Commercial Aircraft Collision Avoidance System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

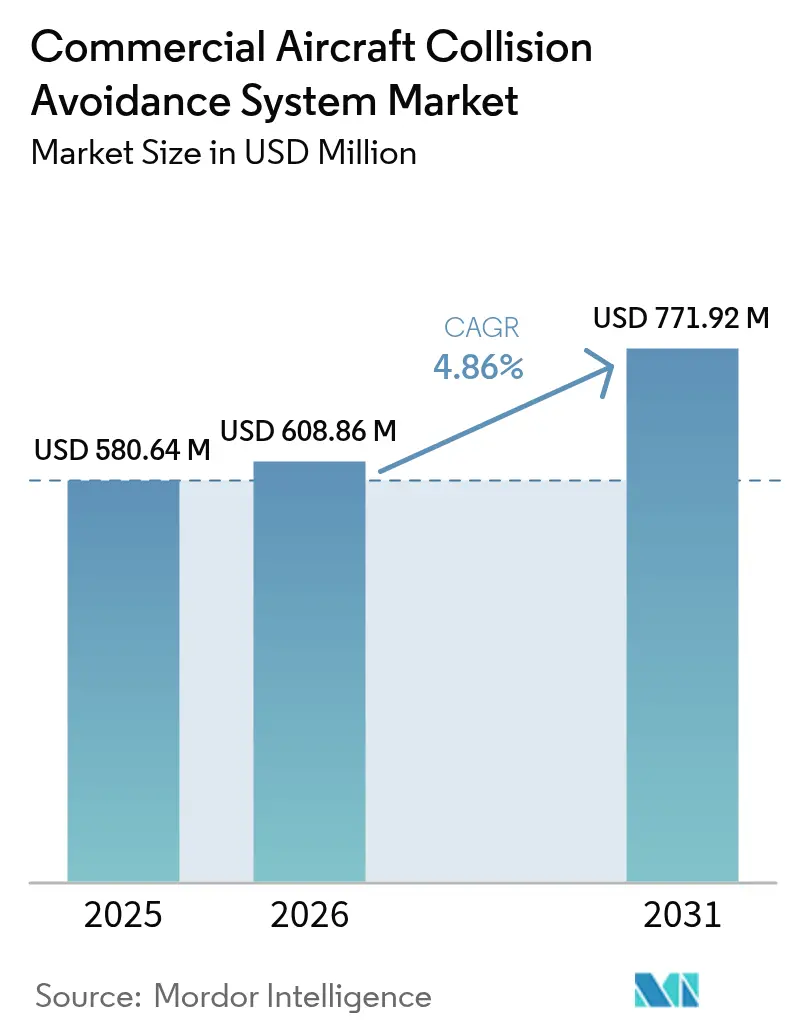

| Market Size (2026) | USD 608.86 Million |

| Market Size (2031) | USD 771.92 Million |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

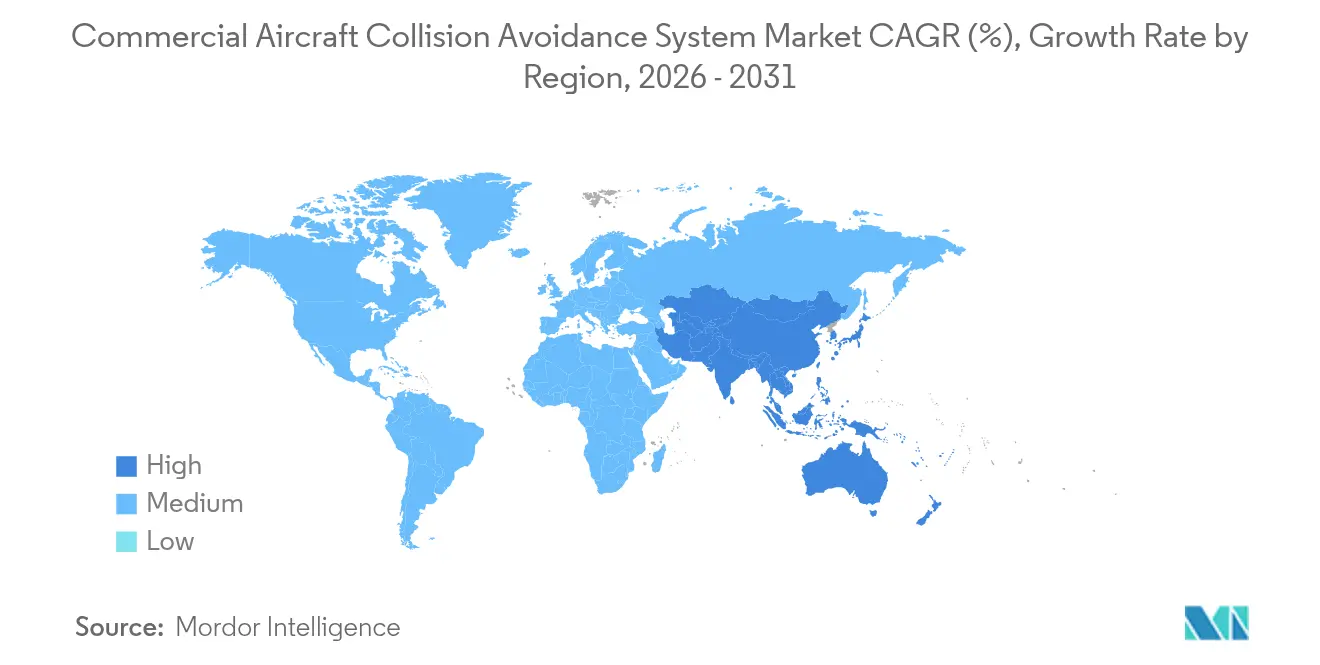

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Collision Avoidance System Market Analysis by Mordor Intelligence

The commercial aircraft collision avoidance systems market size in 2026 is estimated at USD 608.86 million, growing from 2025 value of USD 580.64 million with 2031 projections showing USD 771.92 million, growing at 4.86% CAGR over 2026-2031. Strong retrofit mandates in mature regions, rapid fleet additions in emerging economies, and the shift toward AI-enabled ACAS Xa platforms underpin an extended growth runway for the commercial aircraft collision avoidance systems market. Airspace-modernization programs (NextGen in the US, SESAR in Europe) accelerate integration of surveillance-rich collision avoidance solutions, while sustained R&D in drone integration broadens long-term addressable demand. OEMs focus on vertically integrated avionics suites that combine TCAS, synthetic vision, and ADS-B In to minimize pilot workload, whereas aftermarket specialists position modular upgrades that limit aircraft downtime. Semiconductor supply disruptions and 5G C-band interference risks temper near-term delivery schedules, yet proactive certification guidance from regulators supports continuous program funding and mitigates demand deferrals.

Key Report Takeaways

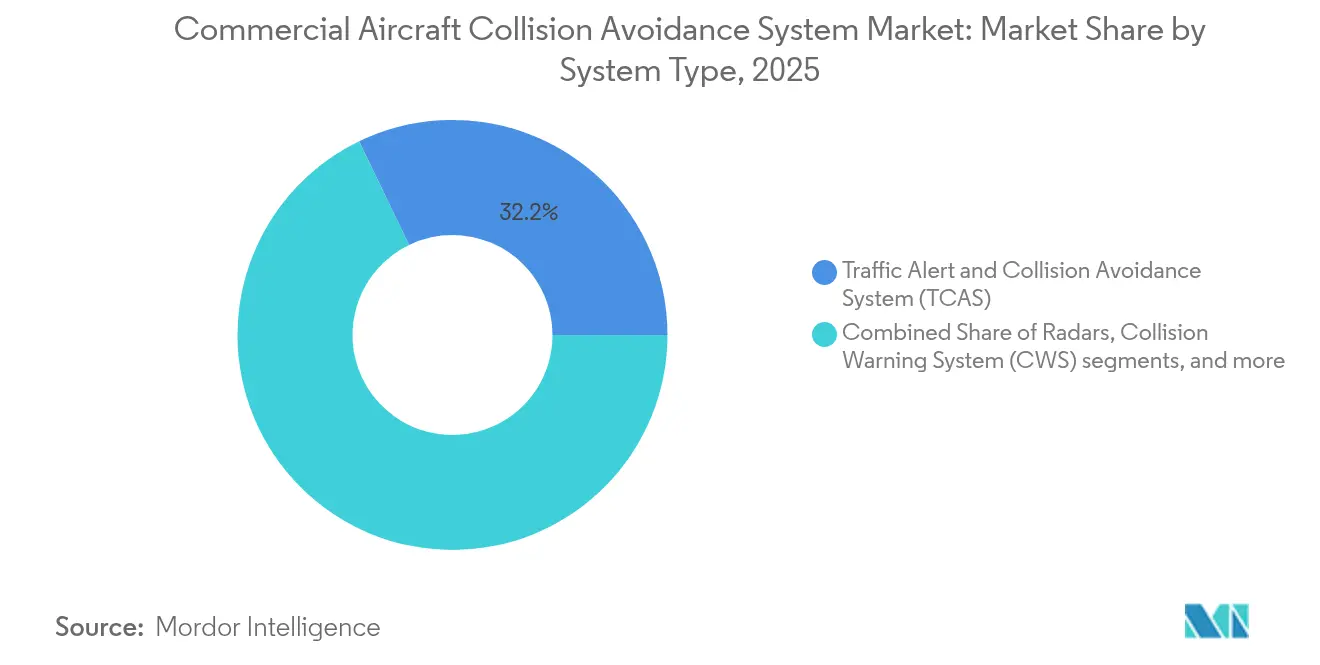

- By system type, TCAS led with 32.15% of the commercial aircraft collision avoidance systems market share in 2025 and is projected to record a 5.46% CAGR through 2031.

- By platform, commercial aviation accounted for an 80.55% share of the commercial aircraft collision avoidance systems market in 2025, while drones are on course for a 6.04% CAGR between 2026 and 2031.

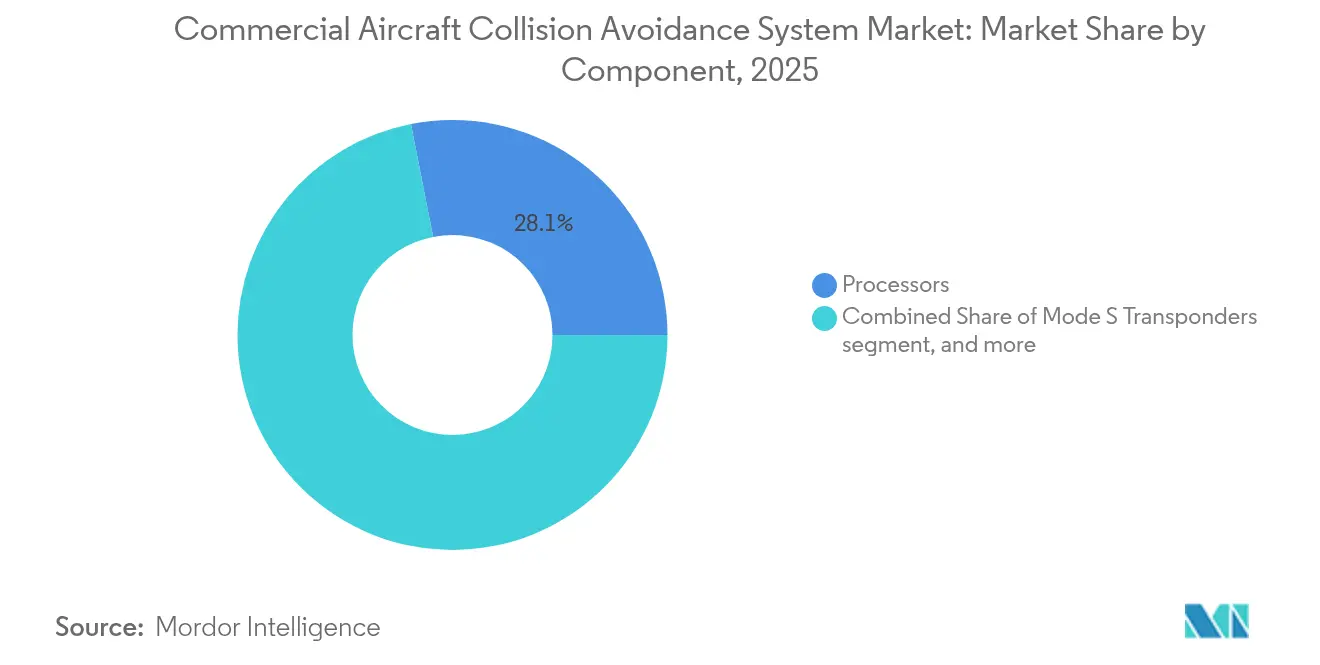

- By component, processors represented 28.10% revenue share in 2025; antennas and sensors are advancing at a 5.32% CAGR to 2031.

- By end user, OEM channels captured 58.10% revenue in 2025, whereas aftermarket services are expanding at a 5.71% CAGR due to aging fleet retrofits.

- By geography, North America retained 38.20% regional share in 2025; Asia-Pacific is forecasted to deliver the fastest 5.68% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Aircraft Collision Avoidance System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandates by ICAO and FAA for TCAS II and ACAS X retrofits | +1.2% | North America and Europe | Medium term (2-4 years) |

| Growth in narrowbody aircraft deliveries driven by low-cost carrier (LCC) expansion | +0.9% | Asia-Pacific, MEA, South America | Long term (≥ 4 years) |

| Advancements in global airspace modernization programs such as NextGen and SESAR | +0.8% | North America and Europe | Long term (≥ 4 years) |

| Deployment of AI-enabled ACAS Xa systems to reduce nuisance alerts | +0.7% | North America and Europe | Medium term (2-4 years) |

| Rising pressure on airlines to improve passenger safety ratings | +0.6% | Global, with emphasis in mature aviation markets | Short term (≤ 2 years) |

| Increasing R&D in collision avoidance systems for drone traffic integration | +0.5% | Global, with concentration in UTM-advanced regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory mandates for TCAS II and ACAS X retrofits

ICAO and FAA upgrade cycles compel airlines to replace legacy TCAS software and hardware well ahead of standard maintenance windows. Trans-Atlantic route operators must accommodate version 6.04a and 7.1 compliance, prompting dual-certified solutions and stimulating demand for hybrid surveillance capability. Network-effect benefits arise because higher fleet-wide equipage densities improve resolution-advisory coordination, amplifying safety and efficiency gains. OEMs leverage the mandate to cross-sell Mode S transponders and ADS-B-In processors as bundled packages, strengthening margins while simplifying customer certification paperwork. The resulting order visibility supports multi-year production planning and insulated earnings streams for avionics suppliers.[1] “AC 20-151B – Airworthiness Approval of Traffic Alert and Collision Avoidance Systems,” Federal Aviation Administration, faa.gov

Rapid growth in narrowbody aircraft deliveries

LCCs in Asia-Pacific fuel a sustained procurement wave focused on A320neo and B737 MAX families, each line-fit with TCAS II as standard. Narrowbody airframes deliver favorable economics for route-dense domestic networks yet expose operators to congested terminal airspace where collision-avoidance integrity is paramount. Because many airlines finance new aircraft via sale-leaseback structures, lessors insist on up-to-date surveillance avionics to protect asset liquidity, reinforcing system-equippage rates across fleets. The narrowbody boom also spurs copycat regulatory action in the Middle East, Africa, and South America, where authorities harmonize guidance with ICAO Annex 10 to facilitate inter-regional connectivity. As a result, the commercial aircraft collision avoidance systems market enjoys a steady installation cadence tied directly to OEM production slots.[2]“TCAS Status Meeting Brief,” International Civil Aviation Organization, icao.int

Airspace-modernization programs (NextGen and SESAR)

Performance-based navigation routes shorten track distance but tighten lateral and vertical separation, elevating reliance on automated conflict-detection logic. SESAR conflict-resolution tools feed trajectory predictions to TCAS processors, cutting interrogation volumes on the 1090 MHz channel and reducing false advisories. NextGen’s data communications tower-to-cockpit links provide real-time intent updates that refine ACAS threat-evaluation accuracy. Joint industry working groups develop standard surveillance message protocols that minimize integration hurdles across avionics brands, reducing retrofit complexity for mixed-type fleets. These initiatives elevate system value beyond baseline safety, positioning collision-avoidance technology as a central enabler of capacity expansion in constrained metropolitan airports.

AI-enabled ACAS Xa deployment

Machine learning (ML) algorithms embedded in ACAS Xa review closure rates, encounter geometry, and velocity vectors to eliminate superfluous resolution advisories that erode pilot confidence. Field trials reveal a 55% reduction in nuisance alerts relative to TCAS II, allowing flight crews to maintain altitude profiles and avoid ATC disruptions. Airlines report measurable fuel burn savings because fewer altitude excursions translate into smoother climb and descent planning. Certification authorities have published guidance that grandfather-approves ACAS Xa processor cards in existing avionics bays, lowering hardware-replacement costs for operators. These performance and cost advantages materially expand the commercial aircraft collision avoidance systems market addressable pool into cost-constrained regional and cargo operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation and lifecycle costs for regional and low-margin carriers | -0.8% | Global, with acute impact in emerging economies | Short term (≤ 2 years) |

| Semiconductor supply chain disruptions affecting avionics systems | -0.6% | Global, with concentration in Asia-Pacific manufacturing | Medium term (2-4 years) |

| Risk of 5G C-band interference with radar altimeter frequencies | -0.4% | North America and regions with 5G C-band deployment | Short term (≤ 2 years) |

| Regulatory delays in system rollout across emerging economies | -0.5% | Emerging economies in APAC, MEA, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High installation and lifecycle costs

Complete TCAS or ACAS X retrofit kits—processors, antennas, wiring, and cockpit displays—carry equipment pricing near USD 150,000; installation labor, flight-test certification, and downtime increase total ownership toward USD 200,000 over 10 years. Thin-margin regional airlines in South America and sub-Saharan Africa often defer such upgrades until just before regulatory deadlines, elongating supplier sales cycles. Financing packages offered by OEMs and lessors alleviate cash-flow strain yet add interest costs that erode projected fuel-efficiency paybacks. Cost-sensitive operators therefore gravitate to modular designs that enable phased functionality roll-outs aligned to scheduled heavy checks, but this staged adoption slows immediate revenue recognition for vendors. The economic hurdle restricts near-term penetration in low-yield markets, trimming upside for the commercial aircraft collision avoidance systems market.[3]“Perspectives on the Aviation Aftermarket,” Solomon Partners, solomonpartners.com

Semiconductor supply-chain disruptions

Aviation-grade microprocessors rely on niche fabrication nodes with extended qualification timelines compared with consumer electronics. Pandemic-era foundry reallocations toward automotive and data-center customers created allocation shortfalls that reverberate across avionics lead-times. Processor scarcity forces integrators to dual-source from secondary fabs, triggering fresh RTCA DO-254 hardware-validation programs that push certifications by 6-12 months. Airlines awaiting spares must park aircraft or operate under minimum-equipment-list exemptions, degrading dispatch reliability and delaying retrofit schedules. Although tier-one suppliers build buffer inventories, extended component backlogs remain risky through at least 2027, restraining shipment growth for the commercial aircraft collision avoidance systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: TCAS Dominance Drives Market Evolution

TCAS held 32.15% of the commercial aircraft collision avoidance systems market share in 2025 and is forecasted to post a 5.46% CAGR through 2031. Adoption momentum stems from mandatory upgrades to version 7.1 software, which integrates ADS-B In surveillance and minimizes 1090 MHz interrogation congestion. TAWS continues to protect turbine fleets operating near mountainous terrain, while synthetic-vision overlays simplify pilot situational awareness on modern glass cockpits. Radar-based surveillance remains critical in secondary airspaces lacking uniform ADS-B coverage, ensuring system redundancy under degraded-signal conditions. OCAS and rotorcraft-specific collision warning products address low-altitude flight envelopes, opening cross-selling channels in commercial-helicopter and emergency-medical-service niches.

Market participants bundle TCAS logic with integrated surveillance suites that share processors and displays, lowering ship-set weight and reducing total power draw. This convergence shrinks cockpit footprint and frees panel space for connectivity upgrades. As AI analytics propagate from ACAS Xa research programs into mainstream TCAS products, legacy fleets benefit from software-only enhancements that meet upcoming performance standards without hardware swaps. Consequently, TCAS remains the anchor product line around which suppliers craft incremental value propositions, underpinning long-run revenue visibility in the commercial aircraft collision avoidance systems market.

By Platform: Commercial Aviation Leads While Drones Accelerate

Commercial aviation platforms commanded 80.55% revenue share in 2025, supported by standardized linefit installations on single-aisle production lines and robust aftermarket service agreements that include data-link subscriptions and periodic software updates. Widebody retrofits involve more complex integration owing to dual-aisle wiring runs and extended certification documentation, yielding higher per-aircraft revenue but longer installation cycles. General aviation operators adopt scaled-down processor boards and integrated traffic displays to upgrade safety without incurring airline-grade costs, bolstering stable replacement demand in the business jet fleet.

Drones are set to register a 6.04% CAGR, fueled by BVLOS regulatory frameworks and urban air mobility (UAM) prototypes that demand detect-and-avoid parity with manned aircraft. Miniaturized processors and lightweight phased-array antennas underpin this expansion, although certification pathways remain nascent and prolong revenue conversion. Cross-industry collaborations between avionics incumbents and robotics start-ups accelerate product maturation, potentially unlocking a sizable incremental addressable opportunity for the commercial aircraft collision avoidance systems market beyond 2030.

By Component: Processors Enable Advanced Functionality

Processors accounted for 28.10% in 2025, reflecting their status as the computational backbone of advanced threat-evaluation algorithms and sensor-fusion routines. Transitioning to AI-ready system-on-chip designs raises bill-of-materials cost yet delivers step-change performance that enables multi-threat tracking and reduced false-alert rates. Mode S transponders, critical for coordinated maneuver logic, retain consistent retrofit demand given their 10-year replacement cycles. Antennas and sensors, experiencing a 5.32% CAGR, benefit from migrating to active electronically scanned arrays capable of dynamic beam shaping that enhances range accuracy without size penalties.

Display and warning units evolve toward high-resolution synthetic-vision overlays and intuitive aural-alert schemes that cut pilot workload. Suppliers leverage shared graphical libraries across avionics functions to deliver cohesive human-machine interfaces. Collectively, component innovation sustains a technology-refresh pipeline that keeps fleet operators engaged in staged upgrade programs, adding recurring revenue streams to the commercial aircraft collision avoidance systems market.

By End User: Aftermarket Growth Reflects Fleet Aging

OEM channels secured 58.10% market revenue in 2025 through contractual inclusion of collision-avoidance hardware at the final assembly line and leveraging type-certificate efficiencies. Structured service-level agreements guarantee software updates and field service engineer support, reinforcing long-term customer loyalty. Importantly, many OEMs now embed data analytics subscriptions into purchase contracts, creating sticky annual revenue.

Aftermarket services are expanding at a 5.71% CAGR because roughly 35% of the in-service commercial fleet is over 15 years old, triggering mandatory obsolescence and compatibility upgrades. Independent maintenance, repair, and overhaul (MRO) centers differentiate themselves by reducing downtime by pre-fabricating wiring harnesses and employing augmented reality (AR) maintenance aids. Digital twin applications predict component failures before flight-critical events, allowing airlines to pool spares across sister fleets and minimize inventory costs. This service-centric model enhances the resilience of the commercial aircraft collision avoidance systems market against new aircraft delivery volatility.

Geography Analysis

North America maintained a 38.20% share of the commercial aircraft collision avoidance systems market in 2025, supported by FAA retrofit mandates and the embedded culture of technology refresh in US mainline carriers. The region benefits from mature MRO infrastructure and original equipment proximity that compress certification lead times and facilitate early adoption of ACAS Xa flight-test programs. Canadian authorities align with US standards, providing a unified cross-border regulatory environment that streamlines fleet-wide upgrade decisions.

Asia-Pacific is projected to post a 5.68% CAGR through 2031, propelled by double-digit traffic growth in India and Southeast Asia and a sustained backlog of narrowbody deliveries. Regulatory harmonization under ICAO Annex 10 fosters accelerated equipage among LCCs eager to secure international traffic rights. Domestic e-commerce demand also catalyzes drone detect-and-avoid investments, augmenting traditional manned-aircraft volume. However, divergent 5G rollout schedules create altitude-meter interoperability challenges that operators must navigate via regional technical directives before completing collision-avoidance upgrades.

Europe holds a solid installed base thanks to early SESAR conflict-management trials. Ongoing integration of ADS-B In data into TCAS logic promises further performance gains, incentivizing carriers to invest ahead of mandated deadlines. Conversely, South America, the Middle East, and Africa still contend with limited ADS-B ground infrastructure, making radar-backed TCAS solutions more attractive in the interim. The resulting patchwork of surveillance capabilities shapes supplier go-to-market strategies, reinforcing localized partnership models in the commercial aircraft collision avoidance systems market.

Regulatory Landscape

Collision-avoidance equipage for commercial aircraft is anchored in ICAO Standards and Recommended Practices under Annex 10, Volume IV. Amendment 91 (effective 2022) introduced the ACAS X family (including ACAS Xa/Xo) as an internationally recognized framework alongside legacy ACAS II/TCAS II provisions. In the United States, the FAA maintains approval pathways through its TCAS/ACAS design-approval guidance and Technical Standard Order TSO-C219 for ACAS Xa/Xo; an updated TSO-C219a has been in review to align with evolving standards and interoperability needs.

In Europe, collision-avoidance compliance connects to EU implementing rules for airborne ACAS equipage. Commission Implementing Regulation (EU) 2025/343 (adopted February 2025) provides explicit European airspace acceptance for ACAS Xa/Xo in addition to TCAS II version 7.1. EUROCONTROL safety materials and operational guidance for ACAS use further reinforce standardized pilot response and operational best practice, supporting multi-state consistency for operators flying across European airspace.

Value Chain Analysis

The value chain starts with aviation-grade electronics and RF components (processors, memory, power management, and 1090 MHz transponder/receiver front ends) feeding LRU manufacturers. These suppliers integrate collision-avoidance computers, Mode S transponders, antennas, and cockpit alerting/display interfaces. Tier-1 avionics suppliers such as Honeywell, Collins Aerospace (RTX), and ACSS (Acron Aviation and Thales joint venture) package TCAS/ACAS functions into surveillance suites, which can share processing and HMI elements with adjacent capabilities (for example, transponder and terrain awareness) to help airlines manage weight, wiring, and provisioning costs.

Certification and interoperability shape product roadmaps across the chain. RTCA SC-147 and EUROCAE working groups maintain performance standards and guidance for multi-vendor coordination, while regulators (FAA, EASA, and national authorities aligned to ICAO Annex 10) validate compliance through TSOs/ETSOs and aircraft-level approvals. Market delivery occurs through OEM line-fit programs at aircraft manufacturers and through the aftermarket via MRO and avionics integrators that execute installations, flight testing, and documentation. This aftermarket route is sensitive to avionics lead times when aviation-grade semiconductor availability tightens. The emergence of UAS-specific ACAS X variants adds a parallel development lane, with FAA actions such as TSOs enabling certification of ACAS Xu equipment and extending the standards-to-products-to-operators loop beyond traditional airline fleets.

Competitive Landscape

The commercial aircraft collision avoidance systems market shows moderate consolidation: the top five players account for major combined revenue, reflecting significant but not dominant concentration. Honeywell International Inc., Thales Group, Garmin Ltd., L3Harris Technologies, Inc., and Collins Aerospace (RTX Corporation) execute vertical integration—designing processors, antennas, and displays in-house—to safeguard margin and reduce certification dependencies. Long-standing relationships with Boeing and Airbus secure line-fit positions that funnel consistent revenue, while military heritage underpins rigorous reliability credentials valued by civil regulators.

Strategic alliances proliferate as incumbents pursue open-system architectures that are compliant with Modular Open Systems Approach mandates. For example, Collins Aerospace adopts a common avionics platform across business-jet and rotorcraft programs, transferring R&D amortization benefits across unit volumes. Meanwhile, L3Harris’ divestiture of its commercial avionics unit (now Acron Aviation) underscores portfolio rationalization trends that enable focus on growth adjacencies such as drone detect-and-avoid sensors.

Competitive intensity sharpens in the drone segment, where agile software firms introduce cloud-based conflict-resolution engines that bypass traditional hardware-centric models. To counter, legacy suppliers embed ML stacks directly onto existing TCAS line-replaceable units, offering an upgrade path without wholesale hardware replacement. Price-sensitive regional carriers thus gain access to advanced functionality at marginal cost, complicating new-entrant disruption prospects but stimulating innovation momentum across the commercial aircraft collision avoidance systems market.

Commercial Aircraft Collision Avoidance System Industry Leaders

Honeywell International Inc.

Thales Group

L3Harris Technologies, Inc.

Garmin Ltd.

Collins Aerospace (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One major opportunity is the ACAS X transition on commercial fleets as regulators and standards bodies formalize acceptance criteria beyond TCAS II version 7.1. Concrete signals include Commission Implementing Regulation (EU) 2025/343 adopting ACAS Xa/Xo acceptance in Europe (February 2025) and EUROCAE publishing ED-256 to define MOPS for ACAS Xa and Xo variants (April 2026). Together, these developments create space for suppliers to offer upgrade paths that preserve pilot-facing RA conventions while reducing nuisance alerts and improving interoperability in surveillance-rich airspace modernization environments.

Another opportunity is retrofit packaging that combines ADS-B In with collision avoidance for out-of-production or mid-life aircraft types where full flight deck modernization is cost-prohibitive. In April 2026, an ATSG-led partnership with Innovative Aerosystems and ACSS launched a program to develop and certify ADS-B In retrofit packages for Boeing 757 and 767 operators, illustrating how integrators and avionics houses can expand demand by targeting specific legacy fleets. UAS and mixed-crew airspace integration also broadens the technology runway: FAA-reported flight test validation activity for ACAS X logic using remotely piloted aircraft as testbeds (April 2026) points to continued investment in autonomous RA computation, supporting product families that span both crewed commercial aircraft and emerging uncrewed operations.

Recent Industry Developments

- April 2026: Airborne Maintenance & Engineering Services (ATSG subsidiary), Innovative Aerosystems, and ACSS launched a program to develop and certify an ADS-B In retrofit package for Boeing 757 and 767 operators. The effort targets a large in-service fleet segment where avionics modernization is often constrained by downtime and economics, creating a structured route to add surveillance inputs that complement collision-avoidance functions.

- February 2026: Cathay Group selected Thales avionics solutions for its new Airbus A330neo and A321neo/A320neo fleets, including the ACSS-manufactured T3CAS traffic collision avoidance system. The selection reinforces line-fit momentum for integrated collision-avoidance LRUs on high-volume commercial platforms and strengthens ACSS positioning through major airline fleet wins.

- August 2024: Garmin announced that Textron Aviation certified its Runway Occupancy Awareness collision-avoidance software on the Cessna Caravan turboprop. The certification adds a deployed runway-conflict awareness capability to an in-production aircraft type, supporting broader adoption of software-led safety functions that can complement airborne collision-avoidance systems across mixed fleets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks the revenue earned from collision avoidance avionics installed on commercial aircraft, covering certified airborne systems that detect traffic and generate resolution advisories to reduce mid air collision risk (for example, TCAS and ACAS variants).

Scope exclusions: We exclude ground based air traffic control infrastructure, airport surface movement systems, and non certified prototypes that are not sold into commercial fleets.

Segmentation Overview

- By System Type

- Radars

- Traffic Alert and Collision Avoidance System (TCAS)

- Terrain Awareness and Warning System (TAWS)

- Collision Warning System (CWS)

- Obstacle Collision Avoidance System (OCAS)

- Synthetic Vision Systems

- By Platform

- Commercial Aviation

- Narrowbody

- Widebody

- Regional Jets

- General Aviation

- Business Jets

- Commercial Helicopters

- Drones

- Commercial Aviation

- By Component

- Processors

- Mode S Transponders

- Antennas and Sensors

- Display/Warning Units

- By End User

- Original Equipment Manufacturer (OEM)

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the operating and compliance context for commercial collision avoidance equipment, then converting that into measurable inputs. We refer to public aviation and safety sources such as ICAO standards and guidance material, FAA advisory and safety publications, EASA regulations and notices, and IATA traffic and fleet updates to understand equipage triggers.

To size demand signals, we also review OEM delivery and backlog disclosures, airline annual reports and investor presentations, airworthiness directives when applicable, and peer reviewed aviation safety papers on surveillance and collision risk. Public trade and customs statistics are used selectively to sanity check cross border avionics shipment direction, and patent databases are scanned to see where technology is moving (for example, ACAS X logic) without mixing concept work into commercial revenue. In some cases, a paid subscription for company financials and news is used to confirm revenue exposure and timing, and then it is cross checked against what is visible in public documents. These examples are not exhaustive, and many other sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm what portion of commercial fleets are operating TCAS II versus newer ACAS capable configurations, and how retrofit cycles differ from line fit demand. We speak with a mix of avionics engineering, certification, aftermarket support, airline technical operations, and MRO planning respondents across major regions so gaps from desk findings can be closed and assumptions can be stress tested.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 15% | APAC: 43% |

| Mid tier: 47% | Functional/Unit leaders: 29% | EMEA: 34% |

| Smaller Players: 15% | Managers: 56% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool assessment where global commercial fleet activity and aircraft delivery schedules are translated into expected installation counts for collision avoidance equipment, then filtered through mandated equipage and upgrade timing. Once the model is assembled, selective bottom-up checks are used, including sampled unit pricing ranges, retrofit kit uptake signals, and channel feedback from MRO and airline technical teams, which are then used to adjust totals when the first pass appears off.

Key inputs used in the model include commercial aircraft deliveries and retirements, retrofit versus line fit mix, replacement intervals tied to avionics refresh and heavy checks, certification and mandate timelines affecting equipage, and average selling price movement by system generation. Forecasting relies mainly on scenario analysis, where base, conservative, and higher delivery cases are mapped and then aligned to what interviewees expect for fleet growth and upgrade pacing. Where bottom-up signals are incomplete for certain geographies, we apply penetration proxies based on fleet composition and regional regulatory alignment, and then validate the output against independent maintenance activity cues.

Data Validation & Update Cycle

Outputs are checked in multiple passes so the totals stay consistent with real world aviation signals. We compare results against independent indicators like commercial fleet size shifts, aircraft delivery backlogs, and known retrofit windows, and then investigate variances that do not fit the expected equipage rhythm.

Before sign off, assumptions go through a second analyst review, and outliers trigger re contact with a small set of respondents to confirm whether a change is real or timing related. Reports refresh annually, and interim updates are made when material events occur such as mandate changes, major delivery swings, or certification driven retrofit accelerations. Right before delivery, an analyst performs a final pass so clients receive an updated view.

Mordor Intelligence's Commercial Aircraft Collision Avoidance System Market Size Compared Against Other Published Estimates

Published market sizes for collision avoidance systems can look far apart even when the topic label is similar. Differences usually come from what platforms are counted, what year is treated as the base, how upgrade pricing is handled, and how often assumptions are refreshed.

The main gap comes from including general aviation and drones in the same pool as airline fleets, where Mordor Intelligence restricts the count to certified commercial aircraft installations and upgrades that track deliveries, retrofit timing, and mandate driven equipage, instead of rolling all airborne platforms into one total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 580.64 M (2025) | |

| Trade Publisher A | USD 455.01 M (2025) | Often uses a tighter commercial definition that can undercount retrofit and upgrade value, and it may assume a flatter price path for newer ACAS capable systems. |

| Industry Portal B | USD 439.46 M (2024) | Uses an earlier base year and a different forecast window, and it can miss timing effects when heavy check cycles shift installations into later periods. |

Looking across the three figures, most of the spread is explained by platform inclusion, base year selection, and how upgrade driven ASP progression is treated. Our sizing keeps the total traceable to fleet counts, equipage triggers, and checkable assumptions that can be re run when deliveries, mandates, or retrofit timing change.

Key Questions Answered in the Report

What is the forecast value of the global commercial aircraft collision avoidance systems market by 2031?

The market is projected to reach USD 771.92 million by 2031, reflecting a 4.86% CAGR from its 2026 level.

Which system type currently leads adoption?

TCAS holds 32.15% market share and remains the fastest-growing system type through 2031.

Which region is expected to grow the fastest?

Asia-Pacific is set to deliver a 5.68% CAGR, driven by narrowbody fleet expansion and regulatory harmonization.

How are supply-chain issues affecting deployments?

Aviation-grade semiconductor shortages extend avionics lead-times by up to a year, delaying some retrofit schedules and tempering near-term growth.

Are drones a meaningful growth segment?

Yes, detect-and-avoid mandates for BVLOS operations place drones among the fastest-growing platforms, with a 6.04% CAGR expected through 2031.

What years does this Commercial Aircraft Collision Avoidance System Market cover, and what was the market size in 2025?

In 2025, the commercial aircraft collision avoidance systems market was estimated at USD 608.86 million. The report covers the Commercial Aircraft Collision Avoidance System Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the commercial aircraft collision avoidance systems market size for the 2026-2031 timeframe.

Page last updated on: