Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

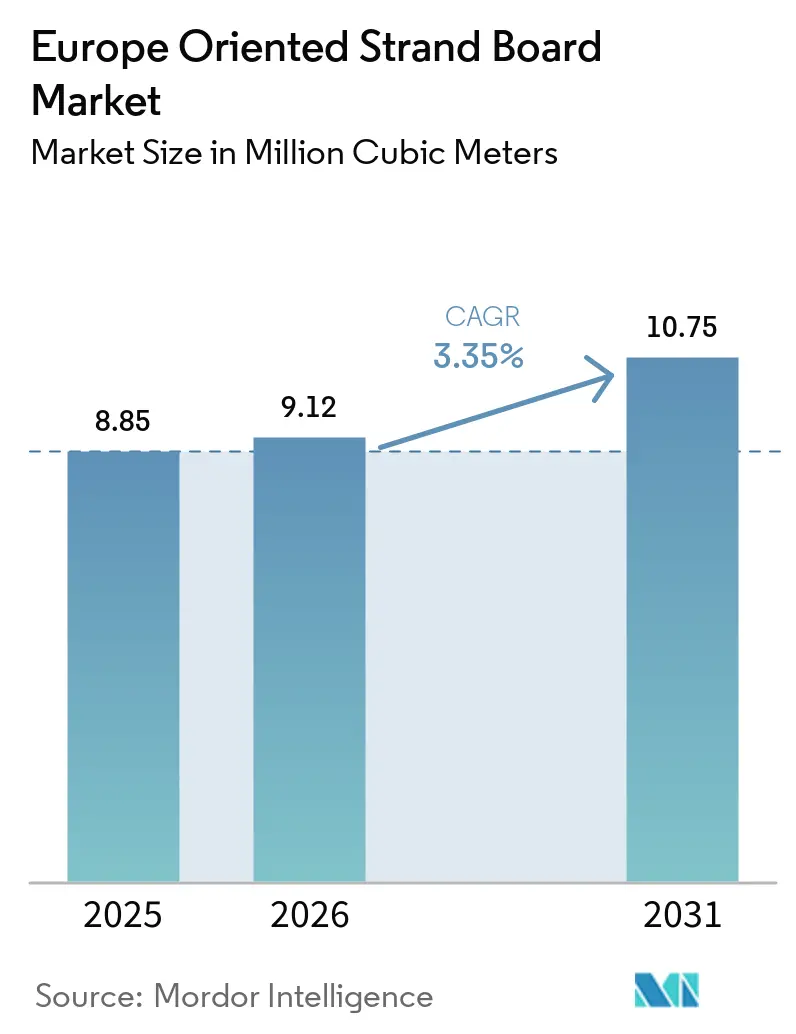

| Base Year Market Size (2025) | 8.85 Million cubic meters |

| Market Volume (2026) | 9.12 Million cubic meters |

| Market Volume (2031) | 10.75 Million cubic meters |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

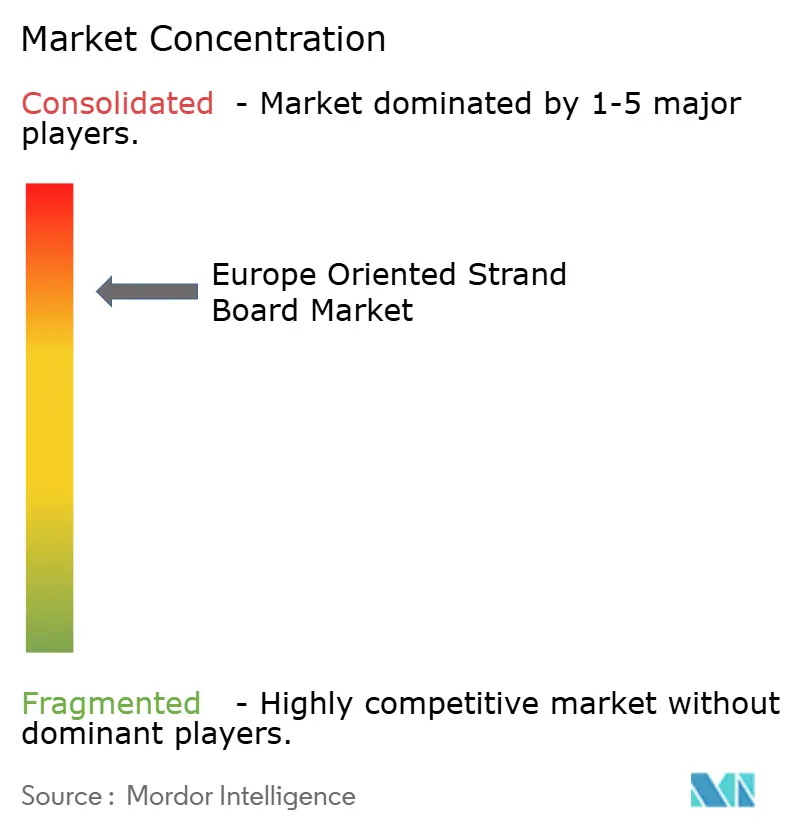

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Oriented Strand Board Market Analysis by Mordor Intelligence

The Europe Oriented Strand Board Market size is expected to increase from 8.85 million cubic meters in 2025 to 9.12 million cubic meters in 2026 and reach 10.75 million cubic meters by 2031, growing at a CAGR of 3.35% over 2026-2031. As structural demand shifts from plywood to oriented strand board - driven by multi-storey timber buildings, factory-built modules, and the REPowerEU retrofit programs - producers are gaining clearer volume insights. Mill trials reveal that Dieffenbacher's EVORIS and Hexion's SmartMDI systems can reduce unit costs. These cost reductions are significant enough to influence share allocations in price-sensitive tenders. Newly commissioned capacity in Ukraine, along with optimization projects in Germany, has not only bolstered the regional supply and spot-market liquidity but also intensified price competition among second-tier operators. Furthermore, with stricter formaldehyde caps set to take effect in August 2026, there is a rapid shift toward MDI binders. This transition is dividing the European-oriented strand board market into two distinct segments: premium low-VOC panels and commodity grades targeting less-regulated export channels.

Key Report Takeaways

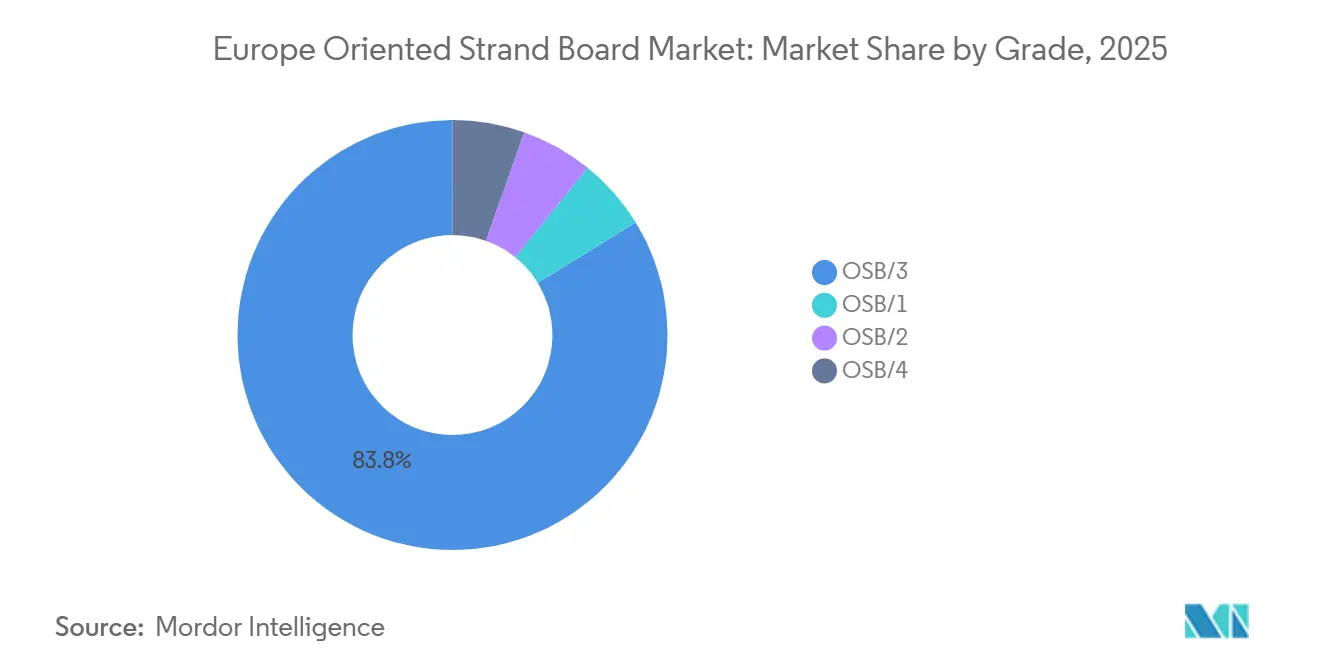

- By grade, OSB/3 captured 83.76% of the Europe-oriented strand Board market share in 2025 and is advancing at a 3.58% CAGR in the forecast period (2026-2031).

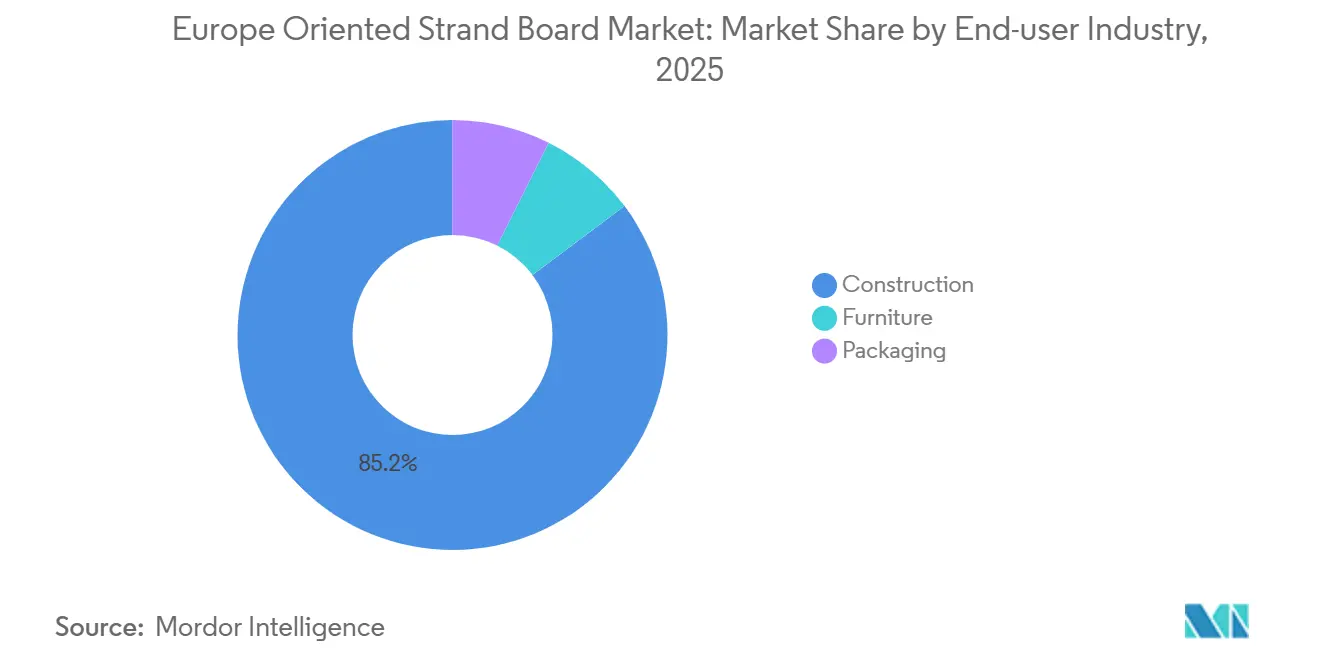

- By end-user industry, construction accounted for 85.24% of the Europe Oriented Strand Board market size in 2025 and is projected to grow at a 3.55% CAGR from 2026 to 2031.

- By geography, the Rest of Europe cluster held 75.39% of the Europe Oriented Strand Board market size in 2025, while Spain is set to record the fastest 5.06% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Oriented Strand Board Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from multi-storey timber buildings | +0.9% | Germany, Austria, Switzerland, UK, Nordics | Medium term (2-4 years) |

| REPowerEU insulation retrofits boosting OSB demand | +0.7% | Germany, France, BeNeLux, Central Europe | Short term (≤ 2 years) |

| Surge in modular off-site construction factories | +0.6% | Spain, Germany, UK, Nordics | Medium term (2-4 years) |

| Adoption of MDI-based zero-formaldehyde binders | +0.4% | Global (EU-wide regulatory alignment) | Long term (≥ 4 years) |

| AI-driven production scheduling cutting fibre loss | +0.3% | Germany, Austria, Belgium, France (large mills) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand From Multi-Storey Timber Buildings

By 2025, timber's share in Germany's single-family homes rose, and its presence in multi-family homes also expanded. This trend underscored a steady pivot toward engineered wood solutions. Developers increasingly favored OSB/3 floor diaphragms in hybrid CLT systems, valuing their racking resistance, which is comparable to plywood, at a fraction of the cost. Binderholz's Rotterdam tower showcased that fire-engineered OSB, when layered with gypsum, proved effective for taller structures[1]Binderholz, “Rotterdam Residential Tower Project,” binderholz.com. This innovation propelled the European-oriented strand board market into the realm of high-rise constructions. The UK Timber in Construction Roadmap projected a notable surge in timber adoption by 2050, a trend likely to amplify OSB demand. Additionally, Germany's federal housing budgets allocated modular timber for social housing, securing volumes in the European oriented strand board market through public procurement channels until the end of the decade.

REPowerEU Insulation Retrofits Boosting OSB Demand

By 2030, member states must renovate the bottom portion of their building stock, as mandated by the revised Energy Performance of Buildings Directive. This directive has spurred a retrofit movement, prominently featuring vapor-permeable OSB as backing boards in EIFS assemblies. In France, biosourced materials have secured a significant share of the market, with renovations playing a pivotal role in the timber turnover. Meanwhile, in Germany, underutilized insulation plants are pushing down material prices, enabling OSB-backed systems to rival traditional cement boards. Additionally, attic conversions and loft extensions are increasingly favoring OSB for its capability to span long joists. This trend highlights the deepening ties between retrofit activities and the European-oriented strand board market. As compliance with the August 2026 E0.5 formaldehyde ceiling becomes a standard tender requirement, there is a noticeable shift in demand towards MDI-bonded panels.

Surge in Modular Off-Site Construction Factories

In a strategic move, Gropyus, Nokera, Haubner, and a consortium of Spanish integrators collectively committed to automated module plants between 2025 and 2026. These factories utilize oriented strand board (OSB) for every square meter of their finished modules. Orders are directed to mills with stringent process controls, as robotic nailing lines require a precise thickness tolerance of approximately ±0.3 mm. Distributors, by negotiating annual volume contracts directly with producers, are experiencing a reduction in throughput. This shift is reshaping the supply chain dynamics in Europe's oriented strand board market. Meanwhile, smaller mills are facing margin compression, which is compelling them to either adopt forward integration or concede market share to their technologically advanced competitors.

Adoption of MDI-Based Zero-Formaldehyde Binders

In recent years, MDI resins have increasingly dominated European output. The chemistries employed not only adhere to forthcoming emissions limits but also excel within the stipulated range. On another front, SmartMDI's innovative dosing method reduces binder consumption, counterbalancing some of the costs tied to MDI raw materials. However, mills operating with older batch presses face hurdles such as plate sticking and prolonged cleaning downtimes, highlighting a technological divide in the European oriented strand board market. Reflecting these shifts, Sweden's regulatory authority has indicated the possibility of implementing a more stringent national limit.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter formaldehyde and VOC emission caps | -0.5% | EU-wide (Germany, France, Sweden, Italy national variants) | Short term (≤ 2 years) |

| Volatile softwood fibre supply in Central Europe | -0.4% | Germany, Czech Republic, Austria, Poland | Medium term (2-4 years) |

| Health concerns over indoor air quality | -0.2% | Germany, France, Nordics (high-awareness markets) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Formaldehyde And VOC Emission Caps

The Commission Regulation 2023/1464 reduced the permissible formaldehyde level to a significantly lower threshold[2]European Commission, “Regulation 2023/1464 Formaldehyde Limits,” eur-lex.europa.eu. This regulation compels PF-bonded mills to either re-engineer their production lines or pivot to unregulated exports. Furthermore, Germany’s AgBB and France’s A+ schemes impose even stricter combined VOC limits, adding complexity within the single market. Transitioning to MDI increases resin costs, while retrofitting for abatement requires significant investment, creating financial strain for cash-strapped plants. Although premium E0.5-certified boards command higher price uplifts, commodity lines that cannot secure certification risk losing out on strategic bids, hindering the growth of Europe’s oriented strand board market during the forecast period of 2026–2031.

Volatile Softwood Fibre Supply In Central Europe

In 2024, ongoing droughts and restrictions on bark-beetle salvage led to a notable decrease in spruce availability, driving log prices up from 2023 levels. During the forecast period of 2026–2031, Italian feedstock costs rose annually, posing challenges for mills lacking long-term contracts. Contamination concerns restricted the use of recycled fiber experiments to a minor fraction of the feedstock. In the Europe-oriented strand board market, cooperatives enforced take-or-pay clauses, shifting price risks onto panel makers and squeezing their margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: OSB/3 Anchors Structural Demand

Engineers favor OSB/3 for load-bearing floors, roofs, and shear walls in the European-oriented strand board market. With superior bending strength and a thickness swell of less than or equal to standard requirements, OSB/3 outperforms OSB/2. Modular factories prefer OSB/3 due to its high shear modulus, enabling thinner assemblies and reducing transport costs. OSB/3, accounting for 83.76% of the 2025 volume, is projected to grow at a 3.58% CAGR from 2026 to 2031.

OSB/4, holding a small market share, is used for crane mats and marine bulkheads, commanding a premium due to its ability to handle extreme loads. Thanks to the EVORIS process, mills can now achieve OSB/4 strength on OSB/3 lines, disrupting traditional pricing structures. Meanwhile, OSB/1 has seen a decline as furniture brands shift their focus to MDF. This evolving grade mix underscores that in the European-oriented strand board market, certification rules now play a pivotal role in determining market share splits, overshadowing strand geometry considerations.

By End-User Industry: Construction Dominates, Furniture Finds Niches

By 2025, construction accounted for 85.24% of the volume and is projected to sustain a 3.55% CAGR from 2026 to 2031, driven primarily by demand for rooftops, subfloors, and retrofit sheathing. Together, floor and roof applications constitute a significant portion of the construction tonnage, as they offer superior nail holding and in-plane shear capabilities at a more economical price than plywood. Wall sheathing, making up another substantial share, benefits from OSB's vapor rating, effectively reducing condensation-related callbacks.

Furniture, claiming a notable share of the volume, has been witnessing steady annual growth. Brands like IKEA are integrating OSB cores for enhanced screw pull-out strength, leading to a reduction in product returns. In Finland, M1-classified kitchen cabinets highlight a niche focus on low-VOC products. Industrial packaging, accounting for a smaller share, predominantly utilizes ISPM 15 crates for machinery. Such diverse applications not only cushion against market cyclicality but also expand the market size of oriented strand board in Europe, extending beyond mere construction cycles.

Geography Analysis

Poland, the Czech Republic, and several smaller European markets collectively represented 75.39% of the 2025 volume, highlighting their rich timber traditions and well-established supply clusters. In Austria, timber is used in over one-third of single-family homes. In Switzerland, fire-rated OSB approvals have expanded, allowing applications for buildings up to 12 stories. Meanwhile, Poland's cost-effective Kronospan hubs are exporting significantly to Germany and Scandinavia, expanding the oriented strand board market's reach across Europe.

Spain, starting with a modest timber share, has seen the fastest growth at a 5.06% CAGR during the forecast period of 2026–2031. As housing starts rise and factory investments intensify, OSB usage, Spain is poised to play a pivotal role in the future of Europe's oriented strand board market. Importantly, each percentage increase in timber penetration directly boosts demand, underscoring Spain's significance in the market.

Germany, a major contributor to the 2025 volume, benefited from social-housing funds backing modular timber. However, challenges such as fiber scarcity and stricter regulations have constrained its growth. The United Kingdom, with a smaller market share, grappled with challenges stemming from England's limited timber-frame adoption. However, with policies aiming at a significant number of homes, there is potential for demand to surge once broader economic challenges ease. France, holding a minor stake, saw a dip in housing starts in 2024, leading to reduced OSB orders despite the RE2020 incentives. These national variations underscore how policy choices, fiber availability, and housing dynamics shape the European-oriented strand board market.

Competitive Landscape

The Europe Oriented Strand Board market is consolidated. In Germany and the Nordic region, early movers are securing premiums from AgBB-certified, fire-rated, and ultra-light boards. Meanwhile, Switzerland's approval of 12-story OSB systems has opened a niche market. Modular integrators are strategically positioning themselves, targeting substantial annual purchases that could influence contract pricing. STEICO is pioneering OSB-insulation composites, combining structural strength with improved R-values. This innovation not only addresses the rising retrofit demand but also has the potential to reshape segmentation dynamics in the European oriented strand board market.

Europe Oriented Strand Board Industry Leaders

Kronoplus Limited

Egger

West Fraser

Sonae Arauco

SWISS KRONO Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: West Fraser announced that it would curtail operations at its High Level, Alberta, oriented strand board (OSB) mill in spring 2026 due to weak demand, reducing annual capacity by 860 million square feet (3/8-inch basis) and impacting 190 employees. The company also continued the indefinite idling of a production line in Cordele, Georgia, further reducing total capacity by approximately 1.3 billion square feet.

- December 2024: Kronospan inaugurated a EUR 200 million OSB mill in Rivne, Ukraine, adding 700,000 m³ of annual capacity and signaling renewed investor confidence in Eastern European panel production despite geopolitical headwinds.

Europe Oriented Strand Board Market Report Scope

Oriented strand board (OSB) is a strong, stiff structural wood-based panel product that possesses a cross-oriented pattern like plywood. OSB is characterized by its constituent strand elements, which vary in size and aspect ratio.

The oriented strand board (OSB) market is segmented by grade, end-user industry, and geography. By grade, the market is segmented into OSB/1, OSB/2, OSB/3, and OSB/4. By end-user industry, the market is segmented into furniture, construction, and packaging. The report also covers the market size and forecasts for the market in 7 countries across the region. For each segment, the market sizing and forecasts are done based on volume (Cubic Meters).

By Grade

| OSB/1 |

| OSB/2 |

| OSB/3 |

| OSB/4 |

By End-user Industry

| Furniture | Residential |

| Commercial | |

| Construction | Floor and Roof |

| Wall | |

| Door | |

| Column and Beam | |

| Staircase | |

| Other Constructions | |

| Packaging | Food and Beverage |

| Industrial | |

| Pharmaceutical | |

| Cosmetics | |

| Other Packaging |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Switzerland |

| Austria |

| Rest of Europe |

| By Grade | OSB/1 | |

| OSB/2 | ||

| OSB/3 | ||

| OSB/4 | ||

| By End-user Industry | Furniture | Residential |

| Commercial | ||

| Construction | Floor and Roof | |

| Wall | ||

| Door | ||

| Column and Beam | ||

| Staircase | ||

| Other Constructions | ||

| Packaging | Food and Beverage | |

| Industrial | ||

| Pharmaceutical | ||

| Cosmetics | ||

| Other Packaging | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Switzerland | ||

| Austria | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large will European-oriented strand board demand be in 2031?

The Europe Oriented Strand Board Market size is expected to increase from 8.85 million cubic meters in 2025 to 9.12 million cubic meters in 2026 and reach 10.75 million cubic meters by 2031, growing at a CAGR of 3.35% over 2026-2031.

Which European country is growing oriented strand board usage the fastest?

Spain shows the highest projected CAGR at 5.06% through 2031, thanks to a rapid shift toward factory-built timber housing.

Why is OSB/3 the dominant grade in Europe?

OSB/3 meets EN 300 structural benchmarks while offering moisture resistance and price advantages over plywood, securing 83.76% of 2025 volume.

Are modular factories reshaping OSB supply chains?

Yes, large integrators now negotiate annual contracts directly with mills, bypassing distributors and concentrating purchasing power among fewer buyers.

Page last updated on: