Helicopter Blades Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

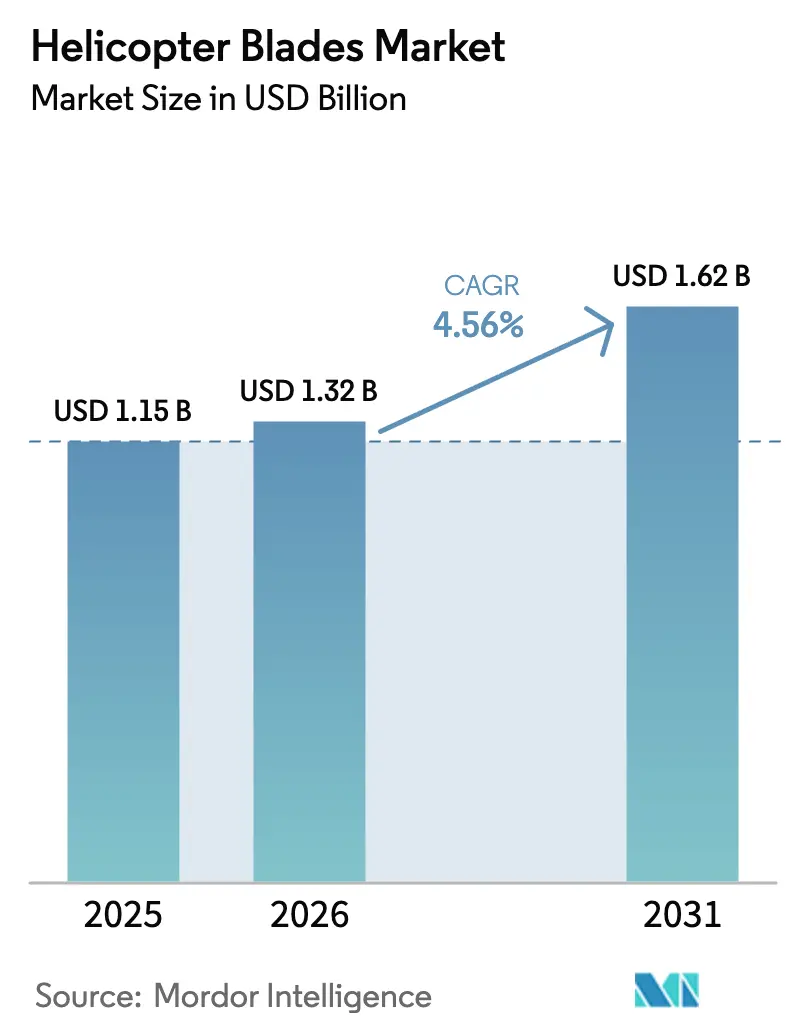

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 1.62 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Helicopter Blades Market Analysis by Mordor Intelligence

The helicopter blades market size is expected to grow from USD 1.26 billion in 2025 to USD 1.32 billion in 2026 and is forecasted to reach USD 1.62 billion by 2031 at a 4.56% CAGR over 2026-2031. This growth is anchored in the accelerating shift from metal to composite blades, rising retrofit activity, and next-generation military programs that tighten performance specifications. Composite materials now underpin more than half of the revenue, and automated fiber placement is shortening production cycles, allowing suppliers to quote tighter delivery windows. Retrofit programs for aging UH-60 Black Hawks, CH-47 Chinooks, and civil utility fleets are expanding, creating steady aftermarket cash flows even as new-build deliveries fluctuate. On the defense side, the US Army’s V-280 Valor contract is setting high-speed, long-range standards that ripple across allied procurement pipelines. Civil operators add another engine of demand as offshore wind, search-and-rescue (SAR), and public service missions drive higher blade utilization in corrosive or high-cycle environments.

Key Report Takeaways

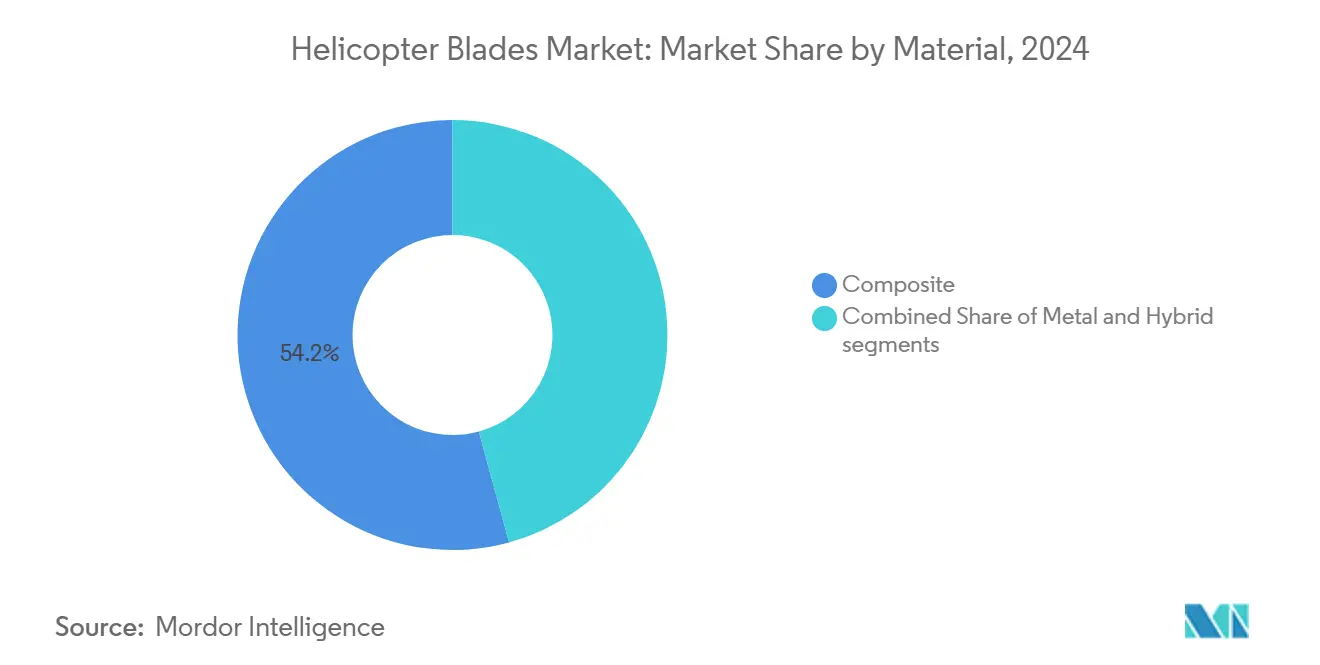

- By material, composite blades held 54.24% of the helicopter blades market share in 2025, while metal alternatives trailed; composites are expected to advance at a 6.17% CAGR through 2031.

- By blade location, main rotor systems captured 70.05% revenue in 2025, whereas tail rotor systems posted the fastest 5.34% CAGR to 2031 on the back of noise-compliance retrofits.

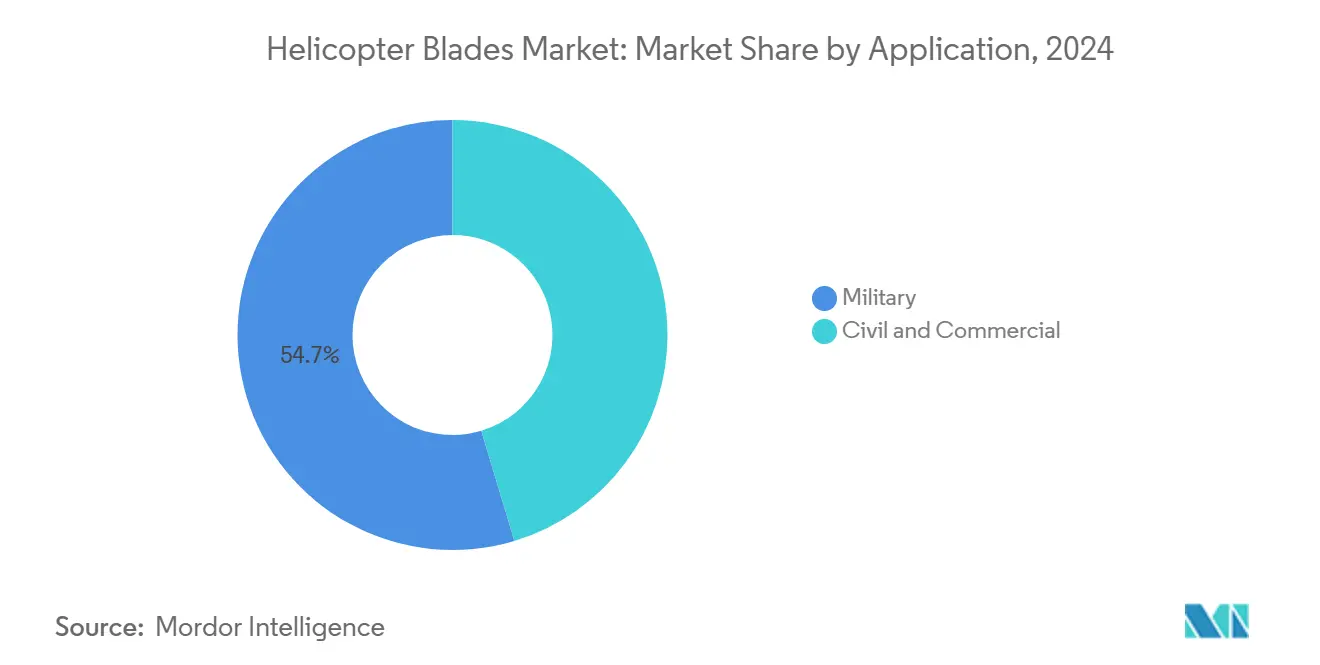

- By application, military fleets commanded 54.65% of the helicopter blades market size in 2025; civil fleets registered the fastest 5.87% CAGR, as offshore wind crew transfer and SAR flights increased.

- By helicopter class, light platforms controlled 44.23% revenue in 2025, while medium helicopters recorded a 5.56% CAGR, reflecting operator preference for multi-mission flexibility.

- By fit, linefit blades accounted for 63.78% of the revenue in 2025; however, retrofit programs delivered the highest 6.21% CAGR as operators extended airframe life cycles.

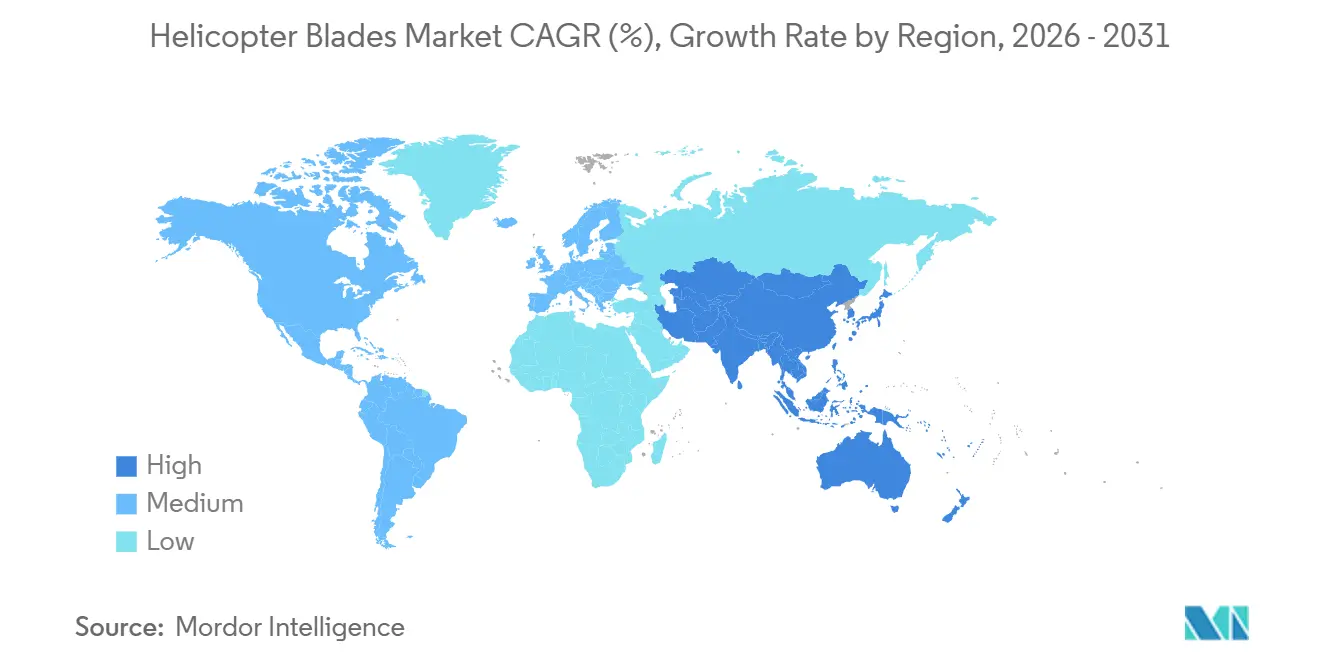

- By geography, the North America region held 36.78% of the 2025 revenue; however, the Asia-Pacific region is expected to record a 6.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Helicopter Blades Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in composite blade retrofit programs for civil and utility helicopter fleets | +1.2% | North America and Europe, spillover to Middle East | Medium term (2-4 years) |

| Future Vertical Lift and next-generation military rotorcraft programs driving advanced blade demand | +1.5% | North America core, allied procurement in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Noise and environmental regulations accelerating adoption of advanced swept-tip blade designs | +0.8% | Global, with strictest enforcement in Europe and North America | Short term (≤ 2 years) |

| Modernization of military helicopter fleets driving demand for upgraded rotor blade technologies | +1.1% | Global, concentrated in North America, Europe, India, Middle East | Medium term (2-4 years) |

| Adoption of digital twin and structural health monitoring to extend blade life cycles | +0.6% | North America and Europe early adopters, Asia-Pacific emerging | Long term (≥ 4 years) |

| Rising offshore, search-and-rescue, and public service helicopter operations increasing blade utilization | +0.9% | Europe (North Sea), Asia-Pacific (Taiwan, Japan), Middle East, Gulf of Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Composite Blade Retrofit Programs for Civil and Utility Helicopter Fleets

Composite retrofits are giving aging civil fleets a cost-effective second life. FAA-approved supplemental type certificates for the Bell 206 and Erickson S-64 models demonstrate that composite blades last two to four times longer than metal designs and reduce weight by up to 20%. North American utility operators capitalize on these gains to defer costly airframe replacements, while European offshore and HEMS fleets follow suit to meet tight mission schedules. Middle East offshore operators have begun to follow suit, but limited composite repair expertise keeps adoption moderate. Pricing still commands a 40-60% premium, but operators recoup the differential through fuel savings, reduced wear on dynamic components, and longer inspection intervals.

Future Vertical Lift and Next-Generation Military Rotorcraft Programs Driving Advanced Blade Demand

Bell’s USD 1.30 billion V-280 Valor contract, awarded in August 2024, exemplifies how future vertical-lift initiatives are reshaping blade requirements toward 280-knot cruise speeds and 1,700 nautical-mile ranges. Composite blades must now withstand both helicopter-mode cyclic loads and airplane-mode cruise stresses, prompting suppliers such as Hexcel and GKN Aerospace to refine their fiber lay-ups for dual-environment fatigue. Production ramps scheduled from 2028 onward will cascade through allied Foreign Military Sales (FMS), amplifying global demand.

Noise and Environmental Regulations Accelerating Adoption of Advanced Swept-Tip Blade Designs

ICAO Annex 16 and FAA Part 36 noise caps have tightened to the point where a 3-6 dB margin can make or break urban landing permits.[1]“ICAO Annex 16 Aircraft Noise,” International Civil Aviation Organization, icao.int Swept-tip geometries reduce blade-vortex interaction noise while improving hover efficiency. The Airbus H145’s five-blade system shows a 5% performance improvement, along with measurable acoustic benefits, prompting law enforcement and HEMS customers in London and Paris to upgrade. Asia-Pacific regulators in Japan and Singapore started mirroring Chapter 13 limits in 2024, signaling a global follow-on effect.

Modernization of Military Helicopter Fleets Driving Demand for Upgraded Rotor Blade Technologies

Digital-cockpit conversions for UH-60 and CH-47 fleets integrate composite blades to reduce vibration and extend range. India’s LCH Prachand and LUH programs ramp domestic composite output for high-altitude missions above 20,000 feet. Saudi Arabia and the UAE retrofit Apache and Black Hawk fleets to improve hot-and-high performance. These overlapping modernization waves generate steady aftermarket volumes, driving market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent FAA and EASA certification and fatigue testing requirements increasing development costs | -0.9% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Carbon-fiber material supply volatility and trade tariff exposure | -0.7% | Global, concentrated in North America and Europe sourcing from Asia | Medium term (2-4 years) |

| Limited composite blade repair and MRO expertise in emerging markets | -0.5% | Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| High manufacturing and replacement costs of advanced composite rotor blades | -0.6% | Global, with highest sensitivity in price-conscious Asia-Pacific and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent FAA and EASA Certification and Fatigue-Testing Requirements Increasing Development Costs

Rotor-blade certification requires 10 million-cycle fatigue testing, lightning-strike validation, and damage-tolerance proofs under FAA Part 27/29 and EASA CS-27/29, which adds USD 5-20 million in non-recurring engineering costs and extends timelines to as long as five years. Smaller suppliers struggle to amortize these costs, resulting in consolidation of innovation among a handful of OEMs and Tier-1 partners. Insurers and financiers further raise the bar by linking coverage to demonstrated regulatory track records, making this the most durable drag on the helicopter blades market.

Carbon-Fiber Material Supply Volatility and Trade-Tariff Exposure

Aerospace-grade carbon fiber cost swings, amplified by US Section 301 tariffs imposing 25% duties on Chinese materials, inflate bill-of-materials costs and disrupt just-in-time manufacturing schedules.[2]“Section 301 Tariffs on Chinese Carbon Fiber,” Office of the U.S. Trade Representative, ustr.gov Spot-market price spikes of 30-50% during 2024 highlighted exposure, while supply is geographically concentrated in Japan, the US, and Germany. Blade suppliers hedge their risks through multi-year contracts with Toray, Hexcel, and SGL Carbon, yet unforeseen precursor shortages still compress their margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Composite Blades Capture Retrofit Wave

Composite blades accounted for 54.24% of 2025 revenue within the helicopter blades market and are expanding at a 6.17% CAGR through 2031. That lead is anchored in demonstrable fatigue-life multiples and 15-20% weight reductions, which together lift useful payload and cut fuel burn. Automated fiber placement has compressed build cycles from six weeks to three, letting suppliers quote aggressive lead times and unlocking retrofit windows during routine C-checks. Hexcel’s HexTow prepregs now enable thinner profiles, while GKN Aerospace’s high-speed lay-up cells achieve ±0.5 mm dimensional accuracy. Metal blades continue to serve legacy fleets and price-sensitive operators, but their market share erodes each year. Hybrid constructions, which mix metal spars with composite skins, remain a niche approach, primarily used on heavy-lift designs such as the CH-53K to balance torsional stiffness and weight.

An uneven repair ecosystem tempers composite demand. Moisture-ingress detection and vacuum bagging for delamination fixes require specialist tooling that remains scarce outside North America and Western Europe. OEMs are responding by bundling remote-monitoring sensors and extended warranties, effectively pulling service work back into factory ecosystems. The helicopter blades market sees composites not only as a materials play but also as a services beachhead, with predictive-maintenance packages becoming a decisive selling point.

By Blade Location: Main Rotor Dominance, Tail Rotor Acceleration

Main rotor assemblies generated 70.05% of 2025 revenue in the helicopter blades market, reflecting higher unit counts, larger surface area, and shorter replacement intervals. Medium helicopters, such as the AW139, consume four to five main rotor blades, each priced at up to USD 150,000, creating a disproportionate revenue anchor. Offshore saltwater exposure and military high-cycle missions shorten main-rotor replacement intervals to 2,000-4,000 hours. Tail rotor blades, by contrast, are accelerating at a 5.34% CAGR due to fenestron conversions and noise-compliance retrofits. The Airbus H135 and H145 tail systems often require replacement at 1,500-2,500 hours, keeping aftermarket volumes brisk.

Swept-tip tail blades provide additional acoustic gains of 3-6 dB, allowing urban-core heliport operations that would otherwise be denied under strict city ordinances. Yet many operators bundle tail blade swaps with main-rotor overhauls to reduce downtime, resulting in lumpy demand cycles that complicate inventory planning in emerging markets.

By Application: Civil Segment Closes Gap on Military Dominance

Military users captured 54.65% of the helicopter blades market size in 2025; however, civil operators are advancing at a 5.87% CAGR and are expected to narrow the gap through 2031. Defense spending is cyclical and tied to multi-year procurement plans, FLRAA, CH-47F Block II, and international Apache upgrades being prime examples. Civil momentum is steadier, driven by offshore wind farm logistics, SAR mandates, and the expansion of public-service fleets. Offshore operators, such as Bristow and CHC, report blade utilization rates above 85%, necessitating replacements every 2,000 to 3,000 hours.

Budget sensitivity remains higher on the civil side, so suppliers now market blade-leasing and power-by-the-hour contracts, aligning cash outflows with operational savings. Asia-Pacific operators, particularly in Taiwan Strait wind projects, value predictable costs more than outright purchase, giving leasing a foothold.

By Helicopter Class: Medium Helicopters Gain on Light Segment Leadership

Light platforms held 44.23% of 2025 revenue but now grow at a gentler pace than medium machines, which log a 5.56% CAGR. Medium helicopters accommodate multi-mission payloads and twin-engine reliability, attributes favored for offshore wind and HEMS assignments. Their five-blade setups yield triple the per-aircraft blade revenue compared with light singles. Heavy-lift platforms such as the CH-53K form a high-value niche. Each 79-ft composite blade on the King Stallion costs more than USD 400,000 and passes rigorous lightning-strike and bird-impact tests.[3]“Sikorsky CH-53K King Stallion Production,” Lockheed Martin, lockheedmartin.com

Operators weigh the cost versus the mission profile: light helicopters dominate law enforcement patrols and training, medium craft fill utility, SAR, and offshore roles, while heavy airframes tackle specialized cargo lifts; blade suppliers, therefore, segment marketing messages by mission rather than by platform to sharpen value propositions.

By Fit: Retrofit Programs Surge as Fleets Age

Linefit orders captured 63.78% of the revenue in 2025, while retrofit activity enjoyed a brisker 6.21% CAGR. A composite conversion for a UH-60 Black Hawk costs more than USD 100,000, compared with millions of dollars for a new airframe, offering a 40-to-1 capital efficiency ratio. FAA-certified retrofit kits from Van Horn Aviation and Erickson have logged over 500 installations worldwide, validating the operator's appetite for these solutions.

Legacy Soviet-era fleets in Asia and Africa represent untapped potential; however, fragmented ownership and sparse certification pathways hinder their penetration. Suppliers exploring low-cost retrofit kits face the challenge of developing multiple installation templates that meet the varied scrutiny of different regulators. Nonetheless, as blades become digital twin-enabled, retrofit value escalates beyond mere material swaps to include data analytics subscriptions.

Geography Analysis

North America leads with 36.78% of 2025 revenue, due to robust US Department of Defense (DoD) programs and a civil fleet topping 12,000 airframes. Gulf of Mexico offshore operators replace blades every 2,000–3,000 hours due to corrosive saltwater, while Canadian Arctic crews seek icing-resistant composite configurations. Growth, however, moderates as procurement budgets shift toward unmanned platforms, prompting suppliers to focus on retrofit and services lines.

Asia-Pacific records the fastest 6.85% CAGR through 2031 for the helicopter blades market. India’s HAL scales up composite blade output for the LCH Prachand and LUH programs, targeting both domestic and export customers.[4]“LCH Prachand and LUH Production,” Hindustan Aeronautics Limited, hal-india.co.in China’s AVIC Z-20 and Z-10 expansions forge a parallel supply chain insulated from Western export licenses. Japan modernizes the UH-2 and upgrades the CH-47JA blades, while South Korea delivers KUH-1 Surion variants featuring local composites. MRO capacity lags demand, extending turnaround times to up to 12 weeks and presenting a services gap ripe for investment.

Europe remains pivotal, bolstered by Airbus Helicopters and Leonardo production lines. North Sea offshore wind projects push blade utilization rates above 85% for operators like NHV and Babcock. HEMS expansions in Germany, France, and the UK rely on low-vibration composite blades to enhance patient comfort and safety. Budget headwinds arise from defense cuts and selective NH90 retirements; however, the civil fleet helps fill part of the slack. Middle East customers accelerate composite upgrades for desert conditions, though MRO skills shortages slow full adoption.

Competitive Landscape

The helicopter blades market is moderately concentrated, with Airbus, Bell Textron Inc., Lockheed Martin Corporation, and Erickson Incorporated capturing an estimated more than 50% of linefit revenue. Their vertical integration bundles airframes, blades, and digital services, securing long-term maintenance contracts. Independent suppliers, such as Van Horn Aviation and Kaman Corporation, disrupt the aftermarket by offering FAA-certified composite retrofits at 30-40% below the cost of OEM spares. Technology enablers Hexcel and GKN Aerospace supply carbon-fiber prepregs and high-speed placement cells to both incumbents and challengers, diffusing process know-how throughout the ecosystem.

Emerging-market white spaces involve composite repair infrastructure. Operators in Saudi Arabia, the UAE, and Indonesia frequently encounter prolonged aircraft-on-ground situations when blades require delamination fixes, thereby inflating the total cost of ownership. Suppliers that package portable vacuum-bag repair kits and remote SHM diagnostics can capture premium service margins. Patent activity in individual-blade-control and morphing-rotor concepts is on the rise, with Airbus and Leonardo leading the development of early prototypes. Certification inertia still favors incumbents with dedicated regulatory teams; however, unmanned platforms open a lower-barrier channel for newcomers, such as Kaman, which specifies composite blades on its K-MAX TITAN unmanned cargo helicopter.

OEMs also hedge material risk by dual-sourcing carbon fiber from Toray, Hexcel, and SGL Carbon and by signing multi-year offtake agreements to shelter against tariff shocks. Digital twin platforms now accompany new build deliveries, bundling predictive maintenance analytics and blade-life forecasting as revenue-generating software subscriptions. As a result, the competitive arena shifts from purely physical components toward integrated hardware-plus-analytics propositions, elevating switching costs for operators and complicating price-based competition.

Helicopter Blades Industry Leaders

Lockheed Martin Corporation

Kaman Corporation

Erickson Incorporated

Bell Textron Inc. (Textron Inc.)

Airbus Helicopters (AIrbus SE)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Sikorsky Aircraft Corp. received a firm-fixed-price delivery order to supply 128 main rotor blade assemblies for the CH-53K aircraft. The contract, with no options, will be executed in Stratford, Connecticut, and is scheduled for completion by October 2032.

- February 2023: Bharat Forge signed a contract with Paramount Group, a global aerospace and technology company, for the development and production of composite rotor blades, storage management systems, and mission systems for medium-lift helicopters at Aero India 2023.

- May 2022: Nova Graphene, a Canada-based company, signed two contracts with the Department of National Defense's Innovation for Defense Excellence and Security (IDEaS) program to develop graphene-enhanced materials that protect helicopter rotors from erosion and wear caused by exposure to sand, ice, and water.

Global Helicopter Blades Market Report Scope

The helicopter's blades perform a function similar to that of an airplane's wings, providing lift as they rotate. Helicopters can have two to seven blades, depending on the mission for which they are used, so the minimum number of rotor blades required for a helicopter to fly effectively is two.

The helicopter blade market is segmented based on material, blade location, application, helicopter class, fit, and geography. By material, the market is segmented into metal, composite, and hybrid. By blade location, the market is segmented into the main rotor blade and the tail rotor blade. By application, the market is segmented into civil, and commercial and military. By helicopter class, the market is segmented into light, medium, and heavy. By fit, the market is segmented into linefit and retrofit. The report also covers the market sizes and forecasts for the helicopter blades market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Metal |

| Composite |

| Hybrid |

| Main Rotor Blade |

| Tail Rotor Blade |

| Civil and Commercial |

| Military |

| Light |

| Medium |

| Heavy |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Material | Metal | ||

| Composite | |||

| Hybrid | |||

| By Blade Location | Main Rotor Blade | ||

| Tail Rotor Blade | |||

| By Application | Civil and Commercial | ||

| Military | |||

| By Helicopter Class | Light | ||

| Medium | |||

| Heavy | |||

| By Fit | Linefit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the helicopter blades market in 2026?

The helicopter blades market size is USD 1.32 billion in 2026 and is forecasted to reach USD 1.62 billion by 2031 at a 4.56% CAGR.

Which material segment is leading revenue generation?

Composite blades command 54.24% revenue and grow at 6.17% CAGR, driven by longer fatigue life and weight savings.

What drives the fastest growth by blade location?

Tail rotor blades, influenced by noise-compliance retrofits adoption, post a 5.34% CAGR through 2031.

Which region shows the highest forecast CAGR?

Asia-Pacific leads with a 6.85% CAGR, fueled by indigenous production in India and China and expanding civil fleets.

How are retrofit programs influencing demand?

Retrofit programs grow at 6.21% CAGR, offering a cost-effective path to extend airframe life and integrate composite technology.

What is the competitive landscape outlook?

The market is moderately concentrated, but retrofit specialists gain share through certified composite upgrades.

Page last updated on: