Flight Navigation System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

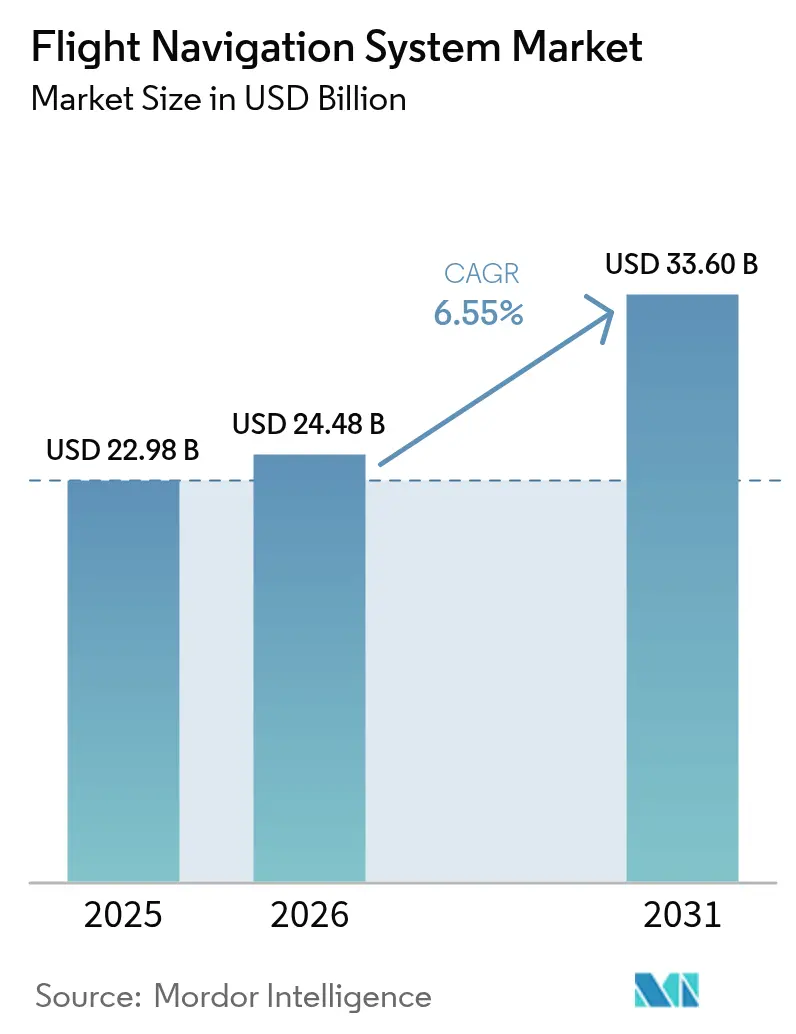

| Market Size (2026) | USD 24.48 Billion |

| Market Size (2031) | USD 33.6 Billion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

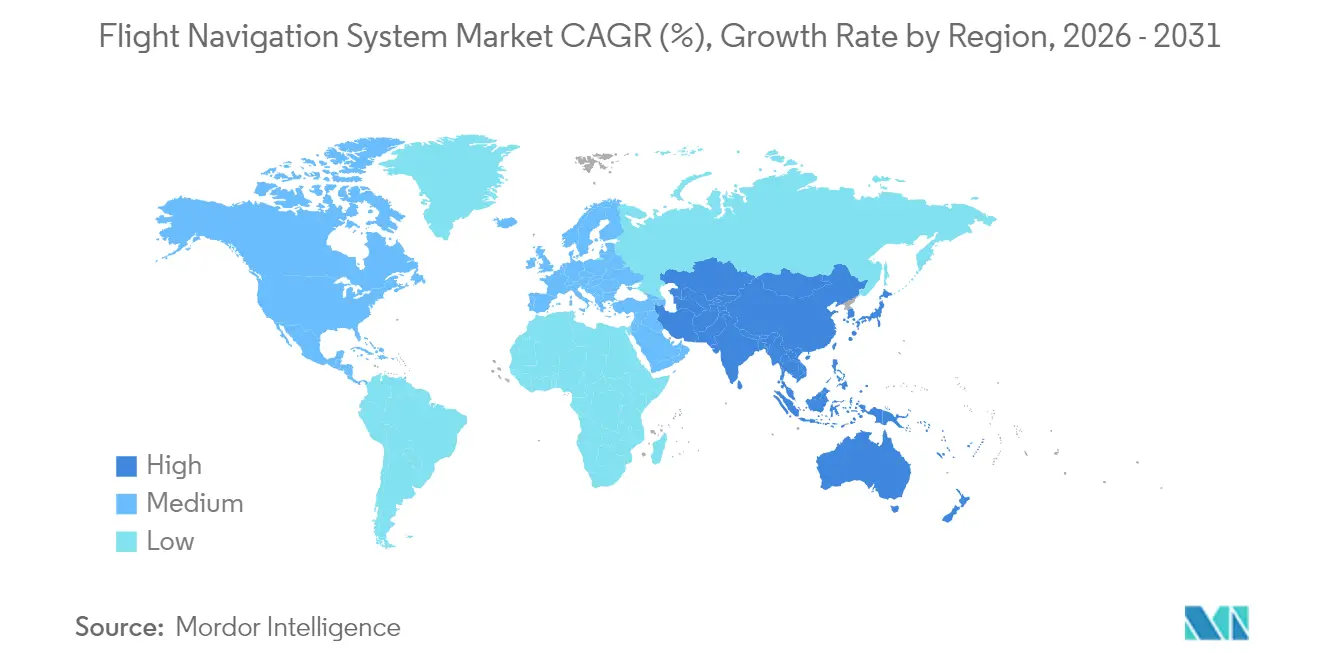

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

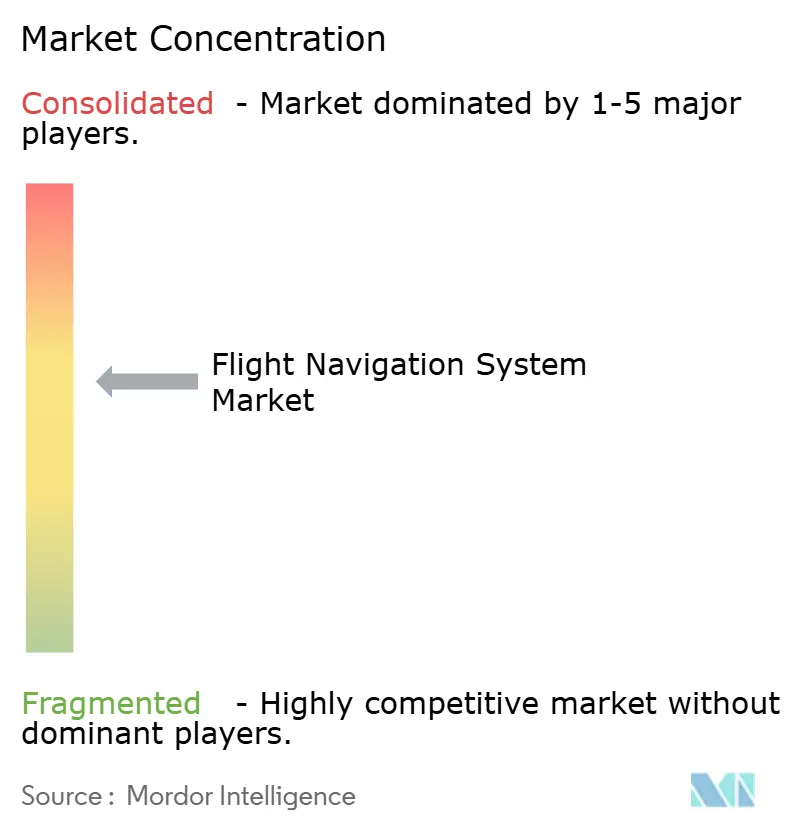

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flight Navigation System Market Analysis by Mordor Intelligence

The flight navigation system market size was valued at USD 22.98 billion in 2025 and estimated to grow from USD 24.48 billion in 2026 to reach USD 33.6 billion by 2031, at a CAGR of 6.55% during the forecast period (2026-2031). The current growth momentum reflects rising aircraft deliveries, mandatory NextGen and SESAR upgrades, and rapid adoption of AI-enabled sensor fusion across flight decks. Demand also benefits from expanding urban air mobility corridors, where centimeter-level positioning and low-latency data links are critical. Meanwhile, multi-layered redundancy architectures combining satellite-based augmentation, inertial sensors, and terrestrial aids lower fuel burn and increase airspace capacity. These advantages help offset the mounting cybersecurity and spectrum-interference risks that accompany higher system complexity.

Key Report Takeaways

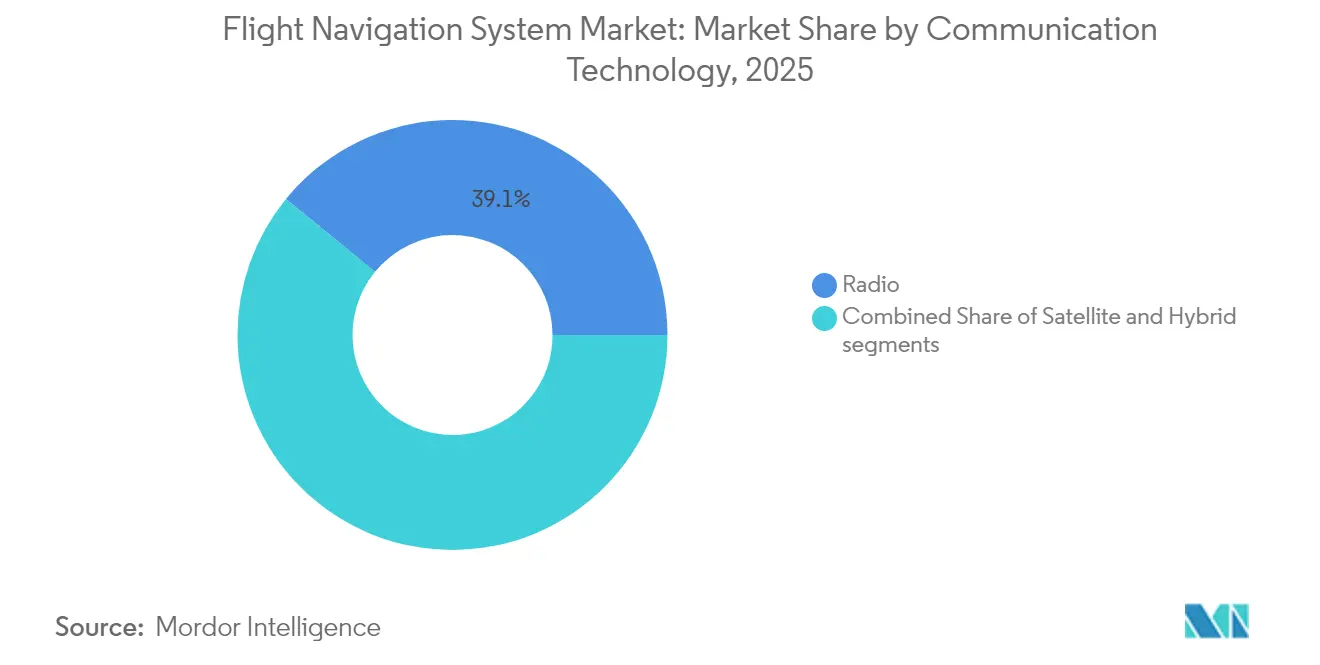

- By communication technology, radio communication led with a 39.10% revenue share in 2025. The growing demand for UAV and long-range UAS navigation reliability is expected to increase at an 8.78% CAGR from 2026 to 2031.

- By platform, civil and commercial aviation accounted for 40.80% of the flight navigation system market share in 2025, whereas military aviation is projected to advance at a 9.05% CAGR through 2031.

- By flight instrument, autopilot systems held a 28.85% share of the flight navigation system market in 2025, and gyroscope instruments are expanding at the fastest rate, with a 9.98% CAGR.

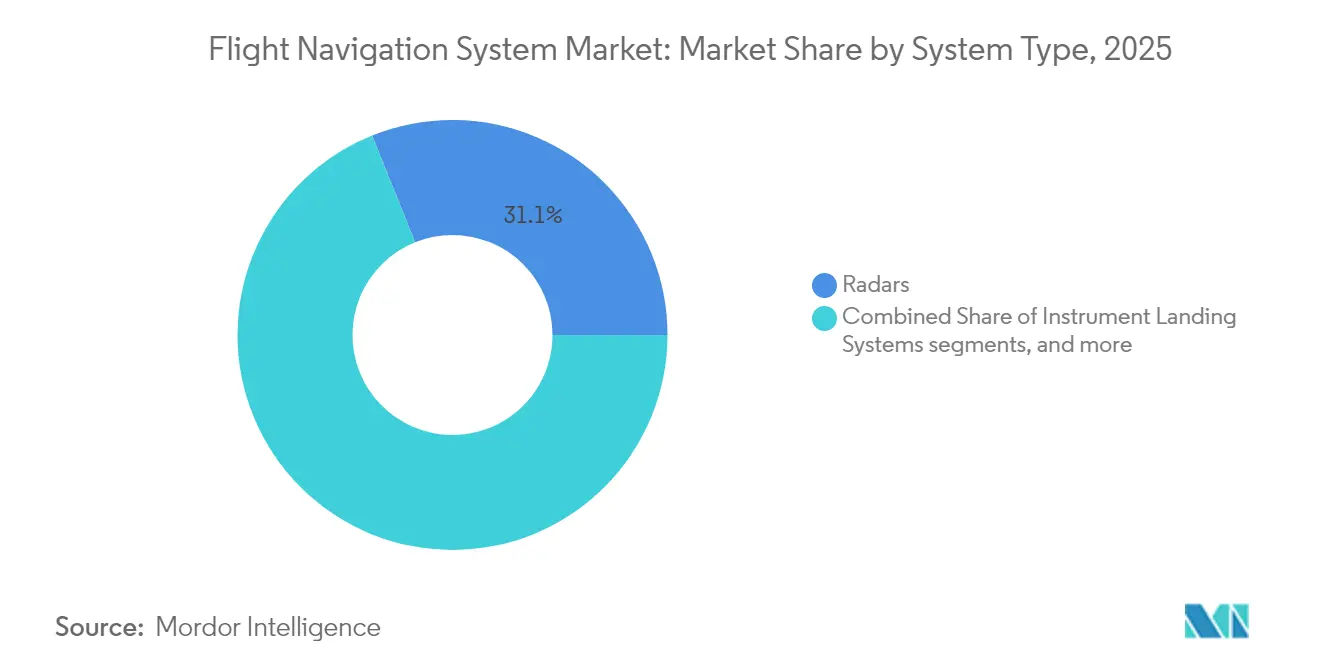

- By system type, radar systems contributed a 31.10% share in 2025, while collision avoidance systems posted the highest CAGR of 6.44% to 2031.

- By component, hardware dominated with a 38.95% share in 2025, but software solutions are registering a 7.15% CAGR as cloud-native architectures gain traction.

- By geography, North America retained a 35.20% share in 2025; however, the Asia-Pacific region is projected to grow at a 7.95% CAGR, reflecting fleet expansion in China and India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flight Navigation System Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Satellite-based augmentation (SBAS) and NextGen/SESAR mandates | +1.2% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Rising global commercial aircraft fleet | +1.8% | Global, with APAC leading growth | Long term (≥ 4 years) |

| Shift to performance-based navigation (PBN) standards | +1.5% | Global, ICAO member states | Medium term (2-4 years) |

| Growing demand for UAV and long-range UAS navigation reliability | +0.9% | North America and Europe, emerging in APAC | Short term (≤ 2 years) |

| Urban-air-mobility corridor integration needs | +0.8% | Major metropolitan areas globally | Long term (≥ 4 years) |

| AI-driven sensor-fusion redundancy for zero-fail cockpits | +0.6% | Advanced aviation markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Satellite-Based Augmentation Systems Drive Infrastructure Transformation

EGNOS secured a EUR 51 million (USD 60.01 million) extension through 2028, enabling European airports to support precision approaches without the need to install new ground beacons.[1]Thales Alenia Space, “EUSPA Signs Contract to Extend EGNOS Service Life,” thalesaleniaspace.com Similar programs in Korea and sub-Saharan Africa have mirrored this success, prompting airlines to retire older receivers in favor of SBAS-ready hardware. Mandatory compatibility clauses within NextGen and SESAR accelerate equipment replacement cycles and promote global interoperability, which lowers pilot-training hours and flight-planning overheads. Airlines welcome lower ground-station maintenance costs because satellite signals deliver the required accuracy for Required Navigation Performance operations. These combined factors amplify upgrade demand across every fleet segment.

Commercial Fleet Expansion Fuels Navigation System Demand

Airbus and Boeing's order books returned to pre-pandemic levels in 2024, prompting OEMs like Thales to report EUR 6.4 billion (USD 7.54 billion) in avionics orders for flight management and navigation suites.[2]Thales Group, “Thales Full-Year 2024 Results,” thalesgroup.com Airlines prioritize continuous-descent and dynamic-routing software that cuts fuel burn and carbon penalties. Concurrently, more-electric aircraft architectures are inviting integrated computing platforms that consolidate navigation, communication, and flight-control tasks to reduce weight. Software-defined navigation unlocks over-the-air feature updates, protecting asset value across long service lives.

Performance-Based Navigation Standards Reshape Operational Requirements

ICAO’s latest Annex 11 revisions ask member states to monitor satellite integrity and protect air-ground data links from cyber compromise. Airlines adopting Performance-Based Navigation fly shorter tracks and optimized vertical paths, boosting capacity at congested hubs. Tiered Required Navigation Performance levels reward carriers that invest in the most precise receivers yet remain backward-compatible with older fleets. Real-time weather overlays inside flight management computers help dispatchers adjust trajectories and avoid turbulence without violating airspace restrictions.

UAV Navigation Reliability Drives Technology Innovation

ICAO’s framework for remotely piloted aircraft mandates precise navigation performance for beyond-visual-line-of-sight (BVLOS) flights, creating demand for resilient inertial sensors blended with AI diagnostics. Quantum-enhanced gyros under development promise four-hour accuracy without GPS, as demonstrated in Boeing trials conducted in March 2025. The same technology appears attractive for long-range military UAS, which must function in jamming scenarios, prompting suppliers to harden systems against electronic attacks.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upgrade and certification costs | -0.8% | Global, smaller operators most affected | Short term (≤ 2 years) |

| Cyber-jamming and spoofing vulnerabilities | -1.1% | Global, heightened in conflict regions | Short term (≤ 2 years) |

| 5G spectrum re-allocation crowding navigation bands | -0.7% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Rare-earth magnet shortages for MEMS gyros | -0.5% | Global supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Threats Expose Navigation Vulnerabilities

Confirmed GPS spoofing incidents rose sharply in 2024, disrupting commercial flights over conflict zones and compelling operators to fit multi-source positioning backups. Such redundancy raises costs and certification workloads. Manufacturers now embed quantum-grade inertial sensors to maintain accuracy during outages, while airlines invest in real-time monitoring to flag anomalous satellite data. Governments respond with spectrum-monitoring networks, but full deployment remains years away.

5G Spectrum Interference Challenges Radar Altimeter Operations

The FAA continues to assess C-band 5G interference with radar altimeters, imposing temporary approach restrictions at several airports during poor visibility.[3]Federal Aviation Administration, “FAA 5G C-Band Guidance,” faa.gov Airlines must budget for filter retrofits or new altimeters, especially on widebody fleets operating across multiple regions with differing spectrum rules. This unplanned expenditure pressures smaller carriers and slows the adoption of other advanced avionics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Communication Technology: Hybrid Architectures Gain Momentum

Radio links accounted for 39.10% of 2025 revenue, owing to entrenched VHF infrastructure and worldwide regulatory mandates. Yet, hybrid GNSS-SBAS solutions are set to outpace all other technologies with an 8.78% CAGR, illustrating the industry's shift toward precision approaches and oceanic coverage without ground aids. The flight navigation system market size for hybrid solutions is projected to grow faster than any other communication category, supported by satellite operators launching dedicated ADS-B constellations that feed real-time traffic data to crews.

Satellite communication gains relevance on polar and transoceanic routes, while software-defined radios enable dynamic frequency selection to mitigate interference. The combination of space-based receivers and ground networks equips airlines with resilient links that underpin future four-dimensional trajectory management exercises. Thales’ 100-satellite ADS-B program exemplifies this migration toward integrated surveillance and communications, reducing hardware counts and certification costs by utilizing standard avionics modules.

By Platform: Military Modernization Accelerates Orders

Civil and commercial fleets controlled 40.80% of the flight navigation system market share in 2025, driven by the replacement of aging narrowbody aircraft and the rebound in passenger demand. Militaries drive the highest spending velocity with a 9.05% CAGR as nations pursue sovereign navigation capacity immune to foreign GNSS signals. These programs frequently bundle electronic-warfare filters, redundant inertial sensors, and AI-assisted mission planning in the same cockpit server to cut wiring and weight.

The Global Combat Air Programme’s (GCAP's) sixth-generation fighter concept demonstrates that sensor fusion and adaptive navigation will underpin future air superiority platforms. At the same time, eVTOL air taxis, categorized under urban air mobility, begin to specify certified antennas and multi-frequency receivers designed for low-altitude corridors. This demand for diversity sustains backlog for platform-agnostic avionics suites that can be repackaged across fighters, freighters, and flying taxis with minimal requalification.

By Flight Instrument: Gyroscopes Lead Next-Wave Innovation

Autopilot computers held the largest instrument share at 28.85% in 2025, reflecting their indispensable role in managing long-haul workloads. Gyroscope instruments are expected to register the sharpest climb at a 9.98% CAGR through 2031, as MEMS refinement and quantum sensing unlock centimeter-level drift characteristics. The resulting performance permits zero-fail cockpits to sustain navigation precision during prolonged GNSS outages, a feature crucial for military and transpolar flights.

Optical gyros from Anello Photonics achieved 0.1% error over 100 kilometers in field trials, underscoring the pace of improvement. Advances in sensor fusion algorithms further reduce position uncertainty by blending gyro, accelerometer, air-data, and celestial cues inside a standard Kalman filter, bolstering resilience against spoofing attacks. These developments power the flight navigation system market by enabling lower-cost inertial reference units suited to small UAVs and eVTOLs.

By System Type: Surveillance and Safety Converge

Radar systems retained a 31.10% share in 2025 because civilian and defense operators depend on them for weather and terrain awareness. Yet collision-avoidance suites grew at a 6.44% CAGR as ICAO implemented enhanced surveillance mandates supported by space-based ADS-B broadcasts. The flight navigation system market size for collision-avoidance hardware and software is forecast to expand steadily as autonomous aircraft require machine-speed conflict resolution.

Simultaneously, inertial navigation remains a core capability for operators flying in GPS-denied areas. At the same time, instrument landing systems (ILS) survive thanks to regulatory insistence on dual-path redundancy during low-visibility approaches. Suppliers, therefore, bundle weather radar, traffic collision avoidance, and precision landing modules into integrated racks that cut lifecycle overhead.

By Component: Software Transforms Value Creation

Hardware accounted for 38.95% of the revenue in 2025, primarily driven by cockpit display units, antennas, and inertial sensors. Software represents the faster-moving frontier, rising at 7.15% CAGR on the back of cloud-native flight planning, predictive maintenance dashboards, and AI copilots. The flight navigation system industry increasingly views over-the-air updates as the key to life-cycle economics; Garmin’s SmartCharts and FlightPath3D’s “Luci” exemplify user-interface innovations that drive subscription revenue.

Edge-cloud synchronization allows crews to receive real-time weather layers and optimized routing mid-flight, while ground engineers monitor health metrics streamed from each line-replaceable unit. This architecture reduces unscheduled maintenance and supports faster certification of minor function releases, strengthening supplier aftermarket ties.

Geography Analysis

North America kept its leadership with a 35.20% share in 2025, underpinned by steady NextGen funding, strong business-jet production, and the FAA's proactive rulemaking on powered-lift aircraft. Area navigation route additions such as Q-143 and T-467 show that en-route efficiency upgrades persist even as passenger numbers rebound. The region's broad adoption of over-the-air software updates positions it as a proving ground for cloud-based navigation analytics that feed directly into dispatch-center algorithms.

The Asia-Pacific region is the fastest-growing arena, with a 7.95% CAGR from 2021 to 2031. China and India dominate the order books for narrowbody jets, while regional governments allocate capital toward satellite-based augmentation and unmanned traffic management frameworks. Thales's new MRO facility in the Delhi-NCR region and its UTM roadmap agreement with Thai authorities illustrate a supplier's pivot toward local engineering hubs, which can reduce time-to-certification for indigenous carriers. These moves accelerate the adoption of hybrid GNSS-SBAS receivers across new single-aisle fleets.

Europe registers solid gains as SESAR-driven PBN procedures proliferate, and the European Union Aviation Safety Agency finalizes comprehensive VTOL regulations that establish navigation performance baselines for urban air mobility. The EGNOS service life extension to 2028 safeguards low-visibility operations for more than 400 airports, thereby sustaining demand for SBAS-capable flight management computers and precision approach displays. Sustainability priorities are driving airlines to adopt trajectory prediction tools that enable continuous-descent arrivals, thereby reinforcing the role of predictive analytics within cockpit servers.

Competitive Landscape

The flight navigation system market is moderately consolidated. Aerospace majors leverage deep certification expertise and long-standing customer relationships to protect their installed bases, while selectively divesting non-core assets. Boeing’s USD 10.55 billion sale of Jeppesen and ForeFlight to Thoma Bravo has refocused the airframer on hardware, creating a pure-play digital aviation platform for rapid subscription growth. Competing bidders such as Honeywell, GE, and RTX Corporation highlighted the strategic importance of flight-planning databases in next-generation cockpits.

New entrants differentiate through quantum sensing, optical gyros, and AI copilots. VIAVI Solutions’ USD 50 million purchase of Inertial Labs expands its inertial sensor lineup for both crewed and uncrewed platforms, mirroring the trend toward vertically integrated motion-sensing portfolios. Meanwhile, Thales Group, Garmin, and Honeywell race to supply multi-frequency antennas and open-architecture flight decks to eVTOL developers, anticipating urban-mobility certification within the decade.

Competitive intensity also manifests in collaborative space-based surveillance ventures. Thales, Spire Global, and ESSP are building a 100-satellite ADS-B service that promises globe-spanning traffic coverage by 2027. Access to such data feeds improves collision-avoidance algorithms and creates premium airline analytics services. Suppliers that pair hardware, data subscriptions, and predictive-maintenance dashboards stand to capture a larger lifetime value across fleets that now average over 20 years of service.

Flight Navigation System Industry Leaders

Honeywell International Inc.

RTX Corporation

Thales Group

Garmin Ltd.

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Garmin unveiled the G5000 PRIME integrated flight deck, enhancing situational awareness with synthetic vision and predictive taxi guidance.

- May 2025: Garmin introduced SmartCharts, delivering interactive charting with real-time data overlays to reduce pilot workload.

- August 2024: Thales became the sole supplier of navigation and communication antennas for Lilium’s eVTOL jet program.

- June 2024: Thales, Spire Global, and ESSP began building a satellite surveillance service that would use 100 satellites to collect global ADS-B messages.

Global Flight Navigation System Market Report Scope

Flight navigation systems pinpoint an aircraft's precise location, aiding pilots in adhering to designated routes. Our market study delves into the diverse flight navigation systems employed across military, commercial, and general aviation. It encompasses all avionics components and systems crucial for navigation and communication, ensuring aircraft can relay their positions effectively to ground stations and other airborne craft.

The flight navigation system market is segmented by communication type, application, flight instrument, systems, and geography. By communication type, the market is segmented into radio and satellite. By application, the market is segmented into civil & commercial aviation and military aviation. By flight instrument, the market is segmented into autopilot, altimeter, gyroscope, sensors, and magnetic compass. By systems, the market is segmented into radars, instrument landing systems, inertial navigation systems, collision avoidance systems, VOR/DME, and global navigation satellite systems (GNSS). The report also covers the market sizes and forecasts for the flight navigation system market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Radio |

| Satellite |

| Hybrid (GNSS+SBAS) |

| Civil and Commercial Aviation |

| Business and General Aviation |

| Military Aviation |

| UAV/eVTOL |

| Autopilot |

| Altimeter |

| Gyroscope |

| Attitude Heading Reference System (AHRS) |

| Sensors (IMU, Air-data, etc.) |

| Magnetic Compass |

| Radars |

| Instrument Landing Systems (ILS) |

| Inertial Navigation Systems (INS) |

| Collision Avoidance Systems (CAS) |

| GNSS/VOR-DME |

| Other Systems |

| Hardware |

| Software |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Communication Technology | Radio | ||

| Satellite | |||

| Hybrid (GNSS+SBAS) | |||

| By Platform | Civil and Commercial Aviation | ||

| Business and General Aviation | |||

| Military Aviation | |||

| UAV/eVTOL | |||

| By Flight Instrument | Autopilot | ||

| Altimeter | |||

| Gyroscope | |||

| Attitude Heading Reference System (AHRS) | |||

| Sensors (IMU, Air-data, etc.) | |||

| Magnetic Compass | |||

| By System Type | Radars | ||

| Instrument Landing Systems (ILS) | |||

| Inertial Navigation Systems (INS) | |||

| Collision Avoidance Systems (CAS) | |||

| GNSS/VOR-DME | |||

| Other Systems | |||

| By Component | Hardware | ||

| Software | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the flight navigation system market?

The market is valued at USD 24.48 billion in 2026.

How fast is the flight navigation system market expected to grow?

It is forecasted to expand at a 6.55% CAGR during 2026-2031, reaching USD 33.6 billion by 2031.

Which communication technology holds the largest share?

Radio communication leads with a 39.10% share, though hybrid GNSS-SBAS solutions are growing faster.

Why is Asia-Pacific the fastest-growing region?

Fleet expansion in China and India and major investments in air-traffic modernization drive the region’s 7.95% CAGR.

How will 5G networks impact flight navigation?

C-band 5G deployments can interfere with radar altimeters, pushing airlines to upgrade equipment and regulators to issue operating constraints.

What technological trend is most disruptive to future navigation systems?

Quantum-enhanced gyroscopes and AI-driven sensor fusion promise GPS-independent accuracy and zero-fail cockpit architectures.

Page last updated on: