Uterine Fibroids Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

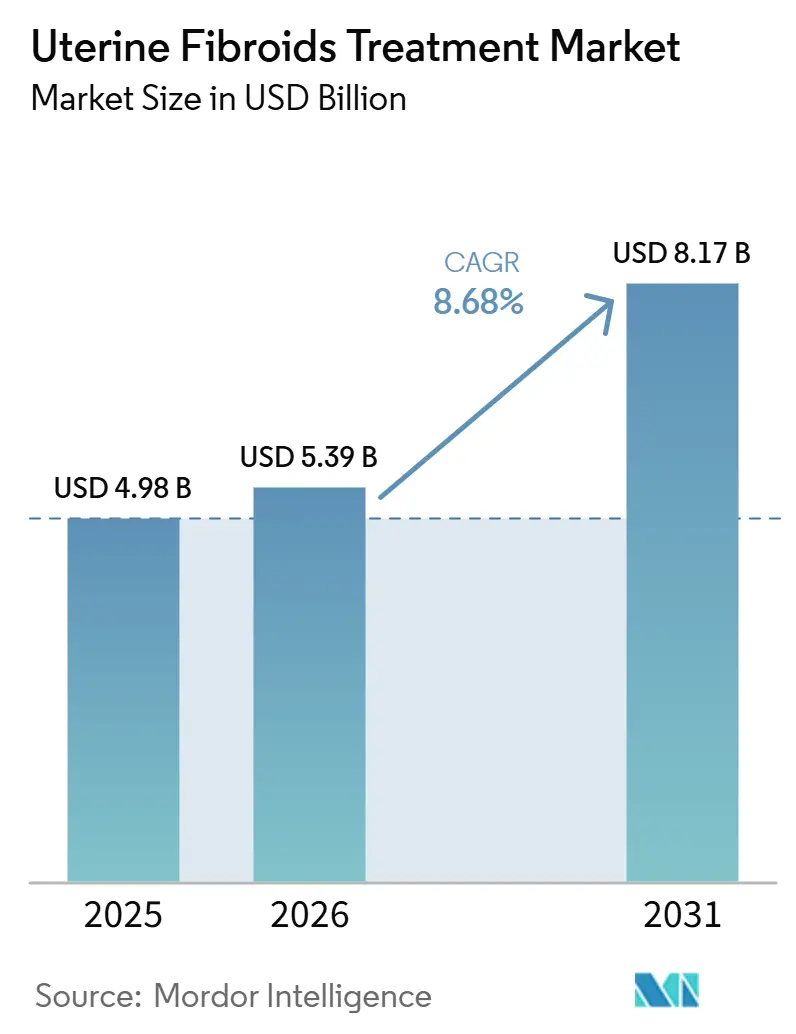

| Market Size (2026) | USD 5.39 Billion |

| Market Size (2031) | USD 8.17 Billion |

| Growth Rate (2026 - 2031) | 8.68% CAGR |

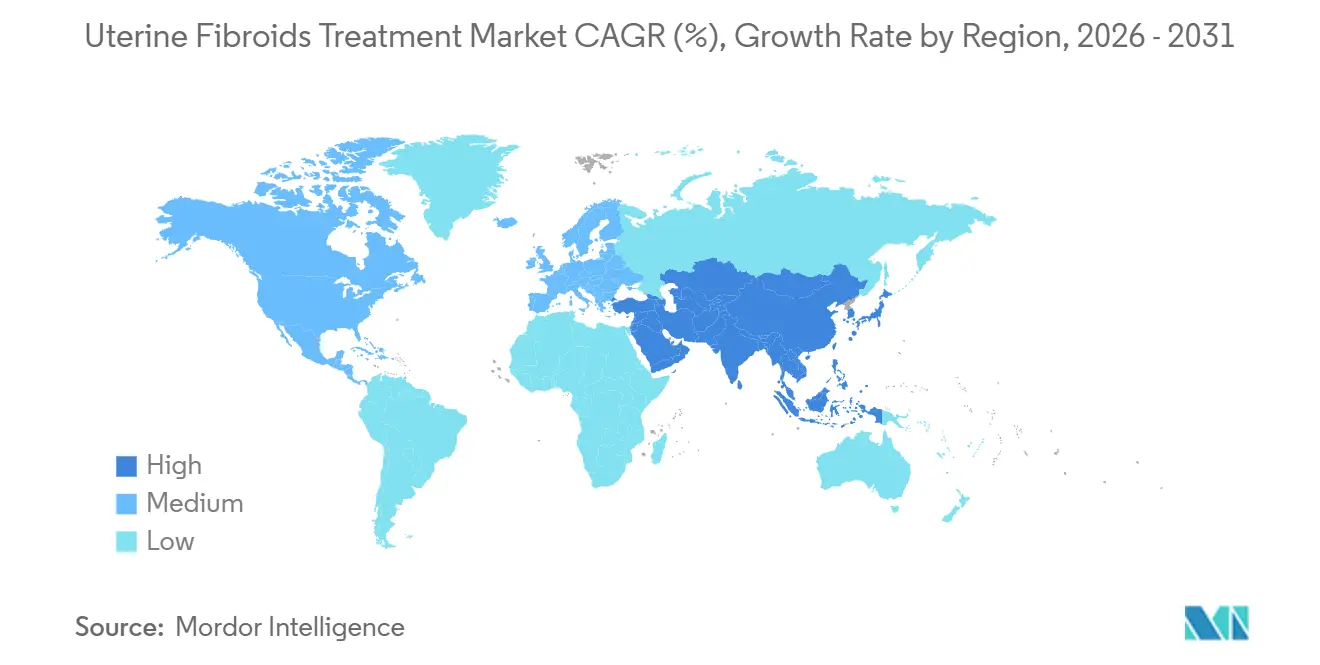

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

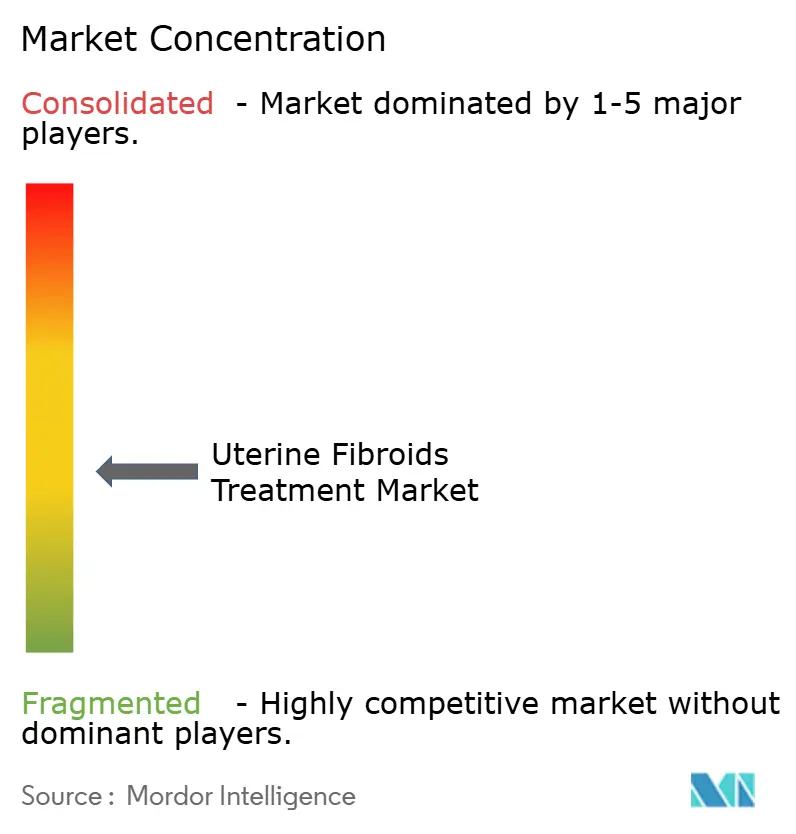

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Uterine Fibroids Treatment Market Analysis by Mordor Intelligence

The Uterine Fibroids Treatment Market size is expected to grow from USD 4.98 billion in 2025 to USD 5.39 billion in 2026 and is forecast to reach USD 8.17 billion by 2031 at 8.68% CAGR over 2026-2031.

Rising prevalence of symptomatic leiomyomas among women in their thirties, rapid uptake of uterus-preserving procedures, and expanded payer coverage for oral GnRH antagonists are widening the addressable patient base. Hospitals are modernizing operating suites with AI-enabled robotic systems that shorten operative time, while ambulatory chains are bundling imaging and interventional radiology to speed the patient pathway. Manufacturers are embedding machine learning into focused ultrasound and embolization platforms, lowering the skill threshold for physicians and enabling scale-up in underserved regions. Supply-chain fragility for embolic agents and MRI contrast media remains a headline risk, yet diversification strategies by large vendors have begun to ease shortages.

Key Report Takeaways

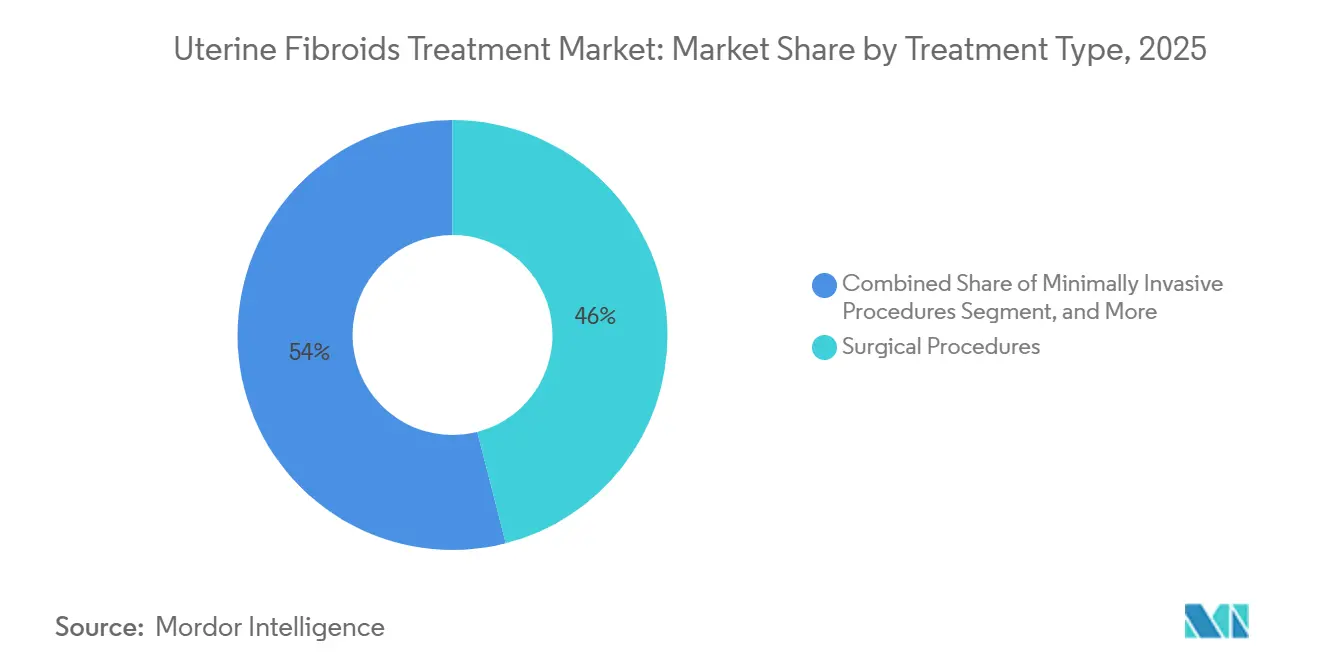

- By treatment type, surgical procedures held 46.02% of uterine fibroids treatment market share in 2025, while non-invasive procedures are projected to advance at a 9.06% CAGR through 2031.

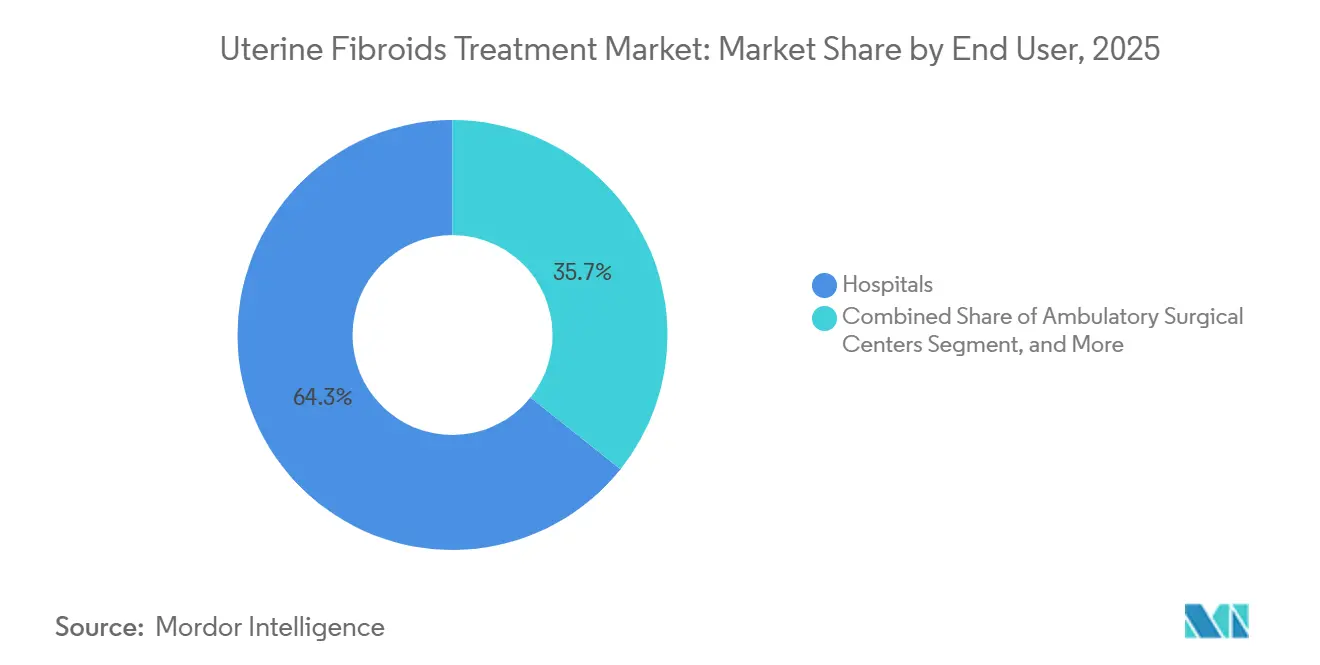

- By end user, hospitals accounted for 64.27% market share in 2025, yet specialty gynecology clinics are forecast to grow at an 11.63% CAGR over 2026-2031.

- By geography, North America accounted for 41.78% of global revenue in 2025, whereas Asia-Pacific is expected to record the fastest growth at a 10.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Uterine Fibroids Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Among Women and Earlier Diagnostic Rates | +1.8% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Shift From Hysterectomy Toward Minimally and Non-Invasive Procedures | +2.1% | North America and Europe lead; Asia-Pacific adoption accelerating | Medium term (2-4 years) |

| Regulatory Approvals and Reimbursement Expansion for Novel Drugs | +1.5% | North America, Europe, Japan; emerging in China and India | Short term (≤ 2 years) |

| Rapid Technology Advances in Image-Guided Ablation and Robotic-Assisted Surgery | +1.3% | North America, Western Europe, select Asia-Pacific hubs | Long term (≥ 4 years) |

| AI-Driven Treatment-Planning Software Improving Procedure Throughput | +0.9% | North America, Europe, Japan, technologically advanced Asia-Pacific markets | Medium to Long term (3–5 years) |

| Decentralised Tele-Gynecology Models Boosting Access in Emerging Markets | +0.7% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Among Women And Earlier Diagnostic Rates

Symptomatic fibroids now affect about 70-80% of women by age 50, and point-of-care ultrasound is expanding early detection in primary care. Portable scanners priced below USD 10,000 are becoming routine in gynecology offices across the United States and Europe.[1]Centers for Disease Control and Prevention, “Fibroid-Related Hospitalization Trends,” CDC, cdc.gov Earlier diagnosis steers younger patients toward fertility-preserving options such as radiofrequency ablation, which reduces future hysterectomy rates. The shift expands the pool of candidates for device-based outpatient care. Manufacturers that bundle imaging and therapy are therefore capturing a larger share of the wallet. Payers benefit when early treatment averts costly emergency admissions.

Shift From Hysterectomy Toward Minimally And Non-Invasive Procedures

U.S. hysterectomy volumes for fibroids fell from roughly 200,000 in 2020 to an estimated 165,000 in 2025, while uterine artery embolization and MR-guided focused ultrasound grew in double digits.[2]American College of Obstetricians and Gynecologists, “2024 Clinical Guidance on Fibroid Management,” ACOG, acog.org Updated clinical guidelines require physicians to present uterus-sparing alternatives first. Robotic myomectomy now accounts for more than 40% of all myomectomies at academic centers, citing lower blood loss and faster recovery. Payers increasingly reward same-day discharge, which gives outpatient centers a margin advantage. The trend also stimulates demand for advanced imaging in pre-operative planning.

Regulatory Approvals And Reimbursement Expansion For Novel Drugs

Medicare and several European health systems covered GnRH antagonists such as Oriahnn and Myfembree for pre-operative fibroid shrinkage in 2025.[3]European Medicines Agency, “Reimbursement Decision for Myfembree,” EMA, ema.europa.eu Access to reimbursed oral therapy extends disease management options for peri-menopausal women who may bridge to menopause without surgery. Pharmaceutical revenues climbed as label expansions endorsed combination regimens. Reimbursement also accelerates adoption in Japan and drives formulary additions in China and India. Drug makers are funding post-marketing trials that test shorter courses to improve adherence.

Rapid Technology Advances In Image-Guided Ablation And Robotic-Assisted Surgery

INSIGHTEC integrated predictive algorithms into its Exablate platform, reducing focused ultrasound sessions from 4 hours to under 2. Intuitive Surgical’s da Vinci 5 added real-time tissue recognition, which trims operative time by up to 20%. Faster case throughput improves the return on million-dollar capital assets. Hospitals in Singapore and South Korea now schedule two MR-guided ablations per MRI suite each day, doubling prior productivity. Capital investment is further justified because AI helps junior surgeons execute complex cases safely.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Cost of MRgFUS and Robotic Systems | -1.2% | Global, most acute in emerging markets and rural hospitals in developed regions | Long term (≥ 4 years) |

| Adverse Effects & Discontinuation Rates of Long-Term Hormonal Therapy | -0.8% | Global, particularly North America and Europe where oral GnRH antagonists are widely prescribed | Short term (≤ 2 years) |

| Limited Trained Interventional Radiologists in Low-Income Regions | -0.6% | Sub-Saharan Africa, South Asia, parts of Latin America | Long term (≥ 4 years) |

| Global Contrast-Media & Embolic-Agent Supply-Chain Fragility | -0.5% | Global, with acute shortages in Europe and Asia-Pacific during 2024-2025 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital And Maintenance Cost Of MRgFUS And Robotic Systems

Focused-ultrasound units list between USD 2 million and USD 3 million, while robotic platforms often top USD 2 million, and service contracts add USD 150,000 annually. Community hospitals, therefore, defer purchases in favor of core imaging upgrades. In India and China, public hospitals prefer radiofrequency devices that cost nearly ten times less. The price gap creates a two-tier landscape where urban elites access high-end technology, while rural women rely on conventional surgery. Vendors now offer leasing and pay-per-use models, yet bank financing in low-income countries remains limited.

Adverse Effects And Discontinuation Rates Of Long-Term Hormonal Therapy

GnRH antagonists can prompt vasomotor symptoms and bone density decline, leading 30-35% of patients to stop therapy within a year. Add-back estrogen reduces side effects, but real-world adherence still lags. A 2025 multicenter study found that only 52% of women completed the recommended six-month course. Early drop-out curbs drug revenue and reduces effectiveness as a standalone solution. Pharmaceutical firms are testing three-month regimens and exploring selective progesterone modulators to improve tolerability. Regulators are unlikely to clear new protocols before 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Non-Invasive Momentum Outpaces Surgical Dominance

Surgical interventions held 46.02% of the uterine fibroids treatment market share in 2025, underscoring the legacy role of hysterectomy and open myomectomy. The segment is losing ground relative to payer policies that favor uterus preservation and shorter hospital stays. Non-invasive modalities are projected to post a 9.06% CAGR to 2031, the fastest within the therapeutic mix. Focused-ultrasound adoption accelerates when hospitals can schedule multiple cases per imaging suite, which boosts asset utilization. Minimally invasive procedures, including uterine artery embolization and radiofrequency ablation, remain vital in regions lacking MR-compatible theaters. Medication-based therapy captures niche demand for women approaching menopause but faces adherence headwinds that limit penetration.

North America and Western Europe lead non-invasive deployments because reimbursement covers MR-guided systems, while Asia-Pacific markets often combine radiofrequency ablation with ultrasound guidance to lower costs. INSIGHTEC reported a 35% jump in U.S. Exablate volumes during 2025 after academic centers marketed the technology as incision-free outpatient care. Surgical procedure volume is gradually shifting from open to robotic myomectomy, yet the capital burden tempers uptake in community hospitals. Minimally invasive options serve as a cost-effective middle path, especially in Latin America, where disposable income is lower. Medication-based care gains traction in Japan and South Korea, where cultural norms often favor pharmacologic management over surgery.

By End User: Specialty Clinics Accelerate The Ambulatory Shift

Hospitals generated 64.27% of total procedures in 2025 because they integrate imaging, surgery, and post-operative monitoring under one roof. Yet specialty gynecology clinics are forecast to expand at a 11.63% CAGR through 2031 as private equity funds back ambulatory networks. These clinics compress diagnostic and treatment pathways, improving patient satisfaction and reducing payer costs. Ambulatory surgical centers appeal to millennials seeking same-day discharge and transparent pricing. Hospitals maintain a stronghold for large or multiple fibroids that require robotic or open surgery, though referral patterns increasingly steer routine cases elsewhere.

Tele-gynecology platforms in India triage rural women and route them to urban specialty centers, boosting clinic footfall while lowering wait times. North American clinics partner with payers to accept bundled payments that cover imaging, embolization, and follow-up on a single invoice. Middle East facilities leverage medical tourism flows to fill high-margin MR-guided ablation slots. Hospitals counter by launching dedicated fibroid centers that combine reproductive endocrinology, radiology, and surgery in a single program. The tug-of-war for volume incentivizes all players to adopt AI dashboards that track outcomes in real time.

Geography Analysis

North America captured 41.78% of global revenue in 2025, supported by broad insurance coverage for the full continuum from oral therapy through robotic surgery. The United States alone performs about 600,000 fibroid-related procedures each year, though growth is moderating as minimally invasive penetration matures. Canada expands access through provincial programs that fund uterine artery embolization, while Mexico combines private clinics with public initiatives to widen screening. Europe ranks second by value, with Germany, France, and the United Kingdom leading the adoption of focused ultrasound and robotic platforms. National health systems recognize that uterus-preserving care lowers lifetime expenditure compared with hysterectomy.

Asia-Pacific is projected to post a 10.27% CAGR from 2026 to 2031, the fastest worldwide, as urbanization and rising disposable incomes broaden demand. China’s national screening initiative aims to raise the diagnosis rate among women aged 30-50 by 25% before 2027. India’s tele-gynecology networks close primary care gaps and funnel patients to specialty clinics that offer embolization and focused ultrasound. Japan and South Korea support medication-based regimens through national insurance, yet demographic aging tempers volume growth. Australia positions itself as a training hub for MR-guided ultrasound, attracting clinicians from Southeast Asia.

The Middle East and Africa display a fragmented landscape. Gulf Cooperation Council nations invest in robotic and focused-ultrasound capacity to anchor medical tourism. Sub-Saharan Africa lacks trained interventional radiologists, so hysterectomy rates remain high, although pilot tele-gynecology projects in Kenya and Nigeria improve diagnosis. South Africa hosts academic centers that perform embolization and laparoscopic myomectomy, but public budgets limit expansion. Supply-chain strain for embolic microspheres during 2024-2025 exposed the vulnerability of smaller markets that rely on imports.

South America divides into private-sector growth in Brazil, Argentina, and Chile, and constrained public-sector access elsewhere. Brazil’s national system reimburses hysterectomy but not MR-guided procedures, so affluent patients self-pay at private hospitals. Argentina expanded coverage for robotic myomectomy in 2025 following advocacy by surgical societies. Chile pilots tele-gynecology outreach in rural provinces, which may unlock latent demand once funding stabilizes. Overall, the growth of the uterine fibroids treatment market in the region hinges on regulatory progress and currency stability.

Competitive Landscape

The uterine fibroids treatment market exhibits moderate fragmentation as pharmaceutical, device, and service companies compete across overlapping niches. AbbVie and Myovant dominate the oral GnRH antagonist segment, leveraging large sales forces and post-marketing studies to secure formulary placements. Boston Scientific and Medtronic lead embolization and radiofrequency spaces after each firm broadened portfolios through targeted acquisitions. INSIGHTEC and Profound Medical specialize in MR-guided focused ultrasound and capitalize on the non-invasive value proposition that resonates with urban patients.

Intuitive Surgical’s da Vinci franchise integrates AI to map fibroid capsules in real time, which differentiates the platform and secures premium pricing. Smaller entrants such as Gynesonics and Minerva Surgical target ambulatory centers with low-cost radiofrequency devices that require minimal capital outlay. Imaging partners Philips Healthcare and Siemens Healthineers embed AI segmentation tools that feed into treatment-planning software, tightening ecosystem control. Tele-gynecology aggregators in India and China negotiate bulk pricing with device makers in exchange for guaranteed case volumes, a strategy that could reshape procurement norms.

White-space opportunities include hybrid protocols that pair short-course medication with outpatient ablation to reduce recurrence. Vendors also explore disposable instrument kits that fit existing laparoscopic towers to lower per-case costs. Lack of harmonized global standards for MR-guided systems permits regional players to gain footholds before multinational approvals. Intellectual property filings around AI tissue mapping suggest an arms race for software differentiation. Service providers that can demonstrate real-time outcomes via cloud dashboards strengthen bargaining power with payers.

Uterine Fibroids Treatment Industry Leaders

Medtronic

Myovant Sciences GmbH

Boston Scientific Corporation

Gynesonics Inc.

INSIGHTEC Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Apotex secured exclusive Canadian rights to Linzagolix for uterine fibroid therapy.

- May 2025: TiumBio and Daewon Pharmaceutical completed Phase 2 trials of Merigolix (TU2670/DW4902) for uterine fibroids.

- January 2025: Hologic completed its USD 350 million acquisition of Gynesonics, adding the Sonata transcervical ablation platform to its minimally invasive portfolio.

Global Uterine Fibroids Treatment Market Report Scope

As per the scope of this report, uterine fibroids, also known as uterine myomas or leiomyomas, are non-cancerous tumors that develop in the muscular wall of the uterus. They can vary in size and number. Symptoms include heavy menstrual bleeding (HMB), anemia, abdominal pressure and pain, bloating, increased urinary frequency, and reproductive dysfunction.

The uterine fibroids treatment market is segmented by type, treatment, end user, and geography. The type segment is further segmented into subserosal fibroids, intramural fibroids, submucosal fibroids, pedunculated fibroids, and other types. Other types include cervical fibroids. The treatment segment is further divided into drugs and surgical techniques. The drugs sub-segment is further divided into progesterone, levonorgestrel, and other drugs. Other drugs include mefenamic acid and raloxifene. The surgical techniques are further divided into hysterectomy, myomectomy, myolysis, and other surgical techniques. Other surgical techniques include uterine artery embolization (UAE) and radiofrequency ablation (RFA). The end user segment is further bifurcated into hospitals, specialty clinics, and other end users. Other end-user segments include outpatient centers, home healthcare services, and telemedicine platforms. The geography segment is further segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD) for the above segments.

| Medication-Based Treatments |

| Surgical Procedures |

| Minimally Invasive Procedures |

| Non-Invasive Procedures |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Gynecology Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Medication-Based Treatments | |

| Surgical Procedures | ||

| Minimally Invasive Procedures | ||

| Non-Invasive Procedures | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Gynecology Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the uterine fibroids treatment market in 2031?

It is expected to reach USD 8.17 billion by 2031, rising from USD 5.39 billion in 2026.

Which treatment category is growing fastest toward 2031?

Non-invasive procedures such as MR-guided focused ultrasound are forecast to grow at a 9.06% CAGR between 2026 and 2031.

Why are specialty gynecology clinics gaining procedure share?

Private-equity funding, bundled care models, and tele-gynecology referrals allow clinics to deliver same-day, uterus-preserving procedures at lower cost than hospitals.

What limits adoption of AI-enabled robotic systems in emerging markets?

Upfront capital exceeding USD 2 million and high annual service fees deter smaller hospitals and favor lower-cost radiofrequency platforms.

How are supply-chain risks being mitigated after 2025 shortages?

Device makers diversified embolic-agent sources and launched next-generation microspheres designed to reduce aggregation during shipment.

Page last updated on: