Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 51.55 Billion |

| Market Size (2026) | USD 53.77 Billion |

| Market Size (2031) | USD 73.09 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

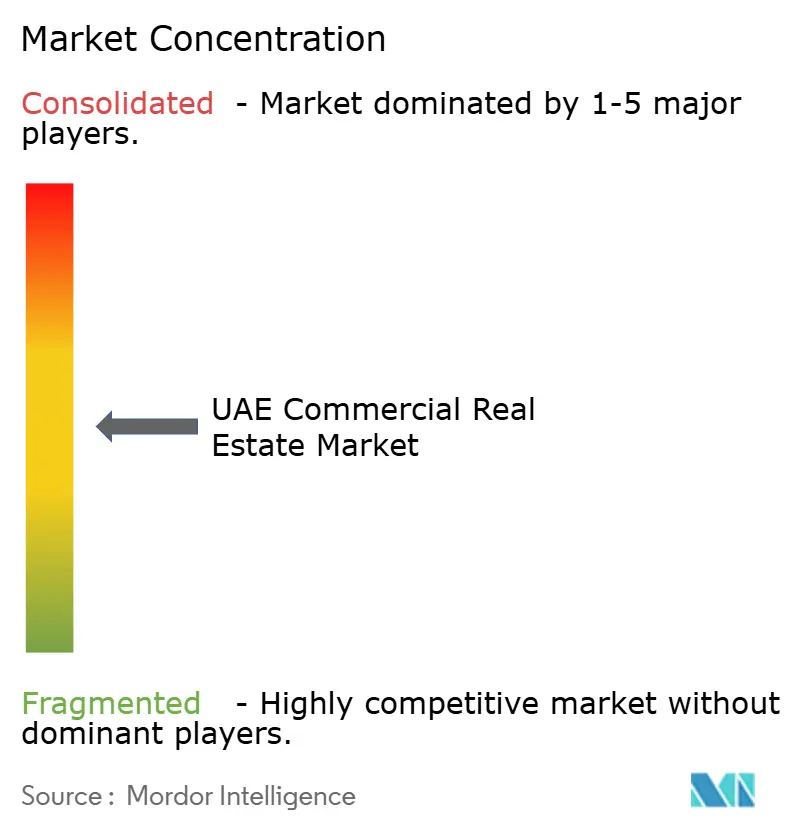

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Commercial Real Estate Market Analysis by Mordor Intelligence

The UAE commercial real estate market size is projected to be USD 51.55 billion in 2025, USD 53.77 billion in 2026, and reach USD 73.09 billion by 2031, growing at a CAGR of 6.33% from 2026 to 2031[1]JLL Research, “Dubai Real Estate Market Overview H1 2025,” JLL.com. As golden-visa reforms attract fresh wealth, prime-office vacancies in Dubai and Abu Dhabi remain below 0.5%, intensifying rent growth and steering capital toward development pipelines. Concurrently, sovereign funds are redirecting energy windfalls into last-mile logistics, data centers, and mixed-use towers, while three base-rate cuts in 2025 reduce borrowing costs and sustain transaction velocity. Developers able to secure land in free zones or industrial clusters are capitalizing on nearshoring and e-commerce demand, whereas smaller sponsors face escalating land prices and green-building compliance costs. Overall, the UAE commercial real estate market benefits from regulatory liberalization, infrastructure spending, and the country’s status as a finance and logistics gateway.

Key Report Takeaways

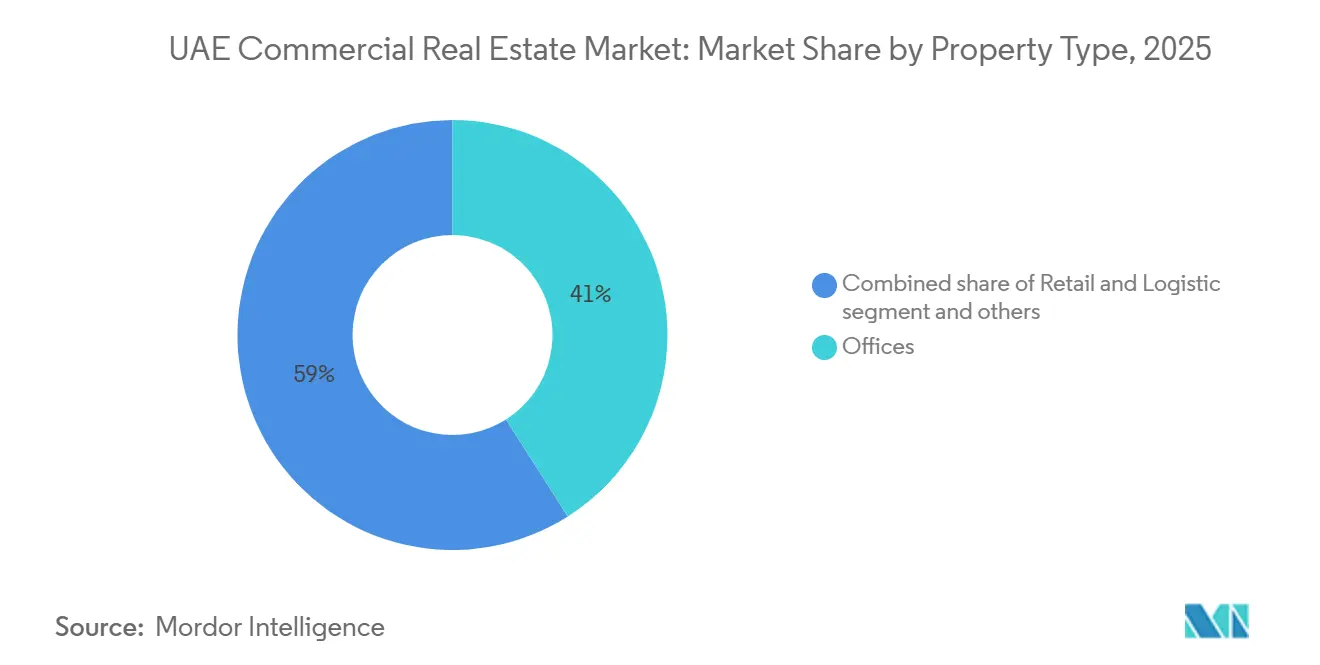

- By property type, offices led with 41% of UAE commercial real estate market share in 2025; logistics is projected to record the fastest 7.80 % CAGR through 2031.

- By business model, rental transactions captured 67% of UAE commercial real estate market share in 2025, while strata sales are forecast to expand at a 6.10 % CAGR to 2031.

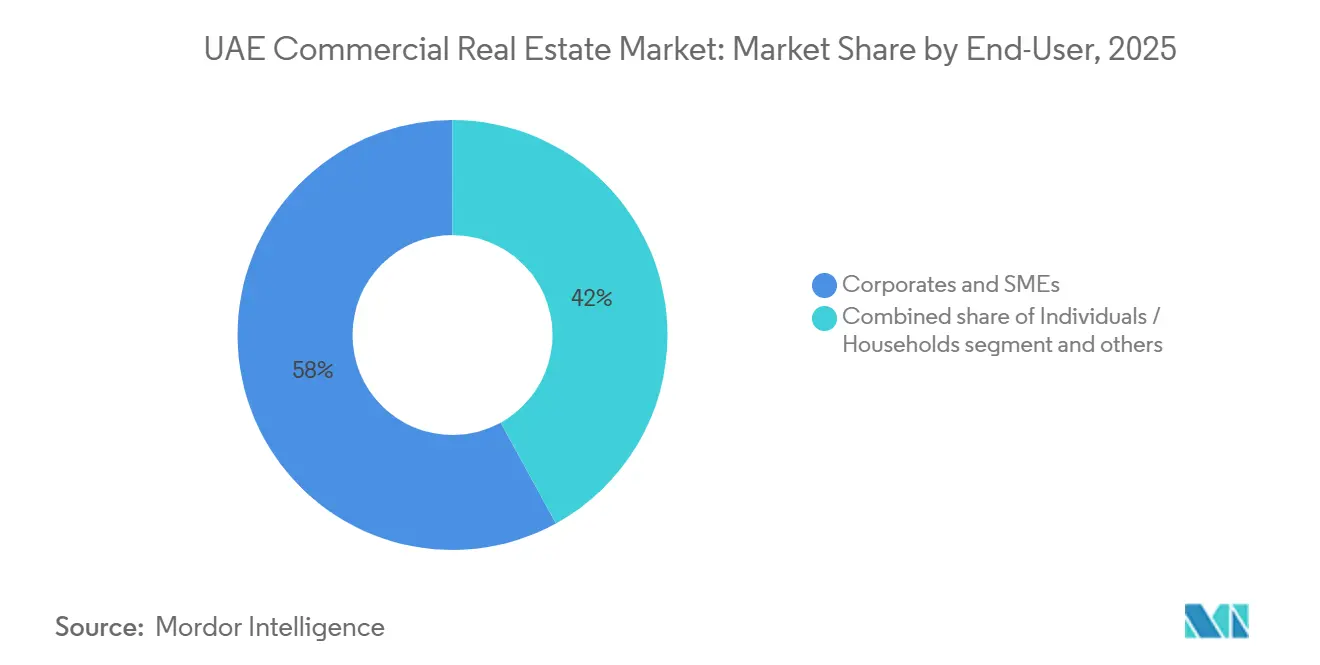

- By end user, corporates and SMEs accounted for 58% of the UAE commercial real estate market size in 2025, whereas individual and household participation is expected to grow at a 6.90 % CAGR between 2026 and 2031.

- By region, Dubai captured 55% of UAE commercial real estate market share in 2025, while Ras Al Khaimah is poised to expand at an 8.1 % CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-1 % prime-office vacancy lifts effective rents | +1.5 % | DIFC, Downtown, Business Bay, ADGM, Al Reem Island | Short term (≤ 2 years) |

| Nearshoring fuels logistics build-to-suit pipelines | +1.3 % | RAK Erisha, Abu Dhabi KEZAD, Dubai Jebel Ali & DIC | Long term (≥ 4 years) |

| Golden-visa inflows unlock permanent investor demand | +1.2 % | Dubai, Abu Dhabi, spillover to Sharjah & RAK | Medium term (2-4 years) |

| Tourism boom under Dubai 2040 expands hospitality footprints | +0.9 % | Dubai coastal zones, Sharjah & RAK beach corridors | Medium term (2-4 years) |

| Corporate net-zero targets push green-building premiums | +0.8 % | Abu Dhabi Estidama, Dubai Al Sa'fat | Long term (≥ 4 years) |

| AI-enabled property management trims operating costs | +0.5 % | Institutional portfolios in Dubai & Abu Dhabi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Golden-Visa Inflows Unlock Permanent Investor Demand

Residency reforms introduced five-year and ten-year permits that removed the need for sponsors, shifting capital from speculative flips to long-horizon income assets. Roughly 10,000 high-net-worth migrants entered the Emirates during 2025, and many directed liquidity toward Grade-A offices in DIFC or strata logistics units in Jebel Ali. Dubai recorded USD 14.24 billion of greenfield FDI in 2024, up 48 % year-on-year, with real estate comprising close to one-tenth of projects[2]Dubai FDI, “FDI Monitor 2024,” Dubaifdi.gov.ae. Offices, logistics parks, and data-center shells now serve as both yield vehicles and residency anchors. The policy also pulls portfolio diversification toward Ras Al Khaimah free-hold clusters, widening geographic dispersion of the UAE commercial real estate market. Looking ahead, steady visa approvals should continue to compress yields, especially for trophy assets that combine security, prestige, and passport optionality.

Sub-1 % Prime-Office Vacancy Lifts Effective Rents

Dubai and Abu Dhabi Grade-A vacancies tightened to 0.3 % and 0.1 %, respectively, during 2025. Limited handovers meant lease rates jumped 19 %-22 % in Dubai and 29 %-31 % in Abu Dhabi even as inflation stayed subdued. Corporations, therefore, renegotiated shorter commitments or relocated to emerging corridors such as Dubai Hills Business Park. Developers responded by fast-tracking space in TECOM’s Innovation Hub Phase 4 and DMCC’s 600-meter Uptown megatower. Meanwhile, LEED-certified buildings enjoyed 96 % occupancy and a 33 % rent premium thanks to tenant ESG mandates. With supply additions back-weighted to 2027-2028, landlords are positioned to maintain pricing power in the UAE commercial real estate market.

Nearshoring Fuels Logistics Build-to-Suit Pipelines

Manufacturers shifting production closer to demand centers are securing long leases in free zones. Ras Al Khaimah’s USD 10 billion Erisha hub will span 25 million sq ft for EVs, chips, and hydrogen systems. KEZAD captured more than USD 1.6 billion of fresh commitments in 2024-2025 from Azizi, Jindal SAW, and Jotun. Industrial rents grew 18 %-20 % while occupancy stayed near 95 %, yet yields of roughly 7 % still provide a 250-basis-point spread over sovereign bonds. Logistics is moving from tactical to core exposure in institutional portfolios, encouraging developers like Aldar and TECOM to acquire land banks exceeding 30 million sq ft in Dubai Industrial City. Over the long term, multi-story warehousing and cold-chain facilities are expected to headline new completions across the UAE commercial real estate market.

Tourism Boom Under Dubai 2040 Expands Hospitality Footprints

Dubai welcomed 19.59 million international guests in 2025, pushing average occupancy close to 80 % and ADRs above pre-COVID peaks. The Dubai 2040 Master Plan targets a 134 % increase in designated tourism land and population growth to 5.8 million. Developers are therefore blending hotels, serviced apartments, and retail promenades: Nakheel’s Palm Jebel Ali revamp and Marjan’s 12,000-key Ras Al Khaimah resort typify the trend. Retail contributes over one-quarter of Dubai GDP, and prime super-regional mall rents climbed 13.5 % in 2025, although experiential concepts are displacing traditional anchors. Sustained visitor inflows underpin mixed-use asset pricing across the UAE commercial real estate market, but infrastructure capacity must keep pace with tourist numbers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interest-rate swings shrink cap-rate spreads | -0.6 % | Dubai & Abu Dhabi institutional corridors | Short term (≤ 2 years) |

| Scarce non-freehold zones outside Dubai limit foreign inflows | -0.4 % | Abu Dhabi, Sharjah & RAK | Medium term (2-4 years) |

| Secondary retail oversupply threatens suburban rents | -0.3 % | Dubai outskirts, Sharjah, Ajman | Medium term (2-4 years) |

| Data-sovereignty rules delay hyperscale data-center launches | -0.2 % | Dubai & Abu Dhabi ICT clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interest-Rate Swings Shrink Cap-Rate Spreads

The Central Bank trimmed its policy rate to 3.65 % in 2025, yet cap-rate compression outpaced borrowing-cost cuts, narrowing spreads for levered buyers. Institutional logistics yields held near 7 %, still 250 bp above five-year UAE notes, but prime offices traded at record low yields amid an 84 % surge in Dubai office transactions to USD 1.47 billion in H1 2025. Should global inflation rebound, rate hikes would erode debt-financed returns and dampen the UAE commercial real estate market size allocated to trophy assets. REIT payouts could also soften, pressuring unit prices. Consequently, sponsors are increasing fixed-rate hedging and exploring sukuk issuance to stabilize funding costs.

Scarce Non-Freehold Zones Outside Dubai Limit Foreign Inflows

Dubai offers clear freehold title across most districts, but Abu Dhabi and northern emirates still rely on usufruct or long leases, constraining asset-allocation mandates that require fee-simple ownership[3]Abu Dhabi Real Estate Centre, “Market Report 2025,” Adrec.gov.ae. Foreign buyers represented 62 % of Abu Dhabi residential sales in 2025, yet commercial options remain largely tied to ADGM and Al Reem Island. Ras Al Khaimah’s Erisha hub uses hybrid tenure models that pension funds often flag as higher risk. Without broader freehold expansion, the UAE commercial real estate market risks over-reliance on Dubai for cross-border inflows. Policymakers are studying unified title frameworks, but near-term execution remains uncertain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Logistics Surges from a Smaller Base

Offices commanded 41% of UAE commercial real estate market share in 2025 on the back of relocations into DIFC and ADGM. Even so, the UAE commercial real estate market size attributable to logistics is poised to rise fastest, expanding at a 7.80% CAGR through 2031 as nearshoring, cold-chain needs, and e-commerce fulfillment reshape land demand in Jebel Ali, KEZAD, and Erisha. Industrial occupancy hovered near 95% in 2025, fostering double-digit rent growth despite a wave of speculative warehouses. Yields near 7% continue to entice sovereign funds, prompting Aldar and TECOM to amass 33 million sq ft of plots in Dubai Industrial City.

Developers are future-proofing stock with high-clearance bays, automated racking, and solar rooftops to comply with Estidama standards. Conversely, secondary offices face obsolescence risk unless upgraded for ESG compliance, a trend underscored by Abu Dhabi LEED premiums. Retail supply climbed to 8.24 million sq m in 2025; while super-regional malls retained occupancy above 95%, community centers compete on experiential offerings like food halls and esports. Mixed-use skyscrapers such as DMCC’s Uptown Phase 3, which combines a five-star hotel, sky residences, and 50% office space, illustrate capital rotation into vertical, multipurpose assets that diversify revenue. Overall, the dichotomy between logistics growth and office dominance will define capital allocation within the UAE commercial real estate market.

By Business Model: Rentals Remain the Institutional Core

Rental transactions captured 67% of the UAE commercial real estate market share in 2025, reflecting pension-fund appetite for predictable cash flow and 5% - 8% dividend yields. Dubai Residential REIT raised USD 3.9 billion in its May 2025 IPO and reported 98.3% occupancy, underscoring investor confidence in stabilized portfolios. Emirates REIT saw property income climb 24% year-on-year as the loan-to-value dropped to 20 %, improving borrowing headroom.

Sales, largely strata offices and build-to-sell industrial condos, are forecast to grow at a 6.10% CAGR, buoyed by golden-visa applicants seeking asset-backed residency. Developers like Azizi are layering sales with long-term leaseback options to satisfy both private and institutional investors. The UAE’s 80 % REIT profit-distribution rule and corporate-tax exemptions keep listed vehicles hungry for acquisitions, further anchoring rental penetration in the UAE commercial real estate market size. Over time, blended models combining upfront sales proceeds with master leases could evolve, giving sponsors balance-sheet flexibility while retaining recurring income.

By End User: Corporates Anchor Demand, Households Accelerate

Corporates and SMEs represented 58% of the UAE commercial real estate market size in 2025, driven by banking, asset-management, and sovereign entities clustering in DIFC and ADGM. As visa reforms entice entrepreneurs, SME office take-up in Dubai Hills and Masdar City is growing swiftly. Household participation is set to expand at a 6.90% CAGR as expatriates shift from short leases to ownership or long-term rental in integrated communities like Palm Jebel Ali and Ghaf Woods.

Listed REITs are beginning to blur lines between end-users: ENBD REIT’s 96% occupancy spans both corporate offices and mid-market residential, while its net asset value rose 20.3% in H1 2025. Family offices and sovereign wealth funds (“Others”) increased allocations following Bloomberg’s projection of GCC REIT AUM reaching USD 16.7 billion by 2030. The confluence of corporate expansions, affluent migrant inflows, and institutional fund formation continues to enrich the demand mosaic across the UAE commercial real estate market.

Geography Analysis

Dubai retained 55 % of transaction value in 2025, fueled by activity in DIFC, Downtown, and Jebel Ali, where office prices rose 22 % and rents grew 26 % year-on-year. Emaar’s December 2025 unveiling of Dubai Square and Dubai Mansions, part of a USD 27.2 billion masterplan, adds 40,000 ultra-luxury residences aimed at golden-visa cohorts. Meanwhile, TECOM launched Innovation Hub Phase 4 and acquired 138 plots in Dubai Industrial City for USD 436 million to meet tech-tenant demand, reinforcing the emirate’s dominance in the UAE commercial real estate market.

Abu Dhabi’s total deal value climbed 44 % to USD 38.7 billion in 2025 as sales accounted for two-thirds of activity and apartment prices rose 19 %. Aldar issued USD 18 billion in development contracts, expanded its Dubai Holding joint venture to USD 10.3 billion, and progressed Noon-Emtelle industrial assets exceeding USD 155 million, spreading its footprint beyond Yas and Al Reem Islands. KEZAD sealed USD 1.6 billion of manufacturing pledges, bolstering warehouse absorption and positioning Abu Dhabi as a logistics heavyweight.

Ras Al Khaimah is forecast to lead growth at an 8.1 % CAGR, anchored by the USD 10 billion Erisha hub and Marjan Beach’s 12,000 hotel keys plus 22,000 residential units. Sharjah and Ajman capture affordability-driven spillover, as evidenced by Sobha’s USD 20 billion Downtown UAQ plan featuring 7 km of beachfront. The geographic mosaic underlines a gradual diffusion of the UAE commercial real estate market away from Dubai toward multi-emirate nodes, although divergent title regimes and building codes raise due-diligence costs and prolong deal cycles.

Competitive Landscape

Market structure remains moderately concentrated: state-linked giants such as Emaar, Aldar, and TECOM command premium land allocations and pipeline depth, whereas private developers like Azizi, Binghatti, and Sobha focus on mid-income and branded-residential niches. TECOM booked USD 789 million in revenue in 2025 with 97 % portfolio occupancy after investing USD 680 million in additional land banks. Aldar’s vertical integration strategy spans contracting arms, property management, and REIT vehicles, supporting USD 18 billion of awards and 45 % in-country value recirculation during 2025.

Strategic moves emphasize cross-emirate partnerships: Aldar-Dubai Holding’s USD 10.3 billion JV de-risks exposure by combining Dubai marketing strength with Abu Dhabi capital. PropTech collaborations are also shaping competition, for instance, DIFC’s tie-up with Keyper advances data transparency, while Yardi’s platform adoption by Emirates Properties reduces operating expenditure. Developers are racing to secure LEED or Estidama badges; 57 % of TECOM’s GLA is certified, placing pressure on laggards whose assets risk liquidity discounts within the UAE commercial real estate market.

White-space opportunities persist in secondary logistics retrofits, hyperscale data-center shells, and affordable housing across Sharjah and Ajman. DP World, long dominant in port logistics, is now monetizing export-processing zones through build-to-suit warehouses that align with nearshoring demand. Bloom Holding is diversifying into hospitality-anchored communities, expanding beyond Abu Dhabi into Northern Emirates resorts. Overall, competitive dynamics reward scale, sustainability credentials, and technology adoption, reinforcing a flight-to-quality narrative across the UAE commercial real estate market.

UAE Commercial Real Estate Industry Leaders

Emaar Properties PJSC

Aldar Properties PJSC

TECOM Group PJSC

Majid Al Futtaim Holding LLC

Nakheel PJSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Union Properties launched Mirdad Tower 2, a USD 545 million smart residential project with 50 % EV-charging readiness.

- January 2026: Deca Properties broke ground on Avana Residences in JVC, integrating 70 wellness amenities for delivery in Q4 2027.

- December 2025: Emaar revealed Dubai Square and Dubai Mansions within a USD 27.2 billion luxury masterplan.

- November 2025: Microsoft and G42 confirmed a 200 MW data-center expansion to serve AI workloads.

UAE Commercial Real Estate Market Report Scope

By Property Type

| Offices |

| Retail |

| Logistics |

| Others (Industrial, Hospitality etc.) |

By Business Model

| Sales |

| Rental |

By End-User

| Individuals / Households |

| Corporates & SMEs |

| Others |

By Region

| Dubai |

| Abu Dhabi |

| Sharjah |

| Ras Al Khaimah |

| Rest of UAE |

| By Property Type | Offices |

| Retail | |

| Logistics | |

| Others (Industrial, Hospitality etc.) | |

| By Business Model | Sales |

| Rental | |

| By End-User | Individuals / Households |

| Corporates & SMEs | |

| Others | |

| By Region | Dubai |

| Abu Dhabi | |

| Sharjah | |

| Ras Al Khaimah | |

| Rest of UAE |

Key Questions Answered in the Report

How big will office space remain in the UAE after 2030?

Offices held 41% of 2025 transaction value, and despite logistics growth, Grade-A office pipelines suggest sustained relevance through 2031.

Which emirate offers the fastest growth in commercial real estate?

Ras Al Khaimah is forecast to register an 8.1% CAGR through 2031, underpinned by the USD 10 billion Erisha manufacturing hub.

What returns can investors expect from stabilized UAE REITs?

Listed REITs such as Dubai Residential REIT provide 7 % - 8 % dividend yields, reflecting strong occupancy and rental escalation.

Are green-building certifications influencing valuations?

Yes, LEED-certified offices receive rent premiums of about 33% and occupancy exceeding 95%, boosting asset valuations.

How are interest-rate changes affecting cap rates?

Base-rate cuts narrowed spreads, so future hikes could pressure leveraged returns, particularly in prime office and retail assets.

Page last updated on: