Automatic Identification And Data Capture (AIDC) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 88.12 Billion |

| Market Size (2031) | USD 142.30 Billion |

| Growth Rate (2026 - 2031) | 10.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

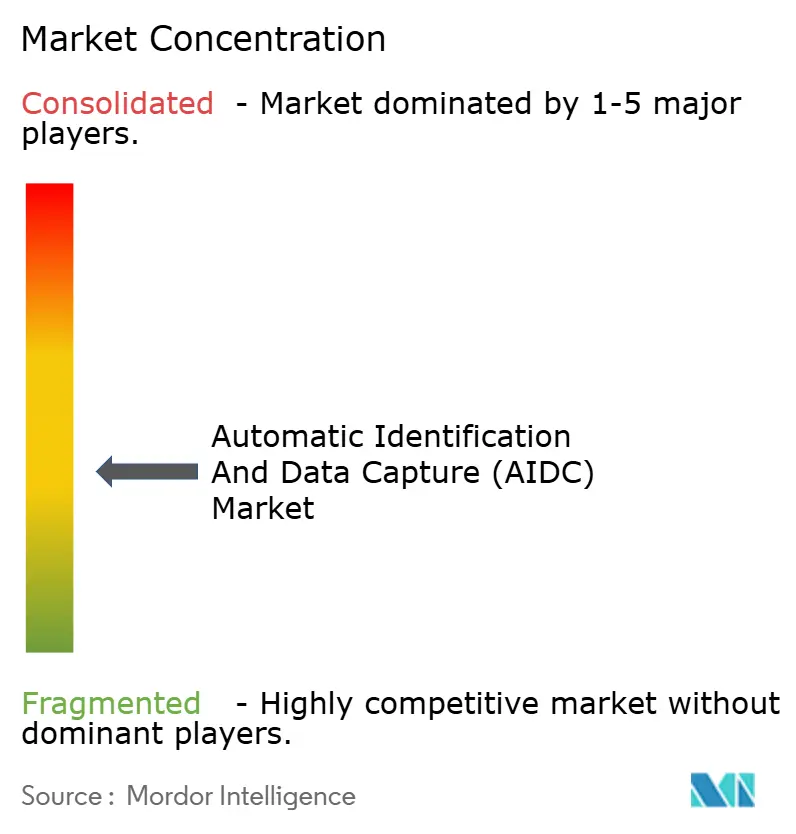

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automatic Identification And Data Capture (AIDC) Market Analysis by Mordor Intelligence

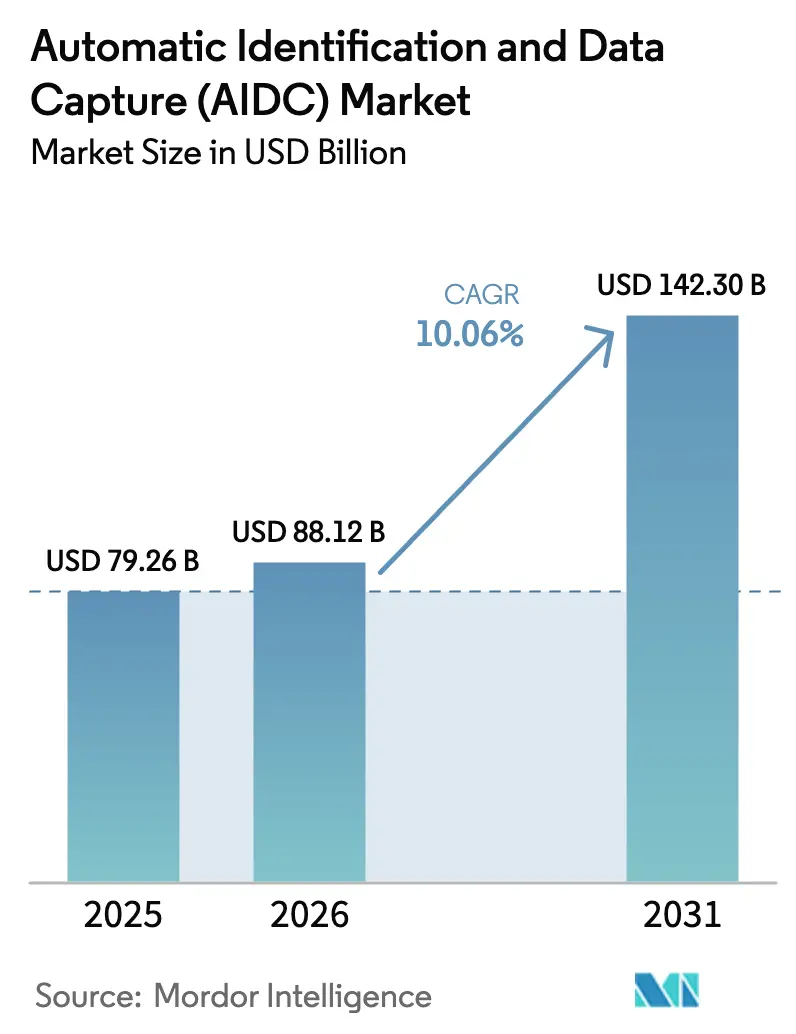

The Automatic Identification and Data Capture market size is expected to grow from USD 79.26 billion in 2025 to USD 88.12 billion in 2026 and is forecast to reach USD 142.3 billion by 2031 at 10.06% CAGR over 2026-2031. Rising omnichannel retail, labour-scarcity-led warehouse automation, and government digital-identity programs are expanding use cases well beyond traditional point-of-sale scanning. Hardware still accounts for the majority of spend, yet software platforms that normalize heterogeneous scan events are scaling quickly as enterprises converge edge, cloud, and legacy ERP estates. Competition is intensifying because low-priced Asian handhelds are eroding margins for Western scanner vendors while RFID chipmakers defend patent moats around backscatter protocols. At the same time, biometric modalities are pivoting to contactless facial and iris recognition to satisfy post-pandemic hygiene preferences, and machine-vision suppliers are embedding inference chips that decode damaged codes without routing images to the cloud.

Key Report Takeaways

- By end-user industry, retail and e-commerce led with 31.48% revenue share in 2025, whereas transportation and logistics is projected to expand at a 10.81% CAGR through 2031.

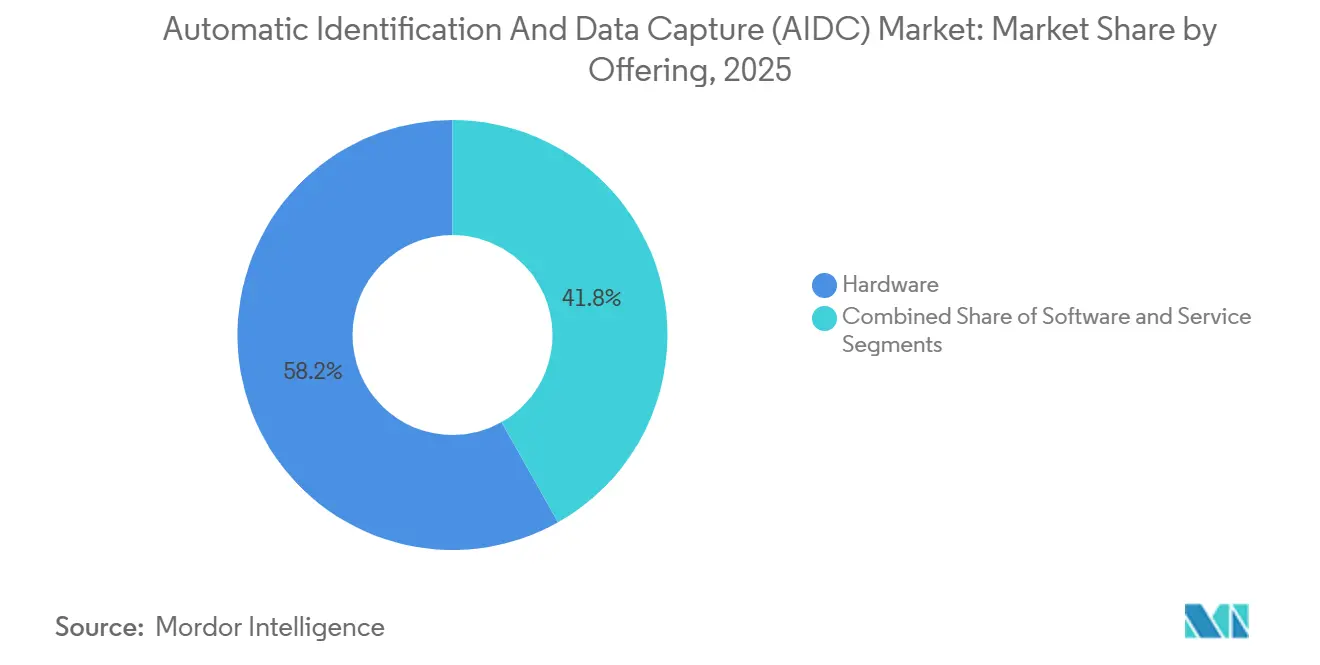

- By offering, hardware captured 58.17% of 2025 revenue while services are advancing at 11.08% CAGR during 2026-2031.

- By product, barcodes held 42.41% of 2025 value and RFID is expected to register a 10.84% CAGR to 2031.

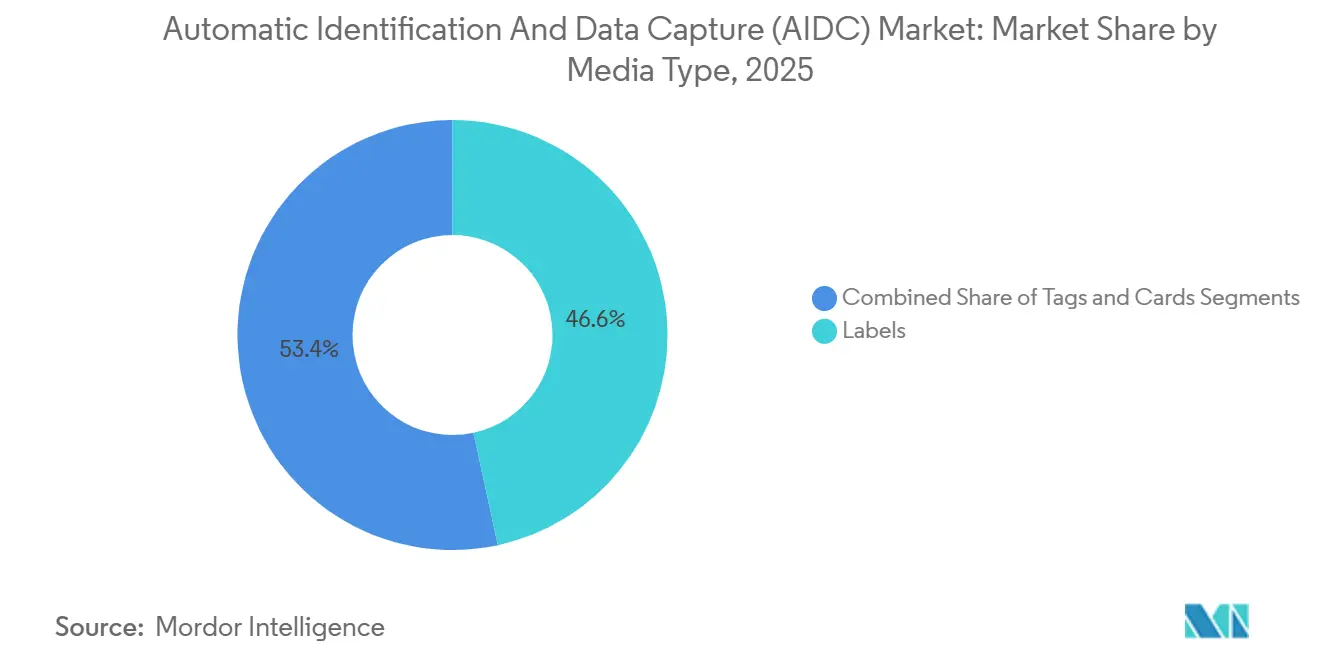

- By media type, labels dominated with 46.63% share of the Automatic Identification and Data Capture market size in 2025, and tags are forecast to expand at a 10.98% CAGR between 2026-2031.

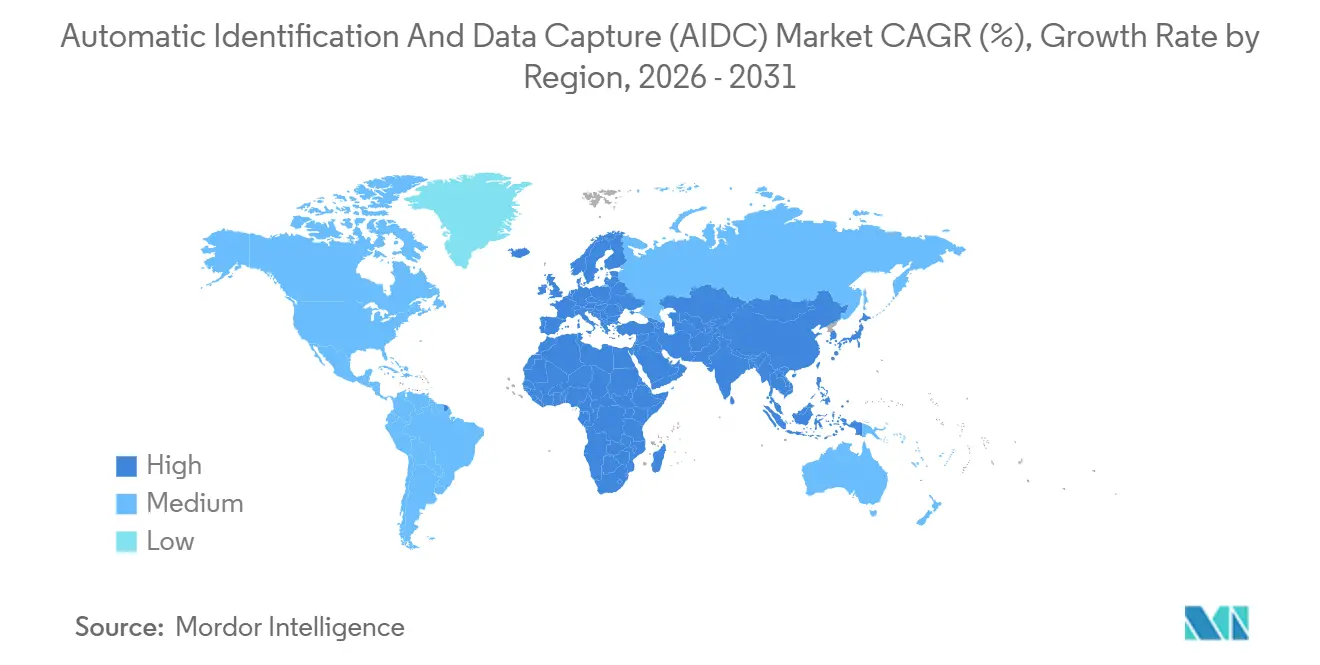

- By geography, North America accounted for 34.77% of 2025 spending whereas Asia-Pacific is the fastest growing region at 10.91% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automatic Identification And Data Capture (AIDC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Migration to 2D/QR Codes in Omnichannel Retail | +2.80% | Global, with early concentration in North America and Europe | Medium term (2-4 years) |

| Surge in UHF-RFID Adoption for Item-Level Inventory | +2.50% | North America and Europe retail, expanding to Asia-Pacific apparel | Medium term (2-4 years) |

| Government e-ID and Digital Health-Card Roll-outs | +1.90% | Asia-Pacific (India, China), Europe (EU Digital Identity Wallet), Middle East | Long term (≥ 4 years) |

| Labor-Scarcity-Led Warehouse Automation | +1.70% | North America and Europe logistics hubs, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Real-Time Cold-Chain Tracking Mandates | +0.90% | Global pharmaceutical and food sectors, regulatory focus in North America and Europe | Medium term (2-4 years) |

| Contactless Biometric Gates in Travel-Security Corridors | +0.70% | North America, Middle East (GCC airports), Asia-Pacific (Singapore, Japan) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Migration to 2D or QR Codes in Omnichannel Retail

Retailers are rapidly replacing linear barcodes with 2D symbols that embed batch numbers, expiry dates, and digital-link URLs connecting physical packaging to e-commerce listings. GS1 has mandated global point-of-sale acceptance of matrix codes by 2027, prompting merchants to upgrade checkout scanners and back-office systems.[1]GS1, “Digital Link and 2D Barcode Migration,” gs1.org Apparel and grocery chains already print QR codes that allow shoppers to access fit guides, allergen data, and return policies with a smartphone scan, reducing staff-assisted lookups and substitution errors. The richer data capacity also supports buy-online-pick-up-in-store workflows where associates validate freshness cues such as packaging date before hand-off. Adoption is reinforced by European Union food-label directives requiring machine-readable disclosures by 2028, turning regulatory pressure into a catalyst for global harmonization. As 2D readiness becomes table stakes, retailers that lag risk stranded hardware assets and slower checkout throughput.

Surge in UHF-RFID Adoption for Item-Level Inventory

Falling inlay costs below USD 0.05 and read ranges beyond 10 meters have pushed passive UHF-RFID from pallet to item serialization.[2]Impinj, “RAIN RFID Solutions,” impinj.com Apparel chains tagging every garment are now achieving inventory accuracy above 98%, enabling real-time store-level fulfilment. Pharmaceutical distributors rely on RFID pedigrees to meet United States and European counterfeit-medicine mandates, while electronics brands embed tags in packaging for automated warranty registration and authenticity checks. Overhead readers at store exits combine with loss-prevention analytics to cut shrinkage by 20-30 basis points. As phased-array antennas become cheaper and denser, read speeds are rising enough to process hundreds of tags within one second, opening use cases in high-velocity cross-docking hubs.

Government e-ID and Digital Health-Card Rollouts

National digital-identity programs are scaling AIDC infrastructure for issuance and verification. India issued 680 million QR-based health cards by late 2025 under Ayushman Bharat, linking clinical records to insurance eligibility.[3]Impinj, “RAIN RFID Solutions,” impinj.com The European Digital Identity Wallet, mandated for 2026 rollout, allows citizens to present credentials via QR or NFC without physical documents.[4]European Commission, “European Digital Identity Wallet,” ec.europa.eu China’s digital-yuan pilots require QR acceptance at all merchant points, effectively embedding AIDC into the monetary system. Gulf Cooperation Council states have begun issuing biometric residence permits with contactless chips, streamlining border and labour-mobility processes. These programs create sustained demand for secure printers, biometric enrolment stations, and handheld verification devices.

Labor-Scarcity-Led Warehouse Automation

Persistent labour shortages pushed North American warehouse wages up 8% in 2025, incentivizing automated sortation and robotics that rely on AIDC navigation. Amazon had 750,000 mobile robots navigating by floor-mounted QR codes by end-2025, and third-party logistics firms are following suit. Vision-based dimensioning systems replace manual measurements, avoiding carrier surcharges and billing disputes. Autonomous forklifts use RFID pallet tags to confirm load identity before transfer, slashing mis-shipments by 40% in pilots. With payback periods now under 18 months even for mid-tier operators, the Automatic Identification and Data Capture market is becoming integral to labour-productivity strategy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inter-System Data-Format Incompatibility Across Legacy ERPs | -1.20% | Global, acute in manufacturing and healthcare sectors with decades-old systems | Medium term (2-4 years) |

| High Initial CAPEX for Vision-Based AIDC in Brown-Field Plants | -0.90% | North America and Europe manufacturing, limited impact in greenfield Asia-Pacific facilities | Short term (≤ 2 years) |

| Counterfeit Low-Cost Barcode Scanners From Grey Markets | -0.50% | Asia-Pacific, Middle East, Africa, and South America emerging markets | Long term (≥ 4 years) |

| Privacy Pushback on Biometric Data Storage | -0.40% | Europe (GDPR enforcement), North America (state-level regulations), selective Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inter-System Data-Format Incompatibility Across Legacy ERPs

Pre-2015 ERP platforms were designed for batch updates and cannot natively parse GS1 Digital Link URIs or RAIN RFID schemas, adding latency and forcing parallel manual workflows. Healthcare institutions see delayed adverse-event alerts when barcode-medication data cannot stream directly into patient-administration systems, undercutting safety goals. Manufacturers using proprietary part-marking struggle to share serialization data with contract assemblers unless both invest in ISO/IEC 15434 syntax translators, fragmenting multi-tier traceability. Full ERP upgrades often exceed USD 10 million, so many firms stay locked into brittle middleware bridges that erode the ROI of AIDC automation.

High Initial CAPEX for Vision-Based AIDC in Brown-Field Plants

Retrofitting legacy lines with industrial cameras, LED lighting, and edge computers regularly tops USD 500,000 per line. Facilities built before 2010 frequently lack network cabling, vibration isolation, or clean power, so ancillary upgrades can double total spend. Lighting alone may consume 30% of the budget because fluorescent flicker compromises image clarity, necessitating synchronized high-frequency LED arrays. Margins near 5% make such outlays hard to amortize for mid-tier contract manufacturers, extending payback beyond three years. Consequently, greenfield factories in Asia-Pacific integrate vision systems during construction, widening the productivity gap and accelerating offshoring of precision assembly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain as Integration Complexity Rises

Services captured a modest share in 2025 yet are growing at 11.08% as companies struggle to reconcile RFID streams, 2D barcode scans, and edge-vision outputs across hybrid infrastructure. Hardware anchors the Automatic Identification and Data Capture market size today, but commoditization is compressing scanner margins and shifting value to consulting, systems integration, and managed uptime agreements. Vendors now pitch outcome-based contracts that guarantee equipment availability, transferring component-failure risk away from operators.

Growing complexity is also spurring platform consolidation. Enterprises want a single pane of glass that normalizes data from mobile computers, fixed readers, and smart cameras into actionable insights. Software startups secure venture capital for SDKs that turn commodity smartphones into enterprise-grade scanners, disrupting dedicated handheld sales. Maintenance teams increasingly prefer evergreen subscription licensing that rolls firmware updates, cybersecurity patches, and analytics features into predictable monthly fees.

By Product: RFID Outpaces Barcodes on Item-Level Economics

Barcodes still dominate point-of-sale and shipping-label workflows, but RFID is gaining momentum as falling inlay prices enable item serialization without margin erosion. RFID IC shipments jumped 22% in 2025, illustrating how the Automatic Identification and Data Capture market share is shifting toward passive UHF use cases. Apparel, pharmaceuticals, and consumer electronics appreciate the ability to read hundreds of items simultaneously without line-of-sight, a feat unattainable with laser scanners.

Matrix barcodes are not standing still. GS1’s Sunrise 2027 deadline compels retailers worldwide to accept 2D symbols, so checkout lanes are being re-equipped with imaging scanners. Smart cards are also transitioning to contactless variants, representing more than 70% of new issuance as tap-and-go convenience reshapes transit and payments. Biometric modules bifurcate into fingerprint for physical access and facial-iris hybrids for border control, the latter benefiting from pandemic-driven contactless norms. Optical character recognition is quietly modernizing customs paperwork and invoice processing, achieving 95% extraction accuracy and saving labour hours that previously resisted automation.

By Media Type: Tags Accelerate on RFID Volume Growth

Labels retained 46.63% revenue in 2025 thanks to entrenched logistic workflows, yet tags are posting a 10.98% trajectory as passive UHF inlays proliferate. Apparel and footwear brands now embed adhesive tags inside every garment, and specialized metal-mount variants expand RFID to automotive parts and surgical tools. Tag diversity enhances the Automatic Identification and Data Capture market size because vendors can price premium inlays for harsh environments while selling commoditized wet inlays at sub-penny margins for soft goods.

Cards remain relevant where smartphone penetration is low or regulations demand a physical credential. Even here, digitization trends are visible, as the European Digital Identity Wallet reduces reliance on plastic by hosting credentials in secure elements on phones. Labels continue to thrive in food, beverage, and pharma, where human-readable data must accompany machine-readable codes throughout cold-chain journeys. Meanwhile, active tags that log temperature excursions carve out a high-value niche in biologics transportation, commanding several dollars apiece.

By End-User Industry: Transportation and Logistics Lead Growth Trajectory

Retail and e-commerce commanded 31.48% revenue in 2025, but transportation and logistics are forecast to rise fastest at a 10.81% CAGR. Parcel carriers equip conveyors with RFID tunnels and vision dimensions that guarantee same-day commitments. Airlines retrofit baggage-handling lines with RFID readers to meet IATA Resolution 753, cutting mishandled rates by one-quarter. Ports trial RFID seals that transmit tamper alerts, reducing theft that costs global supply chains up to USD 30 billion per year.

Manufacturing leverages direct-part marking to satisfy traceability mandates in automotive and aerospace, and healthcare depends on barcode medication administration for patient safety. Financial institutions introduce biometric ATMs to curb identity fraud, while hospitality brands roll out mobile keys that encode room access through QR codes. Government programs like Aadhaar and Ayushman Bharat showcase how large-scale biometrics and QR cards can deliver social services efficiently. Energy utilities embed tags in smart meters and transformers, automating asset audits and predictive maintenance.

Geography Analysis

North America retained 34.77% share in 2025 thanks to early warehouse automation, stringent drug-serialization rules, and expanding biometric screening at 25 airports. Logistics operators deploy vision dimensions and RFID sortation to offset rising wages, gaining sub-18-month paybacks. Canada is ahead of the 2D barcode adoption curve, piloting QR-coded allergen disclosures in grocery. Mexico’s nearshoring boom boosts direct-part-marking demand for automotive and electronics exports. Compliance drivers such as the United States Drug Supply Chain Security Act sustain investment momentum through 2031.

Asia-Pacific is the fastest growing region at 10.91% CAGR. India’s 680 million digital health cards create massive scanner and printer deployments across public hospitals. China mandates QR acceptance for digital-yuan payments, weaving AIDC into its monetary backbone and fuelling demand for high-durability print heads. Japan combats workforce aging by merging vision systems with collaborative robots that decode codes on reflective surfaces at speeds exceeding 200 parts per minute. South Korea’s fulfilment centers deploy autonomous robots guided by RFID floor tags, and Australia pilots RFID-based livestock tracing to satisfy export regulations.

Europe enjoys strong regulatory tailwinds. The Digital Identity Wallet mandates launch by 2026, stimulating smart-card, biometric, and QR infrastructure. Germany’s contactless health card simplifies prescription workflows, and United Kingdom retailers upgrade scanners to parse 2D codes that also surface sustainability scores. Nordic logistics firms tag reusable pallets to automate deposit refunds. Southern European hospitality venues adopt mobile tickets and QR room keys that streamline visitor flows and align with hygiene norms.

South America, the Middle East, and Africa present heterogeneous growth. Brazil pilots RFID in agricultural exports to comply with upcoming deforestation-free sourcing laws. Argentina evaluates QR settlement rails to cut cash usage. Gulf Cooperation Council states invest in biometric gates and e-government platforms, while South Africa upgrades IDs with contactless chips. Nigeria combats counterfeit drugs with RFID pilot lines, and Egypt digitizes port customs with barcode-based cargo manifests to curb corruption.

Competitive Landscape

The Automatic Identification and Data Capture market is moderately fragmented: the top five players Zebra Technologies, Honeywell, Datalogic, Cognex, and Impinj control roughly 35-40% share, leaving ample room for niche specialists. Zebra leverages its installed base of mobile computers to cross-sell cloud analytics that convert scan events into stock-rotation insights. Honeywell bundles robotics and voice picking with scanners to offer turnkey automation for operators lacking integration bandwidth. Impinj defends its RAIN RFID dominance by developing energy-harvesting tags that extend read range without battery cost.

Smaller disruptors thrive by embedding scanning in off-the-shelf phones. Scandit’s computer-vision SDK lets retailers turn consumer devices into enterprise scanners at one-third the hardware cost, attractive for seasonal hiring surges. Chinese vendors such as Newland AIDC and Bluebird undercut premium handhelds by up to 40%, accelerating adoption in cost-sensitive sectors. Patent filings cluster around RFID collision management and anti-counterfeiting features; Impinj and NXP submitted more than 50 applications during 2024-2025. Standards bodies push interoperability so data flows freely across ecosystems, which compresses lock-in rents and increases price competition.

White-space opportunities emerge in cold-chain logistics, where battery-assisted tags with memory log temperature profiles and command prices several multiples higher than passive inlays. Biometric payment cards embedding fingerprint sensors gain traction in markets grappling with skimming fraud. Machine-vision suppliers embed edge AI that decodes degraded marks locally, satisfying data-residency laws that restrict cross-border image transfer. As cloud costs fall, analytics vendors stitch together barcode, RFID, and vision streams to offer predictive maintenance and shrinkage control, moving the battleground from devices to data services.

Automatic Identification And Data Capture (AIDC) Industry Leaders

Datalogic S.p.A.

SICK AG

Honeywell International Inc.

Zebra Technologies Corporation

Omron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Identiv and InPlay Technology announced co-development of BLE-enabled smart labels for high-value logistics applications, targeting cold-chain compliance and asset tracking.

- March 2025: South Korea completed national digital ID rollout for 52 million citizens, establishing comprehensive identification infrastructure that supports government services and commercial applications.

- February 2025: Armenia announced plans to launch a new biometric ID system in 2026 complying with EU standards.

- January 2025: Athens implemented contactless payment systems for public transportation fares, demonstrating growing adoption of NFC technology in urban transport infrastructure.

Global Automatic Identification And Data Capture (AIDC) Market Report Scope

The Automatic Identification and Data Capture Market Report is Segmented by Offering (Hardware, Software, Services), Product (Barcodes, RFID, Smart Cards, Biometric Systems, OCR), Media Type (Labels, Tags, Cards), End-User Industry (Manufacturing, Retail and E-Commerce, Transportation and Logistics, Healthcare and Pharma, BFSI, Hospitality, Government, Energy and Utilities), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Fixed Readers/Scanners |

| Mobile Computers and Handhelds | |

| Printers/Encoders | |

| Software | |

| Services | Integration and Consulting |

| Maintenance and Support |

| Barcodes | 1D |

| 2D/QR | |

| RFID | Passive (LF, HF, UHF) |

| Active | |

| Smart Cards | Contact |

| Contactless | |

| Biometric Systems | Fingerprint |

| Facial/Iris | |

| Optical Character Recognition (OCR) | |

| Other Products | Magnetic Stripe, NFC, BLE Tags |

| Labels |

| Tags |

| Cards |

| Manufacturing |

| Retail and E-Commerce |

| Transportation and Logistics |

| Healthcare and Pharma |

| BFSI |

| Hospitality |

| Government and Public Sector |

| Energy and Utilities |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | GCC |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Offering | Hardware | Fixed Readers/Scanners |

| Mobile Computers and Handhelds | ||

| Printers/Encoders | ||

| Software | ||

| Services | Integration and Consulting | |

| Maintenance and Support | ||

| By Product | Barcodes | 1D |

| 2D/QR | ||

| RFID | Passive (LF, HF, UHF) | |

| Active | ||

| Smart Cards | Contact | |

| Contactless | ||

| Biometric Systems | Fingerprint | |

| Facial/Iris | ||

| Optical Character Recognition (OCR) | ||

| Other Products | Magnetic Stripe, NFC, BLE Tags | |

| By Media Type | Labels | |

| Tags | ||

| Cards | ||

| By End-User Industry | Manufacturing | |

| Retail and E-Commerce | ||

| Transportation and Logistics | ||

| Healthcare and Pharma | ||

| BFSI | ||

| Hospitality | ||

| Government and Public Sector | ||

| Energy and Utilities | ||

| Others | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC | |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Automatic Identification and Data Capture market by 2031?

The sector is forecast to reach USD 142.3 billion by 2031 on the back of a 10.06% CAGR from 2026.

Which segment is expected to expand fastest through 2031?

Transportation and logistics is projected to grow at a 10.81% CAGR as carriers deploy RFID, vision dimensioners, and robotics.

How are 2D barcodes influencing retail operations?

GS1’s Sunrise 2027 mandate drives global scanner upgrades, enabling richer data such as batch numbers, allergen content, and digital-link URLs at checkout.

Why is RFID adoption accelerating in apparel?

Passive UHF tags now cost under USD 0.05, letting brands serialize each garment and achieve inventory accuracy above 98%.

What restrains vision-based AIDC uptake in legacy factories?

Brown-field retrofits often exceed USD 500,000 per line because of camera, lighting, and edge-compute requirements that stretch payback beyond three years.

Which regions will contribute most to future growth?

Asia-Pacific leads with 10.91% CAGR, fueled by India’s digital health cards, China’s digital-yuan rollout, and rapid e-commerce expansion.

Page last updated on: