Affective Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

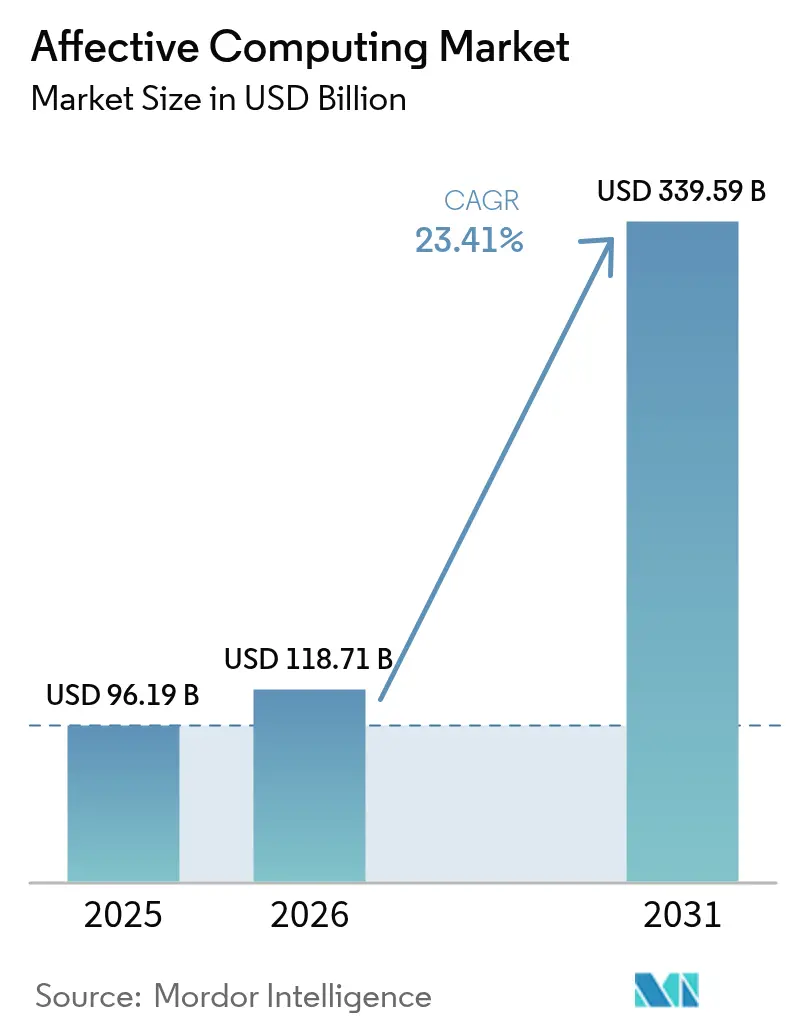

| Market Size (2026) | USD 118.71 Billion |

| Market Size (2031) | USD 339.59 Billion |

| Growth Rate (2026 - 2031) | 23.41% CAGR |

| Fastest Growing Market | Asia |

| Largest Market | North America |

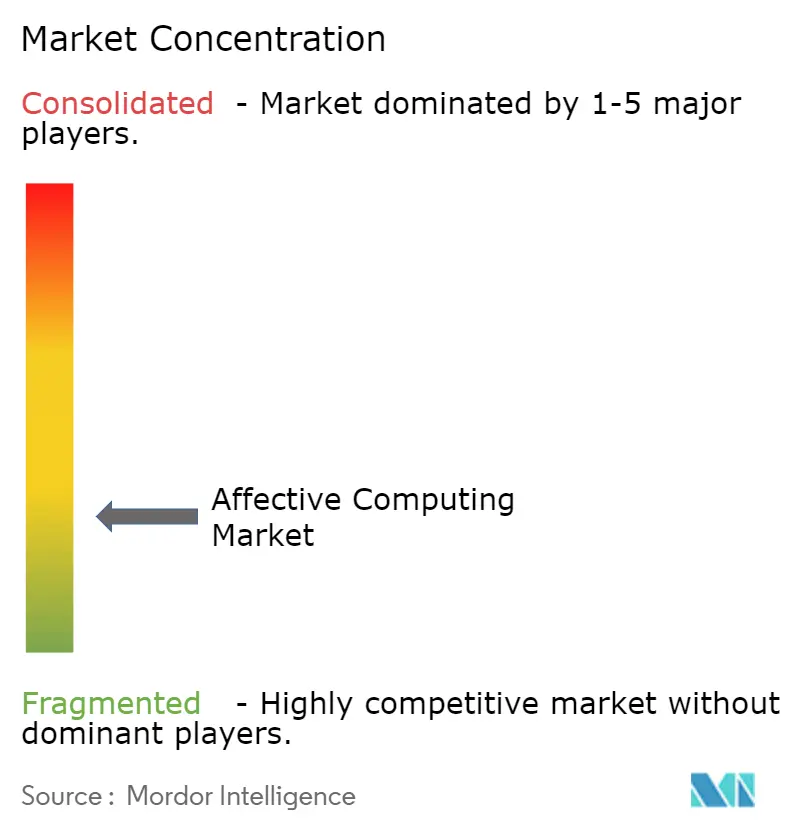

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Affective Computing Market Analysis by Mordor Intelligence

The Affective Computing Market size was valued at USD 96.19 billion in 2025 and estimated to grow from USD 118.71 billion in 2026 to reach USD 339.59 billion by 2031, at a CAGR of 23.41% during the forecast period (2026-2031). Developers are embedding on-device AI chipsets that cut latency and energy draw, multimodal analytics that merge facial, vocal and physiological cues, and edge-first deployments that reduce privacy worries and deliver real-time emotion intelligence in consumer electronics. Momentum also comes from widening healthcare and automotive use cases, where emotion data improves mental-health outcomes and elevates in-cabin safety. Hardware component costs have dropped sharply-sensor and camera prices slid 18% in 2024-broadening the base of devices that can host emotion algorithms. Regional regulation shapes go-to-market strategies: strict European Union rules limit certain workplace applications, while relatively permissive frameworks in North America and Asia encourage broad experimentation, creating distinct product road maps for vendors across the affective computing market.

Key Report Takeaways

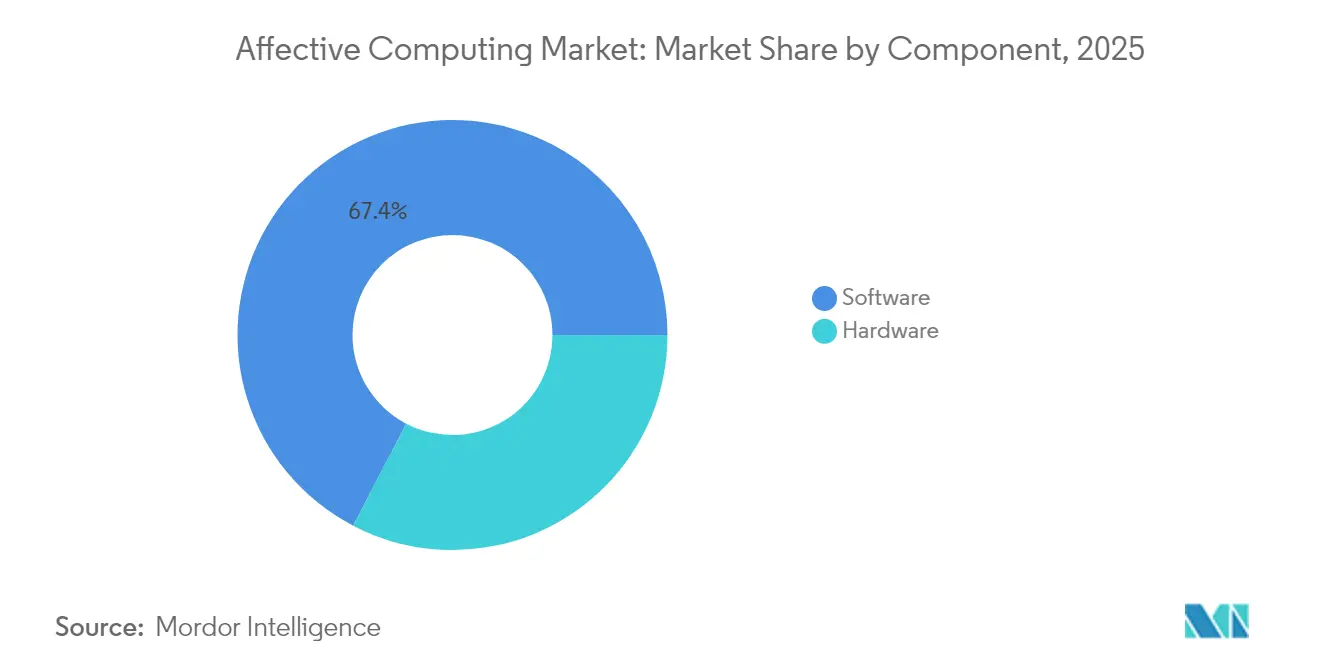

- By component, the software segment held 67.35% of the affective computing market share in 2025 and is advancing at a 25.25% CAGR through 2031.

- By end-user industry, healthcare led with 29.60% revenue share in 2025, while automotive is tracking the fastest 27.90% CAGR to 2031.

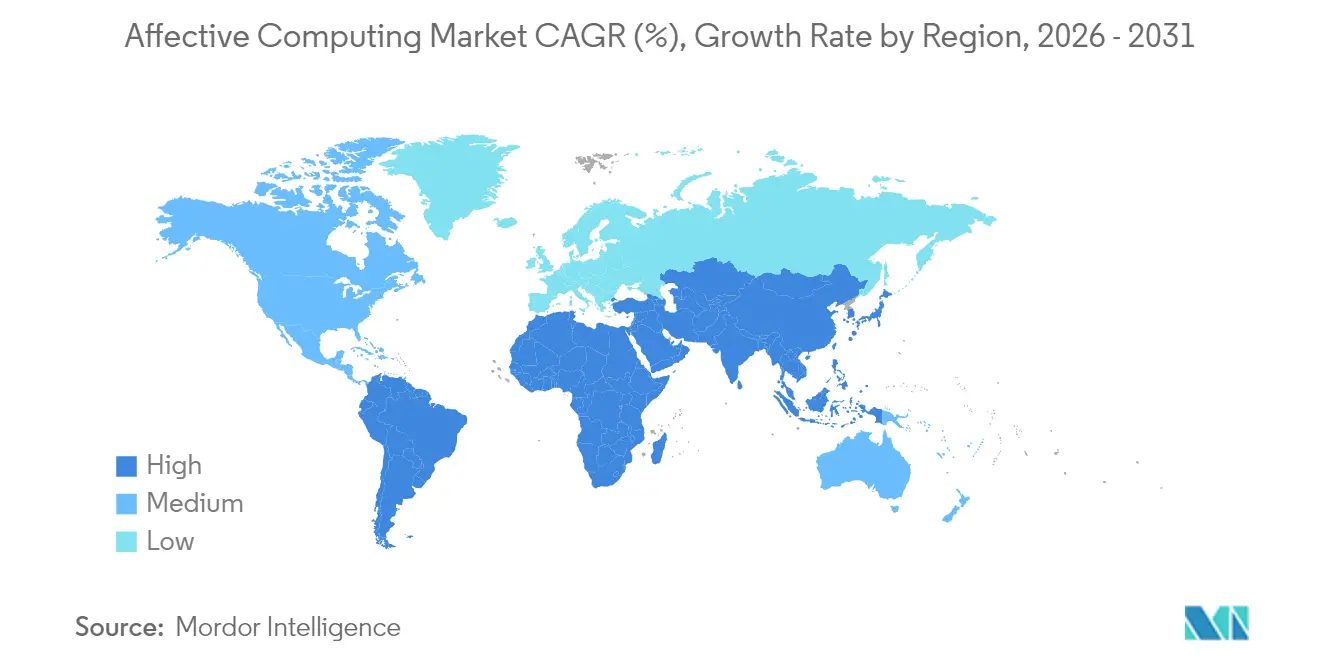

- By geography, North America captured 37.55% of the affective computing market size in 2025; Asia-Pacific is projected to expand at a 26.95% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Affective Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding on-device AI capabilities | +5.2% | Global, strongest in North America & East Asia | Medium term (2-4 years) |

| Multimodal emotion analytics in retail centers | +4.3% | North America, Europe, China | Medium term (2-4 years) |

| Automotive OEM mandates for in-cabin monitoring | +3.8% | North America, Europe | Short term (≤2 years) |

| Surge in telehealth reimbursements for emotion logging | +3.5% | North America, Europe | Medium term (2-4 years) |

| Contact-center voice sentiment scoring | +2.9% | Asia-Pacific, global spillover | Short term (≤2 years) |

| Media-streaming emotion A/B testing | +2.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Deployment of Multimodal Emotion Analytics in Retail Experience Centers

Retailers blend facial cues, vocal tone and physiological signals to craft context-aware product recommendations. A peer-reviewed study found that adding emojis and facial-expression feedback to e-commerce reviews lifted purchase intention and enjoyment by 27% compared with text-only formats.[1]Intel Corporation, “Intel Extends Leadership in AI PCs and Edge Computing at CES 2025,” intel.com Neuro-symbolic Q-learning engines that adjust prices in real time according to shopper sentiment boosted engagement 14% and brand reputation 9%. Luxury boutiques employ the data to deepen emotional affinity, and fast-fashion chains refine new-design rollouts, making retail one of the more dynamic contributors to the affective computing market. The trend resonates most in North America and China, both of which combine mature omni-channel systems with high digital-payment penetration.

Automotive OEM Mandates for In-Cabin Driver Monitoring (U.S., EU)

Regulations on both sides of the Atlantic require vision-based systems to detect distraction, fatigue and impairment. Direct camera solutions identify drowsiness 4.2 seconds faster than steering-input methods, according to field-test data. The European Union General Safety Regulation already obliges new vehicles to embed such functions, and United States legislation under the SAFE Act is shaping similar mandates. Ratings agencies now grade partial-automation features on driver monitoring, adding commercial incentives. Automakers extend the same sensor suite to atmosphere control, infotainment and seat comfort, transforming safety features into premium in-cabin experience platforms and enlarging the affective computing market.

Surge in Telehealth Reimbursements Requiring Patient Emotion Logging

Payers in the United States and parts of Europe reimburse virtual visits that capture emotional data, widening demand in mental-health and chronic-pain care. Research published in Frontiers in Psychiatry showed that late-life mood-disorder screening accuracy improves when voice and facial analytics supplement questionnaires.[2]Rajab Ghandour, “Multimodal Presentation of E-commerce Product Reviews and Ratings,” emerald.com Rural providers adopt these tools to offset specialist shortages, while national health systems justify reimbursements with outcome gains. Higher license volumes for compliant telehealth platforms reinforce the long-term growth trajectory of the affective computing market.

Expanding On-Device AI Capabilities Propelled by Edge-Computing Chipsets

Intel’s Core Ultra processors unveiled at CES 2025 integrate neural processing units that boost AI performance 45% while trimming power use 38%, enabling real-time emotion recognition on mainstream laptops and tablets The architecture removes network hops, safeguards user privacy and meets strict latency thresholds demanded by driver-monitoring and telehealth workflows. Qualcomm’s latest AI Engine offers similar gains for smartphones and automotive platforms, lowering entry barriers for developers pursuing the affective computing market. Spending on edge AI platforms is forecast to surge, with emotion-aware workloads among the most prolific volume drivers. As these capabilities arrive pre-installed in consumer devices, development cycles shorten and time-to-market for emotion-enabled services accelerates within the affective computing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Algorithmic bias litigation risk | −2.4% | European Union, California | Short term (≤2 years) |

| Lack of emotion-data interoperability standards | −1.8% | Global | Medium term (2-4 years) |

| High-bandwidth edge needs in rural facilities | −1.5% | Rural zones worldwide | Medium term (2-4 years) |

| Stringent biometric-consent laws | −1.2% | Illinois, Texas, EU | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Algorithmic Bias Litigation Risk in EU and California

The EU AI Act classifies most workplace and classroom emotion analytics as an unacceptable risk unless used for safety or health, and California’s privacy laws mirror this stance.[3]Brownstein Hyatt Farber Schreck LLP, “EU Takes Steps Toward Regulating Use of Artificial Intelligence with the AI Act,” bhfs.com Nature-published studies warn that bias in emotion algorithms can intensify discrimination during recruitment nature.com. Enterprises therefore face litigation exposure, forcing vendors to invest in privacy-preserving workflows and diverse training datasets, which slows rollouts within regulated regions of the affective computing market.

Absence of Global Standard for Affective Data Interoperability

A meta-review covering 410 trimodal studies highlights inconsistent data schemas that complicate cross-platform integration.[4]Hussein Farooq Tayeb Al-Saadawi et al., “Trimodal Affective Computing Approaches,” doi.org Without shared ontologies, healthcare providers struggle to merge emotion metrics into electronic health records, inflating project costs. AffectEval, released in 2025, offers a modular workaround yet requires broad acceptance to unlock economies of scale. Lack of standards therefore restrains the affective computing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Extends Revenue Lead Across Edge Devices

Software captured 67.35% of the affective computing market share in 2025, a lead it has preserved as developers deploy lightweight facial-, speech- and text-analysis engines on existing hardware. Rapid algorithm iteration allows vendors to release quarterly upgrades that raise accuracy without requiring new sensors, keeping total cost of ownership low for enterprises. Commercial APIs slot into data-science stacks written in Python or JavaScript, shortening build cycles for digital-health dashboards and retail recommendation engines. Contact-center supervisors feed real-time voice sentiment scores directly into customer-experience metrics, while insurance carriers layer emotion classifiers onto claims-video triage to flag potential fraud.

Hardware price compression reinforces software momentum. Edge neural-processing units that once required USD 50 now list near USD 17, lowering barriers for mid-range laptops and infotainment consoles. Miniaturized photoplethysmography and galvanic-skin-response sensors embed inside steering wheels with no design penalty, yet licence fees for the embedded analytics still flow to software vendors, keeping them atop the affective computing market. The widening base of addressable devices strengthens network effects around pretrained models and data-labeling pipelines, suggesting software will hold its dominant share through 2031.

By End-User Industry: Healthcare Retains the Largest Wallet Share

Healthcare generated 29.60% of 2025 revenue as clinicians used multimodal affective scores to flag depression, titrate pain medication and track therapy adherence. One hospital network logged a 12-minute reduction in triage time after integrating speech-driven distress detection into tele-ICU consoles, freeing capacity for critical interventions. Oncology units overlay facial micro-expressions onto electronic health records to refine morphine dosing schedules, while geriatric psychologists rely on voice quiver indices to anticipate anxiety spikes among dementia patients.

Automotive currently grows fastest at a 27.90% CAGR because regulations transform driver-monitoring from a luxury feature into a compliance line item. OEMs now connect mood indicators with ambient-light strips and adaptive HVAC profiles, elevating cabin experience scores in premium models. Retail chains rank third, testing multimodal kiosks that adjust promo imagery in real time according to shopper sentiment. The affective computing industry also gains traction in financial services, where risk-management desks blend text polarity with trader voice stress to modulate position limits.

Geography Analysis

North America accounted for 37.55% of the affective computing market size in 2025, reflecting mature cloud infrastructure and a policy climate that permits broad experimentation outside of states with stringent biometric statutes. United States hospitals moved early because Medicare and major private payers reimbursed emotion-rich teleconsultations, which lifted platform licence volumes. Technology companies based on the West Coast partner with chip designers to push on-device inference that minimizes latency for driver-monitoring and gaming peripherals, while East Coast insurers run pilot projects that mesh voice sentiment and claims data to flag potential false statements.

Asia-Pacific is projected to post a 26.95% CAGR through 2031, the fastest regional clip in the affective computing market. China directs university–industry alliances toward smart-city corridors that synchronize lighting and digital billboards with crowd emotion, raising pedestrian satisfaction ratings. Japan and South Korea bundle driver mood detection into flagship sedans to differentiate cabin comfort, leveraging decades of sensor-fusion expertise. India’s BPO hubs overlay real-time voice stress scores onto agent dashboards to improve first-call resolution metrics, a move that wins renewals from global telecom and banking clients. Southeast Asian e-commerce giants deploy emoji-based review prompts that heighten purchase intention, showing the cultural versatility of emotion cues.

Europe’s trajectory remains mixed after the EU AI Act curtailed workplace and classroom use of emotion recognition. Enterprises pivoted toward automotive and healthcare exemptions, and Germany now leads cross-continental research on multimodal driver fatigue detection. The United Kingdom, outside EU jurisdiction, maintains a regulatory sandbox that encourages tele-mental-health pilots, while Nordic hospitals study pain-emotion indices to refine opioid stewardship. Brussels published a 2025 Action Plan that funds software-defined vehicle stacks, signaling long-term upside for compliant emotion-aware cabins across the affective computing market.

Regulatory Landscape

Regulation is tightening around emotion inference from biometric data, with clear regional divergence. In the European Union, Regulation (EU) 2024/1689 (AI Act) restricts emotion recognition in the workplace and educational institutions under its prohibited practices framework, with carve-outs centered on medical and safety uses. This effectively pushes vendors to re-scope European deployments toward healthcare and automotive driver monitoring, rather than HR and classroom analytics.

Compliance pathways also come through standards and Asia-specific rules. IEEE 7014-2024 provides a lifecycle-oriented standard for empathic AI and affective computing, which offers governance references for procurement and governance teams. In China, the Cyberspace Administration of China issued the Interim Measures for the Administration of Anthropomorphic AI Interaction Services in April 2026 (effective July 15, 2026), requiring algorithm mechanism reviews, ethical reviews, and safety management for AI-driven emotional interaction services.

Competitive Landscape

Incumbent hyperscalers, niche algorithm specialists and academic spin-offs vie for contracts, yielding moderate concentration. Microsoft’s acquisition of Nuance in 2024 embedded medical speech sentiment into Azure’s healthcare cloud, giving the platform a head start in HIPAA-aligned emotion analytics. Google licenses its Multisensory Transformer to automotive suppliers, while Meta funds open-source affective datasets to seed future AR use cases.

Specialists carve out modality depth. audEERING dominates acoustic emotion tagging for media archives, publishing an audio stress corpus that underpins multiple entertainment-industry pilots. EMVAS combines eye-gaze, facial micro-motion and keystroke cadence to flag fatigue in industrial control rooms, tripling pilot conversions during 2024. Sensor firms such as Omnivision pair high-dynamic-range cameras with embedded vision pipelines to deliver turnkey in-cabin kits.

Consolidation is expected to accelerate as vendors seek access to diverse data and global distribution. Lyken.AI, rebranded in May 2025, announced a full-stack platform that bundles edge agents, cloud orchestration and compliance toolkits, aiming to cut enterprise deployment cycles by half. Middleware gaps persist around interoperability; companies that resolve schema mismatches between raw biosignals and sentiment dashboards could command premium valuations.

Affective Computing Industry Leaders

Affectiva Inc.

IBM Corporation

Nuance Communications Inc.

Element Human Ltd

Kairos AR Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The main white space is in deployable, compliant emotion intelligence that can run locally and be audited across the model lifecycle. IEEE 7014-2024 provides a governance anchor for empathic AI, which creates room for productized compliance toolkits (data handling, monitoring, decommissioning) and can reduce friction in enterprise procurement for healthcare, automotive, and customer-experience programs. At the same time, interoperability gaps in affective data schemas limit integration into electronic health records and cross-platform analytics, so middleware that normalizes multimodal signals (facial, voice, text, physiological) into operational KPIs is positioned to translate sensor outputs into measurable workflows for platform vendors and systems integrators.

Interactive, generative experiences also broaden what affective computing can cover beyond sentiment scoring. Edge-first architectures stay practical as on-device AI capability improves, supporting latency-sensitive use cases such as in-cabin monitoring, telehealth emotion logging, and mobile XR research with less reliance on centralized cloud processing and clearer privacy postures. These regulatory and market shifts are already influencing vendor roadmaps, particularly around privacy-preserving, auditable affective solutions across healthcare, automotive, and media.

Recent Industry Developments

- April 2026: Cyberspace Administration of China issued Interim Measures for the Administration of Anthropomorphic AI Interaction Services, effective July 15, 2026. The measures require algorithm mechanism reviews, ethical reviews, and safety management for AI-driven emotional interaction services.

- June 2025: IBM entered a joint study agreement with Inclusive Brains to explore advanced AI and quantum machine learning methods for multimodal brain-machine interfaces, including real-time detection of stress, attention, cognitive load, and fatigue. The collaboration points to deeper investment in multimodal human-state sensing that can feed affective systems used in healthcare and safety-oriented monitoring.

- October 2024: Affectiva renewed a three-year partnership with Kantar to provide attention and emotional insights for advertising and media measurement. The continued work with an insights and measurement partner reinforces emotion analytics as an input in creative testing workflows and supports broader use of multimodal metrics in marketing technology stacks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the affective computing market covers hardware and software that help digital systems detect, interpret, and respond to human emotions using signals like facial cues, voice tone, and physiological inputs, and the related enabling analytics delivered as market revenue.

Scope exclusions: We exclude general purpose AI compute and non-emotion analytics that do not explicitly measure or classify human affect.

Segmentation Overview

- By Component

- Hardware

- Sensors

- Cameras

- Storage Devices and Processors

- Other Components

- Software

- Analytics Software

- Enterprise Software

- Facial Recognition

- Gesture Recognition

- Speech Recognition

- Hardware

- By End-user Industry

- Healthcare

- Automotive

- Retail

- Government and Public Sector

- BFSI

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Peru

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the factual base for our model, especially around AI adoption, device and sensor availability, and the pace of regulation that can slow or speed deployments. We typically refer to public sources such as U.S. Census Bureau and Bureau of Labor Statistics datasets, Eurostat, OECD digital economy indicators, and ITU connectivity statistics, along with standards and guidance notes from bodies such as ISO and NIST.

To translate that foundation into market-ready assumptions, we also review company annual reports, earnings call transcripts, product briefs, and investor presentations to map which emotion-sensing capabilities are being commercialized and where. In parallel, we use paid subscriptions for company financials and intelligence, patent databases to track emotion recognition filings, and a shipment-level trade database for select hardware flows that proxy sensor and camera intensity. The sources listed here are illustrative only, and many other public and paid references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what we see in public data, since affective computing revenues can be bundled into broader AI offerings and not always reported cleanly. We spoke with a mix of hardware makers, software providers, system integrators, and enterprise users across APAC, EMEA, and the Americas. We then validated pricing logic, adoption pace, and use-case boundaries with functional leaders and managers who run deployments day to day.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | APAC: 51% |

| Mid tier: 53% | Functional/Unit leaders: 41% | EMEA: 30% |

| Smaller Players: 20% | Managers: 46% | Americas: 19% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where broader AI spend and enterprise digitalization signals are reconstructed into an addressable demand pool for emotion-aware features, and then filtered by adoption rates across key end users. Once the demand pool is framed, results are corroborated using selective bottom-up approximations such as sampled average selling prices times estimated volumes for sensors, cameras, and software licenses, followed by channel checks with integrators to avoid double counting.

A few practical inputs guide the model, including installed base trends for cameras and biosensors, enterprise software deployment mix, cloud versus edge inference preference, average pricing movement for analytics modules, and the share of use cases that require multimodal signals (face, voice, and biometrics together). Forecasts are built using scenario analysis, since policy and buyer comfort can swing adoption, and then the scenarios are tuned using expert views on regulatory enforcement, procurement cycles, and accuracy threshold expectations. Where bottom-up visibility is thin, gaps are handled by applying conservative attachment rates to device and software baselines and then rechecking against interview feedback before finalizing totals.

Data Validation & Update Cycle

Validation is done through multiple checks that look for inconsistencies across regions, components, and end-user groupings, and the model is reviewed in steps before sign-off. We compare outputs against independent signals such as hardware shipment direction, reported AI and analytics revenue mixes, and patent activity spikes that usually line up with new commercial launches.

If large variances appear, assumptions are revisited and follow-up outreach is triggered to confirm what changed, such as pricing, bundling, or delayed rollouts. The report is refreshed annually, and interim updates are made when material events occur in regulation, platform availability, or major deployment trends. Before delivery, a final analyst pass is completed so the numbers reflect the latest validated view.

Mordor Intelligence's Affective Computing Market Size Measured Against Other Published Estimates

Published market sizes for affective computing can look far apart because each publisher draws the market boundary differently and then applies different adoption and pricing assumptions. In our review, the biggest differences tend to come from what is counted as affective computing revenue versus adjacent AI, and how quickly emotion-aware functions are assumed to scale across industries.

Hardware shipment direction for sensors and cameras, along with software attach rate checks from integrator interviews, are the signals that keep Mordor Intelligence's estimate tied to emotion-specific deployments instead of broader AI analytics revenue that may be bundled into platforms.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 96.19 B (2025) | |

| Global Research House A | USD 91.61 B (2025) | Uses a different boundary for what counts as market revenue, with a broader technology bucket and a longer-dated forecast horizon that can change near-term adoption weighting and currency timing. |

| Industry Publisher B | USD 102.74 B (2025) | Leans on a factory-gate style revenue framing and broader solution inclusions, which can pull in adjacent services and hardware system value that are not always emotion-specific in final deployments. |

The table indicates that the spread is not driven by math alone, since it is mostly about scope control, pricing treatment, and how bundling is handled. By keeping the model anchored to observable deployment signals and repeatable attach rate logic, the final number stays easier to trace back to clear demand and revenue drivers.

Key Questions Answered in the Report

What fuels the affective computing market’s rapid growth?

On-device AI chipsets, multimodal analytics and strong ROI in healthcare and automotive collectively underpin a 23.41% CAGR to 2031.

Which component drives current revenue?

Software leads with 67.35% of 2025 revenue because algorithms deploy on existing hardware without specialized sensors.

How big is the market in 2026?

The affective computing market size reached USD 118.71 billion in 2026 and is projected to hit USD 339.59 billion by 2031.

Which region is expanding fastest?

Asia-Pacific is forecast to grow at a 26.95% CAGR from 2026-2031, led by Chinese smart-city deployments and automotive advances in Japan and South Korea.

What sector shows the strongest future demand?

Automotive posts the highest 27.90% CAGR outlook as driver-monitoring mandates evolve into full cabin-experience platforms.

How do regulations shape adoption?

The EU AI Act restricts workplace emotion analytics, steering European innovation toward healthcare and automotive, while North American and Asian frameworks permit wider experimentation.

Page last updated on: