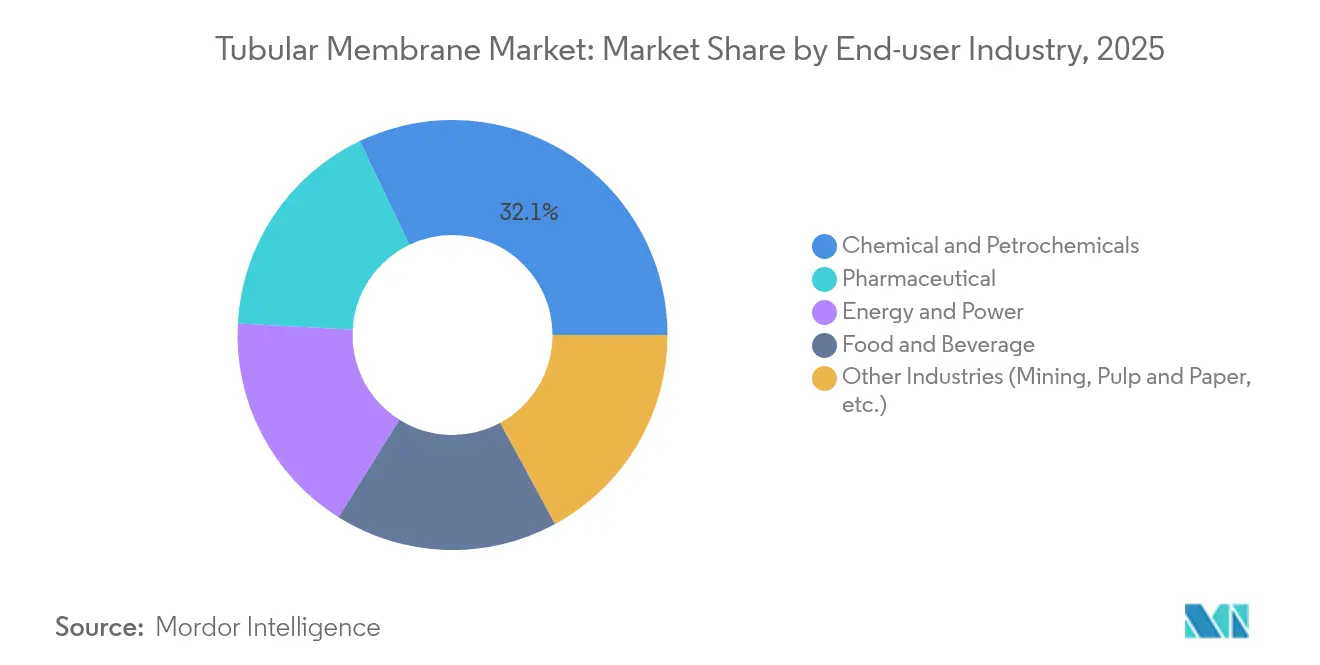

- By end-user industry, chemical and petrochemical plants captured 32.10% of the tubular membrane market size in 2025, while pharmaceutical facilities are forecast to grow fastest at a 5.78% CAGR to 2031.

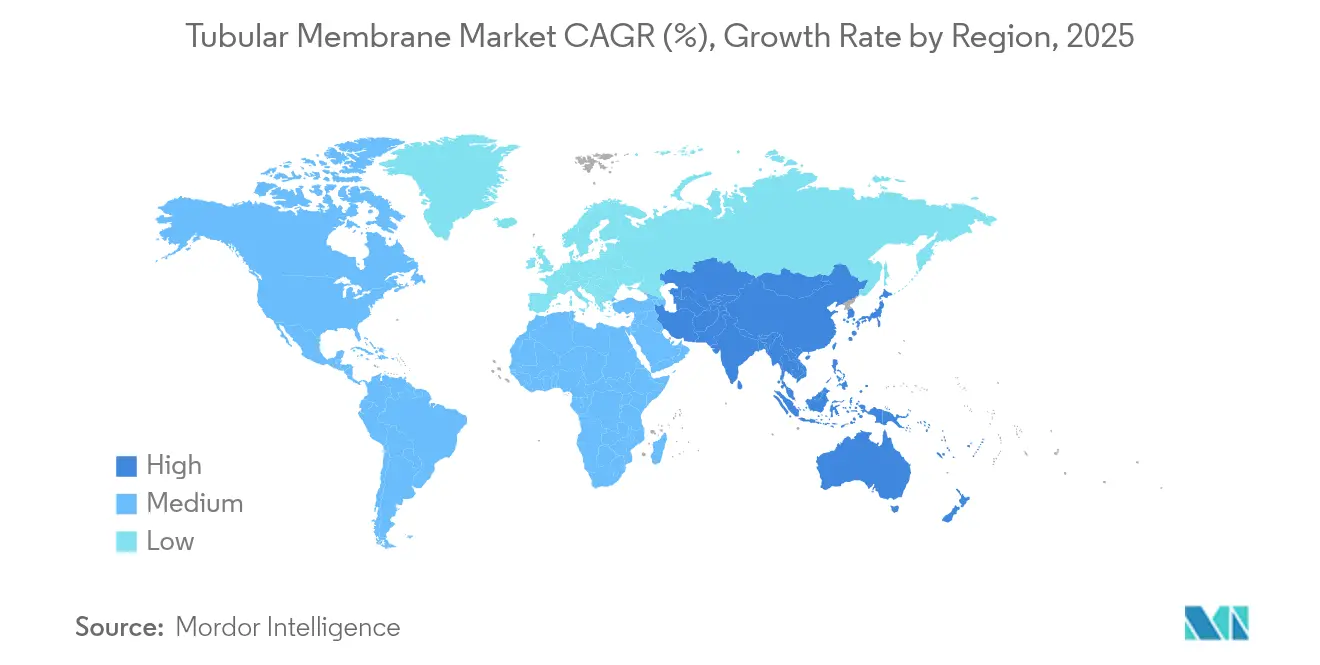

- By geography, Asia-Pacific commanded 42.60% of the tubular membrane market share in 2025, outpacing all regions with a 5.72% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tubular Membrane Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of membrane bioreactors | +1.2% | APAC, North America, Europe | Medium term (2-4 years) |

| Industrial demand for high-strength treatment | +0.9% | APAC core; spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Stricter global discharge and reuse regulations | +0.8% | EU and North America most stringent | Short term (≤ 2 years) |

| Tubular forward-osmosis, low-energy modules | +0.4% | North America and EU; early APAC adoption | Long term (≥ 4 years) |

| Biomimetic aquaporin-based separations | +0.3% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Membrane Bioreactors

Cities increasingly view MBRs as a dual answer to regulatory compliance and potable-reuse ambitions. California’s net-energy-positive staged anaerobic fluidized bed-MBR at Silicon Valley Clean Water cuts biosolids production by 90% and demonstrates energy self-sufficiency, anchoring procurement decisions among U.S. utilities. Similar pilots in Singapore, Beijing and Milan validate robust pathogen removal under high mixed-liquor suspended solids, underpinning global uptake. The compact footprint eases siting in dense metros, while high solids tolerance allows treatment plants to intensify capacity without land expansion. Consequently, capital programs in North America and East Asia now incorporate tubular MBRs as default for new works or major retrofits, reinforcing growth in the tubular membrane market.

Industrial Demand for High-Strength Effluent Treatment

Chemical facilities moving toward circular-water strategies favor tubular membranes because they withstand solvent spikes, high salinity and abrasive particulates better than flat-sheet or hollow-fiber analogs. Recent 20 g/L-salinity MBR trials reported 97% COD abatement and near-complete BOD removal, validating performance in brine and produced-water settings[1]MDPI, “High-Salinity MBR Performance,” mdpi.com. Pharmaceutical formulators shifting to continuous processing generate concentrated wastes that demand mechanically robust modules capable of 24/7 operation at elevated trans-membrane pressures. In mining, ceramic tubular units deliver long runtimes in acid mine drainage service, cutting chemical dosing and downtime. These industrial use cases collectively fuel incremental consumption within the tubular membrane market.

Stricter Global Discharge and Water-Reuse Regulations

Policy tightening is immediate. The EU’s Regulation 2020/741 sets recycled-water quality thresholds and signals future vertical reuse mandates. India’s draft Liquid Waste Management Rules compel zero-liquid-discharge technology adoption by October 2025, effectively mandating advanced membranes for major water-using industries. Japan’s 2025 PFAS cap of 50 ng/L triggers industrial retrofits to meet new ambient standards. The U.S. EPA is finalizing effluent limitation guidelines that tighten nutrient and micro-pollutant thresholds through 2030 EPA.GOV. Tubular systems, proven to deliver sub-ppm effluent under variable loading, emerge as reliable compliance solutions, strengthening adoption across the tubular membrane market.

Tubular Forward-Osmosis Modules Enable Low-Energy Concentration

Forward-osmosis (FO) arrangements using thin-film nanocomposite active layers reach 24.5 L/m²·h flux with minimal reverse solute leakage, shaving energy use by up to 50% versus reverse osmosis in high-salinity concentration duty. Tubular housings simplify cleaning and handle higher suspended solids than spiral-wound FO designs, broadening applicability to food-waste valorization, lithium brine concentration and refinery blow-down minimization. Early adopters in North America pilot hybrid FO-MBR flowsheets that combine energy savings with organics recovery, a trend expected to migrate into mainstream projects over the decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from hollow-fiber and flat-sheet types | –0.7% | Global; strongest in cost-sensitive projects | Medium term (2-4 years) |

| High CAPEX for small and decentralized facilities | –0.5% | Emerging markets and rural applications worldwide | Long term (≥ 4 years) |

| PVDF restrictions linked to PFAS legislation | –0.4% | EU and North America; potential global knock-on | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Hollow-Fiber, Flat-Sheet and Other Alternatives

Hollow-fiber MBRs deliver higher packing density and lower installed costs per square meter, steering price-sensitive municipal tenders toward these designs in regions with ample land. Flat-sheet cassettes provide easy access for visual inspection, a key benefit for operators lacking advanced maintenance tooling. Graphene-oxide laminates boasting 6–66 L cm-² MPa-¹ water permeability threaten to leapfrog all polymeric systems on energy performance[2]Nature, “Graphene-Oxide Membranes for High-Flux Filtration,” nature.com. Meanwhile, photocatalytic self-cleaning coatings under development could narrow the fouling-resistance advantage historically enjoyed by tubular modules. These headwinds temper adoption in segments where high-solids resilience is not critical.

High CAPEX for Small and Decentralized Facilities

Thicker walls, specialty connectors and rugged housings make tubular units more expensive on a per-volume basis than hollow fibers, limiting feasibility in rural municipalities or mobile emergency units. Ceramic tubes in particular carry premium front-end costs even though they offer long service life. Portable recycling systems such as Japan’s WOTA BOX reclaim more than 98% of waste water at lower upfront budgets, underscoring the price gap facing tubular suppliers. Limited access to skilled technicians in remote settings raises the cost barrier further, prolonging payback periods and impeding penetration into the lowest-income regions of the tubular membrane market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: MBR Systems Drive Market Leadership

Membrane bioreactors controlled 44.92% of the tubular membrane market in 2025, underpinned by their capacity to treat high mixed-liquor concentrations without secondary clarification. This dominance reflects the integration benefits of merging biological oxidation with physical separation, lowering overall plant footprints and enabling fast retrofits within existing clarifier basins. The segment leverages modular skid layouts that simplify expansion as flows rise, a consideration for utilities facing population growth and industrial-park hookups. Energy intensity continues to decline as fine-bubble aeration and intermittent operation routines gain traction, further cementing the business case for MBR installations across the tubular membrane market.

Reverse-osmosis pretreatment, while smaller, is projected to post a 5.82% CAGR to 2031 as desalination operators adopt multi-barrier flowsheets to protect high-pressure RO stages from fouling. Tubular membranes’ ability to handle turbid feed waters laced with oil, grease and biopolymers that overwhelm micro-sand filters positions them as a resilient first-stage screen. Dairy clean-in-place recovery, leachate polishing and landfill condensate management remain niche but steady outlets, benefitting from the tubes’ mechanical strength and ease of chemical cleaning. Together, these diversified applications broaden revenue streams and mitigate cyclicality within the tubular membrane market.

By Membrane Material: PVDF Dominance Faces Regulatory Challenges

Polyvinylidene fluoride maintained 50.35% control of the tubular membrane market in 2025 because it offers an advantageous mix of chemical resistance, weldability and mature supply chains. However, the European Chemicals Agency’s planned PFAS restrictions, set to limit PVDF deployment in potable-water systems beginning 2026, spark portfolio reassessments among equipment makers. Some utilities have already shifted specifications toward polyethersulfone and reinforced polypropylene to pre-empt compliance risks.

Ceramic tubes, although more capital intensive, are forecast to rise at a 5.69% CAGR thanks to virtually unlimited pH tolerance and lifetimes exceeding 10 years. Producers exploit economies of scale and 3D-printing methods to drive unit-cost reductions, pulling ceramics into mid-size plant bids where they were once deemed uneconomic. Polytetrafluoroethylene and expanded PTFE membranes occupy niche segments in semiconductor ultrapure washes and aggressive pharma solvents. Nanocomposite PVDF loaded with titanium-dioxide or zinc-oxide nano-fillers enhances anti-fouling characteristics, extending clean-in-place intervals. Emergent biomimetic materials embedding aquaporin proteins promise quantum leaps in flux but remain at prototype stage, leaving the mainstream tubular membrane market anchored to PVDF and ceramic chemistries for most of the outlook period.

By End-User Industry: Chemical Sector Leads Amid Pharmaceutical Growth

Chemical and petrochemical plants represented 32.10% of the tubular membrane market in 2025, reflecting entrenched use in treating solvent-laden effluents, polymerization wash waters and cooling-tower blow-down. Operators appreciate tubes’ tolerance to temperature swings and aggressive acids, traits that reduce downtime relative to thin-film configurations. The sector’s capex cycle aligns with tightening discharge permits and greenhouse-gas-driven water-reuse incentives, sustaining replacement demand.

Pharmaceutical and biotech sites, though smaller in installed capacity, are expected to log a 5.78% CAGR through 2031— the fastest among end users. Continuous manufacturing lines generate highly concentrated streams, and the need for water-for-injection quality drives adoption of tight-pore tubular ultrafiltration and nanofiltration units. Food and beverage processors deploy tubes for whey clarification and sugar deashing, leveraging hygienic welds and predictable clean-in-place protocols. Energy and power producers, especially combined-cycle gas plants, favor tubular ceramic variants for treating high-temperature cooling loops. Mining operators turn to tubes for acid mine drainage neutralization, citing robust acid-resistance and long membrane lifespans. This broadening demand foundation keeps revenue growth resilient across the tubular membrane industry.

Geography Analysis

Asia-Pacific dominated the tubular membrane market with 42.60% revenue share in 2025, buoyed by large-scale municipal rollouts in China and India’s zero-liquid-discharge mandates for bulk chemicals and textiles. China’s Yangtze River protection law pushes advanced treatment retrofits at thousands of industrial clusters, while provincial subsidies accelerate capital recovery for MBR retrofits. India’s 2025 reuse targets compel overnight adoption of integrated membrane trains that guarantee consistent permeate below 10 mg/L BOD. Japanese vendors leverage decades of Johkasou decentralized expertise to export containerized tubular packages across Southeast Asia, and South Korean pharma expansions add demand for ultrapure-water systems.

North America forms the second-largest regional bloc, underpinned by mature replacement cycles and regulatory tightening. The U.S. Infrastructure Investment and Jobs Act allocates billions for lead-service-line replacements and advanced treatment upgrades, and many utilities piggy-back these programs with MBR conversions to meet nutrient caps. Canadian provinces channel climate-resilience funds toward decentralized schemes in indigenous territories, favoring small MBRs and tubular fouling-resistant skids. Mexico’s industrial corridor along the Gulf coast embraces tubular pretreatment to minimize downstream RO fouling at its rapidly expanding petrochemical complexes.

Europe faces a pivotal material-compliance shift. PFAS curbs under REACH accelerate ceramic adoption and favor sulfone, polyetherimide and modified PP chemistries in new bids. Germany’s carbon-neutral-water initiative funds pilot hybrid membrane-ozone plants, while Iberia channels drought-mitigation money toward water-reuse schemes anchored by tubular ultrafiltration. Nordic utilities pioneer low-energy FO-MBR hybrids supported by green-hydrogen producers, illustrating how cross-sector integration underpins incremental demand in the regional tubular membrane market.

Competitive Landscape

The tubular membrane market remains moderately fragmented; the top five suppliers collectively account for roughly 40% of global installed capacity, leaving regional specialists ample room to thrive. Larger vendors emphasize turnkey project delivery, integrating process design, financing packages and long-term service agreements to lock-in annuity revenue. Veolia’s full acquisition of Water Technologies & Solutions exemplifies this strategy, delivering projected EUR 90 million cost synergies and bolstering its North American manufacturing base.

Product differentiation increasingly hinges on proprietary surface modifications that delay biofouling and on digital twins that optimize air-scour regimes in real time. DuPont’s FilmTec™ LiNE-XD elements, for example, target lithium brine pretreatment and showcase how niche, high-margin applications can defend pricing power. Meanwhile, Asian entrants engage in price-competitive bids, leveraging subsidized finance and low production overheads, particularly for stainless-steel and ceramic housings.

Strategic alliances proliferate. Memsift Innovations partnered with Murugappa Group to commercialize the GOSEP™ chemically resistant tube, combining material know-how with local fabrication and after-sales networks. Several European OEMs license aquaporin channels under co-development agreements, positioning themselves early in a potential materials shift. Consolidation is expected to continue as mid-tier firms lacking global footprints seek exit routes, heightening the importance of R&D depth and service breadth in sustaining share within the tubular membrane industry.

Tubular Membrane Industry Leaders

Kovalus Separation Solutions

Pentair

Porex

PCI Membranes

Berghof Membrane Technology GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Memsift Innovations, in collaboration with the Murugappa Group, has officially launched the GOSEP™ Ultrafiltration Membrane. This tubular membrane boasts an innovative, chemically resistant, and highly durable chemistry. Its applications span industrial wastewater treatment, resource recovery, desalination pre-treatment, and chemical separation.

- March 2024: Toray has unveiled a robust reverse osmosis (RO) tubular membrane, aimed at enhancing wastewater reuse and cutting down on frequent cleaning. Boasting double the chemical resistance of traditional membranes, this innovation promises extended lifespans and less frequent replacements. Additionally, by reducing the need for these replacements, the membrane is poised to lower carbon footprints.

Global Tubular Membrane Market Report Scope

The report on the tubular membrane market includes:

| Membrane Bioreactors (MBR) |

| Reverse Osmosis (RO) Pretreatment |

| Other Applications (Dairy CIP, Leachate, etc.) |

| Polyvinylidene Fluoride (PVDF) |

| Sulfone-based (Polyether sulfone (PES) / Polysulfone (PSU)) |

| Polytetrafluoroethylene (PTFE) / Expanded PTFE |

| Polypropylene |

| Ceramic |

| Other Membrane Materials (Polyacrylonitrile (PAN), etc.) |

| Food and Beverage |

| Chemical and Petrochemicals |

| Pharmaceutical |

| Energy and Power |

| Other Industries (Mining, Pulp and Paper, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Membrane Bioreactors (MBR) | |

| Reverse Osmosis (RO) Pretreatment | ||

| Other Applications (Dairy CIP, Leachate, etc.) | ||

| By Membrane Material | Polyvinylidene Fluoride (PVDF) | |

| Sulfone-based (Polyether sulfone (PES) / Polysulfone (PSU)) | ||

| Polytetrafluoroethylene (PTFE) / Expanded PTFE | ||

| Polypropylene | ||

| Ceramic | ||

| Other Membrane Materials (Polyacrylonitrile (PAN), etc.) | ||

| By End-user Industry | Food and Beverage | |

| Chemical and Petrochemicals | ||

| Pharmaceutical | ||

| Energy and Power | ||

| Other Industries (Mining, Pulp and Paper, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the tubular membrane market?

The tubular membrane market size stood at USD 1.5 billion in 2026.

Which application segment dominates demand?

Membrane bioreactors lead with 44.92% market share because their compact layouts meet stringent municipal effluent standards.

Why are ceramics gaining traction despite higher cost?

Ceramic tubes offer exceptional chemical resistance and decade-long lifespans, making them attractive for harsh industrial effluents facing tighter PFAS and salinity regulations.

How will PFAS legislation affect PVDF modules?

EU REACH proposals targeting PFAS may restrict PVDF use in potable-water projects after 2026, prompting utilities to consider sulfone or ceramic alternatives.

Which region is growing fastest?

Asia-Pacific commands the largest share and the highest forecast CAGR at 5.72% due to China’s industrial policies and India’s imminent zero-liquid-discharge rules.

Page last updated on: