Open Source Intelligence (OSINT) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.06 Billion |

| Market Size (2031) | USD 43.49 Billion |

| Growth Rate (2026 - 2031) | 15.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

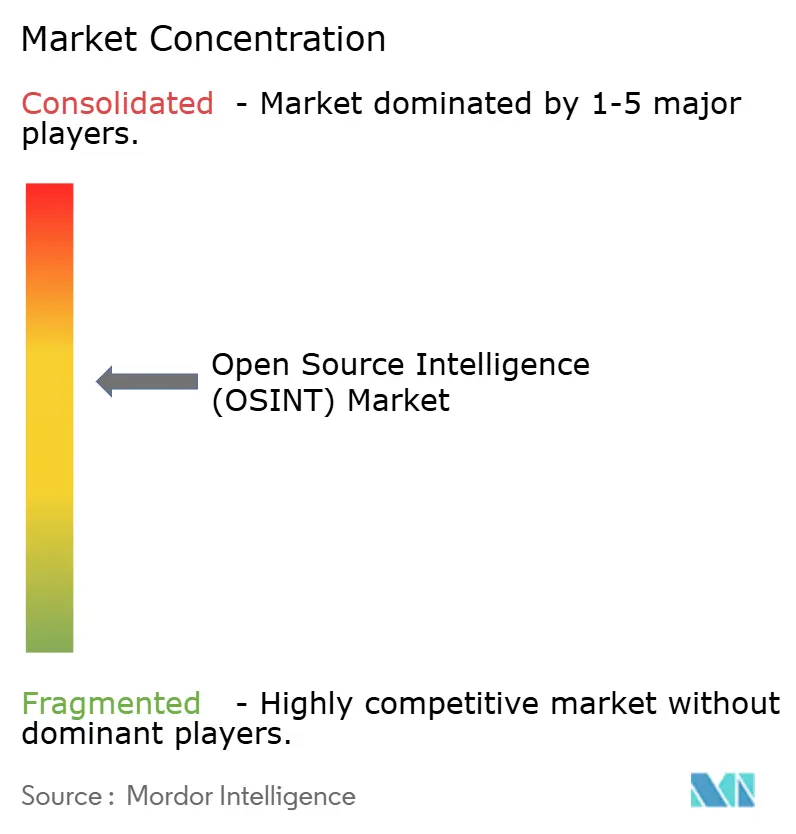

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Open Source Intelligence (OSINT) Market Analysis by Mordor Intelligence

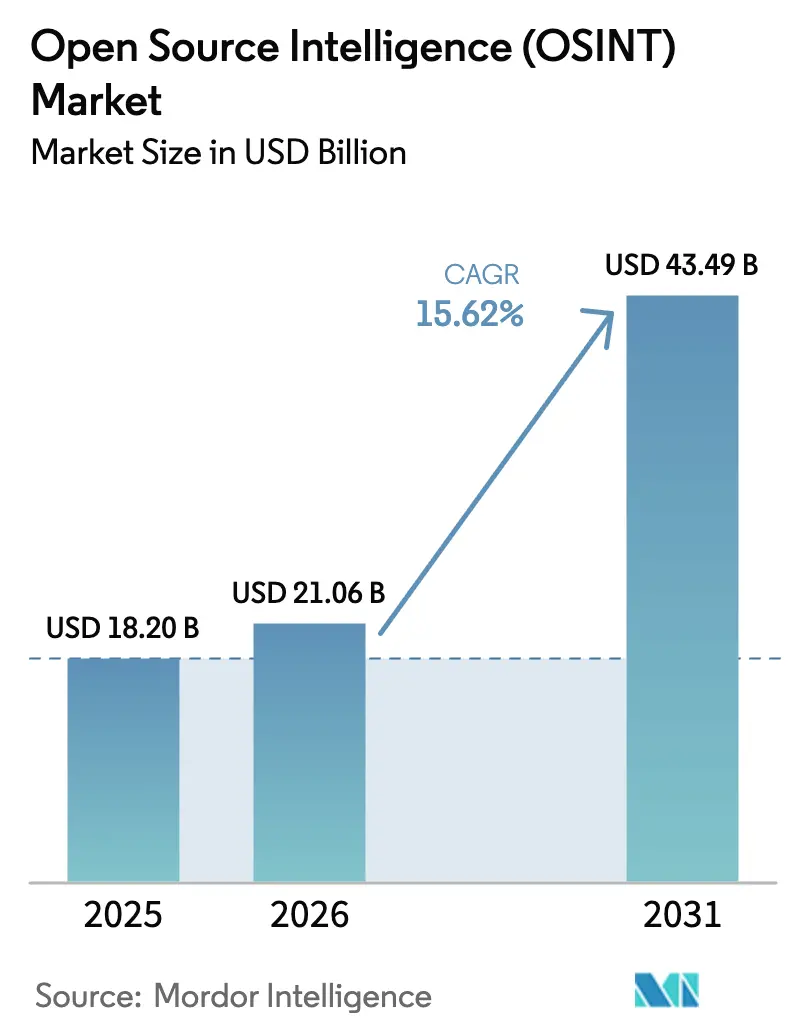

The open-source intelligence market size is expected to grow from USD 18.20 billion in 2025 to USD 21.06 billion in 2026 and is forecast to reach USD 43.49 billion by 2031 at 15.62% CAGR over 2026-2031. Rapid adoption stems from the need to synthesize vast public data pools in an era of geopolitical tension, quantum-era threats, and AI-enabled cyberattacks. Government security agencies continue to anchor spending, while cloud deployment, social-media analytics, and AI-powered automation expand commercial access. Vendors race to embed large language models, automate dark-web collection, and integrate geospatial imagery so users can shift from descriptive to predictive intelligence. Heightened privacy mandates, platform API changes, and adversarial data poisoning temper growth but spur innovation in consent management, secure browsing, and verification tooling across the open-source intelligence market.

Key Report Takeaways

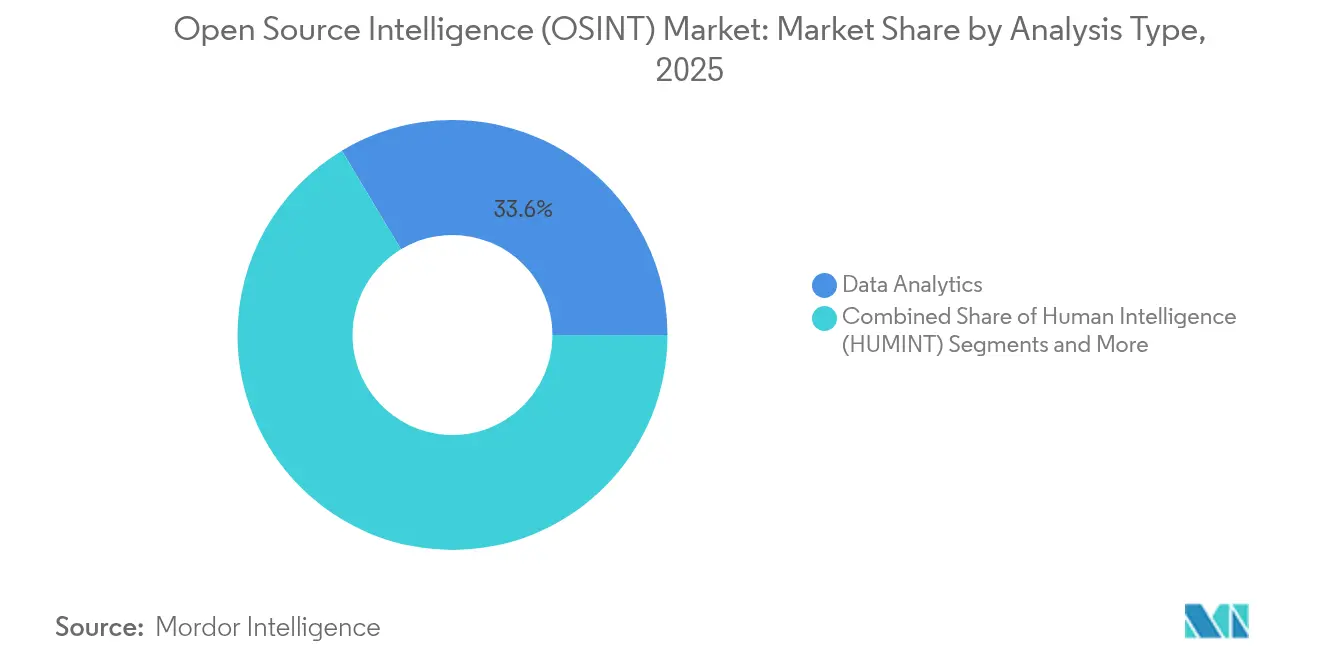

- By analysis type, data analytics captured 33.60% of the open source intelligence market share in 2025, while AI-driven security is projected to climb at an 17.65% CAGR.

- By technology, social media analytics held 42.60% share in 2025; geospatial analytics is forecast to register a 16.25% CAGR to 2031.

- By data source, social media streams accounted for 45.70% of the open source intelligence market size in 2025; dark web and deep web feeds will grow at a 23.25% CAGR.

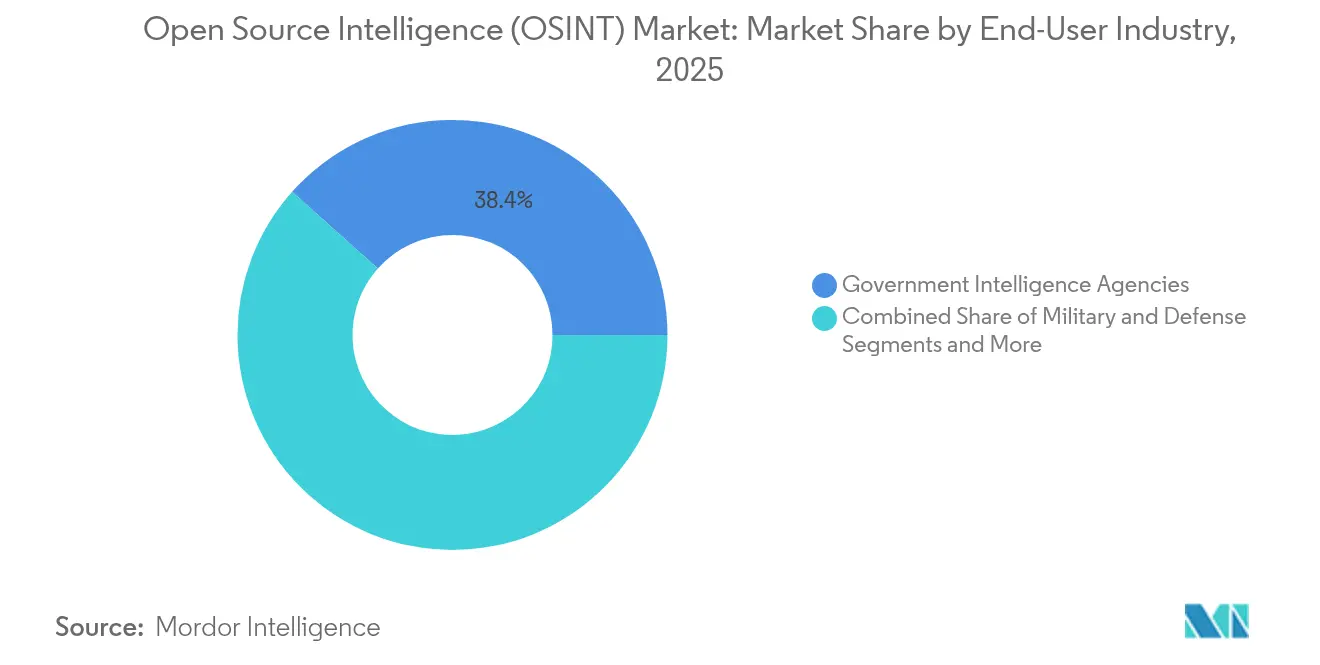

- By end-user industry, government intelligence agencies led with 38.40% revenue share in 2025; financial services and fintech are projected to expand at 15.70% CAGR through 2031.

- By deployment model, cloud-based solutions commanded a 65.80% share in 2025 and will sustain a 15.90% CAGR to 2031.

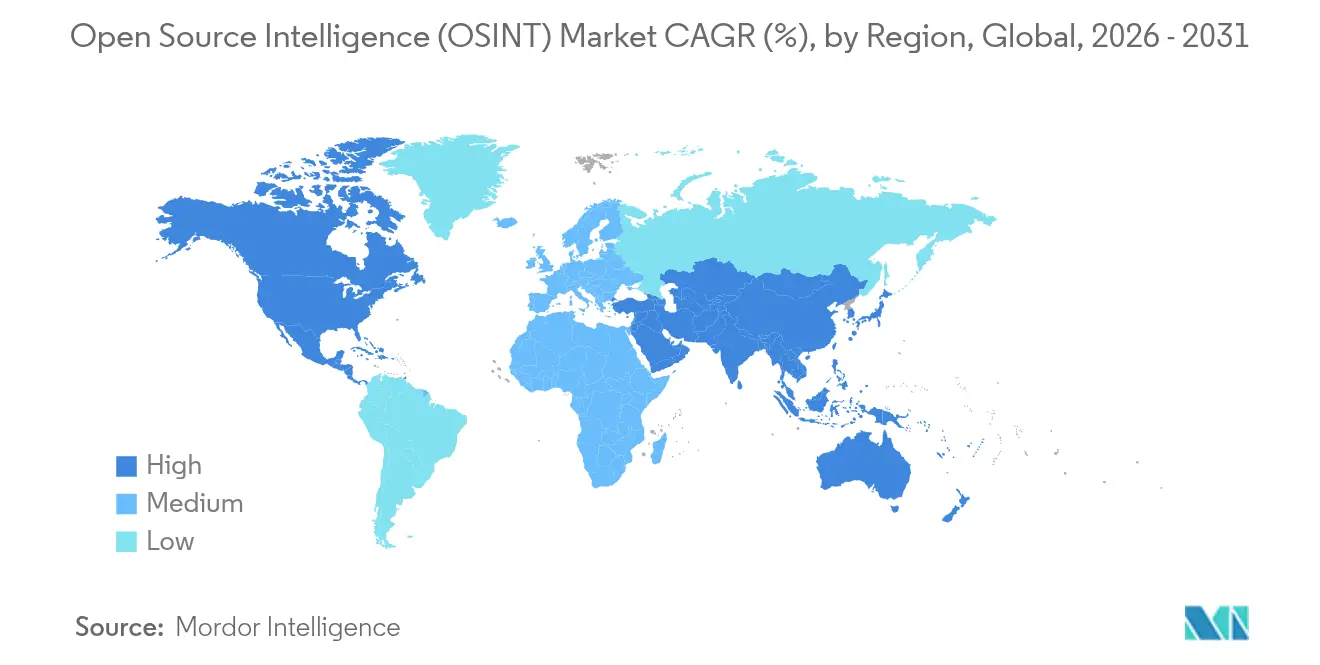

- By geography, North America dominated with 44.10% share in 2025, while Asia-Pacific is advancing at a 14.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Open Source Intelligence (OSINT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enhanced cybersecurity requirements | +2.5% | North America and EU | Medium term (2-4 years) |

| AI/ML automation scaling OSINT | +4.2% | North America and Asia-Pacific | Short term (≤2 years) |

| Explosive social-media data volume | +1.8% | Asia-Pacific and North America | Short term (≤2 years) |

| Rising national-security budgets | +2.1% | North America, EU, Asia-Pacific | Medium term (2-4 years) |

| Supply-chain due-diligence mandates | +1.5% | EU primary, North America secondary | Long term (≥4 years) |

| Quantum-risk mapping initiatives | +2.4% | North America and EU early adopters | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Need for Enhanced Cybersecurity Capabilities

Escalating ransomware, deepfake fraud, and compliance obligations position OSINT as a cornerstone of enterprise cyber defenses. The US Department of Homeland Security’s 2025 report warns that generative AI enables novel identity attacks, pushing financial institutions to monitor dark-web fraud forums, where 34% of listings target banking credentials[1]Department of Homeland Security, “Adversarial AI Threats to Cybersecurity,” dhs.gov. CISA’s Malware Next-Gen service now extends curated intelligence feeds to private companies, reflecting federal recognition of commercial risk. In the European Union, security spending reached 9% of IT budgets in 2024 as firms prepare for NIS 2 Directive audits. These trends lock OSINT platforms into multiyear cybersecurity roadmaps across the open source intelligence market.

AI/ML Automation Expands OSINT Scalability

Artificial intelligence converts manual collection into real-time intelligence. Recorded Future’s Enterprise AI platform applies more than 50 proprietary language models to terabytes of data in 150 languages, cutting analysis cycles from hours to minutes[3]Recorded Future, “Enterprise AI Platform Overview,” recordedfuture.com. The US intelligence community’s Sable Spear operation used AI to trace illicit fentanyl flows, surpassing human teams in speed and recall. Dataminr now delivers 10× more dynamic event briefs via ReGenAI, reinforcing demand for instant alerts around global crises. Such results accelerate adoption across every tier of the open source intelligence market.

Explosive Social-Media Data Volume

Billions of daily posts power sentiment tracking, crisis response, and influence-operation detection. NATO’s Northern Raven exercise proved frontline units can exploit social feeds for mission planning in near-real time. Yet platform API restrictions jeopardize over 250 active research projects, forcing analysts to develop alternative scraping and synthetic-data methods. These pressures spur investment in advanced filtering, verification, and language-agnostic models so users can still capitalize on social data within the open source intelligence market.

Rising National-Security and Threat-Hunting Budgets

Government allocations underpin long-term growth. The ODNI selected Recorded Future for the Sentinel Horizon program, underlining trust in commercial platforms for strategic intelligence. The CIA’s Osiris tool uses generative AI to process unclassified data at scale, showcasing internal modernization. Australia debates a standalone OSINT agency to bolster regional security posture. Such budget trajectories guarantee ongoing platform upgrades, staff training, and data-licensing deals across the open source intelligence market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and compliance barriers | -1.2% | EU primary, select US states | Short term (≤2 years) |

| Data veracity and false-positive risk | -0.8% | Global | Medium term (2-4 years) |

| Social-platform API restrictions | -1.5% | Global | Short term (≤2 years) |

| Adversarial data-poisoning attacks | -0.9% | High-value targets worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Compliance Barriers

GDPR, CCPA, and emerging due-diligence laws force OSINT vendors to build consent, minimization, and localization controls into every workflow. The EU’s probe of DeepSeek underscores regulator scrutiny of language-model training on personal data, with fines that can halt processing. Germany’s Supply Chain Act now requires large employers to evidence third-party screening, raising onboarding costs for mid-market firms. In the US, the FTC has ordered companies to delete models trained on unlawfully obtained data, signaling tighter oversight. Compliance hurdles introduce friction but also spur demand for privacy-preserving analytics within the open source intelligence market.

Social-Platform API Restrictions/Paywalls

Platform shifts from free researcher tiers to revenue-sharing models price small teams out of real-time access. X replaced a USD 42,000 monthly enterprise tier with volume-based fees, causing 57% of financial-crime analysts to report productivity drops. Academic labs face similar cutbacks, narrowing public–sector innovation. Vendors respond by engineering stealth scrapers, partnering with telecom data brokers, and expanding dark-web pipelines. The outcome stratifies the open source intelligence industry between well-funded entities that can absorb API costs and those forced to scale back scope.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Analysis Type: AI-Driven Security Gains Momentum

Data analytics accounted for 33.60% of the 2025 open source intelligence market, reflecting entrenched demand for structured trend discovery and entity correlation. Complementary natural-language tools extract entities, relationships, and sentiment from multilingual text, while network analytics maps infrastructure to expose command-and-control nodes. Human intelligence remains essential for contextual checks that algorithms cannot yet replicate.

AI-driven security is the fastest-growing niche at an 17.65% CAGR. The CIA’s Osiris program illustrates how generative models now triage unclassified data into mission-ready briefs, freeing human analysts for higher-order assessments. Commercial banks deploy automated phishing detection and credential-stuffing monitors to cut incident response times. As attack surfaces widen, hybrid analyst–AI workflows are expected to dominate decision support across the open source intelligence market.

By Technology: Geospatial Analytics Accelerates

Social media analytics held 42.60% share in 2025, driven by crisis-monitoring, market-sentiment tracking, and influence-operation detection. Event-detection firms tap image recognition to isolate protest footage, wildfire alerts, and supply-chain disruptions.

Geospatial analytics will rise at a 16.25% CAGR as government and commercial constellations flood the sky with high-resolution imagery. The National Geospatial-Intelligence Agency’s USD 700 million AI initiative to interpret satellite data underlines public-sector momentum. Retailers apply the same feeds to gauge parking-lot traffic, while insurers quantify wildfire risk. Cost declines in launch services and the advent of sub-daily revisits push geospatial adoption deeper into the open source intelligence market.

By Data Source: Dark-Web Intelligence Surges

Social media streams supplied 45.70% of 2025 collection volume, but new policy barriers stimulate portfolio diversification. Firms integrate public-sector databases, news wires, and podcast transcripts to backfill coverage gaps caused by shrinking APIs.

Dark-web and deep-web feeds will expand at 23.25% CAGR. Healthcare breaches such as the Qilin ransomware attack on London hospitals highlight the need for early warning that credentials and PII are for sale. Managed-attribution browsers, onion-routing gateways, and automated screenshotting mitigate exposure, enabling even regulated industries to harvest criminal-forum chatter. As threat actors migrate to encrypted channels, dark-web intelligence becomes a core pillar of the open source intelligence market size forecasts through 2030.

By End-User Industry: Financial Services Rapidly Scales

Government intelligence agencies continued to command 38.40% of 2025 revenue. Programs such as ODNI’s Sentinel Horizon and the NGA’s AI imagery pipeline ensure steady procurement pipelines, while defense primes embed OSINT modules in mission-planning suites.

Financial services is the fastest-growing vertical, expanding at 15.70% CAGR on the back of anti-money-laundering automation, sanctions screening, and deepfake fraud defenses. Mastercard’s USD 2.65 billion purchase of Recorded Future signals strategic realignment, positioning payment firms as intelligence providers rather than mere consumers. With synthetic-identity fraud expected to exceed USD 5 billion globally in 2025, banks channel budgets into real-time dark-web analytics and social-engineering detection, reinforcing demand within the broader open source intelligence market.

By Deployment Model: Cloud Retains Dominance

Cloud platforms represented 65.80% of deployments in 2025 and will sustain 15.90% CAGR. Spiraling compute requirements for multimodal transformers make on-premise upgrades prohibitive for most enterprises. Cloud vendors bundle GPU clusters, ingestion pipelines, and native compliance modules to shrink time-to-value from months to days.

Highly classified workflows still favor air-gapped installations, but hybrid patterns emerge. Agencies collect and pre-process unclassified feeds in the cloud, then port enriched datasets behind firewalls for correlation with secret holdings. As zero-trust architecture spreads, cloud scalability, combined with granular access controls, cements its role at the heart of the open source intelligence market.

Geography Analysis

North America retained 44.10% share in 2025, buoyed by the ODNI’s multi-year modernization agenda, CISA’s threat-sharing expansion, and vigorous venture funding for AI-native platforms. Mastercard’s acquisition of Recorded Future and Fortress’s USD 100 million investment in Dataminr confirm Wall Street’s appetite for cyber intelligence deals. However, a mosaic of state-level privacy laws and rising Cloud Act scrutiny compel providers to adopt regional data stores and sophisticated consent orchestration.

Asia-Pacific is the fastest-growing region at 14.15% CAGR. China aligns private firms, state enterprises, and universities to harvest foreign tech patents, defense procurement filings, and satellite imagery, challenging Five Eyes dominance. India triples reconnaissance-satellite cAsia-Pacificity, pairing imagery with AI analytics to secure borders and maritime lanes. Japan’s designation as OpenAI’s first Indo-Pacific hub illustrates government support for sovereign AI infrastructure. Territorial disputes, quantum investment exceeding USD 15 billion, and e-commerce expansion combine to drive sustained demand across the open source intelligence market.

Europe posts steady uptake as institutions divert 9% of IT spend to cybersecurity. The EU’s Corporate Sustainability Due Diligence Directive spurs cross-border supply-chain screening, while France pilots trusted generative AI models for defense missions. Ukraine’s real-time satellite analysis partnership with Safran.AI demonstrates wartime collaboration and fuels interest in geospatial OSINT across NATO members. Strict GDPR enforcement and localization rules add complexity, yet they simultaneously reward providers that embed privacy-by-design workflows into the open source intelligence industry.

Competitive Landscape

The market remains moderately fragmented. Top vendors include Palantir, Recorded Future, Dataminr, Babel Street, and ShadowDragon, yet new entrants harness transformer models, cloud GPUs, and alternative data streams to erode incumbents’ edge. Mastercard’s USD 2.65 billion deal signals crossover between financial services and threat intelligence, while Dow Jones’ purchase of Dragonfly Intelligence broadens information-services footprints into geopolitical risk. Babel Street’s buyout of Vertical Knowledge adds identity-analytics depth, reflecting a wave of tuck-ins aimed at filling specialized gaps.

Competitive differentiation hinges on AI model performance, managed attribution, multilingual coverage, and vertical-specific taxonomies. Patent filings reveal momentum: Palantir submitted claims around attribute-based cyber alerting, and Thales partnered with the French atomic agency to co-develop trusted large language models for defense.

Opportunities remain in quantum-risk mapping, automated ESG compliance, and small-satellite analytics, niches where traditional vendors lack bespoke solutions. As platform capabilities converge, service integration, domain expertise, and data-rights transparency will dictate share capture within the open source intelligence market.

Open Source Intelligence (OSINT) Industry Leaders

Google LLC

Palantir Technologies

Recorded Future Inc.

Thales Group

Babel Street

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Dataminr secured USD 100 million from Fortress Investment Group to accelerate enterprise expansion and AI product development.

- March 2025: Siemens Industrial Copilot won the Hermes Award 2025 for introducing generative AI into factory automation.

- March 2025: Ukraine’s military intelligence partnered with Safran.AI to analyze imagery from the new CSO-3 reconnaissance satellite.

- February 2025: Dow Jones acquired Dragonfly Intelligence and Oxford Analytica for USD 40 million to deepen geopolitical-risk coverage.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the open-source intelligence (OSINT) market as all software platforms, data feeds, and managed services that gather, enrich, and analyze information residing in publicly available domains, such as the surface web, deep web, social networks, commercial satellite imagery, and government databases, to turn that data into actionable security, risk, or investigative insights. According to Mordor Intelligence, revenue linked to custom consulting projects that do not embed repeatable OSINT tooling is outside this scope.

Scope exclusion: proprietary classified intelligence, stand-alone threat-hunting services, and hardware-only sensor sales are not counted.

Segmentation Overview

- By Analysis Type

- Data Analytics

- Human Intelligence (HUMINT)

- AI-Driven Security

- Content Intelligence

- Network Analytics

- Other Analysis Types

- By Technology

- Text Analytics

- Social-Media Analytics

- Video Analytics

- Security Analytics Platforms

- Geospatial Analytics

- Other Technologies

- By Data Source

- Surface-Web Content

- Dark-Web and Deep-Web Feeds

- Social-Media Streams

- Public Government Data

- Commercial Satellite and ISR Feeds

- Other Sources

- By End-user Industry

- Government Intelligence Agencies

- Military and Defense

- Cyber-Security Service Providers

- Financial Services and FinTech

- Corporate Risk and Due-Diligence Firms

- Media and Disinformation Watchdogs

- Other Industries

- By Deployment Model

- Cloud

- On-Premise

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cyber-threat analysts, investigative journalists, procurement officers in defense ministries, and CISOs at mid-market enterprises across North America, Europe, Asia-Pacific, and the Gulf. These conversations tested desk findings, revealed typical tool penetration rates, and provided forward views on cloud migration and AI-assisted triage that are rarely published. Follow-up surveys with managed-security providers quantified average seat counts per contract, anchoring volume assumptions.

Desk Research

We began with trade statistics from sources such as the US Bureau of Industry and Security, Eurostat's ICT security surveys, and Japan's MIC cybersecurity spending tracker, which map national demand pools. Analyst teams then drew on public filings and investor decks from leading OSINT vendors to capture average selling price shifts and deployment preferences. Subscription databases that Mordor Intelligence licenses, including D&B Hoovers for company revenue splits and Dow Jones Factiva for deal flow, helped us benchmark vendor traction across regions. Academic journals indexed in IEEE Xplore, plus white papers from industry bodies like FIRST, offered base rates for breach discovery timelines, enriching cost-of-failure assumptions. The sources above illustrate our desk research foundation; many further references were reviewed to cross-check figures and definitions.

A second pass compiled technology fingerprints, annual counts of CVEs tagged 'open-source intelligence,' patent filings retrieved via Questel, and geospatial imagery tasking volumes, so our baseline aligns with observable market signals rather than headlines. This mosaic clarified which techniques, for example, social-media scraping versus geospatial analytics, currently command larger shares and steeper growth.

Market-Sizing & Forecasting

Baseline value is first built top-down by linking national cybersecurity outlays and documented incident response spending to OSINT adoption ratios, which are then moderated through bottom-up vendor revenue samples and channel checks to align with real invoices. Key variables include reported data-breach counts, average cost per breach, social-media content growth, satellite imagery tasking frequency, regulatory compliance deadlines, and share of security budgets allocated to analytics. A multivariate regression model projects each driver, and scenario analysis tests upside from Generative AI integration or downside from spending freezes. Where supplier roll-ups leave gaps, region-specific average selling prices are imputed from the nearest disclosed deals and validated during primary research.

Data Validation & Update Cycle

Outputs pass anomaly scans, peer review, and senior analyst sign-off. We refresh the dataset annually, issuing interim revisions if material events, such as major cyber regulations, landmark acquisitions, or disruptive technology launches, shift demand. Before publication, an analyst revisits key inputs so clients receive the most current view.

Why Mordor's Open Source Intelligence Baseline Commands Reliability

Published estimates often diverge because studies pick different data sources, adopt unique adoption ratios, or freeze exchange rates at dissimilar points. Our disciplined scope selection and yearly refresh narrow those gaps and let decision-makers trace every figure to a transparent input.

Key gap drivers include narrower technique coverage in some studies, conservative cloud-migration assumptions, or optimistic penetration multipliers applied without primary verification.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.20 B (2025) | Mordor Intelligence | - |

| USD 12.10 B (2025) | Global Consultancy A | Limited primary verification and partial vendor revenue capture |

| USD 14.40 B (2024) | Trade Journal B | Excludes deep-web data feeds and understates cloud adoption |

| USD 9.74 B (2024) | Industry Analyst C | Aggressive discounting of average selling prices and limited regional granularity |

The comparison shows that, by anchoring to validated spend signals and blending top-down pools with selective bottom-up proofs, Mordor Intelligence delivers a balanced, defensible baseline clients can replicate with clear steps and available data.

Key Questions Answered in the Report

What is the current value of the open source intelligence market?

The open source intelligence market stands at USD 21.06 billion in 2026.

Which segment is expanding the fastest?

AI-driven security is the fastest-growing analysis type, advancing at an 17.65% CAGR to 2031.

Why are financial institutions investing heavily in OSINT platforms?

Rising deepfake fraud, AML scrutiny, and real-time dark-web threats drive a 15.70% CAGR for OSINT adoption in financial services.

How do privacy regulations impact OSINT programs?

GDPR and CCPA require data minimization, localization, and consent management, adding compliance costs but improving trust.

Which region offers the highest growth potential?

Asia-Pacific leads with a projected 14.15% CAGR due to satellite proliferation, security tensions, and sovereign AI investments.

Page last updated on: