Sandwich Panels Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 16.52 Billion |

| Market Size (2031) | USD 21.21 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

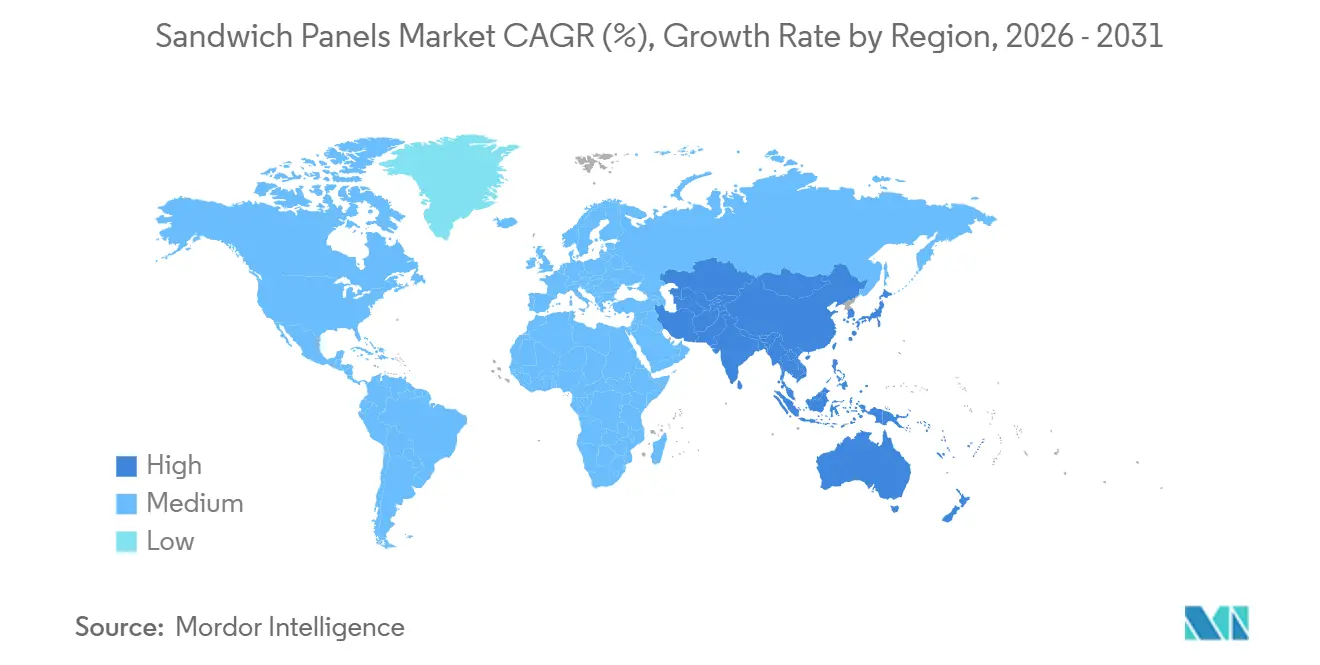

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sandwich Panels Market Analysis by Mordor Intelligence

The Sandwich Panels Market size is projected to be USD 15.72 billion in 2025, USD 16.52 billion in 2026, and reach USD 21.21 billion by 2031, growing at a CAGR of 5.12% from 2026 to 2031. The growth reflects a shift in procurement priorities as owners seek fast occupancy and long-term energy savings, which favors prefabricated envelopes that combine structure, insulation, and finish in one lift. Polyurethane cores continue to dominate because their price-performance ratio is attractive for large industrial buildings, yet fire-safety mandates are steering high-occupancy projects toward mineral wool. Aluminum skins remain the leading facing material, while continuous fiber-reinforced thermoplastics (CFRT) are gaining share thanks to lower embodied carbon and end-of-life recyclability. Continuous production lines strengthen cost leadership by cutting scrap and maintaining tight thickness tolerances that appeal to curtain-wall contractors. Rapid cold-chain expansion and hyperscale data-center construction are the most visible demand spikes, each requiring envelope R-values that few alternatives can match at comparable installed cost.

Key Report Takeaways

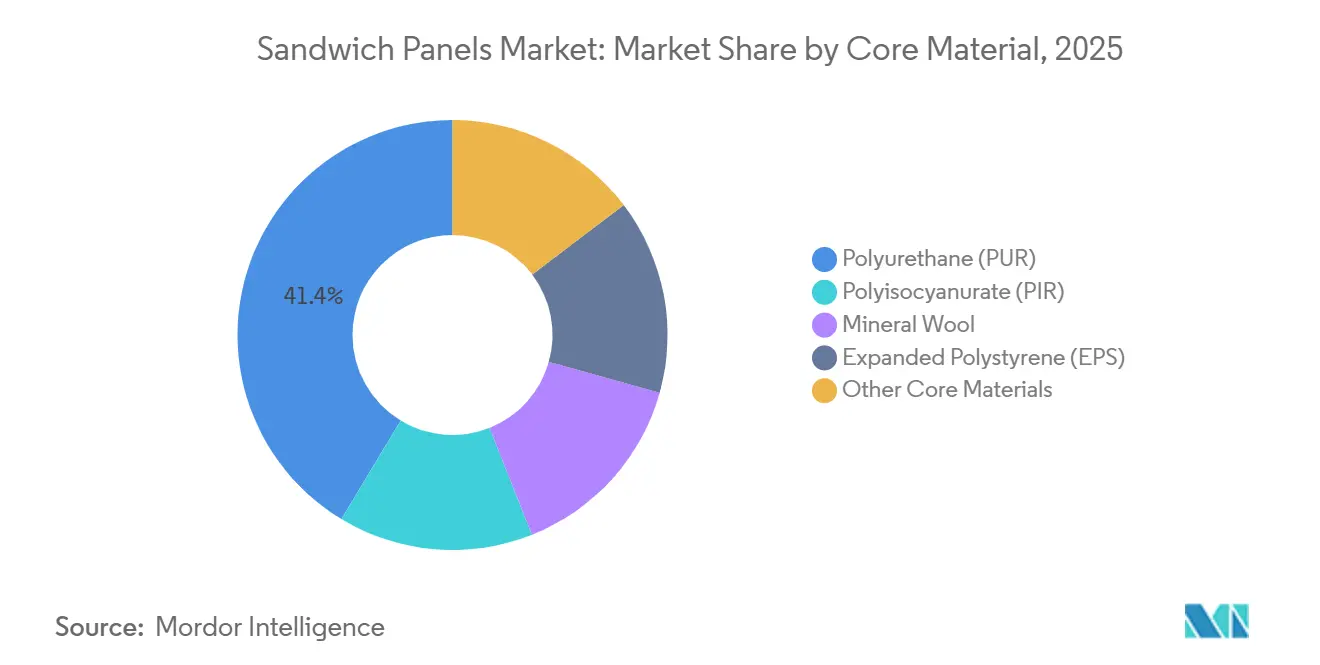

- By core material, polyurethane (PUR) led with 41.36% revenue share in 2025, and also posted the fastest CAGR at 5.38% through 2031.

- By skin material, aluminum maintained 45.31% of the sandwich panels market share in 2025, whereas continuous fiber reinforced thermoplastics (CFRT) recorded the highest projected CAGR at 5.27% to 2031.

- By technology, continuous manufacturing accounted for 75.12% of the sandwich panels market size in 2025 and is advancing at a 5.15% CAGR to 2031.

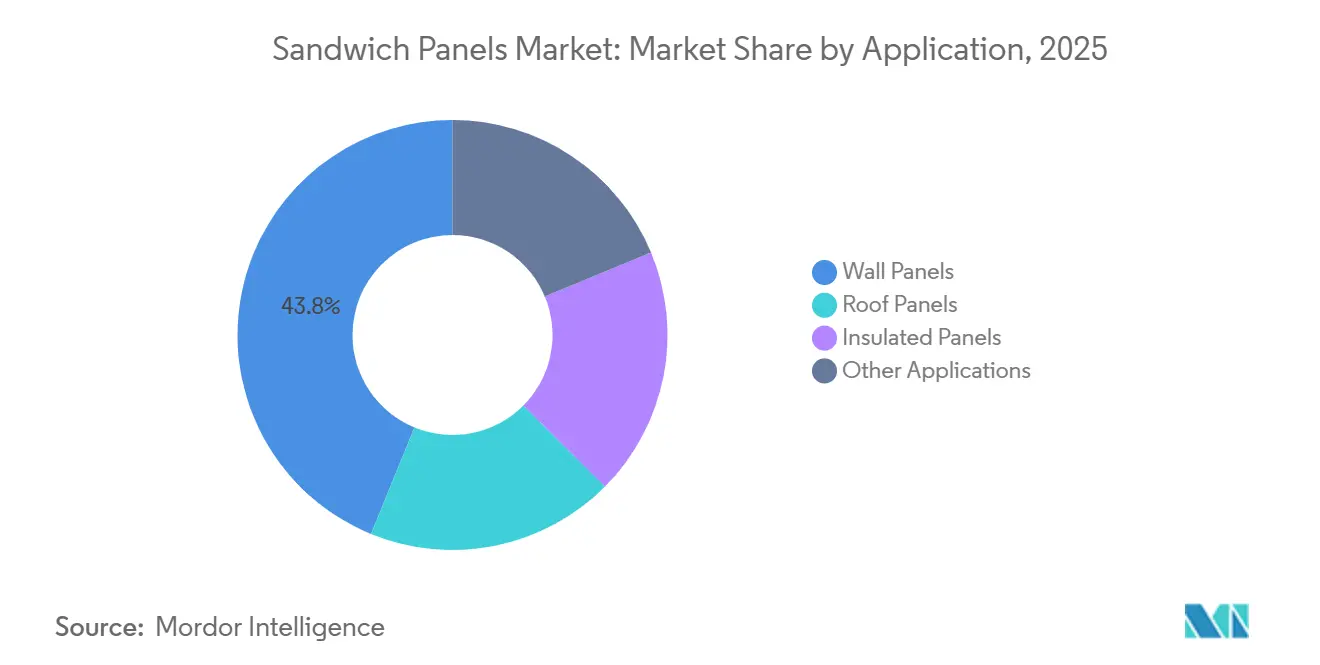

- By application, wall panels represented a 43.82% share in 2025, while insulated panels are projected to expand at a 5.69% CAGR to 2031.

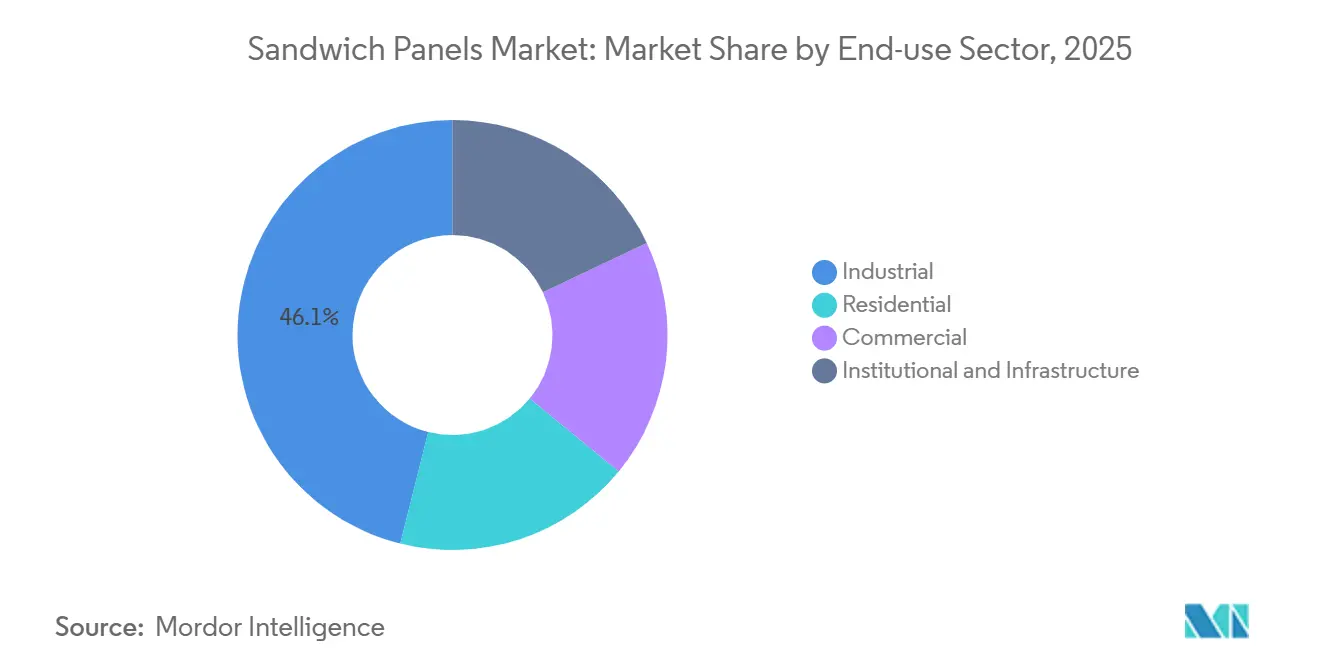

- By end-use sector, industrial buildings held 46.10% of the sandwich panels market size in 2025, and this category is growing at a 5.33% CAGR through 2031.

- By geography, Asia-Pacific held 49.90% of the market in the year 2025, and is growing at a CAGR of 5.81%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sandwich Panels Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for PVDF-based aluminum composite panels | +0.8% | Global, with concentration in Asia-Pacific high-rise markets and Middle East façade projects | Medium term (2-4 years) |

| Rapid growth of prefabricated and modular construction | +1.2% | Asia-Pacific core, North America industrial, Europe residential retrofit | Medium term (2-4 years) |

| Energy-efficiency regulations for building envelopes | +1.0% | Europe (EU Energy Performance of Buildings Directive), North America (IECC updates), emerging in Asia-Pacific | Long term (≥4 years) |

| Data-center boom requiring high-performance envelopes | +0.9% | North America hyperscale hubs, Europe (Ireland, Netherlands), Asia-Pacific (Singapore, India) | Short term (≤2 years) |

| Green-hydrogen gigafactories driving demand for climate-controlled production halls | +0.7% | Europe (Germany, Spain, Nordic), early adoption in Middle East and Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for PVDF-Based Aluminum Composite Panels

Designers benefit from PVDF coatings, which promise long-term color retention and enable a reduction in cladding weight, subsequently lessening seismic loads in towering structures. In Jakarta and Manila, developers achieved a reduction in structural steel by opting for PVDF-clad sandwich panels over precast concrete, all while meeting wind-load standards. Meanwhile, in the Gulf, a high solar-reflectance index for PVDF translates to cooling bill savings during peak heat. Marine locations value the resin's resistance to salt spray, boosting façade lifespans and enhancing net present value for property owners. Due to resin shortages causing a price surge for PVDF, architects now reserve its use for sunlit façades, opting for more affordable finishes on shaded sides, a strategy that maintains thermal advantages at a reduced initial expense.

Rapid Growth of Prefabricated and Modular Construction

Volumetric units, when factory-assembled, can reduce schedules and offer cost savings compared to traditional stick-built methods. Additionally, the use of modular components reduces site waste, a move that resonates well with ESG scorecards[1]Talent Traction, "2025, Outlook: The Rise of Modular Construction," talenttraction.org. Prefabrication is expected to grow significantly by 2026, driven primarily by labor shortages that have heightened the value of factory work. Sandwich panels, achieving tight tolerances, eliminate the need for on-site shimming and ensure air leakage remains below Passive House limits. Thanks to incentive schemes in India, modular factories are increasingly opting for R-30 cores tailored for cleanroom spaces. In China, developers are incentivized with floor-area bonuses to push beyond 50% prefabrication, leading to a surge in demand for sandwich panels, especially in tier-2 cities. With cycle times reduced, owners of data centers and cold storage facilities can sidestep revenue losses from scheduling delays, even when sandwich panels come at a premium over basic cladding.

Energy-Efficiency Regulations for Building Envelopes

By 2028, the EU mandates zero-emission standards for public assets and extends this requirement to all new structures by 2030, driving up the demand for ultra-low-U-value panels[2]European Parliament, Directive (EU) 2024/1275, eur-lex.europa.eu. By 2028, the EU's updated Energy Performance Directive mandates that new non-residential buildings achieve U-values below 0.18 W/m²·K. Notably, 150 mm PIR sandwich panels can meet this requirement without the need for additional layers. In the U.S., jurisdictions implementing the 2024 IECC have increased minimum insulation standards, nudging developers towards opting for thicker panels and hybrid PIR-vacuum solutions. Meanwhile, South Korea has set a carbon-intensity limit for 2025, incentivizing the use of panels with recycled cores. In California, updates to Title 24 now require parametric thermal modeling for larger envelopes. Here, sandwich panels offer an edge in compliance, as their factory-controlled density remains consistent within a ±3% range. Producers operating on a continuous line stand to gain the most, given that their uniform density accelerates the process of third-party certification.

Data-Center Boom Requiring High-Performance Envelopes

In 2026, hyperscale facilities are operational. These facilities maintain server temperatures between 18 °C and 27 °C, even in climates ranging from −20 °C to 45 °C. Utilizing mineral-wool cores, these facilities achieve a 2-hour fire rating without the need for intumescent coatings, resulting in savings on insurance premiums. In 2025, Northern Virginia and Dublin contributed new floor area, with a significant portion opting for 200 mm panels to comply with ASHRAE 90.4 and secure utility rebates. Operators are increasingly opting for vapor-permeable interior skins, which, while adding an extra cost, mitigate mold risks during rapid load ramps. In India, driven by new subsidies, data-center projects have specified panels, aiming for a Power Usage Effectiveness (PUE) below 1.3.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oriented-strand-board VOC emissions | -0.4% | North America (CARB Phase 2 states), Europe (EU VOC limits), emerging in Asia-Pacific | Short term (≤2 years) |

| Moisture ingress and long-term degradation in PUR/PIR cores | -0.6% | Global, with acute impact in high-humidity coastal zones and tropical climates | Medium term (2-4 years) |

| Volatility in MDI, steel and aluminum prices squeezing panel margins | -0.9% | Global, with highest exposure in non-integrated fabricators across all regions | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Oriented-Strand-Board VOC Emissions

In 2025, OSB bonded with urea-formaldehyde neared CARB Phase 2's formaldehyde limit. This led to a shift towards phenolic or zero-VOC adhesives, increasing panel costs. The EU has set a stricter indoor formaldehyde cap. This effectively sidelines conventional OSB in the EU unless manufacturers undertake a reformulation and recertification process, which can extend up to 18 months. In North America, producers tackled the emissions challenge by substituting urea resins with MDI binders. However, this switch resulted in a hike in raw material costs, putting pressure on gross margins. South Korea, implementing real-time VOC monitoring and imposing hefty fines, has hastened the transition to low-emission cores. Meanwhile, Southeast Asian fabricators, primarily export-oriented, encounter fresh hurdles as multinational developers enforce CARB standards on a global scale.

Moisture Ingress and Long-Term Degradation in PUR/PIR Cores

Moisture seeping through seam imperfections can diminish R-value over time. In humid coastal areas, this degradation can escalate to a loss in compressive strength. Buyers seeking a long service life often shy away from PUR/PIR. This hesitation stems from the fact that most warranties, capping at a limited period, notably exclude moisture-related failures. Remediation expenses can sometimes surpass the initial panel budgets. In response to these concerns, European insurers have raised premiums for PUR/PIR buildings situated in flood-prone zones, subtly steering projects towards mineral wool. While hybrid cores, which feature PIR sandwiched between mineral wool layers, come at an added cost, they offer a significant advantage: extending warranties. This extension alleviates concerns for both lenders and insurers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Core Material: Polyurethane Continues to Lead While Mineral Wool Gains

Polyurethane delivered 41.36% of 2025 revenue and is forecast to expand at 5.38%, illustrating how the sandwich panels market balances performance with first cost. PUR’s lower mass helps brownfield warehouses avoid expensive foundation upgrades, and its thermal efficiency keeps panel thickness to 100 mm or less in moderate climates, saving interior space. Polyisocyanurate enjoys a better R-value per inch and resists rooftop temperatures, making it popular in the Middle-East, where roof surfaces reach high temperatures. Code changes after high-profile façade fires push schools and hospitals toward mineral wool even when budgets are tight.

Mineral-wool cores are expanding due to their A1 fire rating and acoustic attenuation. The sandwich panels market size for mineral wool in data centers and production halls is rising as insurers tighten rules around combustible cores. EPS remains critical for farm buildings because the price premium of PUR cannot be recovered in low-margin agriculture. Niche materials such as phenolic foam and vacuum-insulated panels suggest slow but steady penetration where extremely low smoke or extraordinary R-values are mandatory.

By Skin Material: Aluminum Dominates, CFRT Accelerates

In 2025, aluminum commanded a 45.31% market share, lauded for its corrosion resistance, workability, and lightweight nature. Steel, favored for cost-sensitive applications like sheds and barns, also held a notable share. While CFRT accounted for a modest portion of the 2025 revenue, it boasted a 5.27% CAGR, the market's fastest growth rate. This surge is attributed to lifecycle assessments highlighting CFRT's lower embodied carbon compared to aluminum. Even with a higher price tag than coated steel, clients pursuing net-zero certifications are increasingly opting for CFRT.

Fiberglass skins play a crucial role in the food and pharmaceutical sectors, where their non-porous surface simplifies sanitation. Meanwhile, exotic metals like copper and zinc cater to luxury façades and environments with extreme chemical exposure due to their heightened corrosion resistance. With the updated EU CSRD mandating Scope 3 disclosures starting in 2025, developers are turning to CFRT to potentially slash reported emissions. This strategic move is anticipated to dent aluminum's market share in the coming years.

By Technology: Continuous Lines Sustain Cost Advantage

Continuous lines produced 75.12% of global volume in 2025 and will grow at 5.15%. These lines, equipped with double-belt laminators, achieve speeds of 8-12 meters per minute while maintaining a density variation of less than ±3%. This precision is a challenging feat for batch presses. Given that a complete line comes with a high price tag, the cost creates significant barriers to entry. As a result, capacity is concentrated among leading global players, bolstering economies of scale in the sandwich panels market.

Discontinuous presses play a crucial role in crafting curved stadium roofs and terminal façades, where customized geometries are paramount. Their success is attributed to flexible tool changes, allowing small fabricators to switch between PUR, EPS, and mineral wool in just half a day. Meanwhile, emerging hybrid lines are making waves by merging continuous foaming with batch profiling. This innovation enables them to handle bespoke orders without sacrificing throughput, and they have already secured a notable share of the new capacity announced in 2025.

By Application: Wall Panels Hold Lead, Insulated Panels Grow Fast

In 2025, wall panels accounted for 43.82% of total revenue, serving as both the structural backbone and enclosure for expansive warehouses. While they offer essential bracing and can reduce onsite frame erection time, their growth rate is beginning to plateau in more established markets. Roof panels, on the other hand, secured a notable market share, experiencing steady growth. This uptick is largely attributed to snow-belt owners opting for upgraded cores, achieving improved thermal ratings, and realizing reductions in heating fuel costs.

Insulated panels, encompassing both walls and roofs with enhanced thermal breaks, are witnessing a 5.69% CAGR. The demand for sandwich panels in insulated boxes is on the rise, driven by stringent pharmaceutical GDP standards. These standards mandate cold storage facilities to maintain temperatures between 2 °C and 8 °C, all while minimizing energy loss. Lastly, partition walls and doors contribute the remaining share to the revenue pie, growing steadily. This growth is fueled by modular builders' appreciation for factory-cut service penetrations, which expedite the MEP fit-out process.

By End-Use Sector: Industrial Leads and Accelerates

Industrial users held 46.10% of the 2025 demand and are expanding at 5.33%. The construction of gigafactories for batteries, green hydrogen, and semiconductors is driving a surge in demand for high bay cleanrooms, where ISO Class 6 particulate control is a must. Sandwich panels, featuring stainless skins and mineral-wool cores, not only meet essential fire and hygiene standards but can also be installed faster than traditional masonry.

Commercial buildings contributed notably to the revenue, growing consistently. This growth is largely attributed to landlords retrofitting offices to attract tenants willing to pay a premium for LEED Gold certifications. The residential sector is witnessing steady growth. Notably, modular schemes in Scandinavia and Japan are utilizing panels to reduce costs while adhering to stringent airtightness regulations. Meanwhile, the institutional and infrastructure sectors are expanding steadily. This growth is fueled by the establishment of vaccine-storage hubs post-pandemic, which are required to meet the WHO PQS cold-chain standards.

Geography Analysis

Asia-Pacific delivered 49.90% of global revenue in 2025 and will climb at a 5.81% CAGR. This growth is largely driven by China's goal to prefabricate a portion of its new constructions by 2030 and India's push for electronics factories. In 2025, a notable percentage of the new industrial floor area in Chinese provinces utilized sandwich panels, indicating swift policy adoption. India constructed a substantial amount of Grade A warehouses in 2025, with a significant portion featuring insulated boxes that align with Global Cold Chain Alliance standards. Japan and South Korea made up a considerable share of the region's revenue, while aging workforces in these nations are pushing for more labor-saving solutions. Southeast Asia experienced growth as manufacturers shifted operations from China, though ASEAN's import tariffs on steel and aluminum have extended lead times.

North America accounted for a notable share of global sales in 2025, with steady growth. U.S. e-commerce warehouses expanded significantly, and a considerable percentage of high bay facilities over a certain size opted for panels in their construction. In Canada, a stricter code in 2025 has hastened the adoption of these panels in prairie cold rooms. Mexico's growth can be attributed to USMCA regulations promoting nearshoring, with new automotive plants opting for LEED-eligible designs.

Europe, contributing a significant share to global sales, is on a steady rise. Volatility in natural gas prices has led factories to retrofit with thicker panels, achieving a notable reduction in heating loads. Germany and Poland, bolstered by battery cell plants currently under construction, cater to a considerable portion of Europe's demand. The Nordic states, witnessing growth, are seeing a surge in hydrogen projects that necessitate airtightness due to extreme cold.

South America, with a notable share of global revenue, is growing steadily. Brazil established numerous cold storage facilities for protein exports, with a significant portion utilizing 180 mm PIR cores. Meanwhile, Argentina's mining surge is prompting rapid constructions that prioritize quick-install envelopes. The Middle-East and Africa, holding a notable share, are experiencing significant growth, spearheaded by Saudi NEOM and the UAE's industrial zones, both aiming for LEED Gold standards in arid conditions.

Mordor Intelligence provides coverage of the sandwich panels market across other key regional markets. Detailed country-level analysis extends to Morocco incorporating local coverage and market participation, as required.

Competitive Landscape

The global sandwich panels market is fragmented. Regional fabricators, adept at custom profiling, are capitalizing on short lead times. Some are crafting niche cores, such as soy-based PUR that reduces embodied carbon. These eco-conscious offerings attract architects, who are willing to pay a premium for the sustainability branding. In 2025, patent filings spotlighted hybrid mineral-wool-plus-PIR cores. These innovations achieve the A2 fire class while maintaining high R-values, effectively addressing the age-old dilemma of combustibility versus performance. With Industry 4.0 enhancements, including inline density sensors and predictive maintenance, defect rates have significantly decreased. This achievement is something smaller shops can only replicate through labor-intensive inspections. There's a burgeoning opportunity in re-cladding. As aging sheds seek lightweight overlays to comply with new energy codes, they can do so without the need for structural reinforcement. Broad Sustainable Building, a vertically integrated modular builder, is moving backward into panel production. This strategy not only helps them capture the envelope margin but also ensures dimensional compatibility, further propelling consolidation in the sandwich panels market.

Sandwich Panels Industry Leaders

-

Kingspan Group

-

Metecno Group

-

ArcelorMittal

-

Tata Steel

-

Assan Panel A.S.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: EPACK Prefab inaugurated an 800,000 m²-per-year sandwich panel plant in Mambattu, India, to meet rising demand for prefabricated cold-chain and industrial facilities.

- October 2024: ArcelorMittal and Kingspan | Invespanel released a high-recycled-content sandwich panel range using XCarb steel with at least 75% scrap input and 100% renewable electricity, achieving 60% carbon-emission reduction.

Global Sandwich Panels Market Report Scope

A sandwich panel consists of a core/insulating material of low density sandwiched between two layers of metal bonded under pressure.

The market is segmented by core material, skin material, technology, application, end-use sector, and geography. By core material, the market is segmented into polyurethane (PUR), polyisocyanurate (PIR), mineral wool, expanded polystyrene (EPS), and other core materials. By skin material, the market is segmented into continuous fiber reinforced thermoplastics (CFRT), fiberglass reinforced panel (FRP), aluminum, steel, and other skin materials. By technology, the market is segmented into continuous and discontinuous. By application, the market is segmented into wall panels, roof panels, insulated panels, and other applications. By end-use sector, the market is segmented into residential, commercial, industrial, and institutional and infrastructure. By geography, the market is segmented accordingly. The report also covers the market size and forecasts for the structural insulated panels market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD).

| Polyurethane (PUR) |

| Polyisocyanurate (PIR) |

| Mineral Wool |

| Expanded Polystyrene (EPS) |

| Other Core Materials |

| Continuous Fiber Reinforced Thermoplastics (CFRT) |

| Fiberglass Reinforced Panel (FRP) |

| Aluminum |

| Steel |

| Other Skin Materials |

| Continuous |

| Discontinuous |

| Wall Panels |

| Roof Panels |

| Insulated Panels |

| Other Applications |

| Residential |

| Commercial |

| Industrial |

| Institutional and Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| NORDIC Countries | |

| Hungary | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Core Material | Polyurethane (PUR) | |

| Polyisocyanurate (PIR) | ||

| Mineral Wool | ||

| Expanded Polystyrene (EPS) | ||

| Other Core Materials | ||

| By Skin Material | Continuous Fiber Reinforced Thermoplastics (CFRT) | |

| Fiberglass Reinforced Panel (FRP) | ||

| Aluminum | ||

| Steel | ||

| Other Skin Materials | ||

| By Technology | Continuous | |

| Discontinuous | ||

| By Application | Wall Panels | |

| Roof Panels | ||

| Insulated Panels | ||

| Other Applications | ||

| By End-use Sector | Residential | |

| Commercial | ||

| Industrial | ||

| Institutional and Infrastructure | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| NORDIC Countries | ||

| Hungary | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for the sandwich panels market between 2026 and 2031?

The market is projected to grow at a 5.12% CAGR during the 2026-2031 period, growing from USD 16.52 billion to USD 21.21 billion.

Which region shows the fastest growth through 2031?

Asia-Pacific leads with a 5.81% CAGR, driven by prefabrication mandates and industrial expansion.

Why are mineral-wool cores gaining share?

They carry an A1 fire rating that meets stricter codes for high-occupancy buildings.

How do continuous lines outperform discontinuous lines?

Continuous production achieves higher speeds, lower scrap, and tighter thickness tolerances, cutting unit cost.

What application segment is growing fastest?

Insulated panels for cold-storage and data-center envelopes are advancing at a 5.69% CAGR.

Page last updated on: