Interstitial Lung Disease Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

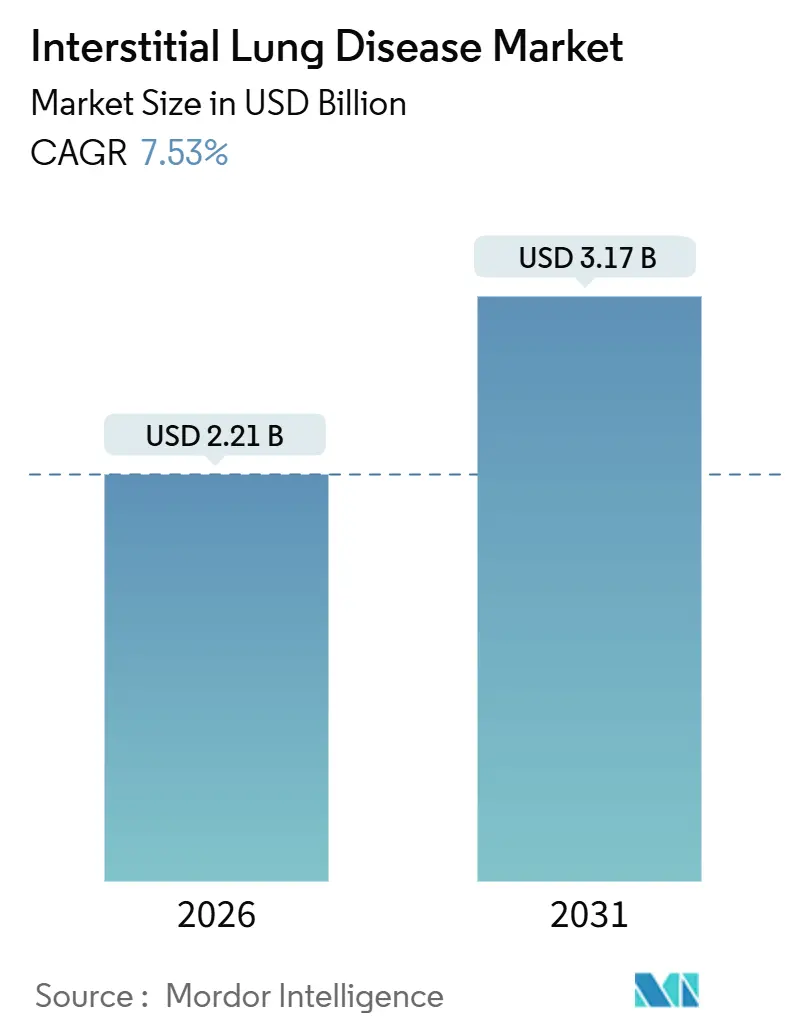

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 3.17 Billion |

| Growth Rate (2026 - 2031) | 7.53% CAGR |

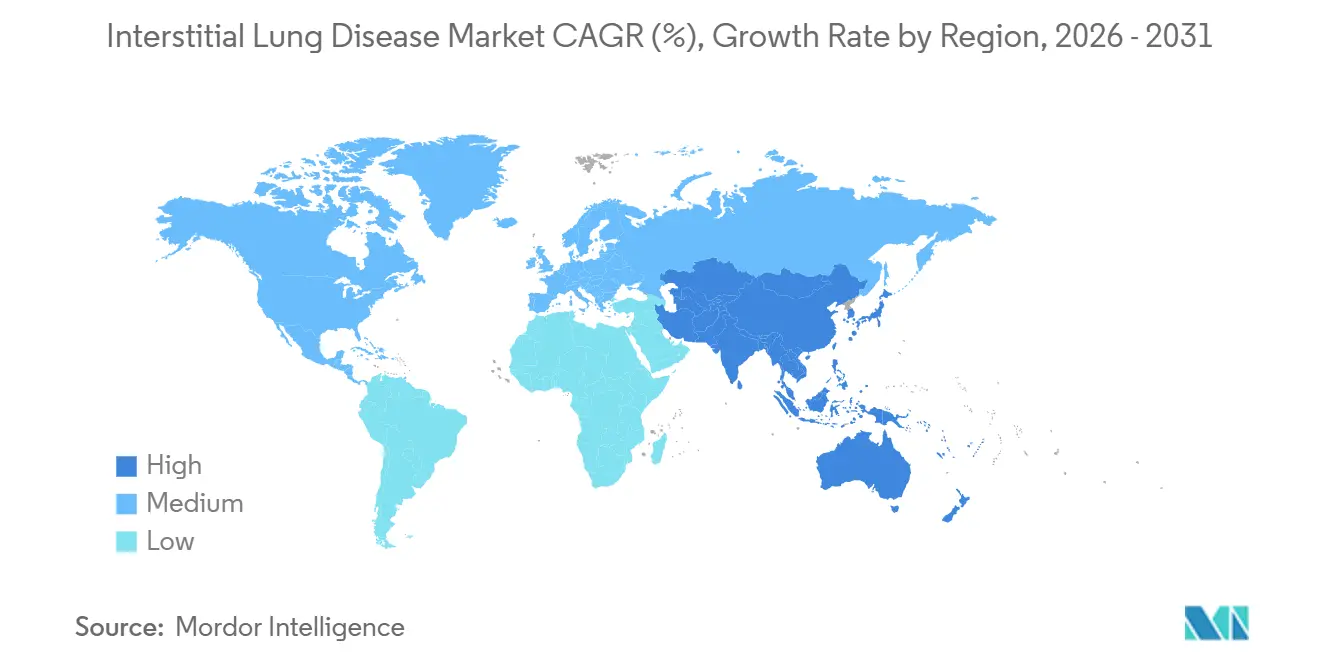

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

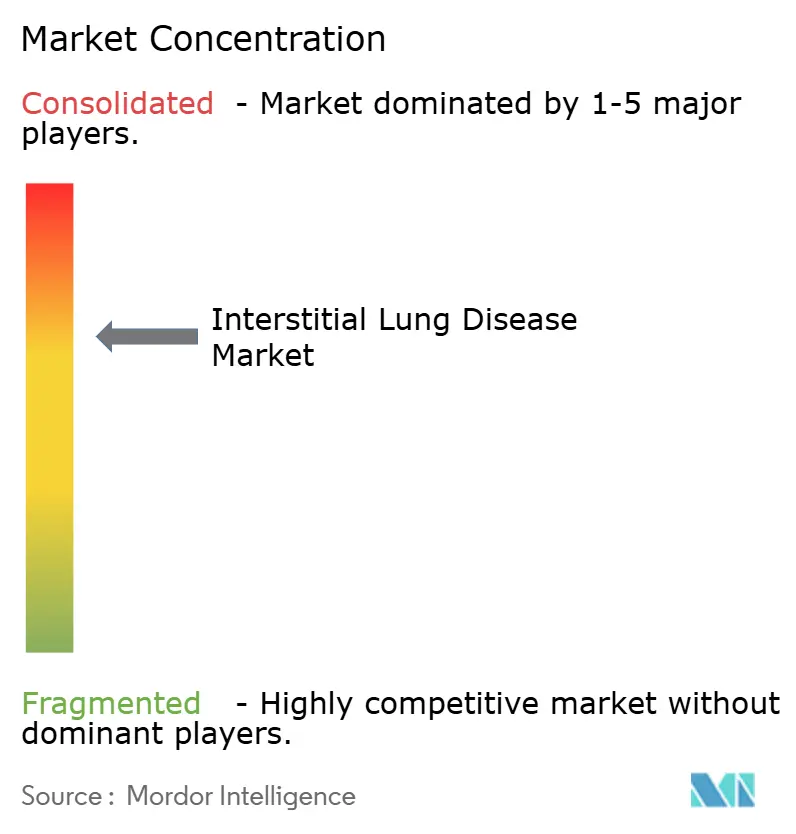

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Interstitial Lung Disease Market Analysis by Mordor Intelligence

The Interstitial Lung Disease Market size is estimated at USD 2.21 billion in 2026, and is expected to reach USD 3.17 billion by 2031, at a CAGR of 7.53% during the forecast period (2026-2031).

Market expansion is underpinned by the October 2025 U.S. approval of nerandomilast, the first novel idiopathic pulmonary fibrosis therapy in more than 10 years, which breaks the long-standing pirfenidone-nintedanib duopoly and signals broader therapeutic optionality for progressive fibrosis care. At the same time, European generic launches of nintedanib in 2024-2025 accelerated price erosion, forcing incumbents to recalibrate value-based contracting while biologics maintain a premium status through demonstrated efficacy in autoimmune-driven phenotypes. Rapid AI adoption in high-resolution CT and the proliferation of portable pulmonary function devices shorten diagnostic timelines, drawing investment toward integrated imaging-software ecosystems. Finally, home-care oxygen therapy and Bluetooth-enabled oximetry are helping stabilize patients outside hospitals, widening device manufacturers’ addressable base and reshaping payer cost-containment strategies.

Key Report Takeaways

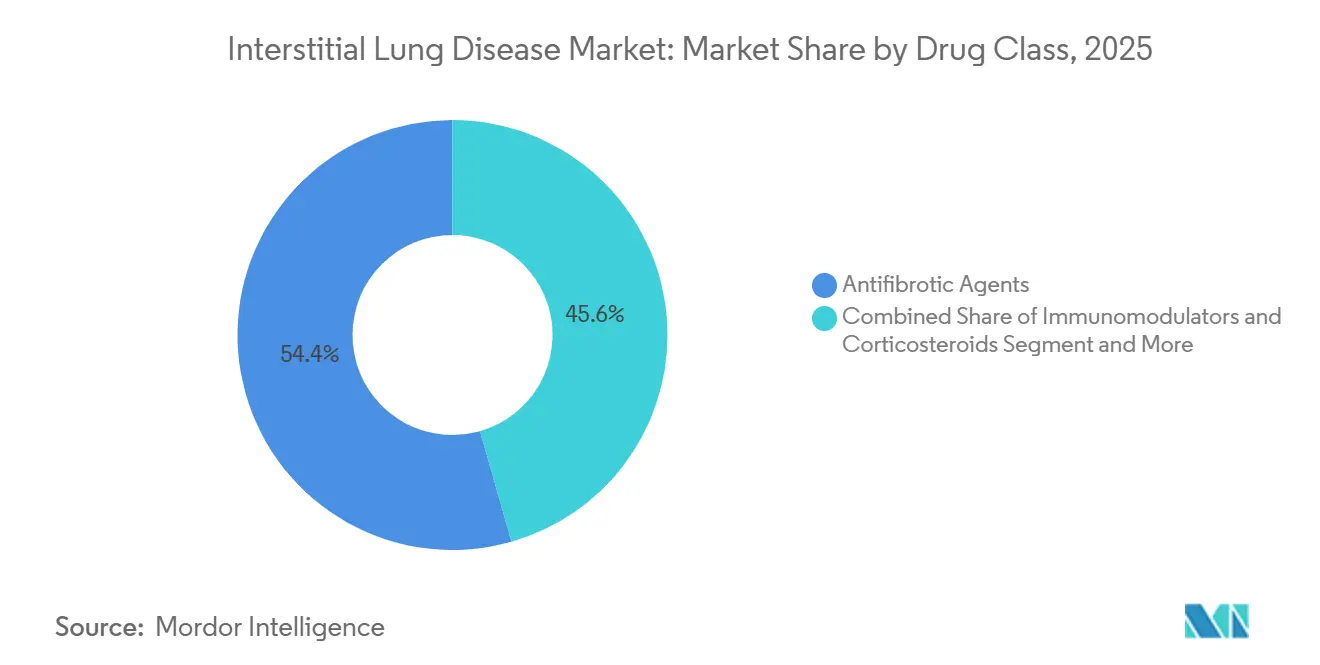

- By drug class, antifibrotic agents led with 54.43% of interstitial lung disease market share in 2025, whereas biologics and targeted therapies are advancing at a 9.54% CAGR to 2031.

- By disease type, idiopathic pulmonary fibrosis accounted for 42.45% of the interstitial lung disease market size in 2025, while systemic sclerosis-associated ILD is projected to expand at a 9.44% CAGR through 2031.

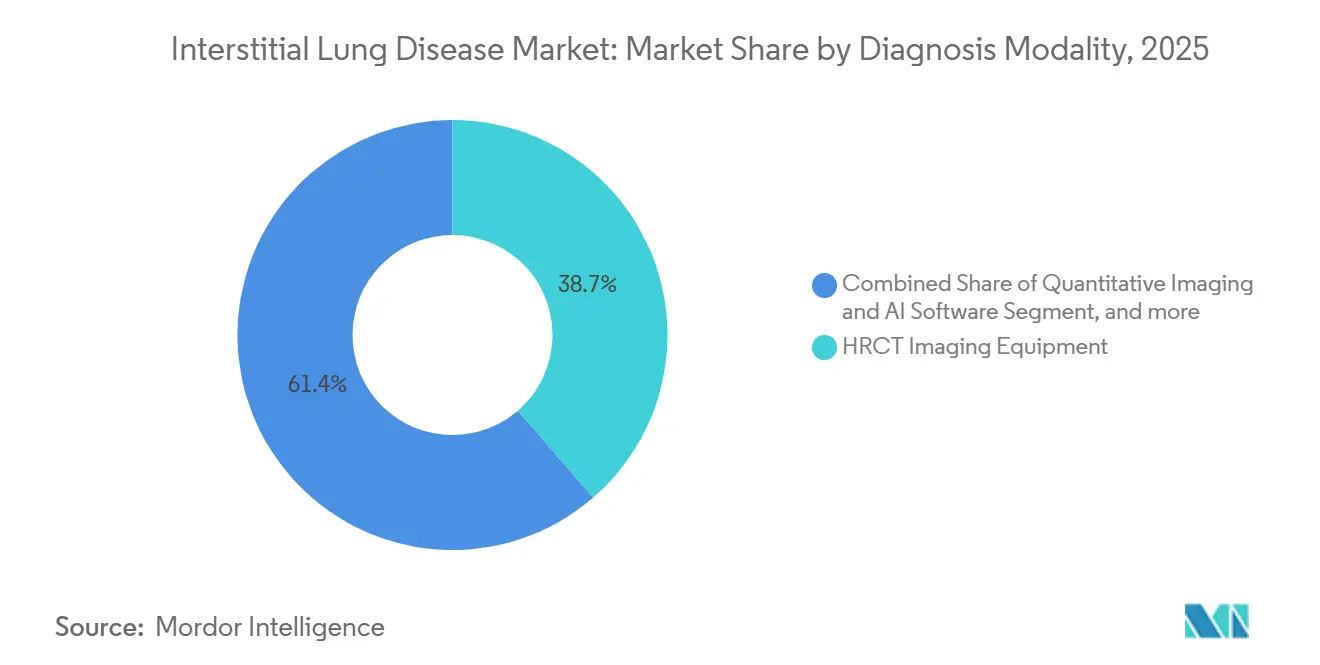

- By diagnosis modality, high-resolution CT equipment captured 38.65% revenue share in 2025; pulmonary function testing devices are tracking a 9.65% CAGR during the forecast period.

- By end user, hospitals held a 55.64% share of the interstitial lung disease market in 2025, and home care settings are set to grow at a 10.23% CAGR through 2031.

- By geography, North America accounted for 42.56% of the interstitial lung disease market share in 2025, while Asia-Pacific is the fastest-growing region at an 8.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Interstitial Lung Disease Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Interstitial Lung Diseases | +1.8% | Global, pronounced in Europe and North America | Medium term (2-4 years) |

| Growing Geriatric Population Susceptible to Pulmonary Fibrosis | +1.5% | North America, Europe, Japan, China | Long term (≥ 4 years) |

| Technological Advancements in High-Resolution Imaging and AI Analytics | +1.2% | North America and Europe, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Expanding Pipeline of Disease-Modifying Antifibrotic Therapies | +1.4% | Global, regulatory approvals centered in the U.S. and EU | Medium term (2-4 years) |

| Increasing Awareness and Early Multidisciplinary Diagnosis | +0.9% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Regulatory Incentives Including Orphan Drug Designations and Fast-Track Approvals | +0.7% | U.S. and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Interstitial Lung Diseases

Registry data from England showed that idiopathic pulmonary fibrosis diagnoses doubled to 6.1 per 100,000 between 2008 and 2018, a trend that persisted through 2024 as refined algorithms reclassified previously unassigned patterns. Systemic sclerosis- and rheumatoid arthritis-associated ILDs also share overlapping demand curves, as rheumatology clinics now routinely screen with HRCT and bronchoalveolar lavage. Multidisciplinary boards integrate radiology, pathology, and clinical data, improving reclassification accuracy and boosting treated prevalence. Hypersensitivity pneumonitis gained visibility once standardized exposure questionnaires and lymphocyte profiling became common practice. Together, better ascertainment and true incidence growth sustain mid-single-digit volume gains irrespective of breakthrough drugs.

Growing Geriatric Population Susceptible to Pulmonary Fibrosis

Age remains the dominant risk factor, with 73% of UK registry pulmonary fibrosis diagnoses occurring after 70 years. The United Nations projects the global 65-plus cohort will hit 1.6 billion by 2050, creating a large reservoir of high-risk lungs. Japan’s accelerated aging curve led to early approval of pirfenidone in 2008, demonstrating how demographic pressure can reshape regulatory priorities. China will exceed 400 million older adults by 2035, yet has limited subspecialty capacity outside tier-1 cities, positioning telehealth and portable diagnostics as critical access levers. Similar mismatches between demand and specialist supply favor remote-monitoring models and AI-enabled triage.

Technological Advancements in High-Resolution Imaging and AI Analytics

Convolutional neural networks trained on HRCT achieve 94% accuracy in differentiating fibrosis patterns, equaling expert radiologists[1]Nature Medicine, “AI for HRCT Pattern Recognition,” nature.com. VIDA Diagnostics’ LungPrint quantifies the extent of fibrosis and provides objective endpoints to trial sponsors and pulmonologists. Siemens’ AI-Rad Companion automatically generates structured lung reports within minutes, reducing bottlenecks in community hospitals. Philips’ Spectral CT 7500 reduces dose while preserving critical honeycombing detail, enabling longitudinal surveillance with a lower safety risk. These tools shift value from manual interpretation toward integrated imaging software bundles that accelerate time to treatment.

Expanding Pipeline of Disease-Modifying Antifibrotic Therapies

Nerandomilast reduced the annual decline in forced vital capacity by 64 mL in a pivotal trial and secured FDA approval in October 2025. Pliant’s bexotegrast, an αvβ6 integrin inhibitor, showed target engagement and favorable safety and entered Phase 3 IPF trials in 2026. FibroGen’s anti-CTGF antibody, pamrevlumab, has mixed efficacy signals but still addresses an unmet need for a mechanism to address progressive fibrosis. Tocilizumab’s systemic sclerosis-ILD indication validates IL-6 inhibition outside rheumatology. Mechanistic diversity raises prospects for future combination regimens and underpins continued venture funding, supported by orphan and breakthrough incentives that shorten development cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Antifibrotic Drugs and Diagnostic Procedures | -1.1% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Limited Availability of ILD Specialty Centers in Emerging Markets | -0.8% | Asia-Pacific (excluding Japan, South Korea), Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Adverse Gastrointestinal Effects Leading to Treatment Discontinuation | -0.6% | Global, heightened in elderly polypharmacy populations | Short term (≤ 2 years) |

| Lack of Curative Therapies Despite Pipeline Progress | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Antifibrotic Drugs and Diagnostic Procedures

Pirfenidone and nintedanib each exceed USD 94,000 in yearly U.S. acquisition cost, ranking among the highest-priced chronic medications[2]American Journal of Respiratory and Critical Care Medicine, “Cost and Adherence in Antifibrotic Therapy,” atsjournals.org. Medicare Part D coverage comes with USD 3,000–8,000 annual copays, creating financial toxicity that drives non-adherence despite insurance. Cost-effectiveness studies often cite incremental ratios beyond USD 150,000 per QALY, exceeding payer thresholds in most health systems. While European generics cut nintedanib prices by up to 40%, U.S. patents delay domestic relief until 2027. HRCT surveillance, priced at USD 500–1,500 per study, adds cumulative burden when performed serially, particularly for uninsured populations[3]RSNA Radiology, “Economic Burden of Serial HRCT,” rsna.org. High costs create a two-tier global market in which insured patients in developed economies receive therapy, while emerging-market patients remain untreated or rely on corticosteroids despite their limited efficacy.

Limited Availability of ILD Specialty Centers in Emerging Markets

India hosts fewer than 50 multidisciplinary ILD units for a population of 1.4 billion, forcing long-distance travel for diagnostic workups. Rural Chinese provinces similarly lack HRCT infrastructure, concentrating expertise in Beijing, Shanghai, and Guangzhou. Sub-Saharan Africa’s shortage is starker: South Africa operates fewer than 10 dedicated clinics, and most neighboring nations have none. COVID-era telemedicine proved conceptually valuable, but reimbursement gaps in emerging markets limit sustainable deployment. Insufficient specialty density also restricts clinical-trial enrollment, slowing regional approvals and perpetuating access disparities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biologics Gain Momentum over Established Antifibrotics

Antifibrotic agents delivered 54.43% of interstitial lung disease market share in 2025, anchored by pirfenidone and nintedanib reimbursement status across major economies. However, biologics and targeted small molecules are expected to grow at 9.54% CAGR, the highest among classes, propelled by approvals such as tocilizumab for systemic sclerosis-ILD and nerandomilast’s entry into the idiopathic segment.

Generic erosion in Europe and anticipated U.S. patent cliffs pressure antifibrotic margins, while precision therapies command premium pricing justified by superior mechanism-specific outcomes. Immunomodulators such as mycophenolate are used off-label but lack formal label expansion, limiting upside. Oxygen and other supportive-care products follow prescription trends but generate lower revenue per patient. As payer policies tilt toward biomarker-defined coverage, manufacturers with targeted portfolios are positioned for faster uptake.

By Disease Type: Autoimmune-Linked ILDs Accelerate on Label Expansions

Idiopathic pulmonary fibrosis contributed 42.45% of the interstitial lung disease market size in 2025, reflecting its higher prevalence and guideline-driven therapy uptake. Systemic sclerosis-associated ILD, however, is slated for a 9.44% CAGR through 2031 on the back of tocilizumab’s approval and ongoing nintedanib label broadening.

Rheumatoid arthritis-ILD and dermatomyositis-ILD remain underserved; the lack of approved drugs leaves a sizable opportunity for targeted biologics. Chronic fibrotic hypersensitivity pneumonitis is gradually transitioning from antigen-avoidance to pharmacologic management as off-label antifibrotic use becomes widespread. Rare phenotypes such as sarcoidosis-associated fibrosis benefit from orphan incentives, drawing smaller developers into narrow but profitable niches.

By Diagnosis Modality: Non-Invasive Monitoring Platforms Gain Ground

High-resolution CT equipment generated 38.65% of segment revenue in 2025, but replacement cycles in mature Western markets temper unit growth. Pulmonary function testing devices are projected to rise at 9.65% CAGR, driven by portable spirometry and diffusing-capacity gadgets that fit telehealth workflows.

Quantitative AI software increasingly bundles with imaging hardware, shifting value from per-scan interpretations to subscription analytics. While tissue biopsy remains the tie-breaker in ambiguous diagnoses, cryobiopsy’s favorable safety profile versus surgical methods is scaling adoption in academic hospitals. Blood-based biomarkers may soon enable primary-care screening, but reimbursement clarity is needed before commercial take-off.

By End-User: Home Care Tilts the Balance Away from Hospitals

Hospitals captured 55.64% of interstitial lung disease market size in 2025 because acute exacerbations and initial diagnostics remain center-based. Home-care settings are forecast to expand at 10.23% CAGR, reflecting payer incentives to manage stable patients remotely with oxygen concentrators and Bluetooth oximeters.

Specialty pulmonary clinics associated with academic centers serve high-acuity cohorts who benefit from clinical-trial access and infusion capabilities. Independent imaging centers enjoy steady HRCT demand but face margin pressure as AI slashes interpretation fees. Research institutes and CROs are modest revenue contributors yet vital for trial execution as the pipeline diversifies.

Geography Analysis

North America held 42.56% market share in 2025, supported by Medicare Part D coverage, more than 100 multidisciplinary ILD boards, and FDA pathways that expedite novel approvals. High drug prices inflate revenue per patient, while AI adoption in community hospitals accelerates diagnostic throughput. Canada negotiates lower list prices while expanding biologic reimbursement for systemic sclerosis-ILD, narrowing access gaps relative to the United States. Mexico’s private hospitals offer advanced care to insured populations, but national penetration remains limited by out-of-pocket payment models.

Europe presents a patchwork of reimbursement: Germany provides swift access following EMA authorization, whereas the United Kingdom’s NICE subjects new entrants to a stringent cost-effectiveness evaluation. Generic nintedanib reduced European price points by up to 40%, pressuring branded margins but boosting volume in cost-sensitive health systems. Eastern European nations struggle with limited ILD infrastructure, despite progressive disease burden, underscoring a need for pan-regional capacity-building and tele-diagnostic solutions.

Asia-Pacific is projected to grow at an 8.54% CAGR as China scales pulmonary subspecialty programs and India’s private sector addresses unmet diagnostic demand. Japan’s early adoption of antifibrotics and proactive geriatric policies keeps prevalence management ahead of regional peers. Tier-2 Chinese cities and rural provinces lack HRCT coverage, so portable spirometry and tele-consult platforms are critical for market capture. Australia and South Korea mirror Western reimbursement patterns but have smaller patient pools.

Competitive Landscape

Boehringer Ingelheim and Roche/Genentech together control roughly 60-70% of global antifibrotic and biologic revenue, anchoring a market that remains moderately concentrated. European generics from Accord and Viatris accelerated price competition but have yet to dent the U.S. due to patent coverage through 2027.

Smaller biotechs such as Pliant Therapeutics and FibroGen pursue mechanism-specific programs and typically partner for late-stage commercialization or ex-U.S. rights. Imaging vendors—including Siemens Healthineers, Philips, and VIDA Diagnostics—compete on AI integration, offering subscription models that align with hospitals’ operating-expense budgets.

White-space opportunities center on autoimmune-associated ILDs, home-care monitoring devices, and blood-based biomarkers. Regulatory incentives make phenotype-specific niche markets economically viable for venture-backed entrants, suggesting that the interstitial lung disease market will fragment into indication-focused clusters rather than re-consolidate under a few broad portfolios.

Interstitial Lung Disease Industry Leaders

Boehringer Ingelheim

F. Hoffmann-La Roche Ltd

Siemens Healthineers

Koninklijke Philips N.V.

United Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Boehringer Ingelheim’s JASCAYD (nerandomilast) tablets have been approved by the U.S. Food and Drug Administration (FDA) as an oral treatment option for idiopathic pulmonary fibrosis (IPF) in adult patients.

- August 2025: PureTech Health plc, a clinical-stage biotherapeutics company dedicated to changing the lives of patients with devastating diseases, launched a new entity, Celea Therapeutics. Celea's mission is to deliver therapies that transform the lives of people with serious respiratory diseases.

- May 2023: Bellerophon Therapeutics LLC completes phase 3 study for fibrotic interstitial lung disease drug.

Global Interstitial Lung Disease Market Report Scope

As per the scope of the report, interstitial lung disease (ILD) refers to a group of lung disorders characterized by inflammation and scarring of the interstitial tissue, which surrounds the alveoli. This leads to reduced lung elasticity, impaired gas exchange, and progressive breathing difficulties. Causes can include environmental exposures, autoimmune diseases, or idiopathic factors.

The Interstitial Lung Disease Market is Segmented by Drug Class (Antifibrotic Agents, Immunomodulators & Corticosteroids, Biologics & Targeted Therapies, Oxygen & Supportive Care, and Other Drug Classes), Disease Type (Idiopathic Pulmonary Fibrosis, Systemic-Sclerosis Associated ILD, Rheumatoid-Arthritis Associated ILD, Hypersensitivity Pneumonitis, and Other Disease Types), Diagnosis Modality (HRCT Imaging Equipment, Quantitative Imaging & AI Software, Pulmonary Function Testing Devices, Blood-Based Biomarkers, and Lung Biopsy), End-User (Hospitals, Specialty Pulmonary Clinics, Diagnostic Imaging Centres, Home-Care Settings, and Research Institutes & CROs), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Antifibrotic Agents |

| Immunomodulators & Corticosteroids |

| Biologics & Targeted Therapies |

| Oxygen & Supportive Care |

| Other Drug Classes |

| Idiopathic Pulmonary Fibrosis (IPF) |

| Systemic-Sclerosis Associated ILD |

| Rheumatoid-Arthritis Associated ILD |

| Hypersensitivity Pneumonitis |

| Other Disease Types |

| HRCT Imaging Equipment |

| Quantitative Imaging & AI Software |

| Pulmonary Function Testing Devices |

| Blood-Based Biomarkers |

| Lung Biopsy (Surgical & Cryobiopsy) |

| Hospitals |

| Specialty Pulmonary Clinics |

| Diagnostic Imaging Centres |

| Home-Care Settings |

| Research Institutes & CROs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Drug Class | Antifibrotic Agents | |

| Immunomodulators & Corticosteroids | ||

| Biologics & Targeted Therapies | ||

| Oxygen & Supportive Care | ||

| Other Drug Classes | ||

| By Disease Type | Idiopathic Pulmonary Fibrosis (IPF) | |

| Systemic-Sclerosis Associated ILD | ||

| Rheumatoid-Arthritis Associated ILD | ||

| Hypersensitivity Pneumonitis | ||

| Other Disease Types | ||

| By Diagnosis Modality | HRCT Imaging Equipment | |

| Quantitative Imaging & AI Software | ||

| Pulmonary Function Testing Devices | ||

| Blood-Based Biomarkers | ||

| Lung Biopsy (Surgical & Cryobiopsy) | ||

| By End-User | Hospitals | |

| Specialty Pulmonary Clinics | ||

| Diagnostic Imaging Centres | ||

| Home-Care Settings | ||

| Research Institutes & CROs | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How fast is the interstitial lung disease market expected to grow through 2031?

It is projected to expand at a 7.53% CAGR, moving from USD 2.21 billion in 2026 to USD 3.17 billion by 2031.

Which drug classes are growing the quickest?

Biologics and targeted small molecules lead with a 9.54% CAGR due to approvals such as tocilizumab and nerandomilast.

Why are home-care settings drawing investment?

Portable oxygen concentrators and remote oximetry enable stable patients to be monitored outside hospitals, supporting a 10.23% CAGR for the home-care segment.

What regions hold the greatest growth potential?

Asia-Pacific shows the fastest regional expansion at 8.54% CAGR, driven by infrastructure upgrades in China and India.

How are generics influencing therapy costs?

Generic nintedanib cut European prices by up to 40%, creating pricing pressure on branded antifibrotics while broadening access.

Which unmet needs remain for patients?

Curative options are lacking, and many patients discontinue therapy due to gastrointestinal side effects, highlighting the need for better-tolerated or disease-reversing treatments.

Page last updated on: