Behcet's Disease Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

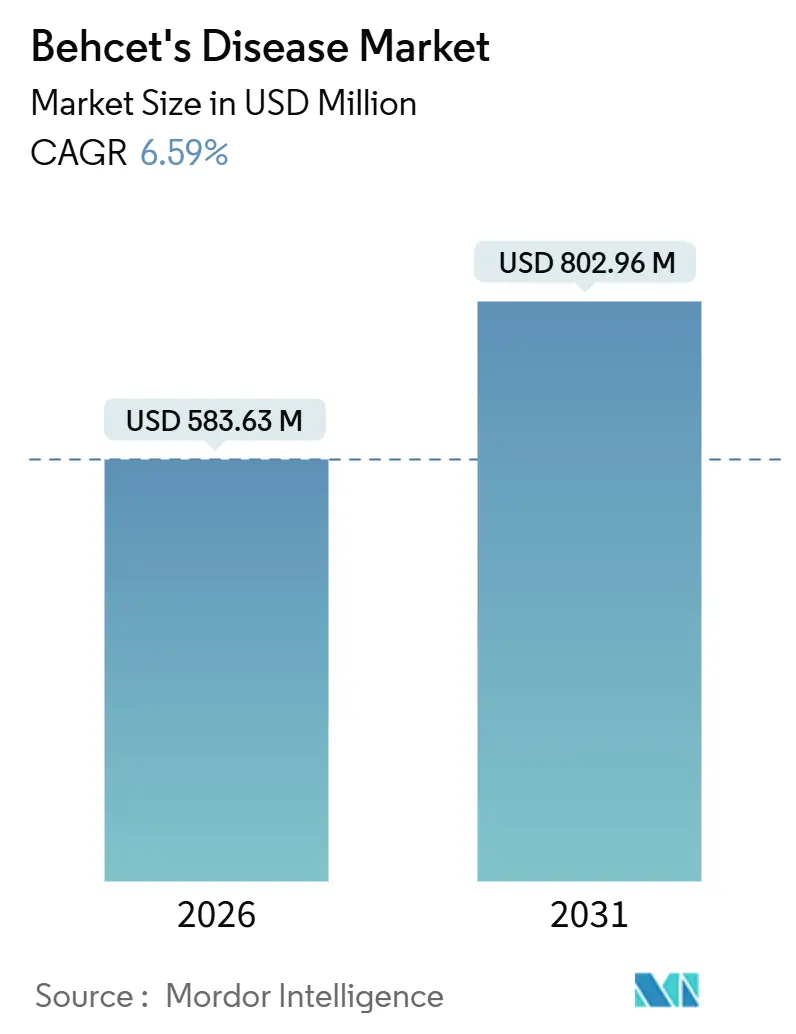

| Market Size (2026) | USD 583.63 Million |

| Market Size (2031) | USD 802.96 Million |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

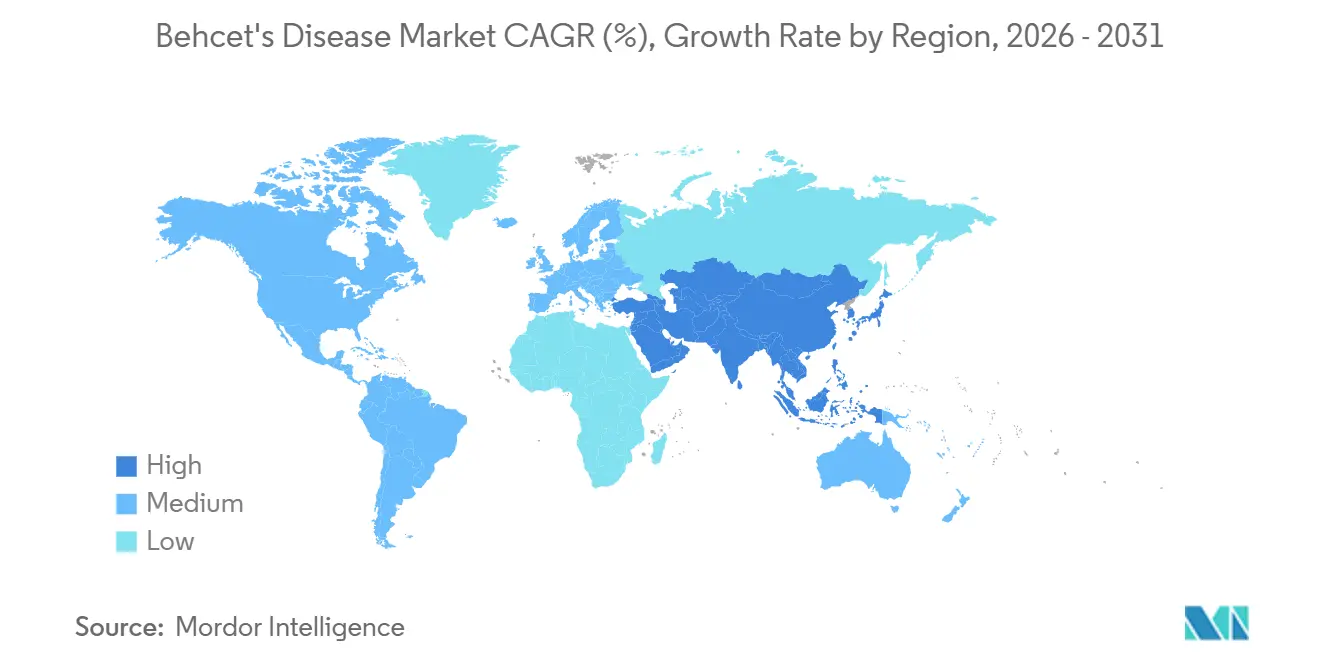

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Behcet's Disease Market Analysis by Mordor Intelligence

The Behcet's Disease Market size is estimated at USD 583.63 million in 2026, and is expected to reach USD 802.96 million by 2031, at a CAGR of 6.59% during the forecast period (2026-2031).

Accelerators include broader orphan-drug incentives, expanding TNF-biosimilar availability that trims average biologic prices by 30% to 40%, and faster physician uptake of treat-to-target protocols now embedded in Turkish and Japanese registries. Conventional immunosuppressants still dominate early-line use, but real-world remission data with infliximab and adalimumab are tilting prescribing toward biologics, particularly in the Asia-Pacific. Parallel growth arises from digital prior-authorization platforms that push dispensing to specialty and online pharmacies, while subcutaneous self-injection devices bolster adherence among working-age patients. Collectively, these shifts are reshaping competitive strategy, with innovators racing to differentiate through oral JAK and TYK2 inhibitors as the next wave of targeted therapy.

Key Report Takeaways

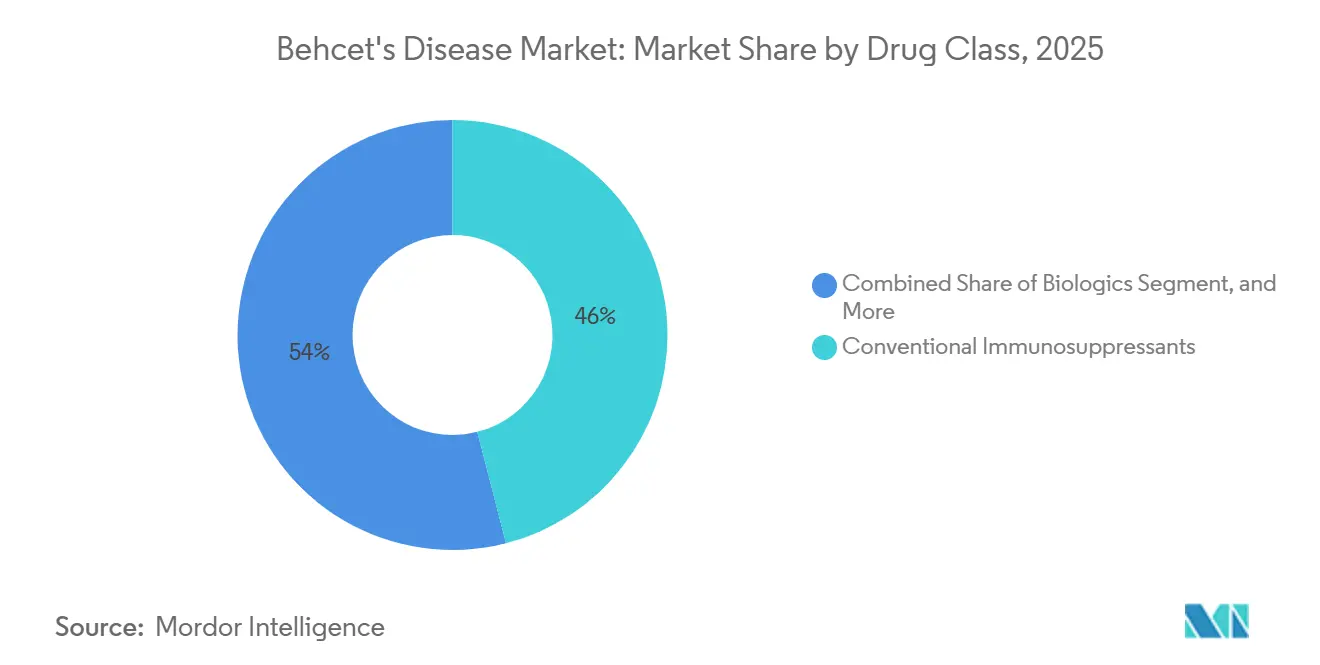

- By drug class, conventional immunosuppressants held 46.01% of the Behçet's disease market share in 2025, while biologics are expanding at a 7.48% CAGR through 2031.

- By route of administration, oral formulations accounted for 49.37% of the Behçet's disease market in 2025; subcutaneous delivery is advancing at an 8.21% CAGR through 2031.

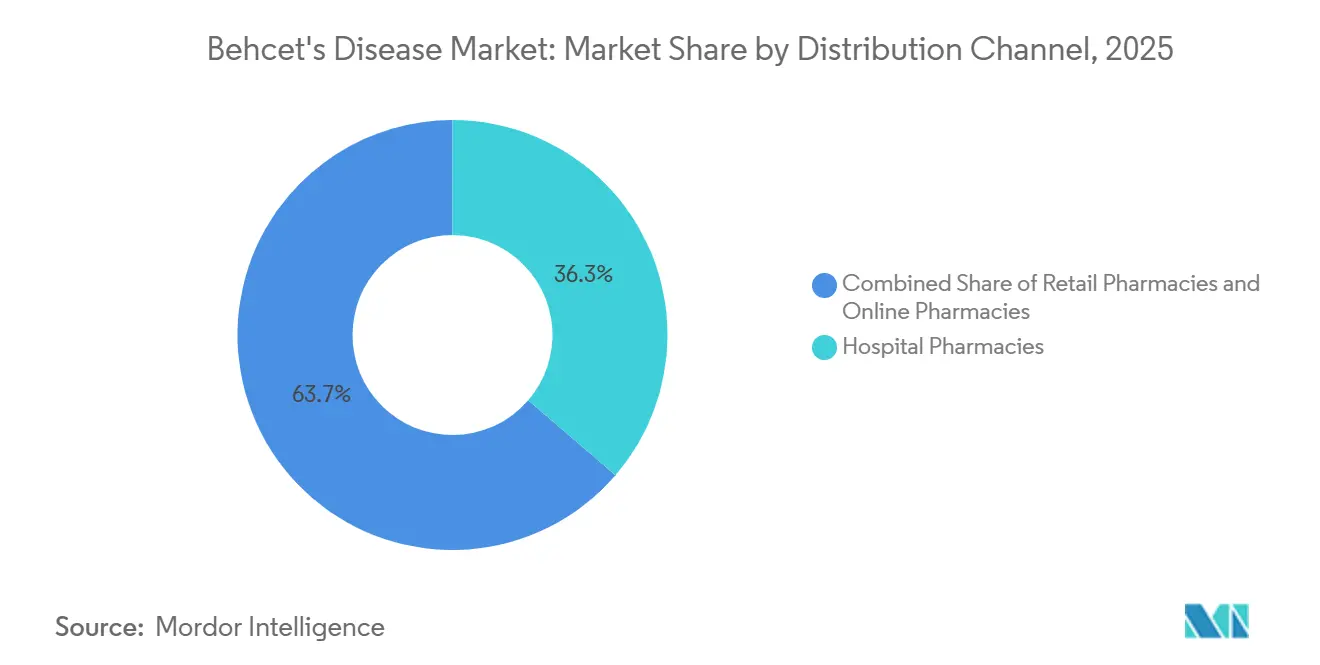

- By distribution channel, hospital pharmacies accounted for 36.32% of revenue in 2025, while online pharmacies are growing at a 10.22% CAGR through 2031.

- By geography, North America accounted for 39.03% of revenue in 2025, and Asia-Pacific is forecast to post the fastest CAGR of 9.83% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Behcet's Disease Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Biologic Therapies | +1.2% | Global, with APAC and MEA acceleration | Medium term (2-4 years) |

| Increasing Diagnostic Rates Through Specialist Guidelines | +0.9% | North America, Europe, Japan | Short term (≤ 2 years) |

| Orphan-Drug Incentives in Major Markets | +0.7% | North America, EU | Long term (≥ 4 years) |

| Expansion of Silk-Road Ocular Treat-To-Target Protocols | +0.8% | Turkey, Iran, Central Asia, GCC | Medium term (2-4 years) |

| Real-World Registries in Japan & Turkey Accelerating Payer Acceptance | +0.6% | Japan, Turkey, spill-over to South Korea | Medium term (2-4 years) |

| TNF-Biosimilar Pricing Unlocking Latent Demand | +1.1% | Europe, APAC, South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Biologic Therapies

Biologics are redefining the standard of care because infliximab and adalimumab achieve higher remission in refractory uveitis and mucocutaneous disease than azathioprine or cyclosporine. Phase 3 trials continue to validate IL-23 and IL-17 inhibitors, and small Japanese cohorts already document baricitinib-mediated remission after TNF failure.[1]National Institutes of Health, “Behçet's Disease,” NCBI, ncbi.nlm.nih.gov Subcutaneous pens reduce clinic visits, and Turkish reimbursement of adalimumab biosimilars in 2024 spurred a 25% surge in biologic prescriptions within six months. Home injection aligns with younger demographics, further amplifying uptake. Together, these elements widen treated prevalence and lift revenue visibility despite biosimilar price compression.

Increasing Diagnostic Rates Through Specialist Guidelines

Global rheumatology and ophthalmology bodies now embed the 2014 International Criteria for Behçet's Disease into continuing-education modules, raising diagnostic sensitivity to 94.8%. Japan’s 2020 intestinal guidelines distinguish ileocecal Behçet's from Crohn’s disease using endoscopic scoring, reducing misclassification by 15%. Earlier recognition shortens the path to biologic initiation, limits irreversible ocular damage, and boosts payer willingness to fund higher-value therapies. Telemedicine pilots in the United States extend specialist reach into rural communities, compressing time-to-diagnosis and underscoring the clinical imperative for prompt biologic escalation.

Orphan-Drug Incentives in Major Markets

Seven-year U.S. and ten-year EU exclusivity windows de-risk investment in rare-disease assets. In August 2025, the FDA granted orphan status for dusquetide, waiving user fees and granting tax credits, underscoring regulatory support for niche indications.[2]ClinicalTrials.gov, “Baricitinib in Behçet’s Disease,” clinicaltrials.gov Similar incentives historically benefited gevokizumab and apremilast, and emerging players such as Dianthus Therapeutics plan to leverage the pathway for FcRn-targeted antibodies. By reducing development cost and sharpening investor appetite, these policies sustain long-run innovation despite modest patient numbers.

TNF-Biosimilar Pricing Unlocking Latent Demand

Adalimumab and infliximab biosimilars entered Europe in 2024 at up to 40% discounts, and U.S. launches replicated the pattern in 2025.[3]U.S. Food and Drug Administration, “Adalimumab Biosimilar Products,” fda.gov South Korea, Australia, and Brazil witnessed rapid formulary inclusion, lowering annual per-patient costs by USD 7,000 to USD 9,000 and converting price-sensitive patients to active therapy. Pharmacy-benefit managers strengthen momentum by steering prescriptions toward biosimilars with lower co-pays, pushing biosimilar share above 55% of new TNF starts by late 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Biologics Limiting Access | -0.8% | APAC (ex-Japan), MEA, South America | Medium term (2-4 years) |

| Infection-Monitoring Burden for Long-Term Immunosuppression | -0.5% | Global | Long term (≥ 4 years) |

| Paradoxical IL-17 Flares Dampening Prescriber Confidence | -0.3% | North America, Europe | Short term (≤ 2 years) |

| Fragmented Eurasian Reimbursement & HTA Pathways | -0.6% | Russia, Central Asia, Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Biologics Limiting Access

Annual biologic therapy costs of USD 20,000 to USD 60,000 outstrip average incomes in many Silk Road countries. Even with partial coverage, Turkish patients face co-pays up to USD 5,000, while China’s provincial spending caps prompt mid-year therapy interruptions when budget ceilings are reached. Patient-assistance programs exist but require complex enrollment, widening urban-rural disparities. Until biosimilar competition fully normalizes pricing, affordability remains a structural drag on penetration.

Infection-Monitoring Burden for Long-Term Immunosuppression

FDA labeling obliges tuberculosis and hepatitis screening before TNF initiation, adding USD 500 to USD 1,000 in upfront diagnostics per patient. Quarterly laboratory checks and annual radiographs strain under-resourced clinics, and registry data in Turkey still record TB reactivation in 1.2% of treated patients. Fear of opportunistic infection drives 12% discontinuation in Japanese surveys, illustrating how monitoring complexity erodes adherence and constrains long-term market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biologics Capture Momentum From Conventional Agents

Conventional immunosuppressants retained 46.01% of the revenue share in 2025, reflecting their low cost and entrenched first-line use. Yet biologics are advancing at a 7.48% CAGR as payer confidence grows around registry-documented visual-preservation benefits. Biosimilar infliximab and adalimumab erode originator pricing, shrinking the cost differential versus azathioprine or cyclosporine. The Behçet's disease market size attributable to biologics is projected to reach USD 470 million by 2031, driven by broader ophthalmology adoption and emerging oral JAK inhibitors poised to cannibalize injectable use in needle-averse patients.

Second-generation agents, including IL-23, IL-17, and FcRn antibodies, offer organ-specific targeting that could redefine treatment pathways for refractory conditions. Apremilast’s 50% ulcer reduction positions it as a niche add-on, while baricitinib and tofacitinib may command 15% of biologic revenue by 2031 if Phase 3 trials confirm early Japanese case-series efficacy. Together, these entrants reinforce biologics’ trajectory, compressing the therapeutic window for conventional agents and accelerating value migration toward targeted therapies.

By Route of Administration: Subcutaneous Delivery Accelerates on Home-Injection Advantages

Oral therapies accounted for 49.37% of revenue in 2025, but subcutaneous formulations posted the steepest 8.21% CAGR, as patient-centric autoinjectors enhance convenience and adherence. The Behçet's disease market share for intravenous therapy is forecast to decline from 28% in 2025 to 22% by 2031 as health systems pivot away from infusion-center overheads. Device innovation, Bluetooth-enabled pens that record time-stamped injections, allows manufacturers to link adherence analytics with payer outcomes contracts, reinforcing subcutaneous preference.

Upcoming oral JAK and TYK2 agents could recalibrate the mix again by 2031, reclaiming share from injectables if they deliver non-inferior ocular outcomes. Nonetheless, loading-dose algorithms and severe flare management will sustain a residual infusion niche, particularly for complex vascular cases. On balance, self-administration aligns with evolving healthcare policies that favor decentralized treatment, underpinning sustained subcutaneous outperformance.

By Distribution Channel: Specialty-Driven Online Pharmacies Outpace Traditional Outlets

Hospital pharmacies accounted for 36.32% of 2025 revenue, yet online channels are growing fastest at a 10.22% CAGR, as payers route high-cost biologics through digital hubs that manage prior authorization, cold-chain logistics, and adherence coaching. Specialty pharmacies in the United States now fill 70% of Behçet’s biologic prescriptions, leveraging volume rebates to trim net costs by 20% to 30%. The Behçet's disease market size handled by online platforms could exceed USD 300 million by 2031 if EU regulatory harmonization unlocks cross-border dispatch and APAC e-pharmacy rules evolve toward biologic inclusion.

Retail pharmacies remain stable in the conventional-agent space but cede share on biologics as reimbursement models reward outcomes tracking that brick-and-mortar stores rarely provide. Hospital outlets will remain for induction dosing and complex ocular emergencies, though their overall weight in revenue terms continues to slip as self-injection and mail-order distribution expand.

Geography Analysis

North America dominated the Behçet's disease market, accounting for 39.03% of revenue in 2025, on the back of robust private-insurance coverage, concentrated specialist centers, and the pull of orphan-drug exclusivity. The United States saw adalimumab biosimilars capture 55% of new TNF-inhibitor starts by late 2025, demonstrating how payer mandates can rapidly reshape the therapeutic mix. Canada mirrors these shifts, but at a slower pace due to provincial formulary negotiations.

Asia-Pacific delivers the fastest 9.83% CAGR, fueled by Japanese and Turkish registries that validate long-term visual-preservation benefits and by price-aligned biosimilar launches in South Korea and Australia. Turkey’s treat-to-target ocular protocols, adopted nationally in 2024, moved biologic initiation two lines earlier, while Japan’s 2025 registry showed 68% two-year remission on infliximab without corticosteroids. China’s inclusion of infliximab biosimilars in the National Reimbursement Drug List widened access, although provincial spending caps still curtail continuous therapy in rural provinces.

Europe’s trajectory remains uneven. Germany and France reimburse biologics within 3 months for refractory uveitis, whereas Italy and Spain require 6 months of azathioprine step therapy. Eastern Europe lags further; fragmented health-technology-assessment frameworks prolong negotiations, and Russia’s bilateral pricing model stalls national uptake. The Middle East and Africa exhibit endemic prevalence but limited cold-chain capacity beyond GCC states, leaving Saudi Arabia and the UAE as regional growth islands under Vision 2030 funding programs. South America signals potential as Brazil’s ANVISA approved three adalimumab biosimilars in 2025, slicing costs to USD 11,000 per patient and expanding treated prevalence by 40%.

Competitive Landscape

Market concentration is moderate, with biosimilar contenders Amgen, Coherus, and Pfizer eroding share via aggressive contracting; European tender data already show originator infliximab pricing down 35% since 2024. Innovators sustain differentiation through device patents and real-world registries that capture five-year ocular-outcome data, an evidence stream that biosimilars now emulate to level the playing field.

Pipeline assets skew toward oral small molecules. Eli Lilly’s baricitinib and Pfizer’s tofacitinib leverage existing rheumatoid arthritis dossiers to accelerate Behçet’s label expansion, while Soligenix’s dusquetide pursues oral ulcer resolution under orphan exclusivity. Dianthus Therapeutics is developing an FcRn antibody that could enter pivotal trials by 2027, aiming to prevent antibody-mediated flares.

Technology differentiation now centers on smart autoinjectors with connectivity features that transmit adherence metrics to cloud dashboards. Coherus positions YUSIMRY’s high-concentration, citrate-free formulation as a user-friendly alternative to AMJEVITA, while originator Humira counters through bundled nursing support. As patent cliffs loom for device innovations, marketing strategy pivots to integrated patient services rather than molecular novelty alone.

Behcet's Disease Industry Leaders

Soligenix Inc.

F. Hoffmann-La Roche Ltd.

Amgen Inc.

Pfizer Inc.

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Soligenix announced FDA orphan-drug designation for dusquetide (SGX945) targeting Behçet’s oral lesions, conferring seven-year market exclusivity upon approval.

- August 2025: The Turkish Ministry of Health expanded reimbursement to include adalimumab biosimilars for first-line treatment of sight-threatening ocular disease, following registry evidence demonstrating a 40% flare reduction.

Global Behcet's Disease Market Report Scope

Behçet's Disease (also known as Behçet's syndrome) is a rare, chronic, multisystemic, autoinflammatory and autoimmune disorder characterized by recurrent episodes of oral and genital ulcers, uveitis (ocular inflammation), skin lesions (erythema nodosum, pseudofolliculitis, pathergy), and involvement of vascular, gastrointestinal, neurological, and articular systems.

The Behçet's Disease Market Report is Segmented by Drug Class (Biologics, Conventional Immunosuppressants, Corticosteroids, Colchicine & NSAIDs, Pipeline Small-Molecule Modulators), Route of Administration (Oral, Subcutaneous, Intravenous, Topical/Ocular), Distribution Channel (Hospital, Retail, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

| Biologics |

| Conventional Immunosuppressants |

| Corticosteroids |

| Colchicine & NSAIDs |

| Others / Pipeline Small-Molecule Modulators |

| Oral |

| Subcutaneous Injection |

| Intravenous Infusion |

| Topical / Ocular Formulations |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Biologics | |

| Conventional Immunosuppressants | ||

| Corticosteroids | ||

| Colchicine & NSAIDs | ||

| Others / Pipeline Small-Molecule Modulators | ||

| By Route of Administration | Oral | |

| Subcutaneous Injection | ||

| Intravenous Infusion | ||

| Topical / Ocular Formulations | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Behçet's disease market in 2031?

The market is forecast to reach USD 802.96 million by 2031, expanding at a 6.59% CAGR.

Which drug class is growing fastest in Behçet’s therapy?

Biologics are advancing at a 7.48% CAGR, driven by broader TNF biosimilar access and emerging IL-23 and JAK inhibitors.

Why are subcutaneous formulations gaining ground?

Self-injectable pens minimize clinic visits, improve adherence, and align with payer strategies to cut infusion-center costs.

Which region offers the highest growth opportunity?

Asia-Pacific is expanding at a 9.83% CAGR, driven by registry-validated outcomes, biosimilar launches, and proactive reimbursement reforms.

What hurdles limit broader biologic adoption?

High annual drug costs and stringent infection-monitoring protocols continue to restrict access in many Silk Road and emerging markets.

Page last updated on: