Media Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.99 Billion |

| Market Size (2031) | USD 10.09 Billion |

| Growth Rate (2026 - 2031) | 10.99% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

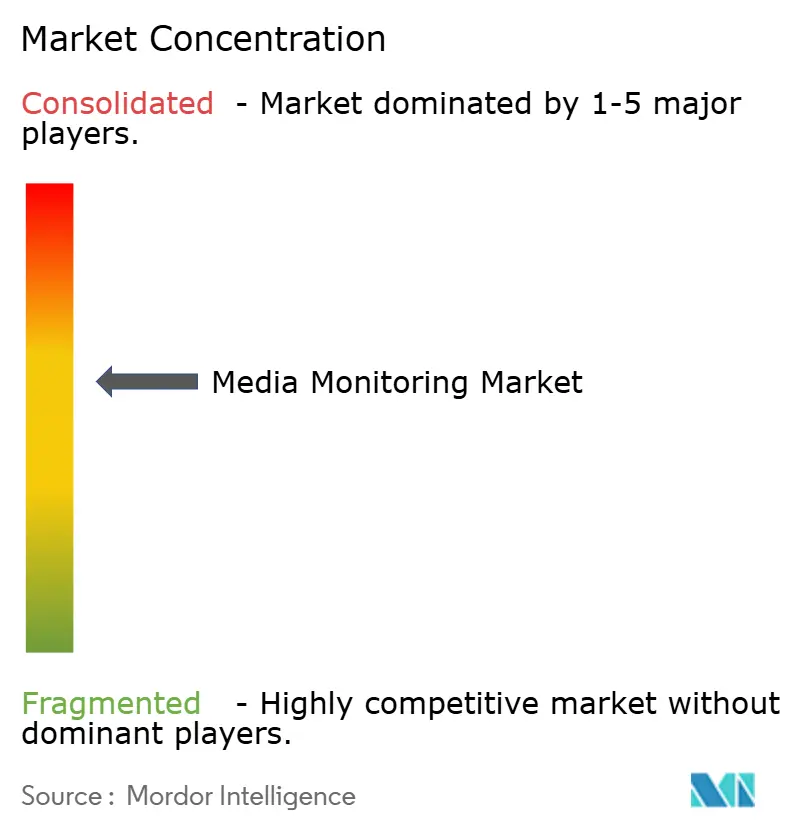

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Media Monitoring Market Analysis by Mordor Intelligence

The media monitoring market size was valued at USD 5.40 billion in 2025 and estimated to grow from USD 5.99 billion in 2026 to reach USD 10.09 billion by 2031, at a CAGR of 10.99% during the forecast period (2026-2031). This strong momentum reflects enterprises’ accelerating need to manage reputation in real-time, comply with mandatory ESG-disclosure rules, and turn vast digital conversations into strategic intelligence. Demand also rises as GenAI delivers multilingual analytics with measurable returns, while podcast and other audio formats become mainstream channels that must be tracked alongside social, news, and broadcast sources. Enterprises view integrated monitoring suites as essential to reduce blind spots, maintain regulatory readiness, and detect narrative threats before they crystallize. Cloud-native architectures, AI-driven data enrichment, and intuitive visual dashboards now define table-stakes capabilities across the media monitoring market.

Key Report Takeaways

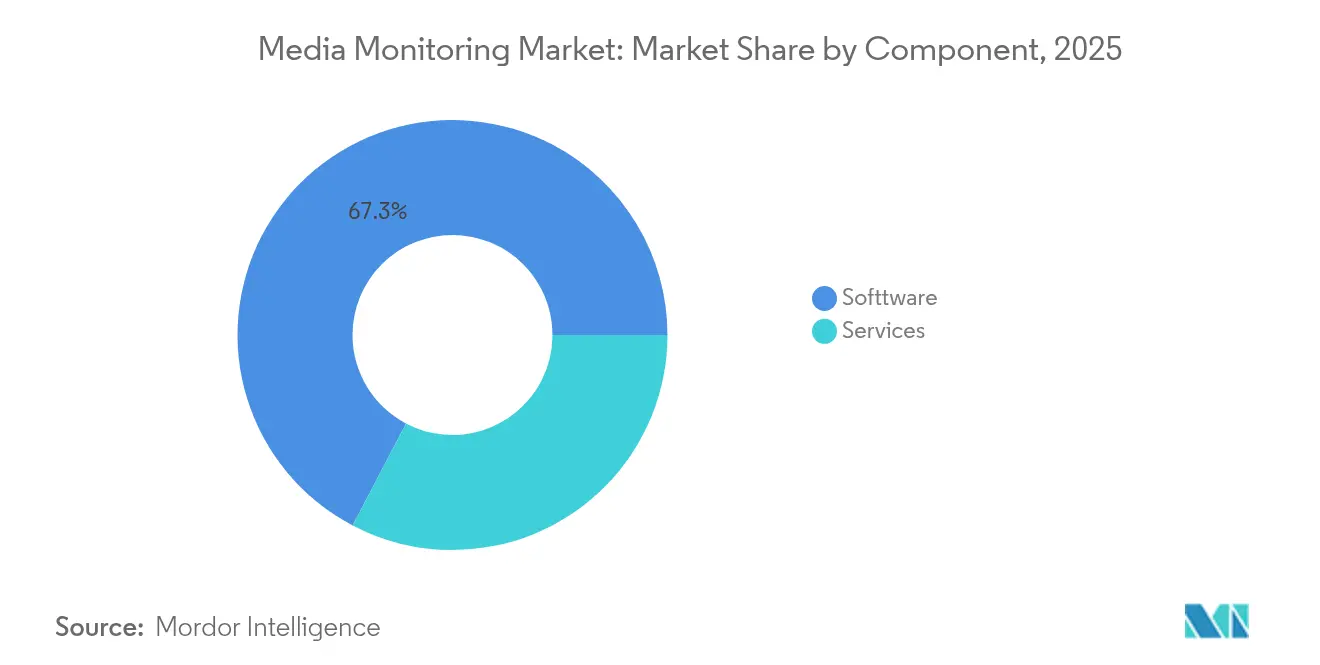

- By component, software platforms captured 67.31% media monitoring market share in 2025; professional services post the fastest expansion at a 12.96% CAGR through 2031.

- By deployment, cloud models commanded 69.85% of the media monitoring market size in 2025 and are forecast to grow at 15.55% CAGR, well ahead of on-premise alternatives.

- By enterprise size, large organizations held 57.92% of media monitoring market share in 2025, while the SME bracket is advancing at 14.63% CAGR to 2031.

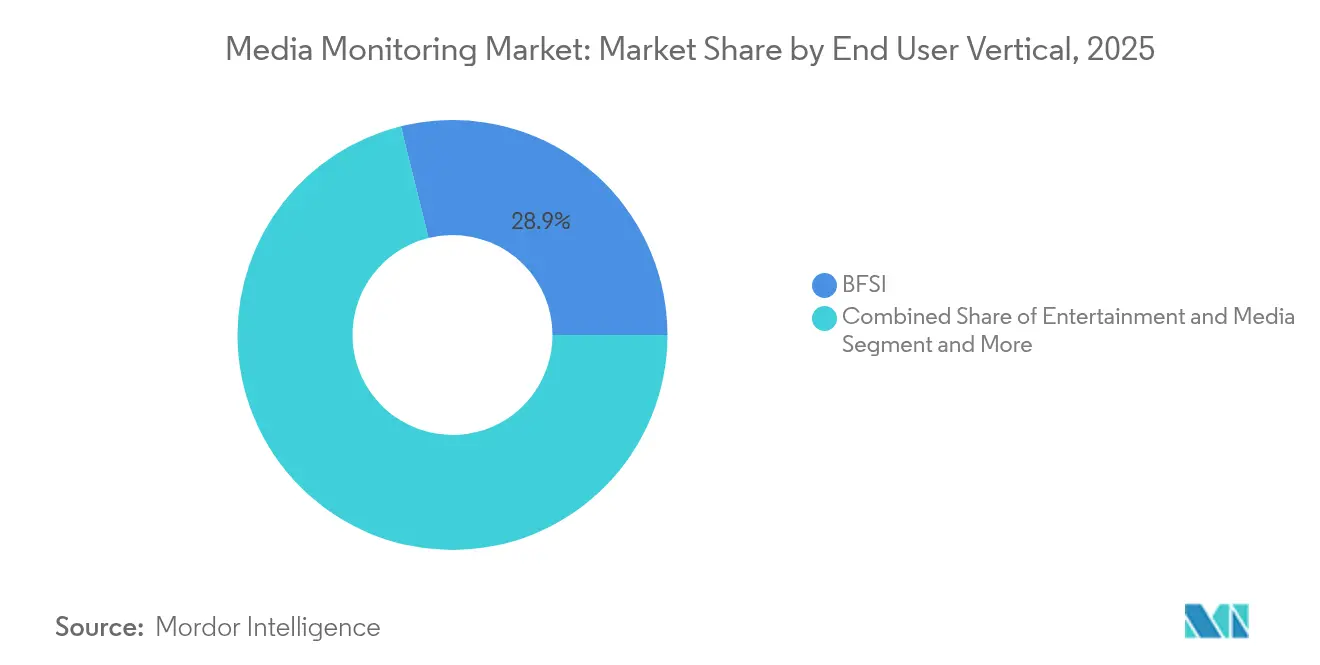

- By end-user vertical, the BFSI segment led with 28.86% revenue share in 2025; healthcare is predicted to post the highest 13.95% CAGR through 2031.

- By media channel monitored, broadcast retained 40.92% of coverage in 2025; online news and blogs represent the quickest-rising channel at a 12.56% CAGR.

- By geography, North America dominated with 37.44% of the 2025 media monitoring market size; APAC is forecast to register a vigorous 17.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Media Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing digital media consumption | +2.8% | Global, led by Asia-Pacific | Medium term (2-4 years) |

| Sales- and marketing-team adoption surge | +2.1% | North America and EU | Short term (≤ 2 years) |

| Real-time reputation and crisis demands | +1.9% | Global, BFSI hubs | Short term (≤ 2 years) |

| GenAI-enabled multilingual analytics ROI | +2.4% | Global, early tech adopters | Medium term (2-4 years) |

| Podcast and audio monitoring emergence | +1.3% | North America, expanding Asia-Pacific | Long term (≥ 4 years) |

| Mandatory ESG-disclosure media tracking | +1.6% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Digital Media Consumption

Digital channels accounted for nearly two-thirds of total United States media spending in the first eight months of 2024, hitting USD 107 billion and intensifying the volume and diversity of content that brands must parse. Over 60% of internet users now engage with podcasts each month, creating a rich stream of unstructured audio that requires specialized monitoring workflows. Enterprises realise fragmented monitoring yields incomplete reputation pictures; consequently, integrated suites that ingest social, news, broadcast, and audio in one pipeline see rising adoption. Marketing teams emphasise AI-driven filtering and sentiment scoring to distil meaning from exponential data inflows. Across APAC, surging mobile usage amplifies this data deluge, positioning scalable cloud platforms as the backbone of effective monitoring strategies.

GenAI-Enabled Multilingual Analytics ROI

Microsoft reported a 3.7-fold return on GenAI deployments, proving tangible value that encourages wider application inside the media monitoring market.[1]Microsoft Research, “AI ROI Benchmarking Study 2024,” microsoft.com Global GenAI spending is set to jump 50% in 2025, with 72% of media companies already quantifying returns from automated categorisation and real-time threat detection. Media Track raised transcription accuracy by 20 percentage points across 20+ languages using advanced speech-to-text models, cutting operational costs and boosting insight reliability. These breakthroughs turn monitoring from reactive alerting to proactive intelligence that anticipates sentiment swings, especially for multinational brands operating across divergent cultures and languages. Vendors that bundle GenAI inside intuitive dashboards shorten time-to-value and win enterprise preference.

Real-Time Reputation and Crisis Demands

Roughly 25% of a public company’s market value is linked directly to corporate reputation, making rapid detection of adverse narratives mission-critical.[2]AYLIEN, “The Value of Real-Time Adverse Media Intelligence,” aylien.com Deutsche Telekom illustrates this priority: its social-data intelligence layer flags potential crises and channels alerts to communications teams within minutes. Within BFSI, adverse-media screening solutions reduce false positives by 75% and lift analyst efficiency 35%, enabling compliance units to focus on genuine threats. Such examples underline why organisations now insist on sub-second data collection, AI-driven context maps, and workflow integrations that accelerate response. The media monitoring market therefore rewards providers that couple exhaustive coverage with actionable, role-specific alerts.

Podcast and Audio Monitoring Emergence

India’s position as the third-largest podcast market and the existence of 1.7 billion monthly listeners worldwide magnify the imperative to capture audio-first conversations. Streaming audio generates USD 3.22 in return for every dollar invested, five times what linear TV achieves, making it a critical metric in media-mix modelling. AI transcription paired with sentiment engines now lets brands mine podcasts at scale and stitch insights across channels. Vendors that seamlessly fold audio into existing dashboards gain share as clients migrate away from manual sampling and fragmented point tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of enterprise-grade suites | -1.8% | Global, acute in SME segments | Short term (≤ 2 years) |

| Tightening global data-privacy laws | -1.4% | EU and North America | Medium term (2-4 years) |

| Volatile API pricing and access limits | -1.1% | Global | Short term (≤ 2 years) |

| AI hallucination / compliance risks | -0.9% | Regulated sectors worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Enterprise-Grade Suites

Enterprise monitoring solutions can exceed USD 57,000 per year, with a median around USD 25,000, creating formidable barriers for budget-constrained firms.[3]Vendr Pricing Desk, “Media Monitoring Software Pricing Trends 2024,” vendr.com Talkwalker averages USD 27,000 annually, and Brandwatch’s enterprise tier surpasses USD 3,000 per month, more than triple its basic offering. Total ownership rises further after factoring onboarding, integrations, and dedicated analysts. As AI features and multilingual packs become add-ons, a two-tier market emerges: deep-pocketed corporates secure comprehensive coverage while SMEs settle for limited point solutions. Vendors are responding with modular licensing, but steep entry prices still temper adoption in emerging economies.

Volatile API Pricing and Access Limits

X (formerly Twitter) doubled its Basic API fee to USD 200 per month and now charges up to USD 210,000 monthly for premium enterprise access, forcing several monitoring providers to rethink business models. Starting July 2025, the platform also moves to a revenue-share model, injecting more cost unpredictability. Large software players can absorb these spikes or secure private data deals, but niche vendors and SME clients risk losing critical channels overnight. The resulting diversification toward open-web crawls and multi-platform architectures raises engineering complexity and can dilute data completeness, slowing overall market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Innovation

The software segment accounted for 67.31% of 2025 revenue, underscoring organisations’ preference for configurable, API-rich platforms that sit at the core of omnichannel communications programmes. Subscription models bundle unlimited data ingestion, AI enrichment layers, and flexible seat licences, which together anchor predictable budgeting for global teams. Growth in the services arm, meanwhile, stems from mounting complexity: clients request bespoke taxonomies, ESG keyword libraries, and custom dashboards that convert raw sentiment feeds into board-level KPIs. Many vendors now embed advisory hours within annual contracts, blurring classic product-service boundaries and bolstering stickiness. Meltwater’s daily processing of over 1 billion content items exemplifies at-scale operations that differentiate enterprise-grade offerings. Strategic partnerships such as Meltwater’s Copilot integration with Microsoft further elevate competitiveness by letting employees query insights inside familiar collaboration tools, accelerating adoption across functions.

Complementary services extend to multilingual model tuning, compliance audits, and automated report creation tailored to investor-relations schedules. As AI maturity rises, clients increasingly offload labour-intensive tasks such as taxonomy updates and negative-news scorecard design to vendor consultants. This convergence reshapes commercial models inside the media monitoring market, fostering outcome-based pricing where platform fees adjust to SLA-bound insight delivery.

By Deployment: Cloud Migration Accelerates

Cloud deployments held 69.85% share in 2025 and are expanding at a forecast 15.55% CAGR, propelled by elastic processing that handles traffic surges during crises or product launches without manual scaling. Cloud vendors bundle containerised microservices for speech-to-text, image recognition, and language detection, letting monitoring suites spin up specialised engines on demand. In regulated sectors, hybrid topologies prevail: sensitive data remain on-premise while public news feeds traverse cloud pipelines, satisfying sovereignty mandates without hampering innovation. Total cost analyses show cloud subscriptions reduce infrastructure spend and shorten implementation cycles, tipping the balance decisively in their favour. The capability to replicate environments across regions also attractive for multinational brands that must mirror compliance configurations while sharing global reporting templates. As AI model training intensifies—even momentarily reaching 100 million parameters for contextual sentiment modules—cloud GPUs supply the horsepower few corporations can economically host in-house.

On-premise installations persist where air-gapped security is non-negotiable, such as defence departments and critical-national-infrastructure operators. Yet even these buyers increasingly subscribe to cloud-delivered threat-intelligence add-ons, marking a gradual migration path that sustains double-digit cloud growth inside the media monitoring market.

By Enterprise Size: SME Adoption Accelerates

Large enterprises retained 57.92% revenue share in 2025, justified by sprawling brand portfolios, multilanguage stakeholder bases, and stringent regulatory oversight that drive heavyweight monitoring needs. They deploy multi-tenant governance, advanced role hierarchies, and custom sentiment taxonomies aligned to corporate risk frameworks. Conversely, SMEs post a 14.63% CAGR through 2031, reflecting a democratisation trend as vendors introduce accessible tiers such as SentiOne’s USD 300 monthly Team plan. Cloud-first architecture and guided setup wizards shrink implementation times from months to days, making sophisticated insights attainable even without in-house analysts. Flexible seat licensing matches fluctuating headcounts common in growth-stage companies.

As brand exposure escalates on social media, smaller firms realise a single viral complaint can inflict outsized harm. Consequently, they prioritise always-on monitoring with automated alerts delivered via Slack or Microsoft Teams. To maintain profitability at low price points, vendors apply usage-based pricing tied to mention volumes and rely on GenAI to streamline onboarding, classification, and report generation, ensuring support costs remain sustainable. This dynamic firmly embeds SMEs as the fastest-rising customer cohort inside the media monitoring market.

By End-User Vertical: BFSI Leadership and Healthcare Growth

BFSI institutions captured 28.86% of 2025 revenue, deploying continuous adverse-media screening to meet “Know Your Customer” and anti-money-laundering mandates. Banks integrate monitoring outputs directly into case-management tools, enriching decision trees that flag reputational exposures before they escalate. Santander Rio’s real-time brand mention dashboards illustrate how financial firms operationalise insights across PR, compliance, and risk desks. Healthcare is the velocity leader at a 13.95% CAGR as hospitals and life-science companies correlate patient sentiment with treatment adherence and service-line improvements. Nearly 88% of clinicians use social media, generating traceable feedback loops that inform quality initiatives and public-health messaging.

Entertainment and media brands leverage monitoring to benchmark content resonance and influencer alignment, while retailers track user-generated reviews that sway conversion rates. Public-sector agencies increasingly employ listening tools for policy feedback and misinformation mapping, underscoring the media monitoring market’s transition from marketing nice-to-have to mission-critical infrastructure across sectors.

By Media Channel Monitored: Broadcast Resilience Amid Digital Shift

Broadcast commanded 40.92% of 2025 coverage, reflecting television and radio’s enduring ability to shape public opinion and seed social-media cascades. Monitoring suites ingest live TV via automated video-to-text pipelines, enabling near-real-time alerting when negative mentions air during primetime. Despite audience migration to streaming, advertisers still allocate large budgets to linear spots, sustaining demand for comprehensive broadcast insight. Online news and blogs, however, are the fastest-climbing channel at 12.56% CAGR as search-driven discovery fuels traffic for digital publishers. Social media remains indispensable, but its fragmentation drives higher complexity, making ai in social media essential for brands to track shorts, reels, and ephemeral stories alongside legacy posts, each with unique metadata.

Podcast analysis emerges as a distinct sub-workstream, as AI transcription converts spoken word into searchable text and sentiment layers. Print coverage maintains relevance in compliance-heavy industries where legal journals and industry gazettes remain authoritative. The successful vendor roadmap therefore unifies dashboards across all channel types, granting users a 360-degree view of reputation trajectories, an imperative reinforced by the overarching demands of the media monitoring market.

Geography Analysis

North America generated 37.44% of 2025 revenue, underpinned by sophisticated adtech ecosystems, high enterprise digitisation, and stringent regulations such as CCPA that necessitate detailed consumer-communication tracking. Organisations in the region routinely embed predictive sentiment modules into marketing clouds, turning monitoring feeds into campaign-optimisation engines. Mature PR agency networks further amplify platform uptake, with many bundling monitoring dashboards into retainer packages for corporate clients. Government agencies also leverage suites to comply with transparency mandates, sustaining baseline demand independent of economic cycles.

Europe continues to prioritise GDPR adherence, driving uptake of solutions with built-in consent workflows and data-sovereignty controls. Enterprises favour vendors hosting data within EU borders, spurring regional cloud partnerships and federated-search architectures. The media monitoring market size for Europe is bolstered by compulsory ESG-disclosure tracking across publicly listed firms, which widens use cases beyond traditional PR teams. In addition, major sporting events and political campaigns fuel spikes in monitoring volumes that reinforce platform reliance.

APAC is the expansion hotspot, forecast at 17.05% CAGR through 2031. Digital advertising across China and Japan constitutes two-thirds of regional spend, amplifying data streams that necessitate multilingual monitoring engines. India’s rapid ascent as an audio-consumption powerhouse accelerates demand for podcast analytics. Regulatory tightening, such as Indonesia’s personal-data protection laws, mirrors European norms and compels organisations to adopt compliant suites. Meanwhile, local-language NLP innovation becomes a competitive moat for vendors, as accuracy in Korean, Thai, or Bahasa is decisive when filtering sentiment at scale.

Latin America and the Middle East and Africa represent emergent growth corridors. Smartphone penetration climbs across these regions, increasing social-media content in Spanish, Arabic, and regional dialects. Governments invest in digital infrastructure and disinformation-tracking initiatives, creating public-sector tenders that introduce new revenue streams. Vendors willing to localise interfaces and offer flexible pricing can capture first-mover advantage, positioning themselves for compounded gains as digital maturity rises.

Competitive Landscape

The media monitoring market remains moderately fragmented, with a mid-tier cluster of global vendors—Cision, Meltwater, Talkwalker, Brandwatch, Signal AI and others—commanding notable but not dominant shares. Combined, the top five players account for roughly 45-50% of global revenue, leaving ample space for niche specialists. Providers differentiate on AI accuracy, breadth of data connectors, and workflow integration depth rather than on raw data volume alone. Meltwater generated USD 558 million in 2024 and continues acquisitive moves, illustrated by its Blackbird.AI collaboration to counter narrative attacks. Cision’s purchase of Factmata augments misinformation detection, signalling a race to own safety-adjacent capabilities vital for regulated industries.

Smaller challengers focus on verticalised solutions—healthcare sentiment, investor-relations intelligence, or influencer analytics—using narrower scopes to deliver accuracy that generalist platforms sometimes lack. Many secure growth through white-label deals, embedding analytics inside PR agency portals. Strategic partnerships with cloud hyperscalers and productivity-suite providers create sticky ecosystems; Meltwater Copilot’s Teams integration is one example, as is Brandwatch’s connectors into Adobe Experience Cloud. Vendor lock-in rises when monitoring outputs feed automated campaign triggers, raising switching costs and supporting premium pricing.

Media Monitoring Industry Leaders

Cision

Meltwater

Intrado/Notified

Agility PR Solutions

Signal AI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TAG, in collaboration with swXtch.io, a provider of cloud-based multicast networking, is set to enhance cloud-based media monitoring for broadcasters and content creators. TAG's software-based multiviewer, now integrated with swXtch.io’s unique cloud capabilities, can monitor any IP stream, such as 2110 and JPEG XS, achieving performance levels akin to on-premises systems. This integration not only elevates the accuracy of stream monitoring in workflows but also cuts costs, diminishes latency, and provides real-time insights into stream health and quality.

- January 2025: TVEyes, a global leader in broadcast, podcast, and online video media intelligence, has teamed up with Medianet, a top-tier media intelligence provider in Australia. This strategic alliance grants Medianet users access to TVEyes' vast repository of Australian broadcast content. By merging TVEyes' global broadcast monitoring prowess with Medianet's in-depth knowledge of the Australian media scene, this partnership marks a significant milestone, coinciding with the launch of Medianet's revamped platform.

- August 2024: Meltwater launched a global Partner Program, teaming with Microsoft and Dig Human to co-create solutions and expand market reach.

- July 2024: Meltwater partnered with Blackbird.AI to combat narrative attacks and misinformation, integrating real-time narrative intelligence into Meltwater’s social and media

Global Media Monitoring Market Report Scope

Media monitoring is the activity of monitoring the output of the print, online and broadcast media. It is based on analyzing a diverse range of media platforms in order to identify trends that can be used for a variety of reasons such as political, commercial and scientific purposes.

The media monitoring market is segmented by component (software, services), by deployment (cloud, on-premises), by enterprises (SMEs, large enterprises), by end-user (BFSI, entertainment and media, healthcare, retail and e-commerce, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Software |

| Services |

| Cloud |

| On-premise |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Entertainment and Media |

| Healthcare |

| Retail and E-commerce |

| Public Sector and NGOs |

| Other Verticals |

| Online News and Blogs |

| Social Media |

| Broadcast (TV/Radio) |

| Podcasts |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment | Cloud | ||

| On-premise | |||

| By Enterprise Size | Small and Medium-sized Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End-user Vertical | BFSI | ||

| Entertainment and Media | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Public Sector and NGOs | |||

| Other Verticals | |||

| By Media Channel Monitored | Online News and Blogs | ||

| Social Media | |||

| Broadcast (TV/Radio) | |||

| Podcasts | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the media monitoring market?

The media monitoring market size reached USD 5.99 billion in 2026.

How fast is the media monitoring market expected to grow

It is forecast to expand at an 10.99% CAGR, reaching USD 10.09 billion by 2031.

Which segment will contribute the most growth through 2031?

Cloud-based deployments are projected to post the highest 15.55% CAGR as enterprises prioritise scalable, real-time analytics.

Why are SMEs adopting media monitoring tools more quickly than before?

Vendors now offer modular, lower-priced tiers and guided setups, enabling smaller firms to access AI-powered insights without large IT teams.

Page last updated on: