Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

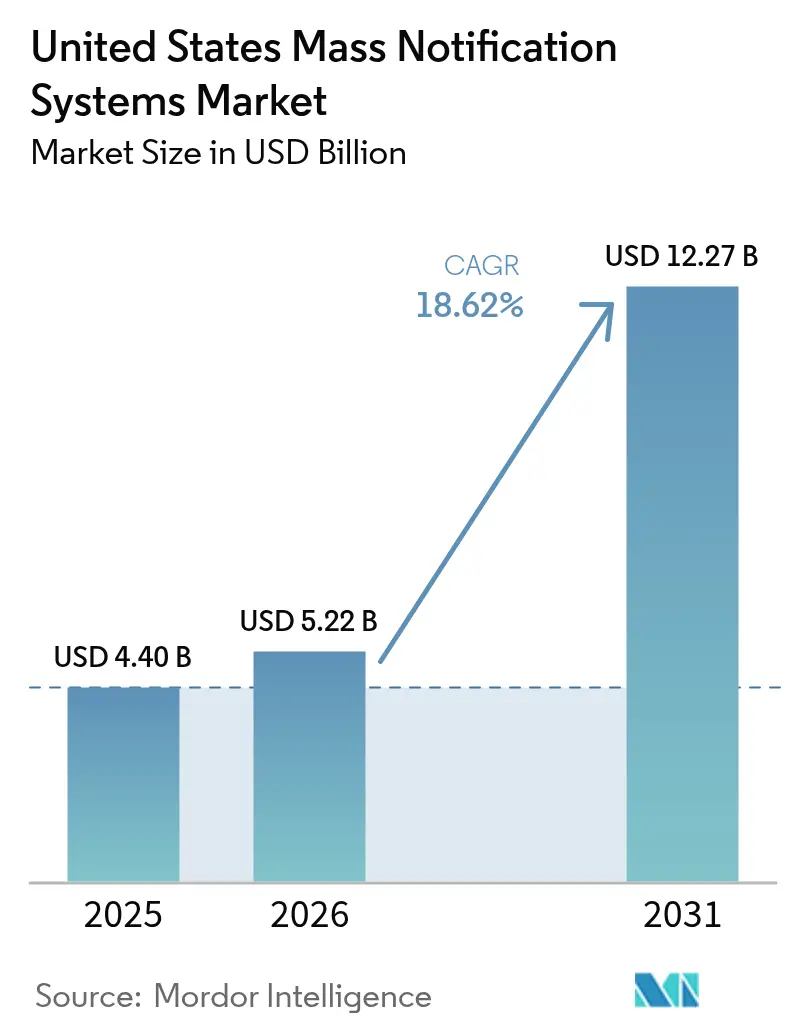

| Base Year Market Size (2025) | USD 4.40 Billion |

| Market Size (2026) | USD 5.22 Billion |

| Market Size (2031) | USD 12.27 Billion |

| Growth Rate (2026 - 2031) | 18.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Mass Notification Systems Market Analysis by Mordor Intelligence

United States mass notification systems market size in 2026 is estimated at USD 5.22 billion, growing from 2025 value of USD 4.40 billion with 2031 projections showing USD 12.27 billion, growing at 18.62% CAGR over 2026-2031. Momentum reflects simultaneous federal mandates, rapid cloud adoption, and heightened risk awareness among both public-sector and private-sector operators. Compliance deadlines tied to FEMA’s Integrated Public Alert and Warning System Open Platform 3.0 (IPAWS-Open 3.0) and the Department of Education’s Clery Act oversight have pulled forward procurement cycles, while hybrid-work policies accelerate demand for cloud-native, mobile-first alerts. Investments in 5G and artificial-intelligence-enabled incident response strengthen product differentiation, yet interoperability gaps between Project 25 (P25) radio networks and new cellular services temper near-term scalability. Competitive dynamics remain moderately fragmented; Everbridge’s 2024 take-private transaction and BlackBerry AtHoc’s FedRAMP High authorization underscore an active MandA environment and federal customer focus.

Key Report Takeaways

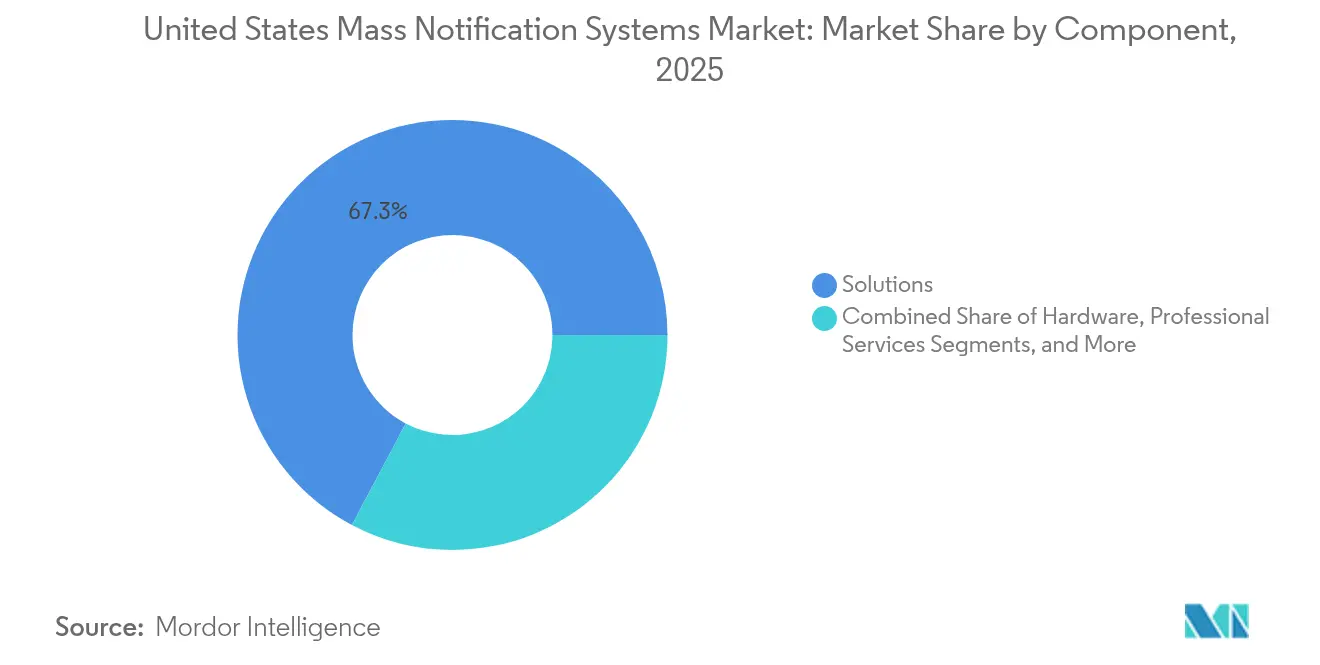

- By component, solutions held 67.25% of the United States mass notification systems market share in 2025, whereas services are set to grow at a 18.95% CAGR to 2031.

- By deployment model, cloud captured 71.80% revenue share in 2025, while hybrid is projected to expand at a 20.05% CAGR through 2031.

- By application, distributed recipient and personal alerting accounted for 45.90% of the United States mass notification systems market size in 2025; in-building systems post the highest 20.24% CAGR outlook.

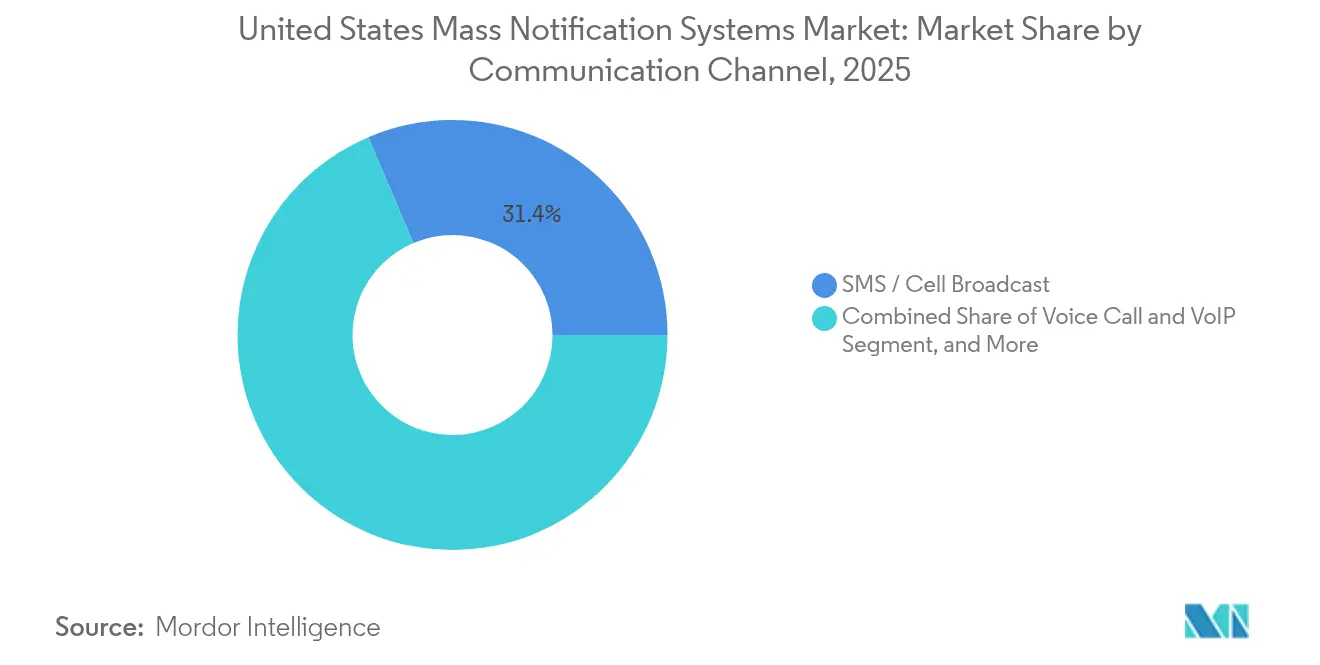

- By communication channel, SMS and text led with 31.40% share in 2025, contrasted with mobile-app push notifications advancing at 20.93% CAGR.

- By end-user vertical, government and public-safety agencies commanded 41.20% share in 2025; healthcare and life sciences represent the fastest-growing segment with a 21.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Mass Notification Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal expansion of IPAWS-Open 3.0 accelerating agency deployments | +4.20% | Nationwide; strongest among federal and state emergency-management bodies | Short term (≤ 2 years) |

| Clery-Act-driven campus-safety mandates | +2.80% | Nationwide; concentrated in states with large public-university systems | Medium term (2-4 years) |

| AI and ML integration enhancing emergency response | +3.50% | Urban centers and critical-infrastructure corridors | Long term (≥ 4 years) |

| Convergence of multiple federal safety mandates | +2.10% | Nationwide; all federal agencies and contractors | Medium term (2-4 years) |

| Cloud-native platforms enabling hybrid-work use cases | +1.90% | Major metropolitan areas with distributed workforces | Short term (≤ 2 years) |

| Next Generation 911 infrastructure modernization | +2.40% | State and local public-safety answering points (PSAPs) nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal Expansion of IPAWS-Open 3.0 Accelerating Agency Deployments

IPAWS-Open 3.0 authorizations surpassed 1,800 alerting authorities in 2024, compelling upgrades across federal, state, local, tribal, and territorial jurisdictions. The FCC’s December 2024 rule requiring IP-based Emergency Alert System transmissions intensified compliance timelines, catalyzing rapid contract awards for BlackBerry AtHoc-compatible solutions [1]Federal Communications Commission, “FCC Sets Dates for Improved Emergency Alert System Messages,” fcc.gov. Concurrently, a USD 136 million Corporation for Public Broadcasting grant accelerates infrastructure modernization for underserved rural and tribal broadcasters.

Clery-Act-Driven Campus Safety Mandates Fueling Higher-Ed Spend

The Department of Education can now levy USD 35,000 per violation for deficient campus alerts, compelling universities to adopt integrated platforms that bundle incident management with mass communication. Vanderbilt University’s AlertVU upgrade illustrates the shift toward centralized command systems. Recent studies indicate more than 80% of higher-education safety professionals find these platforms effective in shaping real-time behavior.

AI and ML to Revolutionize Security and Emergency Response

DHS Science and Technology Directorate pilots show wildfire-response times improving when AI analyzes satellite imagery and atmospheric data. Colorado’s statewide wildfire-risk mapping leverages similar models, while NTIA notes AI-driven 911 call-triage cuts volume by 30% and lifts efficiency by up to 10%. January 2025 FCC approval of multilingual WEA templates in 13 languages positions AI translation as a pivotal accessibility tool.

Convergence of Federal Safety Mandates on Next-Generation Notification Systems

New cyber-incident reporting rules require critical-infrastructure owners to alert CISA within 72 hours, pushing demand for automated, multi-channel notification workflows. TSA’s FY 2024-2028 Capital Investment Plan likewise prioritizes cybersecurity and automated screening in transportation nodes, reinforcing interoperability requirements. EMPG funding of USD 355.1 million targets climate-resilient alert capabilities, further standardizing platform adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability gaps between legacy P25 radio and 5G networks | −2.7% | Rural and tribal jurisdictions nationwide | Medium term (2-4 years) |

| Budget shortfalls in rural municipalities | −1.8% | Small counties and townships across rural America | Long term (≥ 4 years) |

| Expanding data-privacy and breach-notification compliance burden | −1.3% | States with newly strengthened privacy statutes | Medium term (2-4 years) |

| Public alert-fatigue after past false-alarm incidents | −1.0% | Regions with high exposure to frequent test alerts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps with Legacy P25 and 5G Networks

CISA’s LMR/LTE best-practices guide underscores persistent technical hurdles in patching P25 talk groups to broadband channels. Santa Fe County’s USD 8.1 million P25 overhaul—backed by just USD 425,000 in state aid—illustrates the fiscal weight of radio upgrades. The FCC’s 2025 NG911 reliability docket may further widen the gap if existing radio networks cannot meet new standards.

Budget Shortfalls in Rural Municipalities

Declining fee revenue and competing priorities constrain rural 911 centers, with counties increasingly diverting general funds to maintain basic service levels. A USD 2.2 billion NG911 requirement in New York alone exemplifies the scale of modernization costs that exceed local capacities. Hazard-mitigation plans highlight the administrative burden of multiyear grant compliance, often outstripping the staffing resources of small jurisdictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Outpaces Solutions Dominance

The solutions segment accounted for 67.25% of the United States mass notification systems market in 2025, underscoring entrenched spending on core alerting platforms. Services revenue, however, is rising at a 18.95% CAGR as organizations rely on managed integrations to meet IPAWS-Open 3.0 and FedRAMP benchmarks. Professional-services providers benefit from growing demand for AI-enabled analytics configuration and 24/7 system monitoring.

Hardware margins are tightening as cloud architectures reduce on-premises footprint, yet specialized devices such as Alertus Beacons remain indispensable in hospitals and campuses requiring audible and visual redundancy. Subscription licensing aligns vendors and buyers to continuous-update roadmaps, while training services emerge to unlock machine-learning-based threat detection. As a result, services are positioned to capture a growing share of the United States mass notification systems market size, particularly among mid-tier municipalities lacking in-house expertise.

By Deployment: Hybrid Models Bridge Cloud–Premises Divide

Cloud delivery dominated 71.80% of the United States mass notification systems market in 2025, but hybrid models—expanding at 20.05% CAGR—offer the preferred compromise between scalability and data-sovereignty requirements. Federal agencies with classified workloads demand on-premises storage paired with cloud distribution layers, a configuration reinforced by the FedRAMP High framework now supporting BlackBerry AtHoc deployments.

Healthcare providers adopt hybrid to safeguard electronic health information under HIPAA while retaining rapid alert dissemination to mobile caregivers. NG911 migration likewise pulls state PSAPs toward public-cloud resilience. As 5G expands, hybrid architectures are poised to capture a larger portion of the United States mass notification systems market share among enterprises integrating legacy P25 radios with broadband push-to-talk applications.

By Application: In-Building Systems Gain Momentum

Distributed recipient and personal alerting retained 45.90% share of the United States mass notification systems market size in 2025, reflecting the ubiquity of SMS, email, and push communications. In-building notification, however, is charting a 20.24% CAGR as stricter life-safety codes demand targeted alerts that minimize patient and student disruption.

Elevator communication standards requiring video and two-way voice coverage now cover 75% of U.S. jurisdictions, driving retrofits of cab systems. Hospitals deploy real-time location wearables for staff duress calls, while colleges embrace alert beacons to broadcast room-level instructions during severe-weather incidents.

By Communication Channel: Mobile Apps Transform Alert Delivery

SMS held 31.40% of 2025 revenue, prized for network reliability under congestion. Mobile-app push notifications are growing at 20.93% CAGR as organizations favor rich media, read-receipt tracking, and two-way chat. FCC multilingual templates enhance SMS reach but delayed rollouts push adopters toward app-based instant translation.

Voice and VoIP channels remain critical when human confirmation is needed during evacuations. Public-address sirens persist for wide-area coverage, with cloud-controlled systems enabling remote activation. IoT device alerts, leveraging smart-building sensors, represent an emerging avenue expected to deepen recipient engagement.

By End-User Vertical: Healthcare Emerges as Growth Leader

Government and public-safety bodies generated 41.20% of 2025 revenue, reflecting statutory duties to warn populations. Healthcare and life sciences are on track for a 21.08% CAGR as patient-centric facilities deploy silent, room-specific alerts that protect privacy while ensuring rapid incident response.

Education maintains robust budgets under Clery Act scrutiny, with more than 350 colleges subscribing to InformaCast for integrated voice, text, and digital-signage alerts. Energy, utilities, and transport operators embed mass-notification within SCADA, airport, and rail workflows to safeguard critical infrastructure amid rising cyber threats.

Geography Analysis

Federal agencies have largely harmonized requirements, and BlackBerry AtHoc now supports 80% of federal employees following its 2025 FedRAMP High clearance. State and municipal adoption is patchy; well-funded metros such as Los Angeles International Airport (LAWA) deploy multi-channel systems with stakeholder segmentation . Rural and tribal areas remain dependent on FEMA and CPB grants to modernize broadcast relay towers, underscoring an uneven security baseline.

Natural-hazard profiles shape regional spending. Southeast states emphasize hurricane-resilient outdoor sirens, while western jurisdictions prioritize wildfire and earthquake alerts. Hawaii’s post-2018 false-alert reforms now include periodic test messages to combat alert fatigue and rebuild public trust. Coastal emergency-management offices additionally coordinate with the Pacific Tsunami Warning Center, integrating local siren activations with global seismic data.

Higher-education concentration in the Northeast accelerates Clery Act–led deployments, while the Southwest’s rapid population growth fuels municipal demand for scalable cloud solutions. Academic medical centers act as innovation hubs, piloting AI-triage extensions that later trickle to community hospitals. Consequently, regional disparities in funding, hazard exposure, and institutional density collectively steer adoption trajectories across the United States mass notification systems market.

Competitive Landscape

The United States mass notification systems market remains moderately fragmented. Everbridge’s USD 1.8 billion buyout by Thoma Bravo positions the platform for product-suite rationalization and cross-portfolio expansion [3]Everbridge, “Merger Agreement with Thoma Bravo,” everbridge.com. BlackBerry AtHoc’s April 2025 FedRAMP High authorization differentiates its offering for classified federal use cases, potentially locking in long-term subscription annuities.

Motorola Solutions consolidates complementary capabilities, adding RapidDeploy and Theatro for USD 414 million to fuse cloud-based CAD and in-store communications with its P25 backbone, supporting 6% year-on-year revenue growth in Q1-2025. Smaller innovators such as Regroup gain share via feature depth and vertical templates, evidenced by SourceForge user-satisfaction accolades.

Strategic differentiation increasingly rests on AI-powered analytics, multilingual capabilities, and proven compliance automation. Patent activity around IoT-based emergency-location information signals future competition over sensor-native alert delivery [4]Google Patents, “Emergency Location Information Service for IoT,” patents.google.com. Overall, the breadth of public-sector requirements and rapid technology cycles ensure no single vendor eclipses the market, preserving space for niche specialists alongside large integrated-platform providers.

United States Mass Notification Systems Industry Leaders

Everbridge, Inc.

Motorola Solutions, Inc.

Intrado Life & Safety (West Corp.)

OnSolve, LLC

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Motorola Solutions reported USD 2.5 billion Q1 sales, supported by managed-services and P25 contracts.

- April 2025: BlackBerry secured FedRAMP High authorization for AtHoc, expanding its addressable federal cloud market.

- February 2025: Everbridge completed its USD 1.8 billion acquisition by Thoma Bravo at USD 35.00 per share.

- January 2025: FCC approved multilingual Wireless Emergency Alert templates in 13 languages, pending implementation.

United States Mass Notification Systems Market Report Scope

The rapid growth of United States government investments in different public safety purposes is fueling the growth of this market. Moreover, this market is segmented by Component, Deployment, Application, and End-users. However, Application division is further segmented by building, Wide-area, Distributed Recipient further segment its Application segment.

By Component

| Hardware |

| Software |

| Professional Services |

| Managed Services |

By Deployment

| On-Premise |

| Cloud |

| Hybrid |

By Application

| In-Building |

| Wide-Area Outdoor |

| Distributed Recipient / Personal Alerting |

By Communication Channel

| SMS / Cell Broadcast |

| Voice Call and VoIP |

| Email and Desktop Pop-Ups |

| Public Address and Siren Systems |

| Social Media and Web Feed |

| IoT and Connected Device Notifications |

By End-User Vertical

| Government and Public Safety |

| Education (K-12 and Higher-Ed) |

| Healthcare Facilities |

| Energy and Utilities |

| Transportation and Logistics |

| Industrial and Manufacturing |

| Commercial and Corporate Enterprises |

| By Component | Hardware |

| Software | |

| Professional Services | |

| Managed Services | |

| By Deployment | On-Premise |

| Cloud | |

| Hybrid | |

| By Application | In-Building |

| Wide-Area Outdoor | |

| Distributed Recipient / Personal Alerting | |

| By Communication Channel | SMS / Cell Broadcast |

| Voice Call and VoIP | |

| Email and Desktop Pop-Ups | |

| Public Address and Siren Systems | |

| Social Media and Web Feed | |

| IoT and Connected Device Notifications | |

| By End-User Vertical | Government and Public Safety |

| Education (K-12 and Higher-Ed) | |

| Healthcare Facilities | |

| Energy and Utilities | |

| Transportation and Logistics | |

| Industrial and Manufacturing | |

| Commercial and Corporate Enterprises |

Key Questions Answered in the Report

What is the current value of the United States mass notification systems market?

The market is valued at USD 5.22 billion in 2026.

How fast is the United States mass notification systems market expected to grow?

A CAGR of 18.62% is projected between 2026 and 2031.

Which deployment model is expanding most rapidly?

Hybrid architectures are forecast to grow at a 20.05% CAGR as agencies blend cloud scalability with on-premises control.

Which end-user vertical shows the highest growth potential?

Healthcare and life sciences lead with a 21.08% CAGR through 2031 due to patient-centric safety requirements.

Page last updated on: