Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

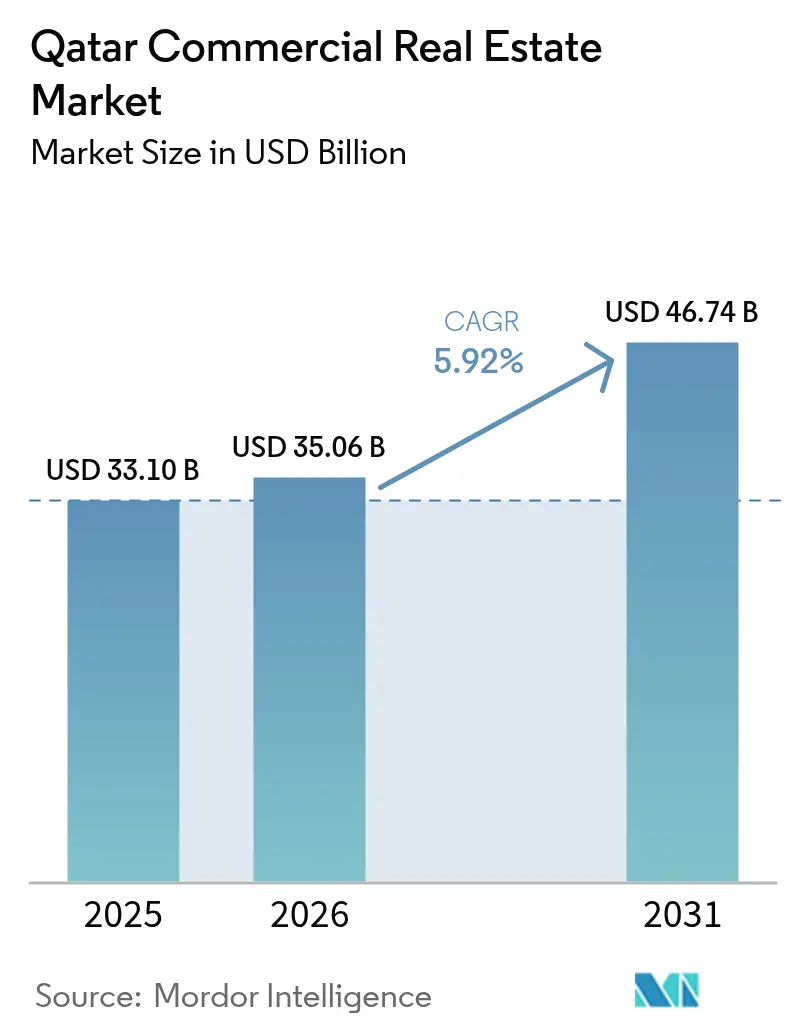

| Base Year Market Size (2025) | USD 33.10 Billion |

| Market Size (2026) | USD 35.06 Billion |

| Market Size (2031) | USD 46.74 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

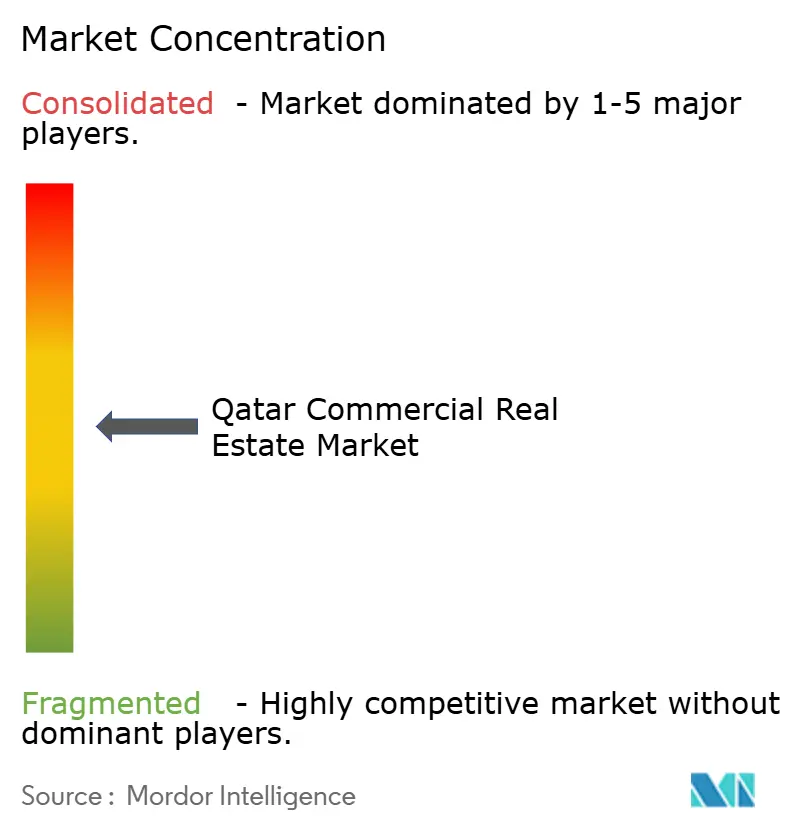

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Commercial Real Estate Market Analysis by Mordor Intelligence

The Qatar commercial real estate market size is expected to grow from USD 33.10 billion in 2025 to USD 35.06 billion in 2026 and is forecast to reach USD 46.74 billion by 2031 at 5.92% CAGR over 2026-2031. Growth remains anchored in the government’s USD 350 billion sustainable-development pipeline and the Third National Development Strategy, which together widen demand for offices, logistics facilities, and mixed-use projects across the country. New-generation free-zone policies that allow 100% foreign ownership, plus residency incentives linked to property investment, continue to draw international corporates and institutional investors, while rising e-commerce volumes accelerate the need for automated last-mile hubs near Hamad Port and Greater Doha. Liquidity conditions are supportive: Qatari banks expanded real-estate lending by 6.3% year on year in 2024, signalling confidence in the sector’s medium-term outlook. At the same time, oversupply in post-World-Cup office and hospitality stock is being absorbed through adaptive-reuse programs, green retrofits, and flexible leasing models that match changing occupier preferences. Advancing construction-tech adoption—highlighted by AI-enabled design showcased at ConteQ Expo24—lowers long-run operating costs and strengthens competitive positioning for new asset[1]Vítor Gaspar, “Qatar: 2024 Article IV Consultation—Press Release; Staff Report,” International Monetary Fund, imf.org.

Key Report Takeaways

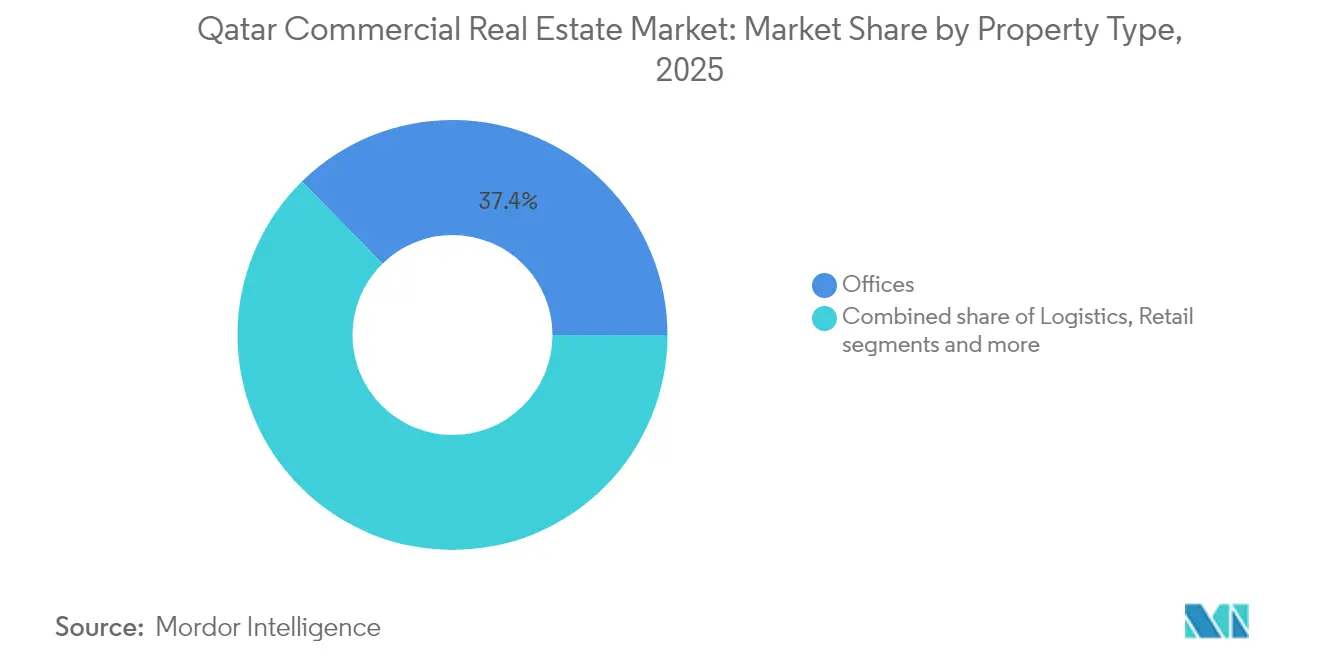

- By property type, Offices led with 37.35% of Qatar commercial real estate market share in 2025, whereas Logistics is projected to register the fastest 6.01% CAGR to 2031.

- By business model, Sales transactions dominated with 63.25% of the Qatar commercial real estate market in 2025, yet Rentals are forecast to grow at 6.15% CAGR through 2031.

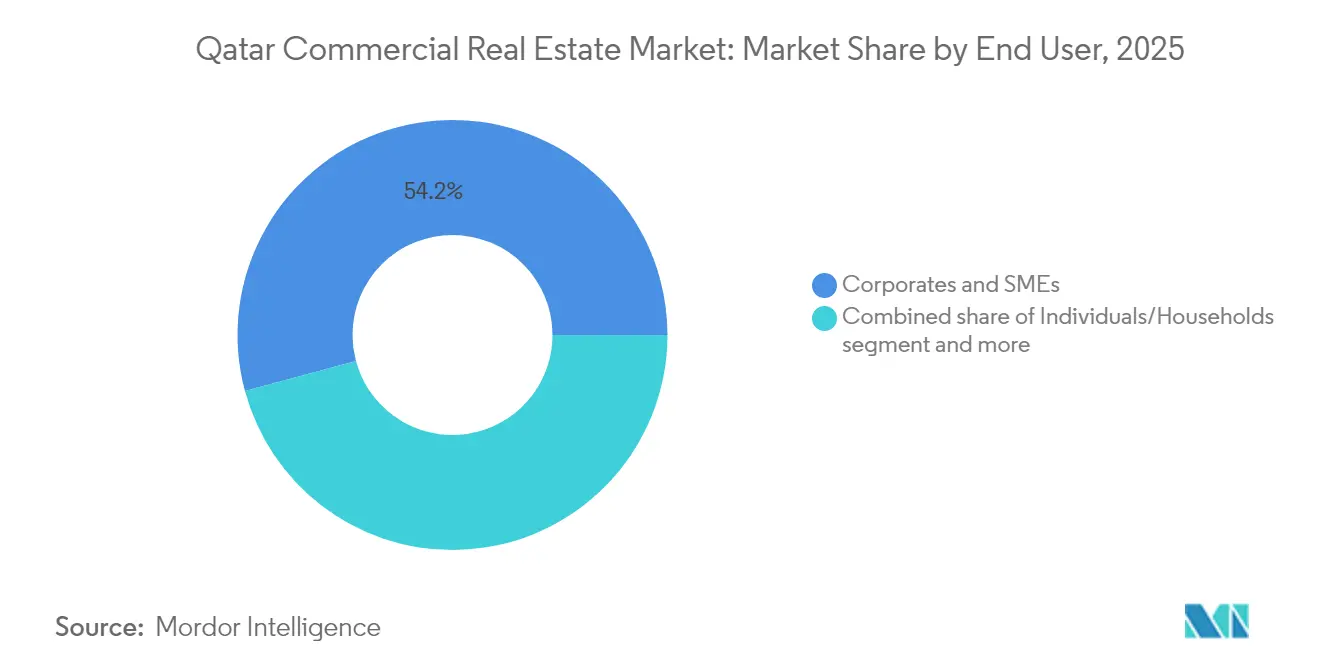

- By end-user, Corporates & SMEs commanded 54.20% share of the Qatar commercial real estate market size in 2025, while Institutional Investors exhibit the quickest 5.98% CAGR toward 2031.

- By city, Doha accounted for 70.35% of the Qatar commercial real estate market size in 2025; Al Wakrah is advancing at the highest 6.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic diversification under Qatar National Vision 2030 | +1.2% | National, with focus on Lusail and industrial zones | Long term (≥ 4 years) |

| Free-zone & 100% foreign-ownership reforms | +1.0% | QFC, QSTP, QFZ areas with spillover effects | Medium term (2-4 years) |

| E-commerce last-mile logistics boom | +0.9% | Greater Doha area and port-adjacent zones | Medium term (2-4 years) |

| FIFA-legacy infrastructure demand surge | +0.8% | National, concentrated in Doha and Al Wakrah | Short term (≤ 2 years) |

| QIA green-building investment mandate | +0.7% | National, prioritizing new developments | Long term (≥ 4 years) |

| Lusail data-centre corridor incentives | +0.6% | Lusail City and surrounding areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FIFA-legacy infrastructure demand surge

Redevelopment of tournament-era venues into hotels, retail clusters, and mixed-use districts is generating fresh leasing activity around stadium precincts, countering the rental-rate dip that followed the 2022 event. Public Works Authority has earmarked USD 22.2 billion for 2025-2029 urban upgrades that leverage these sites, assuring short-term absorption of vacant stock and catalysing related commercial build-outs.

Economic diversification under Qatar National Vision 2030

The strategy pivots GDP away from hydrocarbons by nurturing manufacturing, logistics, and tech services, all of which demand tailored real estate such as research labs, small-batch factories, and co-working floors. Manufacturing added USD 18 billion to GDP in 2024, while the logistics sector is expanding 7.1% annually, underpinning a long-run lift in warehouse and light-industrial absorption[2]Lim Meng Hui, “Qatar Free Zones Authority Launches 1,500-Plot Logistics Park near Hamad Port,” Qatar Free Zones Authority, qfz.gov.qa.

Free-zone & 100% foreign-ownership reforms

The Foreign Investment Law No. 1 of 2019 removed equity caps and enabled land allocation inside QFZ and QFC, propelling Grade-A office take-up above 2,400 registered firms by early 2025. Accompanying tax exemptions reduce total occupancy costs, nudging multinationals toward long leases and boosting pre-commitments for upcoming towers in Lusail and Energy City.

E-commerce last-mile logistics boom

Online retail volume keeps climbing, prompting government release of a 6.3 km² industrial park near Hamad Port with 1,500 serviced plots tailored for automated cross-docks, dark stores, and cold-chain nodes. Small-ticket investors control two-thirds of the plots, widening developer diversity and pushing competitive innovation in facility design and robotics integration.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Office & hospitality oversupply post-World Cup | −1.1% | Doha central business district and hospitality zones | Short term (≤ 2 years) |

| ESG-driven construction cost inflation | −0.8% | National, affecting all new developments | Medium term (2-4 years) |

| Higher lending rates & tighter credit | −0.6% | National, concentrated in high-leverage segments | Short term (≤ 2 years) |

| Slow REIT-law implementation | −0.4% | National, affecting institutional investment flows | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Office & hospitality oversupply post-World-Cup

Roughly 40% expansion in prime office stock during World-Cup preparations outpaced immediate demand, driving a 20% rent fall between 2021-2024 and elevating non-performing loan risk for banks with large real-estate books. Developers are mitigating vacancies by converting single-use towers into flexible workspaces and incorporating experiential retail on lower floors, while hoteliers re-brand surplus rooms into mid-scale extended-stay formats.

ESG-driven construction cost inflation

Green-building mandates under Qatar Sustainable Assessment System add double-digit cost premiums to LEED or GSAS-rated projects, raising feasibility hurdles for price-sensitive schemes. Volatile material prices—47.3% dictated by regulatory factors—compound uncertainty; nonetheless, long-term tenants and institutional capital prefer certified assets, helping developers recoup initial outlays through premium rents and lower utility bills[3]Francis Oppong, “Factors Driving Construction Material Price Volatility in Qatar’s Construction Industry,” Buildings (MDPI), mdpi.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Logistics Infrastructure Drives Growth

Offices retained the largest 37.35% Qatar commercial real estate market share in 2025 thanks to Doha’s CBD pipeline and Lusail tower completions. Yet vacancy pressure and hybrid-work adoption temper growth, steering landlords toward modular floorplates and tech-enabled amenities that improve space efficiency. The Qatar commercial real estate market size attributable to Offices will edge up only modestly through 2031 as occupiers seek lease flexibility and ESG-certified space.

Logistics facilities deliver the fastest 6.01% CAGR to 2031, supported by e-commerce adoption, North Field LNG expansion, and government-backed industrial parks near Hamad Port. Automated racking, temperature-controlled zones, and solar-ready roofs now feature in most tenders, while AI-driven construction showcased at ConteQ Expo24 shortens delivery cycles and cuts long-run energy costs.

By Business Model: Rental Growth Accelerates

Sales transactions commanded a 63.25% slice of the Qatar commercial real estate market in 2025 as foreign freehold demand surged in Lusail and The Pearl. High-net-worth buyers view freehold offices and retail podiums as inflation hedges, and residency schemes tied to USD 1 million purchases reinforce appetite. Still, tighter global financing conditions and a preference for capital-light balance sheets curb outright acquisitions by corporates.

Rentals are on a 6.15% CAGR trajectory to 2031, reflecting occupiers’ turn toward OPEX-friendly models that preserve working capital. Updated Rent Law No. 4 of 2008 and functioning Leasing Dispute Committees raise contractual certainty, while landlords entice tenants with turnkey fit-outs, shorter rent-free periods, and green-lease clauses that share utility-efficiency gains.

By End-user: Institutional Investment Momentum

Corporates & SMEs held a 54.20% share of the Qatar commercial real estate market size in 2025, driven by manufacturing diversification, startup formation in Qatar Science & Technology Park, and reshoring of supply chains into purpose-built warehouses. Occupiers favour clusters offering research labs, light assembly floors, and on-site customs clearance.

Institutional Investors represent the quickest 5.98% CAGR bracket, buoyed by Qatar Investment Authority’s USD 1 billion Fund-of-Funds that lured B Capital and Deerfield into Doha in 2025. Sovereign funds, asset managers, and insurance firms demand core-plus offices with data-rich building-management systems and proximity to financial regulators. Long-income profiles and green-bond financing unlock competitive borrowing costs, making trophy assets in Lusail and West Bay their favoured targets.

Geography Analysis

Doha preserved 70.35% of the Qatar commercial real estate market size in 2025 on the back of Hamad International Airport’s 70 million-passenger capacity, entrenched government institutions, and the 1.1 million m² Lusail Towers block that houses Qatar National Bank and the central bank. While the capital still garners the lion’s share of multinational demand, supply overhang in Grade-A offices and hotels keeps headline rents flat in the near term. Adaptive-reuse programs that transform surplus hospitality suites into serviced apartments and senior-living units help moderate vacancy pressures.

Al Wakrah is the fastest riser with a 6.26% CAGR through 2031, catalysed by a 6.3 km² logistics park beside Hamad Port and Mesaieed Industrial City. Public Works Authority budgets USD 22.2 billion for roads, utilities, and drainage that elevate the city’s competitiveness, while small-parcel land sales encourage local entrepreneurs to roll out specialised warehousing and cold-chain modules. Improved coastal highways shorten drayage times to the port, enabling 24-hour fulfilment cycles for e-commerce players.

Al Rayyan and the Rest of Qatar offer steady but smaller bases for future growth. Al Rayyan benefits from spill-over tenant demand as Doha’s core tightens, spurring mixed-use precincts that merge coworking, mid-scale retail, and residential towers. Outlying industrial zones host fabrication yards and service bases for the North Field LNG project, with built-to-suit plots attracting engineering, procurement, and construction contractors. Growth across these districts supports a balanced geographic spread for the Qatar commercial real estate market, reducing over-reliance on the capital.

Competitive Landscape

A moderate concentration characterises the Qatar commercial real estate market, with leading developers—Barwa Real Estate, Ezdan Holding, United Development Company, and Qatari Diar—leveraging joint ventures and PPP awards to secure land and financing for headline schemes. The government aims to award USD 85 billion in PPP projects by 2030, prompting consortium bids that marry local knowledge with international design-build expertise.

Technology and sustainability have become the prime battlegrounds. ConteQ Expo24 demonstrated AI-assisted quantity-surveying and drone-based progress tracking, tools now embedded by Alfardan Properties and Msheireb Properties to compress build times and lift margins. Green-building compliance is no longer optional: developers courting sovereign wealth capital must achieve GSAS 4-star or LEED Gold as the minimum entry ticket, spurring alliances with global EPC firms skilled in net-zero design.

Specialist niches provide white-space opportunities. Global providers such as GLP and Goodman are studying entry strategies for temperature-controlled logistics, while Equinix and Digital Realty scout plots in Lusail’s data-centre corridor to capitalise on government incentives for cloud infrastructure. Local challengers—First Qatar Real Estate and Mazaya—target mid-market rental housing and community malls that recycle stranded land parcels.

Qatar Commercial Real Estate Industry Leaders

Barwa Real Estate Company

Ezdan Holding Group

United Development Company

Mazaya Real Estate Development

Qatari Diar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Public Works Authority launched a USD 22.2 billion infrastructure plan for 2025-2029 covering roads, drainage, and 5,500 residential plots through PPPs.

- February 2025: Qatar Investment Authority marked one year of its USD 1 billion Fund-of-Funds; six global investment managers opened regional headquarters in Doha.

- January 2025: Third National Development Strategy commenced, placing private enterprise at the center of economic expansion and elevating demand for R&D hubs and flexible offices.

- September 2025: ConteQ Expo24 highlighted AI-driven construction solutions developed with the Public Works Authority and Ministry of Communications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Qatari commercial real estate (CRE) market as the aggregate capital value of income-producing and owner-occupied offices, retail centers, hotels, industrial and logistics facilities, and mixed-use stock that is completed, trading, or under active development within the nation's municipal borders.

Gross land sales without vertical construction, purely residential assets, and agricultural holdings sit outside this scope.

Segmentation Overview

- By Property Type

- Offices

- Retail

- Logistics

- Others (Industrial, Hospitality, etc.)

- By Business Model

- Sales

- Rental

- By End-user

- Individuals / Households

- Corporates & SMEs

- Others

- By Cities

- Doha

- Al Wakrah

- Al Rayyan

- Rest of Qatar

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed developers, facility managers, REIT analysts, regional valuers, and brokerage directors in Doha, Lusail, Al Rayyan, and Al Wakrah.

These conversations validated vacancy trends, effective rents, pipeline slippage, and typical development costs, and they allowed us to ground secondary figures in on-the-ground sentiment before triangulating the final model.

Desk Research

We began with public datasets from sources such as Qatar Planning and Statistics Authority, Qatar Central Bank price indices, UN-Comtrade trade-linked cement and steel flows, and free-zone tender bulletins, which outline construction pipelines and foreign-ownership shifts.

Company filings, stock-exchange disclosures, and press releases provided project-level capex and lease rate signals, while news archives on Dow Jones Factiva and project trackers on D&B Hoovers supplied supplemental deal values.

Industry bodies, Qatar Financial Centre, Gulf Organization for Industrial Consulting, and World Tourism Organization, helped calibrate demand drivers for office, logistics, and hospitality space.

The list is indicative; many additional public and subscription sources were tapped for cross-checks and clarifications.

Market-Sizing and Forecasting

A top-down build derived the 2025 baseline. Stock-level gross leasable area by property type was multiplied by average replacement cost and adjusted for depreciation, then reconciled with recorded transaction values and mortgage data.

Bottom-up checks, sampled developer financials, select channel lease roll-ups, and airport hotel ADR times keys estimates flagged outliers that were corrected before lock-in.

Key variables feeding the forecast include GDP non-oil growth, free-zone foreign-company registrations, construction material imports, prime office vacancy, and logistics warehouse absorption.

A multivariate regression, stress-tested through ARIMA overlays, shaped 2026 to 2030 trajectories, while scenario analysis captured policy or event shocks.

Gaps in granular bottom-up data were bridged using mean regional cost multipliers corroborated by expert opinion.

Data Validation and Update Cycle

Outputs pass variance thresholds against benchmark indicators, after which a senior reviewer signs off.

Reports refresh annually; material events such as new free-hold legislation trigger interim updates, and an analyst re-checks key numbers just before delivery.

Why Our Qatar Commercial Real Estate Baseline Commands Reliability

Published estimates often diverge because firms size different asset pools, apply varied valuation bases, or freeze exchange rates at dissimilar points.

Key gap drivers include whether pipeline projects are counted, if owner-occupied premises are valued, the treatment of land banks, and refresh cadence. Mordor Intelligence applies a full-stock lens, current-year QAR to USD rates, and yearly updates, which together yield a defensible, decision-ready baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 33.10 B (2025) | Mordor Intelligence | |

| USD 4.14 B (2024) | Regional Consultancy A | Counts only rental income assets; omits owner-occupied and under-construction stock |

| USD 2.75 B (2024) | Global Consultancy A | Reports annual deal turnover, not capital value; limits scope to Doha office and retail only |

In short, because we harmonize scope, live exchange rates, and dual-track validation, Mordor's numbers present the most balanced and transparent view for strategists comparing investment options across Qatar's fast-evolving CRE landscape.

Key Questions Answered in the Report

What is the current size of the Qatar commercial real estate market?

The Qatar commercial real estate market is valued at USD 35.06 billion in 2026 and is projected to reach USD 46.74 billion by 2031.

Which property type is expanding the fastest?

Logistics facilities lead growth, advancing at a 6.01% CAGR on the back of e-commerce gains and the new 6.3 km² industrial park near Hamad Port.

How large is Doha’s share of the market?

Doha accounts for 70.35% of the Qatar commercial real estate market size in 2025, supported by Lusail’s CBD towers and Hamad International Airport’s expansion.

Why are rental models growing more quickly than sales?

Rentals are forecast to rise at a 6.15% CAGR because corporates prefer capital-light, flexible leasing structures and benefit from stronger tenant protections under Rent Law No. 4 of 2008.

What risk does oversupply pose to the market?

Post-World-Cup office and hospitality oversupply is expected to trim overall market CAGR by 1.1% in the short term, but adaptive-reuse projects and economic diversification efforts are absorbing excess stock.

How are sustainability rules affecting development costs?

Mandatory GSAS and LEED compliance adds cost premiums, yet certified assets command higher rents and attract institutional capital focused on ESG goals.

Page last updated on: