Subcutaneous Biologics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 286.30 Billion |

| Market Size (2031) | USD 498.90 Billion |

| Growth Rate (2026 - 2031) | 11.75% CAGR |

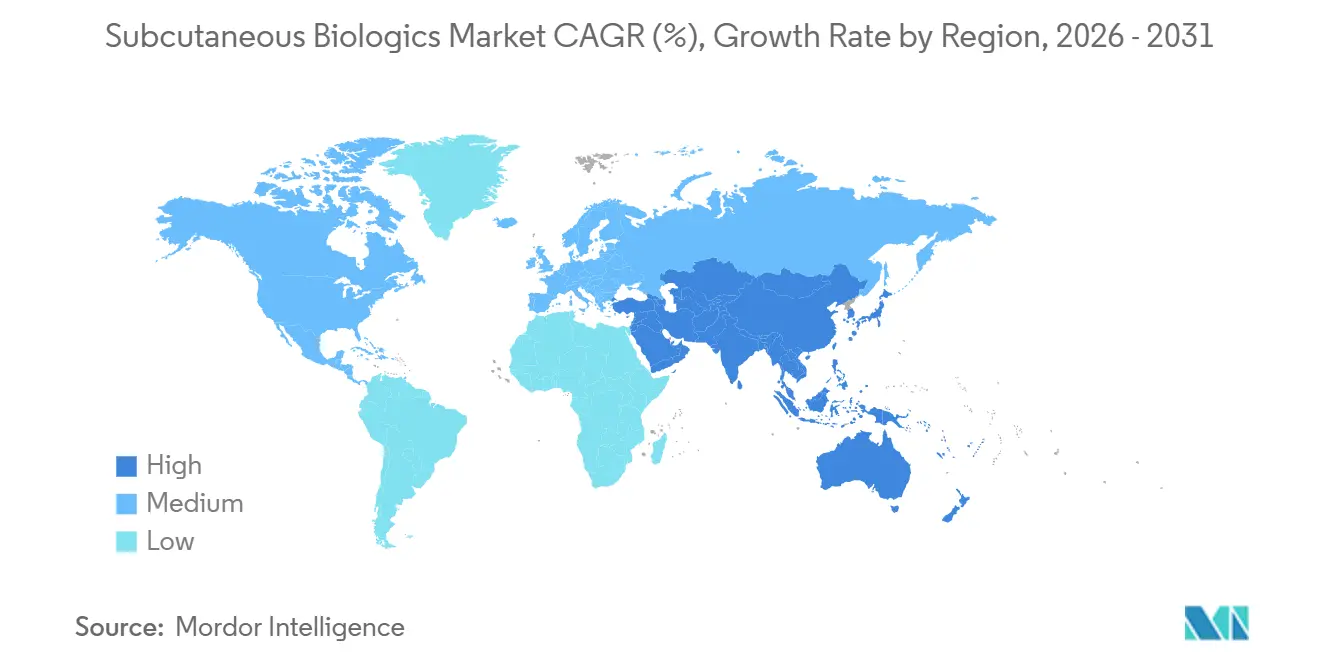

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Subcutaneous Biologics Market Analysis by Mordor Intelligence

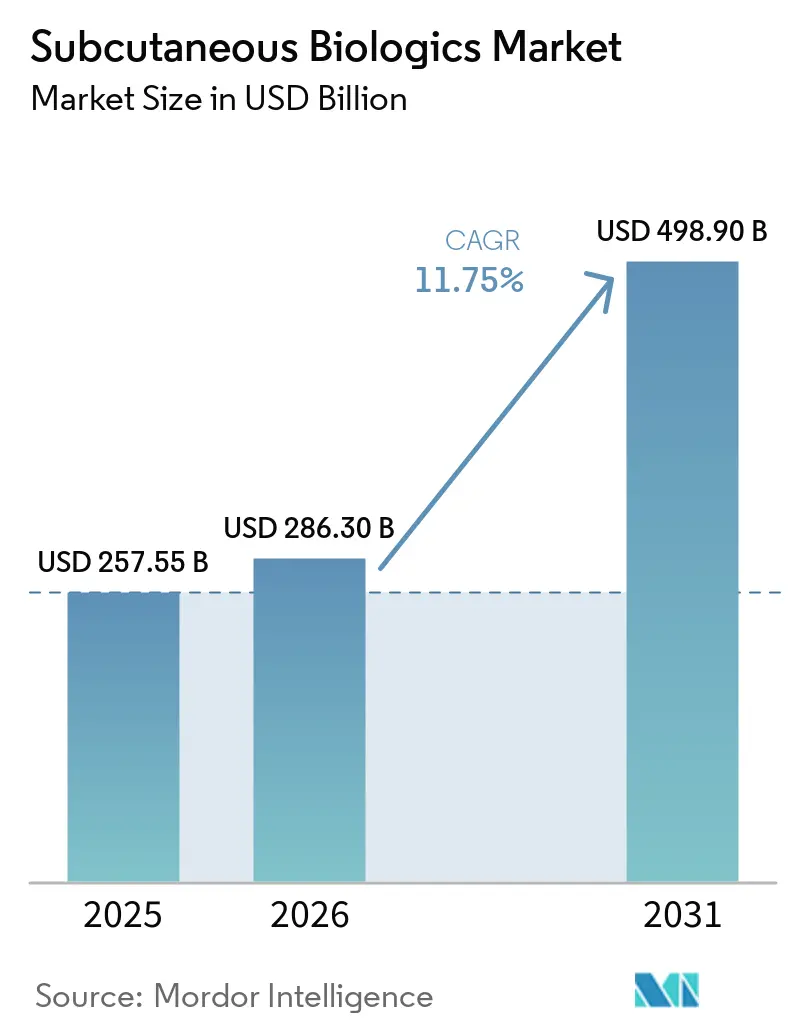

The Subcutaneous Biologics Market size is expected to grow from USD 257.55 billion in 2025 to USD 286.30 billion in 2026 and is forecast to reach USD 498.90 billion by 2031 at 11.75% CAGR over 2026-2031.

A wave of rapid-switch approvals is compressing infusion times from hours to minutes, which reallocates hospital chairs and encourages payers to reimburse at-home administration. Biosimilar launches at 30-40% list-price discounts are expanding treated volumes even as they erode originator pricing. At the same time, innovators are embedding hyaluronidase, connectivity, and wearable technologies to justify device premiums and sustain revenues. Large-volume on-body injectors and dual-agonist GLP-1 peptides are widening the therapeutic scope beyond immunology into oncology, hematology, and obesity.

Key Report Takeaways

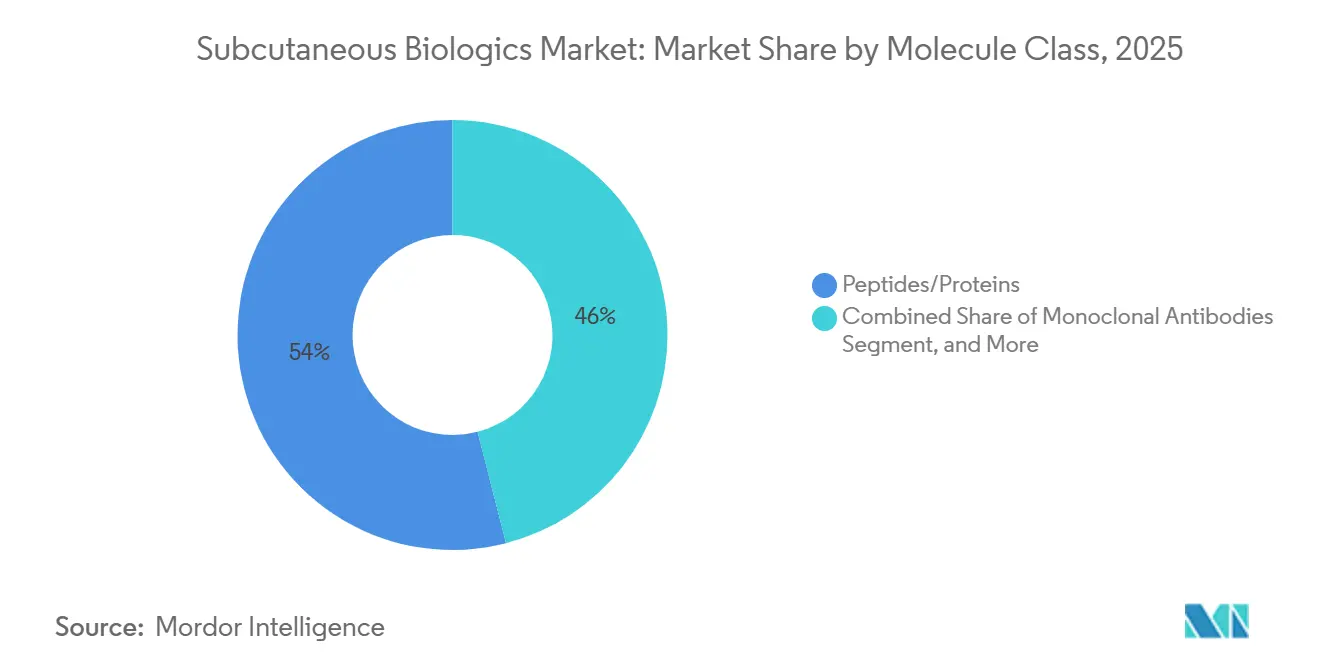

- By molecule class, oligonucleotides led with 54.01% of the subcutaneous biologics market share in 2025, and oligonucleotides are forecast to grow at a 13.45% CAGR through 2031.

- By delivery system, prefilled syringes accounted for 78.00% of the subcutaneous biologics market size in 2025, and on‑body/wearable injectors are advancing at a 14.56% CAGR to 2031.

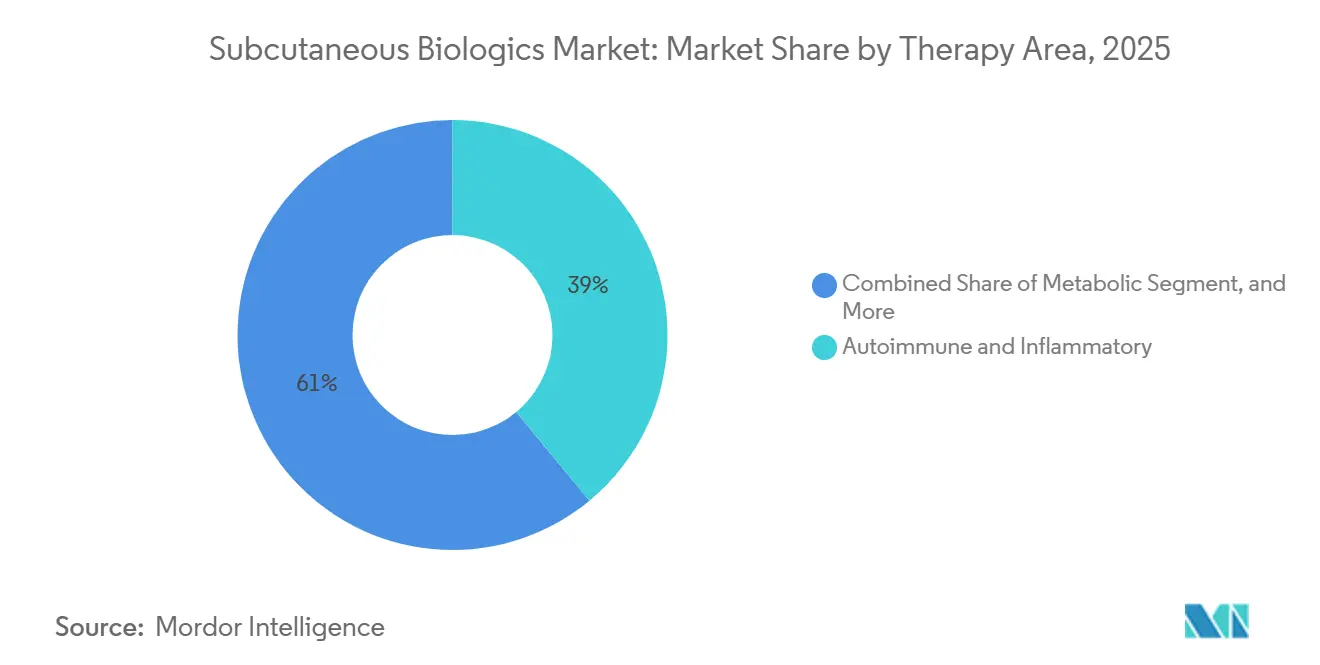

- By therapy area, autoimmune and inflammatory disorders accounted for 39.01% of revenue in 2025, and oncology & hematology are advancing at a 13.65% CAGR over the forecast period.

- By geography, North America retained 51.09% share of the subcutaneous biologics market size in 2025, and Asia-Pacific is expanding at a 13.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Subcutaneous Biologics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GLP-1 expansion in obesity and T2D accelerates SC biologics demand | +2.5% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Shift to at-home self-administration reduces site-of-care costs | +1.8% | North America, Europe, and urban APAC markets | Short term (≤ 2 years) |

| Rapid approvals of SC versions of prior IV biologics (oncology/immunology) | +2.2% | Global, with regulatory momentum in US and EU | Medium term (2-4 years) |

| Biosimilar entry drives volume expansion in self-injected immunology | +1.5% | North America and Europe, with emerging APAC uptake | Long term (≥ 4 years) |

| High-volume/viscous SC delivery via wearables unlocks larger doses | +1.3% | North America and Europe, with pilot programs in APAC | Long term (≥ 4 years) |

| Connected autoinjectors improve adherence and persistence | +0.9% | North America and Western Europe, with digital-health infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GLP-1 Expansion in Obesity and T2D Accelerates SC Biologics Demand

Dual and triple agonists are achieving weight-loss results previously reserved for bariatric surgery, which is shifting payer calculus toward earlier pharmacologic intervention. Novo Nordisk’s amycretin delivered 22% mean weight reduction at 36 weeks, outpacing semaglutide and moving into Phase III in 2026 [1]Novo Nordisk, “Pipeline Update 2025,” novonordisk.com. Generic liraglutide introductions in late 2024 and mid-2025 lowered entry prices and opened cost-sensitive markets. Canadian semaglutide generics expected in early 2026 will further broaden access through provincial formularies. Pipeline combinations such as CagriSema are designed to fine-tune satiety and glycemic control, sustaining demand for high-concentration pens. Even with an oral semaglutide filing under FDA review, adherence data suggest high-dose obesity regimens will continue to favor injection. Collectively, these dynamics elevate pen and autoinjector volumes, reinforcing the growth trajectory of the subcutaneous biologics market.

Shift to At-Home Self-Administration Reduces Site-of-Care Costs

Patient-reported outcomes from the IMscin002 study showed that 70.7% preferred subcutaneous delivery because it liberates time and eliminates cannulation discomfort [2]ClinicalTrials.gov, “IMscin002 Patient-Preference Study,” clinicaltrials.gov. The FDA’s December 2024 approval of subcutaneous nivolumab cut chair time from 60 minutes to 5 minutes, while mosunetuzumab’s December 2025 nod compressed delivery of a bispecific antibody to 1 minute. Regional U.S. payers responded in 2025 by paying 90-95% of the IV rate when patients inject at home. European oncology units cite similar efficiencies, pushing hospitals to redeploy infusion nurses to more complex procedures. As convenience and cost incentives align, the subcutaneous biologics market gains volume across oncology, immunology, and metabolic lines.

Rapid Approvals of SC Versions of Prior IV Biologics

CheckMate-67T established pharmacokinetic non-inferiority for subcutaneous nivolumab, setting a precedent for checkpoint-inhibitor conversions. The EMA’s November 2025 clearance for subcutaneous pembrolizumab echoed the FDA’s stance and signaled regulatory consensus. Roche combined atezolizumab with Halozyme’s ENHANZE hyaluronidase to reduce administration to 7 minutes and awaits multi-region approvals. The FDA proposed in 2025 to waive Phase III trials for certain biosimilar SC switches when analytical similarity and PK data suffice, potentially shaving two years off development. These frameworks increase sponsor appetite, thereby enlarging the pipeline and accelerating growth of the subcutaneous biologics market.

Biosimilar Entry Drives Volume Expansion in Self-Injected Immunology

Samsung Bioepis counted 73 approvals and 48 launches by Q2 2025, with three ustekinumab biosimilars priced below Stelara. Denosumab follow-ons seized notable osteoporosis volume within 18 months of launch. Celltrion leveraged self-injectable infliximab to win European tenders where device convenience offsets lower discounts. Viatris and Biocon’s Semglee undercut Lantus, proving price elasticity in diabetes. Medicare’s Inflation Reduction Act negotiations for Enbrel and Stelara accelerate mandated switches, propelling biosimilar penetration and reinforcing long-run volume growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply constraints for GLP-1s and injection components | -0.6% | Global, with acute pressure in North America and Europe | Short term (≤ 2 years) |

| Payer controls and price pressure on specialty drugs | -1.0% | North America and Europe, with emerging impact in APAC | Medium term (2-4 years) |

| Tissue tolerability limits for high-volume/viscosity SC injections | -0.5% | Global, with formulation challenges in oncology and rare diseases | Medium term (2-4 years) |

| Sustainability pressure on single-use injectors | -0.4% | Europe and North America, with regulatory scrutiny intensifying | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Constraints for GLP-1s and Injection Components

Although Wegovy and Mounjaro shortages were resolved by February 2025, downstream constraints in glass barrels, plungers, and wearable electronics linger. Stevanato pledged EUR 400 million to raise syringe output significantly by 2027, and Gerresheimer added 200 million units of annual capacity in Serbia. West Pharmaceutical invested USD 150 million in high-speed autoinjector lines in Ireland and the United States. Nonetheless, lead times for custom wearable injectors hover at 18-24 months, slowing launches of next-generation formulations. These bottlenecks temporarily limit how fast the subcutaneous biologics market can scale, despite underlying demand.

Payer Controls and Price Pressure on Specialty Drugs

The IRA’s first negotiation cycle lopped Enbrel’s reimbursement to USD 2,355 and Stelara to USD 4,695, slashing net prices by two-thirds [3]Centers for Medicare & Medicaid Services, “Medicare Drug Price Negotiation 2026,” cms.gov. Commercial PBMs adopted step-therapy in 2025, diverting 15-20% of new starts to lower-cost biosimilars. Prior-authorization prevalence rose significantly, and European HTA agencies tightened acceptable cost-effectiveness thresholds. As a result, manufacturers resort to outcomes-based deals that increase administrative overhead and curb price flexibility. The drag on revenue growth tempers the otherwise robust trajectory of the subcutaneous biologics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Molecule Class: Oligonucleotides Surge as Peptides Retain Scale

Oligonucleotides siRNA and antisense constructs form the fastest-growing slice of the subcutaneous biologics market, advancing at a 13.45% CAGR to 2031 as refined lipid-nanoparticle carriers, and GalNAc conjugates improve tissue penetration and temper injection-site reactions. Peptides and proteins still controlled 54.01% of 2025 revenue, helped by Novo Nordisk’s amycretin, which delivered 22% mean weight loss at 36 weeks, and by generic liraglutide launches that widened access across Medicaid and provincial formularies.

Monoclonal antibodies remain the second-largest class as subcutaneous checkpoint inhibitors—nivolumab SC (FDA, December 2024) and pembrolizumab SC (EMA, November 2025)—shrink administration windows to 1-5 minutes, freeing infusion capacity. Immunoglobulin replacement therapies are unlocking new volume as 20-mL wearable pumps condense the four- to six-site regimens common in primary immunodeficiency management.

By Delivery System: Wearables Disrupt While Prefilled Syringes Dominate

On-body and wearable injectors post the steepest growth curve, projected to grow at a 14.56% CAGR through 2031, because platforms like enFuse can deliver 2-50 mL of high-viscosity biologics that were once limited to intravenous settings. West’s SmartDose 3.5 targets oncology and rare-disease doses over 3.5 mL, and SteadyMed’s PatchPump moves 20 mL SCIG regimens into single-patch wearables, illustrating how form-factor innovation expands the subcutaneous biologics market size for high-dose therapies.

Prefilled syringes still held 78.00% of 2025 volume, and Stevanato’s EUR 400 million outlay is set to lift glass-barrel capacity 30% by 2027 to meet GLP-1 surge demand. Autoinjector pens rank second; connected versions from Biocorp transmit adherence data that underpin outcomes-based rebates. Vial-and-syringe use declines as ready-to-use formats prove safer for at-home care. At the same time, prefilled cartridges remain relevant in insulin and GLP-1 therapy, as reusable pens dominate European reimbursement practices. Halozyme’s ENHANZE enzymatic co-formulation continues to cut injection time by up to 95%, reinforcing device-formulation co-development as a competitive moat.

By Therapy Area: Oncology Accelerates, Autoimmune Retains Lead

Oncology and hematology command the fastest trajectory, forecast at a 13.65% CAGR to 2031, as subcutaneous checkpoint inhibitors—nivolumab, pembrolizumab, mosunetuzumab, and amivantamab compress multi-hour infusions into sub-five-minute injections, opening outpatient and even home-based administration pathways. Daratumumab SC already converts 60% of new U.S. multiple myeloma starts, demonstrating 3-minute delivery versus 3-7-hour IV infusions.

Autoimmune and inflammatory diseases still accounted for 39.01% of 2025 revenue, led by AbbVie’s Skyrizi at USD 7.8 billion and buoyed by the convenience of IL-23 inhibitors relative to TNF competitors. Ustekinumab biosimilars priced 30-40% below Stelara spur mandatory switches that lift treated volumes while curbing price inflation. Metabolic disorders remain the breakout growth pocket as tirzepatide revenues mount and dual-agonist CagriSema enters Phase III, whereas neurology, respiratory and rare-disease segments expand more modestly but gain adherence benefits from high-volume wearables.

Geography Analysis

Asia-Pacific posts a 13.14% CAGR outlook, driven by China’s 2024-2025 subcutaneous biosimilar wave, Japan’s broadened GLP-1 reimbursement, and South Korea’s export-oriented biosimilar giants. India’s fill-finish expansion and Australia’s PBS coverage gains further widen regional access, though affordability gaps persist outside urban centers.

North America still accounted for 51.09% of the subcutaneous biologics market share in 2025 as IRA price negotiations paradoxically fueled biosimilar volume growth and as payers reimbursed at-home injections at near-IV parity. Europe ranks second; EMA’s sub-one-minute pembrolizumab approval and hospital capacity constraints speed adoption, while Southern European tenders push biosimilar penetration in immunology lines by 2025. GCC investment and Latin American public-health initiatives support nascent uptake elsewhere, though macro volatility moderates growth in Argentina and parts of Sub-Saharan Africa.

Competitive Landscape

The top five players, AbbVie, Eli Lilly, Novo Nordisk, Roche, and Novartis, collectively hold about a major share of global revenue, signaling moderate consolidation. AbbVie’s autoinjector-enabled Skyrizi earned USD 7.8 billion in 2024, while Rinvoq neared USD 3.2 billion as label expansions progressed. Novo Nordisk scaled GLP-1 capacity significantly at Kalundborg, removing Wegovy from shortage status. Eli Lilly’s USD 2.5 billion North Carolina plant adds 400 million pens annually, preparing for volume ramps of tirzepatide.

Biosimilar specialists—Samsung Bioepis, Celltrion, Viatris, Biocon now command a notable share in mature immunology lines, leveraging aggressive pricing and tender wins. Halozyme monetizes ENHANZE via 20-plus partnerships that accelerate high-volume SC conversions, making the platform a critical enabler of formulation differentiation. Device firms such as Enable Injections, Ypsomed, and West capture greater economies of scale by bundling hardware, connectivity, and fill-finish know-how.

Regulatory shifts that permit PK-bridge approvals for SC biosimilars intensify competition and invite mid-tier entrants. Value-based reimbursement linked to digital adherence favors companies that integrate sensors and analytics into devices. Consequently, incumbents balance margin defense with R&D for next-generation delivery formats, shaping a dynamic yet opportunity-rich subcutaneous biologics market.

Subcutaneous Biologics Industry Leaders

Novartis AG

Eli Lilly and Company

Novo Nordisk A/S

F. Hoffmann-La Roche Ltd

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Biologics License Application (BLA) for the subcutaneous formulation of the Alzheimer's treatment Leqembi was accepted for review in China.

- January 2026: FDA approved Darzalex Faspro in combination with VRd for newly diagnosed multiple myeloma patients.

- September 2025: The U.S. FDA approved Merck & Co.’s SC formulation of Keytruda, branded as Keytruda Qlex, which reduces administration time from 30 minutes (IV) to just one to two minutes.

Global Subcutaneous Biologics Market Report Scope

As per the scope of the report, subcutaneous biologics are specialized medications derived from living cells that are injected into the fatty tissue layer just beneath the skin to treat chronic conditions like rheumatoid arthritis, diabetes, and certain cancers.

The subcutaneous biologic market is segmented by molecule class, delivery system, therapy area, and geography. By molecule class, the market is segmented into monoclonal antibodies (mAbs), peptides, immunoglobulins (SCIG), cytokines, oligonucleotides, enzymes/hormones, and others specified. By delivery system, the market is segmented into prefilled syringes, autoinjector pens, and on‑body/wearable injectors, vial‑and‑syringe, and prefilled cartridges for pens. By route of administration, the market is segmented into metabolic, autoimmune & inflammatory, oncology & hematology, neurology, respiratory & allergy, rare diseases & immunodeficiencies.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Monoclonal antibodies (mAbs) |

| Peptides/proteins (incl. GLP‑1s, insulin analogs) |

| Immunoglobulins (SCIG) |

| Cytokines/interferons |

| Oligonucleotides (siRNA/ASO) |

| Enzymes/hormones and others specified |

| Prefilled syringes |

| Autoinjector pens |

| On‑body/wearable injectors |

| Vial‑and‑syringe |

| Prefilled cartridges for pens |

| Metabolics |

| Autoimmune & inflammatory |

| Oncology & hematology |

| Neurology |

| Respiratory & allergy |

| Rare diseases & immunodeficiencies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Molecule Class | Monoclonal antibodies (mAbs) | |

| Peptides/proteins (incl. GLP‑1s, insulin analogs) | ||

| Immunoglobulins (SCIG) | ||

| Cytokines/interferons | ||

| Oligonucleotides (siRNA/ASO) | ||

| Enzymes/hormones and others specified | ||

| By Delivery System | Prefilled syringes | |

| Autoinjector pens | ||

| On‑body/wearable injectors | ||

| Vial‑and‑syringe | ||

| Prefilled cartridges for pens | ||

| By Therapy Area | Metabolics | |

| Autoimmune & inflammatory | ||

| Oncology & hematology | ||

| Neurology | ||

| Respiratory & allergy | ||

| Rare diseases & immunodeficiencies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the subcutaneous biologics market expected to grow through 2031?

It is projected to advance at an 11.75% CAGR from 2026 to 2031, moving from USD 286.30 billion to USD 498.90 billion.

Which molecule class currently commands the largest revenue?

Peptides and proteins, fueled by GLP-1 receptor agonists and insulin analogs, held 54.01% of 2025 revenue.

What delivery format dominates commercial volumes today?

Prefilled syringes represent 78.00% of worldwide volumes and will remain the backbone of high-throughput fill-finish lines.

Why are payers encouraging at-home injections?

One- to five-minute subcutaneous injections lower facility fees and free infusion chairs, so plans reimburse them at 90-95% of IV rates.

Page last updated on: